1.1 -e. iakovou

TRANSCRIPT

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 1/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Value Innovation: A Strategic

Roadmap for High Growth

Eleftherios Iakovou, Ph.D. Associate Professor

Director, Lab of Quantitative Analysis,Logistics & Supply Chain Management

Department of Mechanical Engineering

Aristotle University of Thessaloniki

President, Greek Society of Logistics,

Branch of Thessaloniki

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 2/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Observation

We can expect more change in

our lifetimes, thanthan has occurredsince the beginning of civilization,

over ten thousand years ago!

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 3/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Observation

We’re in the midst of great upheaval in the

business world – established brand namesare disappearing, new upstarts are thriving,

job security is diminishing, the demands ofthe workplace are increasing, newtechnology requires constant retraining,

globalization means new competitors …and the list of challenges continues to grow.

Newsweek (020413)

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 4/40‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

The Main Issue of Our Time

C h a n g eC h a n g e

•Accelerating

•Turbulent

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 5/40‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Observation

It is not the strongest of the species

that survive, nor the most intelligent,

but the one most responsive to change.

Charles Darwin

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 6/40‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Major Business Change Sources

EN

T

E

RP

R

I

SE

TechnologicRevolution

EconomicGlobalization

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 7/40‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Globalization ProcessThe simultaneous impact of

• Information technology

• Worldwide financial flows

• Logistics methodologies

compounded by• Deregulation & Privatization

• Worldwide market economy

• Reduction in trade barriers

is decoupling

procurement, production,

distribution & consumption

of offers in space & time.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 8/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Change: Main Consequences

• INCREASING COMPLEXITYMore variables & relationships

• INCREASING RISKHigher stakes & volatility, increasing threats

• INCREASING UNCERTAINTYMore discontinuities & surprises.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 9/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

INCREASING VOLATILITY

1980s

1990s

2000s

Probability

VariableMean

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 10/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Observation

Under accelerating change

track record is irrelevantvision about future fit is critical.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 11/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Change: Illustration

Between 1975 & 1985,

one third of the Fortune 500

companies disappeared.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 12/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Change: Illustration

5 of the top 15 companies

in the S&P 500 in 2000

didn’t exist in 1980.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 13/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Change: Illustration

• An analysis of Fortune 1000 reveals:

– 35% in the top 20 were new for the period

1973-1983

– 45% new for the period 1983-1993

– 60% new for the period 1993-2003

–Where will it be for the period 2003-2013?

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 14/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

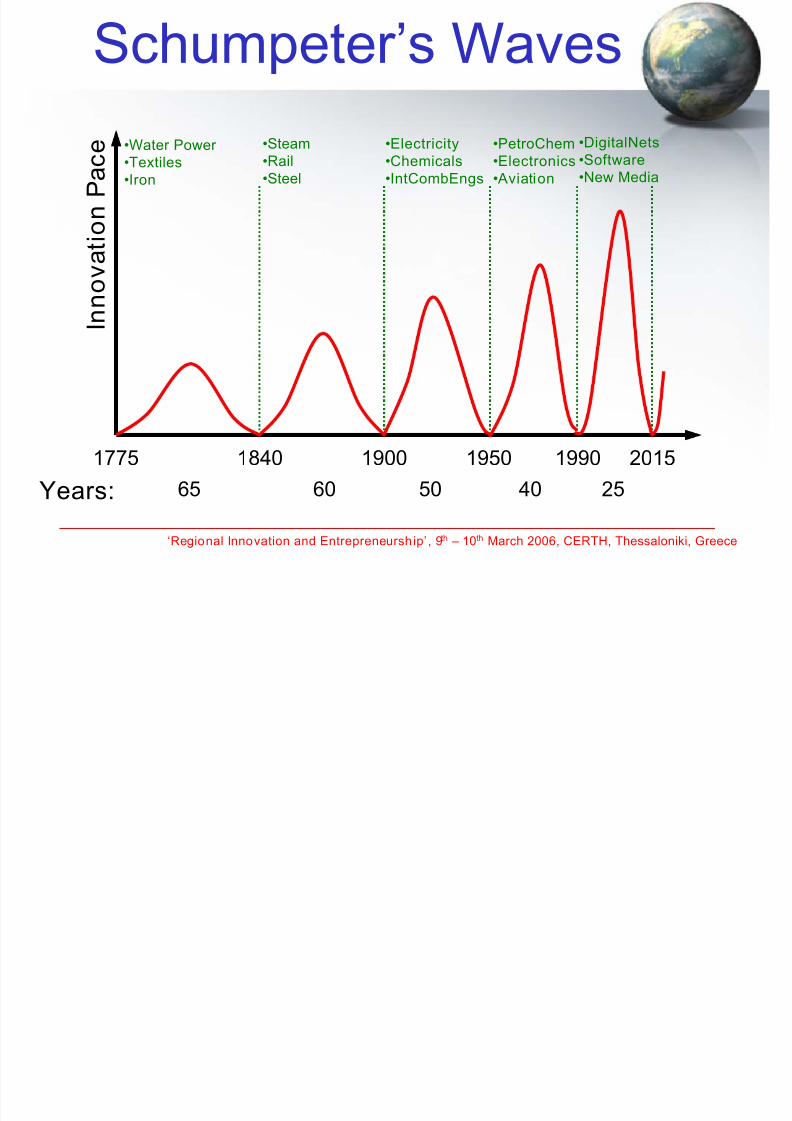

Schumpeter’s Waves

I n n o v a t i o n P a c e

1990 2015

25

1775 1840 1900 1950

•Water Power

•Textiles

•Iron

•Steam

•Rail

•Steel

•Electricity

•Chemicals

•IntCombEngs

•PetroChem

•Electronics

• Aviation

•DigitalNets

•Software

•New Media

Years: 65 60 50 40

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 15/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Observation

Survival is not compulsory.

W. Edwards Deming

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 16/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Change: Critical Consequence

INCREASING

OPPORTUNITIESOPPORTUNITIES

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 17/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

OBSERVATION

Reengineering &

Benchmarking

only help to catch up:

successsuccess requiresrequiresr i n v n t i n g i n v n t i n g the businessthe business

before the competitionbefore the competition ..

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 18/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

How to Reinvent a Business

• Restructure portfolio

• Downsize headcount Smaller

• Reengineer processes• Continuous improvement Better

• Reinvent industry

• Regenerate strategiesDifferent

Source: Hamel & Pralahad: “Competing for the Future”

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 19/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Flexibility is the Key Attribute

• Very few companies (e.g. Toyota, Johnson &

Johnson, Procter & Gamble) have managed to

sustain high performance over long periods!

• The problem: We continue to design

organizations which are averse to change!

A paradigm shift is necessary in corporate

strategy and culture that rewards innovation.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 20/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Major Consequence

The fastoutperform

the big.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 21/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Major Consequence

The sm r t

outperform

all others.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 22/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

OBSERVATION

You are either

a master of change

or

a victim of change.

T Vi f St t

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 23/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Two Views for Strategy

• The Stucturalist (Conventional):

– Changes are induced by factors external to the

market (changes in basic economic conditions,

technological breakthroughs)• The Reconstructionist (Value Innovation):

– Endogenous growth: internal factors such as

innovation and knowledge can influence systemic

growth.

– (Traces Back to J. Schumpeter’s innovation theory).

The Structuralist View:

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 24/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

The Structuralist View:

Ramifications

• Leads to competition-based strategic thinking

• The issue is obtaining a larger share of the existing

market share, by assessing what the competitors do

and try to do it better:a zero-sum game!

• Companies mainly seek to capture and

redistribute wealth instead of creating wealth.

The Reconstructionist View:

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 25/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

The Reconstructionist View:

Ramifications

• Structure and market boundaries exist

only in managerial minds!

• There is extra demand out there, untapped

• Necessary paradigm shifts: – from supply to demand

– from competing to value innovation: thecreation of innovative value to unlock

new demand.

V l I ti

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 26/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Value vs. Innovation

• Value without innovation tends to focus

on value creation at an incrementallevel:

– Not sufficient to stand out on the

marketplace

• Innovation without value tends to be

technology driven: – May provide offerings well beyond

buyers are willing to pay for!

T Diff t Vi

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 27/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Two Different ViewsThe FiveThe Five

DimensionsDimensions

of Strategyof Strategy Conventional LogicConventional Logic Value Innovation LogicValue Innovation LogicIndustryIndustry

Assumptions Assumptions

Industry’s conditions are given. Industry’s conditions can be shaped.

StrategicStrategic

FocusFocus

A company should build competitive

advantages. The aim is to beat the

competition.

Competition is not the benchmark. A company

should pursue a quantum leap in value to

dominate the market.

CustomersCustomers A company should retain and expand itscustomer base through further

segmentation and customization. It

should focus on the differences in what

customers value.

A value innovator targets the mass of buyersand willingly lets some existing customers go. It

focuses on the key commonalities in what

customers value.

Assets and Assets andCapabilitiesCapabilities

A company should leverage its existing

assets and capabilities.

A company must not be constrained by what it

already has. It must ask: what would we do if

we were starting anew?

Product andProduct and

ServiceServiceOfferingsOfferings

An industry’s traditional boundaries

determine the products and services a

company offers. The goal is to maximizethe value of those offerings.

A value innovator thinks in terms of the total

solution customers seek, even if that takes the

company beyond its industry’s traditionalofferings.

I ti A D fi iti

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 28/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Innovation: A Definition

• “ The successful production,

assimilation and exploitation ofnovelty in the economic and social

spheres”Commission's Communication on

Innovation Policy (2003)

The Value Innovation

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 29/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Framework

• Which of the factors that our industry takes

for granted should be eliminated?

• Which factors should be reduced well below

the industry’s standard?• Which factors should be raised well above

the industry’s standard?• Which new factors should be created that

the industry has never offered?

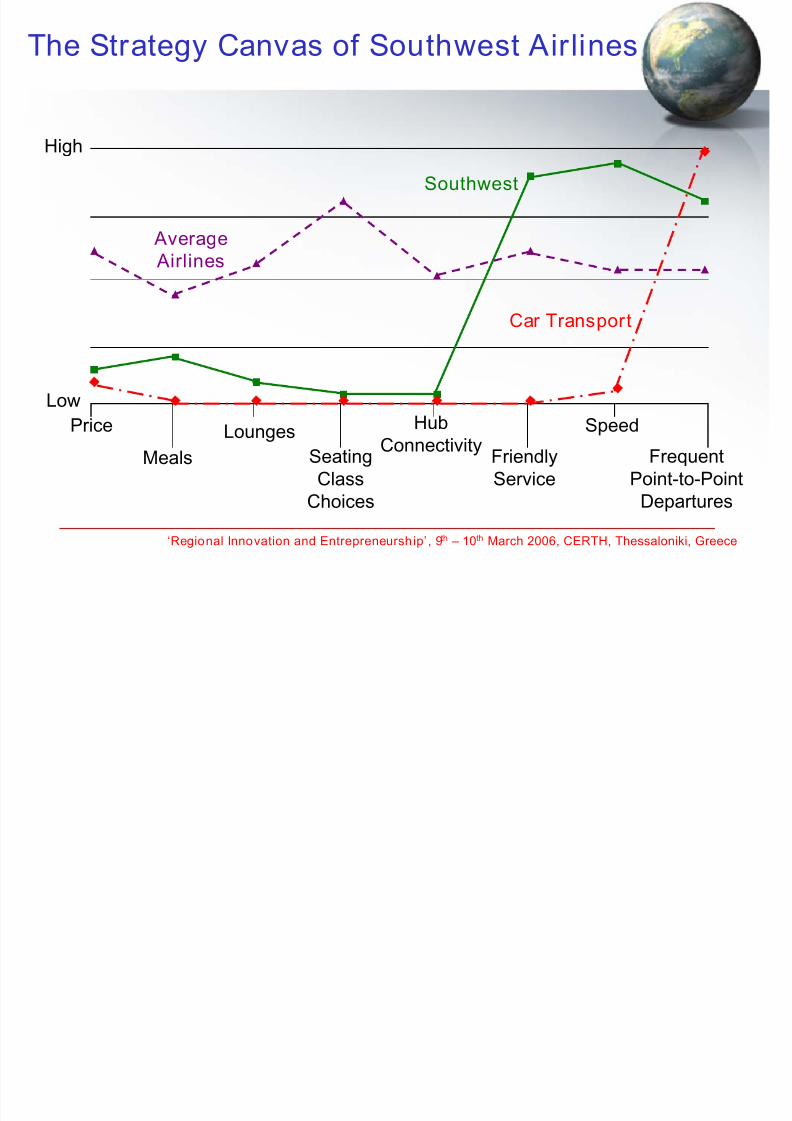

Th St t C f S th t Ai li

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 30/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

The Strategy Canvas of Southwest Airlines

High

LowPrice

Meals

Lounges

Seating

Class

Choices

Hub

ConnectivityFriendly

Service

Speed

Frequent

Point-to-Point

Departures

Average

Airlines

Southwest

Car Transport

Value Cost Model & Strategic Positioning

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 31/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Value-Cost Model & Strategic Positioning

High Cost

Low

Value

Perceived Value

to Customer

High

Value

Low CostDelivered Cost

Value Cost Model Descriptions

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 32/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Value-Cost Model Descriptions

VALUE

(What and Who?)

COST

(How?)

Product Excellence

-- Performance, Functionality, Durability, Reliability

(e.g., Nike, Sony, Nokia)

Service Excellence-- Access, Customization, After-sales-Service, Packaging

(e.g., Nordstrom, Virgin, Singapore Airl ines)

Process Excellence

-- Procurement, Assembly, Distribution, Logistics(e.g., Wal-Mart, Dell, Southwest)

Innovation is at the Heart of Strategy:

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 33/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

gy

Product, Process, Service Innovations

High

Value

Low

Value

High Cost Low Cost

Product Excellence

OrService Excellence

Process Excellence

VALUE INNOVATION

(Product / Service Innovation)

VALUE NETWORK INNOVATION

(Process Innovation)

Today’s Goal is to Understand

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 34/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

the Innovation Life Cycle

Product

Innovation

Disruptive

Innovation

Service

Innovation

Process

Innovation

Disruptive

Technology

Model

Dominant Design Model

Value-Cost

Model

Shifts in Consumers’ PreferencesCreate Opportunities for New Firms

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 35/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Create Opportunities for New Firms

to Enter or Take Leadership…..

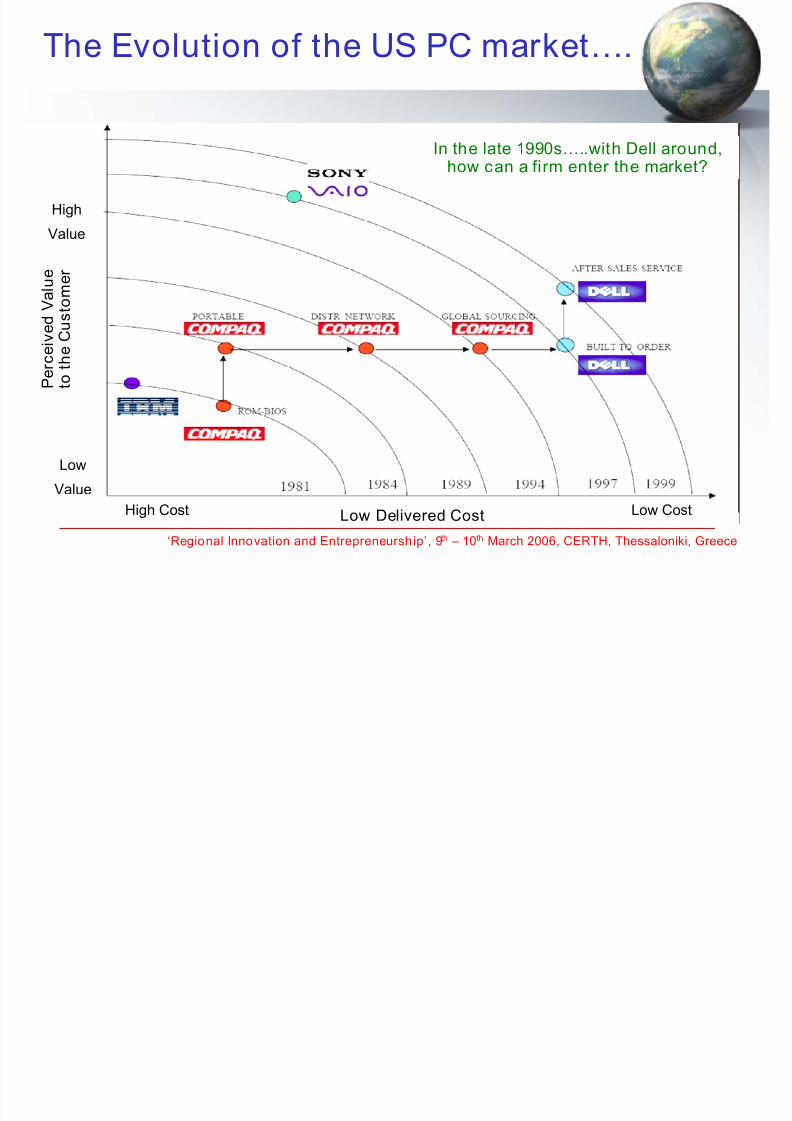

• Dell did not succeed because its product were better thanthose of its competitors.

• The basis of competition shifted from technicalperformance to price, speed, convenience, customizationand after-sales service.

• Dell in the late 1990s:

– Selling more than $50 million per day through its website

– More than 50% of technical support delivered over the web

– Dell held just 5 days worth of inventory – It had a negative cash conversion cycle of 8 days

– It had a 12% cost advantage over rivals

– Since 1999 Dell held the #1 rank in customer satisfaction.

The Evolution of the US PC market

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 36/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

The Evolution of the US PC market….

High Cost Low Cost

Low

Value

High

Value

In the late 1990s…..with Dell around,how can a firm enter the market?

Low Delivered Cost

P e r c e i v e d V a l u e

t o t h e C u s t o

m e r

“ Value Curves” and Competitive

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 37/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Shifts in the industry….

Elements

of Product

or Service

Relative Value Level

PC Servers

Low Medium High

Expandability

Performance

Price

Open Operating System

Compatibility

File & Print Performance

Configurability / Manageabili ty

Storability / Serviceability

Some Well-Known Value

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 38/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Innovators…

• Dell Computers

• IKEA• ZARA

• Virgin Atlantic

• Wal-Mart

• CNN

• Cirque du Soleil

• SAP

ZARA

Wrapping-Up

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 39/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

Wrapping Up

• Need for a paradigm shift in corporate strategy

across all businesses• Value Innovation is not a static achievement but

rather a dynamic process

• As imitators/competitors threaten value innovators

rotate among innovations on:

– Product – Service

– Delivery.

8/13/2019 1.1 -E. Iakovou

http://slidepdf.com/reader/full/11-e-iakovou 40/40

‘Regional Innovation and Entrepreneurship’ , 9th – 10th March 2006, CERTH, Thessaloniki, Greece

tt

THE ENThank you for your attention!