11 · 2013-08-22 · 11.2.1 competition and contestability issues intermodal competition (or the...

TRANSCRIPT

11

11

High Speed Rail Phase 2 / 481

11. Procurement and delivery structures for HSR

11.1 IntroductionThischapterpresentsthepreferreddeliverymodelfortheprocurement,constructionandoperationofafutureHSRprogram.ThismodelestablishesthemostappropriatestructuralmodelforthedeliveryofHSRservicesandthepreferredprocurementoptionsforthedeliveryoftheHSRsystem.

Thechapterisstructuredintothreesections, covering:• Theassessmentofalternativestructuraloptions.• Thepreferredprocurementoptions.• Acomparisonofthepreferreddelivery

modelforHSRinAustraliawiththevariousinternationalexamplesofHSR.

11.2 Preferred delivery model for a future HSR systemGiventhelargeamountofpublicfundingrequired,itisimportantthatthegovernanceandinstitutionalstructuressupportthelikelypublicinterestobjectivesofafutureAustralianHSR program.

ThecentralaimmustbeforHSRtodeliveraneffectiveandaffordabletransportservicetocustomers.Otherobjectiveswouldlikelyincludeensuringthattransportmarketsareefficient,andthattransportsystemsareintegratedandnetworkedandcontributetoregionalandurban development.

Chapter 11 Procurement and delivery structures for HSR

ThereisarangeofoptionsforstructuringthedeliveryofthepreferredHSRsystemtoachievetheseobjectives.Optionsinclude1:• Theseparationofinfrastructurecomponentsof

thepreferredHSRsystemfromthetransportservicessupply,intermsofownershipand/ormanagement(describedas‘verticalseparation’).

• TheseparationofcomponentsofthepreferredHSRsystemoneitherageographicorproductbasis(describedas‘horizontalseparation’).

Competitionissues,includingtheroleofcontestabilityintheprovisionofHSRservices,eitherthroughcompetitionforconcessionrightsordirectcompetitionbetweenservicesuppliers,arecentraltodecidingthemosteffectivedeliveryoptions.Thesearediscussedinthefollowing section.

11.2.1 Competition and contestability issuesIntermodalcompetition(orthethreatofcompetition)fromairandcartravelwouldgenerallyactasastrongbindingconstraintonHSRfareandservicelevelsacrossmostcoreHSRmarketsegments.Asaconsequence,thereisunlikelytobearequirementforeconomicregulationofHSRservices,i.e.thecontrolofHSRpriceandservicelevels,toconstrainthepotentialfortheHSRoperatortoexerciseanymonopoly power.

Evenwithstrongcompetitionfromothermodes,theremaybeadditionalefficiencybenefitsachievedbyencouragingcompetitivepressuresinthesupplyofHSRservices.ThenaturallyhighbarrierstoentryforanewHSRoperatorwishingtocompetewithanincumbentHSRoperatorsuggestthatconsiderationhastobegiventohowtoensureongoingsupply-sidecompetitioninthedeliveryofHSRservicesinAustralia.

Head-to-headcompetitionbetweenHSRlinesinAustraliaisunlikelytobecommerciallyoreconomicallyjustifiedwithinanyreasonable

timeframe,giventhatoneintegratedHSRsystemwouldprovideallofthecapacityAustraliarequiresfortheforeseeablefuture.

AnopenaccessregimetofacilitatemultipleHSRoperatorscompetingforthesamemarketsonthesamerailsystemisprobablynotpractical,giventhealreadygreatchallengeofencouragingatrainoperatingcompanytocommittocreatingasustainabletransportbusinessinagreenfieldmarket.Itisprobablyalsounnecessarybecauseofthecompetitivepressurefromothertransportmodesalreadymentioned.Therefore,verticalseparationoftraincontrolandinfrastructuremaintenancefromtrainoperationswouldnotbenecessarytofacilitatenon-discriminatoryaccessofcompetingtrainoperators.

Competitionforthemarket,i.e.competitionfortherighttoprovidecertainservicesonanexclusivebasisforadefinedperiod,wouldbethemosteffectivemeansofencouragingcompetitivepressuresinthesupplyofHSRservicesandinmeetinggovernments’objectivesfortheHSRprogram.Aconcessionmodelistypicallythemechanismusedtodelivercompetitionforthe market.

Wheretheservicesarecommerciallyviable,thesuccessfulbidderwouldpaygovernmentsfortherighttooperatetheconcession;wheretheyarenot,governmentswouldneedtopaythesuccessfulbiddertooperatetheconcession.Theconcessionagreementensuresthattrainservicesthatusepubliclyfinancedinfrastructuredeliverpublicinterestobjectives(suchasminimumservicelevels)whilehavingsufficientcommercialfreedomandagilitytocompetesuccessfullywiththeothertransportmodes.Thereisarangeofpossibleconcessionmodels,withthevariationsrelatedtotheresponsibilitiesof,anddegreeofriskpassedto,theconcessionholder.Furtherdiscussionoftrainoperationsconcessionsisprovidedinsection 11.3.3.

1 Verticalseparationinthiscontextreferstotheseparationofarailorganisationbyfunction(e.g.operationsandinfrastructure).Horizontalseparationreferstotheseparationofarailorganisationbygeography(e.g.bystateorregion),bylineofbusiness(e.g.urbanoperationsfromregionaloperations)orbyproduct(e.g.inter-capitalfromsuburbanservices).

High Speed Rail Phase 2 / 483

AlthoughgovernmentswouldlikelyowntheHSRsystembecauseofthelargepublicfinancialcontributionrequired,abroadrangeofoptionsexistsforhowthedeliveryofHSRservicescouldbestructured.Theseoptionsareoutlined below.

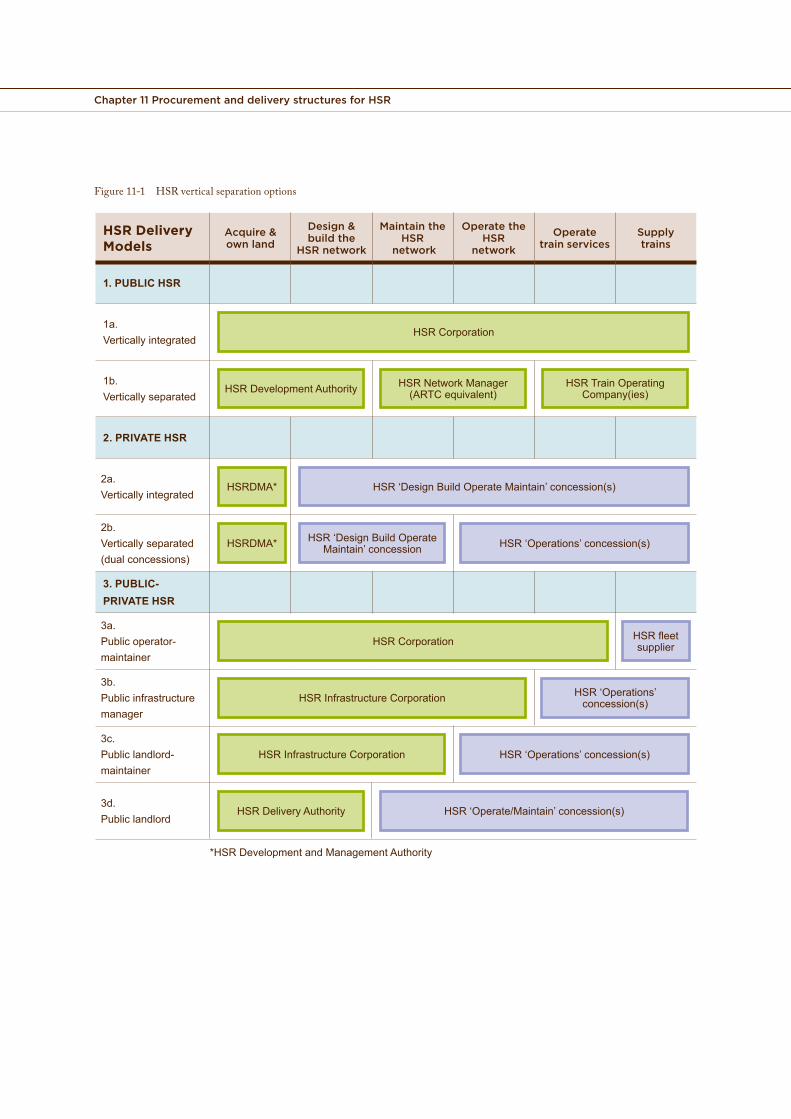

11.2.2 Vertical separation optionsThevariousvertical(orfunctional)separationoptionswouldvarythescopeofpublicandprivatesectorparticipationinthedevelopmentandoperationofthepreferredHSRsystem.Thescopeofpotentialrolesisasfollows:• Acquireandownland–inallcasesitis

assumedthatanentityownedbytheAustralianGovernmentandpossiblytheACTandrelevantstategovernmentswouldacquireandownthelandtosupportthepreferredHSR system.

• DesignandbuildtheHSRsystem–constructingthetrack,structures,signallingandelectricalinfrastructure.

• MaintaintheHSRsystem–maintainingthetrack,structures,signallingandelectrical infrastructure.

• OperatetheHSRsystem–controllingthemovementoftrainsthroughthesystem.

• Operatetrainservices–thedeliveryoftrainservicesinaparticularmarketormarkets.

• Supplytrains–thesupplyofrollingstock,whichmayalsoincludefinanceand/ormaintenanceoftheequipment.

Someoftheserolesmaybebundledtogethertofacilitateoptimalpackagingandprocurementoutcomes,whicharediscussedfurtherinsection 11.3.

Intermsofpublic/privatesectorparticipation,therearethreebroadoptionsfordevelopingandoperatingtheHSRsystem–public,privateoracombinationofpublicandprivatesectors.Withineachbroadoption,therearevarioussub-options,as

outlinedinFigure 11-1.Thelistofsub-optionsinFigure 11-1 isnotexhaustivebutcoversthemaincombinationsobservedinthemarkettoday.

Public HSR delivery optionsUndertheverticallyintegratedpublicHSRoption(1a),apubliclyownedHSRcorporationwouldbecreatedtodevelop,buildandoperatethepreferredHSRsystem.ThecorporationmaybeownedjointlybytherelevantstateandterritorygovernmentsandtheAustralianGovernment2.TheHSRcorporationwouldacquireland,buildtheHSRsystemandprocurerollingstockutilisingtraditionalpublicsectorprocurementapproaches.ThecorporationwouldalsooperateandmaintaintheHSRsystemandoperatetrainservices.Componentsofconstructionandmaintenancecouldbeoutsourcedtoprivatesectorcontractors,butthepublicsectorenterprisewouldmanageandoperatethetrainservices.

Alternativeverticallyseparatedoptionscouldbecontemplatedwhichwouldcreatepublicagenciestodeliverdifferentcomponentsofthesystem,andwhichwouldallowagreaterdegreeoffocusandspecialisation.Option1bcontemplatesanHSRdevelopmentauthority(HSRDA)toconstructthepreferredHSRsystem,aseparateHSRsystemmanagertooperateandmaintainthesystem,andoneormoreHSRtrainoperatingcompaniestooperatethetrainservices.

The‘pure’publicHSRoptionsperformrelativelypoorlyintermsoflikelycompetitivenessandpotentialforinnovation.Althoughintermodalcompetitionwouldexertcompetitivepressureonpubliclyownedtrainoperators,lackofcompetitiononthesupplysidemayleadtoalessefficientandlesscustomerfocusedoutcomethanalternativestructuraloptionsallowingcontestabilityoftrainoperations.ThisconclusionissupportedbygeneralexperienceintransportoperationsinAustraliaandbyinternationalexperience.Historically,Australia’spubliclyownedrailwayshavebeencharacterisedbyrelativelylowproductivity,high

2 ArelevanthistoricalexampleistheNationalRailCorporationwhichwascreatedtooperateinterstaterailfreightservicesandwasinitiallyjointlyownedbytheAustralian,NSWandVictorianGovernments.

Chapter 11 Procurement and delivery structures for HSR

Figure 11-1 HSR vertical separation options

HSR Delivery Models

Acquire & own land

Design & build the

HSR network

Maintain the HSR

network

Operate the HSR

network

Operate train services

Supply trains

1. PUBLIC HSR

1a. Vertically integrated

HSR Corporation

1b. Vertically separated

HSR Development Authority HSR Network Manager(ARTC equivalent)

HSR Train Operating Company(ies)

2. PRIVATE HSR

2a. Vertically integrated

HSRDMA* HSR ‘Design Build Operate Maintain’ concession(s)

2b. Vertically separated (dual concessions)

HSRDMA* HSR ‘Design Build Operate Maintain’ concession HSR ‘Operations’ concession(s)

3. PUBLIC-PRIVATE HSR

3a. Public operator-maintainer

HSR Corporation HSR fleet supplier

3b. Public infrastructure manager

HSR Infrastructure Corporation HSR ‘Operations’ concession(s)

3c.Public landlord-maintainer

HSR Infrastructure Corporation HSR ‘Operations’ concession(s)

3d. Public landlord

HSR Delivery Authority HSR ‘Operate/Maintain’ concession(s)

*HSR Development and Management Authority

High Speed Rail Phase 2 / 485

costsandpoorservicequality3.Freightrailwayshavebeenprogressivelyseparatedandprivatised.PassengerrailwaysstillinpublicownershipinAustraliaarebureaucratic,inefficientandcurrentlyundergoingmajorreformsandthereislikelytobelittlepublicappetitetoestablishanewpublicsectortrainoperator4.

AlthoughtherewouldbeanoptiontocommenceoperationwithapublicoperatorandprivatiseoncetheHSRsystemmatured,ashasbeenthecaseforHSRtrainoperationsinsomecountriessuchasJapan,therewouldseemtobelittleneedforsuchanapproach.Thisoptionwouldforegothebenefitofleveragingprivatesectorexpertise,experienceandincentivestructurestotacklecompetitiveprivatesectorairlinesintheearlyphaseofHSRoperations.Concessionarrangementsforprivatesectoroperatorscouldbestructuredtomanagerisksinthestart-upphase,particularlythemarketrisks,andtherewouldbenocompellingneedtocommenceoperationswithapublicoperator.Therefore,apurepublicdeliverymodel(option1)isnotdesirableandwasnotconsideredfurther.

Private HSR delivery optionsUndertheverticallyintegratedprivateHSRoption(2a),aprivateconcession(orconcessions)wouldbeestablishedtodesign,build,operateandmaintainthepreferredHSRsystem.Privatefinancecouldalsobeutilisedbutwoulddependon,amongotherthings,howthepublicfinancialcontributionswerestructured.IthasbeenassumedthatapubliclyownedHSRDMAwouldneedtobeestablishedtoprocurethelandnecessarytosupportthedevelopmentofthepreferredHSRsystem.

AswiththepublicHSRdeliveryoptions,alternativeverticallyseparatedoptionscouldbecontemplatedthatwouldallowdifferentorganisationstodeliverdifferentcomponentsofthesystem.Option2bcontemplatesan

HSRconcessiontodesign,buildandmaintain(DBM)theHSRsystem.Oneormoreadditionaloperationsconcessionswouldbeestablishedtooperatethesystem(i.e.controllingthemovementoftrainsthroughthenetwork)andtheservice(i.e.deliveringtrainservices).AvariationtothismodelwouldseetheDBMcontractoralsooperatethesystem(i.e.controlthemovementoftrains),whichmayhavesomemeritiftherearemultipleoperationsconcessionsoverthesystem.

ThepurelyprivateHSRoptionstransferconstruction,maintenance,operationsandinvestmentriskstotheprivatesector.Theoperatingrailwayishandedbacktogovernmentsattheendoftheconcessionperiod(s).AnumberoffactorsmakethistypeofcontractproblematicinthecaseofanHSRprogramontheeastcoastofAustralia:• Itwouldnotbefeasibletoprivatelyfinance

thefullinfrastructureinvestment,giventheinabilityoftrainoperationstoprovideacommercialreturnoninfrastructurecosts.

• ThesheersizeandcomplexityofafutureHSRprogramwouldprecludemostprimecontractors(bothdomesticandinternational)fromcarryingtheinfrastructuredeliveryriskontheirbalance sheet.

• Substantialpublicfundingwouldberequired,necessitatinggovernments’responsibilitytoensuretheHSRprogrammeetspublicinterestaimsthroughoversightandstewardship.

• WiderpublicinterestsincludeaneedtointegratethepreferredHSRsystemwithstatetransportsystemsandstateinfrastructure.

Therefore,apurelyprivateHSRdeliverymodel(option2)isnotappropriateandwasnotconsideredfurther.

3 ProductivityCommission,Progress on Rail Reform,InquiryReport,April2000.Williams,GreigandWallis,The Results of Railway privatisation in Australia and New Zealand,TransportPapers,WorldBank,2005.

4 RailCorp,thepassengeroperatorinNSW,iscurrentlyundergoingmajorreform.InMay2012,theNSWGovernmentannouncedmajorreformstotacklemiddlemanagementinefficiencyandbureaucracy–see Sydney Morning Herald19May2012.QueenslandRail,thepassengeroperatorinQueensland,alsorecentlyannouncedthecommencementofreformswithaproposaltoreducecorporateandsupportareasby500personnel(seeMediaStatement,theMinisterforTransportandMainRoads,HonScottEmerson,Tuesday,11September2012).

Chapter 11 Procurement and delivery structures for HSR

Public-private HSR delivery optionsArangeofhybridoptionscontemplatedifferentrolesforthepublicandprivatesectors.Option3aissimilartotheintegratedpublicHSRoption,exceptthatthefleetissuppliedthroughaprivatethirdpartyrollingstocksupplier,similartoPPPfleetarrangementsthatpresentlyexistinsomeAustralianurbanrailways.

Options3bto3drespectivelyprovideanexpandedrolefortheprivatesector.Option3bcontemplatesapubliclyownedHSRinfrastructurecorporationthatwouldbuild,operateandmaintaintheHSRsystem.However,aprivateconcession,orconcessions,wouldbeestablishedtooperatetheHSRtrainservices.Option3cissimilartoOption3bbutwiththeoperationsofthesystem(i.e.thecontrolofthemovementoftrains)undertakenbytheprivatesectortrainoperator.Option3dstillhasthepubliclyownedHSRDAresponsibleforbuildingthepreferredHSRsystem,buttheprivatesectortrainoperatorwouldberesponsibleforbothcontrolofthemovementoftrainsandmaintenanceofthesysteminfrastructure.

ThemostpromisingverticaloptionsforthedeliveryofthepreferredHSRsystemprovideforpublicdeliveryoftheHSRinfrastructurewithtransportservicesprovidedbyprivatecompanies.Evenwithpublicdeliveryoftheinfrastructure,lettingasingleturnkeycontractmaynotbefeasible.Someunbundlingoftheinfrastructureintomultiplecontractswouldberequired.Othervariationsincludetheextenttowhichsystemoperations(i.e.themovementoftrains),infrastructuremaintenanceandrollingstocksupplyarebundledwiththeoperator(s)oftrainservicesorwithalternativesuppliers.

Adetailedassessmentofthepackagingandprocurementoptionswouldberequiredbeforeapreferreddeliverymodelcouldbefinalised,asdiscussedinsection 11.3.

11.2.3 Horizontal separation optionsInadditiontovertical(functional)separationofcomponentsoftheHSRsystem,arangeofhorizontalseparationoptionsmayalsobecontemplated,typicallyeitherbygeographyorproduct(service).InthecontextofanAustralianHSRsystem,themostpromisingoptionsforgeographicseparationrelatetosectorswhichcoverthemajormarketpairs:• Anorthconcession(Brisbane-Sydney).• Asouthconcession

(Sydney-Canberra-Melbourne).

GivenpublicdeliveryoftheHSRinfrastructurenetwork,thehorizontalseparationoptionsareconcernedwiththedeliveryoftrainoperationsandotherfunctions.Separatetrainserviceoperatorsinthenorthandinthesouthcouldeachoperateontheirrespectivesystemsasverticallyintegratedoperations(i.e.witheachoperatingtrainservices,controllingthemovementoftrainsontheirsystems,andpossiblyalsomaintainingtheirsystems).Insuchcircumstancestherewouldbeaneedforajointoperationsarea(suchasCentralstationinSydney)withcommonuseaccessareas.FortheHSRsystemservices(i.e.traincontrol),itwouldbepossibletoseparateintonorthandsouthoperationswithaco-locatedareaatCentralstationinSydney.

Althoughprovidingforseparationofnorthandsouthconcessionswouldaddsomeoperationalcomplexityandcost,forinstancebyhavingtoestablishmultiplecontrolcentresorpossiblyajointfacility,itwouldbefeasible.GiventherecommendedstagingisthatSydney-MelbourneshouldprecedeBrisbane-Sydney,thisoptionwouldpermitaseparatecompetitiontoberunforthenorthconcession.

Optionsalsoexisttosegmentconcessionsbyproductorservicetype.ThisstudyhasidentifiedthreetypesofpotentialHSRproductthatwouldexistonboththenorth(Brisbane-Sydney)andsouth(Sydney-Canberra-Melbourne)lines:

High Speed Rail Phase 2 / 487

• Inter-capitalexpressservices.• Inter-capitalregionalservices.• Commuterservices.

Theseservicescouldbefurthersegmentedintonorthandsouthconcessions.Separatemarketorproductconcessionswouldallowgreatermarketfocusandaccesstospecialistskillsandservices.Forexample,anairlinecompanymightbeastrongcandidateforaconcessionthatalignedHSRregionalserviceswithitsairoperations,whereascommuterHSRoperationsmightbemoreattractivetoanurbanrailoperator.Aswithgeographicseparationoptions,theadditionalbenefitsofmultipleconcessionswouldneedtobeweighedagainstthepotentiallossofsynergiesbetweenoperationsandtheadditionalcostandcomplexity(e.g.multiplecontrolresponsibilities,duplicationoffacilities,havingtosharestation facilities).

InthecontextofthepreferredHSRsystem,separationofcommuterservicesfrominter-capitalexpressandregionalserviceswouldseemmostmerited.Therearestrongoperationalandmarketingsynergiesbetweentheinter-capitalexpressandregionalservicesineitherofthenorthorthesouthsegments,thoughlesssynergybetweenthetwosegmentsthemselves.Bycontrast,commuterserviceswouldhavedifferentcharacteristicsanddifferenteconomicstotheinter-capitalexpressandregionalservices,requiringdifferentrollingstockandlikelyrequiringongoingstategovernmentfinancialsupport.Itmightthereforebedesirabletostructureacommuterconcessioninadifferentwayfromaninter-capitalexpress/regionalconcession(e.g.involvingtrainoperationsonlywithashorterconcessionterm).

Wheretheverticaldeliveryoptionsprovideforsystemoperationstobeundertakenbyatrainoperationsconcession,withmultipleproduct-basedtrainoperationsconcessions(thatis,separatecommuterandinter-capitalexpress/regionaloperators),theinter-capitalexpress/regionaloperatorshouldcontrolthemovementoftrainsonthesystem.Thisarrangementreflectsthisoperator’swiderspanofoperationsanddominantrole.

Thecommuteroperatorswouldbegivenaccessunderanaccessagreementwiththeinter-capitalexpress/regionaloperator.

Aswasthecasewiththeverticalseparationoptions,adetailedassessmentofthepackagingandprocurementoptionswouldberequiredbeforeapreferreddeliverymodelcouldbefinalised,asdiscussedinsection 11.3.

11.3 Procurement and packaging strategy of the preferred HSR systemTheprocurementstrategyforthepreferredHSRsystemwouldneedtotakeintoaccountitsstagedimplementationandensurethattheHSRprogramcouldbeprocuredcosteffectivelyandefficientlytodeliverthebestvalueformoney.Criticalquestions are:• Whatpackageofassetsandservicesshouldbe

procuredinanysinglecontract?• Whatprocurementmodelismostsuitable

for delivery?

11.3.1 Procurement considerationsAsindicatedin section 11.2.2,aprivatefinancingsolutionfortheprocurementofthepreferredHSRsystemwouldnotbefeasible,duetothehighcapitalcosts,theabsenceofsufficientcommercialreturntorecovercapitalcosts,andthesignificantconstruction,deliveryanddemandrisks.

WithrespecttotheprocurementofinfrastructureassetsforthepreferredHSRsystem(broadlycomprisingtunnels,bridges,earthworksandpermanentway),thesizeandscaleoftheworksforanyofthestagesenvisagedasawholewouldbeoutsidethedeliverycapacityofmajorindustryparticipants,bothlocallyandglobally.‘Deliverycapacity’relatestotheabilityto:• Carrytheriskofdeliveryonabalancesheet.• Accessappropriatelevelsofparentcompany

financialsupport.• Carrysufficientinsurance.• Securethedepthandavailabilityofskilled

personnelandotherrelevantresources.

Chapter 11 Procurement and delivery structures for HSR

Deliveryoftheinfrastructureworksasasingle,integratedpackageisthereforeunlikelytogeneratesufficientmarketappetitetogenerateeffectivecompetitionamongcontractors.Theinfrastructureassetspackagewouldthereforeneedtobefurthersplittocreatesub-packagesthatwouldbeattractivetothemarket.

ContractorsintheAustralianmarkethavedemonstratedacapacitytodeliverprojectsof$1-2 billion.ThispackagesizehasthereforebeenadoptedforanalysingtheprocurementoptionsforthepreferredHSRsystem,althoughitisacknowledgedthatatthetimeofprocurementthemarketmayhavethecapacitytodeliverlargerpackages,likelyinconsortiawithinternationalcontractors.Ajudgementwouldneedtobemadeatthetimeofgoingtomarket.

Inadditiontoinfrastructureassets,thereareanumberofothercorenetworkcomponentsincludingsignallingsystems,stations,rollingstockandassetmaintenance.SomecomponentsoftheHSRsystem,suchassignallingandsafeworkingsystemsandrollingstock,wouldrequirespecialisedtechnologicalexpertiseandproducts.Onlyafewglobalcompaniessupplytheadvancedsignallingsystemsand/orrollingstocksuitableforHSR.Thiswouldsuggestthat,wherefeasible,thesecomponentsshouldbepackagedandprocuredinaseparatecompetition,ratherthanformanelementofalargercivilengineeringtender,wheretheabilitytocreatecompetitionbetweenbiddingconsortiawouldbeconstrainedbythelimitednumberofthesespecialisttechnology suppliers.

11.3.2 Core works packagesConstructionofthepreferredHSRsystemwouldbeundertakeninstages,withthecorecomponentsineachstageprocuredthroughthefollowingworkspackages:• Infrastructureassetpackages(broadly

comprisingtunnels,bridges,earthworksandpermanentway)wouldbesplitandprocuredinanumberofsub-packagesofasizeandscopethatisattractivetothemarketandwhichwouldfacilitatestrongcompetitivebidding,generallythroughdesignandconstruct(D&C)contracts.

• Signallingsystemsandrollingstockwouldbedeliveredasacombineddesign,supplyandmaintain(DSM)contract,thenleasedfromtheHSRDMAtotheconcessionoperator.

• StationsandmaintenancewouldbedeliveredasasetofPPPcontracts,combinedwherepossible,butlikelytobeseparatedatmajorcity stations.

Infrastructure assetsAsthesizeoftheinfrastructureassetprocurement(estimatedatarisk-adjustedcostofapproximately$20billion(in$2012)fortheSydney-Canberrastagealone)istoolargetobedeliveredasasingleintegratedpackage,itwouldneedtobesplitandprocuredinanumberofsub-packages.Appendix 7Aprovidesasummaryoftheproposedinfrastructureassetssub-packagingsolutionforSydney-Canberra,whichcomprises11infrastructuresub-packages(includingthreetunnellingpackages).

Thepreferredapproachwouldbefortheinfrastructureassetssub-packagestobedeliveredasindividualD&Ccontracts.Therationaleforthisapproachisasfollows:• Asthescopeofworksandrisksforeachsub-

packageareexpectedtobedefinableandwellunderstood,fixedpricemodels(i.e.D&C)andcompetitivetensionsshoulddeliverbestvalue.Giventherelativelyhighnumberofsub-packages,theHSRDAwouldneedtoimposeahighdegreeofbothtechnicalandperformancespecificationintheD&Ccontractstoensureconsistentandinteroperablestandardsbetweensub-packages.

• Keyrisksrelatingtolandacquisition,planningandenvironmentalapprovalswouldberetainedbygovernmentsinallprocurementoptions.Otherrisks(suchasconstructability)areexpectedtobewellunderstoodandabletobeassessedbycontractors.Assuch,riskcanbeeffectivelytransferredtothepartybestabletomanagethatrisk,whichsupportstheuseofaD&Cmodel.

• Internationalanddomesticmarketinterestislikelytobesignificantforeachsub-package,whichshouldcreatecompetitivetensionsand

High Speed Rail Phase 2 / 489

enablegovernmentstodrivevalueformoneythroughthetenderprocess.AD&Cmodeliswellunderstoodbythecontractormarket.

• AD&Cmodelinvolvesashorterandlesscomplexprocurementprocessrelativetotheotherprocurementoptions,suchasdesign,buildandmaintain(DBM),giventhemorelimitedscope(e.g.excludinginfrastructuremaintenanceandoperations)andmorelimitedrisktransfer(e.g.constructionrisksonly).

Procuringmultiplesub-packagesofworkswouldcreatesignificantandcomplexinterfacerisksbetweencontracts.Forinstance,thereareinterfacesbetweentheindividual‘geographic’workspackages,betweeninfrastructureworksandtechnologysystems,andbetweenstationscontracts.Theseriskswouldinevitablyberetainedbygovernmentsirrespectiveofthedeliverymodelforeachsub-package.

Tomitigatethisrisk,governments,throughtheHSRDA,wouldneedtoretainastrongtechnicalcapabilitytoeffectivelyspecifyinterfacestandardsandoverseedeliveryoftheD&Ccontracts.Underthismodel,governmentsareeffectivelytakingontheroleofsystemsintegratorandwouldneedtosecond,orcontract,worldclasssystemsintegrationexpertisetomanagetheinterfacerisksinthecontractingstrategy.ProcuringafutureHSRprogramusingproventechnologyandcontemporaryinternationalstandardsandprotocolsofthetimewouldalsohelptomitigatethisrisk.

Signalling systems and rolling stockModerntraincontrolandsignallingsystemsrelyheavilyondigitalcommunicationsandin-cabequipment,comparedwithhistoricalsystems,whichreliedalmostexclusivelyontrack-sideinfrastructure.TheAustralianRailTrackCorporation(ARTC)iscurrentlyimplementingacommunications-basedsignallingandsafe-workingsystemacrossitsnationalrailfreightnetwork.Interfacesbetweenthetraincontrolandsignallingsystems,thecommunicationssystemsandtherollingstockareconsideredoneofthebiggestsystemintegrationrisksintheprocurementofthepreferredHSRsystem.

Bypackagingthesignallingsystemsandrollingstocktogether,thiskeyrisk(includingrollingstockcommissioningandacceptancerisk)islikelytobesubstantially,ifnotentirely,transferredtotheprivatecontractor.Therewouldalsobesignificantcommissioningefficiencies,giventhetraincontrolandsignallingsystemsandrollingstockwouldbedevelopedinconjunctionwitheachother.

Reflectingtheuniquenatureofthesignallingworksandrollingstockpackage,thepreferredprocurementoptionisaDSMcontract,asopposedtoadesignandsupply(D&S)contract.Therationaleforthisapproachisthat:• Linkingsupplyandmaintenancefora

significantpartoftherollingstock’slifeencouragesawhole-of-lifeapproachbythecontractor.ADSMmodelwouldlikelydrivethebestvalueformoneyoutcome,sincecontractorswouldbeinherentlyincentivisedtoreflectthemaintainabilityofthesysteminits design.

• Thesignallingsystemsandrollingstockcomponentsarelikelytooffersignificantopportunitiesforcontractorinvolvementintermsofmarketinnovationinallaspectsoftherespectivetechnicalsolutions.Deliverymodelsthataccessinnovationfrommultiplepartiesthroughacompetitiveprocessshoulddeliverthemostinnovation.ADSMmodelwouldachievethisoutcome.

• Thechoiceofsignallingsystemwouldneedtoensureitdoesnotconstrainflexibilityand/orcompetitivetensionforfuturesignallingprocurementsinsubsequentstagesoftheHSRprogram.OneapproachwouldbefortheHSRDAtospecifyasignallingperformancerequirementbasedonopenarchitecturesystems,suchasEuropeanTrainControlSystemLevel2.Thiswouldfacilitateinteroperabilitywithhardwarefromothersuppliersutilisingthesameprotocols,therebyensuringmultiplesupplierscouldbidforsignallingsystemsprocurementsforlaterHSRprogramstages.

Chapter 11 Procurement and delivery structures for HSR

TheHSRDMAwouldprocurethetraincontrolandrollingstockassets,withtherollingstockbeingsubjecttoafinanceleasearrangementtofundthesupplycomponentoftheDSMcontract.TheHSRDMAwouldleasethetraincontrolsystemandnovatetherollingstockfinanceleaseandmaintenancearrangements(undertheDSMcontract)tothetrainoperationsconcessionaire.

StationsGreenfield stationsTheoptimalapproachwouldbeforthegreenfieldstationstobedeliveredasmultiplePPPs.ThePPPmodelwouldbestructuredtoincluderesponsibilityfordesigning,building(includingstationfit-out),financingandmaintaining(butnotoperating)thestationoveraperiodof20to25years.ThePPPmodelwouldlikelybebasedonaformofaccesscharge.TherationaleforaPPPapproachis:• Thestationspackage,includingmaintenance,

offersoneofthefewopportunitiestocaptureprivatefinancefortheHSRprogram.ExperienceindicatesthatthereismarketappetiteforPPPstationsinAustralia(e.g.SouthernCrossstationinVictoria).

• APPPmodelwoulddeliverenhancedvalueformoneythroughtheprivatecontractorandfinancierdrivingoptimumon-timeandqualityperformance,andthroughsynergiescreatedbybundlingtherelevantdesign,constructionandmaintenanceservices.

Thereshouldbebenefitsfromprocuringandconstructingthenon-CBDgreenfieldstationsfortheinitialstageofconstructionaspartofasinglePPPcontract,giventheyarelikelytohaveacommonriskprofile(specificcivilworks),synergisticbenefits(suchasreducedpreliminariesandoverheads)andpotentiallyreducedinterfacerisks(withonecontractorresponsibleforallstagestations).Greenfieldstationswithinastage(e.g.SydneySouthandSouthernHighlandsstationsintheSydney-Canberrastage)wouldbepackagedtogetherandprocuredusingaPPPmodel.Revenuetofundprocurementwouldcomefromstationaccesschargespaidbythetrainoperatingconcessionaireandotherpossiblecashflowssuchascarparking.Theremight

bebenefitsinfurthersplittingthegreenfieldstationsintoindividualsub-packages,asitcouldfacilitateincreasedcompetitionandopenupthedevelopmentopportunitytosmallerconstructionfirms.ThisdecisioncanbemadebytheHSRDAattheprocurementstagebasedoncontemporarymarket conditions.

CBD stationsWithrespecttotheCBDstations,suchasCentralstationinSydney,abroadersetofconsiderationswouldcomeintoplay,includingtheredevelopmentofexistingstationsandconnectivitywithexistingtransportsystems,linkstobroaderstationprecinctdevelopmentandthebroaderoperationalanddevelopmentobjectivesofthestateandACTgovernments.TheCBDbrownfieldstationredevelopmentswouldbeseparatelypackagedandprocuredasanalliance,D&CorDCMcontract,subjecttothetechnical,interfaceandriskattributesoftheworks,particularlytheinterfacewithCentralstationandassociatedtrain operations.

Propertyandcommercialdevelopmentopportunitiesmayexistaboveandaroundstations.Thisrevenuewouldbemaximisedbyimplementinga‘precinctplanning’approachtonewstationsthatfocusesonmaximisinglanddevelopmentandusesateachstationandintegrationofstationswithinthoseprecincts.

Inclusionofpropertydevelopmentwiththestationspackageneedstobeassessedonacase-by-casebasis.Ontheonehand,propertyandcommercialdevelopmentcouldbebestpursuedseparatelyfromthePPPs,basedonthefollowing:

• Theskillsrequiredtoundertakepropertydevelopmentactivitiesdifferfromthoserequiredtodesign,constructandcommissionlargerailtransportinfrastructureprojects.

• Thefinancingrequirementsandbankabilityofreturnsdifferbetweeninfrastructureprojectsandpropertydevelopmentprojects.

• SeparationofaPPP,whichisintegraltotheoperationoftheHSR,fromcommercialdevelopmentencouragesthecompletefocusofthePPPcontractor.

High Speed Rail Phase 2 / 491

However,thereisacountervailingviewthatincludingthepropertydevelopmentopportunitieswiththestationworkspackagewouldallowforbetterassimilationofthestationandthedevelopmentaroundit,particularlywherethedevelopmentisintegraltotheoperationofthestation.Inaddition,inclusionofskilledpropertyspecialistsinthedesignandconstructionofthestationscanensurethatthevalueofthepropertydevelopmentopportunitiesismaximised.

Atthisstage,theoptionforincludingpropertydevelopmentopportunitiesshouldbeleftopen.TheviabilityandoptimalformofaPPPsolutionforthegreenfieldHSRstationsshouldbesubjecttoarobustvalueformoneyassessmentbytheHSRDAatthetimeofgoingtomarket.

11.3.3 Train operations concessionsTrainoperationsconcessionswouldbeofferedtothemarketandwouldcombine:• Theoperationoftrainservices,includingthe

operationofstations.• Controlofthemovementoftrains.• Maintenanceoftheinfrastructureassets.

Maintenanceoftherollingstock,signallingequipmentandcontrolcentreswouldbetheresponsibilityofaseparateDSMcontractor.AlthoughtheDSMcontractwouldbeheldbytheHSRDA,itwouldbestructuredtofacilitatedeliveryofthecontractor’smaintenanceobligationsincollaborationwiththetrainoperations concessionaire.

Governmentsshouldpreservetheoption,butnotassumetheobligation,toawardseparateconcessionsforcombinedinter-capitalexpress/regionaloperationsnorthandsouthofSydney,withthepotentialforacompanytobidforboth concessions.

Allocationoftrackcapacitybetweeninter-capitalexpress/regionalconcessionholdersandcommuteroperationswouldbetheresponsibilityoftheHSRDMA.TrackcapacityforcommuterserviceswouldbenegotiatedbytheHSRDMAwitheach

stateandterritory,andtheinter-capitalexpress/regionalHSRconcessionholderwouldprovideaccesstotheHSRnetwork(i.e.wouldprovideagreedtrainpaths)forthecommuteroperatorassetoutinitsconcessionagreement.

Therationalefortheproposedapproachis:• Aneffectivelystructuredconcessionshould

facilitateavalueformoneytransferofongoingoperational,maintenanceandcommercialriskstotheoperator.Inaddition,aconcessionarrangementhastheadvantageofashorterfixedterm(ofaroundtento15years)comparedtoalternativeprivatisationmodels,whichwouldpermitgovernmentstomorefrequentlytestthemarketandcapturethebenefitsofcompetitionbetweenpotentialcontractors.

• ItisunlikelythattheconcessionholderwouldassumethefullrevenueriskassociatedwithHSRoperationsuntilthesystemisproven.Theremay,however,beconcessionaireinterestinamechanismtoshareadegreeofrevenueriskwherecompetitivetensionfortheconcessioncontractdrivesit.Givenrevenueriskoffersgovernmentsthebestopportunitytoincentiviseappropriateoperatorbehaviours,includinginrespectofimprovedcustomerservice,aconcessionstructuredtoshareadegreeofrevenueriskwouldbepreferred.

• Procuringtheinfrastructureassetsandmaintenanceandtraincontrolservicesaspartofthetrainoperatingconcessionwouldmateriallyreduceinterfacecomplexitiesasitcreatesasinglepointofaccountabilityforday-to-dayoperationofthepreferredHSRsystem,eveniftheoperatorsubcontractscomponentsofmaintenancetospecialistmaintenance companies.

• CreatinginstitutionalstructuresthatwouldallowforseparateconcessionsnorthandsouthofSydneyprovidestheoptionofeffectivecompetitionforservicesprovisiononthelaternorthstagesofafutureHSRprogram.Separatingcommuterconcessionsallowsspecificarrangementstobeestablishedwithstateandterritorygovernmentsfortheirdelivery,withoutcompromisingthedeliveryofcompetitivecommercialinter-capitalexpress/

Chapter 11 Procurement and delivery structures for HSR

regionalHSRservices.AllowingoperatorstobidformultipleconcessionsallowsthemarkettodeterminetheoptimalnumberofoperatorsontheHSRnetwork.

Theproposedtrainoperationsconcessionswouldbestructuredona‘netcost’basis.Thatis,theoperatorwouldtakebothrevenueandcostriskandwouldbidfortheconcessiononthebasisofthenetcost(afterforecastrevenueisdeductedfromforecastcosts).IntheearlystagesofthepreferredHSRsystemdelivery,itwouldbenecessaryfortherevenuerisktobeprimarilyunderwrittenbygovernment,givenitsgreenfieldnature,butwithincentivesfortheoperatortobuilddemand,innovateanddeliverhighqualityservices.Governmentsmaychoosetosetmaximumfaresforspecificfaretypes(suchaseconomyclass)andminimumservicelevelstoensuretheirsubstantialinvestmentinHSRdeliverstheintendedpublic benefits.

TheconcessionagreementwouldbestructuredsothatcommercialrevenuesfromtheHSRoperatorswouldcovertheirtrainoperatingcosts,thenetworkoperationsandinfrastructuremaintenancecosts,andmakeacontributiontocapitalcosts.TherollingstockwouldbeprocuredthroughtheDSMcontractandleasedbytheHSRDMAtotheconcessionholderonacommercialbasis.Commercialrevenuesfromtheconcessionswouldnotbeabletofundthefullcostsoftheinfrastructurecapital,butanaccesschargewouldbeimposed,similartothemodelthatappliesinJapan.Theconcessionarrangementswouldneedtostrikeabalancebetweenprovidingprofitincentivestotheconcessionholdersandmaximisingthefinancialrecoveryofthepublicinvestmentin infrastructure.

11.4 Comparison with international models for HSRAcrosstheglobe,thereisnosingle,wellestablishedgovernanceandinstitutionalmodelforHSR.Differencesinconstitutional,industryandmarketstructurespreventthesimpletranslationofapproachesfromotherjurisdictionstoAustralia.

ThepreferredHSRsystemidentifiedinthisstudyhasbeendevelopedspecificallyfortheeastcoastofAustralia,basedonAustraliancircumstancesandparameters.However,giventhesimilarpolicydimensionsandeconomicchallengesofHSRinAustraliaandothercountries,itisnotunexpectedthatmanyofthefeaturesofthepreferredHSRsystemarealsofoundincountrieswhereHSRhasbeenadopted.ThissectioncomparesthegovernanceandinstitutionalmodelfortheHSRprograminAustraliawiththeinstitutionalmodelsforoperatingHSRservicesinothercountries(seeTable 11-1).FurtherdetailsofinternationalcasestudiesarepresentedinAppendix 7A.

Inalltheoverseasexamplespresented,thegovernmentownstheHSRinfrastructure,havingviewedHSRaspublicinfrastructureofnationalimportanceand/orcontributedsubstantiallytoitsfunding.Invirtuallyallcases,thegovernmenthasalsoretainedanongoingroleinthestewardshipofthesector.ThestudyrecommendsthesameapproachbeadoptedbygovernmentsforthedeliveryofthepreferredHSR system.

Inmostoverseascases,HSRinfrastructureisadministeredonbehalfofthegovernmentbyastate-ownedentity,althoughthereareexceptions.IntheUnitedKingdomandNetherlands,privatemanagersholdtheconcessions,whileinJapan,responsibilityhasbeendevolvedtoprivatetrainoperatingcompaniesthroughalease-styleagreement.ForAustralia,itisproposedthatthedeliveryandmanagementofthesystembeundertakenbyagovernment-ownedHSRDA,whichwouldevolveduringtheoperationalphaseintoadeliveryandmanagementauthority (HSRDMA).

High Speed Rail Phase 2 / 493

ThesevenEuropeanUnion(EU)countrieswith to-dayresponsibilityofbothtraincontrolandHSRlineslistedinTable 11-1areallobliged infrastructuremaintenance.toprovidethirdpartyaccesstotrainsthatcross

Althoughstate-ownedtrainoperatingcompaniesinternationalboundariesofmemberstates,indominateinmostofthecountrieswithHSR,accordancewithEURailwayDirectivesandallthosecountrieshadadominantstate-ownedsinglemarketprinciples.Inpractice,thirdpartynationalrailpassengeroperatorbeforetheHSRtrainkilometresarecurrentlyaveryminorintroductionofHSR.Giventhecompetenceandproportionofthetotalinanycountrycomparedexperience(andpoliticalpower)ofthoseexistingwiththedominantHSRoperator,exceptincompanies,theassumptionofresponsibilityBelgium,wheretheservicesoffourmemberforoperatingHSRfellnaturallytothem(ortostates’HSRcompanies(insomecasesjointsubsidiarycompanies).InAustralia,wherenoventuresofmemberstates)convergeinBrussels.singlesubstantialordominantlong-distanceOnlyGermanyprovidesthirdpartyaccesstopassengerrailtransportsupplierexists,thedomesticHSRroutes,butnoprivatethirdpartyawardofconcessionstoproperlyqualifiedprivateHSRoperatorhasyetenteredthemarket.Fastcompaniestooperatetrainsisrecommended.commuter-typeservicesalsouseHSRlinesin

Germany(aspartofthestate-ownedrailoperator’s ThepreferredmodelforAustraliaisperhapsproductoffering)andintheUnitedKingdom, closest,thoughnotidentical,totheJapanesemodelontheHS1track(operatedbyacommuter fornewHSRlines.InJapan,asinglestate-ownedconcession company). entity,JRTT,isresponsibleforthedevelopment

andstrategicmanagementoftheHSRnetwork,ThestudyproposesthatAustralianHSRbutoperationoftrainservices,controloftheconcessionsnotadoptanEU-styleaccessregimemovementoftrainsandmaintenanceoflinesbutinsteadconcedeexclusiverightstoprovidetheiscarriedoutby(mainly)privatesectortraindefinedservicegroups,thoughthestructurewouldoperatingcompaniesservingparticularhighspeedbeconsistentwithsomeoverlapatafewstationsroutesonanexclusivebasis,forwhichtheypay(suchasNewcastle)betweenlong-distanceandJRTTafeetousetheline.commuterconcessions.ForAustralia,itisproposedthatanHSRDATofacilitatetheopenaccessarrangements,the(whichwouldevolveintoanHSRDMA)beEUcountriesoperatingHSRhaveseparatedestablishedtodevelopandmanagetheHSRinfrastructureoperationsandmaintenancenetwork,butthattheoperationoftrainservices,fromtrainoperationsbycreatingseparateincludingcontrolofthemovementoftrainsandinfrastructure companies.maintenanceoflines,beconcessionedtoaprivate

InGermany,thenetworkcompanyisasubsidiary sectortrainoperatingcompanytoserveaspecificofthestate-ownedrailoperator,butinmost routeonanexclusivebasis.InAustralia’scase,thecasesseparatestate-ownedcompanieshavebeen optiontodevelopseparateconcessionsnorthandestablished.InFrance,thetraincontroland southofSydneyshouldbepreserved.maintenanceofthenetworkiscontractedbytheinfrastructurecompanybacktothedominantstate-ownedtrainoperator.InFrance,theUnitedKingdom,Japan,ChinaandTaiwan,thedominanttrainoperatingentityisresponsiblefortraincontrolandinfrastructuremaintenanceeitherdirectly,underconcessionorundercontract.ForAustralia,thiswouldalsobethepreferredapproach,realisedthroughaconcessionstructurethatwouldincludedevolutionofday-

Chapter 11 Procurement and delivery structures for HSR

Table 11-1 Features of institutional frameworks for the preferred HSR system on the east coast of Australia and for international HSR systems

Preferred Australian model

France Germany Great Britain (HS1)

Italy

HSR lines ownership

Public Public Public Public Public

HSR network administration

HSRDA (state-owned)

RFF (state-owned)

DB Netz (state-owned)

HS1 Ltd (private)

RFI (state-owned)

HSR network Contracted by Contracted DB Netz Contracted RFIoperations HRSDA to by RFF to by HS1 to (train control dominant train dominant train national function) operations

concessionaireoperations entity (SNCF)

network operator (Network Rail)

HSR network Contracted by Contracted DB Netz Contracted RFImaintenance HRSDA to by RFF to by HS1 to

dominant train dominant train national operations operations network concessionaire entity (SNCF) operator

(Network Rail)Third party No For For For For infrastructure international international international international access rights for trains of trains of trains of trains of HSR trains member states

(EU law)member states (EU law)

member states (EU law)

member states (EU law)

HSR Private Dominated by Dominated by International Trenitalia passenger train concessions: SNCF DB Fernvekehr HSR services (state-owned)operations • Inter-capital

express south• Inter-capital

(state-owned)

Plus a few international

(state-owned)

Plus a few international

operated by Eurostar (state-owned)

NTV (private open access operator)

express north trains using trains using Domestic fast • Commuter track access track access services by

by state (3) rights rights Southeastern (private concession)

Source: Compiled from multiple sources, including Beckers et al., Long-Distance Passenger Rail Services in Europe: Market Access Models and Implications for Germany, Discussion Paper No. 2009-22, OECD/ITF, December 2009.

High Speed Rail Phase 2 / 495

Belgium Netherlands Spain Japan China Taiwan

HSR lines ownership

Public Public Public Public (new HSR) lines)

Public Public

HSR network Infrabel Infraspeed Adif JRTT (state- Joint venture THSRC administration (state- (private) (state- owned) companies (initially private

owned) owned) leases lines (typically but now public to train majority- following operating companies

owned Ministry of

government take-over in

to manage Railways, plus provincial

2009)

governments)HSR network Infrabel Infraspeed Adif Contracted Ministry of THSRC operations to train Railways (train control operating (the national function) company

by lease agreement

railway manager)

HSR network maintenance

Infrabel Infraspeed Adif Contracted to train operating company by lease agreement

Ministry of Railways

THSRC

Third party infrastructure access rights for HSR trains

For international trains of member states (EU law)

For international trains of member states (EU law)

For international trains of member states (EU law)

No No No

HSR Several Two Renfe Three private Ministry of THSRC passenger train state-owned concessions: Operadora and one Railways • 35 year operations operators of • NS Hi (state- state-owned concession

international Speed (state owned) companies for train HSR trains owned) serving operations

Thalys Eurostar, Fyra, DB

until 2015) • HAS (NS/

KLM joint-

different routes/regions

• Separate 50 year concession for

Inter-city venture) station area Express until 2024 redevelopment(ICE), TGV

Source: Compiled from multiple sources, including Beckers et al., Long-Distance Passenger Rail Services in Europe: Market Access Models and Implications for Germany, Discussion Paper No. 2009-22, OECD/ITF, December 2009.

Chapter 11 Procurement and delivery structures for HSR

11.5 ConclusionThefollowingkeyconclusionshavebeenreachedinregardtothepreferreddeliverymodelforafutureHSRprogram:• ApubliclyownedHSRDAwouldbe

establishedtodevelopandmanagetheHSRsystem,buttheoperationoftrainservices,includingcontrolofthemovementoftrainsandmaintenanceoflines,wouldbeconcessionedtotheprivatesectortoserveaspecificrouteonanexclusivebasis.

• TheoptiontodevelopseparateconcessionsnorthandsouthofSydneyshouldbepreserved.

• ConstructionofthepreferredHSRsystembytheHSRDAwouldbeundertakeninstages,withthecoresystemcomponentsineachstageprocuredthroughthefollowingworks packages:– Infrastructureassetpackages(broadly

comprisingtunnels,bridges,earthworksandpermanentway)wouldbesplitandprocuredinanumberofsub-packages,ofasizeandscopethatisattractiveandmanageabletothemarketandthatwouldfacilitatestrongcompetitivebidding,generallythroughanumberofD&Ccontracts.

– SignallingsystemsandrollingstockwouldbedeliveredasacombinedDSMcontract,andthenleasedfromtheHSRDMAtotheconcession operator.

– StationsandmaintenancewouldbedeliveredasasetofPPPcontracts,combinedwherepossible,butlikelytobeseparatedatmajorcitystations.