100g overview and outlook - vde...

TRANSCRIPT

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.1

100G Overview and

Outlook

Driving business value through collaborative intelligence

Dana Cooperson, VP Network Infrastructure

20 September 2009

ECOC Workshop 5

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.2

Agenda

� Where are we?

� Lessons from 40G and 10G

� Outlook

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.3

If I had a € for every time a service provider said…

“I’d deploy 100G

today if I had it.”

…I’d be richer, if no less skeptical.

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.4

What will drive deployment pace?

� Availability

� Economics

� Alternatives; e.g., light a 10G λ or do a network overbuild� Timeframe and scope of business case calculation vs. capex available

� Investment and Innovation, for an end-to-end solution

� Standards, e.g. for client and line optics� Merchant and captive chips, modules/MSAs

� Outlook

� Traffic growth, revenue growth, macroeconomic indicators, …

� Ugliness (size, power) vs. the desire for Ubiquity (operationalizing)

� (sometimes) You just gotta do it

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.5

100G timeline: From “heroes to hype”…

� Verizon tested Alcatel-Lucent 100G with live traffic (504km) network Tampa – Miami, FL

� Ciena demo’d 100G OTN at SC08

� AT&T and NEC demo’d 61 wavelengths @ 114Gbps each

� Verizon tested NSN100G over 1040kmdistance

� Comcast tested Nortel100G prototype –300km span of livenetwork

� VZ tested Nortel 100G on high PMD fiber

� OpVista demo’d 100G using proprietary DMC technology

� Huawei announced 100G prototype

� Ciena and NYSE Euronextannounced 2010 deployment of 100G

� Neos Networks tested Nortel100G in live network trial

� Banverket ICT completed live trial of Nortel 100G

� DT and Ericsson completed 100G field trial

� Juniper announced 100GE interface for T1600 router

� Alcatel-Lucent announced 100G interfaces for 7750 SR, 7450 ES, and 1625 LamdaXtreme

� Qwest announced 2010 deployment of ALU 100G network

� Adva demo’d DPSK-3ASK 100G modulation format

� IEEE 100GE standard approval in June 2010

� NYSE Euronextdeployment

� Qwest network-wide deployment

2007

R&D 2008

Demos2009

Trials & first products 2010

Standards,

Early adopters

…with lots of “heavy lifting” along the way

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.6

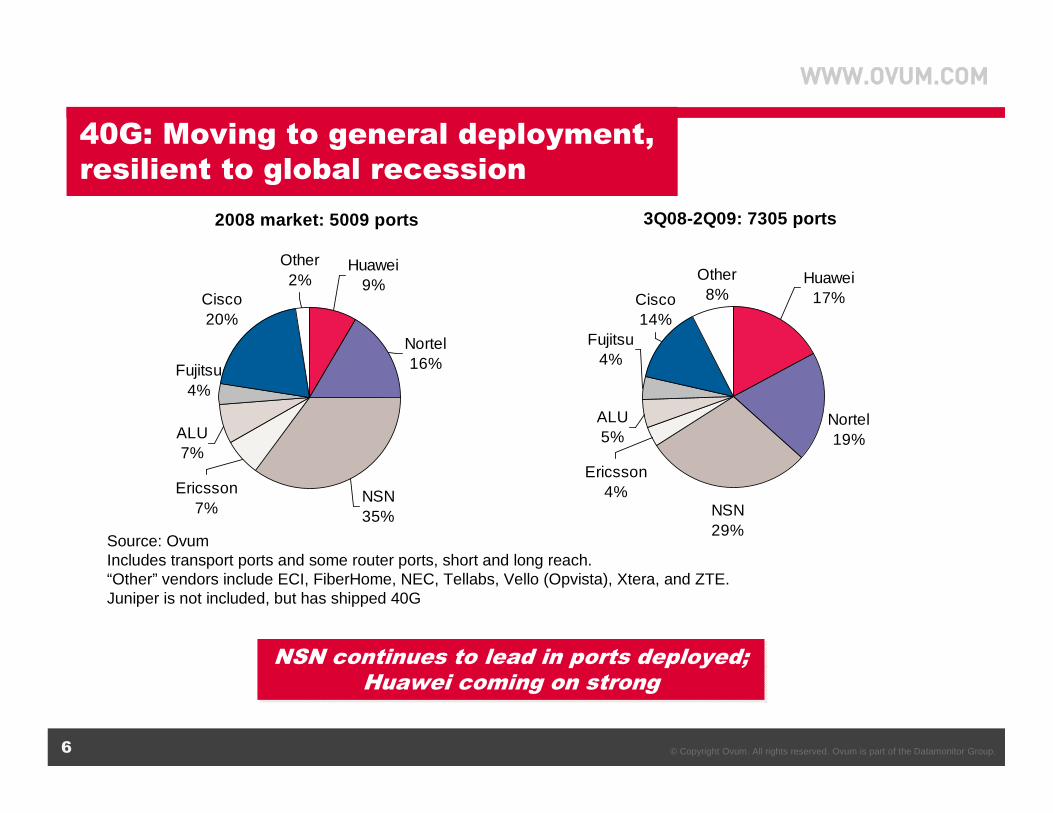

40G: Moving to general deployment,

resilient to global recession

2008 market: 5009 ports

Cisco20%

Other2%

Ericsson7%

ALU7%

NSN35%

Fujitsu4%

Huawei9%

Nortel16%

Source: OvumIncludes transport ports and some router ports, short and long reach. “Other” vendors include ECI, FiberHome, NEC, Tellabs, Vello (Opvista), Xtera, and ZTE.Juniper is not included, but has shipped 40G

3Q08-2Q09: 7305 ports

Cisco14%

Other8%

Ericsson4%

ALU5%

NSN29%

Fujitsu4%

Huawei17%

Nortel19%

NSN continues to lead in ports deployed;Huawei coming on strong

NSN continues to lead in ports deployed;Huawei coming on strong

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Year1

Year2

Year3

Year4

Year5

Year6

Year7

Year8

Year9

Year10

Year11

Year12

Year13

Year14

Year15

Year16

Year17

Year18

AS

P R

atio

s (x

)10G / 2.5G ASP Ratio 40G / 10G ASP Ratio

The bottom line comparison: Transponder ASP ratios

� Red zone: Heroes, hype, haggling, and headway

� Yellow zone: Economics move in favor of higher-capacity signal

� Green means go: Volume parity is likely to happen.

� Too early to graph 100G curve, but highly likely to improve on 40G’s timeline

� WDM transponders will benefit from datacom’s use of 40GE/100GE

Telecom bust

10G price

decline>>40G

You are here

10G/2.5 unit parity

Year 1

1996: 10G/2.5G

2006: 40G/10G

Source: OvumASP = Average Sales Price

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.8

Global 40/100G volume forecast

40/100G line card volume

0

20,000

40,000

60,000

80,000

100,000

120,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Un

its

40G backbone 40G metro 100GSource: OvumNotes: Figure on left is strictly ON systems transponders, does not included router SR or transponder sales.

Figure on right is Ethernet transceivers for datacom (aka short reach) applications.MSA is multi-source agreement; IA is implementation agreement

DWDM WAN transponder cards:CAGR (2008-2014) = 72%

Volume will be critical to lower price; standards, MSAs, IAs will all helpWAN prices/volumes should benefit from IEEE/ITU spec coordination

Ethernet transceivers:CAGR (2009-2014) = 240%

Datacom 40GE & 100GE Forecast

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2009 2010 2011 2012 2013 2014U

nits

40GE 100GE

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.9

100G outlook and 10G/40G lessons learned

� Overall market health (or lack of health) can drastically affect the pace of innovation and deployments

� Venture capital firms’ telecoms investment trend is worrying

� More technology options aren’t necessarily better

� First to market doesn’t guarantee market leadership, volume does

� Components can and will be critical path

� Operationalizing a technology can take years

� Product flexibility is critical, e.g. mixing waves in a shelf, in a span

� 100G interest is clear, but deployments will depend— a lot—on comparative port ASPs

� Datacom is the volume market for 100GE and 40GE through 2014

© Copyright Ovum. All rights reserved. Ovum is part of the Datamonitor Group.10

THANK YOU

For more information about Ovum Telecoms, please contact us at [email protected]