100209 george cope business overview - bce inc. · 2006-2008 highlights arpu increased by over $3...

TRANSCRIPT

George CopePresident and Chief Executive Officer

Cautionary statement concerning forward-looking statements

Today’s remarks will contain forward-looking statements with respect to items such as revenue, EBITDA, earnings per share, free cash flow and capital intensity and other statements that are not historical facts. Several assumptions were made by BCE in preparing these forward-looking statements and there are risks that actual results will differ materially from those contemplated by the forward-looking statements. As a result, we cannot guarantee that any forward-looking statement will materialize and you are cautioned not to place undue reliance on these forward-looking statements. For additional information on such assumptions and risks, please consult BCE’s Safe Harbour Notice Concerning Forward-Looking Statements dated February 11, 2009 filed by BCE with the Canadian securities commissions and with the SEC and which is also available on BCE’s website.

Forward-looking statements made today represent BCE’s expectations as of February 11, 2009 and, accordingly, are subject to change after such date. Except as may be required by Canadian securities laws, we do not undertake any obligation to update any forward-looking statement made today, whether as a result of new information, future events or otherwise.

5 strategic imperatives

Strategic imperatives

Achieve a competitive cost structure

Accelerate wireless

Leverage wireline momentum

Invest in broadband network and services

Improve customer service

1

2

3

4

5

Our goal

“To be recognized by customers as Canada’s leading communications company”

Focused on key drivers of value

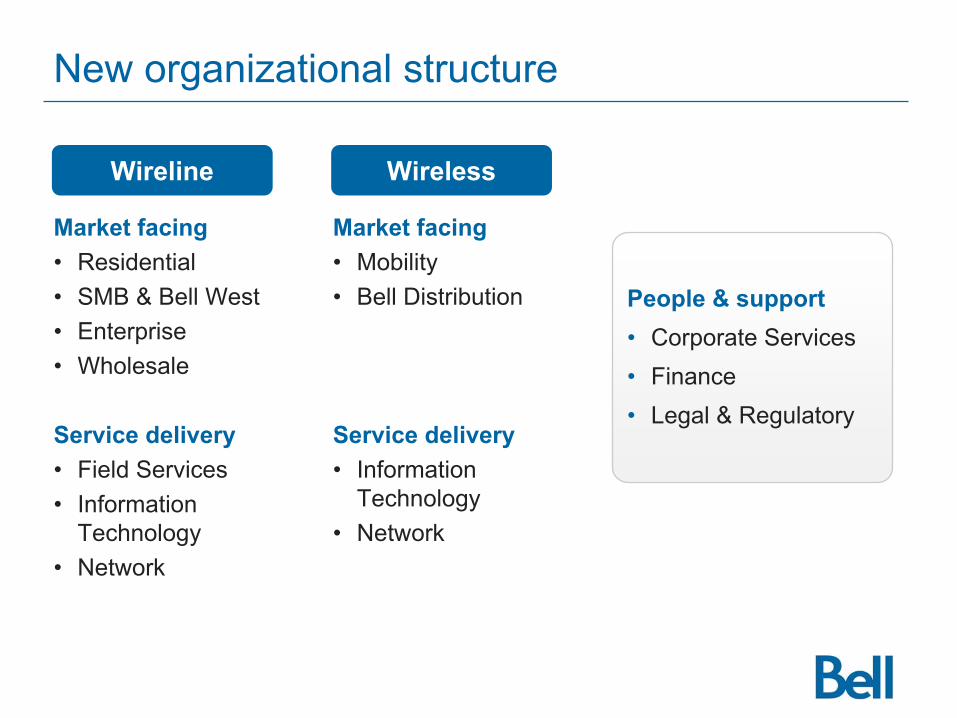

New organizational structure

Market facing• Residential• SMB & Bell West• Enterprise• Wholesale

Service delivery• Field Services• Information

Technology• Network

Wireline

Market facing• Mobility• Bell Distribution

Service delivery• Information

Technology• Network

Wireless

People & support• Corporate Services• Finance• Legal & Regulatory

New executive team

Mary Ann Turcke Executive Vice-President –

Field Services

Michael ColeExecutive Vice-President and

Chief Information Officer

J. Trevor AndersonExecutive Vice-President –

Network

Martine TurcotteExecutive Vice-President and

Chief Legal & Regulatory Officer

Siim A. VanaseljaExecutive Vice-President and

Chief Financial Officer

David WellsExecutive Vice-President –

Corporate Services

Stéphane BoisvertPresident – Enterprise

Charles BrownPresident – Small & Medium

Business and Bell West

Kevin W. CrullPresident –

Residential Services

Wade OostermanPresident – Bell Mobility and

Channels, and Chief Brand Officer

John SweeneyPresident – Wholesale

Service delivery People & support Market facing

George CopePresident and

Chief Executive Officer

Strategic imperative 1 :Achieve a competitivecost structure

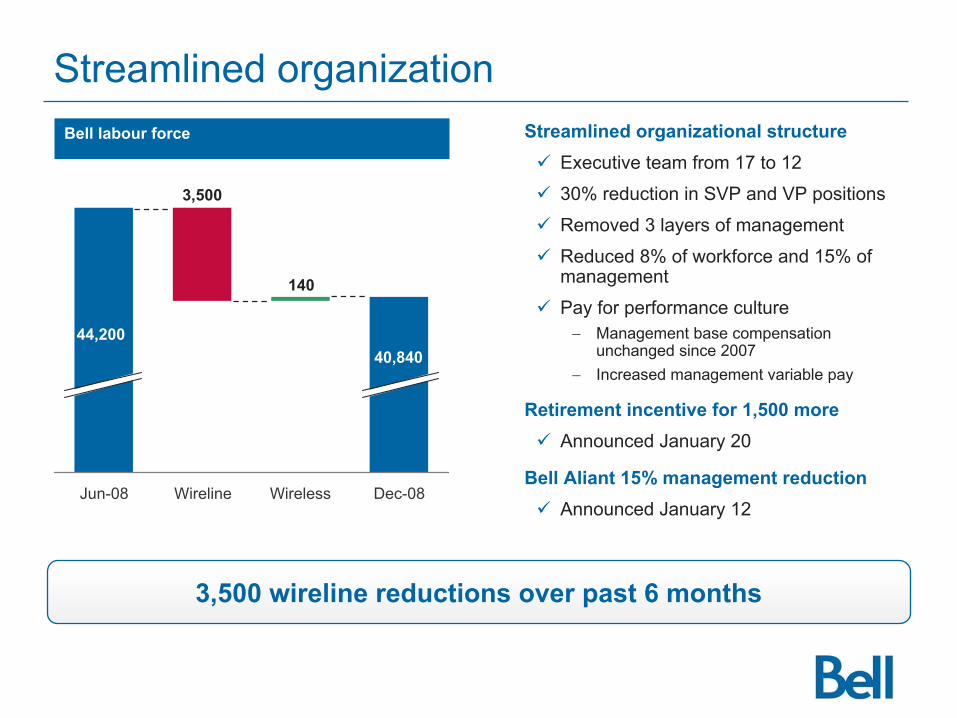

Jun-08 Wireline Wireless Dec-08

Streamlined organizationStreamlined organizational structure

Executive team from 17 to 12

30% reduction in SVP and VP positions

Removed 3 layers of management

Reduced 8% of workforce and 15% of management

Pay for performance culture− Management base compensation

unchanged since 2007− Increased management variable pay

Retirement incentive for 1,500 moreAnnounced January 20

Bell Aliant 15% management reductionAnnounced January 12

44,20040,840

3,500 wireline reductions over past 6 months

Bell labour force

3,500

140

2008 2009

Further cost reductionsLowering costs of wireline services

• Field force productivity− Drive performance culture− Increase jobs/day

• Renegotiate contracts with key IT vendors

Driving down other support costs• Outsourcing and offshoring

− Non-customer affecting− Call center/IT/back office

• Real estate consolidation− 10,000 employees at 3 campuses− Moved out of 40 locations in past two years

• Reducing discretionary spend− Consulting expense down dramatically− 47 ad agencies to 11− Eliminated ~7,000 credit cards

Multi-year plan will continue to take costs out

Wireline service delivery costs

-15%

2.7

2.3

OPEX and CAPEX for Wireline Field Services, IT and Network ($B)

Disciplined capital management

Investing in strategic priorities

Bell capital expenditures(1)

2,459

16.5%

2008 2009E

Capital expenditures ($M)Capital intensity

15% - 16%

(1) Excludes AWS spectrum licences

Tighter capital management

• Rigorous new capital governance− Single company priorities list− Common investment criteria

• Aggressive buying

• Tighter network provisioning intervals

• Leverage common IT platforms

Accelerating investment

• 80% focused on our 5 strategic imperatives, including:− HSPA roll out− FTTN acceleration

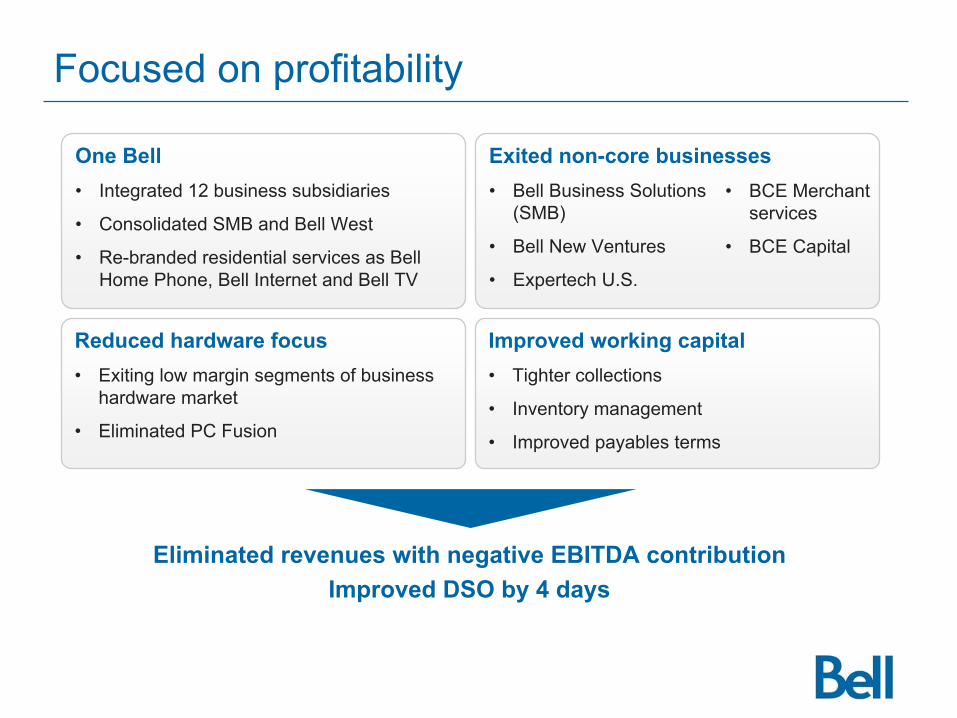

Focused on profitability

Eliminated revenues with negative EBITDA contributionImproved DSO by 4 days

One Bell• Integrated 12 business subsidiaries

• Consolidated SMB and Bell West

• Re-branded residential services as Bell Home Phone, Bell Internet and Bell TV

Exited non-core businesses• Bell Business Solutions

(SMB)

• Bell New Ventures

• Expertech U.S.

Reduced hardware focus• Exiting low margin segments of business

hardware market

• Eliminated PC Fusion

Improved working capital• Tighter collections

• Inventory management

• Improved payables terms

• BCE Merchant services

• BCE Capital

Strategic imperative 2 :Accelerate wireless

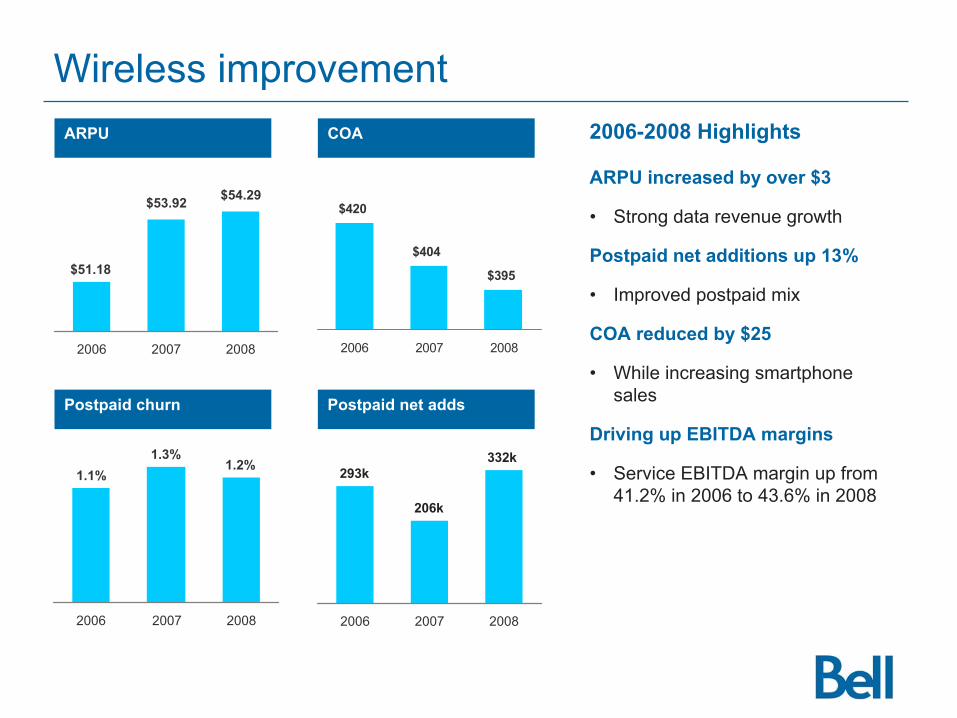

Wireless improvement2006-2008 Highlights

ARPU increased by over $3

• Strong data revenue growth

Postpaid net additions up 13%

• Improved postpaid mix

COA reduced by $25

• While increasing smartphone sales

Driving up EBITDA margins

• Service EBITDA margin up from 41.2% in 2006 to 43.6% in 2008

ARPU COA

Postpaid churn

$51.18

$53.92 $54.29

2006 2007 2008

$420

$404

$395

2006 2007 2008

1.1%1.3%

1.2%

2006 2007 2008

Postpaid net adds

2006 2007 2008

293k

206k

332k

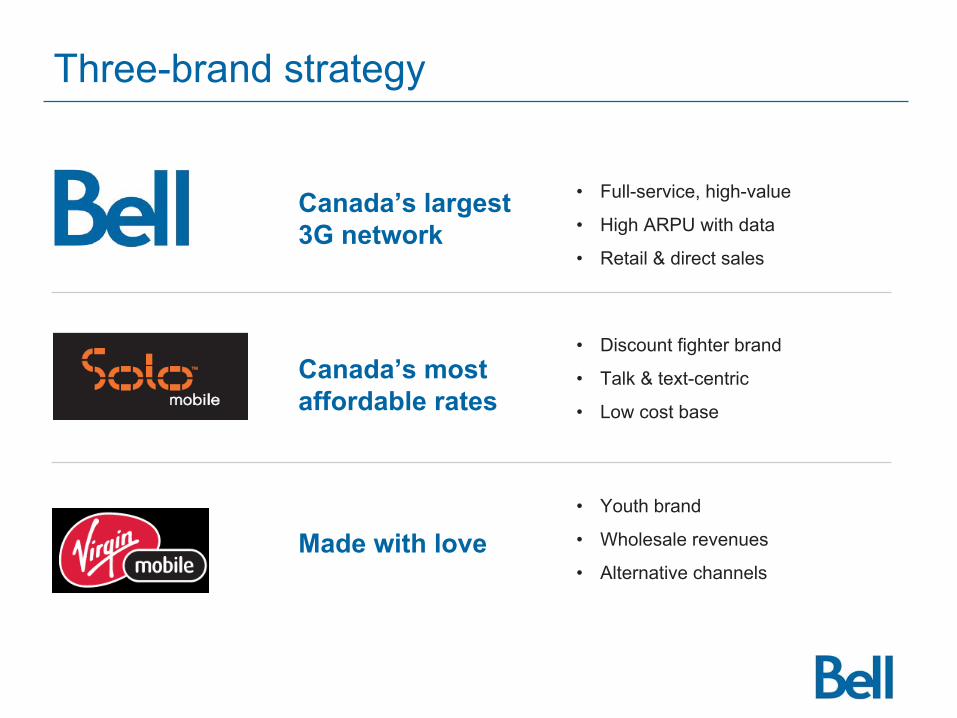

Three-brand strategy

• Full-service, high-value

• High ARPU with data

• Retail & direct sales

Canada’s largest 3G network

• Discount fighter brand

• Talk & text-centric

• Low cost base

Canada’s most affordable rates

• Youth brand

• Wholesale revenues

• Alternative channelsMade with love

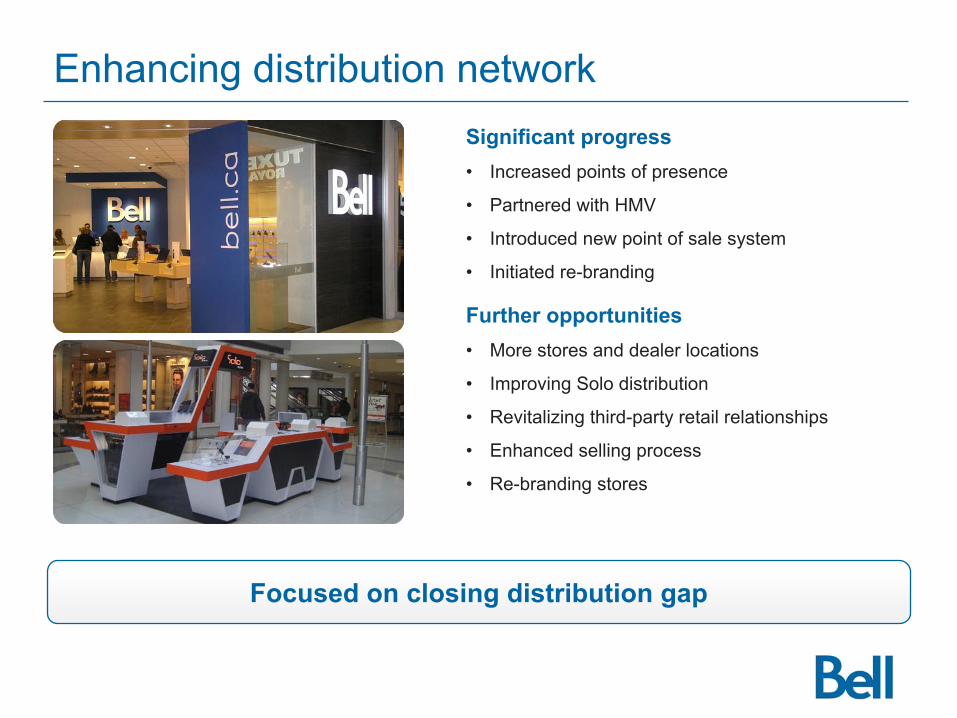

Enhancing distribution networkSignificant progress• Increased points of presence

• Partnered with HMV

• Introduced new point of sale system

• Initiated re-branding

Further opportunities • More stores and dealer locations

• Improving Solo distribution

• Revitalizing third-party retail relationships

• Enhanced selling process

• Re-branding stores

Focused on closing distribution gap

Significant improvement in data ARPU

Growing wireless dataIncreasing mix of smartphones• RIM World Edition (CDMA/GSM)

• Over 50% of handsets

More music, entertainment and data applications• Exclusive NHL content

Wireless data revenues

Data revenue growthData % of ARPU

31%46%

54%

10%

13%15%

0%

10%

20%

30%

40%

50%

60%

2007 2008 Q4080%

5%

10%

15%

HSPA rollout

Customer benefits

Financial benefits

• Global standard

• Path to next generation data services

• More choice in handsets

• Improved rural coverage

• International roaming

• Bell/Telus agreement lowers capital requirement

• Network operating cost savings

• Lower handset costs

• New entrant roaming revenues

• Faster time to market and greater coverage

Launching by early 2010

2009 priorities

Broadband network

• Enhanced distribution

• Leverage new brandDistribution and brand

• Fighter brand management

• Prepare for new entrants

• Cost management

Competition

• HSPA network

• Continue to close data ARPU gap

Strategic imperative 3 :Leverage wireline momentum

Slowing NAS losses

Maintain momentum in 2009

Lower NAS losses

580423

6.9%

5.4%

2007 2008

Net NAS losses (thousands)Y/Y erosion rate

2009

Year-over-year improvement• Only major North American carrier with

slowing rate of decline

Residential• Increase multi-product households

• Accelerate winbacks

• Fewer households moving

Business• Focus on retaining small businesses

• Shift to IP PBX

• Managing through economic downturn

2008 2012E

Improving Internet experienceInternet growth slowed in 2008

• Net additions 50k

Focus on improving product and service performance

• Continue to harden and groom network

• Introduce Full Installs

FTTN delivering solid results

• Coverage in GTA/GMA nearly complete– Customer satisfaction 50% higher – Churn is 25% lower– ARPU is higher

Continuing to monetize traffic growth

• Maintaining usage caps

2.4M

5.0M

FTTN homes passed

Healthy video business

Leveraging triple-play

Bell TV ARPU

$53.85

$65.37$59.69

2006 2007 2008

Most HD channels in CanadaMaintaining HD leadership• Increased HD and PVR

penetration− HD set-top box penetration up

10 percentage points − PVR penetration over 25%

• Successful launch of Nimiq 4

Increasing MDU footprint• Passed ~1,700 MDUs in 2008

• Targeting ~700 more in 2009

Strong EBITDA growth• Programming and pricing

drive ARPU

• Driving down set-top box costs

• Improved distribution

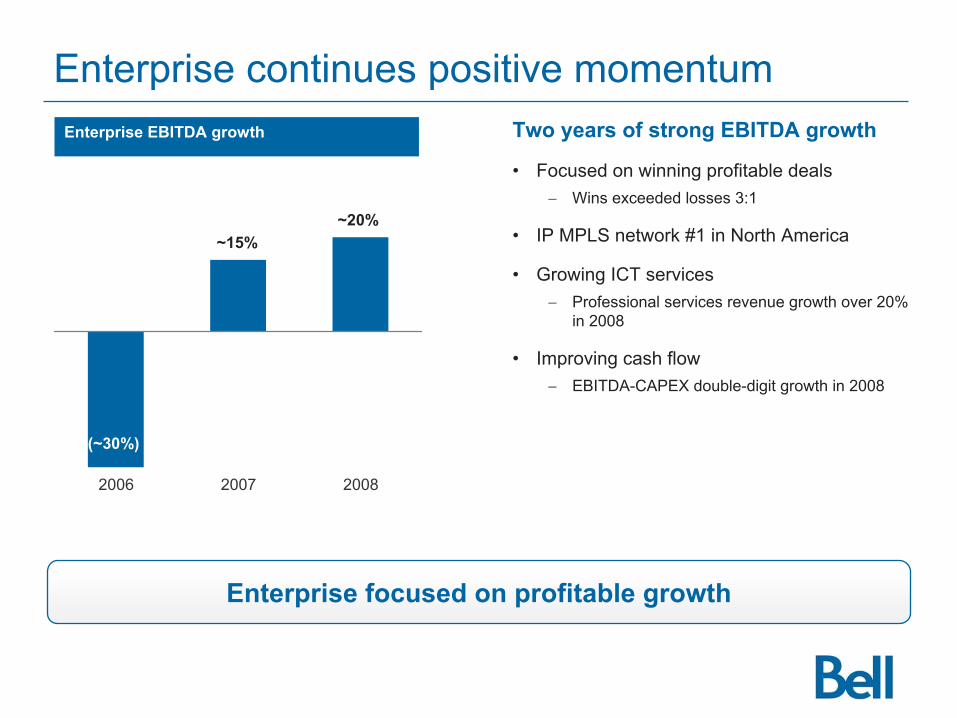

Enterprise continues positive momentum

Enterprise focused on profitable growth

Enterprise EBITDA growth

2006 2007 2008

(~30%)

~15%~20%

Two years of strong EBITDA growth

• Focused on winning profitable deals− Wins exceeded losses 3:1

• IP MPLS network #1 in North America

• Growing ICT services− Professional services revenue growth over 20%

in 2008

• Improving cash flow− EBITDA-CAPEX double-digit growth in 2008

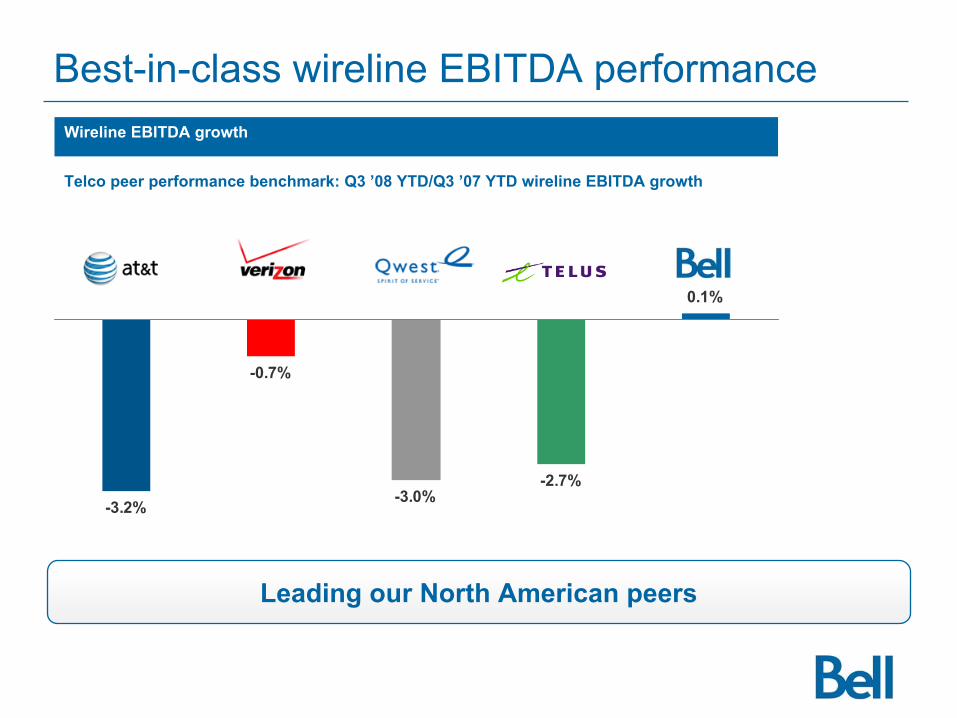

-3.2%

-0.7%

-3.0%-2.7%

0.1%

Best-in-class wireline EBITDA performanceWireline EBITDA growth

Telco peer performance benchmark: Q3 ’08 YTD/Q3 ’07 YTD wireline EBITDA growth

Leading our North American peers

Strategic imperative 4 :Invest in broadbandnetwork & services

Building platforms for the future

Rolling out HSPAReady by early 2010

• Accelerated time to market

• Joint build reduces capital requirement

• Global standard and path to next generation data services

Investing in FTTNAccelerating FTTN deployment

• Advanced by one year

• ~$700M cumulative investment over next 3 years

• 175 condos set up for fibre

Leveraging best-in-class IP coreInvestments in core made Bell #1 IP MPLS network in North America

• Reduced outages for Enterprise customers

Strategic imperative 5 :Improve customerservice

New levels of service

Same Day/Next Day

• Faster repair on Bell Home Phone, Bell Internet and Bell TV

Express Install

• Premium service that offers customers next-day installation of Bell Home Phone, Bell Internet and Bell TV

Internet Full Install

• Bell Internet installation now includes – Modem delivery and installation– Speed and performance optimization– Email set-up and account registration

Call Centres

• Moved key service desks on-shore

• Raised level of quality with vendors– From cost/call to pay for performance

Field Services

• Purchased ~2,000 new trucks

Service enhancements Support investments

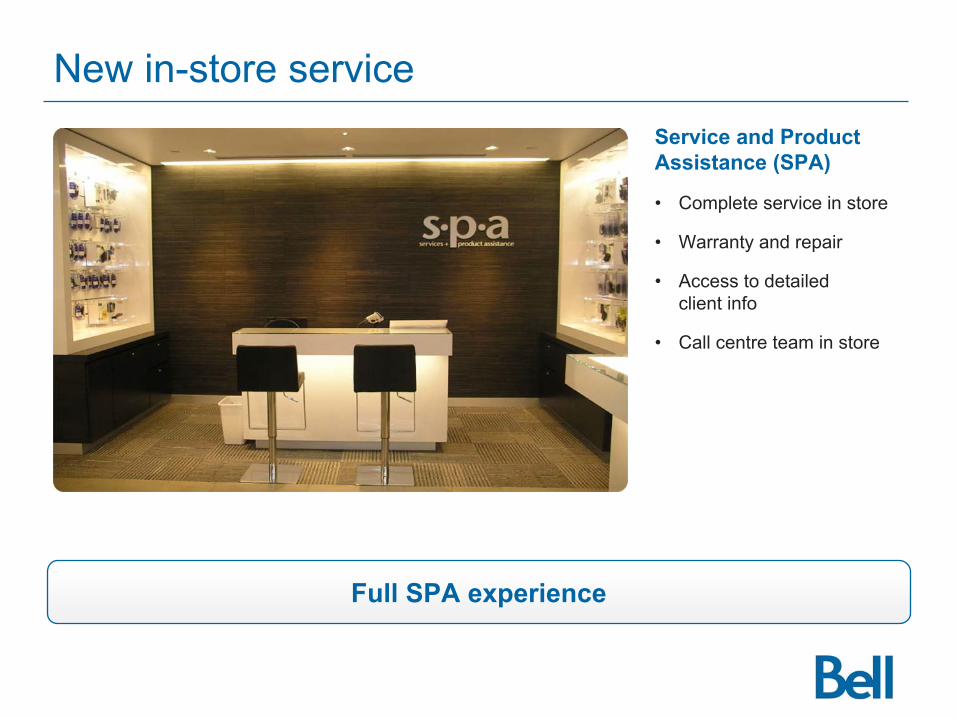

Full SPA experience

New in-store serviceService and ProductAssistance (SPA)

• Complete service in store

• Warranty and repair

• Access to detailed client info

• Call centre team in store

New brandFour new brand elements

1. New logo

2. New tag lines in French and English

3. New look

4. Theme of “on Bell”

Aligned business unit names

Sympatico

ExpressVu

Residential

Mobile

Successful and effective new brand

Bell Internet

Bell TV

Bell Home Phone

Bell Mobility

What changed at Bell since July ’08?

New organizational structure

Removed 3 layers of management

Reduced Wireline workforce by 3,500

Renegotiated IT contracts

Campus consolidation

New capital governance process

Exited non-core businesses

Announced new HSPA wireless network build

Launched a new satellite for HD capacity

Announced fibre to the building for MDUs

Awarded #1 IP MPLS network ranking in North America

Rolled out new service initiatives • Same Day/Next Day• Express Install• Full Install

Changing the culture to “One Bell” and pay for performance

Launched a new brand – received best new brand award in Quebec market

Focus on cost…… balanced with investments

in strategic priorities

Driving shareholder value through dividend growth

Value for investors

• Focus on core business drives free cash flow growth

• Supported by strong balance sheet and capital structure

– Conservative approach to liquidity given market environment

• Clear dividend policy

Increased dividend