10 common gaps in business insurance mark w. cote, aai commercial insurance producer, brown &...

TRANSCRIPT

10 Common Gaps in Business Insurance

Mark W. Cote, AAICommercial Insurance Producer, Brown & Brown Insurance

Overview

• About Brown & Brown

• The Reason To Buy Business Insurance

• Most Common Coverage Gaps/Errors – Vulnerabilities and Deficiencies in the policies

• The Typical Process

• A Better Process To Identify Ticking Time Bombs

Brown & Brown Insurance

Brown & Brown, Inc. is recognized as one of the largest and most respected independent insurance intermediaries in the nation. With over 75 years of continuous service, Brown & Brown is ranked the sixth largest insurance intermediary in the world by U.S. business by Business Insurance magazine as of July, 2012. Brown & Brown’s reach includes over 38 states and offers insurance programs and services through their 200+ Retail, Brokerage, National Programs and Services offices throughout the country.

Reasons To Buy Insurance

1. To Protect Your Balance Sheet If/When A Catastrophe Strikes

2. Required By Law to Carry Work Comp

3. You Can’t Always Rely On Other People’s Insurance

4. You can’t predict the future!

10 Most Common Gaps

1. Employment Practices Liability

2. Cyber Liability

3. Employee Benefits Liability

4. Notice & Knowledge

5. Temporary and Leased Workers

6. Business Income aka Business Interruption

7. Errors & Omissions

8. Ordinance or Law

9. Blanket Limits

10. Mental Anguish

1. Employment Practices Liability Insurance (EPLI)

• Wrongful Termination

• Discrimination

• Sexual Harassment

• Retaliation

• Wage & Hour Claims

• Whistle Blower Claims

EPLI Continued

• 3 out of 5 firms will be sued by an employee

• The median compensatory award to plaintiffs is $325,000

• Wage and hour litigation has quadrupled

• Over 40% of EPL claims are against firms with fewer than 100 employees

Typical EPLI Exclusion

EPLI Claim Examples

• Wage & Hour: A mortgage company was sued by 54 of its loan officers for over $220,000 in unpaid overtime. The owner was under the impression that FLSA did not apply to highly compensated employees. Many of his staff members earned well over 150k per year with the average compensation being $105,000. There is an exception to the FLSA law for highly compensated individuals earning at $100,000 per year or more but the exception also stipulates that a minimum of $455 per week must be paid. These employees were not paid during weeks where they did not close loans.

• Pregnancy Discrimination: A motel was forced to layoff ten employees due to tough economic conditions. The motel claimed they were unaware that one of the affected employees was pregnant. The claimant sued the motel for $50,000, contending that she was targeted due to her pregnancy. The case settled in mediation for $42,000 plus defense costs.

• Third Party Liability: A blind customer entered a local grocery store with his guide dog. The manager of the meat/deli department asked the customer to take his dog outside because he thought the dog presented a health hazard. The customer sued for violation of the Americans with Disabilities Act.

2. Cyber Liability

“According to a recent survey conducted by Hanover Research and sponsored by ISO, 40% of companies don’t think they need cyber coverage and 29% believe they’re already covered under existing policies.They’re wrong.” Independent Agent Magazine, January 19, 2015

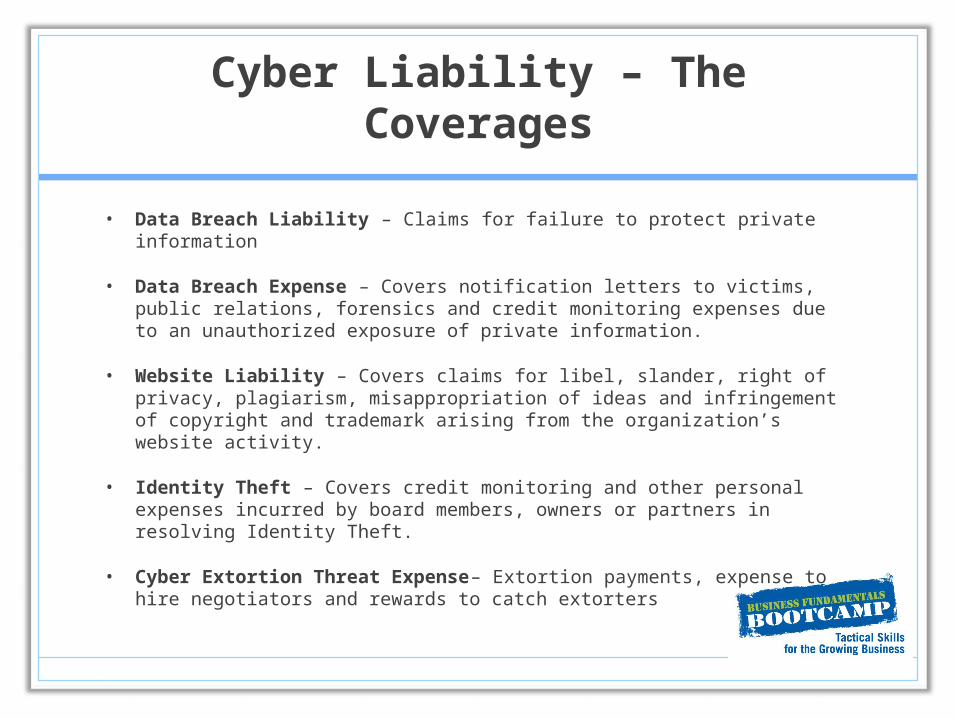

Cyber Liability – The Coverages

• Data Breach Liability – Claims for failure to protect private information

• Data Breach Expense – Covers notification letters to victims, public relations, forensics and credit monitoring expenses due to an unauthorized exposure of private information.

• Website Liability – Covers claims for libel, slander, right of privacy, plagiarism, misappropriation of ideas and infringement of copyright and trademark arising from the organization’s website activity.

• Identity Theft – Covers credit monitoring and other personal expenses incurred by board members, owners or partners in resolving Identity Theft.

• Cyber Extortion Threat Expense– Extortion payments, expense to hire negotiators and rewards to catch extorters

Cyber Liability Claim Examples

**Premiums are fairly low for a good Cyber Policy

3. Employee Benefits Liability (EBL)

• EBL is coverage that is used to insure against negligent acts, errors, or omissions committed by an insured or any person whose acts the insured is legally responsible for while engaging in the administration of their company’s employee benefits plans.

• The term “employee benefits programs” is defined to include (but not limited to) group life insurance and group accident and/or health insurance, profit sharing plans, employee stock subscription plans, worker’s compensation, unemployment insurance, social security benefits, and disability benefits.

Employee Benefits Liability Claim Example

Suppose your company owns several apartment buildings. Bob, a new maintenance employee, completes paperwork to enroll in the company-sponsored health plan. Due to a clerical error by a human resources employee Bob is not enrolled.

Several months later Bob is hospitalized with a serious illness and he discovers he has no health insurance. When his medical bills begin to pile up Bob seeks restitution by suing the HR worker and your firm.

Claims like Bob’s are not covered under commercial general liability policies because an administrative error is not an “occurrence” as that term is usually defined.

To insure itself against such claims your firm can purchase employee benefits liability (EBL) coverage.

EBL Sample Endorsement

4. Notice & Knowledge of Occurrence

• The Notice & Knowledge Condition can be problematic if not fixed

• Unenhanced GL Policy Condition: You (the insured) must see to it that we are notified as soon as practicable of an occurrence or an offense which may result in a claim or suit (to the carrier).

Notice & Knowledge of Occurrence Continued

Unfavorable Wording: Favorable Wording:

**The gap may not be obvious but the problem lies in the definition of the word “you”.

5. Temporary & Leased Workers

• The general liability policy typically has an extension that amends the definition of “employee” to include a leased worker or a temporary worker.

• The Issue Is: “Employee” is excluded coverage under the general liability policy so this amendment broadens the exclusion to include a leased worker or a temporary worker.

Temporary & Leased Workers Cont.

• Solution 1 – Require the staffing agency to add the Alternate Employer Endorsement scheduling your company as the Alternate Employer

• Solution 2 - Add Endorsement CG 04 24 to your General Liability policy. This changes the definition of the term “employee”

The Gap here is not always obvious and you need a broker that can uncover this for you!

If a worker is injured in the course of his or her work for a CGL-insured employer and sues If a worker is injured in the course of his or her work for a CGL-insured employer and sues that employer for BI, the employer’s CGL insurer that employer for BI, the employer’s CGL insurer will not defend the employer will not defend the employer or pay any or pay any

damages that result from the suit.- IRMIdamages that result from the suit.- IRMI

6. Business Income aka Business Interruption

Business interruption insurance is intended to compensate the insured for the income lost during the period of restoration or the time necessary to repair or restore the physical damage to the covered property.

This includes continuing expenses such as taxes, insurance, utilities, payroll for key employees, mortgage obligations, etc.

The issues we find are:•No Business Income included in the policy!•Absence of agreed value endorsement•Incorrect Limit(s)•No Extra Expense Coverage built in•72 Hours vs. 24 Hours Time Element Deductible

Business Income Claim Examples

• Software Developer -A developer of tax accounting software suffered a fire loss to its facility, which forced a halt to production and an interruption of the shipment of its products. As the fire occurred right before tax season, the developer incurred a business income loss of $500,000.

• Manufacturer - A critical piece of equipment at a tool and die manufacturer suffered a machinery breakdown. The manufacturer needed to order a new part and had to wait two months for it arrive from Germany. The manufacturer suffered a $3 million business income loss, since it wasn’t able to complete the manufacturing of its products and get them to market.

7. Errors & Omissions (E&O)

What is E&O? - Errors and Omissions is a type of insurance designed to cover providers of technology services or products. For example, data storage companies and website designers provide technology services, while computer software and computer manufacturers offer technology products.

•Tech E&O policies cover both liability and property loss exposures

•Tech E&O insurance is often confused with cyber and privacy insurance. In contrast to tech E&O coverage, cyber and privacy insurance is intended to protect consumers of technology products and services.

E&O Claim Examples

E&O Claim Examples

8. Ordinance or Law

The Ordinance or law coverage endorsement is used to add coverage for the direct damage portion of this loss exposure created by local building ordinances. Often times, local ordinances require

any building damaged to a certain extent to be demolished and rebuilt to current building codes (usually 50% damage).

Ordinance or Law Claim Example

Example: You have a fire rip through your building. You find out that due to zoning and land use ordinances, you are prohibited from rebuilding a similar structure on the site. You must either rebuild somewhere else or rebuild under a completely new building design. The exclusion in the typical property policy eliminates any additional costs imposed on you as a result of such requirements.

But… This could have been added to your policy!

9. Blanket Limits

• Blanket insurance combines a number of separate property coverage’s and/or 2 or more locations under a single combined limit of insurance.

• Blanket coverage should be used when an insured has a number of buildings or a number of locations where the business personal property values fluctuate or move between the locations, etc.

Blanket Limits Cont.

Solution: Create a statement of values after analyzing the operations and exposures. In the scenario above, the insured could have avoided that issue by having a blanket limit of $1,000,000.

10. Mental Anguish

Mental and emotional issues are generally referred to in personal injury litigation as “pain and suffering”.

Problem: The definition of Bodily Injury in the General Liability Policy, Auto Policy and Umbrella policy typically does not include Mental Anguish.

Mental Anguish Claim Example

Mental Anguish

Sample Definition from a General Liability Policy

Example of an Endorsement with the preferred wording

Why Do We Have These Gaps???

• Who reviews these policies?

• Who reviews the company exposures?

• Do you ever get quotes for additional coverages?

• Is anyone doing a thorough policy analysis?

Rundown Of The Typical Process

• Broker asks you for limits needed

• Broker asks you for Sales and Payroll information

• Applications are filled out

• 2 days before renewal broker brings out proposal

• You may see a Coverage Comparison along with your Proposal, but what have they done for you??

Coverage Comparison

Renewal Proposal Sample

Proposal Section Cont.

The Binder That Collects Dust

Things to consider

Things to consider

• Gaps and errors can be buried deep in these policies

• Did anyone read the policies???

• An Uncovered Claim can bankrupt a business

• What is the process to uncover these issues?

The Brown & Brown Process

Proprietary Analysis - Brown & Brown’s process centers on a proprietary policy analysis that examines each line of coverage individually to provide a holistic indication of the overall insurance program’s effectiveness.

Finished Product = A Better Built Policy That Will Cover You When You Need It!

ANY FINAL QUESTIONS?

43

Remember to Complete the Speaker Survey:sm15.bfbootcamp.net / ‘click’ on speakers / select

your speaker

Mark W. Cote, AAICommercial Insurance Producer, Brown &

Brown [email protected]

www.bbnhins.com