1 q09 results presentation

TRANSCRIPT

2

Disclaimer

This presentation may include forward-looking statements about future events or results according

to the regulations of Brazilian and international securities and exchange commissions. These

statements are based on certain assumptions and analyses by the Company that reflect its

experience, the economic environment, future market conditions and events expected by it, many

of which are beyond its control. Important factors that may lead to significant differences between

actual results and the statements of expectations about future events or results include the

company’s business strategy, economic conditions in Brazil and abroad, technology, financial

strategy, client business development, financial market conditions, uncertainty regarding the

results of its future operations, plans, objectives, expectations and intentions, among others. As a

result of these factors, the actual results of the Company may significantly differ from those

mentioned or implicit in the statement of expectations about future events or results.

The information and opinions contained in this presentation should not be understood as a

recommendation to potential investors and no investment decision should be based on the veracity,

currency or completeness of this information or these opinions. No advisors to the company or

parties related to them or their representatives will be responsible for any losses that may result

from the use or the contents of this presentation.

3

Cards Market and CardSystem

Base growth was greater than market

growth;

The unit has the most modern and

complete processing structure in Brazil;

Study of the card market carried out by

the Brazilian Central Bank suggests

creation of a specific regulation for the

segment and opening up of issuers.

Private Label + Credit Market CardSystem

Average Annual Growth - 3 years 20.9% 26.0%

2008 Growth - 12 months 16.0% 18.1%

Source: ABECS, CSU

89 102 124 153 17756 70

87109

127

2005 2006 2007 2008 2009

Growth of the Cards Market

Private Label Credit

(million, end of March, source: ABECS)

8.6 10.4 13.017.6

20.8

2005 2006 2007 2008 2009

CSU Card Base Performance(million, end of March)

4

CardSystem – Operational Data

1Q09 was the best quarter in CSU’s history in terms of card issue;

6 million new cards issued in the last 12 months;

Issue of new cards will grow each year.

Source: CSU

1.1 1.4

1.7 1.6 1.3

1Q08 2Q08 3Q08 4Q08 1Q09

Issue of cards in CSU's base (million, quarter issue)

5

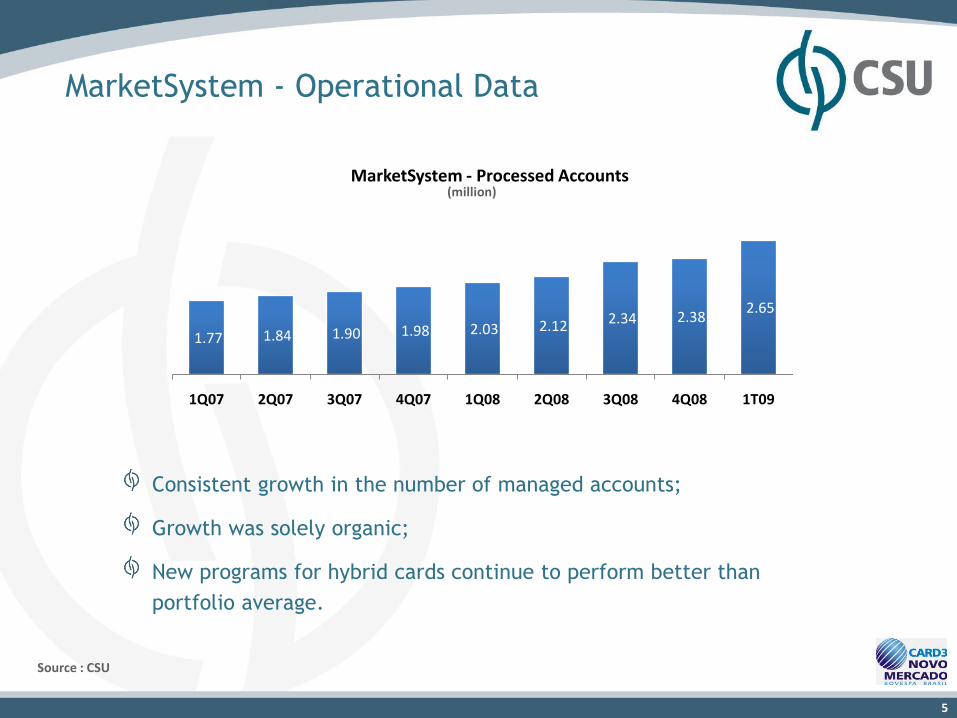

MarketSystem - Operational Data

Consistent growth in the number of managed accounts;

Growth was solely organic;

New programs for hybrid cards continue to perform better than

portfolio average.

Source : CSU

1.77 1.84 1.90 1.98 2.03 2.12 2.34 2.38 2.65

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1T09

MarketSystem - Processed Accounts(million)

6

TeleSystem / Credit&Risk

Decree 6,523 led companies contracting call center

services to expand the scope of their agreements,

consequently increasing the demand for these

services;

Expansion of workstations;

Transfer of Credit&Risk’s workstations to TeleSystem

to meet the demand for specific operations.

758 776 748 619 435 282 305

3,114 2,546 2,218

3,476 3,445 3,314 3,288

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

PAs in operation at TeleSystem and Credit&Risk

PA's Credit&Risk PA's TeleSystem

3,872 3,596

3,880 4,095

2,966 3,322 3,593

7

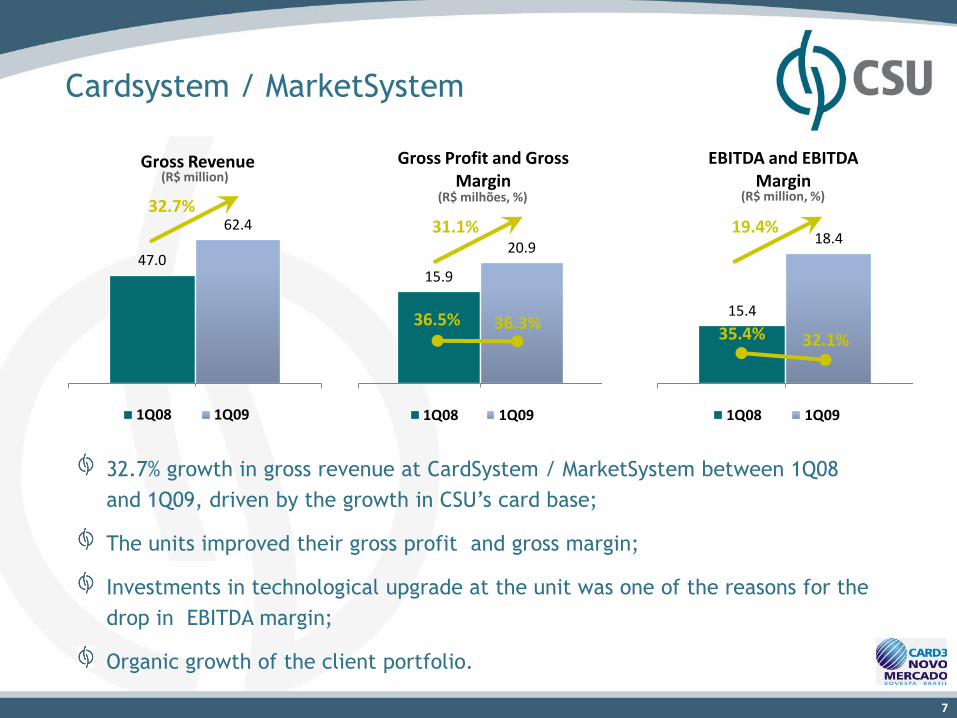

15.4

18.4

EBITDA and EBITDA Margin

1Q08 1Q09

15.9

20.9

Gross Profit and Gross Margin

1Q08 1Q09

Cardsystem / MarketSystem

36.3%36.5%

32.7% growth in gross revenue at CardSystem / MarketSystem between 1Q08

and 1Q09, driven by the growth in CSU’s card base;

The units improved their gross profit and gross margin;

Investments in technological upgrade at the unit was one of the reasons for the

drop in EBITDA margin;

Organic growth of the client portfolio.

31.1% 19.4%

32.1%35.4%

(R$ milhões, %) (R$ million, %)

47.0

62.4

Gross Revenue

1Q08 1Q09

32.7%

(R$ million)

8

(0.4)

2.0

EBITDA

1Q08 1Q09

41.2

44.9

Gross Revenue

1Q08 1Q09

TeleSystem / Credit&Risk

The new operational setup at the call centers in Recife has optimized

operations, improved service quality and reduced costs;

The company plans to extend this structure to workstations at other sites

in 2009, to continue the improvement in the units’ profitability

indicators.

9.0%

(R$ million)(R$ million) (R$ million)

(0.6)

2.9

Gross Profit

1Q08 1Q09

9

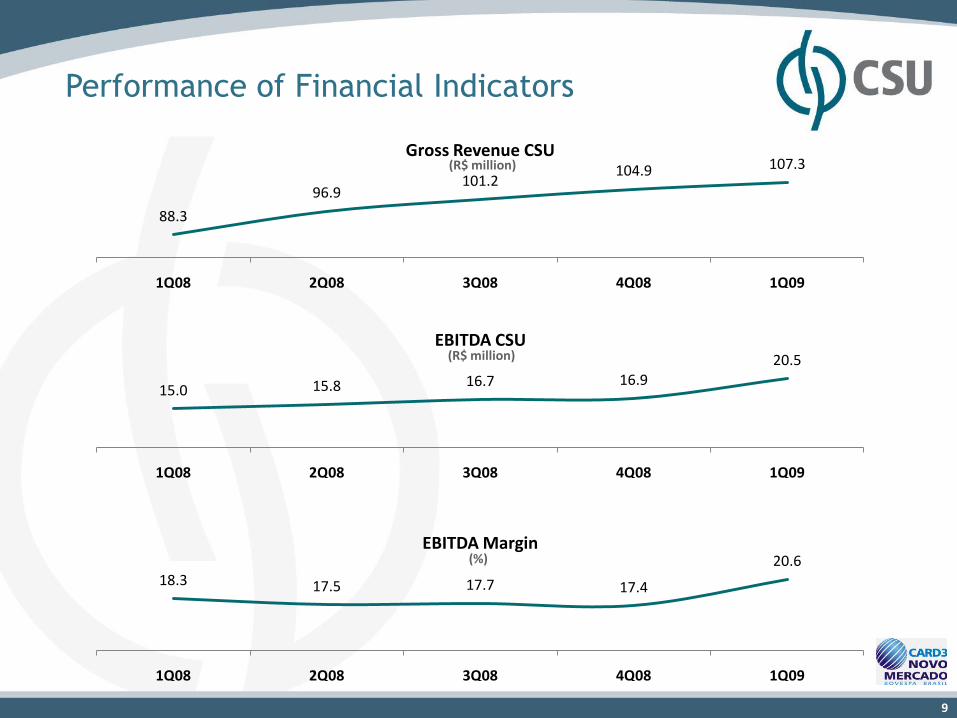

Performance of Financial Indicators

88.3

96.9101.2

104.9 107.3

1Q08 2Q08 3Q08 4Q08 1Q09

Gross Revenue CSU

15.0 15.8 16.7 16.920.5

1Q08 2Q08 3Q08 4Q08 1Q09

EBITDA CSU

18.3 17.5 17.7 17.4

20.6

1Q08 2Q08 3Q08 4Q08 1Q09

EBITDA Margin

(R$ million)

(R$ million)

(%)

10

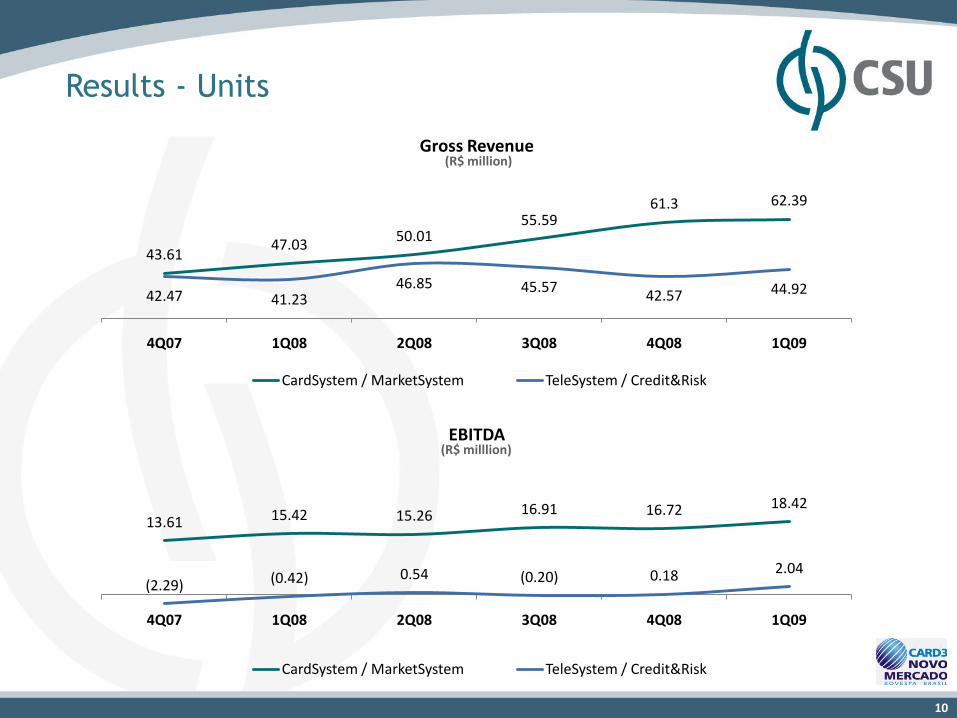

13.61 15.42 15.26 16.91 16.72 18.42

(2.29) (0.42) 0.54 (0.20) 0.18 2.04

4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

EBITDA

CardSystem / MarketSystem TeleSystem / Credit&Risk

43.6147.03

50.0155.59

61.3 62.39

42.47 41.2346.85 45.57

42.57 44.92

4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

Gross Revenue

CardSystem / MarketSystem TeleSystem / Credit&Risk

Results - Units

(R$ million)

(R$ milllion)

11

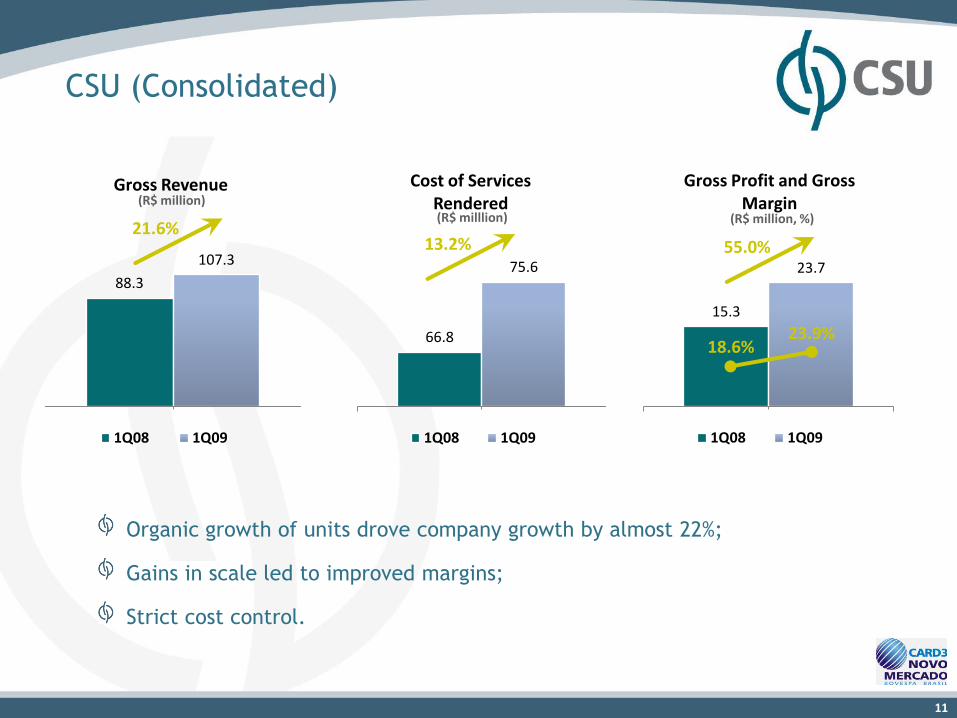

15.3

23.7

Gross Profit and Gross Margin

1Q08 1Q09

66.8

75.6

Cost of Services Rendered

1Q08 1Q09

88.3

107.3

Gross Revenue

1Q08 1Q09

CSU (Consolidated)

Organic growth of units drove company growth by almost 22%;

Gains in scale led to improved margins;

Strict cost control.

21.6%

23.9%18.6%

13.2% 55.0%

(R$ million)

(R$ million, %)(R$ milllion)

12

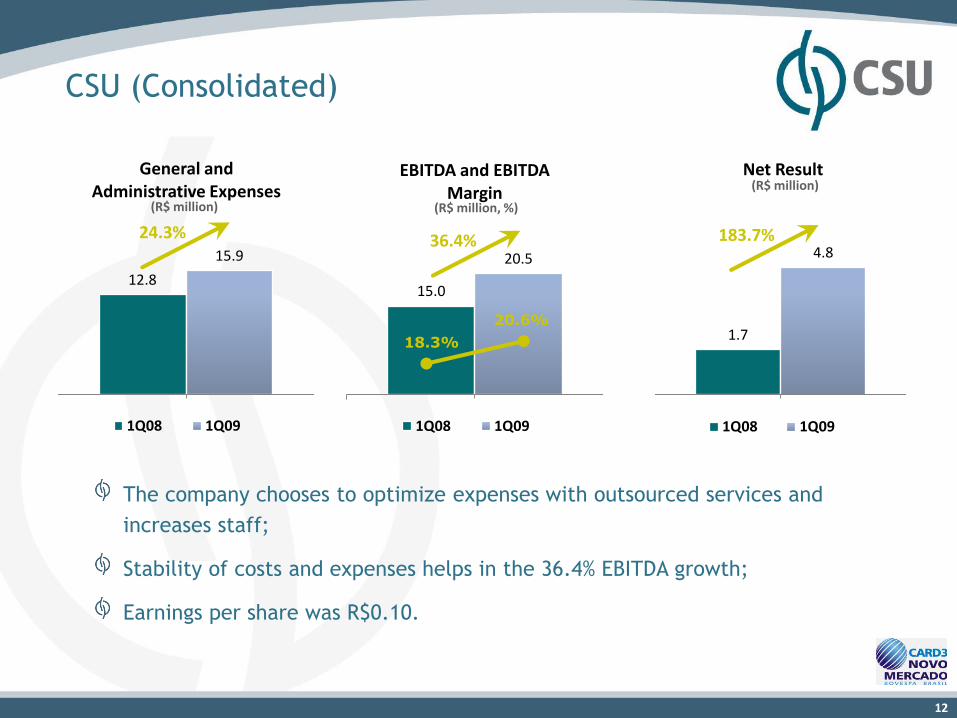

1.7

4.8

Net Result

1Q08 1Q09

15.0

20.5

EBITDA and EBITDA Margin

1Q08 1Q09

12.8

15.9

General and Administrative Expenses

1Q08 1Q09

CSU (Consolidated)

20.6%

18.3%

The company chooses to optimize expenses with outsourced services and

increases staff;

Stability of costs and expenses helps in the 36.4% EBITDA growth;

Earnings per share was R$0.10.

24.3% 183.7%36.4%

(R$ million) (R$ million, %)

(R$ million)

13

63.2 68.5 70.8 60.3

10.7 4.8 4.0 4.6

26.3 22.7 17.9 22.8

0.5 0.3 0.1 -

2Q08 3Q08 4Q08 1Q09

Debt Composition

W. Capital Overdraft Leasing BNDES

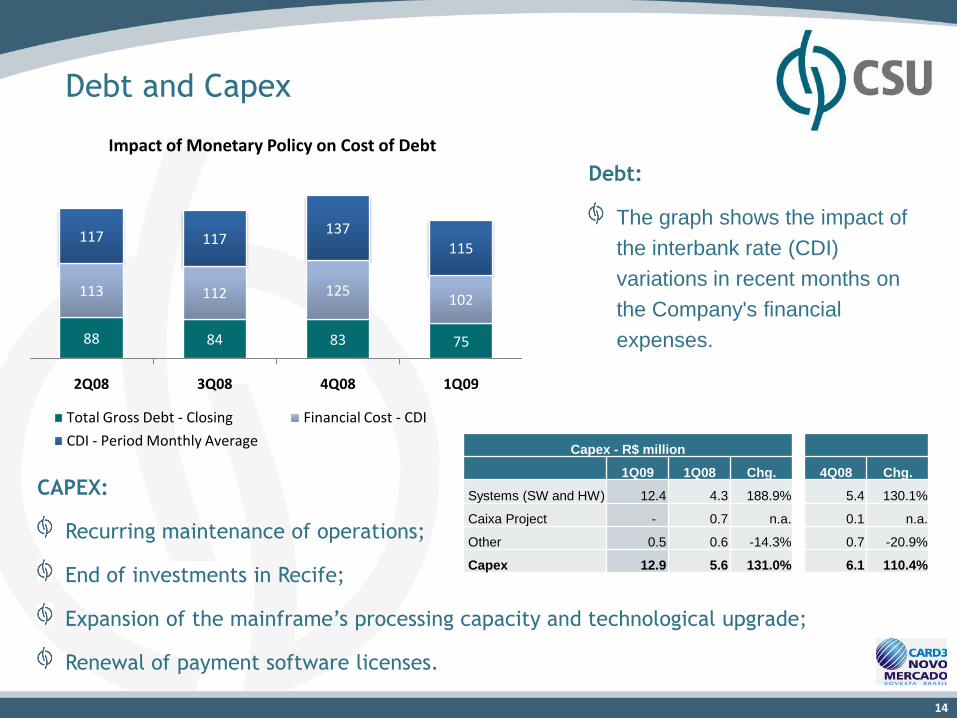

Debt and Capex

Debt - R$ million

1Q09 1Q08 4Q08

Short Term Debt 58.0 55.8 62.5

Financing and Debt loan 47.4 33.3 49.7

Leasing 10.7 22.5 12.8

Long Term Debt 29.7 58.6 34.0

Financing and Debt loan 17.9 49.0 25.4

Leasing 11.8 9.7 8.6

Gross Debt 87.7 114.3 96.5

(-) Cash 1.5 1.8 1.6

Net Cash (Debt) 86.3 112.5 94.9

Debt:

Cash generated in three months enabled

the company to reduce net debt from R$

94.9 million to R$ 86.3 million;

The company sought to reduce financial

expenses by paying off debt installments

on maturity;

CSU neither has loans indexed to the US

dollar nor derivatives contracts. Its debt

is in Brazilian reais and indexed to the

interbank (CDI) rate.

(R$ million, end of the period)

14

CAPEX:

Recurring maintenance of operations;

End of investments in Recife;

Expansion of the mainframe’s processing capacity and technological upgrade;

Renewal of payment software licenses.

Debt and Capex

Debt:

The graph shows the impact of

the interbank rate (CDI)

variations in recent months on

the Company's financial

expenses.

Capex - R$ million

1Q09 1Q08 Chg. 4Q08 Chg.

Systems (SW and HW) 12.4 4.3 188.9% 5.4 130.1%

Caixa Project - 0.7 n.a. 0.1 n.a.

Other 0.5 0.6 -14.3% 0.7 -20.9%

Capex 12.9 5.6 131.0% 6.1 110.4%

88 84 83 75

113 112 125102

117 117137

115

2Q08 3Q08 4Q08 1Q09

Impact of Monetary Policy on Cost of Debt

Total Gross Debt - Closing Financial Cost - CDI

CDI - Period Monthly Average

15

Social Responsibility and Sustainability

CSU Institute

Provides job-oriented training

CSU carries out the following Socio-Environmental Responsibility projects:

Environmental Responsibility

Selective waste collection for the recycling project, whose sale proceeds

are donated to the CSU institute

Centro Crescer Sorrindo (Grow-up Smiling Center)

Crèche in Belo Horizonte for children from low-income communities

16

Key Strategies for 2009

Maintain investments to ensure growth of all of the Company’s units;

Finalize the new organizational structure of TeleSystem and Credit&Risk;

Increase profitability and margins of CSU as a whole.

17

CSU CardSystem S/A

Questions and Answers

Décio Burd

Phone: (0xx55 11) 3030-3821

Email: [email protected]

Site: www.csu.com.br/ri