1 principles of tax analysis © allen c. goodman, 2009

Post on 21-Dec-2015

228 views

TRANSCRIPT

1

Principles of Tax Analysis

© Allen C. Goodman, 2009

2

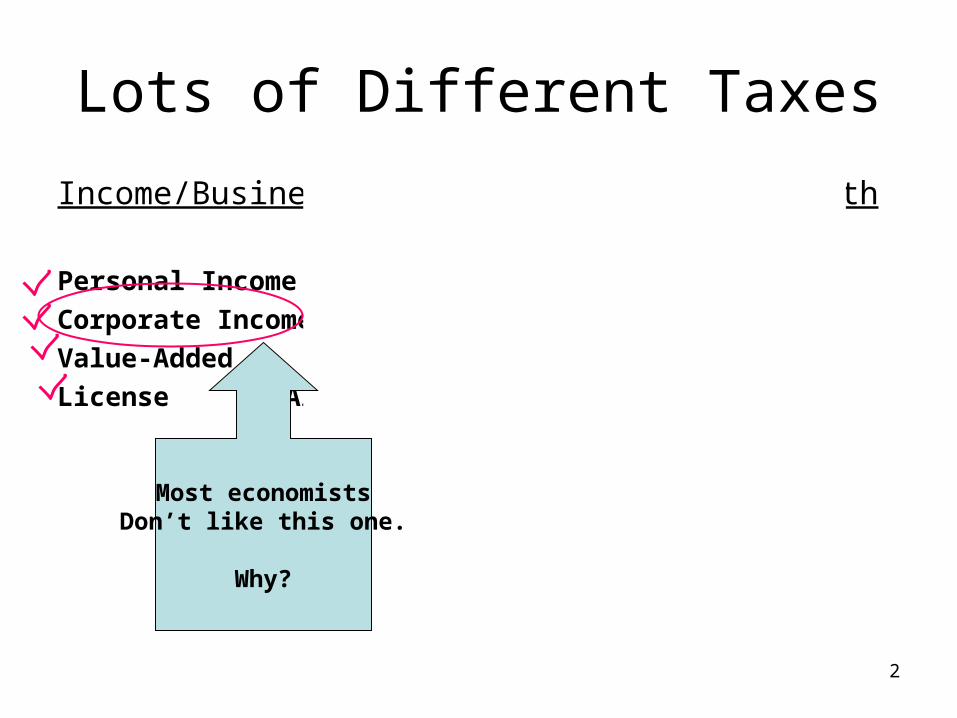

Lots of Different Taxes

Income/Business Consumption Wealth

Personal Income Sales Property

Corporate Income Use Estate

Value-Added Motor Fuel Inheritance

License Alcoholic Beverage Transfer

Hotel/Motel

Restaurant Meals

Telephone Call

Gambling

Most economistsDon’t like this one.

Why?

3

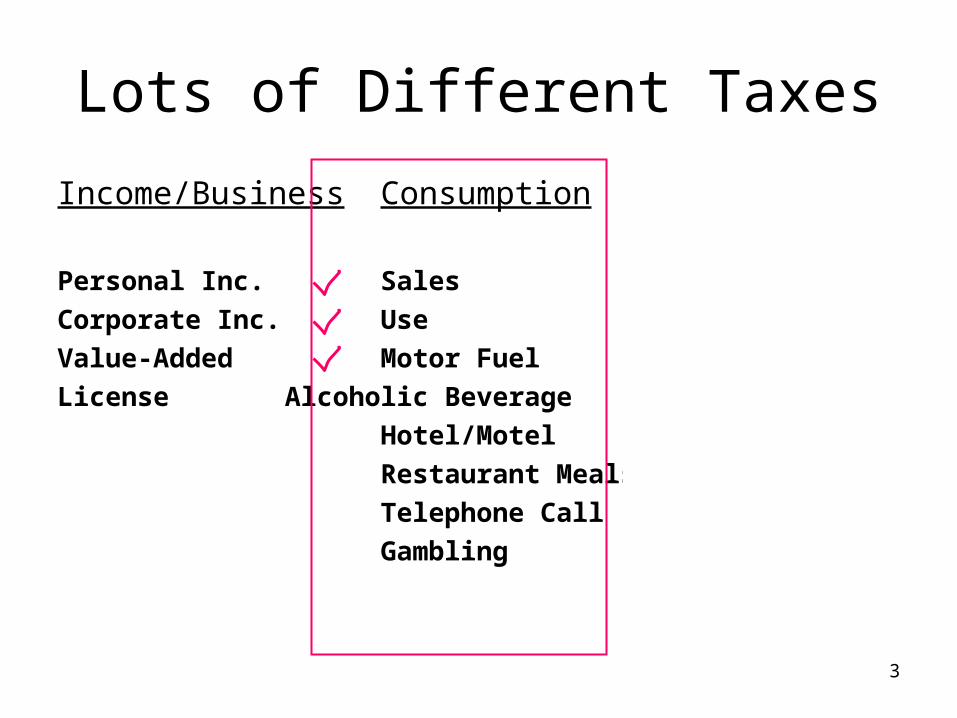

Lots of Different Taxes

Income/Business Consumption Wealth

Personal Inc. Sales Property

Corporate Inc. Use Estate

Value-Added Motor Fuel Inheritance

License Alcoholic Beverage Transfer

Hotel/Motel

Restaurant Meals

Telephone Call

Gambling

4

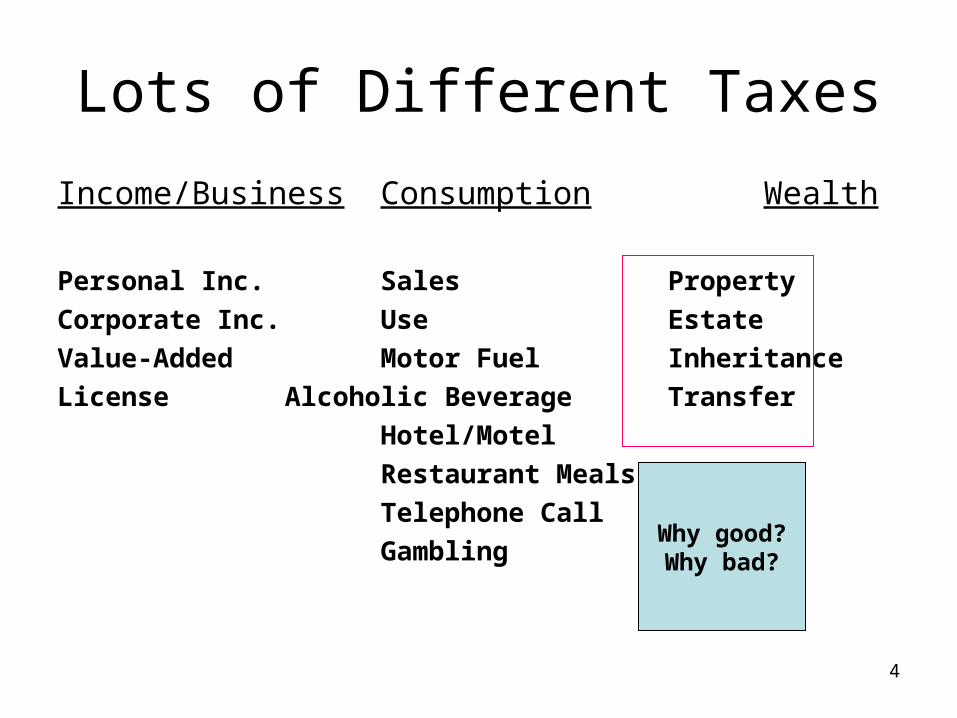

Lots of Different Taxes

Income/Business Consumption Wealth

Personal Inc. Sales Property

Corporate Inc. Use Estate

Value-Added Motor Fuel Inheritance

License Alcoholic Beverage Transfer

Hotel/Motel

Restaurant Meals

Telephone Call

GamblingWhy good?Why bad?

5

Tax Incidence

• Who REALLY pays the tax

• If you buy something at the store, you give $ to the clerk, and the store pays $ to the gov’t, but who really pays?

• If you rent an apartment and property taxes in your city rise, what happens to the rent that you pay? Who really pays?

6

Tax Incidence and Burden

• Progressive Tax– Tax Burden/income ↑

as income ↑

• Proportional Tax– Tax Burden/income

is constant as income ↑

• Regressive Tax– Tax Burden/income ↓

as income ↑Income

Tax

7

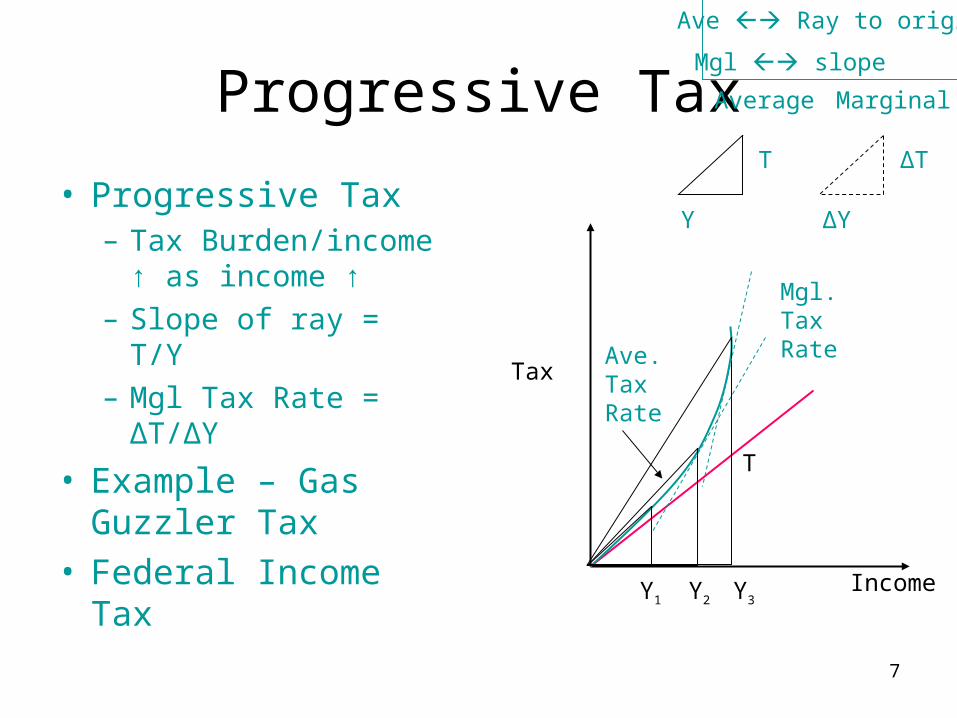

Progressive Tax

• Progressive Tax– Tax Burden/income ↑

as income ↑– Slope of ray = T/Y– Mgl Tax Rate =

ΔT/ΔY

• Example – Gas Guzzler Tax

• Federal Income TaxIncome

Tax

T

Y

Y1 Y2 Y3

Ave.TaxRate

Mgl.TaxRate

T

ΔT

ΔY

Average Marginal

Ave Ray to origin

Mgl slope

8

Proportional Tax

• Proportional Tax– Tax Burden/income

constant as income ↑– Slope of ray = T/Y– Mgl Tax Rate =

ΔT/ΔY

• Example – Medicare Tax

Income

Tax

Y1 Y2 Y3

T

Y

ΔT

ΔY

Average Marginal

Ave Ray to origin

Mgl slope

9

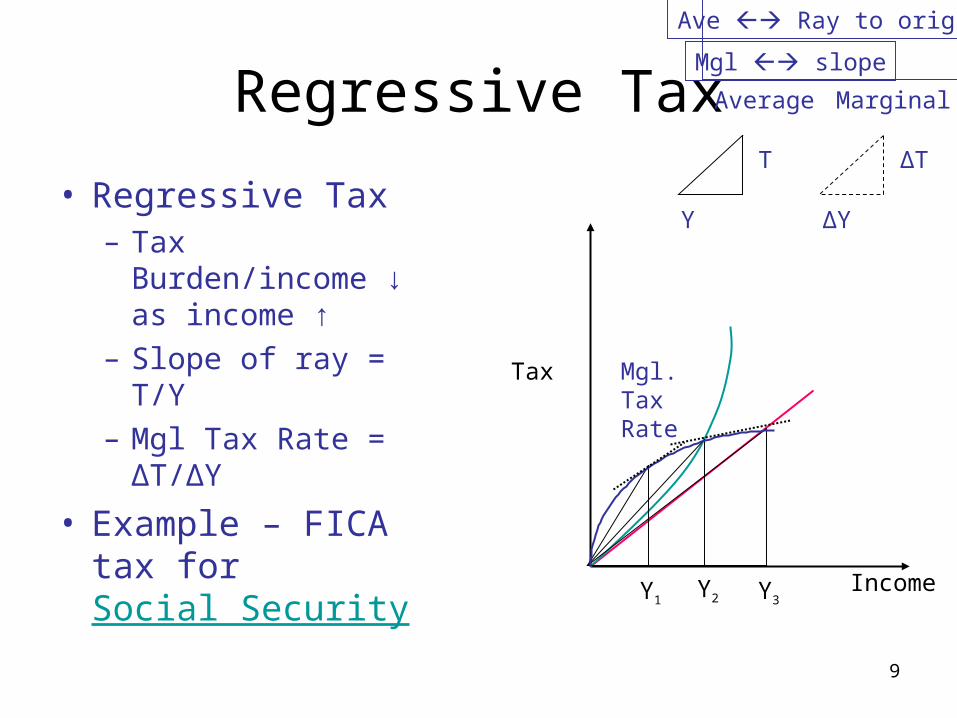

Regressive Tax

• Regressive Tax– Tax Burden/income ↓

as income ↑– Slope of ray = T/Y– Mgl Tax Rate =

ΔT/ΔY

• Example – FICA tax for Social Security

Income

Tax

Y1Y2 Y3

Mgl.TaxRate

T

Y

ΔT

ΔY

Average Marginal

Ave Ray to origin

Mgl slope

10

FICA and Medicare Taxes

0

1000

2000

3000

4000

5000

6000

7000

0 20000 40000 60000 80000 100000 120000

Payroll Income

Tax

es (

$)

FICA Tax - 2008

FICA Tax - 2009

Medicare Tax

FICA and Medicare

11

General Rules for Taxes

• Only way (legally) to avoid taxes is to change behavior.

• The more that one agent can avoid the tax – the less is collected– the more someone else pays

12

Taxes and Efficiency

• Excise Tax– Tax on a particular

good.– Look at a unit (as

oppose to percentage) tax.

• Partial eq’m analysis looks at a single market.

$

Q

D S

Q0

P0

EfficientQuantity! WHY?

EfficientQuantity! WHY?

13

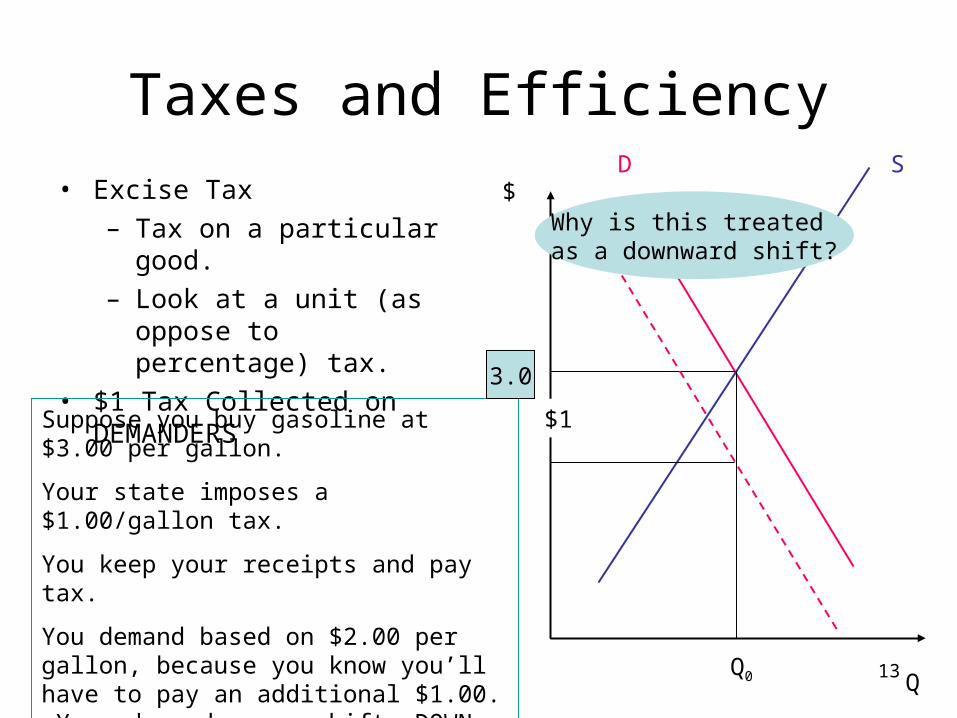

Taxes and Efficiency

• Excise Tax– Tax on a particular good.– Look at a unit (as oppose to

percentage) tax.• $1 Tax Collected on

DEMANDERS

$

Q

D S

Q0

P0

$1

Why is this treated as a downward shift?

Suppose you buy gasoline at $3.00 per gallon.

Your state imposes a $1.00/gallon tax.

You keep your receipts and pay tax.

You demand based on $2.00 per gallon, because you know you’ll have to pay an additional $1.00. Your demand curve shifts DOWN by $1.00.

3.0

14

Total Revenue

Taxes and Efficiency

• Excise Tax– Tax on a particular

good.– Look at a unit (as

oppose to percentage) tax.

• $1 Tax Collected on DEMANDERS

$

Q

D S

Q0

P0

Who Pays?

P1

Q1

D'

$1

3.0

15

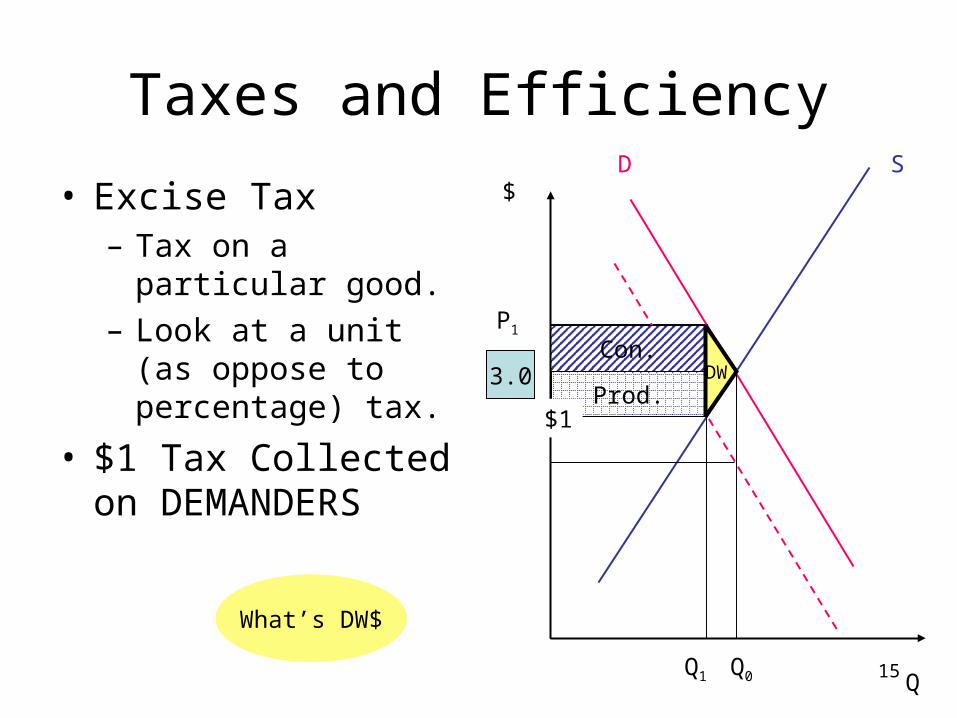

Taxes and Efficiency

• Excise Tax– Tax on a particular

good.– Look at a unit (as

oppose to percentage) tax.

• $1 Tax Collected on DEMANDERS

$

Q

D S

Q0

P0

What’s DW$

P1

Q1

Prod.

Con.DW

$1

3.0

16

Total RevenueProd.

Suppose the $1 is on Suppliers?

$

Q

D S

Q0

P0

• Excise Tax– Tax on a particular

good.– Look at a unit (as

oppose to percentage) tax.

• $1 Tax Collected on SUPPLIERS

Who Pays?

Cons.

EXACTLY the same result.

EXACTLY the same result.

DW

P1

Q1

3.0

17

If result is same …

• Why do we usually collect sales taxes from the sellers?

• Do we ever try to collect it from the buyers?

• What happens when we do?

18

Important Concepts!

• DW loss relates to the change in quantity. Remember, we saw that efficiency related to quantity. The more behavioral change that a tax makes, the more DW loss.

• Incidence relates to elasticity of demand and supply. Remember elasticity addresses whether quantity changes a little or lot. If you can change your behavior a lot, and avoid the tax, its incidence on you is small.

• If you can’t change your behavior and avoid it, its incidence is a lot! Does it matter how we collect the tax?

19

Total (yellow)

Another Gas Tax Example

• Suppose that Southfield puts a $1/gallon tax on gas.

• Let’s look at demand and supply.

• Why did I draw demand and supply like I did.

$

Quantity

D

S

Who Pays?

Q0

$1

P0

P1

Q1

Price ↑ a little;Quantity ↓ a lotMost is paid by

producers.

S'

Consumer

by producer

20

TaxCollected

Another Gas Tax Example

• Suppose that the US puts a $1/gallon tax on gas.

• Let’s look at demand and supply.

• Why did I draw demand and supply like I did.

$

Quantity

D

S

Who Pays?

Q0

$1

P0

P1

Q1

Price ↑ a lot;Quantity ↓ a littleMost is paid by

consumers.

S'

WHY?

21

Excess Burden – Gen’l Eq’m

• Previously, we looked only at a single market. Even if a tax doesn’t change quantity in a given market it may change behavior in other markets. U0

U1

U2

• We can’t measure U1 – U2, but we CAN, in principle, measure the cost in $ of this excess burden.

Gasoline

Other Goods

Excess Burden

22

Even if Q doesn’t change! – Gen’l Eq’m

• Previously, we looked only at a single market. Even if a tax doesn’t change quantity in a given market (again, suppose it’s gasoline) it may change behavior in other markets. U0

U1

U2

• Again we can’t measure U1 – U2, but we CAN, in principle, measure the cost in $ of this excess burden, even though the amount of gas did not change.

Gasoline

Other Goods

23

Tax Incidence

© Allen C. Goodman, 2009

WHOREALLY PAYS?

WHOREALLY PAYS?

24

What has been happening

• Over time, the share of output generated from the relatively less cyclically sensitive service-producing industries has risen modestly in comparison with relatively larger cyclically sensitive goods-producing industries.

• So, as the share of services has risen the share (and possibly the amount) of goods-based sales taxes has fallen.

25

Sources of State Revenues

• Go to Spreadsheet

All States

http://www.census.gov/compendia/statab/cats/state_local_govt_finances_employment/state_government_finances.html

26

Where does Michigan stand?

• Go to Spreadsheet.

http://www.census.gov/compendia/statab/cats/state_local_govt_finances_employment/state_government_finances.html

27

Total Sales

Short-Run and Long-Run Impacts

• Look at SR supply elasticities?

• Look at SR demand elasticities?

• What is impact of 6% tax on services?

D S$

Quantity

S'

Why drawn like this?

Why drawn like this?

Total Tax Rev.P1

Q1Q2

P2

DW is small

28

Tot Sales

Long-Run Impacts

• Look at LR supply elasticities?

• Look at LR demand elasticities?

• What is impact of 6% tax on services?

D S$

Quantity

S'

Supply more elastic

Supply more elastic

Tot. Tax Rev.P1

Q1Q2

P2

S''

D''

Demand more elastic

Demand more elastic

29

Tot Sales

Long-Run Impacts

• What is net impact as drawn?

• P3 < P2 because demand is more elastic

• TR? Depends on whether price ↑ (leading to ↑ in tax per unit) by greater % than quantity ↓.

D S$

Quantity

S'

Tot. Tax Rev.P1

Q1Q2

P2

S''

D''

P3

Q3

New Tax Rev.

30

A Model of a Michigan Service Tax

1 = goods produced nationally– examples?

2 = goods produced locally – examples?

T = Taxes Collected by MichiganT = National sector taxes + Local Sector taxes

T = t1 p1 Q1 (t1, t2, p1, p2, y) + t2 p2 Q2 (t1, t2, p1, p2, y)

y = p1 Q1 + p2 Q2

+ -

-+ +

What happens if we establish (increase) taxeson local goods, services?

31

• Lots of things happen!!

• Prices of local goods , in quantity demanded of local goods.

in demand for national goods.

• What will be the TAX IMPACT and who will pay it?

What will the Full Impact of a tax on local goods be?

32

dT/dt2 = p2 Q2 + t2 p2 (dQ2/dt2) + t2 p2 (dQ2/dp2 ) (dp2/dt2 ) + t1 p1 (dQ1/dt2 )

What will the Full Impact of a tax on local goods be?

Less Sold! But itIs now taxed.

Higher prices,Less sold.

More taxes onSubstitutes.

33

dT/dt2 = p2 Q2 + t2 p2 (dQ2/dt2) + t2 p2 (dQ2/dp2 ) (dp2/dt2 ) + t1 p1 (dQ1/dt2 )

dT/dt2 = p2 Q2 + t2 (dQ2/dt2 ) (Q2/Q2) p2 + (Q2/Q2)(p2/p2) t2 p2 (dQ2/dp2 ) (dp2/dt2 ) + (t2/t2) (Q1/Q1) t1 p1 (dQ1/dt2)

dT/dt2 = p2 Q2 + dQ2/dt2 (t2 /Q2) (p2 Q2) + p2 Q2 [(dQ2/dp2) (p2/Q2)] [(dp2/dt2) (t2/p2)] + (t1/t2)(p1Q1) (dQ1/dt2) (t2/Q1)

dT/dt2 = p2 Q2 + Elas Q2t2 (p2 Q2) + p2 Q2 (Elas Q2p2) (Elas p2t2) + (t1/t2)(p1Q1) (Elas Q1t2)

dT/dt2 = p2 Q2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2)+ p1Q1 (t1/t2) (Elas Q1t2)

What will the Full Impact of a tax on local goods be?

34

dT/dt2 = p2 Q2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2)+

p1Q1 (t1/t2) (Elas Q1t2)

A Model of the Service Tax+ or - ? + or - ? + or - ?

+ or - ?

KEY POINT --- There are LOTS of Impacts!

35

dT/dt2 = p2 Q2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2)+ p1Q1

(t1/t2) (Elas Q1t2)

0.06* (dT/dt2) = 0.06 * p2 Q2 (1 + Elas Q2t2 + Elas Q2p2

Elas p2t2)+ 0.06 * t1p1Q1 (Elas Q1t2)

Elas Tt2 = s2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2) + s1 *

Elas Q1t2 ; s1 = t1p1Q1/T; s2 = t2p2Q2/T.

A 6% Service Taxt2 = 0.06

This is a one UNIT

in tax. We want 0.06 of that.

36

dT/dt2 = p2 Q2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2)+ p1Q1

(t1/t2) (Elas Q1t2)

0.06* (dT/dt2) = 0.06 * p2 Q2 (1 + Elas Q2t2 + Elas Q2p2

Elas p2t2)+ 0.06 * p1Q1 (t1) (Elas Q1t2)

Elas Tt2 = s2 (1 + Elas Q2t2 + Elas Q2p2 Elas p2t2) + s1 *

Elas Q1t2 ; s1 = t1p1Q1/T; s2 = t2p2Q2/T.

A 6% Service Taxt2 = 0.06

6% of original sales of Q2

Change in sales of Q1