1 presented by m. kim anderson robertson stromberg pedersen llp non-title tax enforcement in...

TRANSCRIPT

1

Presented by M. Kim AndersonRobertson Stromberg Pedersen LLP

Non-Title Tax Enforcement

In Saskatchewan

2

Tax Enforcement

• Method of choice – title proceedings

3

Tax Enforcement

• Method of choice – title proceedings

• Other methods available and may be preferable to title proceedings

4

Non-Title Proceedings

Why take non-title Proceedings?

5

Non-Title Proceedings

Why take non-title Proceedings?

• Depressed resale market limits recovery on taxes

6

Non-Title Proceedings

Why take non-title Proceedings?

• Depressed resale market limits recovery on taxes

• Resale unlikely – will deplete tax base

7

Non-Title Proceedings

Why take non-title Proceedings?

• Depressed resale market limits recovery on taxes

• Resale unlikely – will deplete tax base

• Potential environmental problems with land

8

Non-Title Proceedings

Why take non-title Proceedings?

• Depressed resale market limits recovery on taxes

• Resale unlikely – will deplete tax base

• Potential environmental problems with land

• Delay involved in taking title proceedings

9

Prerequisites to Enforcement

Current taxes or only arrears?

10

Prerequisites to Enforcement

Current taxes or only arrears?

• Some remedies only permit collection of arrears

11

Prerequisites to Enforcement

Current taxes or only arrears?

• Some remedies only permit collection of arrears

• Some remedies permit collection of current taxes

12

Prerequisites to Enforcement

Current taxes or only arrears?

• Some remedies only permit collection of arrears

• Some remedies permit collection of current taxes

• If put to the expense of collecting arrears, why not collect current taxes as well?

13

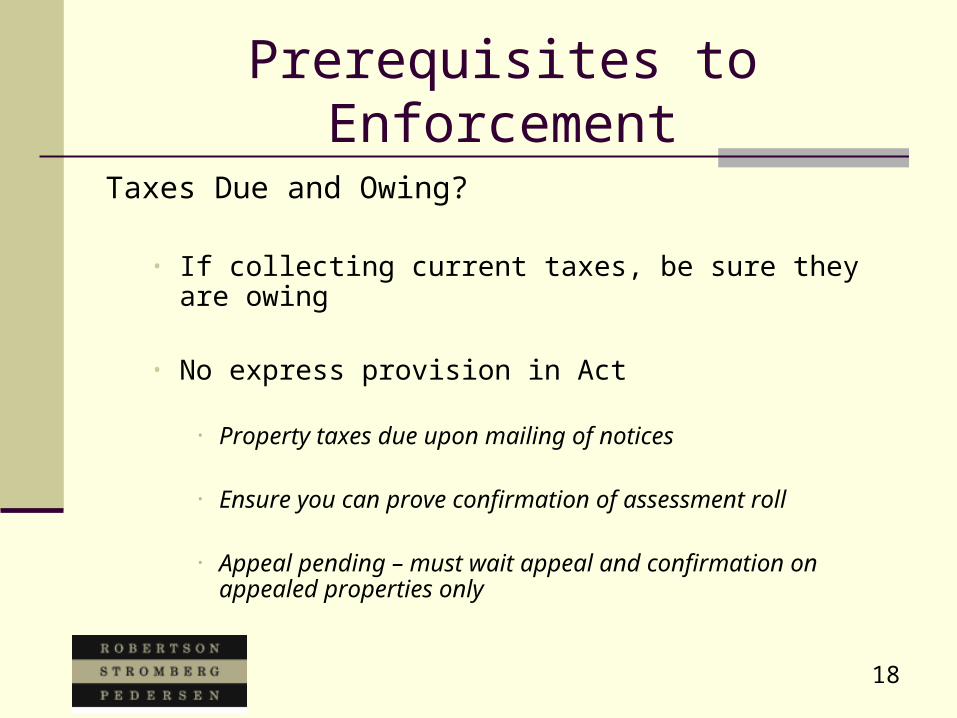

Prerequisites to Enforcement

Taxes Due and Owing?

14

Prerequisites to Enforcement

Taxes Due and Owing?

• If collecting current taxes, be sure they are owing

15

Prerequisites to Enforcement

Taxes Due and Owing?

• If collecting current taxes, be sure they are owing

• No express provision in Act

16

Prerequisites to Enforcement

Taxes Due and Owing?

• If collecting current taxes, be sure they are owing

• No express provision in Act

• Property taxes due upon mailing of notices

17

Prerequisites to Enforcement

Taxes Due and Owing?

• If collecting current taxes, be sure they are owing

• No express provision in Act

• Property taxes due upon mailing of notices

• Ensure you can prove confirmation of assessment roll

18

Prerequisites to Enforcement

Taxes Due and Owing?

• If collecting current taxes, be sure they are owing

• No express provision in Act

• Property taxes due upon mailing of notices

• Ensure you can prove confirmation of assessment roll

• Appeal pending – must wait appeal and confirmation on appealed properties only

19

Prerequisites to Enforcement

Items added to taxes

20

Prerequisites to Enforcement

Items added to taxes

• Be sure you are entitled to collect

21

Prerequisites to Enforcement

Items added to taxes

• Be sure you are entitled to collect

• Clear statutory authority to add to taxes

22

Prerequisites to Enforcement

Items added to taxes

• Be sure you are entitled to collect

• Clear statutory authority to add to taxes

• Enabling bylaws and resolutions all passed

23

Prerequisites to Enforcement

Items added to taxes

• Be sure you are entitled to collect

• Clear statutory authority to add to taxes

• Enabling bylaws and resolutions all passed

• Costs are properly documented

24

Prerequisites to Enforcement

Items added to taxes

• Be sure you are entitled to collect

• Clear statutory authority to add to taxes

• Enabling bylaws and resolutions all passed

• Costs are properly documented

• Necessary time frame has passed

25

Prerequisites to Enforcement

Demand for Payment?

26

Prerequisites to Enforcement

Demand for Payment?

• Not legally required

27

Prerequisites to Enforcement

Demand for Payment?

• Not legally required

• May result in taxes being paid

28

Prerequisites to Enforcement

Demand for Payment?

• Not legally required

• May result in taxes being paid

• Weigh advantage of having demand come from legal counsel

29

Suing the Taxpayer

When should we sue?

30

Suing the Taxpayer

When should we sue?

• Taxpayer has funds, but simply won’t pay

31

Suing the Taxpayer

When should we sue?

• Taxpayer has funds, but simply won’t pay

• Don’t want to deplete dwindling tax base

32

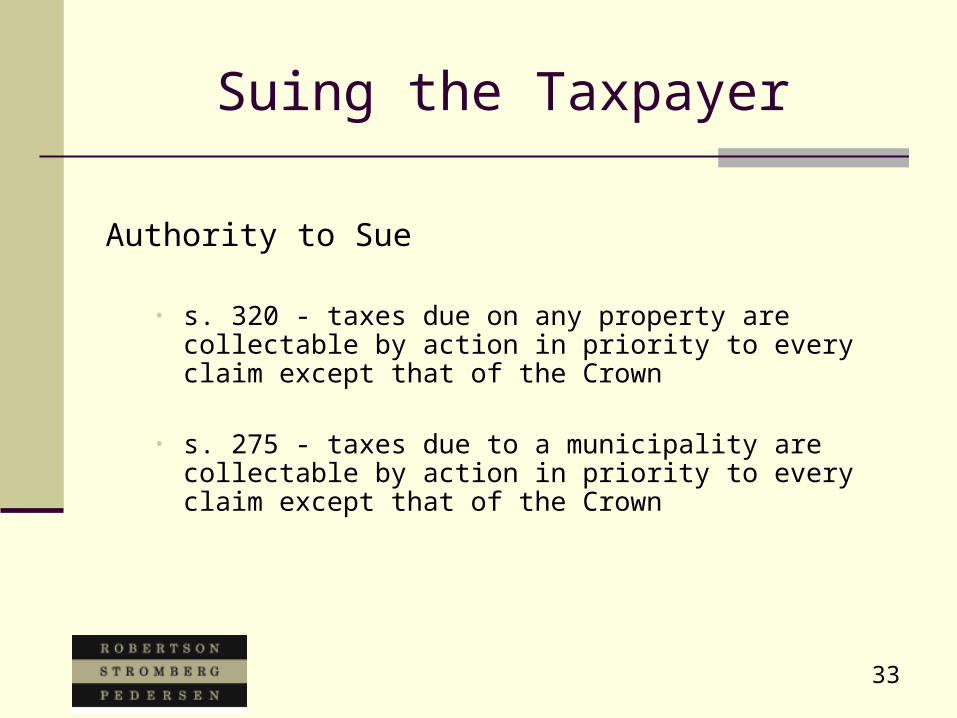

Suing the Taxpayer

Authority to Sue

33

Suing the Taxpayer

Authority to Sue

• s. 320 - taxes due on any property are collectable by action in priority to every claim except that of the Crown

• s. 275 - taxes due to a municipality are collectable by action in priority to every claim except that of the Crown

34

Suing the Taxpayer

Which Court

• Under $20,000.00 can go to Provincial Court

• Otherwise go to Queen’s Bench

35

Suing the Taxpayer

Why choose Provincial Court?

36

Suing the Taxpayer

Why choose Provincial Court?

• Circuit court location may be nearby

37

Suing the Taxpayer

Why choose Provincial Court?

• Circuit court location may be nearby

• Can present case without assistance of a lawyer

38

Suing the Taxpayer

Why choose Queen’s Bench?

39

Suing the Taxpayer

Why choose Queen’s Bench?

• May be able to obtain default judgment

40

Suing the Taxpayer

Why choose Queen’s Bench?

• May be able to obtain default judgment

• Use of summary procedure may limit need to attend court

41

Suing the Taxpayer

Getting Underway in Provincial Court

42

Suing the Taxpayer

Getting Underway in Provincial Court

• Prepare summary of claim with copies of all supporting documents

43

Suing the Taxpayer

Getting Underway in Provincial Court

• Prepare summary of claim with copies of all supporting documents, and

• Transmit to nearest Provincial Court with a request to issue a summons at the nearest circuit court location

44

Suing the Taxpayer

Getting Underway in Provincial Court

• Prepare summary of claim with copies of all supporting documents, and

• Transmit to nearest Provincial Court with a request to issue a summons at the nearest circuit court location, or

• Take to nearest Provincial Court office and meet with clerk

45

Suing the Taxpayer

Getting Underway in Provincial Court

• Prepare summary of claim with copies of all supporting documents, and

• Transmit to nearest Provincial Court with a request to issue a summons at the nearest circuit court location, or

• Take to nearest Provincial Court office and meet with clerk

• Issue Summons and serve on Defendant

46

Suing the Taxpayer

Provincial Court - Service of Documents

47

Suing the Taxpayer

Provincial Court - Service of Documents

• Must serve at least ten days before return date

48

Suing the Taxpayer

Provincial Court - Service of Documents

• Must serve at least ten days before return date

• May try to serve by registered mail, but taxpayer must sign acknowlegment card and return it

49

Suing the Taxpayer

Provincial Court - Service of Documents

• Must serve at least ten days before return date

• May try to serve by registered mail, but taxpayer must sign acknowlegment card and return it

• Best to serve in person (use process server if you prefer)

50

Suing the Taxpayer

Provincial Court - Procedure

51

Suing the Taxpayer

Provincial Court - Procedure

• Case management conference usually held

52

Suing the Taxpayer

Provincial Court - Procedure

• Case management conference usually held

• Defendant does not attend – judgment entered

53

Suing the Taxpayer

Provincial Court - Procedure

• Case management conference usually held

• Defendant does not attend – judgment entered

• Defendant does attend – “privileged” settlement discussion with a judge

54

Suing the Taxpayer

Provincial Court - Procedure

• Case management conference usually held

• Defendant does not attend – judgment entered

• Defendant does attend – “privileged” settlement discussion with a judge

• No settlement – trial date set

55

Suing the Taxpayer

Provincial Court - Trial Preparation

56

Suing the Taxpayer

Provincial Court - Trial Preparation

• Prepare for possible objections by taxpayer

57

Suing the Taxpayer

Provincial Court - Trial Preparation

• Prepare for possible objections by taxpayer

• Claiming the wrong amount

58

Suing the Taxpayer

Provincial Court - Trial Preparation

• Prepare for possible objections by taxpayer

• Claiming the wrong amount

• Assessment is incorrect

59

Suing the Taxpayer

Provincial Court - Trial Preparation

• Prepare for possible objections by taxpayer

• Claiming the wrong amount

• Assessment is incorrect

• Didn’t get notice

60

Suing the Taxpayer

Provincial Court - Document Preparation

61

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare certified copy of tax roll - s. 277 states it is proof of taxes owing

62

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare certified copy of tax roll - s. 277 states it is proof of taxes owing

• Prepare certified copy of any ledger account associated with claim

63

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare certified copy of tax roll - s. 277 states it is proof of taxes owing

• Prepare certified copy of any ledger account associated with claim

• Prepare certified copy of assessment roll and of confirmation

64

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare certified copy of tax roll - s. 277 states it is proof of taxes owing

• Prepare certified copy of any ledger account associated with claim

• Prepare certified copy of assessment roll and of confirmation

• Prepare certified copy of tax notice and certificate of mailing under s. 258

65

Suing the Taxpayer

Provincial Court - Document Preparation

66

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare copy of any relevant correspondence

67

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare copy of any relevant correspondence

• Review documents so you are fully familiar

68

Suing the Taxpayer

Provincial Court - Document Preparation

• Prepare copy of any relevant correspondence

• Review documents so you are fully familiar

• Prepare three copies of each – one for each party and one for the Court

69

Suing the Taxpayer

Provincial Court - Trial Procedure

70

Suing the Taxpayer

Provincial Court - Trial Procedure

• Appear early – advise the clerk you are present

71

Suing the Taxpayer

Provincial Court - Trial Procedure

• Appear early – advise the clerk you are present

• Tell the judge the nature of your claim and the amount claimed

72

Suing the Taxpayer

Provincial Court - Trial Procedure

• Appear early – advise the clerk you are present

• Tell the judge the nature of your claim and the amount claimed

• Take the stand and present the certified copy of the tax roll and any associated ledger account.

73

Suing the Taxpayer

Provincial Court - Trial Procedure

• Appear early – advise the clerk you are present

• Tell the judge the nature of your claim and the amount claimed

• Take the stand and present the certified copy of the tax roll and any associated ledger account.

• Testify positively as to the amount owing

74

Suing the Taxpayer

Provincial Court - Resources

75

Suing the Taxpayer

Provincial Court - Resources

• Review the information at www.sasklawcourts.ca

76

Suing the Taxpayer

Provincial Court - Resources

• Review the information at www.sasklawcourts.ca

• Consider having legal counsel prepare and instruct you the first time you sue for taxes with a view to learning the “how-tos”

77

Suing the Taxpayer

Provincial Court - Resources

• Review the information at www.sasklawcourts.ca

• Consider having legal counsel prepare and instruct you the first time you sue for taxes with a view to learning the “how-tos”

• If your comfort level requires – use your legal counsel

78

Suing the Taxpayer

Queen’ Bench - Procedure

79

Suing the Taxpayer

Queen’ Bench - Procedure

• No Defence filed within 20 days – enter default judgment

80

Suing the Taxpayer

Queen’ Bench - Procedure

• No Defence filed within 20 days – enter default judgment

• Defence entered – proceed to meditation session

81

Suing the Taxpayer

Queen’ Bench - Procedure

• No Defence filed within 20 days – enter default judgment

• Defence entered – proceed to meditation session

• Apply for summary judgment

82

Suing the Taxpayer

Queen’ Bench - Procedure

• No Defence filed within 20 days – enter default judgment

• Defence entered – proceed to meditation session

• Apply for summary judgment

• If summary judgment not granted, prepare documents and move to trial

83

Suing the Taxpayer

Judgment

84

Suing the Taxpayer

Judgment

• 30 days after judgment granted in Provincial Court – present to Queen’s Bench for Registration

85

Suing the Taxpayer

Judgment

• 30 days after judgment granted in Provincial Court – present to Queen’s Bench for Registration

• No registration required if judgment granted in Queen’s Bench

86

Suing the Taxpayer

Judgment

• 30 days after judgment granted in Provincial Court – present to Queen’s Bench for Registration

• No registration required if judgment granted in Queen’s Bench

• Appeal will Stay Judgment

87

Suing the Taxpayer

Enforcement

88

Suing the Taxpayer

Enforcement

• Garnishee Summons – attach debt owing or wages

89

Suing the Taxpayer

Enforcement

• Garnishee Summons – attach debt owing or wages

• Seizure under Writ of Execution

90

Suing the Taxpayer

Enforcement

• Garnishee Summons – attach debt owing or wages

• Seizure under Writ of Execution

• Process may change soon – The Enforcement of Money Judgments Act

91

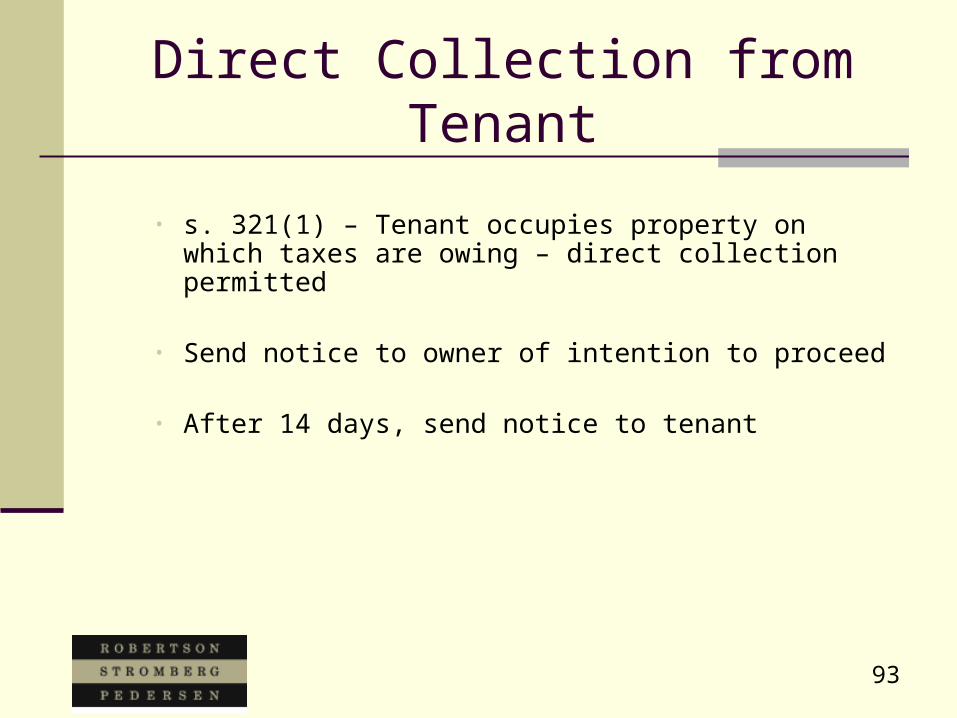

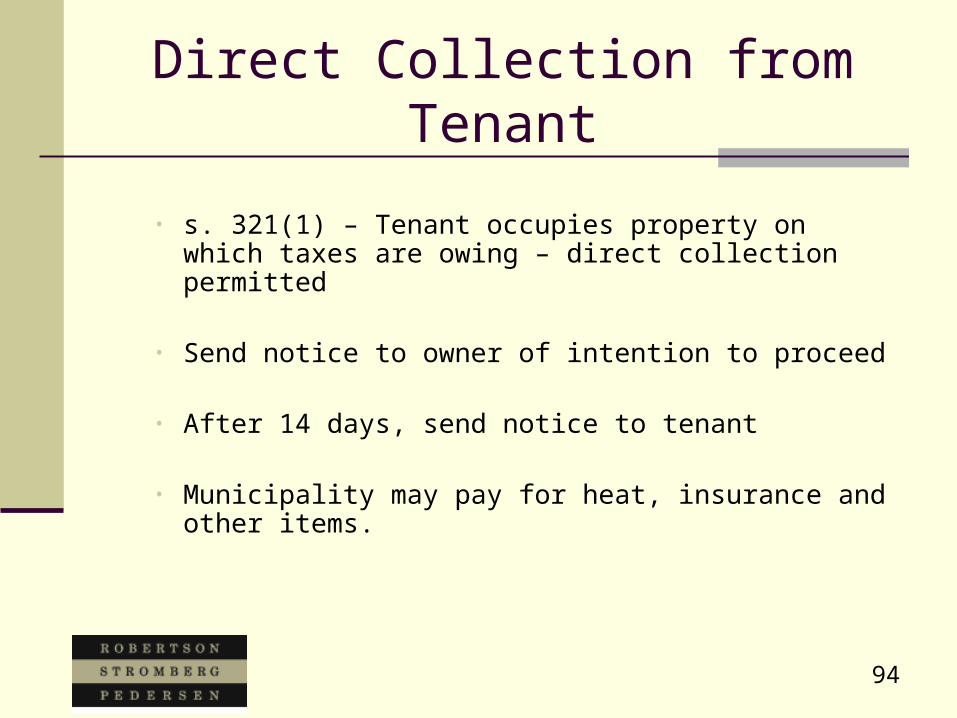

Direct Collection from Tenant

• s. 321(1) – Tenant occupies property on which taxes are owing – direct collection permitted

92

Direct Collection from Tenant

• s. 321(1) – Tenant occupies property on which taxes are owing – direct collection permitted

• Send notice to owner of intention to proceed

93

Direct Collection from Tenant

• s. 321(1) – Tenant occupies property on which taxes are owing – direct collection permitted

• Send notice to owner of intention to proceed

• After 14 days, send notice to tenant

94

Direct Collection from Tenant

• s. 321(1) – Tenant occupies property on which taxes are owing – direct collection permitted

• Send notice to owner of intention to proceed

• After 14 days, send notice to tenant

• Municipality may pay for heat, insurance and other items.

95

Direct Collection from Tenant

• s. 321(1) – Tenant occupies property on which taxes are owing – direct collection permitted

• Send notice to owner of intention to proceed

• After 14 days, send notice to tenant

• Municipality may pay for heat, insurance and other items.

• Tenant does not pay – municipality may distrain on tenant (does not apply to residential tenancy)

96

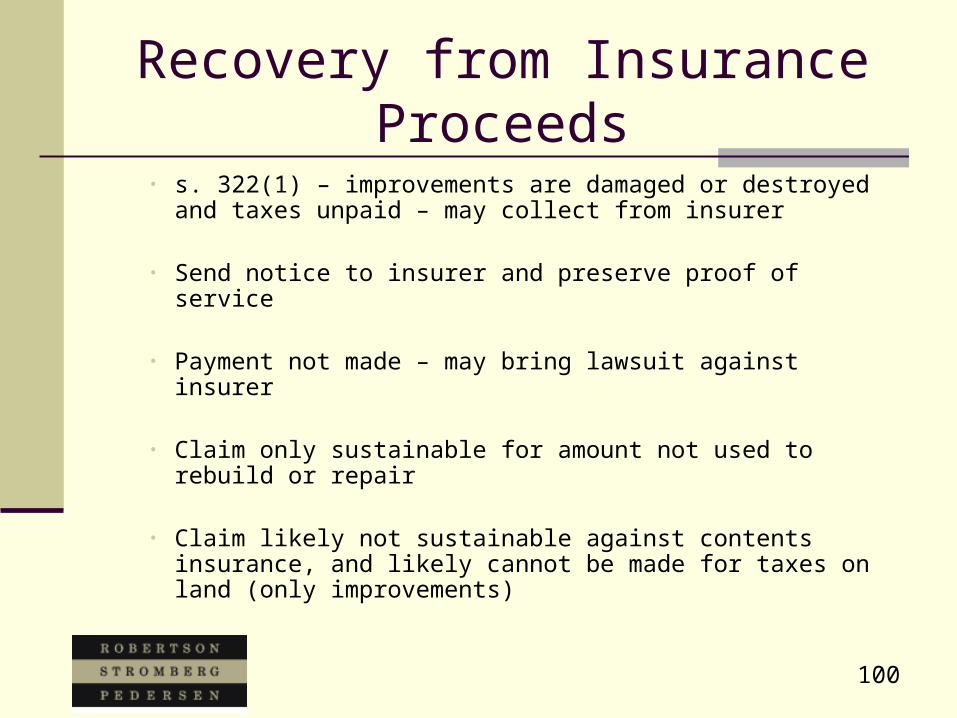

Recovery from Insurance Proceeds

• s. 322(1) – improvements are damaged or destroyed and taxes unpaid – may collect from insurer

97

Recovery from Insurance Proceeds

• s. 322(1) – improvements are damaged or destroyed and taxes unpaid – may collect from insurer

• Send notice to insurer and preserve proof of service

98

Recovery from Insurance Proceeds

• s. 322(1) – improvements are damaged or destroyed and taxes unpaid – may collect from insurer

• Send notice to insurer and preserve proof of service

• Payment not made – may bring lawsuit against insurer

99

Recovery from Insurance Proceeds

• s. 322(1) – improvements are damaged or destroyed and taxes unpaid – may collect from insurer

• Send notice to insurer and preserve proof of service

• Payment not made – may bring lawsuit against insurer

• Claim only sustainable for amount not used to rebuild or repair

100

Recovery from Insurance Proceeds

• s. 322(1) – improvements are damaged or destroyed and taxes unpaid – may collect from insurer

• Send notice to insurer and preserve proof of service

• Payment not made – may bring lawsuit against insurer

• Claim only sustainable for amount not used to rebuild or repair

• Claim likely not sustainable against contents insurance, and likely cannot be made for taxes on land (only improvements)

101

Distress

• s. 325 – taxes unpaid for 30 days after mailing of tax notice – municipality may issue warrant to bailiff

• S. 333 – may distrain for licence fees if unpaid for 14 days

• If there is reason to believe the goods to be seized will be removed from the municipality before 30/14 days expire, may apply to a justice of the peace for an order authorizing earlier seizure

102

Distress

Under s. 324 – the municipality may distrain on the following:

103

Distress

Under s. 324 – the municipality may distrain on the following:

• Goods belonging to the taxpayer, wherever those goods may be found within the municipality;

104

Distress

Under s. 324 – the municipality may distrain on the following:

• Goods belonging to the taxpayer, wherever those goods may be found within the municipality;

• Goods in the possession of the taxpayer, wherever those goods may be found within the municipality; and

105

Distress

Under s. 324 – the municipality may distrain on the following:

• Goods belonging to the taxpayer, wherever those goods may be found within the municipality;

• Goods in the possession of the taxpayer, wherever those goods may be found within the municipality; and

• Goods found on the property with respect to which the tax has been levied and that are owned by or in the possession of any occupant of the premises, other than a tenant.

106

Distress

The municipality may not distrain on the following:

107

Distress

The municipality may not distrain on the following:

• Goods that are the subject of a valid and subsisting lien in favor of a vendor (the interest of the taxpayer, or other occupant may still be seized subject to the vendor's interest)

108

Distress

The municipality may not distrain on the following:

• Goods that are the subject of a valid and subsisting lien in favor of a vendor (the interest of the taxpayer, or other occupant may still be seized subject to the vendor's interest)

• The vendor's or lessor's share of a crop

109

Distress

The municipality may not distrain on the following:

• Goods that are the subject of a valid and subsisting lien in favor of a vendor (the interest of the taxpayer, or other occupant may still be seized subject to the vendor's interest)

• The vendor's or lessor's share of a crop

• An animal not belonging to the taxpayer or to any occupant of the premises (unless the person is related)

110

Distress

The municipality may not distrain on the following:

• Goods that are the subject of a valid and subsisting lien in favor of a vendor (the interest of the taxpayer, or other occupant may still be seized subject to the vendor's interest)

• The vendor's or lessor's share of a crop

• An animal not belonging to the taxpayer or to any occupant of the premises (unless the person is related)

• Goods in the possession of the taxpayer only for storing and warehousing, or for sale on commission

111

Distress

Priorities –

112

Distress

Priorities -

• Municipal distress appears to have priority over a “chattel mortgage”

113

Distress

Priorities -

• Municipal distress appears to have priority over a “chattel mortgage”

• Municipal distress appears to be subject to the priority of a “conditional sale”

114

Distress

Priorities -

• Municipal distress appears to have priority over a “chattel mortgage”

• Municipal distress appears to be subject to the priority of a “conditional sale”

• Municipal distress has priority over distress by the landlord

115

Distress

Priorities -

• Municipal distress appears to have priority over a “chattel mortgage”

• Municipal distress appears to be subject to the priority of a “conditional sale”

• Municipal distress has priority over distress by the landlord

• Search the PPR prior to seizing

116

Distress

Notice and Sale

117

Distress

Notice and Sale

• Must provide written notice of sale

118

Distress

Notice and Sale

• Must provide written notice of sale

• Sale governed by s. 330

119

Distress

Notice and Sale:

• Must provide written notice of sale

• Sale governed by s. 330

• Costs recoverable only on tariff under The Distress Act

120

Distress

Notice and Sale:

• Must provide written notice of sale

• Sale governed by s. 330

• Costs recoverable only on tariff under The Distress Act

• May release part of goods without compromising claim

121

Distress

Following Hidden Goods:

• If goods have been fraudulently and clandstinely removed, may follow, break and enter in order to seize.

• Very technical remedy – get legal advice

122

Goods in Hands of Others

• s. 355 – applies where goods have been seized by sheriff, bailiff, liquidator, receiver, trustee in bankruptcy

123

Goods in Hands of Others

• s. 355 – applies where goods have been seized by sheriff, bailiff, liquidator, receiver, trustee in bankruptcy

• applies where goods or proceeds still in hands of third party

124

Goods in Hands of Others

• s. 355 – applies where goods have been seized by sheriff, bailiff, liquidator, receiver, trustee in bankruptcy

• applies where goods or proceeds still in hands of third party

• Municipality may serve written notice

125

Goods in Hands of Others

• s. 355 – applies where goods have been seized by sheriff, bailiff, liquidator, receiver, trustee in bankruptcy

• applies where goods or proceeds still in hands of third party

• Municipality may serve written notice

• Notice binds goods and proceeds – amount of taxes to be paid in priority to other claims except for fees of sheriff or bailiff, and amounts owing to the Crown

126

Collection – Oil or Gas Wells

• s. 355 – tax unpaid after year end on resource production equipment of an oil or gas well – can collect from anyone who purchases oil or gas originating on that well

• Send written notice to purchaser and preserve proof of service

127

Removed Improvements

• s. 356 – tax unpaid on land or improvements located thereon – improvements not to be removed from the municipality or demolished

128

Removed Improvements

• s. 356 – tax unpaid on land or improvements located thereon – improvements not to be removed from the municipality or demolished

• If removed, may locate the improvement, sever from land and restore to its former location

129

Removed Improvements

• s. 356 – tax unpaid on land or improvements located thereon – improvements not to be removed from the municipality or demolished

• If removed, may locate the improvement, sever from land and restore to its former location

• Alternatively, may distrain on improvement and sell for unpaid taxes and costs

130

Sharing Expenses

• Subject to express limitations, may recover costs

131

Sharing Expenses

• Subject to express limitations, may recover costs

• s. 309– if costs are not recoverable in full, reasonable costs may be apportioned between municipality and other taxing authorities

132

Sharing Expenses

• Subject to express limitations, may recover costs

• s. 309– if costs are not recoverable in full, reasonable costs may be apportioned between municipality and other taxing authorities

• Apportionment to be on a pro-rata basis

133

Sharing Expenses

• Subject to express limitations, may recover costs

• s. 309– if costs are not recoverable in full, reasonable costs may be apportioned between municipality and other taxing authorities

• Apportionment to be on a pro-rata basis

• Cannot include amounts paid to compensate municipal employee

134

Non-Title Enforcement

• Select your remedy carefully

135

Non-Title Enforcement

• Select your remedy carefully

• Ensure that the sum sought is accurate

136

Non-Title Enforcement

• Select your remedy carefully

• Ensure that the sum sought is accurate

• Satisfy pre-conditions

137

Non-Title Enforcement

• Select your remedy carefully

• Ensure that the sum sought is accurate

• Satisfy pre-conditions

• Prepare necessary documentation

138

For information on non-title proceedings or other muncipal matters, contact M. Kim Anderson at [email protected]