1 ppi inclusive growth, infra & construction v3

TRANSCRIPT

1

Inclusive Growth, Infrastructure and the

Role of the Construction Industry

Philippine Institute for Development StudiesSurian sa mga Pag-aaral Pangkaunlaran ng Pilipinas

www.pids.gov.ph

Adoracion M. NavarroSenior Research Fellow

Pandi, Bulacan28 April 2016

Philippine Press Institute’s Seminar-Workshop on Sustainable Construction Reporting

2

OUTLINE• Macroeconomic trends and poverty alleviation

• Suggested analytical frameworks

• State of physical infrastructure • Role and contribution of the construction

industry

3

Macroeconomic trends and poverty alleviation

4

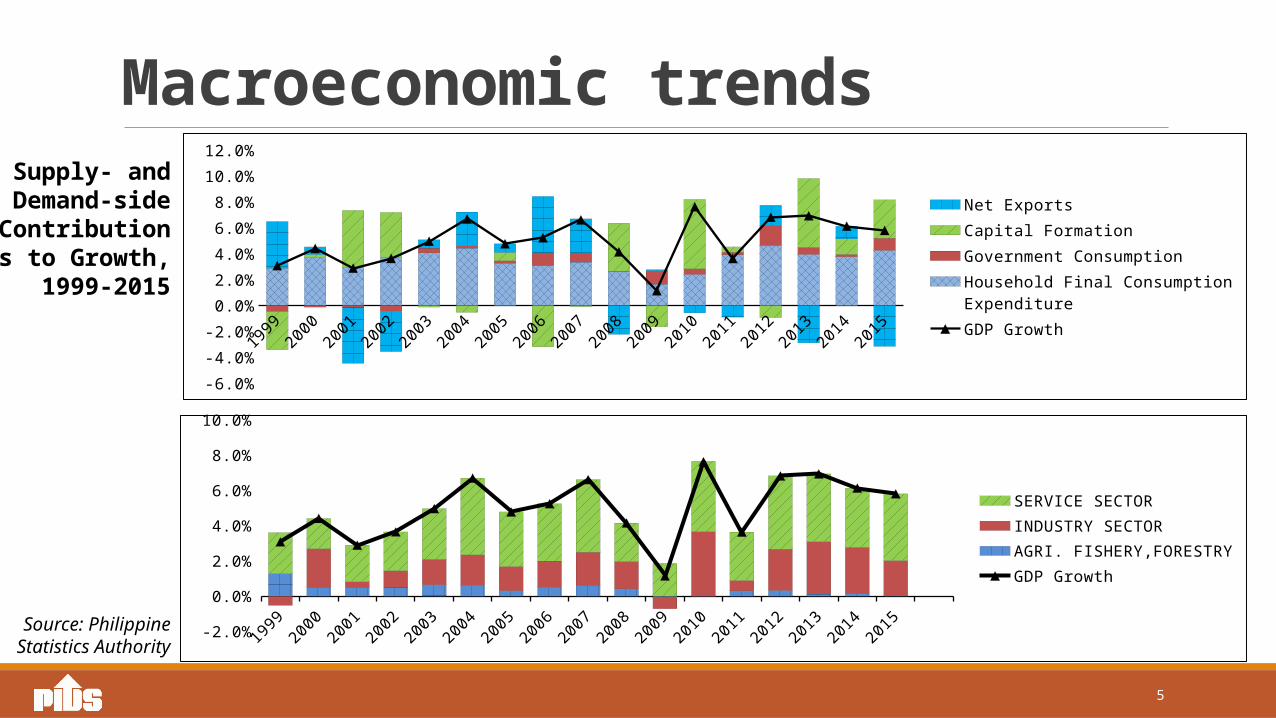

Macroeconomic trends

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

3.1%

4.4%

2.9%3.6%

5.0%

6.7%

4.8%5.2%

6.6%

4.2%

1.1%

7.6%

3.6%

6.8% 6.9%6.1% 5.8%

GDP Growth Rate

GDP Growth, at constant 2000 prices

Source: Philippine Statistics Authority

5

Macroeconomic trends

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Net ExportsCapital FormationGovernment ConsumptionHousehold Final Consumption ExpenditureGDP Growth

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

SERVICE SECTORINDUSTRY SECTORAGRI. FISHERY,FORESTRYGDP Growth

Supply- and Demand-side

Contributions to Growth,

1999-2015

Source: Philippine Statistics Authority

6

Poverty alleviation• Poverty incidence among

Filipinos has been declining since 2008

From an estimate of 28.8 percent in first sem 2006, it went down to 26.3 in first sem 2015

• The same trend can be observed with regards to the poverty incidence among families

From 23.4 percent in first sem 2006, it went down to 21.1 percent in first sem 2015

2006 2009 2012 20150.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

23.4 22.9 22.3 21.1

28.8 28.6 27.9 26.3

Poverty Incidence among Families (%)Poverty Incidence among Population (%)

Poverty Incidence among Families and Population: first semesters of 2006, 2009, 2012 and 2015

Source: Philippine Statistics Authority

7

Poverty alleviation

NCRRegion IV-A

Region IIIRegion IIRegion I

Region XICAR

Region IV-BRegion VI

Region VIIRegion IXRegion VRegion X

CaragaRegion XII

Region VIIIARMM

0.0 10.0 20.0 30.0 40.0 50.0 60.04.5

10.413.0

16.517.2

20.520.6

22.024.2

27.030.930.9

34.935.3

37.439.3

53.4

First Semester Poverty Incidence among Families (%)

NCRRegion IV-A

Region IIIRegion IIRegion I

CARRegion XI

Region IV-BRegion VIIRegion VIRegion VRegion IXRegion X

CaragaRegion XII

Region VIIIARMM

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.06.5

13.415.8

21.521.7

26.726.7

29.830.530.5

39.039.0

40.943.944.5

47.359.0

First Semester Poverty Incidence among Population (%)

First Semester Poverty Incidence among Families and Population, Per Region: 2015

Source: Philippine Statistics Authority

8

Income inequality is the bigger challenge

2009 20121st Decile 2.9% 3.0%2nd Decile 3.9% 3.9%3rd Decile 4.6% 4.6%4th Decile 5.5% 5.4%5th Decile 6.5% 6.5%6th Decile 7.8% 7.8%7th Decile 9.8% 9.5%8th Decile 12.2% 12.1%9th Decile 16.2% 16.3%

10th Decile 30.5% 30.8%

2000 2003 2006 2009 201220

25

30

35

40

45

50

55

60

46.1744.04 44.2 42.91 43.04

Gini-Coefficient

Inequality in the Philippines: 2000, 2003, 2006, 2009 and 2012

Source: World Bank

Per Capita Income Decile, % Distribution

Sour

ce: P

hilip

pine

Sta

tistic

s Aut

horit

y

• Gini coefficient has decreased (inequality declined) from 46.17% in 2000 to 43.04% in 2012. Minimal movement from 2009 to 2012.

• With respect to income distribution, the richest decile earns approximately 10 times more than the poorest decile. The same trend can be seen in 2009.

9

Suggested analytical frameworks

10

What Adam Smith saidAn Inquiry into the Nature and Causes of the Wealth of Nations (1776):

“Good roads, canals, and navigable rivers, by diminishing the expense of carriage, put the remote parts of the country more nearly upon a level with those in the neighborhood of the town. They are upon that account the greatest of all improvements. They encourage the cultivation of the remote, which must always be the most extensive circle of the country… Though they introduce some rival commodities into the old market, they open many new markets to its produce.”

11

Physical infrastructure promotes inclusive growth

• enables connectivity and increases opportunity for engaging in economic activities

• stimulates mobility of production inputs like labor, financial capital, machineries, and equipment

• speeds up the delivery of social services to remote areas.

Source: http://goo.gl/DTtm0c

12

Infrastructure and urbanization• Infrastructure also facilitates the

process of urbanization Urbanization is a process characterized by

the spatial concentration of production activities as well as clustering and sorting in other human activities (Scott and Storper, 2014)

Infrastructure allows smooth interaction of the production space and the social space.

Urban development plans should have strong focus on the need to facilitate the circulation of people within and between the production spaces and social spaces

Production Space

Circulation Space

Social Space

production space where work and employment are

concentrated

circulation space as represented by infrastructures and arterial connections

social space as manifested in

residential neighborhoods

Urban land nexus

13

State of physical infrastructure

14

Roads• Road Network

Location and Road ClassificationLength (km)

Paved Unpaved Total

Metro ManilaArterial 88 - 88Secondary 943 - 943Total 1,032 - 1,032

PhilippinesArterial 12,747 2,812 15,559Secondary 8,259 5,551 13,810Total 21,006 8,363 29,370

Good, 34.0%

Fair, 31.5%

Poor, 17.1%Bad, 9.3%

No As-sessment,

8.1%

Location and Road Classification

National Road Condition, 2014

Source: DPWH, Stakeholder Relations Office

Source: DPWH Atlas, 2014

15

Mass Rail Transport & Bus Rapid Transit

Planned systems:• LRT 1 extension to Bacoor, Cavite• LRT 6, which will extend LRT 1 Bacoor

terminus to Dasmariñas• LRT 2 extension to Port Area, Manila• LRT 2 extension to Masinag, Antipolo• LRT 4, which will connect EDSA-Ortigas to

Taytay, Rizal• MRT 7, which will link North EDSA to San

Jose del Monte, Bulacan• new rail lines to be built over the existing

PNR routes, Tutuban-Malolos and Tutuban-Calamba

• BRT• Cebu BRT• Metro Manila BRT via Quezon Ave• EDSA BRT

Figure 2. Philippine Rail Network Source: DOTC

16

Airports• National Airport System

• No of Airports with Commercial Flight Operations = 42• No of Airports without Commercial Flight Operations = 43

• Runway Congestion• Maximum aircraft movement per hour is 40, but can spike up to 48 per hour in peak hours• Congestion leads to cascading delays; PAL estimates losses of Php 84,000 per 30-min delay

Philippine Airports, by Classification

Source: Civil Aviation Authority of the Philippines

CLASSIFICATION CAAP Authorities PPP Total

International 7 3 1 11

Principal Class 1 14 - - 14

Principal Class 2 18 - 1 19Community 40 1 - 41Total 79 4 2 85

17

Ports• National Port System

Type No. of PortsBaseports 26Terminal Ports 82Satellite and RORO Ports 103

Source: Philippine Ports Authority

Shipcalls 2012 2013 2014

Domestic 335,272 345,945 347,841

Foreign 10,598 10,572 9,639

Total 345,870 356,517 357,480

Source: Philippine Ports Authority Sour

ce: P

hilip

pine

Por

ts A

utho

rity

No. of Ports, by Type

Domestic and Foreign Shipcalls, 2012-2014

Figu

re 3

. Map

of P

hilip

pine

Por

ts

18

Infra Quality across ASEAN

Myanmar

Cambodia

Philippines

Vietnam

Lao PDR

Indonesia

Thailand

Malaysia

Singapore

0 1 2 3 4 5 6 7

2.3

3.3

3.3

3.3

3.6

3.7

4.4

5.7

6.2

Myanmar

Cambodia

Philippines

Lao PDR

Vietnam

Indonesia

Thailand

Malaysia

Singapore

0 1 2 3 4 5 6 7 8

2.6

3.7

3.7

3.8

4.2

4.4

5.1

5.7

6.8

Quality of Roads, across ASEAN Quality of Air Transport Infra, across ASEAN

Source: The Global Competitiveness Report 2015–2016, World Economic ForumNote: Values are on a 1-to-7 scale. A total of 14 economies were surveyed.

19

Infra Quality across ASEANQuality of Railroad Infra, across ASEANQuality of Port Infra, across ASEAN

Source: The Global Competitiveness Report 2015–2016, World Economic ForumNote: Values are on a 1-to-7 scale. A total of 140 economies were surveyed.

Cambodia

Myanmar

Philippines

Thailand

Vietnam

Indonesia

Malaysia

Singapore

0 1 2 3 4 5 6

1.6

1.8

2.2

2.4

3.2

3.6

5.1

5.7

Lao PDR

Myanmar

Philippines

Cambodia

Indonesia

Vietnam

Thailand

Malaysia

Singapore

0 1 2 3 4 5 6 7 8

2.2

2.6

3.2

3.7

3.8

3.9

4.5

5.6

6.7

20

ICT Indicators across ASEAN

Myanmar

Lao PDR

Philippines

Indonesia

Thailand

Vietnam

Malaysia

Cambodia

Singapore

0 20 40 60 80 100 120 140 160 180

49.5

67.0

111.2

126.2

144.4

147.1

148.8

155.1

158.1

Myanmar

Cambodia

Philippines

Vietnam

Thailand

Indonesia

Lao PDR

Malaysia

Singapore

0 5 10 15 20 25 30 35 40

1.0

2.8

3.1

6.0

8.5

11.7

13.4

14.6

35.5

Source: The Global Competitiveness Report 2015–2016, World Economic Forum

Mobile Subscriptions/100 pop., across ASEAN Fixed-Telephone Lines/100 pop., across ASEAN

21

ICT Indicators across ASEAN

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

BRU, 68.77

CMB, 9.00

IND, 17.14LAO, 14.26

MAL, 67.50

MYA, 2.10

PHI, 39.69

SIN, 82.00

THA, 34.89

VIE, 48.31

Philippines

Myanmar

Indonesia

Laos

Malaysia

Brunei

Cambodia

Vietnam

Thailand

Singapore

0 20 40 60 80 100 120 140

3.64

6.54

6.68

6.92

7.03

7.99

9.04

17.7

19.82

122.43

Percentage of Internet Users, 2000-2014 Household Speed Index (in Mbps)

Source: International Telecommunications Union, 2015 Sour

ce: O

okla

, May

201

5

22

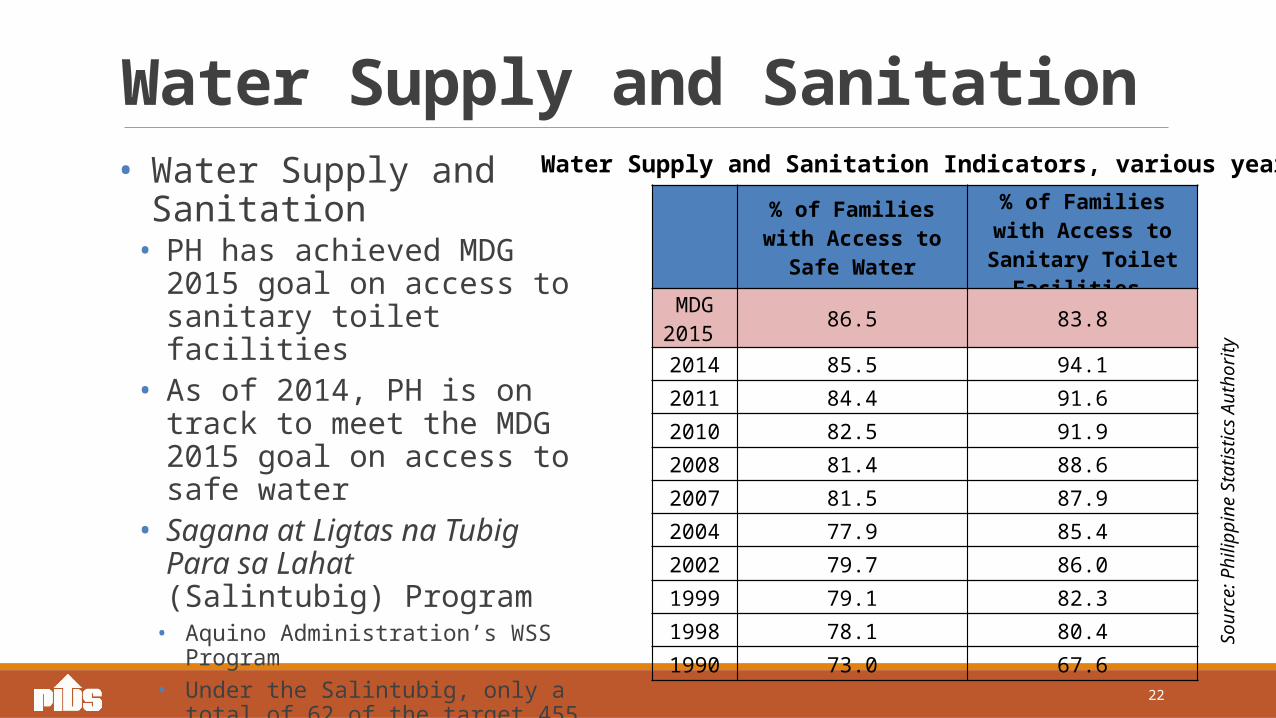

Water Supply and SanitationWater Supply and Sanitation Indicators, various years

Sour

ce: P

hilip

pine

Sta

tistic

s Aut

horit

y

% of Families with Access to Safe Water

% of Families with Access to Sanitary Toilet

Facilities

MDG 2015 86.5 83.8

2014 85.5 94.12011 84.4 91.62010 82.5 91.92008 81.4 88.62007 81.5 87.92004 77.9 85.42002 79.7 86.01999 79.1 82.31998 78.1 80.41990 73.0 67.6

• Water Supply and Sanitation• PH has achieved MDG 2015 goal

on access to sanitary toilet facilities

• As of 2014, PH is on track to meet the MDG 2015 goal on access to safe water

• Sagana at Ligtas na Tubig Para sa Lahat (Salintubig) Program

• Aquino Administration’s WSS Program• Under the Salintubig, only a total of 62 of

the target 455 municipalities have reportedly graduated as of June 2015.

23

Energy• Generation Mix

Source: DOE Database of Power Plants as of September 2015.

Dependable Capacity Installed Capacity

24

Energy• In a USAID study prepared by CATIF, electricity prices in the Philippines

are not competitive compared to selected ASEAN countries.

PHL SGP INA MAL THAPer kWh

Residential 0.3608 0.2523 0.1156 0.1302 0.2484Commercial 0.3727 0.2523 0.2447 0.2353 0.2869Low voltage Industrial 0.3021 0.2432 0.1999 0.2082 0.2765High voltage Industrial 0.2995 0.2183 0.1769 0.1894 0.2557

Conversion Factors for Local Currency UnitsUS dollars, average in 2011 43.31 1.26 8,770.43 3.06 30.49PPP$, 2011 24.79 1.03 6,565.87 1.9 17.42

Cross-peso, average in 2011 34.4567 0 14.1716 1.4219

Comparison of 2011 Electricity Tariffs after Adjusting for Price Differences (in 2011 PPP dollars)

Sour

ce: C

ATIF,

201

3

25

Energy• Based on the 2015-2016

World Economic Forum – Global Competitiveness Report, the Philippines ranks 89th among 140 countries in terms of quality of electricity.

• Philippines - among the bottom three in terms of quality of electricity supply

Source: WEF Global Competitiveness Report 2015-2016Note: Values are on a 1-to-7 scale, with 7 being the highest rating. Survey includes 140 countries. Brunei Darussalam is not included.

Quality of Electricity Supply, across ASEAN Countries

Myanmar

Cambodia

Philippines

Indonesia

Vietnam

Lao PDR

Thailand

Malaysia

Singapore

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

2.7

3.1

4.0

4.1

4.1

4.7

5.2

5.8

6.7

26

Role and contribution of the construction industry

27

Share of construction in GDP• On the production

side, largest sectoral share is from the Service Sector (57%), followed by the Industry Sector.

• In the Industry Sector, manufacturing is 23% of GDP, while the construction industry is 6% of GDP.

AGRI.FISHERY,FORESTRY, 9%

SERVICE SECTOR, 57%

Manufacturing, 23%

Construction, 6%Elec., Gas and Water

3% Mining & Quarrying, 1%

Share of GDP by Industrial Origin, 2015

Source: Philippine Statistics Authority, 2015

28

Capital Formation and Construction• On the expenditure side,

23% of the GDP can be attributed to Capital Formation. Since 2012, the share of Capital Formation in GDP has been increasing

• In 2015, capital formation increased by 13.6% compared to the 5.4% growth it registered in 2014

• Among the components of Capital Formation, construction remains second in terms of percentage share (9.3%) in 2015, next to Durable Equipment (11.9%)

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

23.5%

9.3%

11.9%

1.3%0.7%

Total Capital Formation ConstructionDurable Equipment Breeding Stock & Orchard Dev'tIntellectual Property Products

Capital Formation and its Sub-sectors, as Percent of GDP

Source: Philippine Statistics Authority

29

Public and Private Construction

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-10.6%

8.5%

-6.2%

-0.6%

3.6%

-0.7% -2.1%

7.7%

11.3%

4.2%

1.6%

17.5%

-8.4%

17.6%

11.0%

10.9%

8.4%

PUBLIC PRIVATETotal Construction (Growth Rates)

Value and Growth Rates of Private and Public Construction, 1999-2015

Source: Philippine Statistics Authority

• In terms of real values (at constant 2000 prices), total construction value has been increasing since 2011. However, the growth rates has been steadily decreasing. In 2015, construction has been down to 8.4% growth, from 10.9% the previous year.

• Private contribution to construction has been growing faster than public contribution. In 2015, growth rate of the private sector has been 4.3%, while the public sector’s contribution is only 4.1%.

2010 2011 2012 2013 2014 2015

Public (Growth

Rate)1.4% -11.6% 3.6% 3.5% 1.3% 4.1%

Private (Growth

Rate)16.1% 3.2% 14.0% 7.5% 9.6% 4.3%

Growth Rates of Public & Private Construction, 2010-2015

Source: Philippine Statistics Authority

30

Public and Private Construction

• The increase in the value of construction as percent of GDP is primarily driven by the private sector.

• Since 2011, the share of total value of construction as percent of GDP has been increasing. In 2011, it was 7.6%, and is not at 9.3% in 2015.

• The 9.3% share of GDP in 2015 is the highest in the last 15 years.

• The private sector has the larger share with 7.2% of the GDP in 2015, while public only has 2.1%.

• This has been the highest share of the private sector as percent of GDP since 1998.

• As for the public sector’s share, 2.1% is the highest since 2011.

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

3.6%2.9% 3.1% 2.9% 2.4% 2.2% 1.8% 1.8%

2.4% 2.3% 2.2% 2.6% 2.5%1.5% 1.6% 1.8% 1.8% 2.1%

7.2%

6.5% 6.7%6.0%

6.2% 6.2%6.0% 5.5%

5.1% 5.5% 5.6% 5.3%6.1%

6.1%6.7% 6.9% 7.3% 7.2%

10.9%

9.4%9.8%

8.9%8.6% 8.4%

7.9%7.3% 7.5%

7.8% 7.8% 7.9%

8.6%

7.6%

8.4%8.7%

9.1% 9.3%

PUBLIC (as % of GDP) PRIVATE (as % of GDP)GROSS VALUE IN CONSTRUCTION (as % of GDP)

Construction Growth Rates and Private vs Public Value in Construction, 1999-2015

31

Philippine Institute for Development Studies

Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas

Service through policy research

WEBSITE: www.pids.gov.ph

FACEBOOK: facebook.com/PIDS.PH

TWITTER: twitter.com/PIDS_PH

Thank you!