1 politics and monetary policy michael ehrmann and marcel fratzscher european central bank...

TRANSCRIPT

1

Politics and Monetary Policy

Michael Ehrmann and Marcel FratzscherEuropean Central Bank

Conference on Central Bank Communication, Decision-Making and Governance

Waterloo, 28/29 April 2009

The usual disclaimers apply.

2

“We have continuously asked and asked the European Central Bank to review its rates to reduce the euro-dollar exchange level. If this does not happen, I think we should aim to have a political committee with government representatives to work alongside the central bank”

What the paper is about

3

“We have continuously asked and asked the European Central Bank to review its rates to reduce the euro-dollar exchange level. If this does not happen, I think we should aim to have a political committee with government representatives to work alongside the central bank”

Silvio Berlusconi, 08 June 2004

What the paper is about

4

“We have continuously asked and asked the European Central Bank to review its rates to reduce the euro-dollar exchange level. If this does not happen, I think we should aim to have a political committee with government representatives to work alongside the central bank”

Silvio Berlusconi, 08 June 2004

Background:

– Exchange rate at 1.15, policy rates at 2%

– European elections on June 13, 2004

– Voting support for Forza Italia had just dropped by 5.8%, from a high of 33% in 2002Q1 to 23% in 2004Q1

– GDP growth, 2004Q1: 0.8% in Italy, 1.7% in euro area

What the paper is about

5

• Kydland and Prescott (1977), Barro and Gordon (1983): inflationary bias, time inconsistency if monetary policy run by governments

• Rogoff (1985): appoint a conservative central banker, with greater weight on price stability than government

• Alesina and Tabellini (2007, 2008): socially optimal vs actual delegation of tasks to bureaucrats

– Socially optimal to delegate tasks with time inconsistent preferences

– Actual delegation of tasks that are exposed to risk: shift blame

• Given these incentives, politicians are likely to put pressure on independent central banks, or criticise their actions

Introduction

6

• This paper analyses the political controversies for the ECB

– Is the ECB conservative in Rogoff’s sense?

– Additional disagreement due to different constituencies in a monetary union?

– Are politicians’ preferences time varying?

• Database containing politicians’ statements about the ECB’s monetary policy, covering 9 years and heads of governments plus all ministers of 12 countries

Introduction

7

• Politicians’ preferred interest rates substantially lower than actual rates

• ECB is conservative in Rogoff’s sense, i.e. politicians would like to put more emphasis on growth

• Bulk of controversies arises due to different constituencies

• Time variations matter: preference shift

– If national economic performance is weak

– If the public has generally little trust in the ECB

– Depending on the affiliation of parties in government

Results

8

• Literature review

• A model of politicians’ preferences

• Data, stylized facts

• What weights on price stability and growth?

• Time variations in politicians’ preferences

• Politicians’ desired interest rates

• Conclusions

Overview

9

• Normative aspects of delegation of tasks

– Intrinsic motivation differences between politicians and bureaucrats: Dewatripont, Jewitt and Tirole (1999), Maskin and Tirole (2001), Besley and Coate (2003), Schultz (2008)

– Socially optimal to delegate if time inconsistency and short-termism are an issue, or if tasks are technically complex; no delegation in case of uncertainty about social preferences, or if compensation of losers is important (Alesina and Tabellini 2007)

• Positive aspects of delegation of tasks (Alesina and Tabellini 2008; Epstein and O’Halloran 1999)

– Politicians decide on delegation, given their incentive structure

– Delegate risky tasks, attempt to shift blame with adverse outcomes, claim responsibility with positive outcomes

Literature review

10

• Empirical literature

– Is the Fed influenced by Congress? Role of monetary policy in political business cycles

• Yes: Alesina and Sachs (1988), Grier (1993), Abrams and Iossifov (2006), Hellerstein 2007)

• No: Wooley (1984), Faust and Irons (1999)

– Measurement of political pressure and its effects

• Havrilesky (1993): number of reports in Wall Street Journal about politicians arguing for more or less restrictive monetary policy; affects actual interest rates

• Maier, Sturm and de Haan (2002): no effect for Bundesbank

• Gersl (2006): no effect for Czech National Bank

• Maier and Bezoen (2004): index for ECB, until 02/2002

Literature review

11

• Based on politicians’ statements

– 20 October 2006: “German Economics Minister Michael Glos said Friday that the European Central Bank is in no hurry to raise interest rates from a German perspective, pointing to the country's low inflation rates.” Source: Dow Jones International News

– 01 February 1999: “German Finance Minister Oskar Lafontaine again hinted Monday at the desirability of an ECB rate cut to stimulate growth and employment in the euro-zone.” Source: Market News International

– 27 February 2007: “Austrian Chancellor Alfred Gusenbauer said the European Central Bank (ECB) might have to adapt its interest rate policy to match the current economic situation.” Source: Reuters News

A model of politicians’ preferences

12

• Preferred interest rates a function of inflation and growth in the euro area and the national economies

A model of politicians’ preferences

Pt

EAt

Ct

CPEAt

EAPEAt

Ct

CPEAt

EAPPPt yyyi )()( ,,,,

0;0;0;0 ,,,, CPEAPCPEAP

13

• Preferred interest rates a function of inflation and growth in the euro area and the national economies

• This need not be the actual interest rate; abstracting from a possible monetary policy rule, we model

A model of politicians’ preferences

Pt

EAt

Ct

CPEAt

EAPEAt

Ct

CPEAt

EAPPPt yyyi )()( ,,,,

0;0;0;0 ,,,, CPEAPCPEAP

actt

EAt

actEAt

actactactt yi

0;0 actact

14

• Preferred interest rates a function of inflation and growth in the euro area and the national economies

• This need not be the actual interest rate; abstracting from a possible monetary policy rule, we model

• Rogoff tells us that

A model of politicians’ preferences

Pt

EAt

Ct

CPEAt

EAPEAt

Ct

CPEAt

EAPPPt yyyi )()( ,,,,

0;0;0;0 ,,,, CPEAPCPEAP

actt

EAt

actEAt

actactactt yi

0;0 actact

EAP

EAP

act

act

,

,

15

• The interest rate gap is then

A model of politicians’ preferences

tEAt

Ct

CPEAt

EAPact

EAt

Ct

CPEAt

EAPactPactPt

actt

yyy

ii

)()(

)()()(,,

,,

16

• The interest rate gap is then

– Rogoff implies

– Additional weight on national variables implies

A model of politicians’ preferences

tEAt

Ct

CPEAt

EAPact

EAt

Ct

CPEAt

EAPactPactPt

actt

yyy

ii

)()(

)()()(,,

,,

0/0 ,, EAPactEAPact orand

0;0 ,, CPCP

17

• The interest rate gap is then

– Rogoff implies

– Additional weight on national variables implies

• Need to run a proxy regression due to unobservability of preferred interest rate

– assume that political pressure is increasing in the gap

A model of politicians’ preferences

tEAt

Ct

CPEAt

EAPact

EAt

Ct

CPEAt

EAPactPactPt

actt

yyy

ii

)()(

)()()(,,

,,

tEAt

Ct

EAt

EAt

Ct

EAtt yycycbbapp )()( 2121

0/0 ,, EAPactEAPact orand

0;0 ,, CPCP

18

• Time variations: preference shift in periods xt

A model of politicians’ preferences

Pttt

EAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAP

tEAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAPPPt

xxyyxyyyy

xxi

)()(

)()(,,,,,,

,,,,,,

19

• Time variations: preference shift in periods xt

– Preference shift towards growth, away from inflation

– Preference shift towards national variables

– What dominates for national inflation?

A model of politicians’ preferences

Pttt

EAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAP

tEAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAPPPt

xxyyxyyyy

xxi

)()(

)()(,,,,,,

,,,,,,

0;0 ,,,, xEAPxEAP

0,, xCP

?,, xCP

20

• Time variations: preference shift in periods xt

– Preference shift towards growth, away from inflation

– Preference shift towards national variables

– What dominates for national inflation?

• Again: estimated by means of proxy regression

A model of politicians’ preferences

Pttt

EAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAP

tEAt

Ct

xCPt

EAt

xEAPEAt

Ct

CPEAt

EAPPPt

xxyyxyyyy

xxi

)()(

)()(,,,,,,

,,,,,,

0;0 ,,,, xEAPxEAP

0,, xCP

?,, xCP

21

• Extract politicians’ statements

– Factiva (14,000 sources)

– 1999-2007

– Heads of government, ministers of 12 euro area countries

– Avoid double counting (in contrast to Havrilesky)

• Classify and code politicians’ statements

– Statements about future interest rate decisions and those about mandate, independence, past decisions, exchange rate

– Code as

Data, stylized facts: political pressure

rateshigherforcall

statementneutral

rateslowerforcall

Ct

1

0

1

22

• Issues

– Search in English; consistency check with other languages gave few differences (newswires important!)

– Exclusion of local government officials, opposition parties, lobby groups, trade unions, international institutions

– Classification and coding subjective

• Done independently according to content analysis (Holsti 1969)

• Rather plain language, coding comparatively uncontroversial

– An independent role of the media?

• Aggregation into 299 quarterly observations per political party, ranging from -1 to 11

Data, stylized facts: political pressure

23

– Strong asymmetry, only 5% of statements calling for higher rates

– Considerable cross-country variation

– National performance seems to matter, e.g. Spain

Data, stylized facts: political pressure

Lower rates Neutral Higher rates Total

Austria 28 2 0 30Belgium 42 4 0 46Spain 22 7 8 37Finland 1 3 0 4France 83 7 0 90Germany 92 8 2 102Greece 4 5 0 9Ireland 2 1 2 5Italy 24 2 1 27Luxembourg 11 8 0 19Netherlands 1 4 3 8Portugal 7 0 0 7

Total 317 51 16 384

Comments on future interest rate decisions

Country

24

– Time variations; high pressure in 2001-2003, 2005/2006

– Discussion since French presidential election campaign reflected in comments on mandate

Data, stylized facts: political pressure

23

45

inte

rest

rat

e

05

10

15

20

pol

itica

l pre

ssur

e

1999q3 2001q3 2003q3 2005q3 2007q3

.political pressure interest rate

25

– Economic performance matters: more pressure from low-growth countries

Data, stylized facts: political pressure 0

51

01

5

1999q3 2001q3 2003q3 2005q3 2007q3

.high GDP low GDP

26

Data: political economy variables

• Periods when politicians might shift preferences towards growth, or more likely to pressure ECB

– Pre-election period (Drazen 2000); dummy for election quarter

– Low voting support; rate of decline of voting support

– Low public trust in ECB; dummy equal one if share of respondents in Eurobarometer survey mistrusting the ECB is above sample mean

– Excessive deficit procedure; dummy when procedure in place

– Negative growth differential (Alesina and Cukierman 1990, Rogoff and Sibert 1988); dummy if national growth below euro area

– Left-wing party (Hibbs 1977, Powell and Whitten 1993, Swank 1993); dummy based on Chapel Hill Party Dataset 2002

27

Hypo-thesis

BenchmarkAll

commentsPre-2007

No fixed effects

Ordered probit

Negative binomial

Euro area macro variables:

t

EA b1>0 -0.526 -0.507 -0.454 -0.373 -0.309 -0.460*

y tEA c1<0 -0.143* -0.099 -0.184** -0.173** -0.151** -0.186***

Country-specific macro differences:

tC

tEA b2<0 -0.444*** -0.512*** -0.248 -0.482*** -0.386*** -0.476***

y tC -y t

EA c2<0 -0.073* -0.105** -0.081 -0.091*** -0.043* -0.161**

Party fixed effects Yes Yes Yes No Yes Yes

Observations 299 299 257 299 299 299

R-squared 0.27 0.28 0.29 0.12 0.14

– Larger desired weight on GDP growth

– Larger desired focus on national economy

– Robust to adding unemployment or the exchange rate

What weights on price stability and growth?

tzEAt

Ctz

EAt

EAt

Ctz

EAtztz yycycbbapp ,,

21,

21, )()(

28

What weights on price stability and growth?

– Larger desired weight on GDP growth

– Larger desired focus on national economy

– Robust to adding unemployment or the exchange rate

tzEAt

Ctz

EAt

EAt

Ctz

EAtztz yycycbbapp ,,

21,

21, )()(

Hypo-thesis

Benchmark All commentsNo fixed

effectsOrdered

probitIncidence of

commentsNegative binomial

Euro area macro variables:

t

EA b1>0 -0.526 -0.507 -0.373 -0.309 -0.157 -0.460*

y tEA c1<0 -0.143* -0.099 -0.173** -0.151** -0.211*** -0.186***

Country-specific macro differences:

tC

tEA b2<0 -0.444*** -0.512*** -0.482*** -0.386*** -0.326* -0.476***

y tC -y t

EA c2<0 -0.073* -0.105** -0.091*** -0.043* -0.023 -0.161**

Party fixed effects Yes Yes No Yes Yes Yes

Observations 299 299 299 299 299 299

R-squared 0.27 0.28 0.12 0.14 0.24

29

Time variations

– Preference shift • If national economy performs poorly

• If the public has generally little trust in the ECB

• Depending on affiliation of parties in government

tztztzEAt

Ctztz

EAt

EAt

Ctz

EAtt

EAt

Ctztz

EAt

EAt

Ctz

EAtztz dxxyycxycyycycxbxbbbapp ,,,,

4,

3,

21,

4,

3,

21, )()()()(

Hypo-thesis

Pre-election period

Low voting support

Low public trust in ECB

Excessive deficit

procedure

Negative growth

differential

Left-wing party

Political economy variables & interaction terms:

tEA * x t b3>0 1.132** -0.016 -0.550 -0.094 -0.350 0.018

y tEA * x t c3<0 -0.332 0.001 -0.080 -0.518* -0.062 -0.148

(t

C t

EA ) * x t b4=? 0.290 -0.005 0.038 0.016 -0.507* 0.216

(y tC -y t

EA ) * x t c4<0 0.139** 0.005 -0.344** -0.175 -0.235* -0.432**

x t d = 0 -1.874 0.035 1.203 1.061 1.553 -0.095

Party fixed effects Yes Yes Yes Yes Yes YesObservations 299 299 299 299 299 299R-squared 0.27 0.27 0.30 0.28 0.31 0.35

30

Time variations, robustness: negative binomial

– Broadly robust to using only calls for lower rates, all comments, country fixed effects, ordered probit model

tztztzEAt

Ctztz

EAt

EAt

Ctz

EAtt

EAt

Ctztz

EAt

EAt

Ctz

EAtztz dxxyycxycyycycxbxbbbapp ,,,,

4,

3,

21,

4,

3,

21, )()()()(

Hypo-thesis

Pre-election period

Low voting support

Low public trust in ECB

Excessive deficit

procedure

Negative growth

differential

Left-wing party

Political economy variables & interaction terms:

tEA * x t b3>0 1.927** 0.007 -0.410 0.310 -0.326 0.016

y tEA * x t c3<0 -0.461* 0.002 0.047 -0.225 0.081 -0.020

(t

C t

EA ) * x t b4=? 0.190 0.005 0.048 0.044 -0.235 0.182

(y tC -y t

EA ) * x t c4<0 0.268* 0.007 -0.307*** 0.025 -0.370* -0.267**

x t d = 0 -3.562* -0.013 0.706 -0.301 1.021 -0.170

Party fixed effects Yes Yes Yes Yes Yes Yes

Observations 299 299 299 299 299 299

31

• Extracting politicians’ preferred interest rates

– Assume

– Estimate preferred rate for all neutral speakers

– Use estimated parameters to predict preferred interest rates for the non-neutral speakers (assuming model constancy)

0 tactt

Pt ppifii

Politicians’ desired interest rates

Ptz

EAt

Czt

CPEAt

EAPEAt

Ctz

CPEAt

EAPPz

actt yyyi ,

,,,

,, )()(

32

Politicians’ desired interest rates

Ptz

EAt

Czt

CPEAt

EAPEAt

Ctz

CPEAt

EAPPz

actt yyyi ,

,,,

,, )()(

Hypothesis Benchmark

Euro area macro variables:

t

EA P,EA>0 0.518***

y tEA P,EA>0 0.437***

Country-specific macro differences:

tC

tEA P,C>0 0.327***

y tC -y t

EA P,C>0 -0.007

Const. 0.759*

Party fixed effects YesObservations 131R-squared 0.610

33

Politicians’ desired interest rates

• Preferred interest rates rise by

– 50 basis points in response to a 1% increase in euro area inflation

– 40 basis points in response to a 1% increase in euro area growth

– 30 basis points in response to a 1% increase in domestic inflation

34

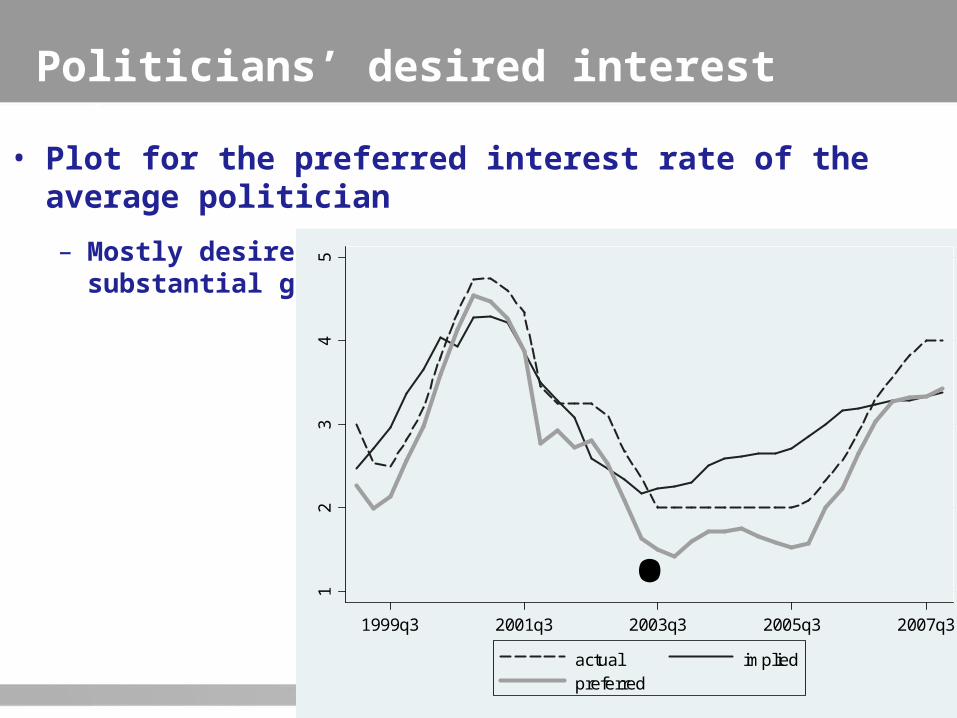

Politicians’ desired interest rates

• Plot for the preferred interest rate of the average politician

– Mostly desire for more accomodation, partially substantial gaps

12

34

5

1999q3 2001q3 2003q3 2005q3 2007q3

.actual impliedpreferred

35

Conclusions

• Politicians’ preferred interest rates substantially lower than actual rates

• ECB puts more emphasis on price stability than politicians, i.e. is a Rogoff-type of central bank

• Lots of controversy arises due to different constituencies

• Time variations in politicians’ preferences

• Independence of ECB important to shield it from

– Time varying demands by politicians

– National concerns of politicians