1. perfect competition: a model learning objectives 1.explain what economists mean by perfect...

TRANSCRIPT

1. PERFECT COMPETITION: A MODEL

Learning Objectives1. Explain what economists mean by

perfect competition.2. Identify the basic assumptions of

the model of perfect competition and explain why they imply price taking behavior.

• Perfect competition is a model of the market based on the assumption that a large number of firms produce identical goods consumed by a large number of buyers.

Market structure can range from perfect competition and one end of the continuum to

monopoly at the other.

Market structure can range from perfect competition and one end of the continuum to

monopoly at the other.

1.1 Assumptions of the Model

• Price takers are individuals or firms who must take the market price as given.

• Identical goods• A large number of buyers and sellers• Ease of entry and exit• Complete information

1.2 Perfect Competition and the Real World

• The perfectly competitive model has strong assumptions.

• When we use the model we assume market forces determine prices.

• We can understand most markets by applying the supply and demand model.

• With this framework we can see how competition affect firms, consumer, and markets.

2. OUTPUT DETERMINATION IN THE SHORT RUN

Learning Objectives1. Show graphically how an individual firm in a perfectly

competitive market can use total revenue and total cost curves or marginal revenue and marginal cost curves to determine the level of output that will maximize its economic profit.

2. Explain when a firm will shut down in the short run and when it will operate even if it is incurring economic losses.

3. Derive the firm’s supply curve from the firm’s marginal cost curve and the industry supply curve from the supply curves of individual firms.

2.1 Price and Revenue

S

D

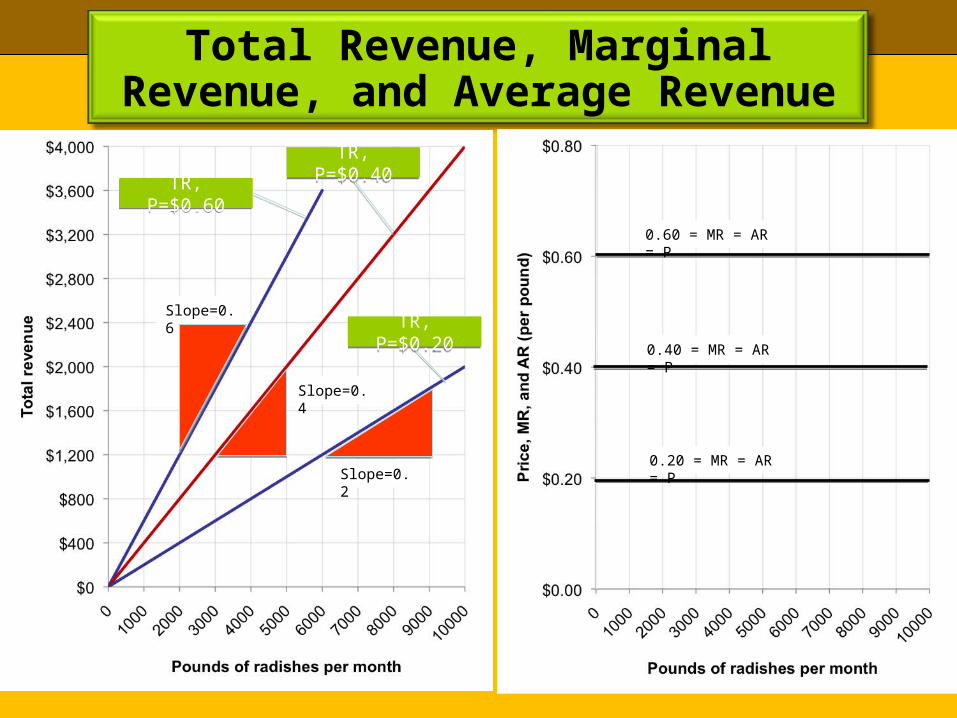

• Total revenue is a firm’s output multiplied by the price at which it sells that output.

EQUATION 2.1 QPTR

TR = $0.40*10 = $4TR = $0.40*10 = $4

Total Revenue, Marginal Revenue, and Average Revenue

Slope=0.4

Slope=0.2

TR, P=$0.60TR, P=$0.60

TR, P=$0.40TR, P=$0.40

TR, P=$0.20TR, P=$0.20

0.60 = MR = AR = P

0.40 = MR = AR = P

0.20 = MR = AR = P

Slope=0.6

Price, Marginal Revenue, and Average Revenue

• Marginal revenue is the increase in total revenue from a one-unit increase in quantity.

• Average revenue is total revenue divided by quantity.

EQUATION 2.1 PQ

QP

Q

TRAR

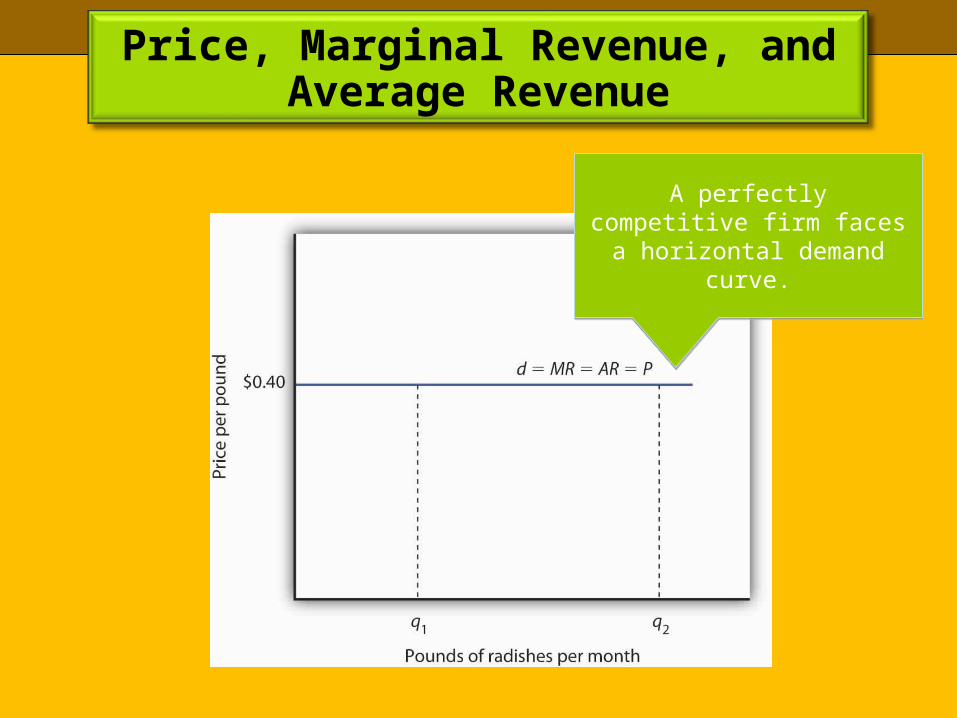

• Marginal revenue, price, and demand for the perfectly competitive firm

Price, Marginal Revenue, and Average Revenue

A perfectly competitive firm faces a horizontal demand

curve.

A perfectly competitive firm faces a horizontal demand

curve.

2.2 Economic Profit in the Short Run

1,50

0 6,70

0$9

38

1,742

2,680

Economic profit, which equals total revenue minus total costs, is

maximized at an output of 6,700 pounds of radishes per month

Economic profit, which equals total revenue minus total costs, is

maximized at an output of 6,700 pounds of radishes per month

Total CostTotal Cost

Total RevenueTotal Revenue

The slope of a line drawn tangent to the total cost curve at 6,700 pounds is

equal to 0.4, which is also equal to the slope of the total revenue curve. The

slope of the total cost curve is marginal cost; the slope of the total

revenue curve is marginal revenue.

The slope of a line drawn tangent to the total cost curve at 6,700 pounds is

equal to 0.4, which is also equal to the slope of the total revenue curve. The

slope of the total cost curve is marginal cost; the slope of the total

revenue curve is marginal revenue.

2.3 Applying the Marginal Decision Rule

• Economic profit per unit is the difference between price and average total cost.

Profit = $938Profit = $938

$0

.14

6,7

00

0.26

MC

MR

ATC

Producing to maximize economic profit.

Producing to maximize economic profit.

2.4 Economic Losses in the Short run

• Economic loss is the amount by which a firm’s total cost exceeds its total revenue.

Total loss = $222.20Total loss = $222.20

4,44

4

0.23

.018

0.14

MR1

MR2

ATC

MC

AVC

Producing to minimize economic loss.

Producing to minimize economic loss.

0.18

2.1 10

A fall in demandA fall in demand

Producing to maximize economic

profit.

Producing to maximize economic

profit.

2.4 Economic Losses in the Short run

• The shutdown point is the minimum level of average variable cost, which occurs at the intersection of the marginal cost curve and the average variable cost curve.

1,70

0

0.14

MR3

ATC

MC

AVC

Shutting down to minimize economic loss

Shutting down to minimize economic loss

2.5 Marginal Cost and Supply

MC

AVC

Industry supply

14 17 19 280 330 380

3. PERFECT COMPETITION IN THE LONG RUN

Learning Objectives1. Distinguish between economic profit and accounting profit. 2. Explain why in long-run equilibrium in a perfectly competitive

industry firms will earn zero economic profits.3. Describe the three possible effects on the costs of the factors of

production that expansion or contraction of a perfectly competitive industry may have and illustrate the resulting long-run industry supply curve in each case.

4. Explain why under perfection competition output prices will change by less than the change in production cost in the short run, but by the full amount of the change in production cost in the long run.

5. Explain the effect of a change in fixed cost on price and output in the short run and in the long run under perfect competition.

3.1 Economic Profit and Economic Loss

• Economic versus accounting concepts of profit and loss– Explicit costs are changes that must be paid for

factors of production such as labor and capital.– Accounting profit is profit computed using only

explicit costs.– Implicit cost is a cost that is included in the

economic concept of opportunity cost but that is not an explicit cost.

• The long run and zero economic profits

Eliminating Economic Profits in the Long Run

Profit = $938Profit = $938

6,7

00

0.26

MC

MR1

ATC

When firms enter supply shifts right and MR shifts down

When firms enter supply shifts right and MR shifts down

$0.22$0.22MR2

13

S1

S2

D

Eliminating Economic Losses in the Long Run

LossLoss

P1

MC

MR2

ATC

When firms exit supply shifts left and MR shifts up

When firms exit supply shifts left and MR shifts up

MR1

Q1

S2

S1

D

Q2

P1

P2P2

C1

q1 q2

3.1 Economic Profit and Economic Loss

• Entry, Exit, and Production Costs– Constant-cost industry are changes that must be

paid for factors of production such as labor and capital.

– Increasing-cost industry is profit computed using only explicit costs.

– Decreasing-cost industry is a cost that is included in the economic concept of opportunity cost but that is not an explicit cost.

– Long-run industry supply curve is a curve that relates the price of a good or service to the quantity produced after all long-run adjustments to a price change have been completed.

3.1 Economic Profit and Economic Loss

SCC

SIC

SDC

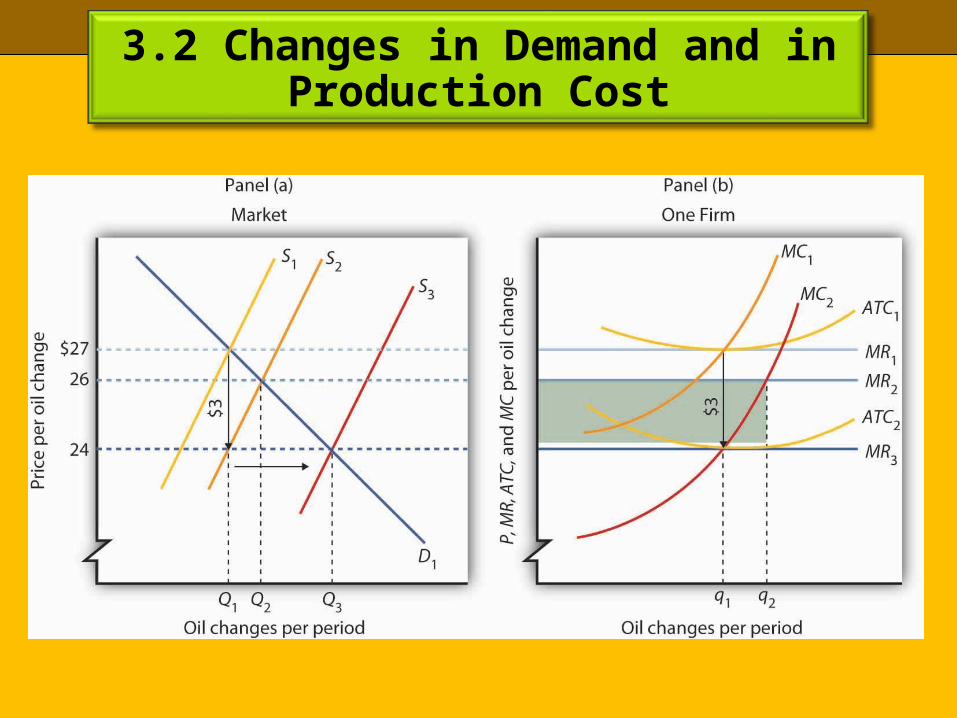

3.2 Changes in Demand and in Production Cost

$2.30

1.70C

B

A

D2

D1

S2

S1

Q3Q2Q1

$2.30

1.70

B?

A?

MCATC

MR2

MR1

q2q1

An increase in demand increases profitability which leads to an

increase in supply.

An increase in demand increases profitability which leads to an

increase in supply.

3.2 Changes in Demand and in Production Cost