1 nonresidential real estate © allen c. goodman, 2002

Post on 20-Dec-2015

217 views

TRANSCRIPT

1

Nonresidential Real Estate

© Allen C. Goodman, 2002

2

4-Quadrant Model

• Real estate is a useful linkage to land use theory and actual land usage.

• Demand for real estate (use of space) comes from occupiers of space. They are willing to rent the use of space.

• For firms, space is a factor of production.• For households space is a commodity• Supply of real estate comes from the construction

sector and depends on the price of those assets relative to the cost of replacing or constructing them.

3

Two explicit linkages

• 2 explicit linkages between the asset market and the property market– Rent levels in the property market are central in

determining the demand for real estate assets.– In the construction or development sector – if

construction increases and the supply of assets grows, not only are prices driven down in the asset market, but rents decline in the property market as well.

4

Four Quadrant Model

(1) R = 40 – (S/10E)

(2) C = (P – 200)/5

(3) S = 100 C, and

(4) P = R/i

(5) S = [E/(iE +2)][800 –4000i]

If E = 10 m; i = 0.5,

S = 240 sq.ft./worker 24 m sq.ft. of C/yr. Rents = $16/sq.ft. P = $320/sq.ft.

Rent R ($)

Stock S (sq. ft.)Price P ($)

Construction C (sq. ft.)

P = R/ 0.05

16

24

240

320

C = (P – 200)/5

R = 40 – (S/10E)

S = 100 C

5

Four Quadrant Model

Suppose falls from 0.05 to 0.04.

Q2 line rotates.

New equilibrium has to satisfy other conditions.

Price rises.

Stock increases.

Rent falls.

Trace it through.

Rent R ($)

Stock S (sq. ft.)Price P ($)

Construction C (sq. ft.)

P = R/ 0.05

C = (P – 200)/5

R = 40 – (S/10E)

S = 100 C

P = R/ 0.04

6

Demand Shift

(1) R = 40 + z – (S/10E)

(2) C = (P – 200)/5

(3) S = 100 C, and

(4) P = R/i

S >240 sq.ft./worker >24 m sq.ft. of C/yr. Rents > $16/sq.ft. P > $320/sq.ft.

Rent R ($)

Stock S (sq. ft.)Price P ($)

Construction C (sq. ft.)

P = R/ 0.05

16

24

240

320

C = (P – 200)/5

R = 40 – (S/10E)

S = 100 C

R = 40 + z – (S/10E)

7

Natural Vacancy Rates

• Comes from inventory theory

• What are inventories?

• Why do firms keep them?– Orders and production are not evenly matched.

• Why don’t they like to keep them?– Costs $ to hold them, guard them, maintain

them. $ could be used elsewhere.

8

How does this fit in for RE

• Landlords hold vacant space to satisfy needs of demanders.

• It’s optimal to hold a certain amount of vacant space for the same reason it’s optimal for merchants to hold inventory.

• What are landlords’ costs?– Property taxes– Interest on the mortgage– Insurance– Security

9

Suggested relationships

R = f (VA – VN); VA = actual; VN = natural

As (VA – VN), R .

Key part of the argument is that rents are slow to change. Why?Long term leases (typically 3 – 15 years on the

office market)

High transactions and search costs, particularly for buyers.

10

Supply is slow to adjust

Additions to office space stock are no more than 1 – 2% per year. If vacancy rate V = 0.05S, and C = 0.01S, then:

C/V = 0.20 sizable, but not instant.

11

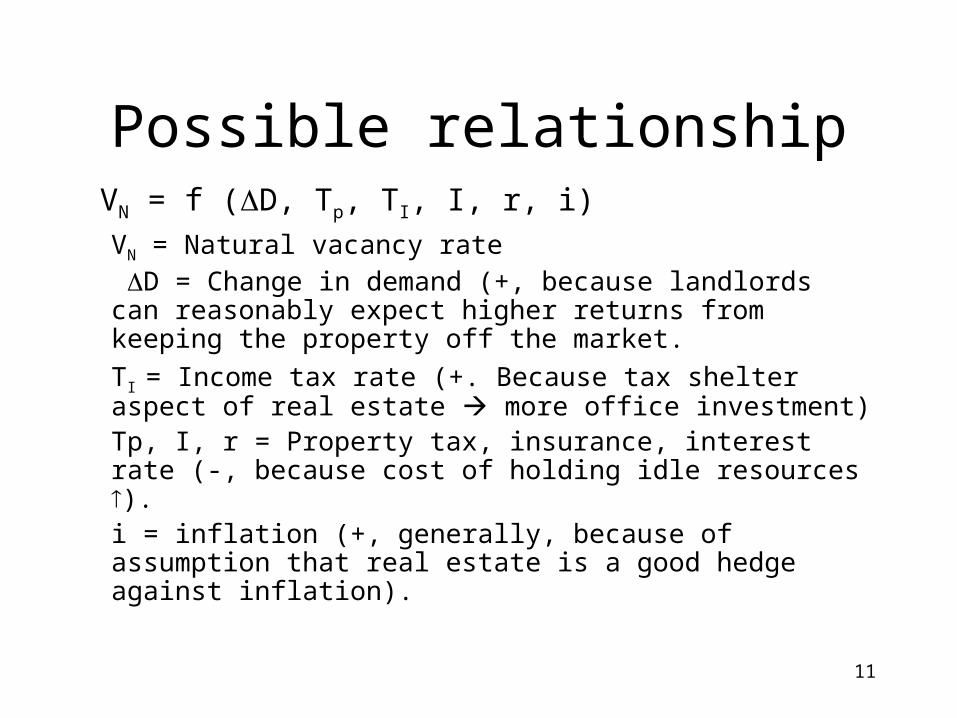

Possible relationship VN = f (D, Tp, TI, I, r, i)

VN = Natural vacancy rate

D = Change in demand (+, because landlords can reasonably expect higher returns from keeping the property off the market.

TI = Income tax rate (+. Because tax shelter aspect of real estate more office investment)Tp, I, r = Property tax, insurance, interest rate (-, because cost of holding idle resources ).i = inflation (+, generally, because of assumption that real estate is a good hedge against inflation).

12

Possible relationship Vacancy gap G

G = VN – VA.

Changes in rental rates, R, are functions of inflation i and the vacancy gap G.

R = f (i, G)

i nominal terms

G real terms

Let’s draw a picture

13

Vacancy Dynamics

Start at eq’m at which vacancy rate = natural rate.

This is consistent with a constant rate of construction, to replace buildings that wear out.

Change in real rent, R

Vacancy rates, VN and VA

Construction C as a ftn of S

R = f (G)

C = h(R)

VNVA =

S

S

+-

14

Vacancy Dynamics

Suppose we have a shift in QI of the 4-Quad diagram.

Decrease in V below the natural vacancy rate. This tends to push up real rent so R.

Increase in R will eventually lead to increases in construction.

Since construction rises above replacement level, stock eventually from S1 to S2.

Change in real rent, R

Vacancy rates, VN and VA

Construction C as a ftn of S

R = f (G)

C = h(R)

VNVNVA =

VA

G

S

S

15

Vacancy DynamicsSince construction rises

above replacement level, stock eventually from S1 to S2.

Vacancy rate and G , reducing growth of real rents.

Change in real rent, R

Vacancy rates, VN and VA

Construction C as a ftn of S

R = f (G)

C = h(R)

VNVNVA =

VA

G

S

SEventually VA VN, R

0.

New construction replacement percentage, but replacement level is associated with new, higher stock of space S2.

16

Vacancy Dynamics

What about negative demand shock.

Key point is that minimum construction is 0.

Change in real rent, R

Vacancy rates, VN and VA

Construction C as a ftn of S

R = f (G)

C = h(R)

VNVA =

S

S

VA

G

So, when demand , office mkt may be left w/ high vacancy and declining rents for a while.

Must wait for depreciation, and + growth in demand

17

We’ve concentrated on demand shocks

• Supply shocks– In mid to late 1980s cost of financing new

office construction decreased.– Interest rates fell.– Lots of tax shelters led to a lot of building,

possibly overbuilding.

18

Estimating VN

Does VN change or doesn’t it?

For a city,

R = b0 + b1E – b2V +

R = change in base rent/sq.ft.

E = change in operating expenses

V = actual vacancy rate

If we estimate this city by city then we can get a “natural” rate.

19

Estimating VN

R = b0 + b1E – b2V + R = change in base rent/sq.ft. E = change in operating expensesV = actual vacancy rate

Schilling et al. found rates varying from 1% (New York City) to over 20% (Kansas City)

Rate was low in Chicago, San Francisco, Atlanta

Rate was high in Portland, Spokane, Pittsburgh

WHY so different?Central tendency through 70s and

90s was 8 – 9%.

R

V

Set E = 0, orE = constant

Solve for Vsuch thatR = 0!

20

Bargaining Model

Wheaton/Torto use a “bargaining model.”Argue that rents are set in bargaining between

landlords and tenants.More tenants higher optimal rental rate by

landlords. Large amount of vacant space more tenants

opportunities and lower optimal rental rate. Here rental rates adjust rather than vacancy rates.

No role, really for new construction to influence rents.

21

Other critiques

• Distinction between vacant and abandoned properties is sometimes artificial. Vacant properties exert market pressure – abandoned ones do not. If some cities are more strict about tearing down abandoned buildings, their vacancy rates will look low, when they’re really not.

• Need to model shifts in the structure of relationships that produce VN. What if office tenants are moving to suburbs?

• Leases are becoming shorter and tenant turnover is becoming higher. This would tend to lower VN.

• Many metro areas have initiated slow-growth policies to limit office growth. Would tend to limit adjustment.

22

Recent Research – San Francisco FED Table 1

Natural Vacancy Rates, 2001.Q2

Estimated natural Actualvacancy rate vacancy rate

Boston 7.2 8.7

Houston 17.0 13.6

Los Angeles 12.2 14.1

Phoenix 15.0 16.9

Portland 10.9 9.9

Salt Lake City 13.3 15.3

San Francisco 7.9 10.3

Seattle 10.9 9.4http://www.frbsf.org/publications/economics/letter/2001/el2001-27.html John Krainer

23

Tauchen/Witte – JUE 1984

Inter-firm contacts depend on - density (how distributed)- actual number of firms

F identical firms, each with N transactions with each of the other firms.

Semi-net revenue (net of spatially invariant costs such as wages) is a function of the number of firms, F.

S-n rev = q = q (F), qF > 0; qFF < 0.

24

CBD is a square

Cost to a firm at (x, y) for a contact at (u, v) is

T (x, y, u, v) =

c {|x – u| + |y – v|}

Total transactions costs

v, y

u, x

(x0, y0)

(u0, v0)

,

( , ) ( , , , ) ( , )v u

T x y N t x y u v G u v dudv

G(u,v) is density function of firms

25

Cost of Providing Office Space

K = K (G); KG > 0, KGG > 0Basically, increased density lowers transactions costs, but raises cost of space.

Planning problem: Maximize net value of output

2

, ,

( ) ( , ) ( , ) [ ( , ]x y x y

V Fq F N T x y G x y dxdy K G x y dxdy LS L is opportunity cost of land.

Maximize with respect to F and G, subject to:

,

( , )x y

F G x y dxdy This is an adding up condition.

26

Using the calculus of variations

Q (F*) + F*qF(F*) – 2T*(x,y) – KG (G*(x,y) = 0.

Q (F*) + F*qF(F*) – (2T*(x,y) + KG (G*(x,y))= 0.

Mgl semi-net revenue

Mgl semi-net revenue

Mgl social costs

Mgl social costs

27

Does a market get us there?

Two equilibrium conditionsZero economic profit

(x, y) = q(F) – T(x,y) – R(x,y) = 0.Rent for office space = marginal cost of providing it.

R (x,y) = KG (G (x,y))Combined:

q(F) – T(x,y) – KG (G (x,y))= 0.

This is NOT the same as a planning optimum unless

FqF(F) = T(x,y).

28

What happened

FqF is external benefit to other firms from the new firm.

T (x,y) is the increased transactions costs to the other firms (remember there are N transactions per firm with EACH other firm.

Rent function is interesting.As you go further out, you’re

moving away from increasing number of firms.

Distance, x, y

Rent

0

R(x,y)