1 mÜnchener steuerrevisions- und treuhand gmbh steuerberatungsgesellschaft (tax consultants) ...

TRANSCRIPT

11

MÜNCHENER STEUERREVISIONS- UND TREUHAND GMBHMÜNCHENER STEUERREVISIONS- UND TREUHAND GMBH Steuerberatungsgesellschaft Steuerberatungsgesellschaft ((Tax ConsultantsTax Consultants))

MÜNCHENER WIRTSCHAFTSPRÜFUNGSGESELLSCHAFTMÜNCHENER WIRTSCHAFTSPRÜFUNGSGESELLSCHAFT ((Auditing CompanyAuditing Company))

SENFT & COLLEGENSENFT & COLLEGENRECHTSANWALTSGESELLSCHAFTRECHTSANWALTSGESELLSCHAFT MBH MBH ((LawfirmLawfirm))

22

Directive of German Federal Directive of German Federal

Ministry of Finance 16-04-2010:Ministry of Finance 16-04-2010:

The Application of

DTA to Partnerships

Petra Kanz, Lawyer / Tax AdvisorGothenborg 24-09-2010

33

Legal forms in GermanyLegal forms in Germany

Legal formLegal form numbernumber

one-man businessone-man business 2 039 100 2 039 100

partnershipspartnerships 373 440 373 440

corporationscorporations 519 382 519 382

other legal formsother legal forms 240 849 240 849

In total In total 3 172 771 3 172 771

Source: Statistisches Bundesamt 2006Source: Statistisches Bundesamt 2006

44

Legal form of Partnership (tax respect)Legal form of Partnership (tax respect)

In part. business „co-entrepreneurship“(§ 15 EStG): In part. business „co-entrepreneurship“(§ 15 EStG): oHGoHG, , KGKG, hybrid form: , hybrid form: GmbH & Co. KGGmbH & Co. KG

Tax Tax transparenttransparent

Exemption: Trade Tax + VAT on level of partnership!Exemption: Trade Tax + VAT on level of partnership!

Profits / LossesProfits / Losses separately assessed / p.r. allocated to separately assessed / p.r. allocated to partners;partners;

LossesLosses: unlimited carry forward but limited offset on : unlimited carry forward but limited offset on level of partnerslevel of partners

„„Sonderbetriebsvermögen“Sonderbetriebsvermögen“

55

German Specifics (1)German Specifics (1)

„SONDERBETRIEBSVERMOEGEN“„SONDERBETRIEBSVERMOEGEN“

Operational use giving distinction to private property Operational use giving distinction to private property no expense with tax effect but addition as no expense with tax effect but addition as operating revenue:operating revenue:

Management fees & partners‘ remunerationManagement fees & partners‘ remuneration (loan (loan interest, service fees, lease, royalties etc.)interest, service fees, lease, royalties etc.)

Partner owned private propertyPartner owned private property which is used for the which is used for the operating business of p‘ship is deemed specific business operating business of p‘ship is deemed specific business asset in tax respects.asset in tax respects.

66

German Specifics (2)German Specifics (2)„FICTION OF BUSINESS PARTNERSHIP“„FICTION OF BUSINESS PARTNERSHIP“

• Actually Actually asset managingasset managing partnership; partnership;

• Corporate entity (GmbH) is exclusive general Corporate entity (GmbH) is exclusive general partner + manager (§ 15 para.3 No. 2 EStG)partner + manager (§ 15 para.3 No. 2 EStG)

• Typically: Real Estate Typically: Real Estate GmbH & Co. KGGmbH & Co. KG

Trade or business co-entrepreneurshipTrade or business co-entrepreneurship by legal definitionby legal definition („(„gewerblich geprägte Personengesellschaftgewerblich geprägte Personengesellschaft“)“)

2nd legal definition: „2nd legal definition: „gewerblich infiziertegewerblich infizierte“ partnership“ partnership

77

German view: German view: Treaty Entitlement as to PartnershipsTreaty Entitlement as to Partnerships

Transparent PartnershipTransparent Partnership PE (Art 5 OECD-MC) PE (Art 5 OECD-MC) triggering trade or business income (Art. 7) on account triggering trade or business income (Art. 7) on account of its partners;of its partners;

Principle: Treaty entitled persons are the partners only. Treaty entitled persons are the partners only. If resident in a third country If resident in a third country respective DTA respective DTA

Intransparent PartnershipIntransparent Partnership - Fiction of treaty entitlement - Fiction of treaty entitlement ifif- defined as defined as corporate entitycorporate entity under DTA or foreign law under DTA or foreign law treaty benefits in favour of p‘ship: e.g. WHT cap applyingtreaty benefits in favour of p‘ship: e.g. WHT cap applying

88

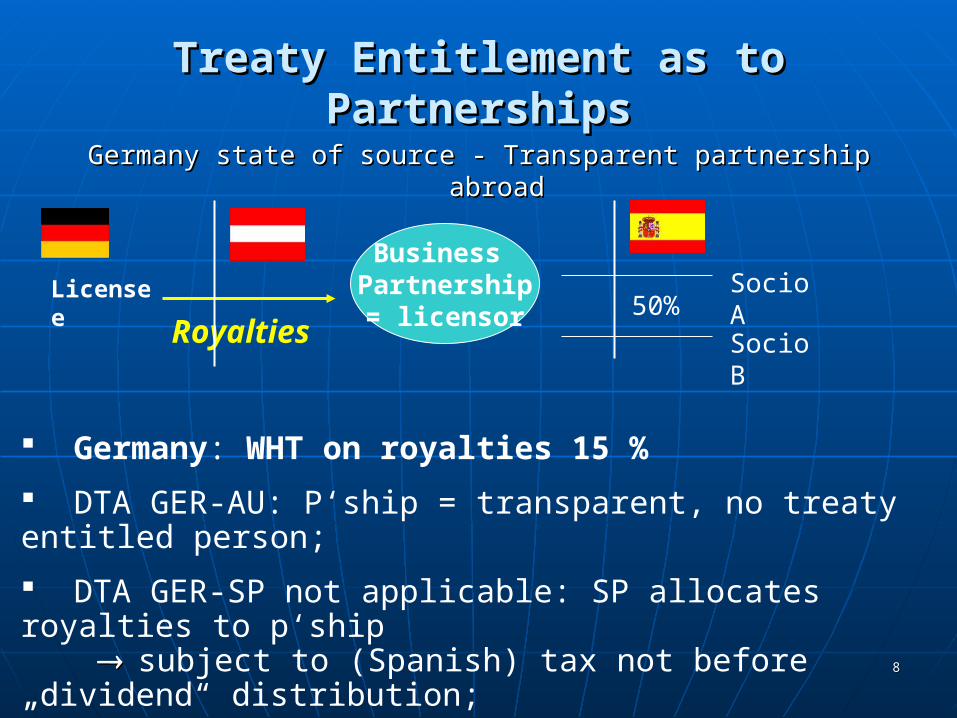

Treaty Entitlement as to PartnershipsTreaty Entitlement as to Partnerships

Germany state of source - Transparent partnership abroadGermany state of source - Transparent partnership abroad

Licensee

Business Partnership= licensor

Socio A

Socio BRoyalties50%

Germany: WHT on royalties 15 %

DTA GER-AU: P‘ship = transparent, no treaty entitled person;

DTA GER-SP not applicable: SP allocates royalties to p‘ship subject to (Spanish) tax not before „dividend“ distribution;

No reduction of WHT in Germany

99

(European) DTA :(European) DTA : profits allocated to a partner of a partnership profits allocated to a partner of a partnership

deemed trade or business income, Art. 7 OECD-MAdeemed trade or business income, Art. 7 OECD-MA

FranceFrance UKUK IrelandIreland LuxembourgLuxembourg The NetherlandsThe Netherlands AustriaAustria SwitzerlandSwitzerland

Source: BMF 16-04-2010, sec. 2.2.1.Source: BMF 16-04-2010, sec. 2.2.1.

1010

German view of DTA (1):German view of DTA (1):

Partnership-PE / Business Profits (Art. 7 OECD)Partnership-PE / Business Profits (Art. 7 OECD)

FEDERAL MINISTRY OF FINANCEFEDERAL MINISTRY OF FINANCE 16-04-2010 16-04-2010::

1) Originally trade or business income 1) Originally trade or business income plusplus2) 2) income income deemed trade or businessdeemed trade or business by definition by definition („ („gewerblich geprägtgewerblich geprägt“) “) i.e. asset managing GmbH & Co. KG i.e. asset managing GmbH & Co. KG

FEDERAL COURT OF FINANCEFEDERAL COURT OF FINANCE 28-04-2010 28-04-2010: :

Fiction Fiction notnot applying applying under DTA-Law, under DTA-Law, neither inbound nor outbound!neither inbound nor outbound!

1111

GERMAN FEDERAL COURT OF FINANCE GERMAN FEDERAL COURT OF FINANCE

- 28 April 2010 -- 28 April 2010 -..

U.S. partnership

Real estate fund German partner

Interest from capital investment of M&R reserves

USA: fund‘s option for business income potential US taxation of interest as „effectively connected income“;

Germany: Question whether tax exemption due to PE Prerogative or interest taxation in state of residence ?

Court Judgment ( BMF): Fiction of „business“ acc. German tax law not applying under DTA interest taxable in Germany

As the case may be, material issue of double taxation !

1212

German view of DTA (2):German view of DTA (2):

Partnership-PE / Business Profits (Art. 5, 7 OECD) Partnership-PE / Business Profits (Art. 5, 7 OECD)

Exercise of business operations in the state of seat Exercise of business operations in the state of seat of PE:of PE:

• Fixed placeFixed place of business; of business;

• Managing (holding) activityManaging (holding) activity

• Constitutional seat of general partner (GmbH), Constitutional seat of general partner (GmbH), not sufficient if: managing director resident not sufficient if: managing director resident abroad and no permanent office in PE state. abroad and no permanent office in PE state.

1313

BASIC OUTBOUND STRUCTURINGBASIC OUTBOUND STRUCTURING

Trade or business partnershipTrade or business partnership with its seat / with its seat / management abroad management abroad deemeddeemed a a foreignforeign PE PE of of (German) partner in terms of DTA;(German) partner in terms of DTA;

Exclusive (Exclusive (lowerlower) taxation in the state of PE ;) taxation in the state of PE ;

Repatriation of profitsRepatriation of profits to Germany exempt to Germany exempt from WHT or national minimum taxation from WHT or national minimum taxation (# dividends)(# dividends)

1414

Challenge: INBOUND PE STRUCTURINGChallenge: INBOUND PE STRUCTURING

CaseCase: :

EmigrationEmigration of a German shareholder of a German GmbH of a German shareholder of a German GmbH to a to a low-tax countrylow-tax country (issue of § 6 Foreign Transaction Tax Act) (issue of § 6 Foreign Transaction Tax Act)

Prior transfer of sharesPrior transfer of shares to a German GmbH & Co. KG asto a German GmbH & Co. KG as managing holding PE managing holding PE intended PE taxationintended PE taxation

Avoidance of expatriation taxation ??Avoidance of expatriation taxation ??

Federal Ministry of FinanceFederal Ministry of Finance: YES – on certain conditions: : YES – on certain conditions:

Issue „partnership holding“ subject to constant discussion Issue „partnership holding“ subject to constant discussion

1515

German view of DTA (3):German view of DTA (3):

Partnership-PE / Business Profits (Art. 5, 7 OECD) Partnership-PE / Business Profits (Art. 5, 7 OECD)

Condition: Condition: Functional attributionFunctional attribution of the asset the profits are of the asset the profits are resulting from to the PEresulting from to the PE

Additional requirements in case of Additional requirements in case of (managing) partnership (managing) partnership holdings:holdings:

Not only participation administration but: Not only participation administration but:

Functional, strategic or economic impact of participating Functional, strategic or economic impact of participating interest / shareholding in favour of partnership interest / shareholding in favour of partnership or substantial service relationsor substantial service relations

Federal Court of Finance (0Federal Court of Finance (07-12-2003 / 19-12-2007)7-12-2003 / 19-12-2007) International StandardsInternational Standards

1616

OUTBOUND SITUATIONOUTBOUND SITUATIONLimitation of PE PrerogativeLimitation of PE Prerogative

PrinciplePrinciple: :

ExemptionExemption of foreign PE profits from taxation in Germany as state of of foreign PE profits from taxation in Germany as state of partners‘ residence (but progression) partners‘ residence (but progression)

Unless case ofUnless case of::

• Activity test in DTAActivity test in DTA: if passive : if passive profit taxable in state of profit taxable in state of residenceresidence ((recently signedrecently signed DTA UK); DTA UK);

• Switch-over / subject-to-tax clause in DTASwitch-over / subject-to-tax clause in DTA::

• Unilateral Switch-over rulingUnilateral Switch-over ruling (§ 50d para. 9 EStG), in particular (§ 50d para. 9 EStG), in particular case of case of qualification conflictqualification conflict

► ► change to crediting methodchange to crediting method ! !

1717

Qualification Conflicts:Qualification Conflicts:Trouble shooting from German viewTrouble shooting from German view

Case of Case of double taxationdouble taxation:: BMF: State of residence is bound to qualification of BMF: State of residence is bound to qualification of state of source, i.e. responsible to provide for release;state of source, i.e. responsible to provide for release;

Case of Case of zero-taxationzero-taxation:: Germany as state of residence: § 50d para.9 EStG Germany as state of residence: § 50d para.9 EStG (unilateral switch-over) (unilateral switch-over) change of method from exemption to crediting change of method from exemption to crediting

1818

UNILATERAL SWITCH-OVER CLAUSEUNILATERAL SWITCH-OVER CLAUSE

§ 50d para. 9 EStG§ 50d para. 9 EStG

((possibly subj. to constitutional ban on retroactive effectpossibly subj. to constitutional ban on retroactive effect))

„Partner“Deutschmann

State B = PE

royalties paid by licensees

State of Source= C

Licensee

► Non-resident tax liability rules in B: Royalties from State of Source C tax exempted ►Subject to German tax: § 50 d para. 9 No. 2 EStG

Business Patent Partnership

1919

Negative Qualification Conflict (1)Negative Qualification Conflict (1)

OUTBOUNDOUTBOUND

Trade/Business Partnership

(no tax subject)

- car dealing -

German perception:

- PE prerogative business income (no interest Art. 11 OECD);

- Taxation in PE state;- If actually no taxation in PE state switch-over acc. 50d IX

Bridge financing; customers paying interest

Source State view: INTEREST (Art 11 OECD)

German view: BUSINESS PROFITS ?

Germany = State of Residence

2020

Constant dispute: „Sondervergütungen“Constant dispute: „Sondervergütungen“

Specific Feature under German Tax LawSpecific Feature under German Tax Law (see chart 5 - similar in Europe: Austria, Switzerland)(see chart 5 - similar in Europe: Austria, Switzerland)

§ 50d para. 10 EStG affecting DTA Law ? § 50d para. 10 EStG affecting DTA Law ? Business Income by definition Business Income by definition

Application challenged by Application challenged by German Jurisdiction !!German Jurisdiction !!

Treaty Override; inbound: rule coming to nothing Treaty Override; inbound: rule coming to nothing

2121

„„Sondervergütungen“ Sondervergütungen“ Negative Qualification Conflict Negative Qualification Conflict

OUTBOUNDOUTBOUND

Partner

Trade or Business

Partnership

Loan

German perception:

- Interest = business profit acc. national tax law, impact on DTA: § 50d para.10 EStG - Principle: Taxation in PE state;- If actually no taxation in PE state no obligation of state of residence to stick to exemption method switch-over acc. DTA or § 50 d para. 9 EStG

PE State view: INTEREST Art. 11 OECD

German view: BUSINESS PROFIT

Foreign State

Interest

2222

„„Sondervergütungen“ Sondervergütungen“ Positive Qualification ConflictPositive Qualification Conflict

INBOUNDINBOUND

Foreign Partner

German

Business

Partnership

Loan

Foreign state of residence: Taxation of worldwide income = interest, 11 OECDForeign state of residence: Taxation of worldwide income = interest, 11 OECD

GermanyGermany: : § 50d para 10 EStG§ 50d para 10 EStG: : DTA impact of German legal fiction DTA impact of German legal fiction

„business profit“ „business profit“ allocation to German PE = taxing power allocation to German PE = taxing power;;

Foreign state of residence is responsible to clear double-taxationForeign state of residence is responsible to clear double-taxation

BUTBUT: : Appeals pendingAppeals pending at Federal Court of Finance (Treaty Override?) at Federal Court of Finance (Treaty Override?)

Interest

2323

FOREIGN P.E. LOSSESFOREIGN P.E. LOSSES

German Federal Court of Finance 09-06-2010German Federal Court of Finance 09-06-2010

PrinciplePrinciple: Germany has : Germany has no taxing rightno taxing right with respect to with respect to losseslosses which have been generated in a which have been generated in a foreign ‹French› Permanentforeign ‹French› Permanent Establishment operated by an enterprise resident in Establishment operated by an enterprise resident in Germany Germany (= permanent jurisdiction in line with general PE principles).(= permanent jurisdiction in line with general PE principles).

ExceptionException:: Possible consideration of losses in Germany due Possible consideration of losses in Germany due to EC Law as far as the German taxpayer furnishs proof that to EC Law as far as the German taxpayer furnishs proof that the the losses definitely can not be used in the state of sourcelosses definitely can not be used in the state of source

time limit of loss carryforward pursuant to foreign law. time limit of loss carryforward pursuant to foreign law.

(Principle of „Final Losses“, EU-CoJ 15-05-2008 – Lidl/Belgium)(Principle of „Final Losses“, EU-CoJ 15-05-2008 – Lidl/Belgium)

2424

Participation interest of German partners in foreign Participation interest of German partners in foreign trade or business partnership:trade or business partnership:

Assessment process in GermanyAssessment process in Germany

BasicallyBasically: : Exemption methodExemption method with with progressionprogression

Uniform and separate assessmentUniform and separate assessment of the shares in profits allocated to of the shares in profits allocated to German partners;German partners;

Great Great administrative effortadministrative effort, crossborder cooperation with tax advisors;, crossborder cooperation with tax advisors;

Federal Central Tax Office (Bundeszentralamt/Steuern) collecting and Federal Central Tax Office (Bundeszentralamt/Steuern) collecting and

providing information through offical channels providing information through offical channels

(„IZA“= („IZA“= information centerinformation center for tax relevant foreign relations). for tax relevant foreign relations).

Müller

Huber

Maier

Foreign PE / Fund