1 martin goldberg, citigroup - advanced stress testing 9 nov 2006 stress testing for market risk...

TRANSCRIPT

1 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Stress Testingfor Market Risk

Advanced Stress Testing TechniquesRisk Training

New York, Nov 9, 2006

Martin GoldbergHead of Model Validation

Risk ArchitectureCitigroup

The analysis and conclusions set forth are those of the authors. Citigroup is not responsible for any statement or conclusion herein, and opinions or theories presented herein do not necessarily reflect the position of the institution.

2 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

3 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

4 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

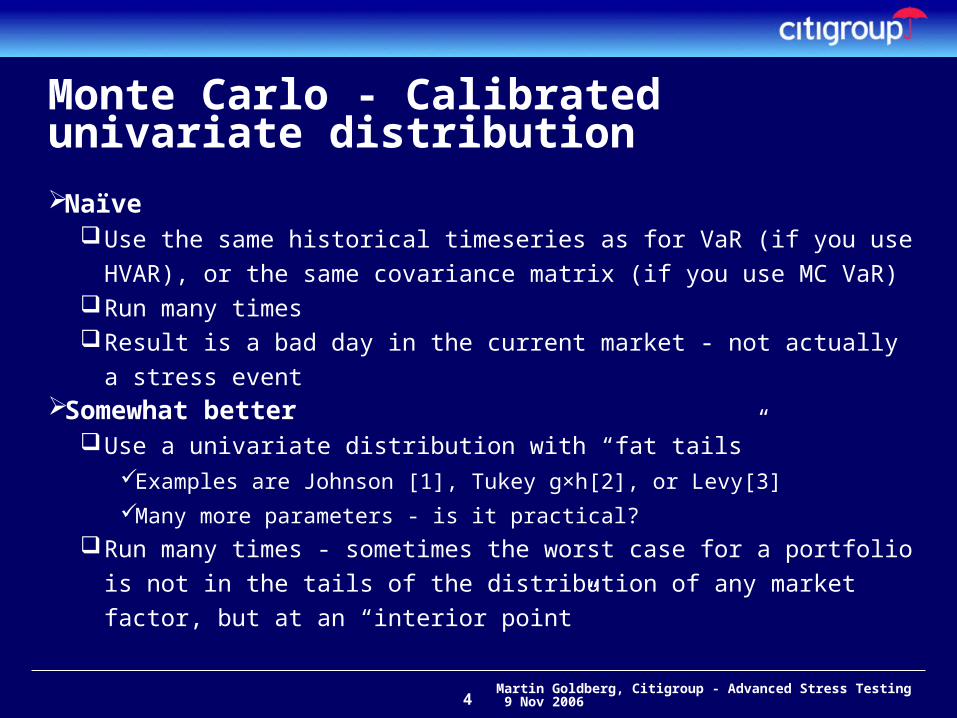

Monte Carlo - Calibrated univariate distributionNaïve

Use the same historical timeseries as for VaR (if you use HVAR), or the same covariance matrix (if you use MC VaR)

Run many times Result is a bad day in the current market - not actually a stress

eventSomewhat better

Use a univariate distribution with “fat tails”Examples are Johnson [1], Tukey g×h[2], or Levy[3]Many more parameters - is it practical?

Run many times - sometimes the worst case for a portfolio is not in the tails of the distribution of any market factor, but at an “interior point”

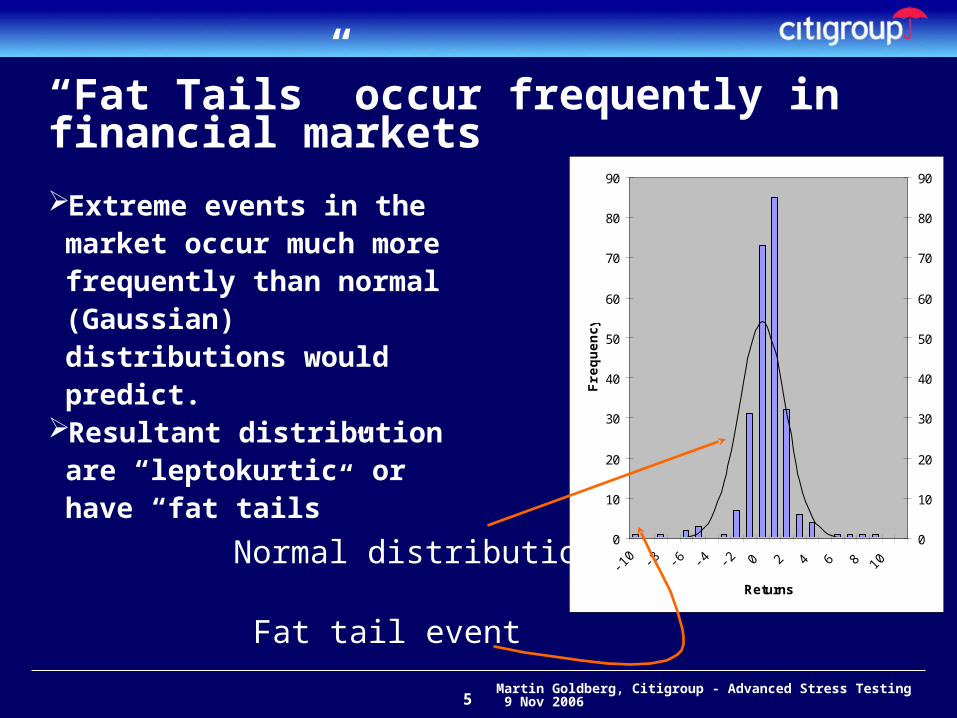

5 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

“Fat Tails” occur frequently in financial markets

Extreme events in the market occur much more frequently than normal (Gaussian) distributions would predict.

Resultant distribution are “leptokurtic” or have “fat tails”

0

10

20

30

40

50

60

70

80

90

ReturnsF

req

uen

cy

0

10

20

30

40

50

60

70

80

90

Fat tail event

Normal distribution

6 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

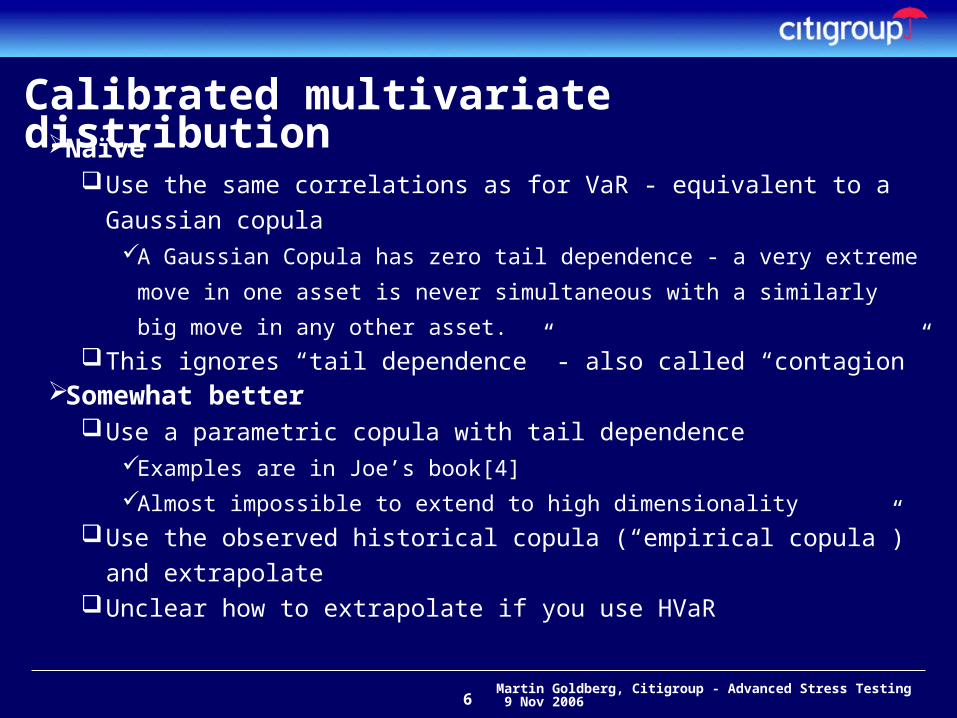

Calibrated multivariate distributionNaïve

Use the same correlations as for VaR - equivalent to a Gaussian copula

A Gaussian Copula has zero tail dependence - a very extreme

move in one asset is never simultaneous with a similarly big move

in any other asset.This ignores “tail dependence” - also called “contagion”

Somewhat betterUse a parametric copula with tail dependence

Examples are in Joe’s book[4]Almost impossible to extend to high dimensionality

Use the observed historical copula (“empirical copula”) and extrapolate

Unclear how to extrapolate if you use HVaR

7 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Joint market moves can lead to extreme $$$ losses

-6

0

6

6 5 4 3 2 1 0 -1 -2 -3 -4 -5 -6

-1,500,000-1,000,000

-500,0000

500,0001,000,0001,500,0002,000,0002,500,0003,000,000

P&L

Vol

FX

8 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

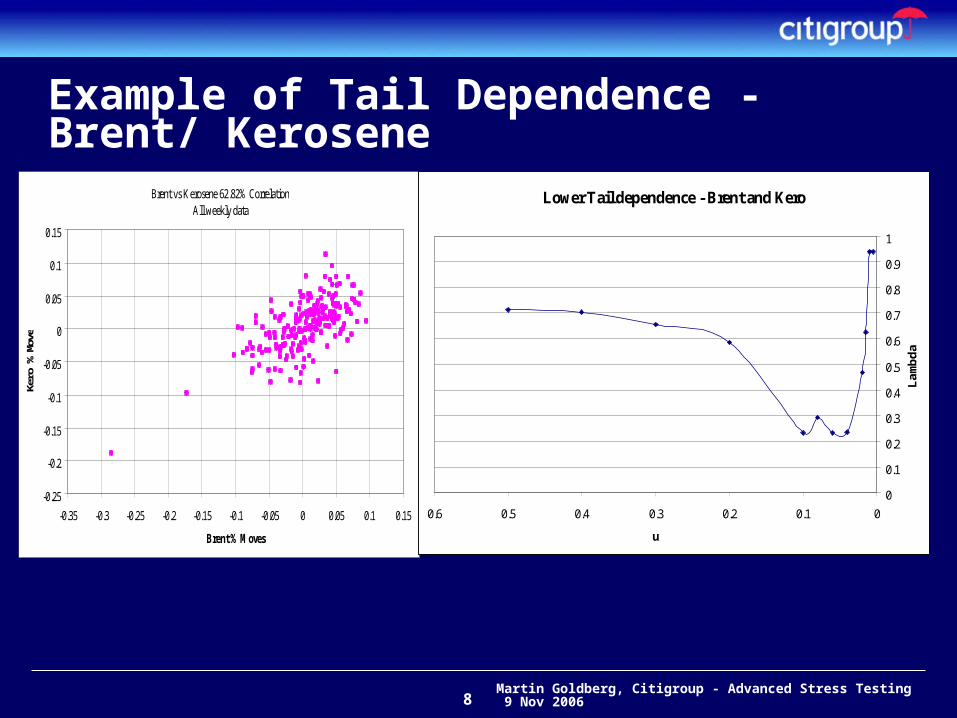

Example of Tail Dependence - Brent/ Kerosene

Brent vs Kerosene 62.82% CorrelationAll weekly data

-0.25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

-0.35 -0.3 -0.25 -0.2 -0.15 -0.1 -0.05 0 0.05 0.1 0.15

Brent % Moves

Ker

o %

Mov

es

Lower Tail dependence - Brent and Kero

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

00.10.20.30.40.50.6

u

Lam

bda

9 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Shortcomings of using a calibrated MC

If the assumed functional form is too simple, there are no stress events generated, or only unrealistic ones

If you add parameters, calibration becomes impractical

The past may not be a good predictor of future stress eventsStationarity is unlikely for extreme moves

If this could be done analytically by even a roomful of Nobel Prize winners, using calibrated MC, then LTCM would still be a powerhouse

10 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

11 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Named Scenarios - Historical

Historical means that we look at the impact of past events if they happened again today. However, it needs careful application:Relative vs. absolute changesStructural changes in financial environment (e.g. EUR

convergence)New markets

Typically, named historical scenarios might include US Stock Crash of 1987Russian Default

The selection should be appropriate to your portfolio

12 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Named Scenarios - Hypothetical

Hypothetical means that we propose scenarios that have not necessarily occurred in the past.

Needs careful construction.Might help to involve economists, traders, etc. in constructing plausible but unlikely scenarios

Examples (my own ideas - I have no idea if anyone uses these)US Congress can’t pass budget - US defaultsChina invades Taiwan“Mr Fusion” - free electricity

Be sure to include knock-on effects on all other marketsHistorical correlations are irrelevant here

13 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

14 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Stressed Distributions Rather than specify the change in each asset for scenarios, this involves “tweaking” the regular VaR scenario generatorHVaR

Exaggerate the size of selected day’s (or all days’) changesScaling need not be uniform across assetsDo for as many sets of tweaks as desired

MC VaRExaggerate selected volatilites as desiredChange correlations, but must preserve non-negative definite matrix

Run VaR engine on this stressed datasetAdvantage: Easy to implementDisadvantage: Difficult to create many plausible but novel stress scenarios with appropriate contagion

15 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager EstimatesCommunicating results

16 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Contagion Stress

In extreme events, the concept of correlation is as misleading as trying to use volatilities for these sudden jumps and regime shifts

Historical relationships may not be relevant in stress eventsDo not use historical covariance as a proxy for contagion

estimatesCrashes/Skyrocketing in one asset might be contagious to other assets (“Tail dependence”) anti-contagious (“flight to quality”), or unexpectedly irrelevant (“circuit breakers”)

Assessing these changes in relationships is more an art than a science

17 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Concentration StressA different but important kind of stress test is when liquidity changes either alone or simultaneously with price jumps

If you have a large exposure that suddenly becomes illiquid, there may be no meaningful price, but your capital is in effect frozen

A recent concentration stress example is the downfall of Amaranth. They kept buying the same futures contract as the price

went up, but the price was only going up due to their buying. What percent of the liquid float of any given asset does your firm hold?

If you are very long (short) one strategy, what happens if that one collapses?

18 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

19 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

How stressful of a stress do you use?Although much of stress scenario construction is subjective, there are usually corporate guidelines on what they mean by a stress event. Value at Risk is by definition a 99% worst ten-day eventBasel 2 looks at 99.9% worst one-year eventsAA firms such as Citigroup and JPMorganChase

nominally set economic capital as being large enough to withstand 99.97% worst one-year stress losses

The worst year in a thousand is very bad. Stress events of this magnitude might involve revolutions, global political upheavals, and such. No corporation has lasted 10,000 years, or even 1,000.

20 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

How stressful of a stress do you really use?Often, what the guidelines really mean is that you look at the realized volatility in the recent past, assume it is a stationary lognormal or Gaussian pdf, and scale it up accordingly.

This is a difficult question to ask the Policy Committee, but usually someone can indicate what level of stress is appropriate Ask “them” if they really mean:

Same stress as the crash of 1987Ten times worsePrivate ownership of assets is outlawed

The various scenarios should be roughly of equal severity so each of them is a meaningful exercise

21 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

22 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Setting Economic CapitalEconomic capital is defined as the value of assets your firm needs to withstand a specified level of stress losses and still avoid bankruptcy.

It could beMax(VaR*multiplier, worst stress test result)Average(VaR*multiplier, average stress test result)Etc.Something even more clever

This means that the stress scenarios have to be comparable in magnitude so that it is not clear which scenario will dominate next time.

23 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

24 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Combining Stress Tests, VaR, and Risk Manager EstimatesIn some firms, the risk managers periodically give a subjective estimate of how risky their business is, in terms roughly comparable to a narrowly targeted stress test.

When scaling VaR multipliers, stress tests, and RM estimates to be aggregatable, part of the art form is to not punish desks for hedging against shocks. It may help to compare the impact on random portfolios of the desk’s asset classes rather than on the actual hedged desk holdings, to ensure fairness.

25 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Outline

Types of Stress TestingMonte Carlo with calibrated distributionNamed scenarios

Historical eventsHypothetical events

Stressed DistributionContagion and Concentration

Quantile selectionUse in setting Economic CapitalCombining Stress Tests, VaR, and Risk Manager Estimates

Communicating results

26 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Communicating results

Part of the stressing process is to try to safeguard against desks gaming the specifics of the scenarios, so some secrecy may be desirable.

Part of the process is analyzing the results to point out weak areas, inadvertent side bets, and helping to decide where extra hedging or diversification might be warranted. This is where the process adds the most value.

Senior management, the desks, and the regulators all may have a keen interest in some or all of the results, presented in some digestible form - this too is an art.

27 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

Conclusions

Stress testing is not easyFormulaic approaches are not optimalThe past may not be a good proxy for the future

Decide what level of stress to aim forUse multiple scenarios and kinds of stress test, but make them comparable in stressfulness

Be creative in designing, and get economists and research involved in designing the tests

Know your audience

28 Martin Goldberg, Citigroup - Advanced Stress Testing 9 Nov 2006

References

1. Johnson NL, Kotz S (1970), Distributions in Statistics: Continuous Univariate Distributions

- 1, John Wiley & Sons, NY

2. http://fic.wharton.upenn.edu/fic/papers/02/0225.pdf

and http://fic.wharton.upenn.edu/fic/papers/02/0226.pdf

3. http://en.wikipedia.org/wiki/Levy_distribution

4. H. Joe, “Multivariate Models and Dependence Concepts” Chapman&Hall, 1997