1 “macroeconomic implications of demographic developments in the euro area” angela maddaloni,...

TRANSCRIPT

1

““Macroeconomic implications Macroeconomic implications of demographic developments of demographic developments

in the euro area”in the euro area”

Angela Maddaloni, Alberto Musso, Philipp Angela Maddaloni, Alberto Musso, Philipp Rother, Thomas Westermann, Melanie Ward-Rother, Thomas Westermann, Melanie Ward-

WarmedingerWarmedinger

13th Economic Conference, Dubrovnik, 28 June 2007

Disclaimer: Any views expressed are only the author’s own and do not necessarily reflect the views of the ECB or the Eurosystem

2

The current situation

From The Economist, 14 June 2007:

“…Europe is fast becoming a barren, ageing, enfeebled place. Vast numbers of old people, [..] will be looked after, or neglected, by too few economically active adults, supplemented by restless crowds of migrants. The combination of low fertility, longer life and mass immigration will put intolerable pressure on public health, pensions and social services, leading (probably) to upheaval.”

Maybe this looks a bit gloomy, but…

3

The current situation

Available projections suggest that all Western countries face the prospect of population ageing

The problem is even more pronounced in the euro area, although there are considerable differences across countries concerning the pace of ageing

Important consequences for economic growth, labour markets, public finances and possibly financial markets

4

Overview

Look at the impact of population ageing for:

Economic growth

Labour markets

Public finances

Financial markets

5

Impact on growth - demographic projections

Notwithstanding the high uncertainty surrounding population projections, working age population growth is projected to turn negative after 2010

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1950-55 1960-65 1970-75 1980-85 1990-95 2000-05 2010-15 2020-25 2030-35 2040-45

euro area

United States

working age population growth

6

Impact on growth - demographic projections

Compared to the US, euro area dependency ratio is growing muchfaster. After 2050 every third person will be older than 64

0

5

10

15

20

25

30

35

40

45

50

55

60

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

euro area

United States

old age dependency ratio

7

Impact on growth – demographic projections

The net migration rate is expected to fall up to 2010 and thereafter to stabilise in the euro area

1

2

3

4

5

1995-00 2010-15 2025-30 2040-45

United States

euro area

Net migration rate (1,000 population)

8

Impact on growth - backward

In the euro area the contribution of demographic factors to growth decreased since 1980, reflecting increasing dependency ratio and a decline in labour productivity linked to ageing

Euro area growth accounting

-2

-1

01

2

3

45

6

7

1965 1970 1975 1980 1985 1990 1995 2000

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

9

Impact on growth - backward

Working age population growth contributed to real GDP growthin the US more than twice than in the euro area

US Growth Accounting

-2-101234567

1965 1970 1975 1980 1985 1990 1995 2000

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

10

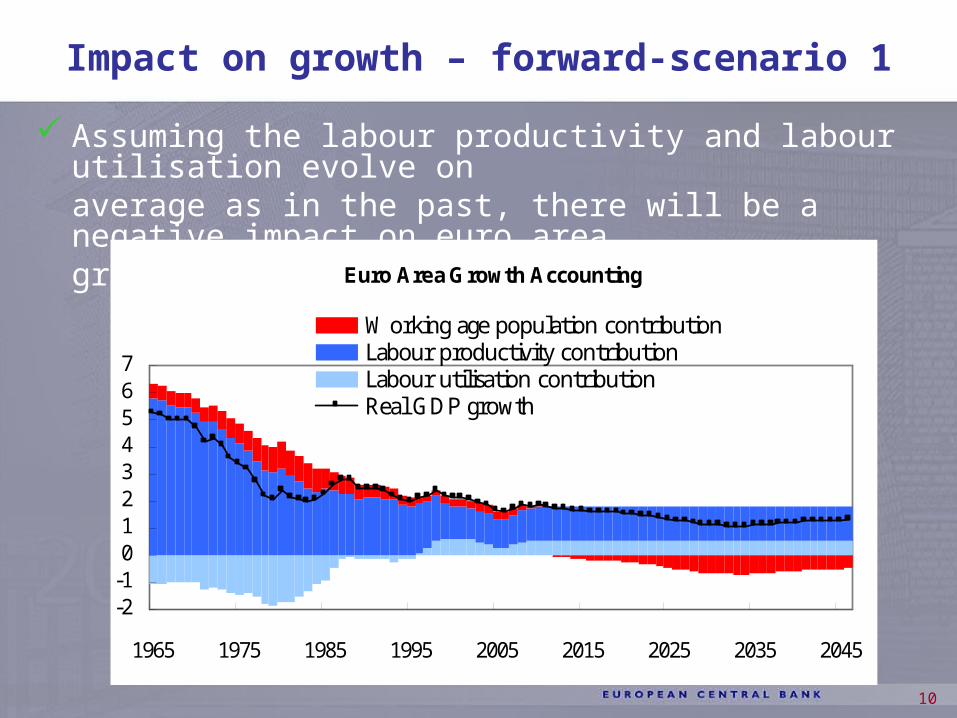

Impact on growth – forward-scenario 1

Assuming the labour productivity and labour utilisation evolve onaverage as in the past, there will be a negative impact on euro areagrowth

Euro Area Growth Accounting

-2-101234567

1965 1975 1985 1995 2005 2015 2025 2035 2045

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

11

Impact on growth – forward-scenario 1

Same scenario for the US…

US Growth Accounting

-2-101234567

1965 1975 1985 1995 2005 2015 2025 2035 2045

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

12

Impact on growth – forward-scenario 2

Assuming the labour productivity and labour utilisation grow in line with more optimistic assumptions, still there will be a negative impact on euro area growth

-2

-1

0

1

2

3

4

5

6

7

1965 1975 1985 1995 2005 2015 2025 2035 2045

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

13

Impact on growth – forward-scenario 2

Same scenario for the US…

US Growth Accounting

-2

-1

0

1

2

3

4

5

6

7

1965 1975 1985 1995 2005 2015 2025 2035 2045

Working age population contributionLabour productivity contributionLabour utilisation contributionReal GDP growth

14

Overview

Go through the impact on:

Economic growth

Labour markets

Public finance

Financial markets

What are the options for reforms?

15

Increase labour market participation, employment, productivity: there is significant potential for female participation…

Labour markets: current situation

Source: Eurostat

Female participation rate

0

10

20

30

40

50

60

70

80

Belgium

Germ

any

Greec

e

Spain

Franc

e

Irelan

dIta

ly

Luxe

mbo

urg

Nether

lands

Austri

a

Portu

gal

Finlan

d

Euro area average%

16

…and for an increased participation of 55-64 years old

Labour markets: current situation

Source: Eurostat

55-64 participation rate

0

10

20

30

40

50

60

Belgium

German

y

Greece

Spain

France

Irelan

dIta

ly

Luxem

bourg

Netherl

ands

Austria

Portuga

l

Finlan

d

%

euro area average

17

Reform needs: labour markets

Reduce disincentives to enter work

interplay of taxes and benefits, early retirement schemes

Encourage female labour market entry

increase flexibility of working hours and provision of childcare services

Encourage workers to remain at work later in life

encourage policies of gradual exit from work, part-time work, increases in statutory retirement age

Invest in quality of education, research and development, increase lifelong learning and tackle old age discrimination

18

Reform needs: labour markets

The stabilisation of the old-age dependency ratios through migration alone is unlikely, due to the large number of migrants that would be required

The EC states that “using migration to fully compensate the impact of demographic ageing on the labor market is not a realistic option”.

19

Overview

Go through the impact on:

Economic growth

Labour markets

Public finances

Financial markets

What are the options for reforms?

20

Impact on public finances

The most important expenditure effects arise from public pension systems and health and long-term care

The estimated fiscal impact of the increase in pension expenditures (from different sources) find a cumulative increase in pension expenditure of more than 5 pp of GDP for most euro area countries, with pressure rising rapidly after 2010 (for some countries [GR, PT] up to 10 pp).

Looking at the outstanding stock of pension debt, it can be estimated an incremental implicit pension liability of close to 50% of GDP for the four largest euro area countries.

21

Impact on public finances

Offsetting effects through unemployment and education expenditure are small and uncertain

The EPC/European Commission projections may still turn out too low (e.g. favourable assumptions re. labour productivity)

Recent projections by the OECD point to a much more gloomy scenario, especially concerning the cost increases of public spending on health and long-term care.

22

Reform options: public finances

Major reform needs in public pension systems and health care and long-term care arrangements:

Parametric reform of conventional pay-as-you-go pension systems necessary, but most likely insufficient

Systemic pension reform: shift part of pension financing to funded arrangements and reduce exposure to demographic risks

One option: notional defined contribution (PAYG) system combined with funded pillar

Health care: raise efficiency through setting the right incentives for all participating parties (insurers, providers, patients)

23

Overview

Go through the impact on:

Economic growth

Labour markets

Public finance

Financial markets

What are the options for reforms?

24

Impact on financial markets

Impact on prices and quantities due to changes in savings patterns and savings allocations of people belonging to different generations

Changes in financial structures linked to ongoing pension reforms

Workers are required to save more and contribute to funded pension arrangements

25

Possible changes in savings patterns are based on the idea that wealth follows a life-cycle pattern; moreover risk tolerance may change with age

Impact on financial markets

0

0

0

0

1

1

1

1

1

16 20 24 28 32 36 40 44 48 52 56 60 64 68 72 76 80

age

wealth

current situation

future (2030)

26

Impact on financial markets

Theoretical and empirical analysis suggests that a meltdown is unlikely

Forward-looking simulations results (usually based on closed-economy assumptions) models suggest that current workers will earn returns around 60 basis points

below historical norm (given the assumptions in the models, this would represent an upper bound)

Empirical studies report ambiguous results results are different across countries, which would imply that the

relationship is affected by other fundamental factors

27

Impact on financial markets

Will there be an asset meltdown? Probably not, but therecould be an impact on prices:

people may change their saving and investment behaviour (and invest more in financial assets) especially if the benefits of public pension schemes are significantly reduced

international capital flows could help to smooth imbalances in domestic capital markets (for all kind of assets?)

28

Impact on financial markets: housing

housing wealth as % of disposable income in the euro area…

Source: ECB estimates based on national data

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0

50

100

150

200

250

300

350

400

450

500

financial wealthhousing wealth

29

Impact on financial markets: housing

A significant portion of households’ income is invested in housing

the relationship between house prices and ageing remain largely an open question; difficult to disentangle the effect of age from other characteristics (income, marital status, education)

Recent developments in some countries (US, UK but also most of euro area countries) suggest that households may treat real estate as a source of portfolio diversification

may be risky: a future house prices meltdown?

30

Impact on financial markets: the retirement industry

Euro area households have invested their private savings more via financial intermediaries (particularly retirement industry)

Source: Eurosystem, as a % of total financial assets

0

10

20

30

40

50

60

70

Belgium France Germany Italy Netherlands

% of savingsto institutions in 1990

% savingsto institutionsin 2005

31Source: OECD

The retirement savings industry

0

20

40

60

80

100

120

Belgium Germany Italy Japan Netherlands Sweden UK US

Pension funds assets, as % of GDP, 2004

Impact on financial markets: the retirement industry

Role played by institutional investors is expected to grow and this may have a number of implications and possibly an impact on corporate governance

32

Impact on financial markets: the retirement industry

Likely increase in savings for retirement over the next decades savings need to be invested and later on withdrawn to finance consumption of

elderly

Portfolio allocation of pension funds likely to exert significant pressures on financial markets

possible shifts towards less risky assets as people become older?

The extent of the impact is likely to depend on the financial structure and in particular on the social security arrangements

if countries in continental Europe shift more strongly towards funded systems, financial asset prices could in theory show more pronounced swings related to demographic changes

33

Impact on financial markets: the retirement industry

Shift from defined benefits to defined contributions plans portfolio choices will be more aligned with individuals’ preferences

Revised industry regulations place more emphasis on risk management

need to increase the supply of products to hedge against interest rate and inflation risk

long-dated bonds inflation-linked products financial innovation

Instruments to hedge against longevity risks are more problematic to develop

annuity reverse mortgages

34

Conclusions

Scenario analysis shows that projected demographic trends imply a decline in average GDP growth in the euro area to around 1% from 2020 to 2050

It is important to implement the European Employment Guidelines to mitigate the impact of population ageing

Reforms of pension systems and health care arrangements are needed to counteract pressures on public expenditures

Impact on financial markets will derive from changes in portfolio sizes/allocations, the likely increase in the role of financial intermediaries and the related adjustment in the supply of some financial instruments