1 investor relations presentation m ichael b aker c orporation 20022002 engineering & energy...

Post on 19-Dec-2015

217 views

TRANSCRIPT

1

Investor Relations PresentationInvestor Relations PresentationMICHAEL BAKER CORPORATIONMICHAEL BAKER CORPORATION2002200220022002

Engineering & Energy

Ninth AnnualEmerald Groundhog Day

Investment ForumFebruary 5, 2002

Ninth AnnualEmerald Groundhog Day

Investment ForumFebruary 5, 2002

2

2002 Engineering & EnergySafe HarborSafe Harbor

This presentation will contain information related to events which may occur in the future. These

forward-looking statements may include future business trends, revenue and earnings forecasts,

and acquisition and corporate finance activity. These statements are subject to market, regulatory,

operating and other risks and uncertainties and, as a result, actual results may vary. Such forward-

looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation

Reform Act of 1995.

This presentation will contain information related to events which may occur in the future. These

forward-looking statements may include future business trends, revenue and earnings forecasts,

and acquisition and corporate finance activity. These statements are subject to market, regulatory,

operating and other risks and uncertainties and, as a result, actual results may vary. Such forward-

looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation

Reform Act of 1995.

3

2002 Engineering & EnergySummary / HighlightsSummary / Highlights

Focused on Two Segments Engineering and Energy

Leader in Professional Services Oil & Gas Production O&M

Transportation and Civil Infrastructure Engineering

Positioned to Accelerate Margin Growth, Led

by Energy Segment

Currently Valued at 5x EBITDA

Focused on Two Segments Engineering and Energy

Leader in Professional Services Oil & Gas Production O&M

Transportation and Civil Infrastructure Engineering

Positioned to Accelerate Margin Growth, Led

by Energy Segment

Currently Valued at 5x EBITDA

4

2002 Engineering & EnergyDecade of PerformanceDecade of PerformanceDecade of PerformanceDecade of Performance

$134$150

$162 $165$179

$203

$228

$45$39

$43$55

$69

$80

$121

$157

$199 $205$210

$248

$349

$390

$240

$127

$93

$115

$86

$150

$72

$42

$43$41

$179$189

$283

$136$127

$0

$100

$200

$300

$400

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001(E)

Dollars in Millions

Engineering Energy

Co

nti

nu

ing

Bu

sin

es

s R

ev

en

ue

5

2002 Engineering & EnergyCore Energy Service OfferingsCore Energy Service Offerings Oil & Gas

Operations & Maintenance Operations Engineering Competency-Based Training Supply Chain Management

Oil & Gas Operations & Maintenance Operations Engineering Competency-Based Training Supply Chain Management

Power Operations & Maintenance New Equipment Installation Outage Planning/Overhauls Engineering / Start-up Assistance

Power Operations & Maintenance New Equipment Installation Outage Planning/Overhauls Engineering / Start-up Assistance

6

2002 Engineering & EnergyDifferentiation of ServicesDifferentiation of Services Energy

OPCOSM

Integrated Services and Solutions for Global O&G Upstream Production Operations

Competency-Based Training and Nationalization Programs

Energy OPCOSM

Integrated Services and Solutions for Global O&G Upstream Production Operations

Competency-Based Training and Nationalization Programs

7

2002 Engineering & EnergyOPCOOPCOSMSMOPCOOPCOSMSM

OPCO Integrated Decision-makingin Production Operations

OPCO Integrated Decision-makingin Production Operations

Idea Explore Construct Develop Produce Monetize

Management Operations

Maintenance

Supply ChainManagement

Human Resources

Training & Development

HS&E

Network Growth

Production Operations Functions and Critical Decisions

Production Operations Functions and Critical Decisions

OPCO

8

2002 Engineering & EnergyEnergy Growth DriversEnergy Growth Drivers

OPCOOPCOSMSM

ClientClient

BakerBakerVALUE CREATIONVALUE CREATIONSHARED SAVINGSSHARED SAVINGS

LEVERAGED LEVERAGED ECONOMIES of SCALE ECONOMIES of SCALE

Fixed Fee IncomeAnnual Performance Bonus

Sharing Cost Savings

Reduced Operating Costs

Increased RevenuesIncreased RevenuesIncreased EfficiencyIncreased Efficiency

9

2002 Engineering & EnergyPrice DriverPrice Driver

$0

$5

$10

$15

$20

$25

$30

$35

$40Ja

n-9

8

Mar

-98

May

-98

Jul-

98

Sep

-98

No

v-98

Jan

-99

Mar

-99

May

-99

Jul-

99

Sep

-99

No

v-99

Jan

-00

Mar

-00

May

-00

Jul-

00

Sep

-00

No

v-00

Jan

-01

Mar

-01

May

-01

Jul-

01

Sep

-01

No

v-01

Jan

-02

$/b

bl

Historical Oil Prices (WTI)Historical Oil Prices (WTI)

Data Source: www.eia.doe.govData Source: www.eia.doe.gov

10

2002 Engineering & EnergyOPCO Diffusion CurveOPCO Diffusion Curve

Early Early

AdoptersAdopters

Early Early

AdoptersAdoptersEarly Early

MajorityMajority

Early Early

MajorityMajorityLate Late

MajorityMajority

Late Late

MajorityMajorityLaggardsLaggardsLaggardsLaggards

11

2002 Engineering & EnergyOur OPCO Potential MarketOur OPCO Potential Market

12

2002 Engineering & EnergyOur OPCO-Served MarketOur OPCO-Served Market

13

2002 Engineering & EnergyDeepwater OpportunitiesDeepwater Opportunities

Largest Supplier of Manpower to Deepwater GOM

Ops Engineering Support to New Facilities

Largest Supplier of Manpower to Deepwater GOM

Ops Engineering Support to New Facilities

14

2002 Engineering & EnergyeOPSeOPSeOPSeOPS

Fully-Integrated, Operations and Maintenance System

for Upstream Energy Industry

Alliance: Baker - Content SAIC - Technology, Telecom and Knowledge Management Deloitte - Planning, Strategy and Analysis

Global Market - $160 Billion

Benefits Shortened Cycle Time Improved Operating Performance Lower Cost of Operation Greater Asset Return

Fully-Integrated, Operations and Maintenance System

for Upstream Energy Industry

Alliance: Baker - Content SAIC - Technology, Telecom and Knowledge Management Deloitte - Planning, Strategy and Analysis

Global Market - $160 Billion

Benefits Shortened Cycle Time Improved Operating Performance Lower Cost of Operation Greater Asset Return

15

2002 Engineering & Energy

Core Engineering Service OfferingsCore Engineering Service Offerings

Transportation Engineering Services Highways Bridges (Structures) Program Management Asset Management

Civil InfrastructureServices Cold Region Pipelines DoD / Federal Markets Water/Waste Water Asset Management

Transportation Engineering Services Highways Bridges (Structures) Program Management Asset Management

Civil InfrastructureServices Cold Region Pipelines DoD / Federal Markets Water/Waste Water Asset Management

16

2002 Engineering & EnergyGrowth DriversGrowth Drivers

Transportation: TEA-21Transportation: TEA-21

Baker OfficeBaker Office

Ranking TEA-21 Funded StatesRanking TEA-21 Funded States

1st

2nd

3rd

4th

8th12th

11th

23rd

35th

22nd

29th

Source: Projected TEA-21 Apportionments 1998-2003, ENR (08/00)Source: Projected TEA-21 Apportionments 1998-2003, ENR (08/00)

6th

7th

9th

10th

5th

17

2002 Engineering & EnergyGrowth DriversGrowth DriversTEA-21/AIR-21TEA-21/AIR-21

Source: Federal Highway Administrations and FAA, U.S. Department of Transportation

Total Federal AuthorizationsTotal Federal Authorizations

$39.8$38.7$37.8$36.7

$28.4$26.5$24.7$23.9

$0$5

$10$15$20$25$30$35$40$45

2000 2001 2002 (E) 2003 (E)

$ in

bill

ion

s

TEA-21 AIR-21

18

2002 Engineering & EnergyEngineering Highlights - 2001Engineering Highlights - 2001

$290mm in New Work Added

Won $130mm in Open-End Contracts with

Department of Defense

Selected as General Engineering Consultant

for Hampton Roads Third Crossing $4.5 Billion Total Project Cost

Successful Entry into Texas Market

$290mm in New Work Added

Won $130mm in Open-End Contracts with

Department of Defense

Selected as General Engineering Consultant

for Hampton Roads Third Crossing $4.5 Billion Total Project Cost

Successful Entry into Texas Market

19

2002 Engineering & EnergyCompetitive Barriers to EntryCompetitive Barriers to Entry Energy

Customer Relationships Content and Information Delivery Systems Implementation/Delivery Capability OPCO Network

Engineering Alignment of Services to Meet Customer

Needs Long-Term Relationships

Energy Customer Relationships Content and Information Delivery Systems Implementation/Delivery Capability OPCO Network

Engineering Alignment of Services to Meet Customer

Needs Long-Term Relationships

20

2002 Engineering & EnergyKey Customer RelationshipsKey Customer Relationships

Engineering Engineering Energy Energy

21

2002 Engineering & Energy

Acquisition Growth OpportunitiesAcquisition Growth Opportunities

Geographic and Capacity Expansion Energy Opportunities Engineering Opportunities

Additional Capabilities Energy

Training Program Development Maintenance Management Systems

Engineering Water/Wastewater Asset Management

Geographic and Capacity Expansion Energy Opportunities Engineering Opportunities

Additional Capabilities Energy

Training Program Development Maintenance Management Systems

Engineering Water/Wastewater Asset Management

22

2002 Engineering & EnergyTotal RevenuesTotal RevenuesTotal RevenuesTotal Revenues

$521.3

$390.7

$506.0

$390.0

$247.0

$281.9

$348.7

$0

$100

$200

$300

$400

$500

$600

1998 1999 2000 2001 (E)

Do

llars

in M

illio

ns

Total Reported Revenues Engineering Energy

23

2002 Engineering & EnergyRevenuesRevenuesRevenuesRevenues

$129.8

$98.4$92.4

$69.0

$89.7$98.4

$0

$25

$50

$75

$100

$125

$150

1999 2000 2001

Do

llar

s in

Mil

lio

ns

Total Reported Revenues Engineering Energy

Q3/Q3 Total Reported/Engineering/Energy RevenuesQ3/Q3 Total Reported/Engineering/Energy Revenues

$17.5

$51.5

$31.8

$57.9

$37.8

$60.6

24

2002 Engineering & EnergyOperating PerformanceOperating Performance(in Thousands of $)(in Thousands of $)

Operating PerformanceOperating Performance(in Thousands of $)(in Thousands of $)

‘98 ‘99 ‘00 TOTAL CONTRACT REVENUES

Total Reported $521,271 $506,012 $390,710

Less Non-Core 274,249 224,132 42,018

ENERGY 68,607 80,158 120,708

ENGINEERING 178,414 201,722 227,984

Total Core 247,021 281,880 348,692

TOTAL OPERATING INCOME (Pre-Corp. O/H and I/C Ins. Premiums)Total Reported 7,075 (511) 17,543

% 1.4% -.1% 4.5%

ENERGY 5,297 9,314

% 7.7% 6.8% 7.7%

ENGINEERING 13,796 13,356 16,783

% 7.7% 6.6% 7.4%

Total Core $19,093 $18,827 $26,097

% 7.7% 6.7% 7.5%

‘98 ‘99 ‘00 TOTAL CONTRACT REVENUES

Total Reported $521,271 $506,012 $390,710

Less Non-Core 274,249 224,132 42,018

ENERGY 68,607 80,158 120,708

ENGINEERING 178,414 201,722 227,984

Total Core 247,021 281,880 348,692

TOTAL OPERATING INCOME (Pre-Corp. O/H and I/C Ins. Premiums)Total Reported 7,075 (511) 17,543

% 1.4% -.1% 4.5%

ENERGY 5,297 9,314

% 7.7% 6.8% 7.7%

ENGINEERING 13,796 13,356 16,783

% 7.7% 6.6% 7.4%

Total Core $19,093 $18,827 $26,097

% 7.7% 6.7% 7.5%

Adjusted for $1 Million Non-Recurring ChargeAdjusted for $1 Million Non-Recurring Charge

5,471

25

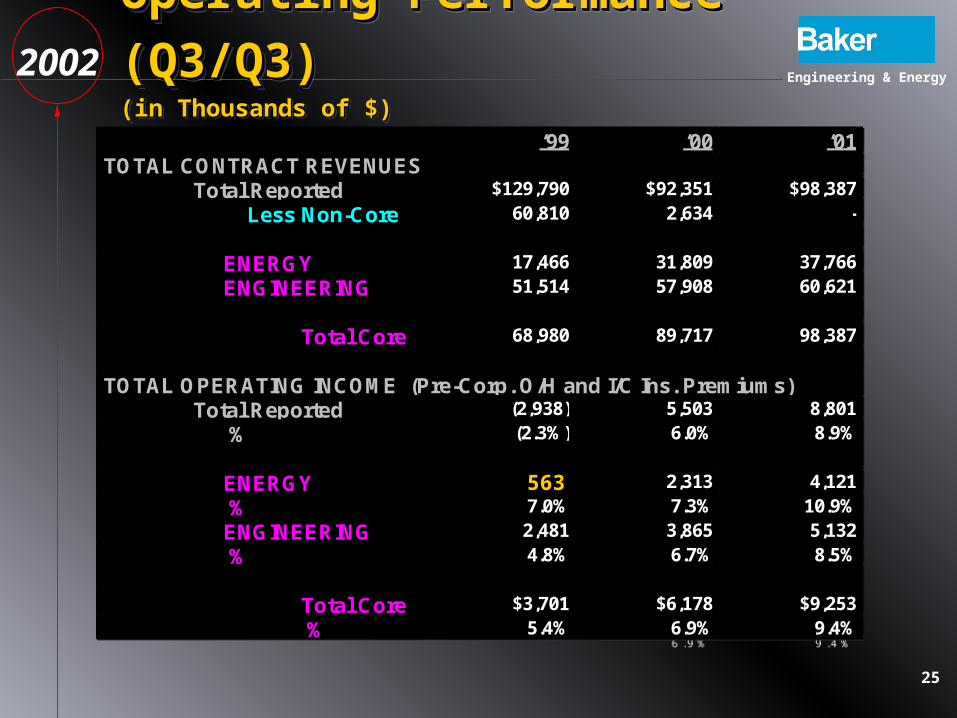

2002 Engineering & EnergyOperating Performance (Q3/Q3)Operating Performance (Q3/Q3)(in Thousands of $)(in Thousands of $)

Operating Performance (Q3/Q3)Operating Performance (Q3/Q3)(in Thousands of $)(in Thousands of $)

‘99 ‘00 ‘01 TOTAL CONTRACT REVENUES

Total Reported $129,790 $92,351 $98,387

Less Non-Core 60,810 2,634 -

ENERGY 17,466 31,809 37,766

ENGINEERING 51,514 57,908 60,621

Total Core 68,980 89,717 98,387

TOTAL OPERATING INCOME (Pre-Corp. O/H and I/C Ins. Premiums) Total Reported (2,938) 5,503 8,801

% (2.3%) 6.0% 8.9%

ENERGY 1,220 2,313 4,121

% 7.0% 7.3% 10.9%

ENGINEERING 2,481 3,865 5,132

% 4.8% 6.7% 8.5%

Total Core $3,701 $6,178 $9,253

% 5.4% 6.9% 9.4%

‘99 ‘00 ‘01 TOTAL CONTRACT REVENUES

Total Reported $129,790 $92,351 $98,387

Less Non-Core 60,810 2,634 -

ENERGY 17,466 31,809 37,766

ENGINEERING 51,514 57,908 60,621

Total Core 68,980 89,717 98,387

TOTAL OPERATING INCOME (Pre-Corp. O/H and I/C Ins. Premiums) Total Reported (2,938) 5,503 8,801

% (2.3%) 6.0% 8.9%

ENERGY 1,220 2,313 4,121

% 7.0% 7.3% 10.9%

ENGINEERING 2,481 3,865 5,132

% 4.8% 6.7% 8.5%

Total Core $3,701 $6,178 $9,253

% 5.4% 6.9% 9.4%

563

26

2002 Engineering & Energy

‘98 ‘99 ‘00

Net Income $(2.4) $(8.2) $5.4 Depreciation & Amortization 5.0 7.4 7.1 Other (4.0) 1.9 (0.1)

Cash from Operations (1.4) 1.1 12.4

Capital Expenditures (10.6) (5.3) (2.9)Acquisition/Investments (.8) (4.9) (9.0)Share Repurchase (.8) - -Proceeds from Sale of Assets/Stock Options - - 15.0NET Borrowings (Repayments) 2.7 7.8 (10.1)

NET Increase (Decrease) in Cash $(10.9) $(1.3) $5.4

‘98 ‘99 ‘00

Net Income $(2.4) $(8.2) $5.4 Depreciation & Amortization 5.0 7.4 7.1 Other (4.0) 1.9 (0.1)

Cash from Operations (1.4) 1.1 12.4

Capital Expenditures (10.6) (5.3) (2.9)Acquisition/Investments (.8) (4.9) (9.0)Share Repurchase (.8) - -Proceeds from Sale of Assets/Stock Options - - 15.0NET Borrowings (Repayments) 2.7 7.8 (10.1)

NET Increase (Decrease) in Cash $(10.9) $(1.3) $5.4

Cash Flow(in millions of $)

Cash Flow(in millions of $)

27

2002 Engineering & Energy

‘98 ‘99 ‘00 ASSETS Cash $5.0 $3.7 $9.1Short-Term Investment - - 9.0A/R 82.7 77.4 68.0Cost in Excess of Billing 22.4 20.8 16.1

PPE 17.5 17.1 10.1Intangibles 7.5 14.6 10.8Other 16.8 15.6 10.2

151.9 149.2 133.3LIABILITIES Current Prt LTD .8 3.5 2.2Trade A/P 43.4 28.9 25.7Accrued Other 51.7 57.1 55.0

Long Term Debt 3.1 14.9 0.1

Owners’ Equity 52.9 44.8 50.3 $151.9 $149.2 $133.3

‘98 ‘99 ‘00 ASSETS Cash $5.0 $3.7 $9.1Short-Term Investment - - 9.0A/R 82.7 77.4 68.0Cost in Excess of Billing 22.4 20.8 16.1

PPE 17.5 17.1 10.1Intangibles 7.5 14.6 10.8Other 16.8 15.6 10.2

151.9 149.2 133.3LIABILITIES Current Prt LTD .8 3.5 2.2Trade A/P 43.4 28.9 25.7Accrued Other 51.7 57.1 55.0

Long Term Debt 3.1 14.9 0.1

Owners’ Equity 52.9 44.8 50.3 $151.9 $149.2 $133.3

Balance SheetBalance Sheet(in millions of $)(in millions of $)

Balance SheetBalance Sheet(in millions of $)(in millions of $)

28

2002 Engineering & EnergyEPS GrowthEPS GrowthEPS GrowthEPS Growth‘98 ‘99 ‘00

Reported EPS $(.30) $(1.00) $.65

Pro Forma EPSCore Operating Income $19,093 $17,827 $26,097Less Corporate Overhead (8,744) (7,664) (7,715) Operating Income 10,349 10,163 18,382

Provision for Income Taxes(47% Rate for 1998 & 1999 and51% Rate for 2000) (4,864) (4,777) (9,375)

5,485 5,386 9,007

Pro Forma EPS $.67 $.66 $1.09

‘98 ‘99 ‘00 Reported

EPS $(.30) $(1.00) $.65

Pro Forma EPSCore Operating Income $19,093 $17,827 $26,097Less Corporate Overhead (8,744) (7,664) (7,715) Operating Income 10,349 10,163 18,382

Provision for Income Taxes(47% Rate for 1998 & 1999 and51% Rate for 2000) (4,864) (4,777) (9,375)

5,485 5,386 9,007

Pro Forma EPS $.67 $.66 $1.09

2001 Estimate: $1.25 - $1.302001 Estimate: $1.25 - $1.30

29

2002 Engineering & EnergyStock Performance (12 mos.)Stock Performance (12 mos.)Stock Performance (12 mos.)Stock Performance (12 mos.)

$8.25 $8.30

$8.93

$10.00

$11.55

$13.85

$14.00 $15.00

$12.26

$13.38$13.60

$15.20

$12.70

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

01/01 02/01 03/01 04/01 05/01 06/01 07/01 08/01 09/01 10/01 11/01 12/01 01/02

Clo

sin

g S

ha

re P

ric

e

$8.25 $8.30

$8.93

$10.00

$11.55

$13.85

$14.00 $15.00

$12.26

$13.38$13.60

$15.20

$12.70

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

01/01 02/01 03/01 04/01 05/01 06/01 07/01 08/01 09/01 10/01 11/01 12/01 01/02

Clo

sin

g S

ha

re P

ric

e

30

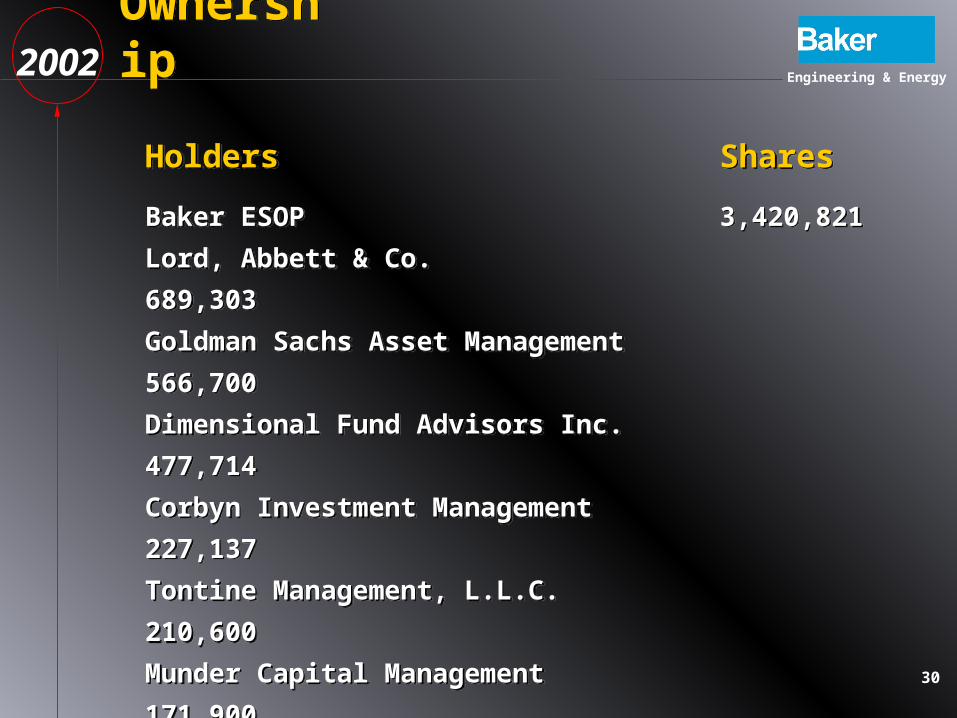

2002 Engineering & EnergyOwnershipOwnership

Holders Shares

Baker ESOP 3,420,821

Lord, Abbett & Co. 689,303

Goldman Sachs Asset Management 566,700

Dimensional Fund Advisors Inc. 477,714

Corbyn Investment Management 227,137

Tontine Management, L.L.C. 210,600

Munder Capital Management 171,900

Paradigm Capital Management 154,400

Emerald Advisers 87,100

Holders Shares

Baker ESOP 3,420,821

Lord, Abbett & Co. 689,303

Goldman Sachs Asset Management 566,700

Dimensional Fund Advisors Inc. 477,714

Corbyn Investment Management 227,137

Tontine Management, L.L.C. 210,600

Munder Capital Management 171,900

Paradigm Capital Management 154,400

Emerald Advisers 87,100

31

2002 Engineering & EnergyConclusionConclusion Leader in:

Oil & Gas Production O&M Transportation and Civil Infrastructure

Engineering Energy Market Conditions Catalyst for

Significant Growth Investment in Transportation

Infrastructure Providing Substantial Opportunity

Debt-free, Leverageable Balance Sheet

Currently Valued at 5x EBITDA

Leader in: Oil & Gas Production O&M Transportation and Civil Infrastructure

Engineering Energy Market Conditions Catalyst for

Significant Growth Investment in Transportation

Infrastructure Providing Substantial Opportunity

Debt-free, Leverageable Balance Sheet

Currently Valued at 5x EBITDA

32

Investor Relations PresentationInvestor Relations PresentationMICHAEL BAKER CORPORATIONMICHAEL BAKER CORPORATION2001200120012001

Engineering & Energy