1 health care access, cost, and quality health care access, cost, and quality (what we don’t know...

TRANSCRIPT

1

Health Care Access, Health Care Access, Cost, and QualityCost, and Quality

(What we don’t know can hurt us)

Doug Hall NH Center for Public Policy Studies

New Hampshire Public Health Association

October 29, 2004

With generous support from

2

All of our reportsare available on the web:

www.nhpolicy.orgwww.nhpolicy.org

New Hampshire Center New Hampshire Center for Public Policy Studiesfor Public Policy Studies

Board of Directors

Martin L. Gross, Chair

John B. Andrews

Cotton M. Cleveland

John D. Crosier

Todd I. Selig

Donna Sytek

Georgie A. Thomas

James E. Tibbetts

Kimon S. Zachos

Co-Directors

Douglas E. Hall

Richard A. Minard, Jr.

“…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.”

3

HYPOTHESIS: The employment-based health insurance system that has been relatively stable for decades, is approaching a “tipping point,” where it may become unstable and could collapse.

1. Rising costs of care lead to rising insurance premiums2. Unable to pay increased premiums, employers increase % of

premiums to be paid by employees or substitute high deductible plans. Some employers may drop coverage altogether.

3. Younger, healthier employees with low medical costs opt out of offered insurance coverage, knowing they are at low risk.

4. Through this adverse selection, older, less healthy employees constitute a larger part of the risk pool, causing average claims/person to rise yet further.

5. Back to step #1. (The positive feedback loop results in rapidly accelerating premiums and numbers of uninsured.)

4

Do you agree ?

• There is already sufficient money in the health care system to provide quality health care for all.

• Less medical care can mean better quality.

• Currently in health care, neither supply nor demand are subject to the market force of price.

5

Access, Cost, and Quality are Interrelated, but How?

We don’t have all the pieces to the puzzle!

6

AccessAccess

7

Common View

Insured Uninsured

Realistic View

Insured for what? drug rehab, prescription drugs, mental health, “experimental” procedures, dental, …

How much annual deductible and out-of-pocket?

Pre-existing conditions

8

Estimated Number of Uninsured NH Residents, 1999-2003

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

1999 2000 2001 2002 2003

Year

Per

son

s

2003 survey funded by Endowment for Health and HNHfoundation

Annual estimates from Current Population Survey of the U. S. Census Bureau indicated by filled central markers

1999 & 2001 surveys funded by NH Department of Health & Human Services

In NH, About 120,000 are Uninsured

9

Percent of Population Uninsured By State, 2003

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%M

inne

sota

Ver

mon

tH

awai

iR

hode

Isla

ndN

ew H

amps

hire

Con

nect

icut

Mai

neM

assa

chus

etts

Mic

higa

nN

orth

Dak

ota

Wis

cons

inK

ansa

sM

isso

uri

Del

awar

eIo

wa

Neb

rask

aP

enns

ylva

nia

Ohi

oS

outh

Dak

ota

Uta

hV

irgin

iaT

enne

ssee

Indi

ana

Mar

ylan

dK

entu

cky

New

Jer

sey

Ala

bam

aD

.C.

Illin

ois

Sou

th C

arol

ina

New

Yor

kW

ashi

ngto

nW

yom

ing

Geo

rgia

Wes

t Virg

inia

Ariz

ona

Col

orad

oO

rego

nN

orth

Car

olin

aA

rkan

sas

Mis

siss

ippi

Flo

rida

Cal

iforn

iaId

aho

Ala

ska

Nev

ada

Mon

tana

Okl

ahom

aLo

uisi

ana

New

Mex

ico

Tex

as

State

Per

cen

t

95% Confidence Intervals displayed

New Hampshire ranked 5th among the 50 states. But confidence intervals of the survey show that it falls somewhere among the 20 states with the lowest rates.

10

Insurance Status of New Hampshire Adults, 2003

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

insured now and all yearinsured now, but not all yearuninsured now, insured during yearuninsured all year

6% chronically uninsured13% transitionally insured

11

Percentage of Persons Insured & Uninsured by Age Group, 2001

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Ag

e G

rou

p

Percentage

Age 0-17

Age 18-24

Age 25-34

Age 35-44

Age 45-54

Age 55-64

Age 65+

Private Health Insurance (primarily employment-based)

PublicInsurance: Medicaid, etc.

Public Insurance: Medicare

Uninsured

12

Applicant Insurance Statusin September 2002

at New Hampshire Hospitals(n=1,147)

55%

44%

1%

Uninsured Insured, but had a Balance Due Unknown

This slide from

Financial Assistance Application StudySeptember 2002

13

Who are Disproportionately Uninsured in NH ?

• Those between ages 18 and 30• Those who have household incomes of less than $30,000• Renters• Self-employed persons• Employees of small businesses (fewer than 50

employees)• Workers in retail, food, or construction industries• Workers who are unemployed, employed only part time,

or employed seasonally• African-Americans and those of Hispanic origin• Adults who are not registered to vote• Singles, living alone• Residents of Coos, Grafton, Carroll, and Sullivan counties;• Those with no education beyond high school or who did

not complete high school

14

What We Don’t Know Can Hurt Us#1

• If the number of people who are uninsured or underinsured begins to grow, how will we know it?

• What is our early warning system?• What health effects will occur and how will

we measure them?• What will be the impact on those still

insured through additional cost-shifting?

15

CostCost

16

Estimated Personal Health Care Spending in NH, 2004(in $ million)

$2,201

$2,104

$415

$175

$931

$83

$533

$188

$438

Hospital Care

Physicians, Clinics, & Other Professional

ServicesDental Services

Home Health Care

Prescription Drugs

Durable Equipment

Nursing Home Care

Other Personal Health Care Total:

$7,068 million

Other Non-durables

17

Projected Personal Health Care Expenditure in NH 2011 (in $ million)

$3,084

$3,248$557

$306

$1,857

$139

$794

$264

$978

Hospital Care

Physicians, Clinics, & Other Professional

Services

Dental Services

Home Health Care

Prescription Drugs

Durable Equipment

Nursing Home Care

Other Personal Health Care

Total:$11,227 million

Other Non-durables

18

Estimated Source of Funds Personal Health Care in US, 2004

Other Public7%

Medicaid18%

Other Private4%

Medicare19%

Insurance36%

Out-of-Pocket16%

Private Sources

Public Sources

19

Personal Health Expenditure per Capita

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1975 1980 1985 1990 1995 2000 2005 2010

Year

US

New Hampshire

New Hampshire health spending per capita has closely tracked national averages. Beginning in 1995 it slightly exceeded the national average but projections show it falling back below national average in about 2008.

Projected

20

NH Health Expenditure as % of Gross State Product (GSP)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1975 1980 1985 1990 1995 2000 2005 2010

Year

During recessions, the expansion of the economy slows but growth in health spending continues to grow and it consumes greater portions of the overall GSP.

Estimated Projected

21

Expenditures on Personal Health Care and Public Schools in NH

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

Year

Mil

lio

ns

of

Do

lla

rs

Personal Health Care Expenditures

Public School Expenditures

Personal health care spending was 166% of public school spending in 1975

Personal health care spending was 325% of public school spending in 2002

22

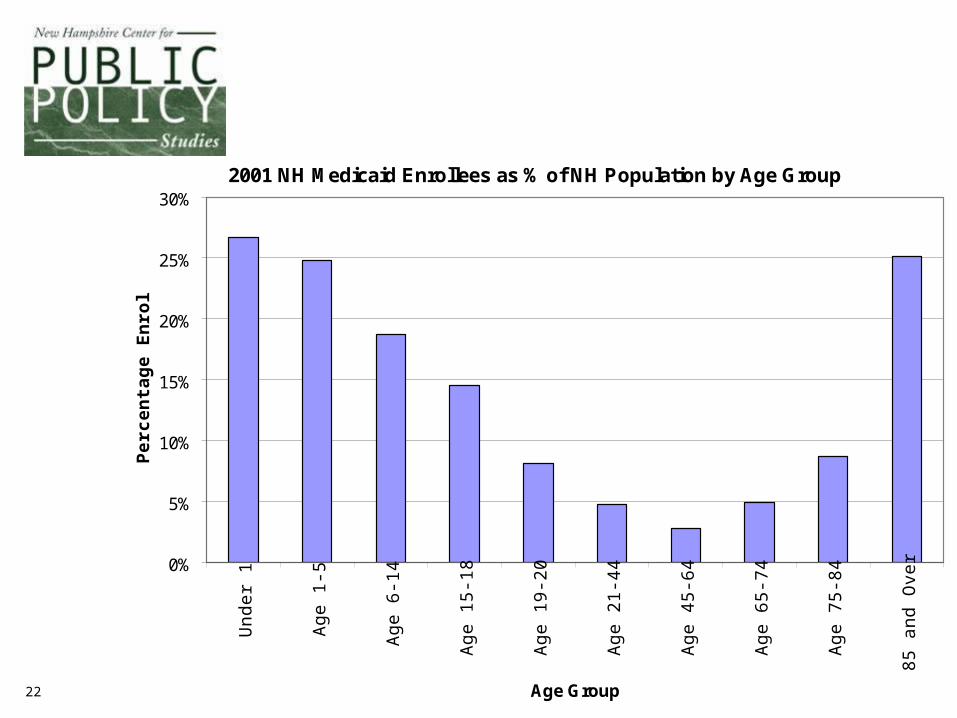

2001 NH Medicaid Enrollees as % of NH Population by Age Group

0%

5%

10%

15%

20%

25%

30%

Un

de

r 1

Ag

e 1

-5

Ag

e 6

-14

Ag

e 1

5-1

8

Ag

e 1

9-2

0

Ag

e 2

1-4

4

Ag

e 4

5-6

4

Ag

e 6

5-7

4

Ag

e 7

5-8

4

85

an

d O

ver

Age Group

Pe

rce

nta

ge

En

roll

ed

23

Medicaid Spending per Enrollee by Age Group, FFY 2001

$0

$2,500

$5,000

$7,500

$10,000

$12,500

$15,000

$17,500

$20,000

$22,500

$25,000

Under 1 Age1-5

Age6-14

Age15-18

Age19-20

Age21-44

Age45-64

Age65-74

Age75-84

Age85 +

Age Group

Ave

rag

e S

pen

din

g p

er E

nro

llee

24

2001 NH Medicaid Enrollees by Eligibility Category

12,833

13,507

66,547

15,675

Children$2,266 per child

Adults$2,336 per

person

Aged$18,182

per person

Disabled$19,727 per person

25

NH Medicaid Spending by Eligibility Category, FFY 2001

$233,326,495

$266,447,475

$150,803,296

$36,611,492

$4,007,029

Children

Adults

Aged

DisabledTotal

$691,195,787

Unknown

Aged and disabled accounted for 72% of the spending

26

Source: Audited financial statements of the hospitals for 2001 and 2002 as provided in spreadsheet form by NH Hospital Association; 4th Quarter, 2002 Trending Report, NH Hospital Association

Revenue/Expense Measure 2001 2002 ChangeInpatent Admissions 124,096 123,764 -0.2%Inpatient Patient-days 543,033 547,094 0.8%

Gross Patient Service Revenue $2,857,633,144 $3,264,893,121 14.3%Charity Care $45,736,960 $61,546,402 34.6%Contractual Allowances $1,077,218,351 $1,276,061,665 18.5%Net Patient Service Revenue $1,734,677,833 $1,927,285,054 11.1%Net Operating Revenue $1,794,578,201 $1,989,630,720 10.9%Bad Debts $96,243,326 $106,671,251 10.8%Total Operating Expense $1,723,705,402 $1,905,109,946 10.5%Net Operating Income $70,872,799 $84,520,774 19.3%

26 NH Acute Care Hospitals

27

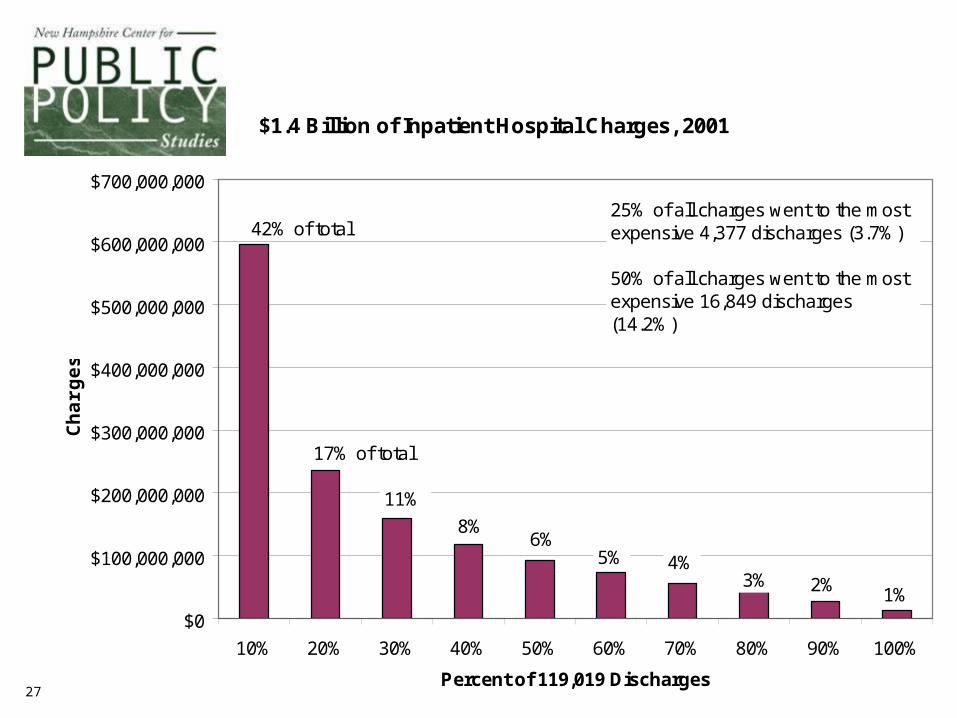

$1.4 Billion of Inpatient Hospital Charges, 2001

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Percent of 119,019 Discharges

Ch

arg

es

42% of total

17% of total

11%

8% 6%

5% 4% 3% 2% 1%

25% of all charges went to the most expensive 4,377 discharges (3.7%)

50% of all charges went to the most expensive 16,849 discharges (14.2%)

28

Cost-Shifting•The allocation of unpaid costs of care delivered to one patient population through above-cost revenue collected from other patient populations.

•For hospitals, nursing facilities and physicians, the historical cause of cost shifting has been below-cost reimbursement rates paid by public programs and uncompensated care losses due to charity care and bad debt.

Source: “Cost Shifting: An Integral Aspect of U.S. Health Care Finance,” The Lewin Group, November 2002

29

NH Hospital Revenue, 2001 (theoretical situation where all payers pay cost + 5% margin)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

% of Gross Charges by Payer

% o

f C

os

t P

aid

Third Party / Insurance46%

Self-Pay7%

Medicare40%

Medicaid6%

Other 1%

0% 100%

30

NH Hospital Revenue, 2001(actual)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Percent of Gross Payer Charges

% o

f C

os

t P

aid

Third Party / Insurance46%

Self-Pay2%

Medicare40%

Medicaid6%

Bad Debt & Charity

5%

Base Case

346%

Other 1%

0%

31

NH Hospital Revenue, 2001(actual)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Source of Payment

% o

f C

os

t P

aid

Shortfall of $119 million

Sho

rtfa

ll of

$3

0 M

illio

n

Sho

rtfa

ll of

$86

mill

ion

Suplus of $64 million

Shortfall of $ 2 million

0% 100%

Third Party / Insurance46%

Medicare40%

Medicaid6%

Bad Debt & Charity

5%

Self-Pay2%

Other 1%

Surplus of $134 million

32

Quantifying the 2001 Cost-Shiftin 26 New Hampshire Hospitals

PayerActual

Revenue

Revenue Needed to

Meet Expenses Plus 5% Margin

Excess or(Shortfall)

ShortfallsMedicare $559,189,410 $678,444,353 ($119,254,943)Medicaid $82,259,512 $111,966,988 ($29,707,476)Bad Debt/Charity Care $0 $85,566,423 ($85,566,423)Other $19,864,074 $22,283,430 ($2,419,356)

Total ($236,948,198)

SurplusesInsurance $916,840,046 $782,740,939 $134,099,107Self-Pay $91,660,528 $27,833,046 $63,827,482

Total $197,926,588Remaining shortfall ($39,021,610)

Operating marginTheoretical operating margin 5.0% $81,373,104Actual margin 2.6% $42,351,494Reduced margin $39,021,610

33

Rough estimate of the cost to provide the “missing” health care to those who are currently uninsured

• 2004 health care costs in NH: $7,000 million• Uninsured are 10% of the population• Their “need gap” is mostly for physicians, hospitals, and

prescription drugs (75% of all services)• They are disproportionately younger than the

insured/Medicare population with costs about 67% of the average.

• Uninsured currently receive 60% of the health care of those who are fully insured (self-pay, cost-shifted, and subsidized).

$140 million additional cost

(By way of comparison, the State obtained $205 million net Medicaid enhancement revenue and recoveries in 2003.)

34

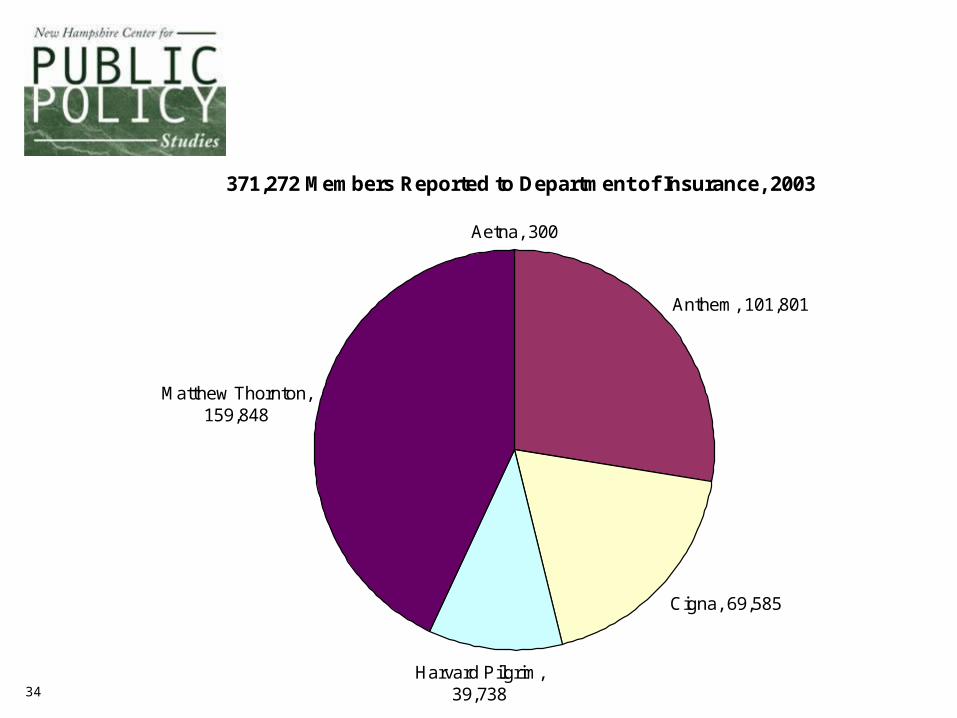

371,272 Members Reported to Department of Insurance, 2003

Aetna, 300

Anthem, 101,801

Cigna, 69,585

Harvard Pilgrim, 39,738

Matthew Thornton, 159,848

35

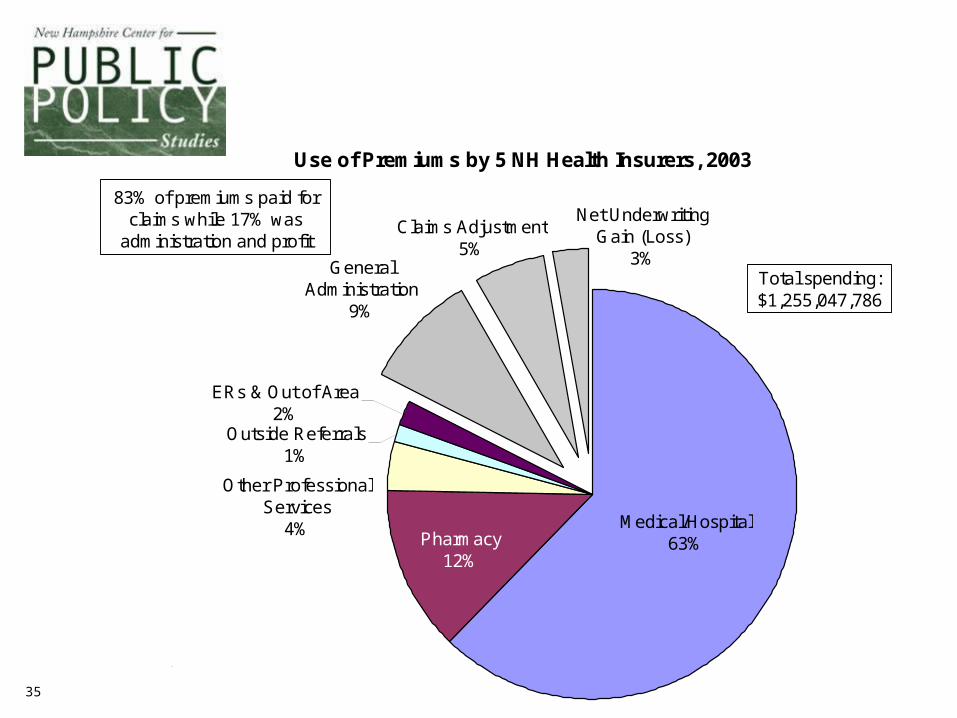

Use of Premiums by 5 NH Health Insurers, 2003

Claims Adjustment5%

Net Underwriting Gain (Loss)

3%General Administration

9%

Outside Referrals1%

ERs & Out of Area2%

Other Professional Services

4%Pharmacy

12%

Medical/Hospital63%

83% of premiums paid for claims while 17% was

administration and profit

Total spending:$1,255,047,786

Based on annual financial reports filed with NH Department of Insurance

36

2001 2002 2003% change in 2 years

Member-months 5,280,024 5,290,688 4,936,816 -6.5%

Net Premium Income $1,194,219,196 $1,241,571,726 $1,254,608,757 5.1%Total medical and hospital claims $973,778,586 $1,003,260,608 $1,035,193,680 6.3%Claims Adjustment Expenses $50,160,374 $63,893,427 $68,615,016 36.8%General Administrative Expenses $100,326,769 $107,312,895 $113,653,270 13.3%Net Underwriting Profit (Loss) $56,638,560 $63,051,904 $36,029,896 -36.4%

Per Member YearNet Premium Income $2,714.12 $2,816.05 $3,049.60 12.4%Total medical and hospital claims $2,213.12 $2,275.53 $2,516.26 13.7%Claims Adjustment Expenses $114.00 $144.92 $166.78 46.3%General Administrative Expenses $228.01 $243.40 $276.26 21.2%Net Underwriting Profit (Loss) $128.72 $143.01 $87.58 -32.0%

Underwriting Finances of 5 NH Health Insurers

37

What Did Each $1,000 of Health Insurance Premium Buy in 2002?

Hospitals$338 Hospitals

$287

Physicians/Clinics$266

Physicians/Clinics$226

Prescription Drugs$125

Prescription Drugs$125

Other Providers$70

Provider Cost-shift$103

Net Profit $51

Admin/Claims Processing$120

Admin/Claims Processing$120

Other Providers$82

Net Profit $51

$18 $18

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

By the books With cost-shift squeezed out

Do

llars

State premium tax

$708 paid for health care of

the insured

38

Missing Pieces of the Cost Puzzle

Amounts paid in claims for different service types by employers’ self-insured health benefit plans.

#1

39

Missing Pieces of the Cost Puzzle

List prices of all providers, including hospitals, physician practices, laboratories, outpatient clinics, surgery centers.

#2

40

Actual payment amounts made by insurers to all types of providers under negotiated discounts and contracts.

#3

Missing Pieces of the Cost Puzzle

41

Missing Pieces of the Cost Puzzle

Aggregate costs of private medical practices broken down by standard line item costs and numbers of units of various codes billed that generate offsetting revenue.

#4

42

QualityQualityFrom work by Elliott Fisher, MD, MPH, and others.

See a series of articles in Annals of Internal Medicine, Vol. 138, #4, February 18, 2003 and another series in Health Affairs, Web exclusive edition, October 7, 2004.

• U.S. health care spending would decline by over 30%.

• The projected deficit in the Medicare Trust fund would be postponed by at least 25 years.

• We could send 30% of the U.S. health care workforce to Africa and -- in theory -- improve the health of both continents.

If all regions of the US could adopt the Medicare medical care practice patterns of the lowest spending 1/5 of the US hospital catchment areas, which of the following statements would apply?

In a Veterans’ Administration study, less care was consistent with both better care and better outcomes

• Followed individuals with serious chronic diseases(6 medical conditions, 3 psychiatric conditions)

• Constrained VA hospital use to 50% of previous level

• Clinic visits increased 10%• Visits for urgent care declined• No compensating use of private hospitals

resulted• Survival rates not adversely affected

(for 5 conditions improved significantly, for 4 conditions remained unchanged)

Physicians control or direct about70% of all health care spending

•How soon will a patient return for follow-up?•What drugs will be prescribed?•What imaging should be performed?•When is discharge from a hospital stay ordered?•What diagnostic tests and procedures are

ordered?•What specialists are consulted and how often?•Is the ICU required?

For similar conditions across different regions, practice patterns appear to be driven by supply, not inherent need.

Supply-Sensitive Care : Highest vs Lowest Spending Regions

1.00 1.5 2.00.5 2.5 3.0

1.00 1.5 2.00.5 2.5 3.0

Office Visits

Initial Inpatient Specialist ConsultationsInpatient Visits

Physician Visits

ElectrocardiogramTests and Procedures

Lower in High Spending Regions Higher in High Spending Regions

CT / MRI BrainPulmonary Function TestElectroencephelogram (EEG)

Discharges

Inpatient Days in ICU or CCUTotal Inpatient Days

Hospital Utilization

Feeding Tube PlacementEmergency Intubation

Procedures -- Last 6 months of life

1 Year Mortality Rate of Medicare Beneficiaries by Spending Regions

0

5

10

15

20

25

30

35

Hip fracture Colorectal cancer Acute myocardialinfarction

Medicare beneficiarysurvey

Annals of Internal Medicine, Volume 138, Number 4, February 18, 2003, page 291

N=614,503 N=195,429N=159,393 N=18,190

•Additional resources 60% more spending per capita

•Content of care Less effective careNo additional major surgeryMore supply-sensitive services

•Access to care, satisfaction Slightly worse accessNo greater satisfaction

•Health outcomes No gain in functionMortality slightly higher

•Physician perceptions Quality worseLower career satisfaction

What do higher spending hospital catchment areas of the country get compared to lower spending?

This comparison is after having controlled for inherent regional price differences, average levels of illness, age, sex, race, and socioeconomic conditions.

Qua

lity

of Care

Rank

OR

MN

NH

VTME

IA ND

WIVA

MTDE

WYWA

CO

NCAZ

SD

HI

NE

NMKY

MO

PA

UT

MA CT

NV

KS

ID

RIIN

OHSC

MDMI

NY

WVCA

OK

ALIL

GA

MSAR

NJTX

LA

TN

FL

0

10

20

30

40

50

2000 3000 4000 5000 6000

1995 Per-capita Medicare Expenditures -- Illness Adjusted

Is spending more likely to make things better?

Law of Diminishing Returns

Inputs of Medical Care

Hea

lth

Ben

efit

Overall, we may be in this region of declining benefit from more medical care

51

What We Don’t Know Can Hurt Us#2

• Are these results regarding quality measures unique to the Medicare population or do they hold true for those with private insurance as well?

• What are the uniform quality-of-care measures and cost-of-care measures that are available for all providers in NH and where can I get them?

52

What We Don’t Know Can Hurt Us#3

• What is the cost of this care/service?Is the potential benefit worth the cost?

• What is the quality of this care/service?Is the potential benefit worth the risk?

• What are the quality and cost of alternatives?

Can I go elsewhere and get higher quality or lower cost?

53

The Important Link Between Policy & Practice:

Information• What are the costs and what is

driving them?• For whom is access limited, why, and

what are the results?• What prevention services and

patterns of care are most effective?• How are the answers to these

questions related?

54

55

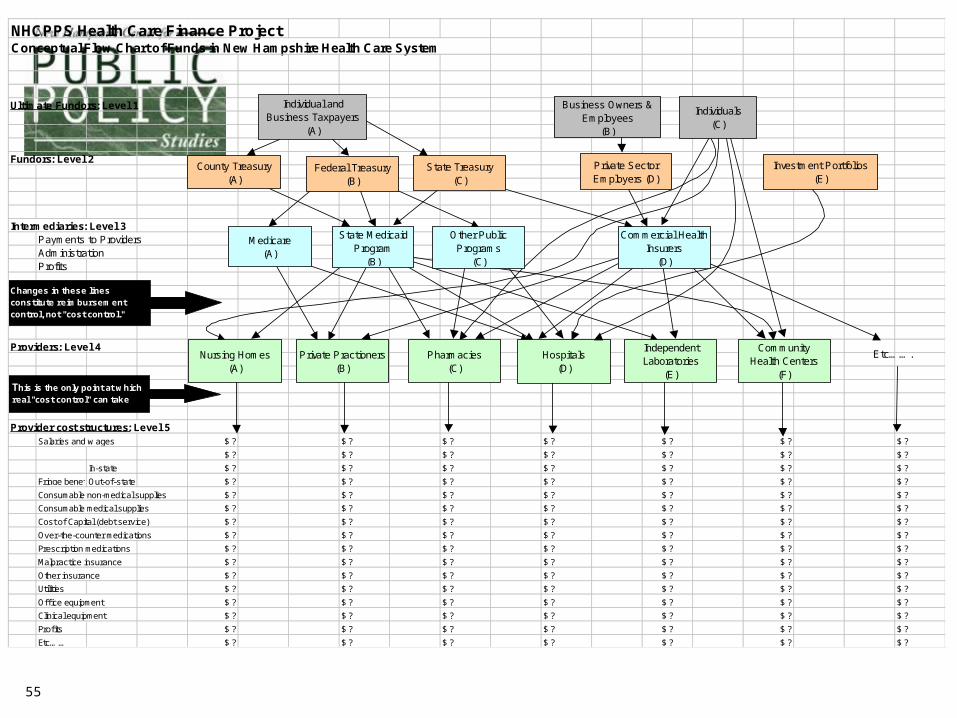

NHCPPS Health Care Finance ProjectConceptual Flow Chart of Funds in New Hampshire Health Care System

Ultimate Fundors: Level 1

Fundors: Level 2

Intermediaries: Level 3Payments to ProvidersAdministrationProfits

Providers: Level 4

Provider cost structures: Level 5Salaries and w ages $ ? $ ? $ ? $ ? $ ? $ ? $ ?

$ ? $ ? $ ? $ ? $ ? $ ? $ ?

In-state $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Fringe benefitsOut-of-state $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Consumable non-medical supplies $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Consumable medical supplies $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Cost of Capital (debt service) $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Over-the-counter medications $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Prescription medications $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Malpractice insurance $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Other insurance $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Utilities $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Office equipment $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Clinical equipment $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Profits $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Etc…… $ ? $ ? $ ? $ ? $ ? $ ? $ ?

Etc…….

Changes in these lines constitute reimbursement control, not "cost control."

This is the only point at which real "cost control" can take place.

Nursing Homes(A)

Private Practioners(B)

Pharmacies(C)

Hospitals(D)

Independent Laboratories

(E)

CommunityHealth Centers

(F)

Commercial Health Insurers

(D)

Other Public Programs

(C)

State Medicaid Program

(B)

Medicare(A)

Investment Portfolios(E)

Private Sector Employers (D)

State Treasury(C)

Federal Treasury(B)

County Treasury(A)

Individuals(C)

Business Owners & Employees

(B)

Individual and Business Taxpayers

(A)

56

St. Joseph Hospital, 2001Nashua, NH

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Percent of Gross Charges by Payer

% o

f C

ost

Pai

d

Third Party / Insurance55%

Self-Pay5%

Medicare34%

Medicaid2%

Bad Debt & Charity4%

Net operating income of $10.8 million on net revenue of $91.4 million

0%

57

Cottage Hospital, 2001Woodsville, NH

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Percent of Gross Charges by Payer

% o

f C

ost

Pai

d

Third Party / Insurance34%

Self-Pay8%

Medicare44%

Medicaid9%

Bad Debt & Charity5%

Net operating loss of $0.8 million on net revenue of $13.5 million

0%

58

Franklin Hospital, 2001

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Percent of Gross Charges by Payer

% o

f C

ost

Pai

d

Third Party / Insurance34%

Self-Pay6%

Medicare46%

Medicaid9%

Bad Debt & Charity6%

This hospital had a net operating loss of $6.2 million on net revenue of $15.0 million

0%

59

Potentially Misleading !!

Is a hospital’s shortfall caused by reimbursement that is low or by a cost structure that is high?

We don’t know!

Hospital B, 2001

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Source of Payment

% o

f C

os

t P

aid

Self-Pay5%

Medicare51%

Medicaid7%

Bad Debt & Charity6%

Third Party / Insurance

31%

This hospital had a net operating loss of $2.7 million on net revenue of $20.5 millionHospital A, 2001

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Source of Payment

% o

f C

os

t P

aid

Third Party / Insurance58%

Self-Pay2%

Medicare31%

Medicaid4%

Bad Debt & Charity3%

Other 3%

190%

This hospital had a net operating gain of $4.7 million on net revenue of $55.1 million