1 financial management and audit anne sherman pat dehoop kal marchi april 13, 2010

TRANSCRIPT

1

FINANCIAL MANAGEMENTAND AUDIT

ANNE SHERMANPAT DEHOOPKAL MARCHI

APRIL 13, 2010

2

COURSE TOPICS

1. Policies2. Financial Management3. Cost Transfers4. Effort Reporting5. Closeout Procedures and Reports6. Audits

3

1. POLICIES

• Federal- OMB Circular A-21- OMB Circular A-110- OMB Circular A-133

• Federal Demonstration Partnership (FDP)• State of Texas Laws and Regulations• Agency/Sponsor Policies• University Policies

4

RULES GOVERNING CONTRACT AND GRANT FUNDS

Individual Agreement

Terms

University Policies & Procedures

Sponsor Cost Policies

Federal Cost Policies

5

OMB CIRCULAR A-21COST PRINCIPLES

• Direct and F&A Cost

• Reasonable, Allowable and Allocable

• Cost Accounting Standards (CAS)

6

OMB CIRCULAR A-21 COST ACCOUNTING STANDARDS (CAS)

• 501 – Consistency in Estimating, Accumulating, And Reporting Cost

• 502 – Consistency in Allocating Costs Incurred for the Same Purpose

• 505 – Accounting for Unallowable Costs

• 506 – Cost Accounting Period

7

OMB CIRCULAR A-110 UNIFORM REQUIREMENTS

OMB Circular A-110 contains administrative management standards for research grants.

8

OMB CIRCULAR A-110 UNIFORM REQUIREMENTS

• Financial and Program Management- Payment Methods, Cost Sharing, Program

Income

• Reports and Record Retention- Financial Reporting, Retention Requirements

9

OMB CIRCULAR A-110UNIFORM REQUIREMENTS

• Termination and Enforcement

• After-the-Award Requirements- Closeout Procedures

(90 Day Requirement)

10

OMB CIRCULAR A-133 AUDIT REQUIREMENTS

OMB Circular A-133 requires independent, regularly scheduled audits of federally funded research and student financial aid programs. Annual audits include reviews of internal controls and compliance tests of financial activity.

11

OMB CIRCULAR A-133AUDIT REQUIREMENTS

• Consistency and Uniformity

• Audit

• Auditees

• Auditors

12

AGENCY POLICY

• Agency Requirements

• Expanded Authorities

• Federal Demonstration Partnership (FDP)

• Agency Specific FDP Guidelines

13

STATE OF TEXAS & UNIVERSITY POLICY

• State of Texas

• Board of Regents

• UH Systems (SAMs)

University of Houston (MAPP) UH – Clear Lake UH – Downtown UH – Victoria UH – System at Fort Bend

14

2. FINANCIAL MANAGEMENT

• New Award Processing

• Award Cost Center Information

• F & A Cost Set-Up

15

Negotiation/Acceptance

Log in Award Document

Review

Negotiation

Acceptance

Prepare Notice of Award

Award Set-UpOffice of Contracts and Grants

Create Account

Issue Noticeof Award

to PI

AwardIssued to

UH AWARD PROCESSING AT UH

- Performs research- Initiates expenditures- Technical reports- Continuations- Renewals

Dept:

- Post award management- Process expenditures- Approve expenditures- Record-keeping - Reconcile accounts

Project ManagementOCG:

RFS:- Invoices- Financial Reports- Close-Outs- Audits

- Post-Award admin.- Approves expenditures- Subcontracts- Prior approvals- Award adjustments

PI:

16

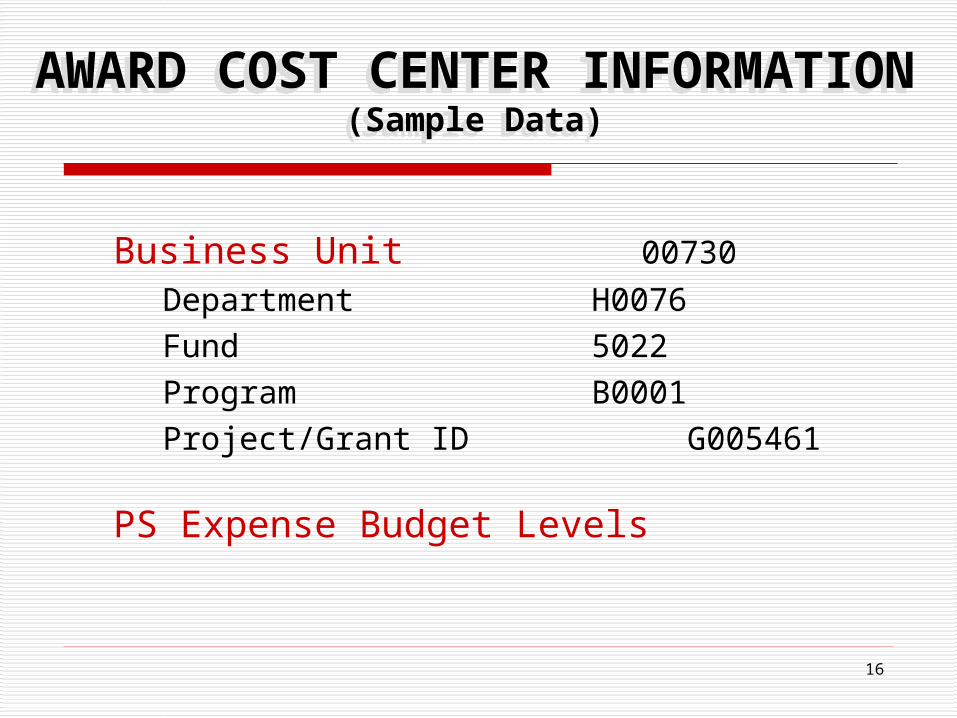

AWARD COST CENTER INFORMATION (Sample Data)

AWARD COST CENTER INFORMATION (Sample Data)

Business Unit 00730

Department H0076Fund 5022Program B0001Project/Grant ID G005461

PS Expense Budget Levels

17

F&A COST SET-UP

• Identify F&A Cost Basis

• Determine Exempt Categories

• Specify PS Account Codes to be Excluded or Included

18

F&A COST RATE EXCEPTIONS

• F&A Reduction

• F&A Waiver

• Sponsor Mandated Rate Restrictions

19

UH F&A COST ANALYSIS

• Are there exempt categories affecting F&A costs?

• Have we prepared an F&A (IDC) analysis?

• Is agency prior approval required to reallocate costs between direct to F&A?

20

3. COST TRANSFERS

Cost transfers (reallocations) occur when goods or services originally paid for under one award (or department cost center) are subsequently transferred to another award (or department cost center).

21

COST TRANSFERS

Once an expense entry has been recorded in a cost center in the general ledger, it is appropriate to make expenditure adjustments only in the following situations:

To correct an erroneous recording

To redistribute certain departmental costs that are applicable and allowable to a sponsored project (e.g. long distance)

22

COST TRANSFERS

Cost transfers involving federal and state funds should be

A V O I D E D

altogether or kept to a minimum. Expenses should be charged directly to the cost centers which they benefit.

Processing cost transfers should not be an SOP for managing your cost centers!

23

COST TRANSFERS “DON’Ts”

Some invalid reasons for requesting cost transfers:• Lack of planning or projecting – convenience

(i.e., yearly review)

• Lack of funds on a different grant

• Unspent balances at or near expiration

• Waiting for a new award, so “I will just use this other one until then.”

• F & A advantage

“My ARP/ATP doesn’t charge IDC so I will move my salary and wages to that award from DOD and move my equipment from my ARP/ATP to my DOD award.”

24

COST TRANSFER GUIDELINES

Cost transfers must be fully explained, justified and approved by the Principal Investigator, the certifying signatory and the Office of Contracts and Grants.

Supporting documentation as required by sponsor and UH Policy should be on file with transfer request forms.

25

COST TRANSFER GUIDELINES

Cost transfers are a red flag to an auditor. If you have a cost that should be direct

charged to more than one cost center, it is better to allocate it to those cost centers then, rather than waiting until after the charge has posted to reallocate it.

When you expect a new award, you should not temporarily use an existing one. We recommend interim funding to deal with that circumstance.

26

COST TRANSFER GUIDELINES

If an employee transfers from one award to another:

• Process a PAR and position request (if needed)

immediately.

• Do not allow payroll to continue to charge the original cost center; do not reallocate later.

• Make correction in the month following the error.

27

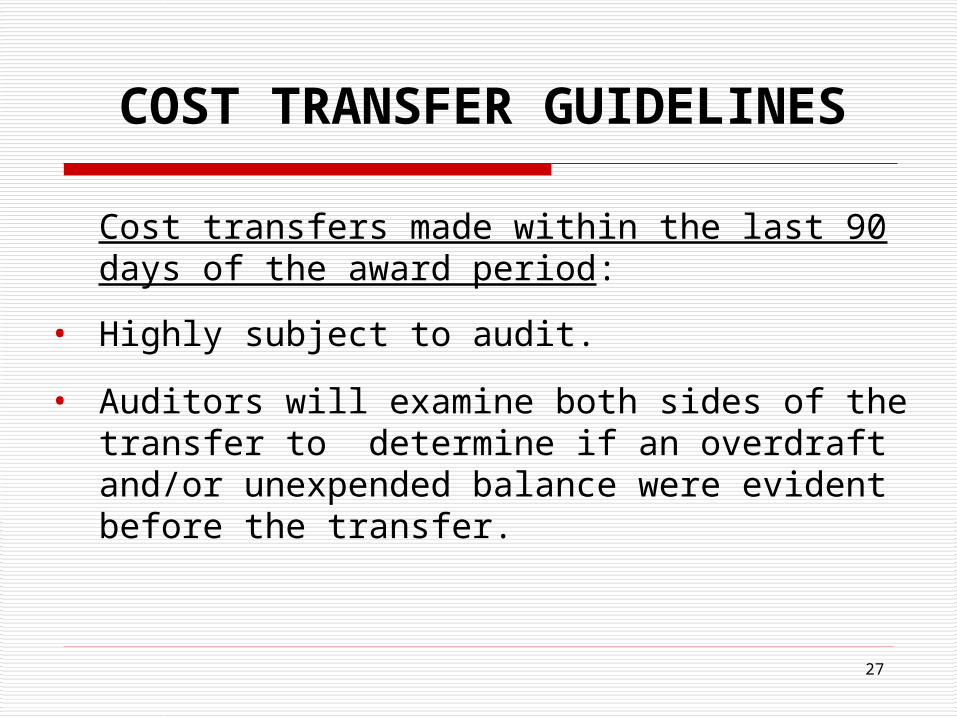

COST TRANSFER GUIDELINES

Cost transfers made within the last 90 days of the award period:

• Highly subject to audit.

• Auditors will examine both sides of the transfer to determine if an overdraft and/or unexpended balance were evident before the transfer.

28

COST TRANSFERS

• Cost transfers are categorized as . . .

Payroll Transfers

Non-Payroll Transfers

29

PAYROLL TRANSFERS

• Justification and documentation required

• Authorized Signatures

• Payroll Account Reallocation Form

• Still accomplished on paper, not through Work Flow

30

NON-PAYROLL TRANSFERS

Reasons for non-payroll transfer:

• Overdrafts

• Correcting a data entry error

• SCR from recharge center

• Account Code Change (i.e. equipment fabrication costs)

• Accomplished through WorkFlow

31

4. EFFORT REPORTING

• After-the-fact Effort Reporting

• Quarterly

• Directly paid from Sponsored Project

• Cost Shared Effort

• Reporting through RD2K

• Paper Signature Certification (biweekly personnel still use time sheet)

32

5. CLOSING PROCEDURES AND REPORTS

• Closing Notices

• Cost Share Reporting

• Required Documentation(non-cost share)

• Closing Process

33

CLOSING NOTICES

Advance Notice

90-60-30 day notice prior to grant end date to Business Administrators and PI providing guidance on how to handle the closeout of the award

34

CLOSING NOTICES

At expiration, a notice goes to Business Administrator with copy to PI notifying them that account is expired and is or will be frozen.

35

CLOSURE NOTICES

In the month that the final report/invoice is due to the Sponsor, Research Financial Services will request from Business Administrator and PI:

• cost-share documentation or • any other required documents for preparation of

the final report or invoice.

36

FINAL INVOICE

Research Financial Services generates final financial invoice or report and sends to Business Administrator and PI for review before submission to the sponsor.

Department Business Administrator and PI have 4 working days to respond before submission.

37

COST SHARE REPORTING

Cost Sharing – must be certified by DBA and copies of expenditure documents must be maintained in the department and supplied to OCG upon request. Some projects require backup documentation to be submitted with invoices.

• UH Participation• Matching• Third-party contributions

38

CLOSING PROCESS

After project end date:

• Project-to-date account reconciliation – Department• Unallowable review – Department• F&A Reconciliation – Research Financial Services• Cost Share Report – Department

• Financial Report and Invoice – Research Financial Services

39

CLOSING PROCESS

• Other closing documents:

Property Report

Invention/Patent Report

Contractor Release

Assignment of Rebates, Refunds, and Credits

40

CLOSING PROCESS

• Sponsor Approval of Final Report/Invoice

• Final Payment Received

• Cash Reconciliation

• Residual Funds transfer (for fixed cost awards)

• RD2K Close and PeopleSoft Inactivation

41

6. AUDIT

42

AUDITS COULD BE PERFORMED BY THE FOLLOWING:

• Sponsor

• An A-133 Auditor such as the State Auditors Office or an external CPA firm like KPMG

• The UH Internal Auditing department

43

AUDIT REQUEST ITEMS

A request from the sponsor or those conducting a single federal audit could ask for any or all the following information:

• Desk procedures

• List of accounts

• List of contracts and grants

• Copy of log maintained by the person monitoring contract performance

44

AUDIT REQUEST ITEMS

• Copies of the “Disclosure or Potential Conflict of Interest Form” and the “Related Party Disclosure Form”

• Copy of the most recent account reconciliation

• Copies of the most recent time and effort reports

• Documentation of cost transfers

• Other items

45

UH INTERNAL AUDIT REQUESTS

A request from the UH Internal Audit department will also cover the following areas:

• Department Policies and Procedures Baseline Standards

• Reconciliation of Account Balances

• Cash Handling

• Petty Cash

46

UH INTERNAL AUDIT REQUESTS

• Long Distance/Mobile Phone Charges

• Contract Administration

• Property Management

• Conflict of Interest/Related-Party Disclosure

• Accounts Receivable

• Negative Budget or Fund Balances

47

AREAS OF POSSIBLE EXAMINATION

• Activities allowed or un-allowed• Allowable Cost / Cost Principles• Cash Management• Davis-Bacon Act (wages of workers on federal

construction project must be not less than local wages)• Eligibility (unique to each program)• Segregation of certain expenses (i.e. Participant

Support)• Equipment and Real Property Management• Matching, Level of Effort, and Earmarking

48

AREAS OF POSSIBLE EXAMINATION

• Period of availability of federal funds• Procurement, Suspension, and Debarment• Program Income• Real Property Acquisition/Relocation assistance• Reporting – Technical or Financial• Sub-recipient Monitoring• Special Tests and Provisions (usually unique to each

program and involve laws, regulations, and the provisions of contract or grants)

49

AUDIT RED FLAGS

• Cost overruns

• Inadequate documentation of costs

• Cost transfers

• Costs incurred outside of funding period

• Recharge activities with financial surpluses

• Incomplete Effort Reports

50

AUDIT RED FLAGS

• Recharge rates not approved or not applied consistently to all users

• Account coding errors

• Unallowable costs charged to project

• Personnel Activity Request (PARs) not property certified

• Technical reports not filed on time

51

ADVERSE AUDIT FINDINGS(Questioned Costs)

• Unallowable costs

• Undocumented costs

• Unapproved costs

• Unreasonable costs

52

ADVERSE AUDIT FINDINGS(Examples)

• Program income not deposited to a designated program income cost center for a particular project

• Indirect costs charged as direct costs (i.e. personnel)

• Improper transfers from grants accounts

• Unauthorized equipment purchases

• Improper asset disposal methods

53

POTENTIAL IMPACT OF ADVERSE AUDIT FINDINGS

• Cost disallowances• Statistical extrapolation of errors in an audit test

sample• Withdrawal of funding• Increased scrutiny for future funding – Audit

finding may have to be disclosed with future applications and proposals

54

WHAT TO DO NOW TO PREPARE?

• Do not wait for the Auditors. Prepare NOW.

• Read over the handouts

• Conduct an audit of your own operations

• Audit each other

• Have Research Financial Services conduct an informal review

55

AVOIDING AUDIT PROBLEMS

• Review award documentation and setup• Monitor financial activity and compare to budget• Complete effort reports and reconcile to payroll• Keep PI informed of the financial status of their

contracts and grants• Avoid cost transfers• Submit timely reports to sponsoring agencies• Ask for assistance

56

COMMON AUDIT FINDINGS

• Improper draw-downs• Program conditions or eligibility requirements not met• Untimely reporting to sponsoring agencies• Undocumented / late cost transfers• Fixed assets not managed properly including asset

disposal• Administrative processes and procedures not followed• Effort reports not completed or inconsistent with payroll

records

Source: UCSB Internal Audit Services

57

SOURCES

• Board of Regents Policy• National Council of University Research

Administrators (NCURA)• Society of Research Administrators (SRA)• University of California Santa Barbara Training

Program• Office of Management and Budget Circulars A-21, A-

110, and A-133