1 finances and the college student ncasfaa/scasfaa fall conference november 6-8, 2006 brad barnett...

Post on 20-Dec-2015

214 views

TRANSCRIPT

11

Finances and the College Finances and the College StudentStudent

NCASFAA/SCASFAAFALL

CONFERENCENovember 6-8, 2006

Brad BarnettSenior Associate DirectorJames Madison UniversityOffice of Financial Aid &

ScholarshipsHarrisonburg, Virginia

22

ObjectivesObjectives• Learn about the format used in “money

management” sessions at JMU• Review strategies to keep the student’s

attention • Discuss partnerships that have been

created with other campus offices to provide an avenue for reaching students

33

JMU & Financial Aid JMU & Financial Aid OfficeOffice

James Madison University– Approximately 16,000 students, of which

15,000 are undergraduates

– Primarily 18-22 year olds who graduate high school, enroll full-time in college, and complete college in 4-5 years

– Male = 40% & Females = 60%

– In-state = 70% & Out-of-state = 30%

– Minority = 10%

44

Session TypesSession Types

• Discussion varies depending on audience– Freshmen– Upperclassmen

• Will focus on freshmen for the purposes of this presentation

55

Understanding FreshmenUnderstanding Freshmen

• A lot of firsts:– Living without parents– Responsible for finances– Able to make decisions without being

“checked on”

• Many have never balanced a checkbook • Think about the financial woes of the

parents you work with…that’s where your students are coming from

66

AttendanceAttendance

• Voluntary• Mandatory

(Partnerships)– IS 202– Athletic Office– Student Organization– Passport Events

77

Basic Set UpBasic Set Up

• 1 to 1 ½ hour sessions• Keep class to approximately 20 – 25

students• Focus on Kinesthetic Learning…hands on!• Movable desks• Chalk board or dry erase board• Paper and pencils for students• Avoid PowerPoint whenever possible

88

BeginningBeginning

Always start by asking, “How many people have created a budget?”

Question: Out of 25 students, how many students do you think have created a budget by this point in their lives?

Answer: Generally no more than a couple

99

Financial ConcernsFinancial Concerns

• Break class into 4 or 5 working groups

• Ask them to develop a list of their top five financial concerns, which can be:– Concerns while in college– Concerns for post-college

• Have each group report and write on the board

1010

Let’s Do It!Let’s Do It!

• Break into groups• Develop a list of the 5 most common

financial concerns you think college students have

• These can be– Concerns while in college– Concerns for post-college

• Paying tuition does not count…that’s a given

1111

Income – Let’s Do It!Income – Let’s Do It!

• Develop a list of the 5 most common income sources for college students

• Generally receive a lot of duplicate responses from the groups

1212

Expenses – Let’s Do It!Expenses – Let’s Do It!

• Develop a list of the 5 most common expenses for college students

• Generally receive a lot of duplicate responses from the groups

1313

Congratulations!Congratulations!

• You just created the framework for a budget– Goals (concerns)– Income– Expenses

• Assign dollar amounts to these items and the budget is created

• Goal of exercise is to take the fear out of budgeting

1414

Typical JMU Freshmen Typical JMU Freshmen ResponsesResponses

Concerns:• Food• Housing• Credit cards• Student loans• Insurance • Not running out of

money• Saving• Paying tuition (this is

a given)• Buying a house• Having a family• Graduate school

Income:• Parents (could be

monthly or lump sum)

• Financial aid (usually disbursed lump sum)

• Summer jobs (earned in summer and sitting lump sum in bank)

• Gambling (sporadic)

• Part time jobs while in school (paid on set schedule)

Expenses:• Food (dining out)

• Beer

• Taxies

• Clothes

• Hair/Nails

• Porn

• Entertainment

• Cell phones

• Dating

• Electric

• Gas

• Rent

• Car (gas, insurance, etc)

1515

Teaching NoteTeaching Note

• While groups are working on lists, walk around the room and listen

• Interact to develop a rapport

• Make mental notes of discussions you hear that you can pull into the instruction

• Let the class guide the topics discussed as much as possible to keep their interest

1616

Additional DiscussionAdditional Discussion

• Use your mental notes to make a connection

• Stress difficulty of planning for items in “concern” list if cannot budget

• Get a handle on it now before it’s too late

• Tell stories of students who got in trouble due to poor budgeting skills

• Focus on topics in “concern” list

1717

Earnings vs. SpendingEarnings vs. Spending

How much you spend is much more important than how much you earn. This is often referred

to as “living within your means.”

1818

Credit CardsCredit Cards

• Positive– Points– Ease– Help with credit score (side bar about FICO)– Loss (versus cash)

• Negative– Easily accumulate debt if do not budget– Ease– Damage credit score

1919

Ways to Establish CreditWays to Establish Credit

• Credit Card payments

• Student Loan payments

• On-time payments with all bills, including:

– Housing

– Utilities

– Medical

– Financed purchases

2020

Establishing Credit cont...Establishing Credit cont...

• Communication is the key to maintaining a positive credit file and may help to avoid student loan default

• Paying bills in a timely manner is important to your future credit needs

2121

Credit Card InterestCredit Card Interest

Scenario:• $3,000 charged on a credit card

• Interest rate of 19.8%

• You pay $50 per month

• It will take 24 years to pay off the card

• At the end of at time you would have paid back $14,070 ($11,070 in interest)

(source: www.visa.com)

2222

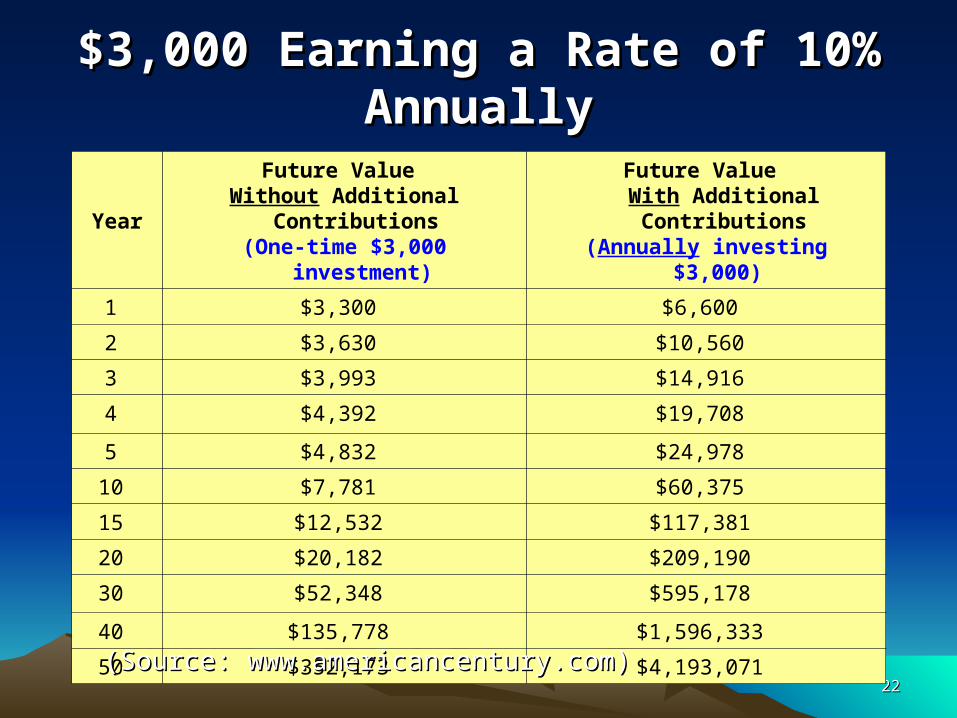

YearFuture Value

Without Additional Contributions (One-time $3,000 investment)

Future Value With Additional Contributions

(Annually investing $3,000)

1 $3,300 $6,600

2 $3,630 $10,560

3 $3,993 $14,916

4 $4,392 $19,708

5 $4,832 $24,978

10 $7,781 $60,375

15 $12,532 $117,381

20 $20,182 $209,190

30 $52,348 $595,178

40 $135,778 $1,596,333

50 $352,173 $4,193,071

$3,000 Earning a Rate of 10% $3,000 Earning a Rate of 10% AnnuallyAnnually

(Source: www.americancentury.com)(Source: www.americancentury.com)

2323

Senior Group TopicsSenior Group Topics

• Cost of living comparisons

• Insurance (health, life, disability, etc.)

• Retirement savings (Roth IRA, 401k, etc.)

• Mortgage

• Cost of a family

• Pay off student loans

• Graduate school

2424

ConclusionConclusion

• Don’t lecture• Be hands on• Make it real• Be VERY basic• Teach to your audience• Ask open ended questions• Involve the students• Shock value is good