1 fiduciary aspects of social investing lloyd kurtz sr. portfolio manager nelson capital management...

TRANSCRIPT

1

Fiduciary Aspects of Social Investing

Lloyd KurtzSr. Portfolio ManagerNelson Capital Management

Santa Clara County Estate Planning CouncilApril 23, 2007

2

Topics

Background on Social Investing Diversification Performance Evidence of Social Outperformance?

3

Background on Social Investing

4

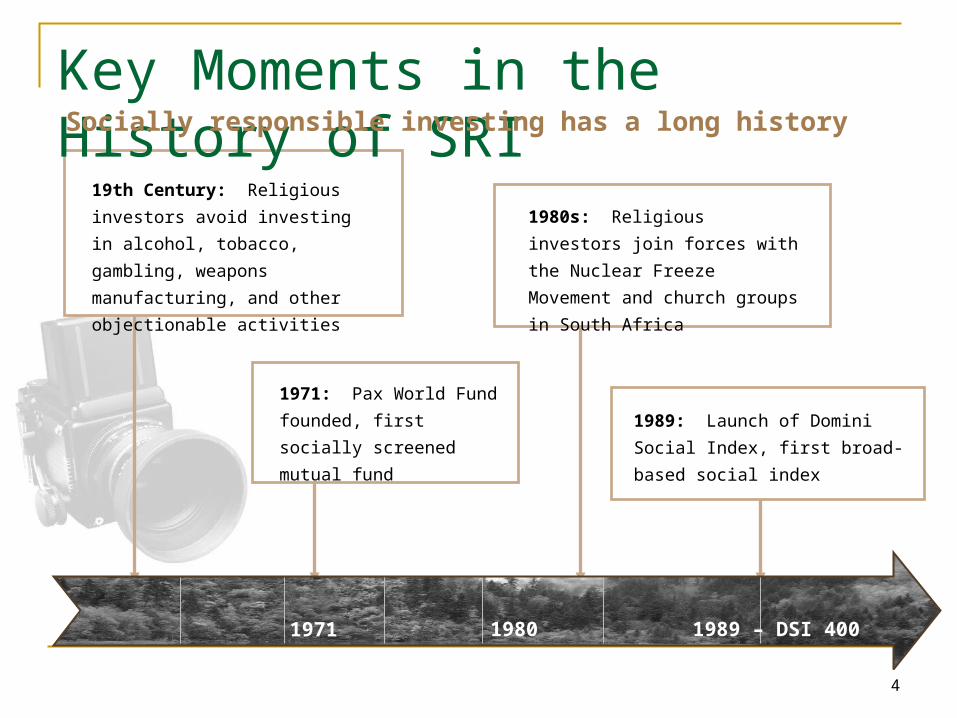

1971: Pax World Fund

founded, first socially

screened mutual fund

1980s: Religious investors join

forces with the Nuclear Freeze

Movement and church groups in

South Africa

1989: Launch of Domini Social

Index, first broad-based social index

1971 1980 1989 – DSI 400

19th Century: Religious investors

avoid investing in alcohol, tobacco,

gambling, weapons manufacturing,

and other objectionable activities

Key Moments in the History of SRISocially responsible investing has a long history

5

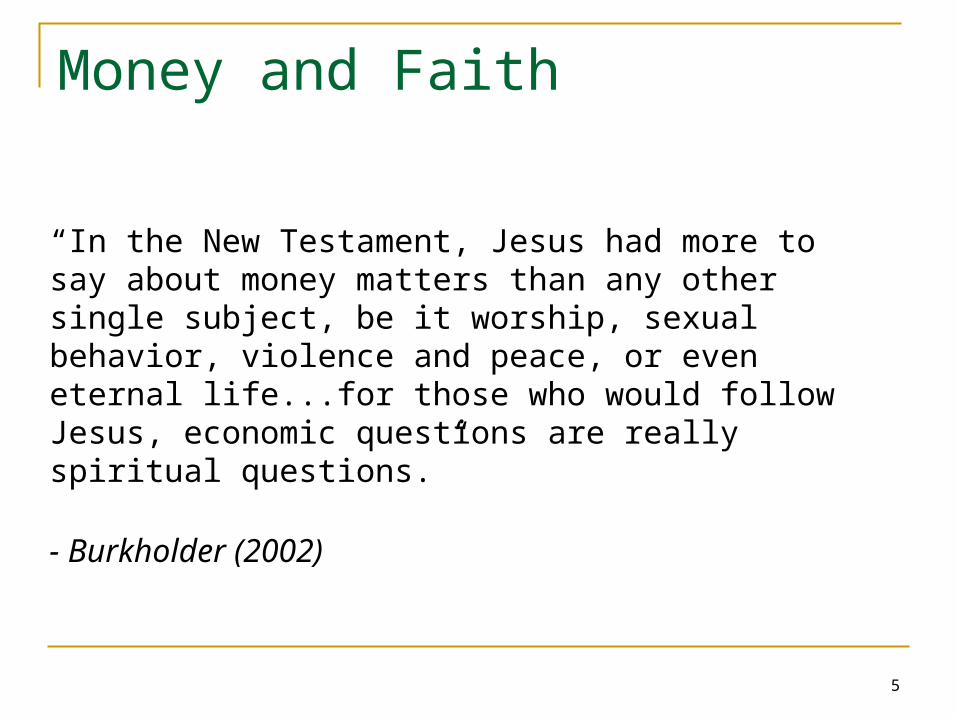

Money and Faith

“In the New Testament, Jesus had more to say about money matters than any other single subject, be it worship, sexual behavior, violence and peace, or even eternal life...for those who would follow Jesus, economic questions are really spiritual questions.”

- Burkholder (2002)

6

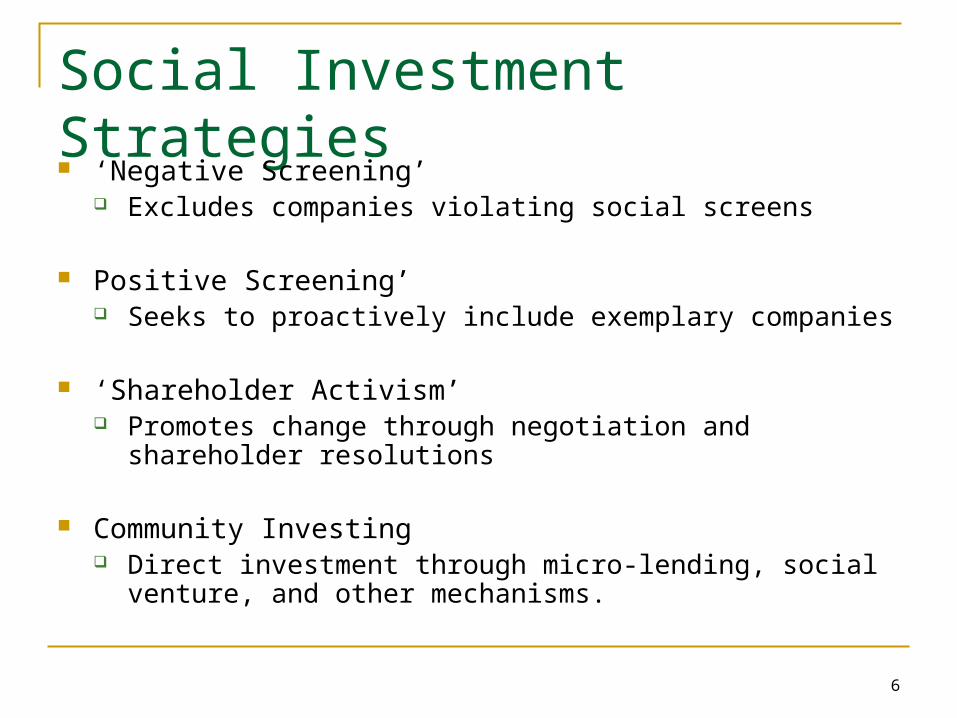

Social Investment Strategies

‘Negative Screening’ Excludes companies violating social screens

Positive Screening’ Seeks to proactively include exemplary companies

‘Shareholder Activism’ Promotes change through negotiation and shareholder

resolutions

Community Investing Direct investment through micro-lending, social venture, and

other mechanisms.

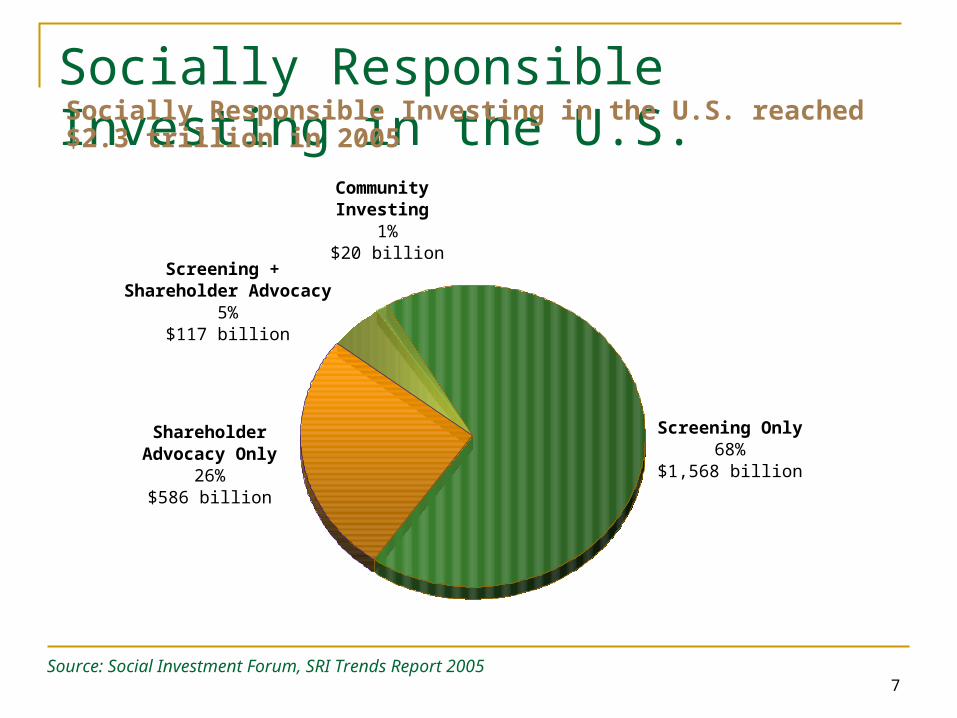

7Source: Social Investment Forum, SRI Trends Report 2005

ShareholderAdvocacy Only

26%$586 billion

Socially Responsible Investing in the U.S.

Screening + Shareholder Advocacy

5%$117 billion

Screening Only68%

$1,568 billion

Community Investing

1%$20 billion

Socially Responsible Investing in the U.S. reached $2.3 trillion in 2005

8

Types of Social Investors

Religious Organizations Catholic

Methodist

Christian Science

Islamic

Family Offices

Non-profits (“Mission-Based Investing”)

Institutional investors in SRI include:

9

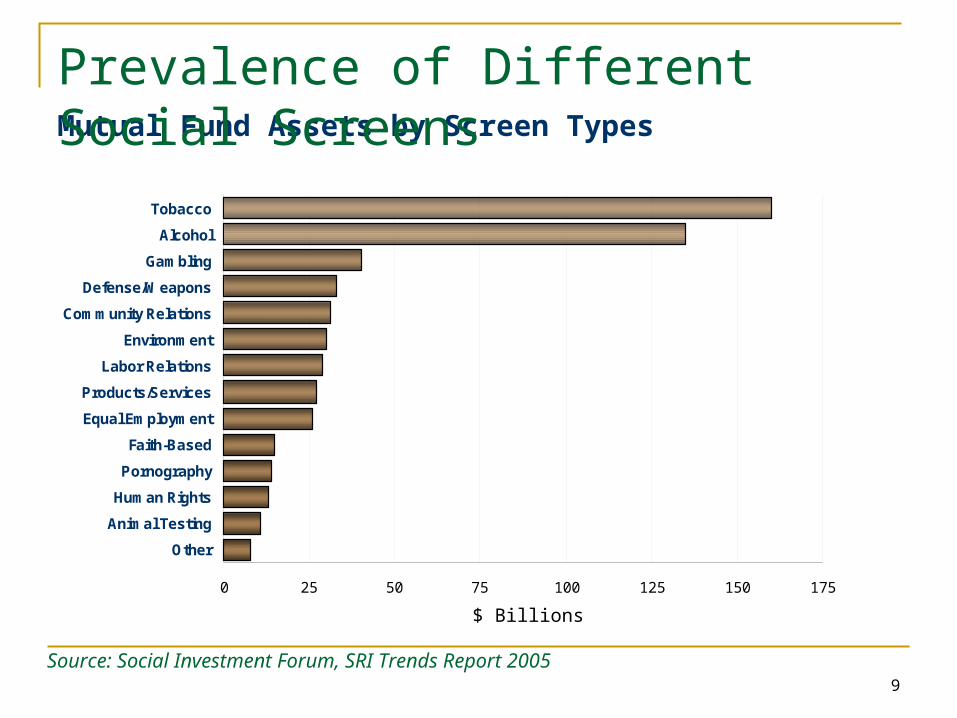

0 25 50 75 100 125 150 175

Other

Animal Testing

Human Rights

Pornography

Faith-Based

Equal Employment

Products/Services

Labor Relations

Environment

Community Relations

Defense/Weapons

Gambling

Alcohol

Tobacco

Mutual Fund Assets by Screen Types

Source: Social Investment Forum, SRI Trends Report 2005

Prevalence of Different Social Screens

$ Billions

10

Diversification

11

ERISA

“A fiduciary must diversify the plan investments so as to minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so.”

12

Uniform Prudent Investor Act of 1994 “A trustee shall diversify the investments of

the trust unless the trustee reasonably determines that, because of special circumstances, the purposes of the trust are better served without diversifying.”

13

CFA Institute

“Diversify. Members and candidates should diversify investments to reduce the risk of loss, unless diversification is not consistent with plan guidelines or is contrary to the account objectives.”

- CFA Institute Standards of Practice Handbook, 2007

14

Two Areas of Apparent Latitude No quantitative guidance as to how much

diversification is enough. Some provision in the language for

exceptions based on the individual situation.

15

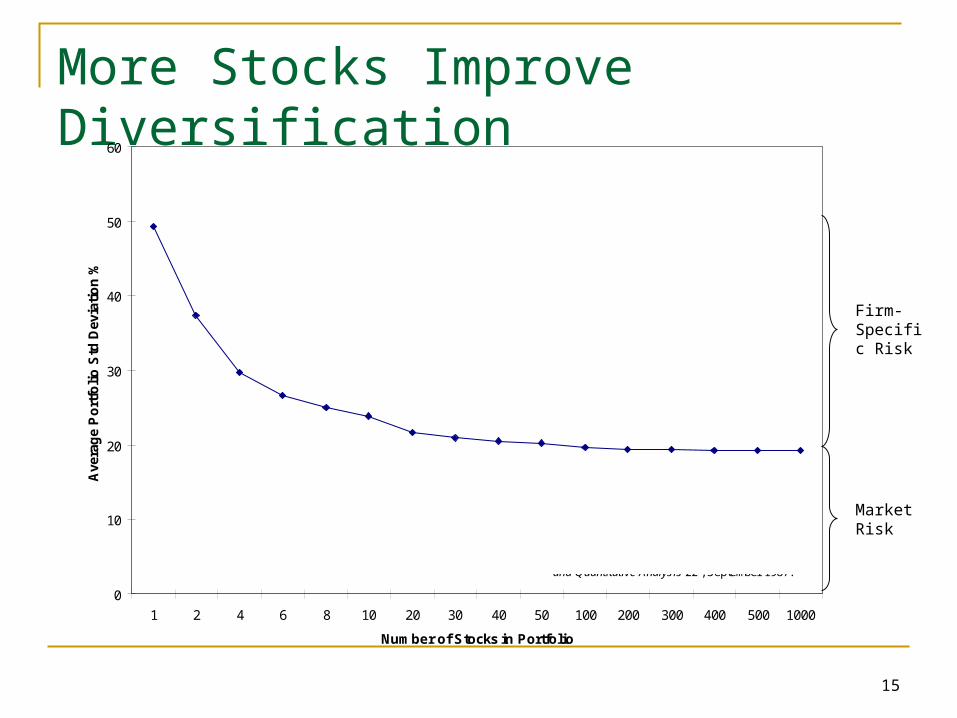

More Stocks Improve Diversification

0

10

20

30

40

50

60

1 2 4 6 8 10 20 30 40 50 100 200 300 400 500 1000

Number of Stocks in Portfolio

Ave

rag

e P

ort

foli

o S

td D

evia

tio

n %

Based on data in M. Statman, "How Many Stocks Make a Diversif ied Portfolio?" Journal of Finance and Quantitative Analysis 22 , September 1987.

Firm-Specific Risk

Market Risk

16

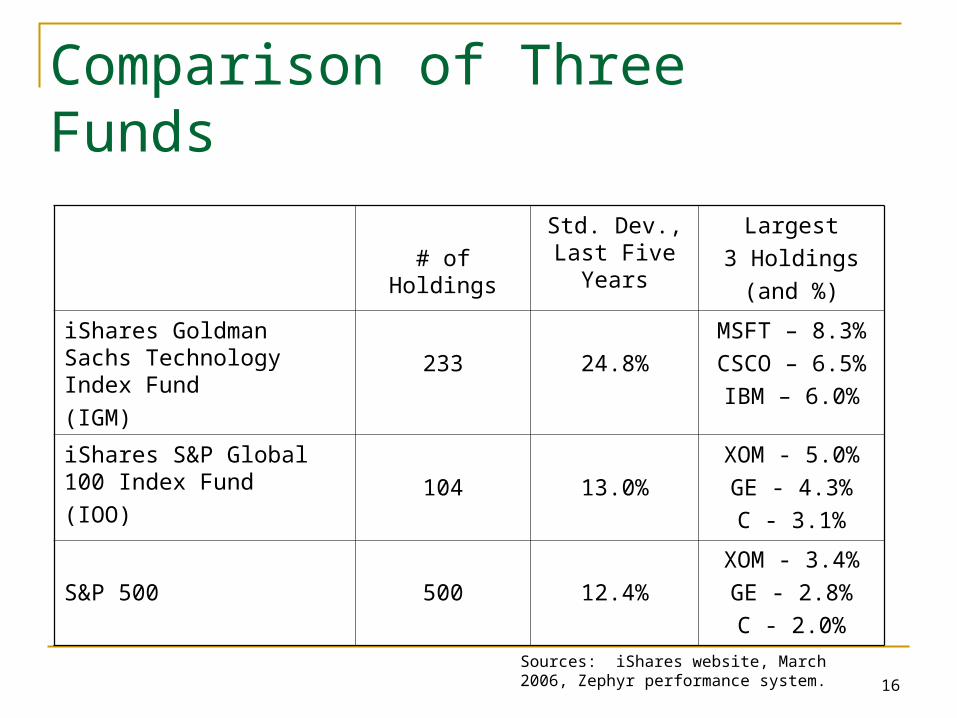

Comparison of Three Funds

# of Holdings

Std. Dev., Last Five Years

Largest

3 Holdings

(and %)

iShares Goldman Sachs Technology Index Fund

(IGM)233 24.8%

MSFT – 8.3%

CSCO – 6.5%

IBM – 6.0%

iShares S&P Global 100 Index Fund

(IOO)104 13.0%

XOM - 5.0%

GE - 4.3%

C - 3.1%

S&P 500 500 12.4%

XOM - 3.4%

GE - 2.8%

C - 2.0%

Sources: iShares website, March 2006, Zephyr performance system.

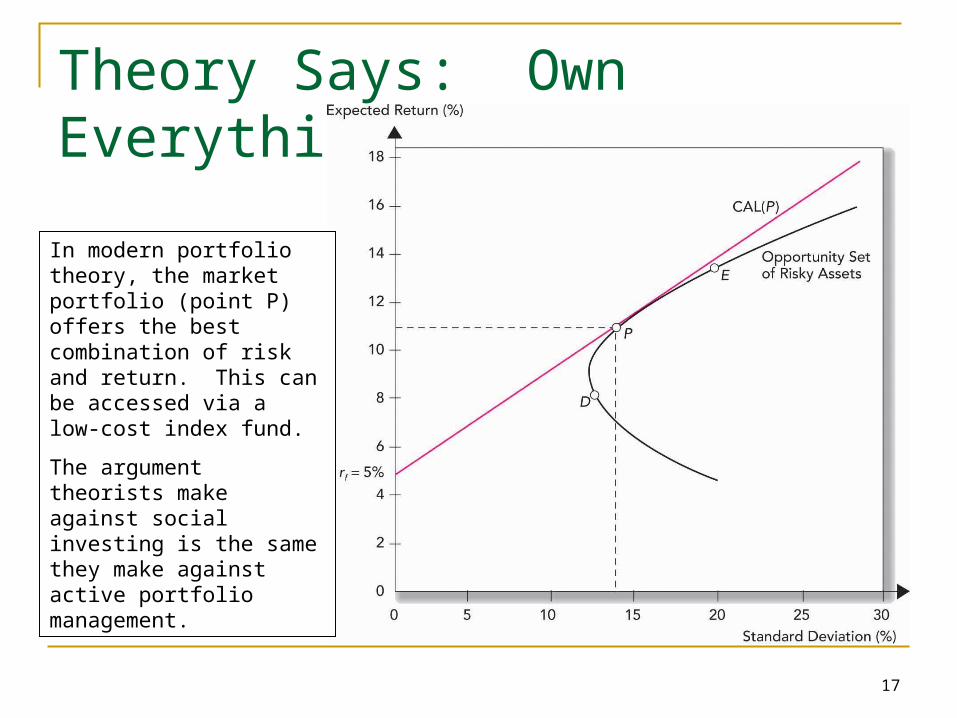

17

Theory Says: Own Everything

In modern portfolio theory, the market portfolio (point P) offers the best combination of risk and return. This can be accessed via a low-cost index fund.

The argument theorists make against social investing is the same they make against active portfolio management.

18

Performance

19

Sin Has its Rewards...

0%

50%

100%

150%

200%

250%

300%

350%

400%

S&P 500 S&P Tobacco S&P Brew ers S&P Casinos

To

tal R

etu

rn, 3

/97

- 3/

07

20

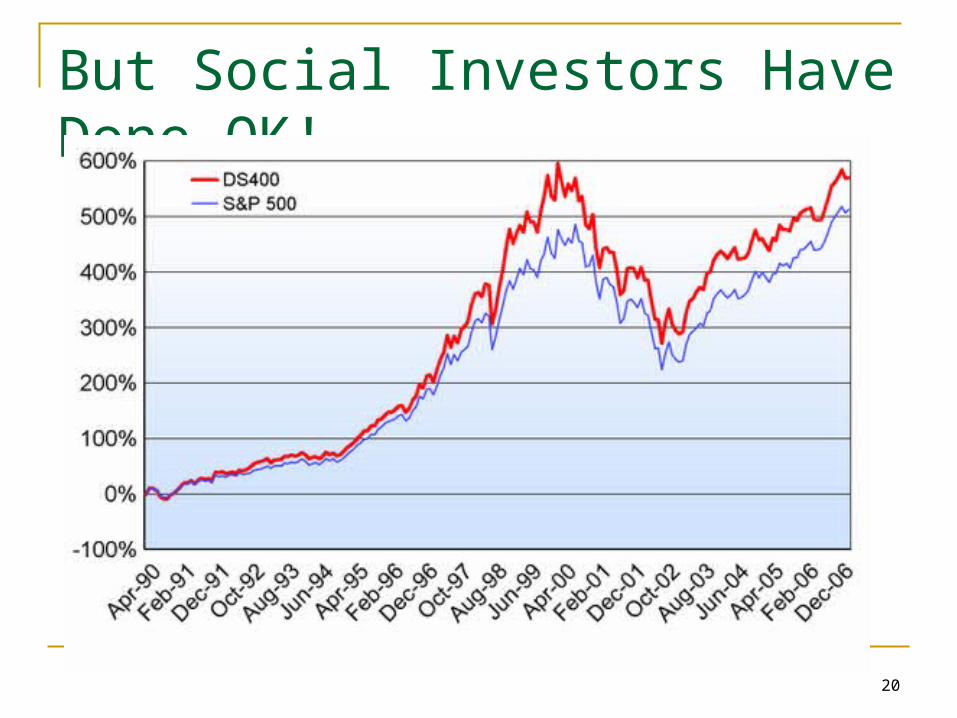

But Social Investors Have Done OK!

21

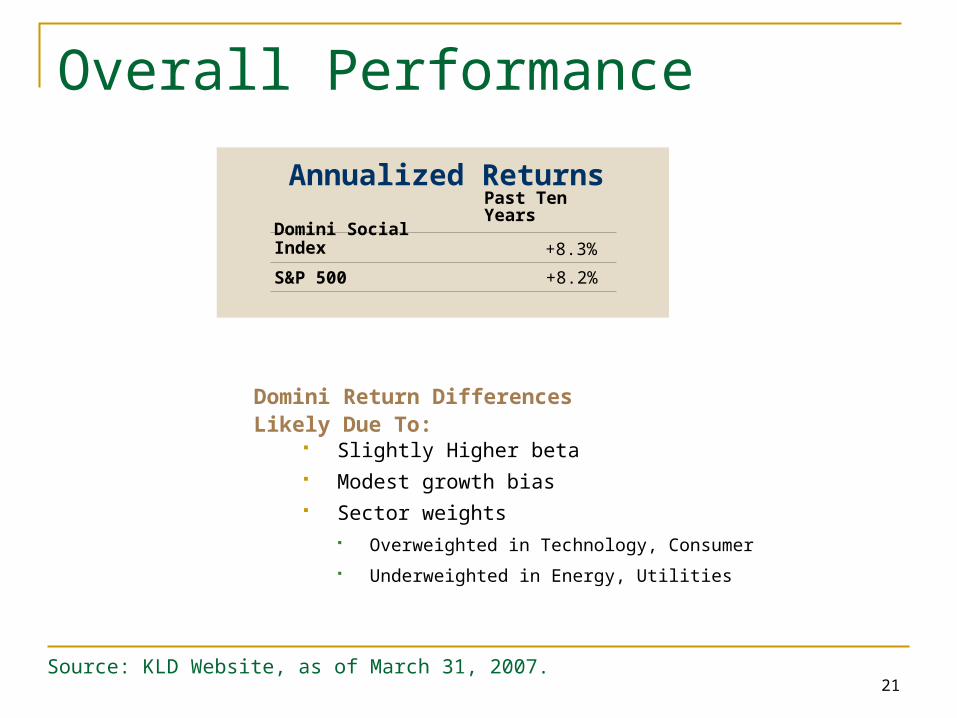

Overall Performance

Slightly Higher beta Modest growth bias Sector weights

Overweighted in Technology, Consumer

Underweighted in Energy, Utilities

Annualized Returns

Source: KLD Website, as of March 31, 2007.

Past Ten Years

+8.3%

+8.2%

Domini Social Index

S&P 500

Domini Return Differences Likely Due To:

22

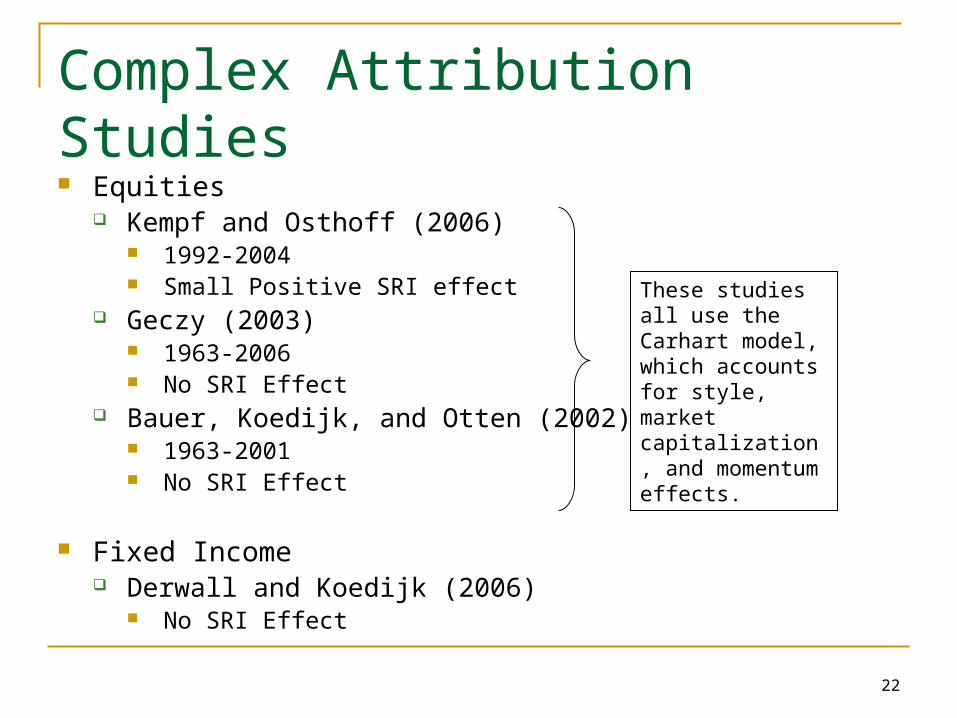

Complex Attribution Studies

Equities Kempf and Osthoff (2006)

1992-2004 Small Positive SRI effect

Geczy (2003) 1963-2006 No SRI Effect

Bauer, Koedijk, and Otten (2002) 1963-2001 No SRI Effect

Fixed Income Derwall and Koedijk (2006)

No SRI Effect

These studies all use the Carhart model, which accounts for style, market capitalization, and momentum effects.

23

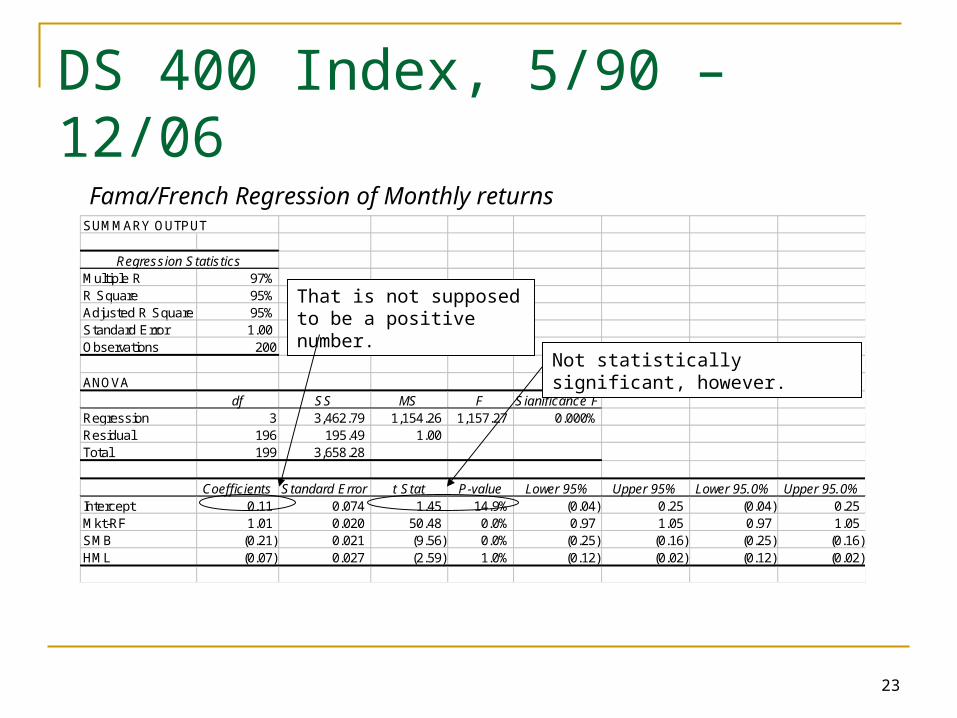

DS 400 Index, 5/90 – 12/06

SUMMARY OUTPUT

Regression StatisticsMultiple R 97%R Square 95%Adjusted R Square 95%Standard Error 1.00 Observations 200

ANOVAdf SS MS F Significance F

Regression 3 3,462.79 1,154.26 1,157.27 0.000%Residual 196 195.49 1.00 Total 199 3,658.28

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%Intercept 0.11 0.074 1.45 14.9% (0.04) 0.25 (0.04) 0.25 Mkt-RF 1.01 0.020 50.48 0.0% 0.97 1.05 0.97 1.05 SMB (0.21) 0.021 (9.56) 0.0% (0.25) (0.16) (0.25) (0.16) HML (0.07) 0.027 (2.59) 1.0% (0.12) (0.02) (0.12) (0.02)

Fama/French Regression of Monthly returns

That is not supposed to be a positive number.

Not statistically significant, however.

24

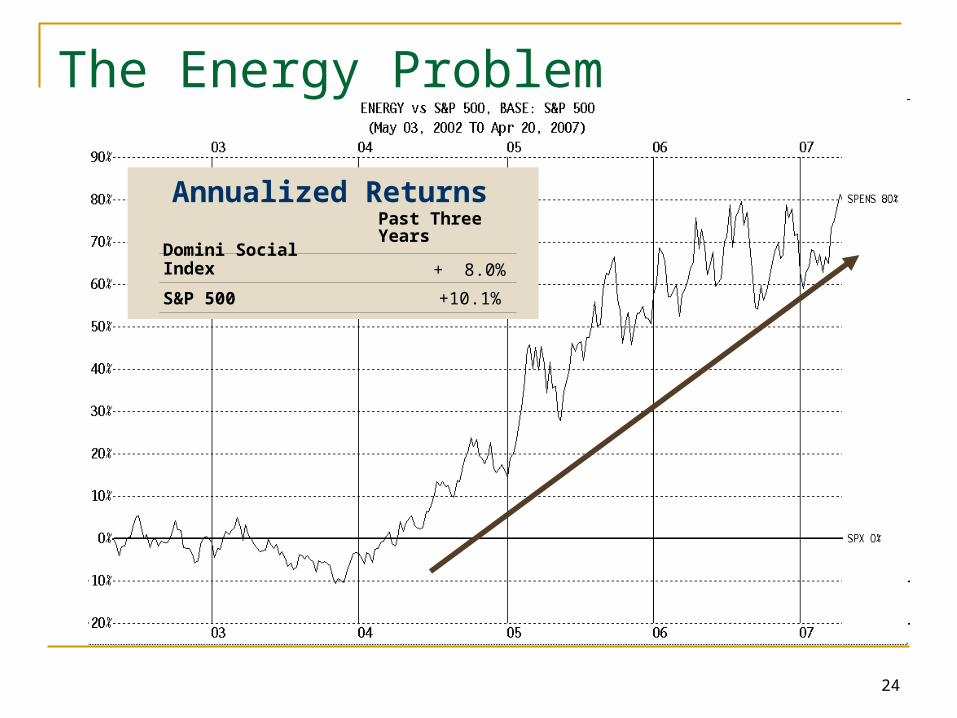

The Energy Problem

Annualized ReturnsPast Three Years

+ 8.0%

+10.1%

Domini Social Index

S&P 500

25

Evidence of Social Outperformance?

26

Two Interesting Areas

Environment Governance

27

Studies Showing an Environmental Effect Guenster,Derwall, Bauer, and Koedijk (2005)

1996-2002 time period Shows stocks ranked highly by Innovest had higher valuation ratios and

capital efficiency ratios.

Derwall, Bauer, and Koedijk (2005) 1995-2003 time period. Backtest shows highly-rated stocks outperformed lowly-rated ones.

Dowell, Hart, and Yeung (2000) Favorable impact on price/book ratios

Cohen, Fenn, and Konar (1997)

Russo and Fouts (1997)

28

Is There a CalPERS Effect?

29

Constructing the CalPERS Focus List Quantitative Screen

Stock Performance Capital Efficiency Corporate Governance

Qualitative Review Overall financial performance Valuation Strategic plans Management and board member relations Compensation Practices Other miscellaneous shareowner issues (including takeover defense)

Engagement Process – Since Exit is Impossible, Try Voice “CalPERS considers the engagement process to be a crucial component of

the overall Focus List Process. CalPERS makes a persistent effort to meet with the management and directors to discuss performance and governance issues. CalPERS will focus on reforming the company's governance practices with an emphasis on accountability, transparency, independence, and discipline.”

Source: CalPERS

30

Short-Term Impact

Barber finds a “small, but reliably positive” +0.25% effect on announcement date.

“My best estimate, based on conservative short-term market reactions, indicates CalPERS activism has resulted in total wealth creation of $3.1 billion between 1992 and 2005.”

31

Long-Term Impact

0

10

20

30

40

50

60

70

80

90

100

1 Day 2 Weeks 1 Month 6 Months 1 Year 2 Years 3 Years 4 Years 5 Years

$ B

illio

ns

Source: Barber (2006)

32

NotesBarber, Brad. “Monitoring the Monitor: Evaluating CalPERS’ Shareholder Activism.” Working Paper, University of California, Davis, March 2006.

Bauer, Rob, Kees Koedijk, and Roger Otten. "International Evidence on Ethical Mutual Fund Performance and Investment Style." Working Paper, January 2002.

Burkholder, J.R. “Biblical Faith and Investment: Toward a Theology for ‘Making Money.’” Mennonite Mutual Aid, 2002.Accessed at: http://www.mmapraxis.com/features/columns/feature_burkholder.html

Cohen, Mark, Scott A. Fenn, Shameek Konar. "Environmental and Financial Performance: Are They Related?" Working paper, May 1997.

Derwall, Jeroen, and Kees Koedijk. "Socially Responsible Fixed-Income Funds." Working Paper, Erasmus University, May 2006.

Derwall, Jeroen, Nadja Guenster, Rob Bauer, and Kees Koedijk. "The Eco-Efficiency Premium Puzzle." Financial Analysts Journal, March/April 2005.

Dowell, Glen, Stuart Hart, and Bernard Yeung. "Do Corporate Environmental Standards Create or Destroy Market Value?" Management Science, August 2000.

Geczy, Christopher C., Robert F. Stambaugh, and David Levin. "Investing in Socially Responsible Mutual Funds." Wharton School, Working Paper, May 2003.

Guenster, Nadja, Jeroen Derwall, Rob Bauer, and Kees Koedijk. "The Economic Value of Corporate Eco-Efficiency." Working Paper, Erasmus University, July 25, 2005.

Kempf, Alexander and Peer Osthoff. "The Effect of Socially Responsible Investing on Financial Performance." Working Paper, University of Cologne, Germany. June, 2006.

Orlitzky, Marc, Frank L. Schmidt, and Sara L. Rynes. "Corporate social and financial performance: A meta-analysis." Organization Studies, 24, 2003.

Russo, Michael V., and Paul A. Fouts. "A Resource-Based Perspective on Corporate Environmental Performance and Profitability." Academy of Management Journal, June 1997.

Wesley, John. “The Uses of Money.” Edited by Jennette Descalzo, student at Northwest Nazarene College (Nampa, ID), with corrections by George Lyons for the Wesley Center for Applied Theology. General Board of Global Ministries, The United Methodist Church, 2000. Accessed at: http://gbgm-umc.org/umhistory/wesley/sermons/serm-050.stm