1 ea exam lite part 2 businesses – ii. 2 topic 1 corporations: formation under sec. 351

TRANSCRIPT

11

EA Exam LiteEA Exam Lite

Part 2Part 2

Businesses – IIBusinesses – II

22

Topic 1Topic 1

Corporations: Corporations: Formation Formation

Under Sec. 351Under Sec. 351

33

1A Sec. 351 Transfers – 1A Sec. 351 Transfers – BasicsBasics

Sec. 351Sec. 351 – No gain on formation if: – No gain on formation if: Transfer consists solely of propertyTransfer consists solely of property Exchanged solely for corporate stockExchanged solely for corporate stock Contributing shareholder(s) in control (at Contributing shareholder(s) in control (at

least 80% of voting and outstanding stock)least 80% of voting and outstanding stock) NonqualifiedNonqualified – Bonds, certain preferred stock – Bonds, certain preferred stock

(redemption rights, dividend tied to int. rates)(redemption rights, dividend tied to int. rates) Sec. 351 ResultSec. 351 Result – No gain, basis carryovers – No gain, basis carryovers

44

1B Sec. 351 Transfers – 1B Sec. 351 Transfers – ServicesServices

Contribution of ServicesContribution of Services – Contributing – Contributing S/H taxed, shares not counted for 80%S/H taxed, shares not counted for 80%

Property Transferred With ServicesProperty Transferred With Services – – Shares issued for services Shares issued for services countedcounted in in 80% test if FMV prop. >10% total 80% test if FMV prop. >10% total transferred (but SH still taxed on transferred (but SH still taxed on services income)services income)

Question 1Question 1

55

1C Sec. 351 Transfers – 1C Sec. 351 Transfers – Gain/Loss Gain/Loss (No Boot (No Boot

Rec’d)Rec’d) If All 3 Conditions MetIf All 3 Conditions Met – (1) No gain – (1) No gain

or loss, (2) basis of stock is basis of or loss, (2) basis of stock is basis of property, (3) corporation’s basis in property, (3) corporation’s basis in property is S/H’s basisproperty is S/H’s basis

If All 3 Conditions If All 3 Conditions NotNot Met Met – – Exchange taxable, FMV as basis for Exchange taxable, FMV as basis for corp & S/Hcorp & S/H

Question 2Question 2

66

1D Sec. 351 Gain/Loss – 1D Sec. 351 Gain/Loss – With With Boot ReceivedBoot Received

BootBoot – Any non-stock property – Any non-stock property received by the shareholder (cash, received by the shareholder (cash, property, bonds)property, bonds)

LossLoss – – NeverNever recognized when boot recognized when boot rec’drec’d

Gain Gain – Recognize – Recognize lesserlesser of realized of realized acct’g. gain or boot receivedacct’g. gain or boot received

Question 3Question 3

77

1E Sec. 351 Transfers – 1E Sec. 351 Transfers – Liabilities Assumed Liabilities Assumed

Sec. 357Sec. 357 – Liabilities assumed by corp – Liabilities assumed by corp not not treated as boot received for gain treated as boot received for gain (but (but areare for basis purposes—see below) for basis purposes—see below)

If Liabilities > Basis of Prop TransferredIf Liabilities > Basis of Prop Transferred – Excess must be reported as gain to – Excess must be reported as gain to prevent a negative basis—see belowprevent a negative basis—see below

Question 4Question 4

88

1F Sec. 351 – Basis of 1F Sec. 351 – Basis of Stock to ShareholdersStock to Shareholders

Shareholder’s Basis of Stock ReceivedShareholder’s Basis of Stock Received:: Adjusted Basis of Property TransferredAdjusted Basis of Property Transferred + Gain Recognized for Tax Purposes+ Gain Recognized for Tax Purposes - Boot Received (- Boot Received (Including LiabilitiesIncluding Liabilities)) - Loss Recognized (Rare)- Loss Recognized (Rare)

ParallelsParallels – In computation to the Method – In computation to the Method 1 basis rules for like-kind exchanges1 basis rules for like-kind exchanges

Question 5Question 5

99

1G Sec. 351 – Basis of 1G Sec. 351 – Basis of Property to CorporationProperty to Corporation

Corporation’s Basis in Property Rec’d.Corporation’s Basis in Property Rec’d.:: Adjusted Basis of Property to TransferorAdjusted Basis of Property to Transferor + Gain Recognized (Taxable) by + Gain Recognized (Taxable) by

TransferorTransferor Importance of LiabilitiesImportance of Liabilities – If gain is not – If gain is not

recognized by shareholder, no step up recognized by shareholder, no step up in basis for corporationin basis for corporation

Figure 1Figure 1 Question 6Question 6

1010

1H Sec. 351 – Holding 1H Sec. 351 – Holding Period IssuesPeriod Issues

Sec. 351Sec. 351 – Provides for a “tacking” of – Provides for a “tacking” of holding periods:holding periods: SH Basis in StockSH Basis in Stock – Includes holding – Includes holding

period of contributed propertyperiod of contributed property Corp Basis in PropertyCorp Basis in Property – Includes holding – Includes holding

period of property of the transferor SHperiod of property of the transferor SH

1111

Topic 2Topic 2

The Corporate The Corporate Dividends Received Dividends Received

and Charitable and Charitable DeductionsDeductions

1212

2A Importance of Corporate 2A Importance of Corporate Tax Format - ExampleTax Format - Example

Gross margin $420,000Gross margin $420,000Gross dividends received (10% int.) 20,000 Gross dividends received (10% int.) 20,000 Capital gains (no losses) 30,000Capital gains (no losses) 30,000Other income Other income 30,000 30,000 Gross income $500,000 Gross income $500,000 Operating expenses (Operating expenses ( 200,000) 200,000) Income before charitable ded. $300,000Income before charitable ded. $300,000Charitable ($42,000, but 10% limit) ( 30,000)Charitable ($42,000, but 10% limit) ( 30,000)Div. received ded. ($20,000 x .70) Div. received ded. ($20,000 x .70) ( 14,000( 14,000))

Taxable income $256,000Taxable income $256,000

1313

2B Dividends Rec’d. 2B Dividends Rec’d. Deduction – In GeneralDeduction – In General

DRDDRD – A pct. deduction allowed to corps – A pct. deduction allowed to corps for dividends received (70%, 80%, 100%) for dividends received (70%, 80%, 100%)

Foreign DividendsForeign Dividends – Do not qualify (Cr.) – Do not qualify (Cr.) Debt-Finan. Portfolio StkDebt-Finan. Portfolio Stk – DRD reduced – DRD reduced DRD Not AvailableDRD Not Available – For REITS, exempt – For REITS, exempt

corps, stock held < 46 days during 90-day corps, stock held < 46 days during 90-day pd. around ex-dividend ( <91 of 180 days pd. around ex-dividend ( <91 of 180 days for preferred), short sale stockfor preferred), short sale stock

Special LimitsSpecial Limits – SBICS, Reg. Inv. – SBICS, Reg. Inv. CompaniesCompanies

1414

2C Dividends Rec’d. 2C Dividends Rec’d. Deduction – General RuleDeduction – General Rule

DRDDRD – In general, following percentages – In general, following percentages

of dividends received are deductible:of dividends received are deductible: 70% (if interest in payor < 20%)70% (if interest in payor < 20%) 80% (if interest in payor =>20% but < 80% (if interest in payor =>20% but <

80%)80%) 100% (controlled sub interest => 80%)100% (controlled sub interest => 80%)

Taxable Income LimitTaxable Income Limit – May apply (see – May apply (see tests below)tests below)

Question 7Question 7

1515

2D Corp DRD: Limitation 2D Corp DRD: Limitation and Exceptionand Exception

(1) General Rule(1) General Rule – 70-80-100% of dividend – 70-80-100% of dividend (2) Limitation(2) Limitation – DRD limited to 70% or 80% – DRD limited to 70% or 80%

of taxable income (operating loss plus gross of taxable income (operating loss plus gross dividend), if less than general ruledividend), if less than general rule

(3) Exception(3) Exception – If full DRD (70%/80% of – If full DRD (70%/80% of gross div) creates or adds to an NOL, full gross div) creates or adds to an NOL, full DRD allowedDRD allowed

Figure 2Figure 2 Questions 8 and 9Questions 8 and 9

1616

2E Corporate Charitable 2E Corporate Charitable Deduction – GeneralDeduction – General

General DeductionGeneral Deduction – Cash plus FMV of – Cash plus FMV of non-inventory property given to charitynon-inventory property given to charity

10% Taxable Income Limit10% Taxable Income Limit – May apply – May apply (see below); unused carryover for 5 yrs.(see below); unused carryover for 5 yrs.

Authorized ContributionAuthorized Contribution – By Board of – By Board of Directors before end of year deductible if Directors before end of year deductible if paid by due date of return (2½ months)paid by due date of return (2½ months)

1717

2F Corporate Charitable 2F Corporate Charitable Deduction – LimitsDeduction – Limits

Deduction LimitDeduction Limit – 10% of taxable income – 10% of taxable income beforebefore (1) charitable, (2) div. received deduction, (3) (1) charitable, (2) div. received deduction, (3) capital loss or NOL carryback (capital loss or NOL carryback (not not carryforward) carryforward)

Property ContributionsProperty Contributions – Limits if – Limits if ord. inc. prop.ord. inc. prop. UnusedUnused – Carry over for 5 years (current first) – Carry over for 5 years (current first) InventoryInventory – Deduction usually limited to cost, – Deduction usually limited to cost,

but allowed cost + 50% of appreciation (limited but allowed cost + 50% of appreciation (limited to 2X cost) deduction for (1) Care of the ill, to 2X cost) deduction for (1) Care of the ill, needy, or infants or (2) Univ. scientific purposesneedy, or infants or (2) Univ. scientific purposes

Question 10Question 10

1818

Topic 3Topic 3

Corporations: Corporations: Other Other

DeductionsDeductions

1919

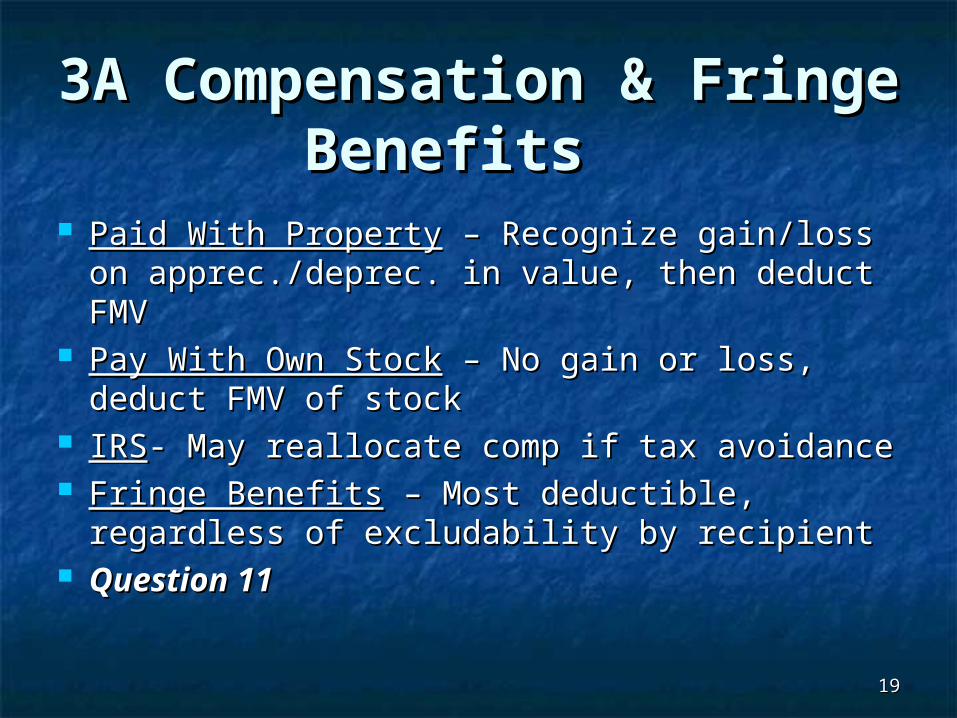

3A Compensation & 3A Compensation & Fringe BenefitsFringe Benefits

Paid With PropertyPaid With Property – Recognize gain/loss on – Recognize gain/loss on apprec./deprec. in value, then deduct FMVapprec./deprec. in value, then deduct FMV

Pay With Own StockPay With Own Stock – No gain or loss, – No gain or loss, deduct FMV of stockdeduct FMV of stock

IRSIRS- May reallocate comp if tax avoidance- May reallocate comp if tax avoidance Fringe BenefitsFringe Benefits – Most deductible, – Most deductible,

regardless of excludability by recipientregardless of excludability by recipient Question 11Question 11

2020

3B Miscellaneous 3B Miscellaneous Corporate DeductionsCorporate Deductions

Worthless Affiliated Co. StockWorthless Affiliated Co. Stock – Ordinary – Ordinary loss allowed if corporation owns at least loss allowed if corporation owns at least an 80% interestan 80% interest

Domestic Activities Production Domestic Activities Production DeductionDeduction – 6% of lesser of (1) qualified – 6% of lesser of (1) qualified production activities income or (2) production activities income or (2) taxable income for the year (AGI for taxable income for the year (AGI for individual); limited to 50% of W-2 wages individual); limited to 50% of W-2 wages

2121

3C Corporate Net 3C Corporate Net Operating LossesOperating Losses

NOL ComputationNOL Computation – NOL deduction, capital – NOL deduction, capital loss and charitable carryovers not allowed in loss and charitable carryovers not allowed in computing an NOLcomputing an NOL

Dividends Received DeductionDividends Received Deduction – May limit – May limit NOLNOL

Casualty or Theft LossCasualty or Theft Loss – Increases NOL – Increases NOL Current-Year NOLCurrent-Year NOL – 2-year c/b and 20-year c/f – 2-year c/b and 20-year c/f ElectionElection – Available to forego carryback; must – Available to forego carryback; must

use same for AMT (irrevocable when made); use same for AMT (irrevocable when made); carryovers used up on FIFO basiscarryovers used up on FIFO basis

Questions 12 and 13Questions 12 and 13

2222

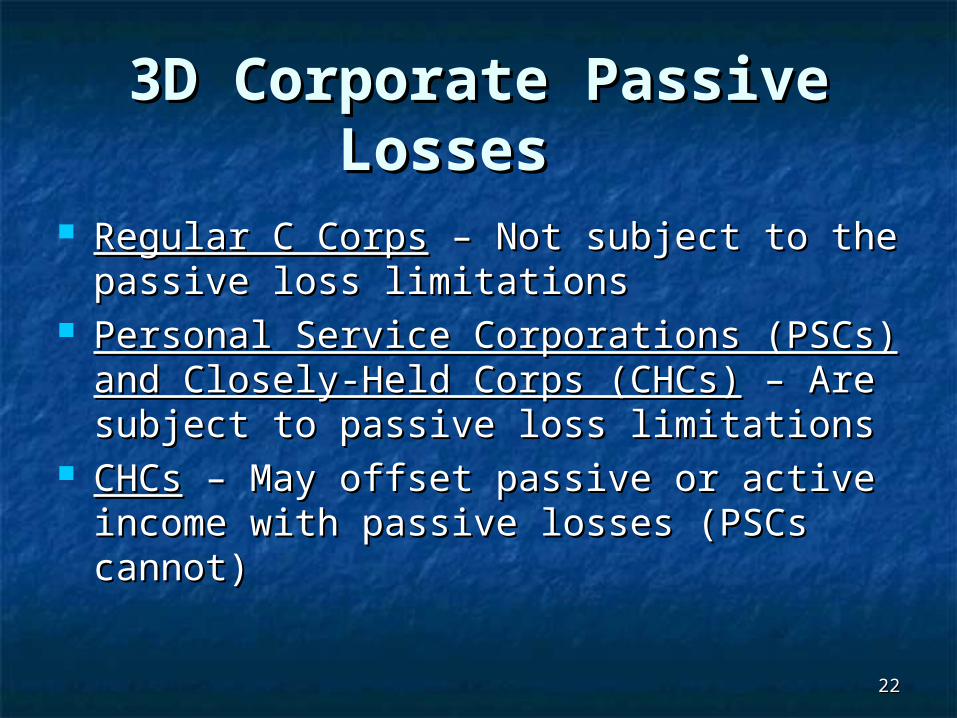

3D Corporate Passive 3D Corporate Passive LossesLosses

Regular C CorpsRegular C Corps – Not subject to the – Not subject to the passive loss limitationspassive loss limitations

Personal Service Corporations (PSCs) and Personal Service Corporations (PSCs) and Closely-Held Corps (CHCs)Closely-Held Corps (CHCs) – Are subject to – Are subject to passive loss limitationspassive loss limitations

CHCsCHCs – May offset passive or active – May offset passive or active income with passive losses (PSCs cannot)income with passive losses (PSCs cannot)

2323

3E Qualifying 3E Qualifying Organizational & StartupOrganizational & Startup

Organizational CostsOrganizational Costs – Licenses, drafting – Licenses, drafting documents, registration fees (but documents, registration fees (but notnot costs of costs of printing and issuing stock certificates); Sec. printing and issuing stock certificates); Sec. 248 permits expensing & amortization (below)248 permits expensing & amortization (below)

Startup CostsStartup Costs – Bringing the bus. to the point – Bringing the bus. to the point of daily operations (training, adv.), but of daily operations (training, adv.), but notnot deductible interest, taxes, or R&E; Sec. 195 deductible interest, taxes, or R&E; Sec. 195 permits expensing & amortization (below)permits expensing & amortization (below)

Elective Expensing & AmortizationElective Expensing & Amortization - $5,000 - $5,000 max. expensing, phaseout $1 for $1 beginning max. expensing, phaseout $1 for $1 beginning at $50,000, 180-mo. amort. of remaining at $50,000, 180-mo. amort. of remaining costs)costs)

2424

3F Org. & Startup Costs – 3F Org. & Startup Costs – Making the ElectionMaking the Election

ElectionElection – For either made by filing Form 4562 – For either made by filing Form 4562 and separate detailed statements listing and separate detailed statements listing qualified costs; qualified costs; irrevocable electionirrevocable election

Valid ElectionValid Election – If filed by due date of return – If filed by due date of return (plus extensions), or by amending first return (plus extensions), or by amending first return w/i 6 months of due date (plus extensions)w/i 6 months of due date (plus extensions)

No ElectionNo Election – No cost recovery until business – No cost recovery until business is liquidated; costs presumably have is liquidated; costs presumably have unlimited lifeunlimited life

2525

3G Org. & Startup Costs 3G Org. & Startup Costs – Computing Deduction– Computing Deduction

Either CostEither Cost – Must be paid – Must be paid or incurredor incurred within the first year of doing businesswithin the first year of doing business

Amortization PeriodAmortization Period – Begins in the first – Begins in the first month that the company is open for bus.month that the company is open for bus.

Change in Amort. PeriodChange in Amort. Period – Is – Is not not allowedallowed Figure 3Figure 3 Question 14Question 14

2626

Part 4Part 4

Corp. Capital Corp. Capital Transactions & Transactions & Related Party Related Party

RulesRules

2727

4A Corp. Capital Netting – 4A Corp. Capital Netting – Similarities to Individual Similarities to Individual

Step 1Step 1 – Net all STs, determine ST result – Net all STs, determine ST result Step 2Step 2 – Net all LTs, determine LT result – Net all LTs, determine LT result Step 3Step 3 – Compare sign of ST & LT results: – Compare sign of ST & LT results:

If same signIf same sign – Each enters income – Each enters income separatelyseparately

If opposite signIf opposite sign – Net result enters income – Net result enters income Differences from IndividualsDifferences from Individuals – How the – How the

final results enter ordinary income (next)final results enter ordinary income (next)

2828

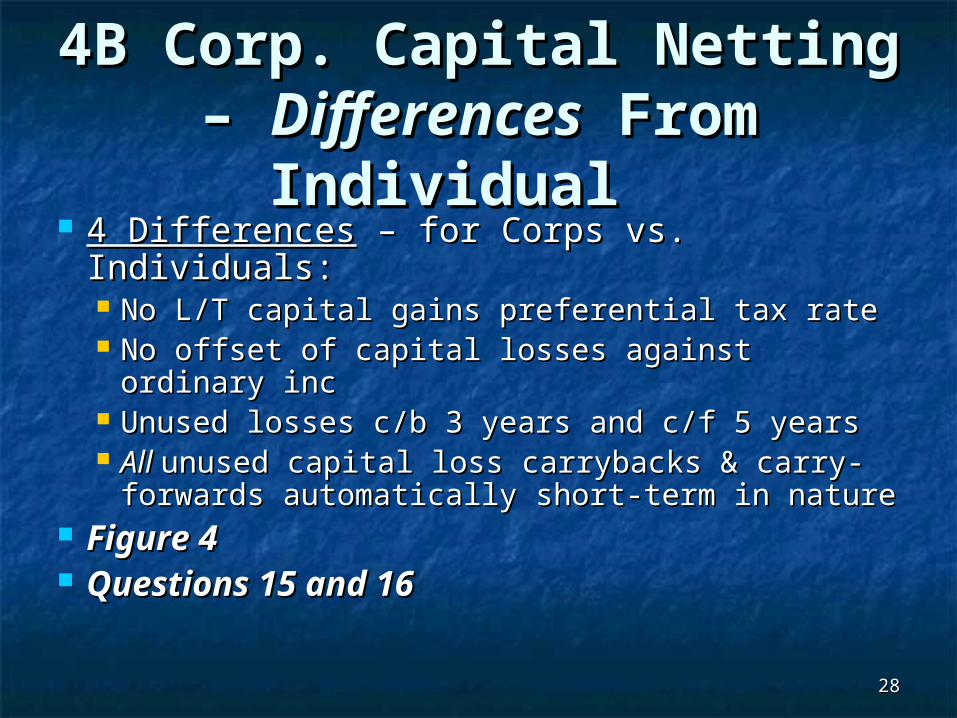

4B Corp. Capital Netting 4B Corp. Capital Netting – – DifferencesDifferences From From

IndividualIndividual 4 Differences4 Differences – for Corps vs. Individuals: – for Corps vs. Individuals:

No L/T capital gains preferential tax rateNo L/T capital gains preferential tax rate No offset of capital losses against ordinary incNo offset of capital losses against ordinary inc Unused losses c/b 3 years and c/f 5 yearsUnused losses c/b 3 years and c/f 5 years All All unused capital loss carrybacks & carry-unused capital loss carrybacks & carry-

forwards automatically short-term in natureforwards automatically short-term in nature Figure 4Figure 4 Questions 15 and 16Questions 15 and 16

2929

4C Sec. 267 Related 4C Sec. 267 Related Party Rules for CorpsParty Rules for Corps

Two Deductions Disallowed by Sec. 267Two Deductions Disallowed by Sec. 267:: Loss on sale or exchange between related partiesLoss on sale or exchange between related parties Year-end accrual-basis deduction for payment to Year-end accrual-basis deduction for payment to

cash-basis related partycash-basis related party Related PartiesRelated Parties – Defined as family members – Defined as family members

and controlled entities (direct or indirect)and controlled entities (direct or indirect) Constructive Ownership (Attribution)Constructive Ownership (Attribution) – –

Indirect double attribution through entities Indirect double attribution through entities (p’ship interest in corp in question), but not (p’ship interest in corp in question), but not with otherswith others

3030

4D Sec. 267 Disallowed 4D Sec. 267 Disallowed Losses on SalesLosses on Sales

No ExceptionsNo Exceptions – To disallowance rules – To disallowance rules (e.g., family hostility ignored), but (e.g., family hostility ignored), but liquidatingliquidating dist. OK dist. OK

Disallowed LossDisallowed Loss – May – May only reduce gainonly reduce gain on on subsequent resale by the related party subsequent resale by the related party (cannot create or add to loss)(cannot create or add to loss)

Gain Reduction RuleGain Reduction Rule – Does not affect – Does not affect basis or holding period rulesbasis or holding period rules

Question 17Question 17

3131

4E Sec. 267 Disallowed 4E Sec. 267 Disallowed Expense AccrualsExpense Accruals

Transactions CoveredTransactions Covered – Expense accrual – Expense accrual by accrual-basis corporation to a related by accrual-basis corporation to a related cash-basis shareholder/employee or cash-basis shareholder/employee or business partybusiness party

Tax ResultTax Result – No deduction for expense – No deduction for expense until included in the related party’s incomeuntil included in the related party’s income

Sec. 267 Related Party DefinitionSec. 267 Related Party Definition – – Includes a PSC and Includes a PSC and anyany cash-basis cash-basis shareholder/employeeshareholder/employee

3232

Topic 5Topic 5

Corp. Earnings Corp. Earnings & Profits (E&P) & Profits (E&P) DeterminationsDeterminations

3333

5A Adjusting Income to 5A Adjusting Income to Determine E&PDetermine E&P

E&PE&P – Represents a corporation’s ability to – Represents a corporation’s ability to pay dividend w/o impairing invested capital; pay dividend w/o impairing invested capital; includes current & accumulated E&Pincludes current & accumulated E&P

AdjustmentsAdjustments – Convert taxable income to a – Convert taxable income to a “wherewithal to pay” economic income (i.e., “wherewithal to pay” economic income (i.e., - cap. loss, + DRD, - tax liability, - excess - cap. loss, + DRD, - tax liability, - excess contributions, + tax-exempt interest) contributions, + tax-exempt interest)

Other Adj.Other Adj. – Depreciation, inventory, – Depreciation, inventory, installmentinstallment

Figure 5Figure 5 Question 18Question 18

3434

5B Cash Distributions – 5B Cash Distributions – Effect on E&PEffect on E&P

Cash Cash – Reduces E&P (taxable dividend if – Reduces E&P (taxable dividend if either either current [CEP] or accumulated E&P [AEP] current [CEP] or accumulated E&P [AEP] exists); then cost recovery, then capital gain exists); then cost recovery, then capital gain (i.e., sale)(i.e., sale)

More Than One Dist. in the YearMore Than One Dist. in the Year – Allocate CEP – Allocate CEP pro ratapro rata to each dist., but apply AEP to each dist., but apply AEP chronologicallychronologically to each to each

If CEP Negative and AEP PositiveIf CEP Negative and AEP Positive – Net on date – Net on date of dist. (a negative CEP allocated on daily of dist. (a negative CEP allocated on daily basis)basis)

Figure 6Figure 6 Question 19Question 19

3535

5C Property Distributions – 5C Property Distributions – Effect on E&PEffect on E&P

Two E&P Effects of Property Distribution:Two E&P Effects of Property Distribution: Unrealized gain on property increases Unrealized gain on property increases

E&PE&P Larger of adjusted basis or FMV of Larger of adjusted basis or FMV of

property decreases E&Pproperty decreases E&P Net Effect of RuleNet Effect of Rule – Reduce E&P by the – Reduce E&P by the

adjusted basis of the propertyadjusted basis of the property Liabilities Assumed by S/HLiabilities Assumed by S/H – Increase E&P – Increase E&P Question 20Question 20

3636

Topic 6Topic 6

Corporate Corporate DistributionsDistributions

3737

6A Classification of Cash 6A Classification of Cash DistributionsDistributions

E&P RulesE&P Rules – Mirrored in determining – Mirrored in determining the tax status of distributions to the tax status of distributions to shareholdersshareholders

ShareholderShareholder – Taxed on dividend to – Taxed on dividend to extent of his or her share of CEP & extent of his or her share of CEP & AEP, then nontaxable recovery of AEP, then nontaxable recovery of capital, then capital gain (as though capital, then capital gain (as though stock is sold)stock is sold)

ReviewReview – E&P allocations (Topic 5) – E&P allocations (Topic 5) Questions 21 and 22Questions 21 and 22

3838

6B Corporate Redemptions 6B Corporate Redemptions – Dividend or Exchange– Dividend or Exchange

5 Ways for Capital Gain on Redemption:5 Ways for Capital Gain on Redemption: Not essentially equivalent to dividend [facts & circumstances]Not essentially equivalent to dividend [facts & circumstances] Disproportionate distribution (50% overall, 80% disprop. test)Disproportionate distribution (50% overall, 80% disprop. test) Complete termination of interest (agree to stay out bus. 10 Complete termination of interest (agree to stay out bus. 10

yr)yr) Partial liquidation (significant business contraction)Partial liquidation (significant business contraction) Pay estate taxes (FMV family stock > 35% estate)Pay estate taxes (FMV family stock > 35% estate)

Other RedemptionsOther Redemptions – Ordinary dividends – Ordinary dividends Effect on E&PEffect on E&P – If div, reduce E&P; if CG, reduce E&P – If div, reduce E&P; if CG, reduce E&P

by larger of (1) FMV distrib. or (2) E&P x % redeemedby larger of (1) FMV distrib. or (2) E&P x % redeemed Question 23Question 23

3939

6C Redemptions – Stock 6C Redemptions – Stock Attribution RulesAttribution Rules

Attribution RulesAttribution Rules – Apply with 50% & 80% tests – Apply with 50% & 80% tests Sec. 318Sec. 318 – Attribute stock owned by spouse, – Attribute stock owned by spouse,

parents, children, grandchildren back to TP parents, children, grandchildren back to TP (but NOT brothers and sisters)(but NOT brothers and sisters)

ATR ATR fromfrom an entity an entity – To an owner possible, but – To an owner possible, but must be at least 50% total direct or indirect int.must be at least 50% total direct or indirect int.

ATR ATR to to an entityan entity – From an owner for all shares – From an owner for all shares (for corporation, must exceed 50% int.)(for corporation, must exceed 50% int.)

Figure 7Figure 7 Question 24Question 24

4040

6D Corporate Partial 6D Corporate Partial LiquidationsLiquidations

Sale or Exchange TreatmentSale or Exchange Treatment – Permitted – Permitted for partial liquidations; reported by:for partial liquidations; reported by: IndividualsIndividuals (capital gain or loss) (capital gain or loss) CorporationsCorporations (dividends, for 70%/80% DRD) (dividends, for 70%/80% DRD)

RequiredRequired – A significant contraction of the – A significant contraction of the business enterprise business enterprise

Examples Examples - Liquidating a business line or - Liquidating a business line or not replacing division destroyed by firenot replacing division destroyed by fire

4141

6E Distributions of Property 6E Distributions of Property – Gain/Loss to SH– Gain/Loss to SH

Dividend IncomeDividend Income – FMV property (limited to – FMV property (limited to the shareholder’s share of E&P); rules do not the shareholder’s share of E&P); rules do not apply to distribution of Co.’s apply to distribution of Co.’s own own stockstock

Liability on Distributed PropertyLiability on Distributed Property – Amount – Amount reduces income to S/H (and increases E&P)reduces income to S/H (and increases E&P)

Bargain Sale to S/HBargain Sale to S/H – Bargain element is – Bargain element is taxed as a dividendtaxed as a dividend

Question 25Question 25

4242

6F Property Distribution 6F Property Distribution – Gain/Loss to Distr. Corp– Gain/Loss to Distr. Corp

CorpCorp – Recognizes gain/loss on – Recognizes gain/loss on

distribution as if sold; character distribution as if sold; character depends on asset (e.g., depreciation depends on asset (e.g., depreciation recapture possibility)recapture possibility)

Liability on Distributed PropertyLiability on Distributed Property – If – If the liability > FMV property, the FMV the liability > FMV property, the FMV is presumed to be equal the liabilityis presumed to be equal the liability

Question 26Question 26

4343

Topic 7Topic 7

S Corporations – S Corporations – Key Key

RequirementsRequirements

4444

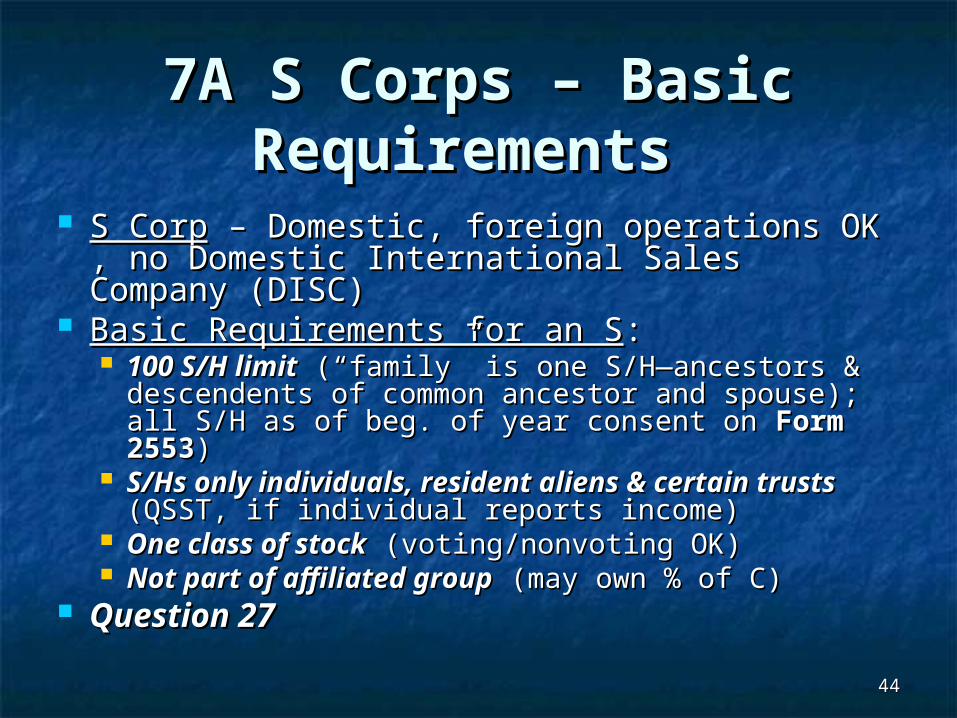

7A S Corps – Basic 7A S Corps – Basic RequirementsRequirements

S CorpS Corp – Domestic, foreign operations OK , no – Domestic, foreign operations OK , no Domestic International Sales Company (DISC)Domestic International Sales Company (DISC)

Basic Requirements for an SBasic Requirements for an S:: 100 S/H limit100 S/H limit (“family” is one S/H—ancestors & (“family” is one S/H—ancestors &

descendents of common ancestor and spouse); all descendents of common ancestor and spouse); all S/H as of beg. of year consent on S/H as of beg. of year consent on Form 2553Form 2553))

S/Hs only individuals, resident aliens & S/Hs only individuals, resident aliens & certain trustscertain trusts (QSST, if individual reports income) (QSST, if individual reports income)

One class of stockOne class of stock (voting/nonvoting OK) (voting/nonvoting OK) Not part of affiliated groupNot part of affiliated group (may own % of C) (may own % of C)

Question 27Question 27

4545

7B S Corp Election – 7B S Corp Election – Effective DateEffective Date

Form 2553Form 2553 – Election, consent of – Election, consent of allall S/H at S/H at the beginning of the first S year the beginning of the first S year

ElectionElection – Due by 15 – Due by 15thth day of 3 day of 3rdrd month of month of year that election is desiredyear that election is desired

11stst Day of 1 Day of 1stst Yr Yr. – . – EarliestEarliest date S Corp. has: date S Corp. has: S/H, assets, or begins businessS/H, assets, or begins business

If Filed After Due DateIf Filed After Due Date – Election effective – Election effective for next year (IRS may accept late for next year (IRS may accept late application if filed within 12 months, if application if filed within 12 months, if reasonably explained)reasonably explained)

Question 28Question 28

4646

7C Termination of an S 7C Termination of an S ElectionElection

Voluntary TerminationVoluntary Termination – Requires consent of > – Requires consent of > 50% shares w/i 2 ½ mos., otherwise, next year50% shares w/i 2 ½ mos., otherwise, next year

Involuntary TerminationInvoluntary Termination – Begin with disq. – Begin with disq. event event

Disqualifying EventsDisqualifying Events - > 100 S/H, ineligible S/H, - > 100 S/H, ineligible S/H, prohibited tax status, 2prohibited tax status, 2ndnd class of stock, class of stock, improper year, or fail passive income test for 3 improper year, or fail passive income test for 3 consecutive years (see below)consecutive years (see below)

5-Year Wait5-Year Wait – To reelect, unless (1) termination – To reelect, unless (1) termination inadvertent (and IRS OKs), or (2) F&C IRS OKsinadvertent (and IRS OKs), or (2) F&C IRS OKs

Question 29Question 29

4747

7D S Corp Built-in Gains 7D S Corp Built-in Gains TaxTax

PurposePurpose – Prevent S election by C to avoid sale gain – Prevent S election by C to avoid sale gain Built-in GainBuilt-in Gain – FMV > basis of any asset at election – FMV > basis of any asset at election ApplicationApplication – Only – Only post-86post-86 elections by C corporations elections by C corporations 35% Rate35% Rate – For any gain within 10 yrs. election – For any gain within 10 yrs. election NUBIGNUBIG – (Potential gain) reported on 1120-S each – (Potential gain) reported on 1120-S each

year, reduced as recognized (B/I loss may offset, if year, reduced as recognized (B/I loss may offset, if proven)proven)

NOL & Cap. Loss C/OsNOL & Cap. Loss C/Os – May reduce BIG, and any – May reduce BIG, and any credit carryover may reduce BIG taxcredit carryover may reduce BIG tax

Question 30Question 30

4848

7E S Corp LIFO Recapture 7E S Corp LIFO Recapture TaxTax

LIFO Recapture TaxLIFO Recapture Tax – If C using LIFO – If C using LIFO converts to S statusconverts to S status

ComputationComputation - Compute marginal tax - Compute marginal tax on excess of FIFO inventory over LIFO on excess of FIFO inventory over LIFO (as if included in last C year income) (as if included in last C year income)

Reporting Reporting - Report as add’l tax over 4 - Report as add’l tax over 4 year period (beginning with year period (beginning with last C last C Corp returnCorp return))

4949

7G Tax on Excessive 7G Tax on Excessive Passive Income of S Passive Income of S

TaxTax – Only if S passive investment income (PII) – Only if S passive investment income (PII) > 25% gross receipts, > 25% gross receipts, && E&P exists from C yrs. E&P exists from C yrs.

35% Rate35% Rate – Applies to Excess Net Passive Inc. – Applies to Excess Net Passive Inc. (ENPI); cannot exceed C corporate tax for year(ENPI); cannot exceed C corporate tax for year

TaxTax – Reduces passive pass-thru to SH – Reduces passive pass-thru to SH If Taxed for 3 Consecutive Yrs.If Taxed for 3 Consecutive Yrs. – Lose S status – Lose S status

as of 1as of 1stst day of 4 day of 4th th year year Figure 8 (skim only; not likely on exam)Figure 8 (skim only; not likely on exam) Question 31Question 31

5050

Topic 8Topic 8

S Corporations: S Corporations: Taxable Income Taxable Income & Distributions& Distributions

5151

8A S Corp – Determining 8A S Corp – Determining Ordinary Inc. & Special Ordinary Inc. & Special

ItemsItems DeterminationDetermination – Very similar to partnerships – Very similar to partnerships Ordinary IncomeOrdinary Income – Items – Items could not varycould not vary in in

treatment across individual S/H returnstreatment across individual S/H returns Special ItemsSpecial Items – Could vary in treatment – Could vary in treatment Sec. 179 MaxSec. 179 Max. – Allocate based on SH % . – Allocate based on SH %

ownedowned Salary to OwnersSalary to Owners – In S, not a guaranteed – In S, not a guaranteed

payment, just an ordinary bus. deductionpayment, just an ordinary bus. deduction Question 32Question 32

5252

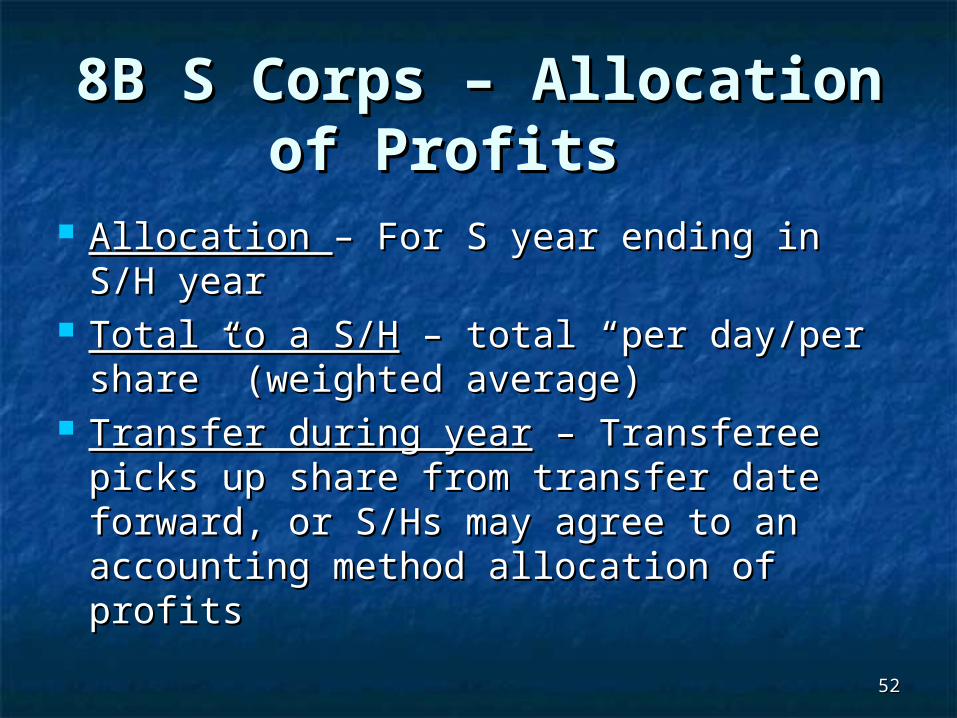

8B S Corps – Allocation 8B S Corps – Allocation of Profitsof Profits

Allocation Allocation – For S year ending in S/H – For S year ending in S/H yearyear

Total to a S/HTotal to a S/H – total “per day/per – total “per day/per share” (weighted average)share” (weighted average)

Transfer during yearTransfer during year – Transferee picks – Transferee picks up share from transfer date forward, up share from transfer date forward, or S/Hs may agree to an accounting or S/Hs may agree to an accounting method allocation of profits method allocation of profits

5353

8C Allocation of S Corp 8C Allocation of S Corp Losses – No S/H LoansLosses – No S/H Loans

LossesLosses – Also allocated “per day/per – Also allocated “per day/per share”share”

Loss LimitLoss Limit – S/H basis + outstanding loans – S/H basis + outstanding loans If loss share > basisIf loss share > basis – Carry over excess – Carry over excess

for possible future increases in basisfor possible future increases in basis S ShareholderS Shareholder – May NOT increase basis – May NOT increase basis

for share of liabilitiesfor share of liabilities S/H BasisS/H Basis – Much like partnership (below) – Much like partnership (below)

5454

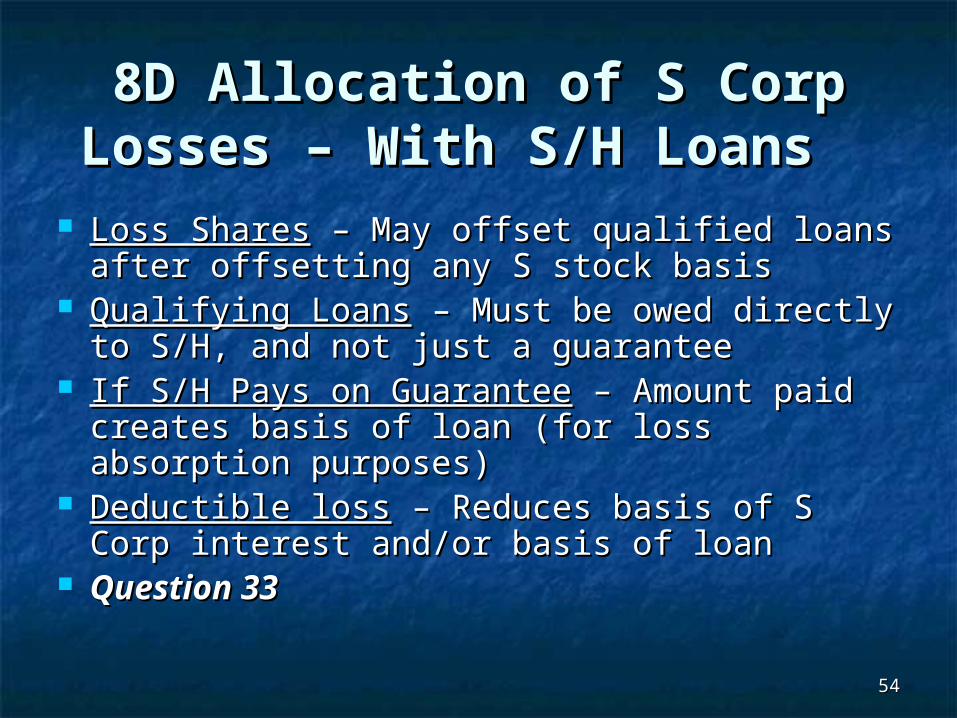

8D Allocation of S Corp 8D Allocation of S Corp Losses – With S/H LoansLosses – With S/H Loans

Loss SharesLoss Shares – May offset qualified loans – May offset qualified loans after offsetting any S stock basisafter offsetting any S stock basis

Qualifying LoansQualifying Loans – Must be owed directly – Must be owed directly to S/H, and not just a guaranteeto S/H, and not just a guarantee

If S/H Pays on GuaranteeIf S/H Pays on Guarantee – Amount paid – Amount paid creates basis of loan (for loss absorption creates basis of loan (for loss absorption purposes)purposes)

Deductible lossDeductible loss – Reduces basis of S Corp – Reduces basis of S Corp interest and/or basis of loaninterest and/or basis of loan

Question 33Question 33

5555

8E S Corp Distributions – 8E S Corp Distributions – In GeneralIn General

Classifying DistributionClassifying Distribution – Depends on – Depends on whether or not S has “E&P” from either (1) whether or not S has “E&P” from either (1) prior years as a C Corp, or (2) a prior prior years as a C Corp, or (2) a prior nontaxable acquisition of a C Corpnontaxable acquisition of a C Corp

Distributions From E&PDistributions From E&P – Taxable, once the – Taxable, once the S Corp exhausts AAA balance (see below)S Corp exhausts AAA balance (see below)

S ShareholdersS Shareholders – May consent to have all – May consent to have all of a distribution of a distribution FIRSTFIRST come from E&P come from E&P (1099-DIV)(1099-DIV)

5656

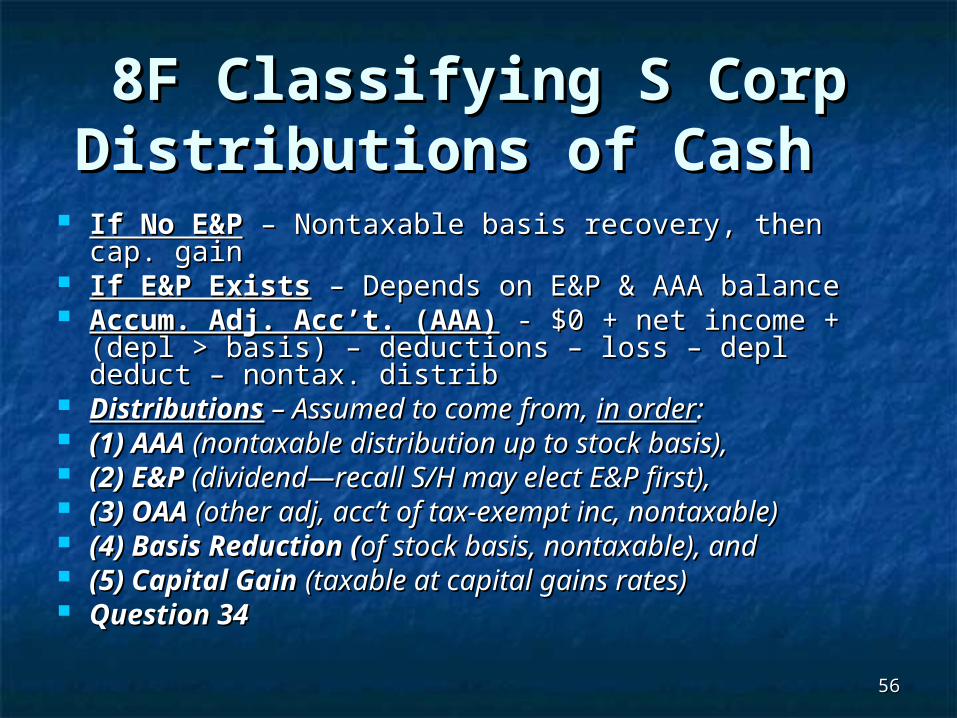

8F Classifying S Corp 8F Classifying S Corp Distributions of CashDistributions of Cash

If No E&PIf No E&P – Nontaxable basis recovery, then cap. gain – Nontaxable basis recovery, then cap. gain If E&P ExistsIf E&P Exists – Depends on E&P & AAA balance – Depends on E&P & AAA balance Accum. Adj. Acc’t. (AAA)Accum. Adj. Acc’t. (AAA) - $0 + net income + (depl > - $0 + net income + (depl >

basis) – deductions – loss – depl deduct – nontax. distribbasis) – deductions – loss – depl deduct – nontax. distrib DistributionsDistributions – Assumed to come from, – Assumed to come from, in orderin order:: (1)(1) AAA AAA (nontaxable distribution up to stock basis), (nontaxable distribution up to stock basis), (2)(2) E&PE&P (dividend—recall S/H may elect E&P first), (dividend—recall S/H may elect E&P first), (3)(3) OAAOAA (other adj, acc’t of tax-exempt inc, nontaxable) (other adj, acc’t of tax-exempt inc, nontaxable) (4)(4) Basis Reduction (Basis Reduction (of stock basis, nontaxable), andof stock basis, nontaxable), and (5)(5) Capital GainCapital Gain (taxable at capital gains rates) (taxable at capital gains rates) Question 34Question 34

5757

8G S Corp Distributions 8G S Corp Distributions of Propertyof Property

S CorpS Corp – Must report gain/loss as though – Must report gain/loss as though property sold first (just like C Corp)property sold first (just like C Corp)

DifferenceDifference – Gain is passed through to S/H – Gain is passed through to S/H S/HS/H – Generally not taxed on property – Generally not taxed on property

distribution unless E&P existsdistribution unless E&P exists If Dist. > BasisIf Dist. > Basis – S S/H must report capital – S S/H must report capital

gain (no basis adjustment like p’ships)gain (no basis adjustment like p’ships)

5858

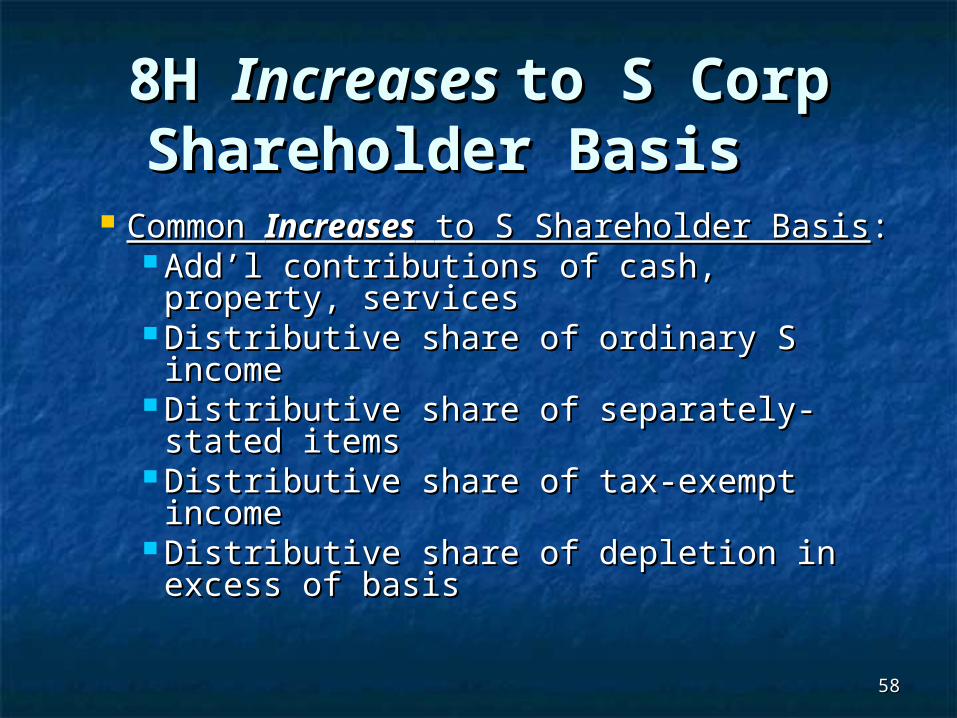

8H 8H Increases Increases to S Corp to S Corp Shareholder Basis Shareholder Basis

Common Common IncreasesIncreases to S Shareholder to S Shareholder BasisBasis:: Add’l contributions of cash, property, Add’l contributions of cash, property,

servicesservices Distributive share of ordinary S incomeDistributive share of ordinary S income Distributive share of separately-stated Distributive share of separately-stated

itemsitems Distributive share of tax-exempt Distributive share of tax-exempt

incomeincome Distributive share of depletion in Distributive share of depletion in

excess of basisexcess of basis

5959

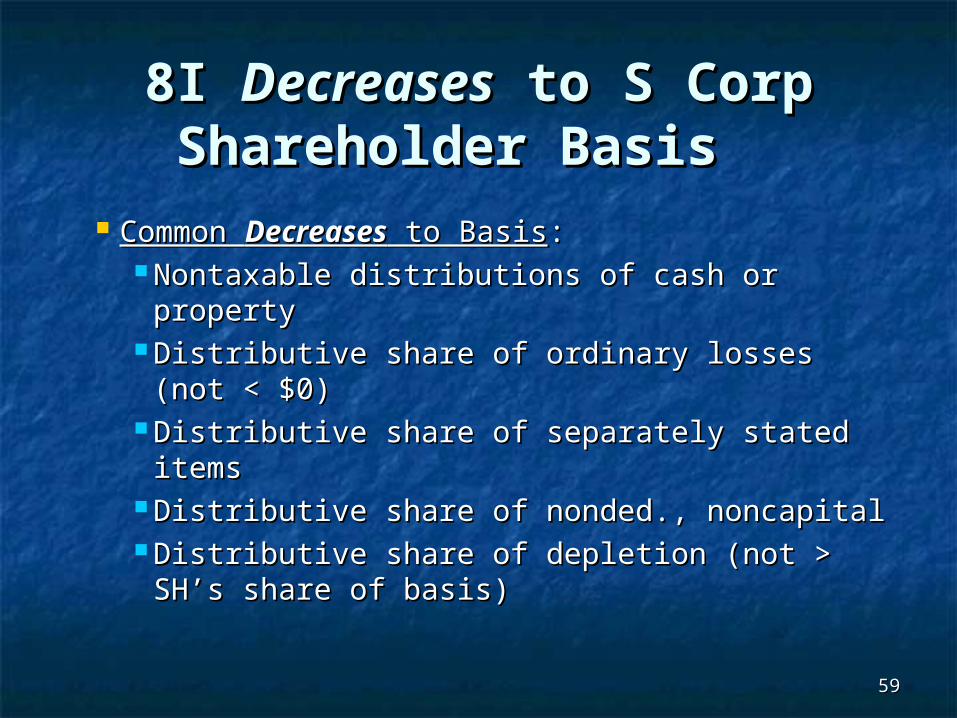

8I 8I DecreasesDecreases to S Corp to S Corp Shareholder BasisShareholder Basis

Common Common DecreasesDecreases to Basis to Basis:: Nontaxable distributions of cash or propertyNontaxable distributions of cash or property Distributive share of ordinary losses (not < Distributive share of ordinary losses (not <

$0)$0) Distributive share of separately stated itemsDistributive share of separately stated items Distributive share of nonded., noncapitalDistributive share of nonded., noncapital Distributive share of depletion (not > SH’s Distributive share of depletion (not > SH’s

share of basis)share of basis)

6060

8J Determining an S Corp 8J Determining an S Corp S/H’s Stock BasisS/H’s Stock Basis

BasisBasis – Can never be zero; if distribution – Can never be zero; if distribution exceeds basis, gain is recognized for exceeds basis, gain is recognized for excess and increases basis to $0excess and increases basis to $0

Loss SharesLoss Shares – Cannot decrease S stock – Cannot decrease S stock basis below zero; deduction limited to basis below zero; deduction limited to basis plus loans (carryover to future years basis plus loans (carryover to future years for possible basis increases)for possible basis increases)

6161

Topic 9Topic 9

Estate & Trust Estate & Trust Income Income

Taxation:Taxation:

A Broad ViewA Broad View

6262

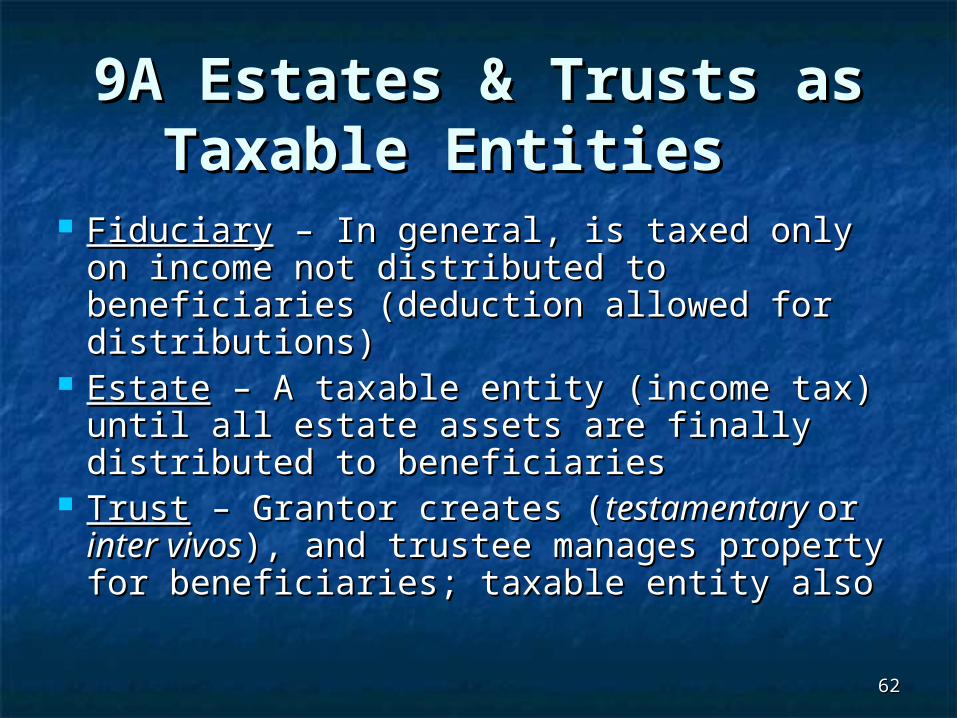

9A Estates & Trusts as 9A Estates & Trusts as Taxable EntitiesTaxable Entities

FiduciaryFiduciary – In general, is taxed only on – In general, is taxed only on income not distributed to beneficiaries income not distributed to beneficiaries (deduction allowed for distributions)(deduction allowed for distributions)

EstateEstate – A taxable entity (income tax) – A taxable entity (income tax) until all estate assets are finally until all estate assets are finally distributed to beneficiariesdistributed to beneficiaries

TrustTrust – Grantor creates (– Grantor creates (testamentary testamentary or or inter vivosinter vivos), and trustee manages ), and trustee manages property for beneficiaries; taxable entity property for beneficiaries; taxable entity alsoalso

6363

9B Form 1041 Filing 9B Form 1041 Filing Requirements for E&TRequirements for E&T

Estates & Trusts (E&T)Estates & Trusts (E&T) – Must file annual Form – Must file annual Form 1041, with Sch. K-1 allocations to beneficiaries1041, with Sch. K-1 allocations to beneficiaries

E&T Tax Rate ScheduleE&T Tax Rate Schedule – Progressive rates – Progressive rates Form 1041Form 1041 – Required if (1) estate has gross – Required if (1) estate has gross

income => $600, (2) trust has gross or income => $600, (2) trust has gross or taxable income =>$600, or (3) a nonresident taxable income =>$600, or (3) a nonresident alien beneficiary (alien beneficiary (Note – gross income similar Note – gross income similar to indto ind.).)

EstateEstate – Personal representative or authorized – Personal representative or authorized officer must sign the returnofficer must sign the return

Question 35Question 35

6464

9C Simple Trusts9C Simple Trusts

TrustsTrusts – Classified as – Classified as simplesimple or or complexcomplex Simple Trust DefinedSimple Trust Defined – One that: – One that:

Is required to distribute all trust acct’g incomeIs required to distribute all trust acct’g income Distributes no corpusDistributes no corpus Has no charitable beneficiariesHas no charitable beneficiaries

RequiredRequired – File return if gross income is – File return if gross income is $600 or more ($300 exemption allowed)$600 or more ($300 exemption allowed)

6565

9D Complex Trusts9D Complex Trusts

Complex TrustComplex Trust – Any trust other than – Any trust other than a simple one (i.e., one that distributes a simple one (i.e., one that distributes corpus, accumulates some income, corpus, accumulates some income, and/or has a charitable beneficiary)and/or has a charitable beneficiary)DeterminationDetermination – Made on an annual – Made on an annual basis; designation may change year basis; designation may change year to yearto year

Question 36Question 36

6666

9E Acct’g. vs. Taxable 9E Acct’g. vs. Taxable Income of FiduciaryIncome of Fiduciary

Broad Overview of E&T TaxationBroad Overview of E&T Taxation:: Distribution DeductionDistribution Deduction – Allocates taxable – Allocates taxable

income between E&T and beneficiariesincome between E&T and beneficiaries Distributable Net IncomeDistributable Net Income – The “common – The “common

denominator” for determining the denominator” for determining the distribution deduction (economic acct’g distribution deduction (economic acct’g income of entity)income of entity)

Trust “Accounting Income”Trust “Accounting Income” – – Determined by governing instrument; if Determined by governing instrument; if silent, then state law governssilent, then state law governs

6767

9F Fiduciary Deductions 9F Fiduciary Deductions – Allocating Expenses– Allocating Expenses

DeductionsDeductions – Same as individuals, but: – Same as individuals, but: Gen. & Adm. ExpenseGen. & Adm. Expense - Allocate between - Allocate between

taxable & nontaxable income, instrument taxable & nontaxable income, instrument doesn’t override (if on 1041doesn’t override (if on 1041, can’t, can’t be on 706); be on 706); contributions also unless specified differentlycontributions also unless specified differently

2% Miscellaneous Itemized Floor2% Miscellaneous Itemized Floor – Does not – Does not apply to expense that would apply to expense that would notnot have been have been incurred outside trust (trustee fee, tax prep.)incurred outside trust (trustee fee, tax prep.)

Unused NOLsUnused NOLs – CAN be used by beneficiary – CAN be used by beneficiary

6868

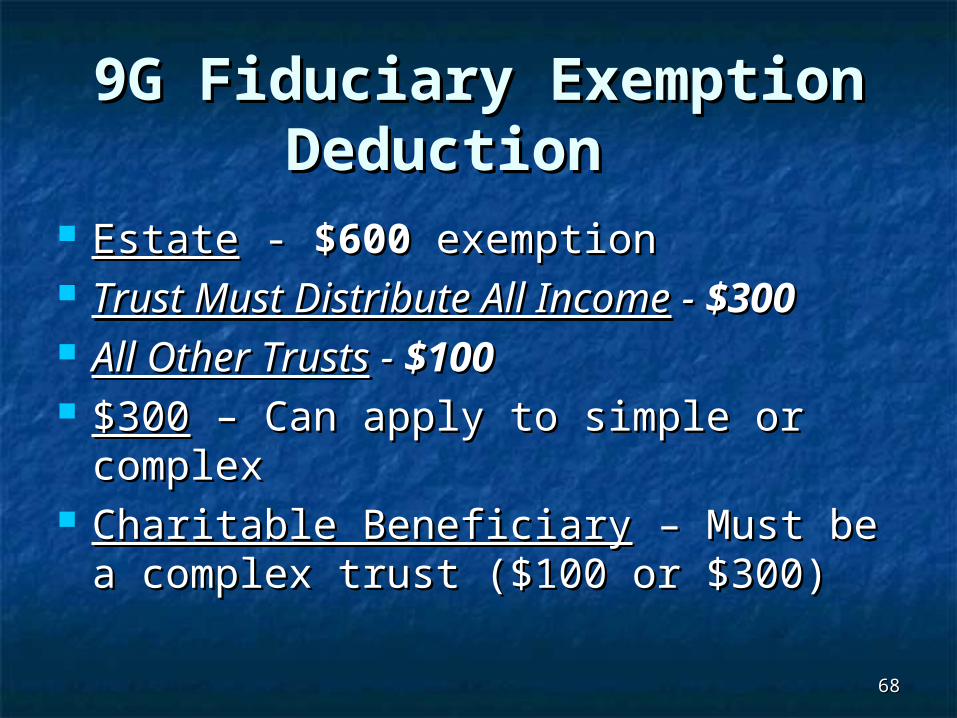

9G Fiduciary Exemption 9G Fiduciary Exemption DeductionDeduction

EstateEstate - - $600$600 exemption exemption Trust Must Distribute All IncomeTrust Must Distribute All Income - -

$300$300 All Other TrustsAll Other Trusts - - $100$100 $300$300 – Can apply to simple or complex – Can apply to simple or complex Charitable BeneficiaryCharitable Beneficiary – Must be a – Must be a

complex trust ($100 or $300)complex trust ($100 or $300)

6969

9H Fiduciary Taxable 9H Fiduciary Taxable Income Computation Income Computation

Beware!Beware! – Read each question carefully – Read each question carefully FocusFocus – On key differences for E&T, and be – On key differences for E&T, and be

SURESURE to use correct exemption to use correct exemption Distribution DeductionDistribution Deduction – Generally for any – Generally for any

distributions to beneficiaries; however, it distributions to beneficiaries; however, it can NEVER exceed DNIcan NEVER exceed DNI

Grantor of TrustGrantor of Trust – Taxed on trust income if – Taxed on trust income if he or she retains beneficial enjoyment or he or she retains beneficial enjoyment or substantial control over corpus or incomesubstantial control over corpus or income

Question 37Question 37

7070

Topic 10Topic 10

Business Business Retirement Retirement

PlansPlans

7171

10A Qualified Retirement 10A Qualified Retirement Plans – Basic RequirementsPlans – Basic Requirements Qualified PlansQualified Plans – Deductible contributions, tax- – Deductible contributions, tax-

free accumulation of earnings, tax deferral free accumulation of earnings, tax deferral ParticipationParticipation – Age 21 with 1 year of service – Age 21 with 1 year of service

(1,000 hrs), or 2 years with immediate (1,000 hrs), or 2 years with immediate vesting; must cover vesting; must cover lesser lesser of 50 employees or of 50 employees or 40% of all 40% of all

CoverageCoverage – 70% non-highly compensated (or – 70% non-highly compensated (or 70% of the highly-compensated coverage)70% of the highly-compensated coverage)

VestingVesting – 100% (5 yrs), or 20% (3 years), – 100% (5 yrs), or 20% (3 years), increasing 20% per year to 100% at 7 yearsincreasing 20% per year to 100% at 7 years

Figure 9 (Deduction/Contribution Limits)Figure 9 (Deduction/Contribution Limits) Question 38Question 38

7272

10B Keogh Plans – Basic 10B Keogh Plans – Basic RequirementsRequirements

KeoghKeogh – Establish by year end, cont. to due – Establish by year end, cont. to due date date

KeoghKeogh – S/E own employer, partner is – S/E own employer, partner is employeeemployee

Profit-Sharing PlanProfit-Sharing Plan – Need definite formula – Need definite formula Small EmployerSmall Employer – 50% credit ($500 max.) for – 50% credit ($500 max.) for

certain startup costs certain startup costs Net S/E EarningsNet S/E Earnings – Sch. C bus. income – Sch. C bus. income

(services involved), less ½ SE tax and less the (services involved), less ½ SE tax and less the Keogh contribution itselfKeogh contribution itself

General PartnersGeneral Partners – Usually have S/E earnings – Usually have S/E earnings Key Question 39Key Question 39

7373

10C Keoghs – Contribution 10C Keoghs – Contribution & Deduction Limits& Deduction Limits

Max. Keogh Limits (SE person & employee)Max. Keogh Limits (SE person & employee) – – subject to limitations (see subject to limitations (see Figure 10)Figure 10)

Excess ContributionsExcess Contributions – Carryover to next year – Carryover to next year ParticipantParticipant – May make nondeductible – May make nondeductible

contributions up to 10%contributions up to 10% Form 5500 or 5500-EZForm 5500 or 5500-EZ – If required, is due the – If required, is due the

last day of the last day of the 77thth month after plan yr., but month after plan yr., but neither required if plan assets < $100,000 neither required if plan assets < $100,000 (note – must file in the final year of plan)(note – must file in the final year of plan)

Figure 10Figure 10

7474

10D SEP-IRAs10D SEP-IRAs

SEP SEP – Employer makes contribution direct – Employer makes contribution direct to IRAs set up for employees (S/E may be to IRAs set up for employees (S/E may be only employee) – establish & contribute by only employee) – establish & contribute by due datedue date

Employer ContributionsEmployer Contributions – Must be – Must be nondiscrimi-natory, not in favor of “highly nondiscrimi-natory, not in favor of “highly comp” (5% own, >$90,000)comp” (5% own, >$90,000)

Max. ContributionMax. Contribution – – Lesser Lesser of (1) 25% of (1) 25% comp or $45,000 for each participantcomp or $45,000 for each participant

S/E PersonS/E Person – Uses S/E income – ½ S/E tax – – Uses S/E income – ½ S/E tax – SEP contribution (nets to 20% deduction)SEP contribution (nets to 20% deduction)

7575

10E SIMPLE Pension Plans10E SIMPLE Pension Plans

SIMPLESIMPLE – Employer with <=100 employees – Employer with <=100 employees ($5,000 salary); use either SIMPLE IRA or SIMPLE ($5,000 salary); use either SIMPLE IRA or SIMPLE 401(k)401(k)

EmployeeEmployee – Elective contributions up to – Elective contributions up to $10,500$10,500 per yearper year ($13,000 ($13,000 if age => 50) if age => 50)

EmployerEmployer – Must match employee contributions – Must match employee contributions up to up to 3%3% of comp; if employer makes nonelective of comp; if employer makes nonelective contribution, contribution, 2%2%

10% Penalty10% Penalty – Premature distribution, 25% if first – Premature distribution, 25% if first 2 yrs.2 yrs.

Question 40Question 40

7676

10F Pension Plans – 10F Pension Plans – Prohibited TransactionsProhibited Transactions

Prohibited TransactionsProhibited Transactions – Include: – Include: Transfer income/assets to “disqualified” Transfer income/assets to “disqualified”

person (e.g., employee, family member, person (e.g., employee, family member, etc.)etc.)

Fiduciary acting in its own self-interestFiduciary acting in its own self-interest Consideration to fiduciary from plan partyConsideration to fiduciary from plan party Any acts between plan/disqualified Any acts between plan/disqualified

Person (sell, lending, etc.)Person (sell, lending, etc.) Tax on TransactionTax on Transaction – 15%, increased to – 15%, increased to

100% if not corrected within one year100% if not corrected within one year

7777

Summaries – Key Factors in Summaries – Key Factors in Choice of Business EntityChoice of Business Entity

Figures 11 through 14Figures 11 through 14 – Provide – Provide summaries of the key nontax and tax summaries of the key nontax and tax factors related to four types of entities factors related to four types of entities (sole proprietorship, partnership, S (sole proprietorship, partnership, S corporation, and C corporation)corporation, and C corporation)

Figure 15Figure 15 – Provides a brief summary of – Provides a brief summary of other factors to consider in entity choiceother factors to consider in entity choice

Topic Topic – May appear in planning – May appear in planning questionsquestions

7878

Questions?Questions?

As Time PermitsAs Time Permits

Contact:Contact:John EverettJohn Everett

Professor of AccountingProfessor of AccountingVirginia Commonwealth UniversityVirginia Commonwealth University

[email protected]@vcu.edu