1 a strategy for fiscal adjustment when the recovery takes hold paolo mauro november 17, 2009...

TRANSCRIPT

1

A Strategy for Fiscal A Strategy for Fiscal Adjustment When the Adjustment When the Recovery Takes HoldRecovery Takes Hold

Paolo MauroPaolo Mauro

November 17, 2009November 17, 2009BangkokBangkok

2

3

Fiscal outlook in advanced G-20 countries (all variables in percent of GDP)

-12

-10

-8

-6

-4

-2

0

-7-6-5-4-3-2-10123

60

70

80

90

100

110

120

130

2000 01 02 03 04 05 06 07 08 09 10 11 12 13 14

General Government Gross Debt

2000 01 02

03 04 05 06 07 08 09 10 11 12 13 14

2000 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Overall balance

Cyclically-adjusted primary balance

Primary balance

4

What’s driving the change in the deficit in the advanced G20 economies?

• 6½ percentage points of GDP from 2007 to 2010

• Fiscal stimulus: 1½ percent of GDP• Automatic stabilizers: ~ 2½ percent • Other structural change: ~ 2½ percent

– Expenditure increases: ~ 1½ percent– Revenue losses: ~ 1 percent

• Losses on financial sector support:– 0.8 percent of GDP in 2009 (U.S., Japan)

5

Decomposition of Decomposition of government debt government debt

increase, 2007 - 2014increase, 2007 - 2014(Total debt increase: 40 percent of

GDP)

Financial Support

(4.9)

(3.3)

Fiscal Stimulus

(11.9)

Automatic Stabilizers

Assets and Commodity Prices

(9.3)

Other

(4.5) Higher Interest Payments

(5.9)

6

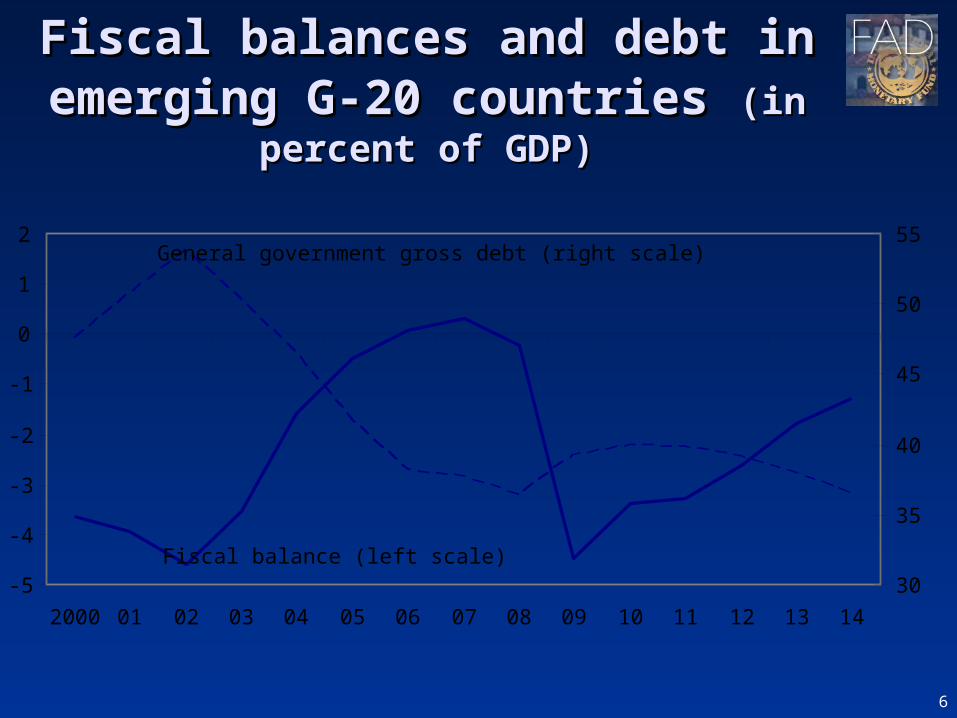

Fiscal balances and debt in Fiscal balances and debt in emerging G-20 countriesemerging G-20 countries (in (in

percent of GDP)percent of GDP)

-5

-4

-3

-2

-1

0

1

2

2000 01 02 03 04 05 06 07 08 09 10 11 12 13 14

30

35

40

45

50

55General government gross debt (right scale)

Fiscal balance (left scale)

7

Fiscal challenge: Stylized Fiscal challenge: Stylized factsfacts

The scale of the problem is The scale of the problem is unprecedentedunprecedented

Demographic trends are unfavorableDemographic trends are unfavorable Financial sector support only a small Financial sector support only a small

part of the increase in gross debt.part of the increase in gross debt.

8

Are markets worried?Are markets worried?Maybe; maybe not…yet? Maybe; maybe not…yet?

Sovereign CDS Spreads and EMBI Index

0

100

200

300

400

500

600

700

800

Ju

n-0

8

Ju

l-0

8

Au

g-0

8

Sep

-08

Oc

t-08

No

v-0

8

De

c-0

8

Jan

-09

Fe

b-0

9

Mar

-09

Ap

r-0

9

May

-09

Ju

n-0

9

Ju

l-0

9

Au

g-0

9

Sep

-09

Oc

t-09

No

v-0

9 0

40

80

120

160

200

EMBI Global Index 3/(lhs)

Emerging Markets CDS Index (lhs)

Advanced EconomiesCDS Index (rhs)

Sources: Markit, CMA, Datastream, and IMF Staff calculations

JAP

ITA

DEU

FRA

USA

GBR

-10 0 10 20 30 40 50 60 70

`

Change in Sovereign CDS Spreads since 2007 1/

1/ Change between October 2009 average and 2007 average.

Some signs of regularization… …some signs of differentiation?

9

Should we be concerned?Should we be concerned?Can’t we live with high debt?Can’t we live with high debt?

High debt may lead to high interest ratesHigh debt may lead to high interest rates Interest rates are historically lowInterest rates are historically low 40 percent increase in debt => 2 percent rise in rates?40 percent increase in debt => 2 percent rise in rates? Crowding out of other spendingCrowding out of other spending

Markets might react abruptly if they worry that governments Markets might react abruptly if they worry that governments do not have a plan for fiscal adjustmentdo not have a plan for fiscal adjustment

Reduced capacity to respond to future shocksReduced capacity to respond to future shocks

High debt may lead to slow growth? High debt may lead to slow growth?

10

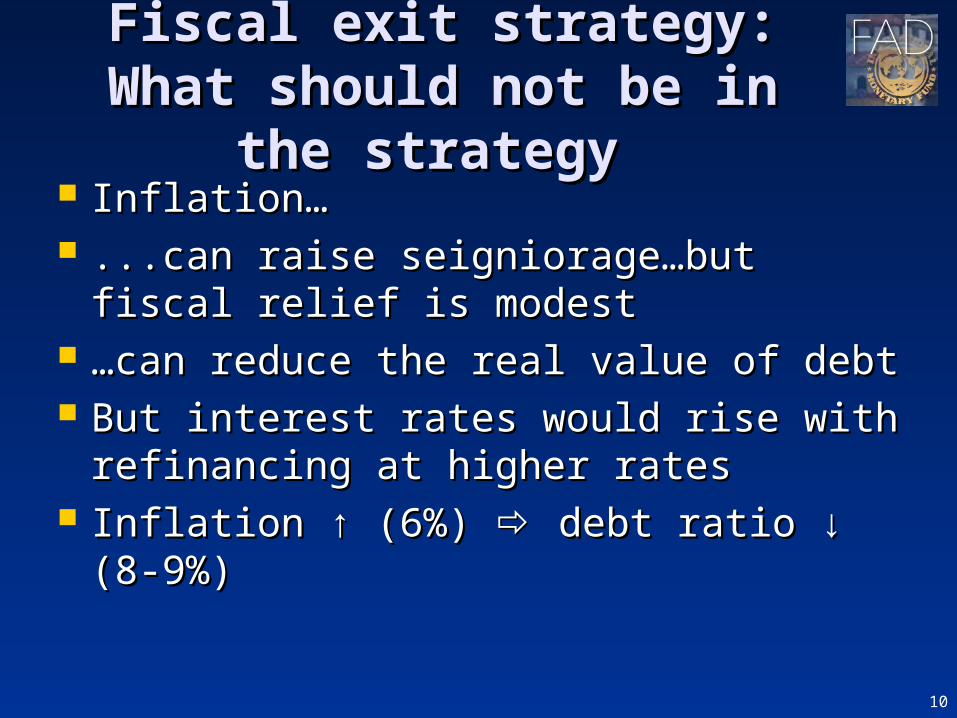

Fiscal exit strategy: What Fiscal exit strategy: What should not be in the should not be in the

strategy strategy Inflation…Inflation… ...can raise seigniorage…but fiscal ...can raise seigniorage…but fiscal

relief is modestrelief is modest ……can reduce the real value of debtcan reduce the real value of debt But interest rates would rise with But interest rates would rise with

refinancing at higher ratesrefinancing at higher rates Inflation ↑ (6%) Inflation ↑ (6%) debt ratio ↓ (8- debt ratio ↓ (8-

9%)9%)

11

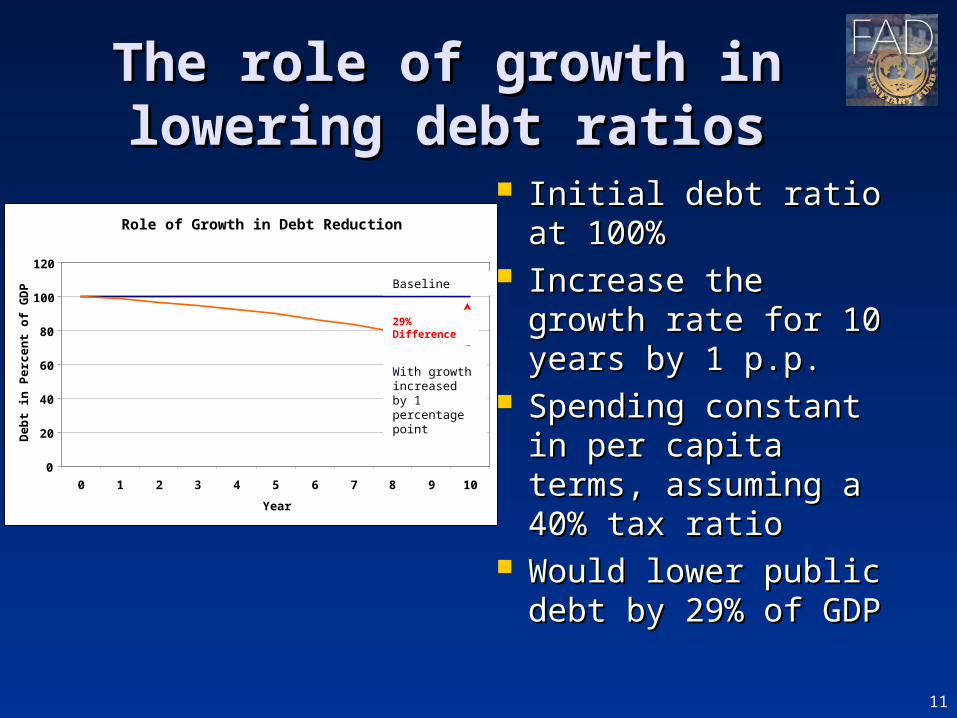

The role of growth in The role of growth in lowering debt ratioslowering debt ratios

Initial debt ratio at Initial debt ratio at 100%100%

Increase the growth Increase the growth rate for 10 years by 1 rate for 10 years by 1 p.p.p.p.

Spending constant in Spending constant in per capita terms, per capita terms, assuming a 40% tax assuming a 40% tax ratioratio

Would lower public Would lower public debt by 29% of GDPdebt by 29% of GDP

Role of Growth in Debt Reduction

0

20

40

60

80

100

120

0 1 2 3 4 5 6 7 8 9 10

Year

Deb

t in

Per

cen

t of

GD

P

29% Difference

With growth increased by 1 percentage point

Baseline

12

AssumptionsAssumptions

Goal: debt ratios < 60% of GDP by Goal: debt ratios < 60% of GDP by 20302030

Adjustment in the primary balance Adjustment in the primary balance will start in 2011will start in 2011

Adjustment will last 10 years; Adjustment will last 10 years; constant primary balance afterwardsconstant primary balance afterwards

13

General government gross debt-to-GDP ratio

0.00

20.00

40.00

60.00

80.00

100.00

120.00

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Cyclically- adjusted primary balance

Primary balance

Overall balance

Fiscal Balances in Advanced Economies (in percent of GDP)

14

Required Fiscal Adjustment in Structural Primary Balance Between 2010 and 2020

Aus

tral

ia

Aus

tria

Bel

gium

Can

ada

Den

mar

k

Fin

land

Fra

nce

Ger

man

y

Gre

ece

Icel

and

Irel

and

Ital

y

Japa

n

Kor

ea

Net

herl

ands

New

Zea

land

Por

tuga

l

Spa

in

Sw

eden

Uni

ted

Kin

gdom

Uni

ted

Sta

tes

-20

-15

-10

-5

0

5

10

Per

cent

of

GD

PFor most advanced economies, For most advanced economies,

major fiscal adjustment is major fiscal adjustment is requiredrequired

15

Why Is So Much Adjustment Needed?Why Is So Much Adjustment Needed?

To reverse discretionary stimulusTo reverse discretionary stimulus

To offset higher interest payments To offset higher interest payments

To address already-high structural deficits in some To address already-high structural deficits in some countriescountries

To address rising spending pressures not linked to To address rising spending pressures not linked to crisiscrisis

To account for revenues that may not come backTo account for revenues that may not come back

16

An optimistic angle on a big problemAn optimistic angle on a big problem

The scale of adjustment is large…The scale of adjustment is large…

… … But Not UnprecedentedBut Not Unprecedented 20+ advanced economies have improved their structural 20+ advanced economies have improved their structural

primary balances by at least 5 percentage points in primary balances by at least 5 percentage points in sustained adjustments in the past four decades.sustained adjustments in the past four decades.

10 have achieved adjustments of at least 10 percent.10 have achieved adjustments of at least 10 percent.

Primary adjustment was the bedrock of these effortsPrimary adjustment was the bedrock of these efforts Inflation is Inflation is notnot the answer the answer

17

Examples of large fiscal Examples of large fiscal adjustmentsadjustments

Episodes of Significant Fiscal Consolidation (Emerging Economies)

0 5 10 15 20 25

Romania 1996 to 1999

Turkey 1997 to 2001

Romania 1979 to 1984

Paraguay 1981 to 1990

Panama 1982 to 1986

Bulgaria 1993 to 1996

Hungary 1993 to 1996

Morocco 1982 to 1988

Chile 1999 to 2007

Slovak Republic 1992 to 1995

Lebanon 2000 to 2006

Egypt 1984 to 1987

Lebanon 1996 to 1999

Czech Republic 1995 to 1999

Jamaica 1997 to 2000

Turkey 1987 to 1990

Mexico 1981 to 1984

Jordan 1987 to 1990

Tunisia 1983 to 1989

Egypt 1991 to 1994

Jamaica 1983 to 1989

Georgia 1994 to 2004

Structural Balance in % of GDP

22 Emerging Economies

Episodes of Significant Fiscal Consolidation (Advanced Economies)

0 2 4 6 8 10 12 14 16 18 20

Japan1978 to1990

United Kingdom 1993 to 2000

Cyprus 2003 to 2007

Canada1985 to 1999

Belgium 1983 to 1998

Israel 1980 to 1983

China,P.R.:Hong Kong 2001 to 2007

Greece 1989 to 1995

Denmark 1982 to 1986

Sweden 1980 to 1987

Finland 1993 to 2000

Sweden 1993 to 2000

Ireland 1978 to 1989

Structural Balance in % of GDP

13 Advanced Economies

18

How fiscal adjustment How fiscal adjustment could be attainedcould be attained

Not renewing the Not renewing the stimulus measuresstimulus measures

Reform entitlements to fix Reform entitlements to fix as share of GDP as share of GDP (otherwise would rise by (otherwise would rise by 3-4% of GDP by 2030)3-4% of GDP by 2030)

Target stable real primary Target stable real primary spending per capita spending per capita (excluding entitlements)(excluding entitlements)

Tax measures: Broaden Tax measures: Broaden the tax base, correct the tax base, correct externalities (carbon externalities (carbon taxes ½ % of GDP)taxes ½ % of GDP)

8% Improvement in Cyclically Adjusted Primary Balance

Fiscal Stimulus Expiring (1.5%)

Freeze in Real

Spending (3.5%)

Tax Measures (3%)

0

1

2

3

4

5

6

7

8

9

Per

cen

t of

GD

P

19

ConclusionsConclusions

Too soon to tighten fiscal policiesToo soon to tighten fiscal policies NotNot too soon to: too soon to:

1.1. Communicate strategies and measures Communicate strategies and measures to ensure fiscal solvencyto ensure fiscal solvency

2.2. Implement actions without a negative Implement actions without a negative impact on demand (transparency and impact on demand (transparency and medium-term fiscal frameworks) medium-term fiscal frameworks)

3.3. Substantive reforms of entitlements Substantive reforms of entitlements with an impact only in the medium term with an impact only in the medium term should start nowshould start now