0802china property weekly digest

TRANSCRIPT

ed-JS / sa- AH

Lower sales as expected

Various Tier II cities, including Wuhan, Changsha,

Xi’an etc., attract talent by offering residency and

subsidies, and these policies would support

housing demand in these cities in the long run Last week (24-30 July), GFA sold in 36 cities fell by

2% w-o-w. GFA sold in Tier I/II/III cities changed by

23%/-7%/-3% w-o-w. In July 2017, GFA sold in 36

cities dropped 20.6% y-o-y and 11.6% m-o-m. CRIC

estimates that sales recorded by major listed

developers would drop by c.20% m-o-m in July

compared with 20% m-o-m increase in June ASP of key cities recovered by 4.2% w-o-w, with Tier

I/II/III cities’ ASP changing by 3%/-2%/7% Inventory level of key cities remained at 43 weeks; sell-

through rate of newly launched projects in Tier I & II

cities improved to 86%

Last week, COGO (81 HK) and Shimao (813 HK)

recorded highest growth in southbound

shareholding while China SCE (832 HK) and

Evergrande (3333 HK) saw the largest declines in

southbound shareholding

HSI: 27,540 ANALYST Trista QIN +852 2863 8820 [email protected] Carol WU +852 2863 8841 [email protected] Danielle Wang, CFA +852 2820 4915 [email protected] Ken HE CFA, +86 21 6888 3375 [email protected]

Weekly sales performance of major cities (Jul 24 – Jul 30)

w-o-wYT D v s

2016YTD v s

2015

Avg weekly GFA sold ↓ 2.3% ↓ 15.1% ↑ 0.6%

ASP ↑ 4.2% ↑ 7.6% ↑ 18.0%

Inventory (no. of weeks) ↑ 0.3 ↓ 0.8 ↓ 16.2

v s same period 2016

v s same period 2015

YTD GFA sold ↓ 15.4% ↑ 11.2% Inventory (no. of weeks of sales) of 16 cities*

0102030405060708090

100

Jan

-11

Mar

-12

Jun

-13

Au

g-1

4

No

v-1

5

Jan

-17

Inventory (no. of weeks) 26 weeks rolling avg

New launches in 10 major cities and sell-through rate

0%10%20%30%40%50%60%70%80%90%100%

0

5,000

10,000

15,000

20,000

25,000

32W

1250

W12

14W

1332

W13

50W

1318

W14

35W

142W

1519

W15

36W

151W

1618

W16

35W

1652

W16

17W

17

Total units launched (LHS)Sell-through rate (RHS)6 mths average sell-Through (RHS)

Source: CREIS, Fang.com, DBS Vickers * Rolling 26 weeks inventory

DBS Group Research . Equity 2 Aug 2017

China / Hong Kong

China Property Weekly Digest (Issue No. 230) Refer to important disclosures at the end of this report

China / Hong Kong

China Property Weekly Digest

Page 2

Share price performance

YTD Share price performance

Average short selling interest as percentage of trading volume (Jul 24 – Jul 28)

-100% 0% 100% 200% 300% 400%

EvergrandeZhong An

SunacC Garden

AgileLarge caps

LongforKaisa

CIFICOGO

YuzhouChina SCE

GreentownPoly HK

PowerlongMid caps

ShimaoGreenland HK

Small capsGZ R&F

CR LandBJ Cap Land

YuexiuYanlord

MSCI ChinaBJ North Star

KWGVanke

COLISino-Ocean

HSI IndexGlorious

SOHOShui On Land

HopsonChina South City

First SponsorYing Li

SRERenhe

CC Land

Sector avg: +61%

0% 5% 10% 15% 20% 25% 30% 35%

CR LandShimao PropertyChina Overseas

Renhe CommercialAgile Property

C C LandSunac China

LongforPoly (Hong Kong)

KWG PropertyGlorious Property

Yuzhou PropertiesSino-Ocean LandCountry Garden

Ying LiCOGO

Guangzhou R&FSoho ChinaEvergrandeGreentown

Times PropertyCentral ChinaShui On Land

China South CityLogan Property

China Vanke 'H'BJ Cap Land 'H'

GreenlandYanlord Land

China SCEYuexiu Property

Sector Avearge: 9%

Daily trading volume (Jul 24 – Jul 28)

0

50

100

150

200

250

300

350

400

Sun

ac

Ever

gra

nd

e

CO

LI

C G

ard

en

Van

ke

CR

Lan

d

GZ

R&

F

Lon

gfo

r

Ag

ile

Shim

ao

KW

G

Poly

HK

Ch

ina

SCE

CIF

I

Gre

ento

wn

Ch

ina

Sou

th C

ity

Sin

o-O

cean

Yu

exiu

Shu

i On

Lan

d

Yu

zho

u

CO

GO

SOH

O

Zho

ng

An

BJ C

ap L

and

Yan

lord

Pow

erlo

ng

Gre

enla

nd

HK

Ho

pso

n

BJ N

ort

h S

tar

Glo

rio

us

CC

Lan

d

Yin

g L

i

Ren

he

SRE

Firs

t Sp

on

sor

Source: Bloomberg Finance L.P, HKEx, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 3

Overall southbound shareholding in CCASS w-o-w % changes of shareholding by southbound trading

8,100 8,200 8,300 8,400 8,500 8,600 8,700 8,800 8,900 9,000

17-M

ar-1

7

31-M

ar-1

7

14-A

pr-1

7

28-A

pr-1

7

12-M

ay-1

7

26-M

ay-1

7

9-Ju

n-17

23-J

un-1

7

mn

-15% -10% -5% 0% 5% 10% 15% 20%

COGO

Shimao

Sunac

Longfor

Agile

Vanke

CIFI

KWG

China South City

BJ North Star

Greentown

GZ R&F

Shui On Land

Poly HK

COLI

Yuexiu

Hopson

CR Land

SOHO

Sino-Ocean

Country Garden

Evergrande

China SCE

Source: Bloomberg Finance L.P, HKEx, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 4

Average weekly trading volume

0

50

100

150

200

250

300

350

400

450

Ever

gra

nd

eC

OLI

CR

Lan

dSu

nac

C G

ard

enV

anke

GZ

R&

FA

gile

Lon

gfo

rSh

imao

KW

GG

reen

tow

nSO

HO

Yu

exiu

Poly

HK

Sin

o-O

cean

Ch

ina

SCE

Yu

zho

uY

anlo

rdC

OG

OSh

ui O

n L

and

BJ C

ap L

and

Gre

enla

nd

HK

BJ N

ort

h S

tar

Zho

ng

An

Yin

g L

iH

op

son

Glo

riou

sC

C L

and

Ren

he

SRE

Ch

ina

Sou

th C

ity

CIF

IFi

rst S

po

nso

rK

aisa

Pow

erlo

ng

YTD 2016 2015

US$ mn

Source: Bloomberg Finance L.P, DBS Vickers

New projects launched (Jul 24 – Jul 30):

31 projects were launched in Major Tier I&II cities. 8 projects were launched in Chengdu

Total of 6.3k units were launched in Major Tier I&II cities. Average sell-through rate for new launches increased to 86%

0%

20%

40%

60%

80%

100%

0

2

4

6

8

10

Bei

jing

Shan

gh

ai

Shen

zhen

Gu

ang

zho

u

Wu

han

Han

gzh

ou

Tian

jin

Ch

on

gq

ing

Nan

jing

Ch

eng

du

Launches (LHS) Sell-through rate (RHS)

Unit

0%10%20%30%40%50%60%70%80%90%100%

0

5,000

10,000

15,000

20,000

25,000

32

W1

25

0W

12

14

W1

33

2W

13

50

W1

31

8W

14

35

W1

42

W1

51

9W

15

36

W1

51

W1

61

8W

16

35

W1

65

2W

16

17

W1

7

Total units launched (LHS)Sell-through rate (RHS)6 mths average sell-Through (RHS)

Source: CREIS, DBS Vickers Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 5

Weekly sales performance of major cities

Tier I cities

Tier I cities: Weekly GFA sales of key cities

G F A % change as compared t o

Cit yLast w eek

(000 sm) w - o- w y - o- y

A v g o f p rev ious 4

w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012

Beijing 193 130% -15% 149% 5% -12% 2% -22% -23%

Shanghai 310 10% -44% -1% -26% -29% -1% -10% 12%

Shenzhen 27 -28% -53% -48% -66% -79% -65% -68% -61%

Guangzhou 105 -5% -67% -33% -61% -50% -34% -48% -49%

T ier I t o t al 635 23% - 45% 17% - 37% - 42% - 24% - 37% - 30%

Source: CREIS, DBS Vickers

Tier I cities: Weekly ASP of key cities

A SP % change as compared t o

Cit yLast w eek

(Rmb/sm) w - o- w y - o- y

A v g o f prev ious 4 w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012

Beijing 50,218 7% 40% 3% 39% 87% 97% 114% 143%

Shanghai 26,753 -3% -3% -4% 1% 16% 42% 44% 72%

Shenzhen 55,877 13% 3% 4% 3% 69% 137% 153% 199%

Guangzhou 14,985 -5% -16% -11% -9% -1% 1% 17% 25%

T ier I t o t al 36 ,958 3% 6% - 2% 8% 43% 69% 82% 110%

Source: CREIS, DBS Vickers

Tier I cities: YTD GFA sales of key cities Tier I cities: Avg ASP of key cities

-60%

-50%

-40%

-30%

-20%

-10%

0%

02,0004,0006,0008,000

10,00012,00014,00016,000

Shan

gh

ai

Bei

jing

Gu

ang

zho

u

Shen

zhen

Yoy (%)000 sm

2017 (LHS) 2016 (LHS)

-2%0%2%4%6%8%10%12%14%16%18%

0

10,000

20,000

30,000

40,000

50,000

60,000

Bei

jing

Shen

zhen

Shan

gh

ai

Gu

ang

zho

u

Yoy (%)RMB/sm

2017 avg (LHS) 2016 avg (LHS) Yoy (RHS)

Source: CREIS, DBS Vickers Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 6

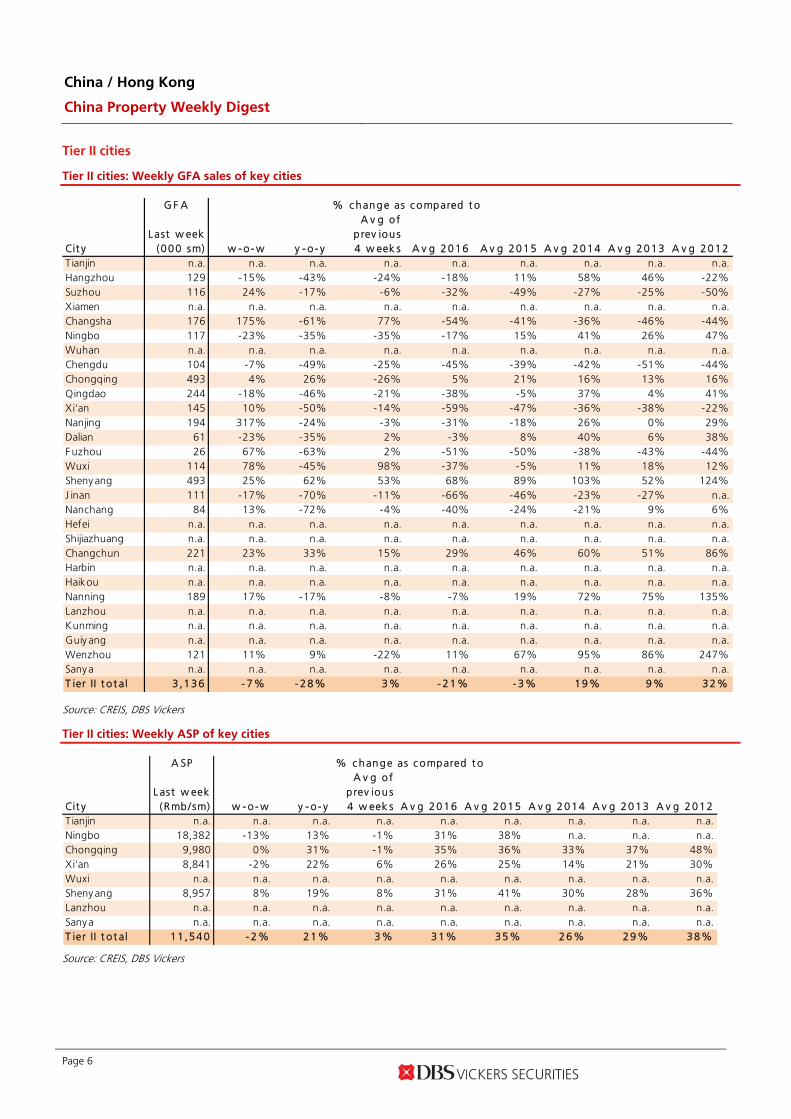

Tier II cities

Tier II cities: Weekly GFA sales of key cities

G F A % c hange as c ompared t o

Cit yL ast w eek

(000 sm) w - o - w y - o - y

A v g o f p rev iou s 4 w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012

Tianjin n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Hangzhou 129 -15% -43% -24% -18% 11% 58% 46% -22%Suzhou 116 24% -17% -6% -32% -49% -27% -25% -50%Xiamen n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Changsha 176 175% -61% 77% -54% -41% -36% -46% -44%Ningbo 117 -23% -35% -35% -17% 15% 41% 26% 47%Wuhan n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Chengdu 104 -7% -49% -25% -45% -39% -42% -51% -44%Chongqing 493 4% 26% -26% 5% 21% 16% 13% 16%Qingdao 244 -18% -46% -21% -38% -5% 37% 4% 41%Xi'an 145 10% -50% -14% -59% -47% -36% -38% -22%Nanjing 194 317% -24% -3% -31% -18% 26% 0% 29%Dalian 61 -23% -35% 2% -3% 8% 40% 6% 38%F uzhou 26 67% -63% 2% -51% -50% -38% -43% -44%Wuxi 114 78% -45% 98% -37% -5% 11% 18% 12%Sheny ang 493 25% 62% 53% 68% 89% 103% 52% 124%J inan 111 -17% -70% -11% -66% -46% -23% -27% n.a.Nanchang 84 13% -72% -4% -40% -24% -21% 9% 6%Hefei n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Shijiazhuang n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Changchun 221 23% 33% 15% 29% 46% 60% 51% 86%Harbin n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Haikou n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Nanning 189 17% -17% -8% -7% 19% 72% 75% 135%Lanzhou n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Kunming n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Guiy ang n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Wenzhou 121 11% 9% -22% 11% 67% 95% 86% 247%Sany a n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.T ier II t o t al 3 ,136 - 7% - 28% 3% - 21% - 3% 19% 9% 32%

Source: CREIS, DBS Vickers

Tier II cities: Weekly ASP of key cities

A SP % c hange as c ompared t o

Cit yL ast w eek

(Rmb /sm) w - o - w y - o - y

A v g o f p rev iou s 4 w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012

Tianjin n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Ningbo 18,382 -13% 13% -1% 31% 38% n.a. n.a. n.a.Chongqing 9,980 0% 31% -1% 35% 36% 33% 37% 48%Xi'an 8,841 -2% 22% 6% 26% 25% 14% 21% 30%Wuxi n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Sheny ang 8,957 8% 19% 8% 31% 41% 30% 28% 36%Lanzhou n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Sany a n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.T ier II t o t al 11 ,540 - 2% 21% 3% 31% 35% 26% 29% 38%

Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 7

Tier II cities: YTD GFA sales of key cities

-80%

-60%

-40%

-20%

0%

20%

40%

60%

(1,500)

3,500

8,500

13,500

18,500

23,500

Wu

han

Ch

ongq

ing

Ch

ang

sha

Ku

nm

ing

Xia

n

Qin

gd

ao

Shen

yan

g

Ch

ang

chu

n

Nan

jing

Suzh

ou

Ch

eng

du

Nin

gb

o

Dal

ian

Nan

chan

g

Wu

xi

Han

gzh

ou

Wen

zho

u

Fuzh

ou

San

ya

Nan

nin

g

Hai

kou

Ch

ang

sha

Yoy (%)000 sm

2017 (LHS) 2016 (LHS) Yoy (RHS)

Source: CREIS, DBS Vickers

Tier II cities: Avg ASP of key cities

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Changsha Xian Chongqing Shenyang Shenyang

Yoy (%)RMB/sm

2017 avg (LHS) 2016 avg (LHS) Yoy (RHS)

Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 8

Tier III cities

Tier III cities: Weekly GFA sales of key cities

G F A % c hange as c ompared t o

Cit yL ast w eek

(000 sm) w - o - w y - o - y

A v g o f p rev iou s 4

w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012Dongguan 82 21% -58% 9% -53% -57% -24% -43% -28%Weifang n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Baotou 70 -17% 31% -8% 6% 26% 27% 31% -1%Guilin n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Xuzhou 244 -10% -5% -13% -16% 16% 34% 23% 68%Bengbu 52 8% -32% 16% -25% 56% 42% 20% 123%Yangzhou n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Huizhou 50 -11% -47% 4% -50% -27% -3% -22% -21%Liany ungang 132 -15% 11% -19% 6% 31% 54% 22% 48%Shantou 99 7% n.a. -18% 62% 185% 441% 355% 425%Zhongshan n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Dandong n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.J iujiang 85 0% 126% n.a. 62% 78% 103% 162% 279%Shaoguan 24 -13% -65% -24% -35% 5% 23% 14% 55%Luzhou n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Nanchong n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Zhoushan 24 3% 0% -10% -13% 7% 48% 18% 99%Dongy ing 46 24% 16% 11% 24% 26% 39% -6% 70%Huaian 2 -97% -98% -98% -99% -98% -98% -98% -97%Wuhu 49 -1% -47% -8% -45% 5% 25% 14% -11%Guan n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.J iaozuo 20 35% 158% 19% 2% 12% 113% 0% -5%Zhaoqing 50 1% 15% -22% -2% 22% 84% 51% 52%T ier III t o t al 1 ,030 - 3% 2% - 11% - 12% 19% 61% 36% 70%

Source: CREIS, DBS Vickers

Tier III cities: Weekly ASP of key cities

A SP % c hange as c ompared t o

Cit yL ast w eek

(Rmb /sm) w - o - w y - o - y

A v g o f p rev iou s 4 w eek s A v g 2016 A v g 2015 A v g 2014 A v g 2013 A v g 2012

Dongguan n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Weifang n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Baotou 5,509 2% n.a. 2% 9% 7% 8% 8% 20%Bengbu n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Shantou 9,452 11% n.a. 8% 15% 17% 17% 6% 34%Dandong n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.J iujiang n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Shaoguan 5,711 2% 141% -5% 27% 13% 9% 6% 8%Dongy ing n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Huaian 5,467 24% 15% 19% 26% 31% 25% 25% 35%J iaozuo n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Zhaoqing 6,641 -4% 23% -10% 23% 27% 17% 11% 28%T ier II I t o t al 6 ,556 7% 60% 3% 20% 19% 15% 11% 25%

Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 9

Tier III cities: YTD GFA sales of key cities

-100%-50%0%50%100%150%200%250%300%

(600)

1,400

3,400

5,400

7,400

9,400

11,400

13,400

Xu

zho

u

Wu

hu

Do

ng

gu

an

Lian

yun

gan

g

Shao

xin

g

Hu

izho

u

Zho

ush

an

Bao

tou

Jiu

jian

g

Yan

gzh

ou

Wu

hu

Ben

gb

u

Zhao

qin

g

Shan

tou

Shao

gu

an

Hu

aian

Do

ngyi

ng

Yoy (%)000 sm

2017 (LHS) 2016 (LHS) Yoy (RHS)

Source: CREIS, DBS Vickers

Tier III cities: Avg ASP of key cities

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

Shaoxing Jiujiang Zhaoqing Baotou Shaoguan

Yoy (%)RMB/sm

2017 avg (LHS) 2016 avg (LHS) Yoy (RHS)

Source: CREIS, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 10

Inventory level

No. of weeks to digest inventory

Source: CREIS, DBS Vickers

Trend: No. of weeks to digest inventory

0

20

40

60

80

100

120

140

Jan

-11

Mar

-12

Jun

-13

Au

g-1

4

No

v-1

5

Jan

-17

Tier I average Tier II average Tier III average

Tier 1

Tier 2

Tier 3

weeks

Source: CREIS, DBS Vickers

Notes: 1. Based on 26 weeks average sales

2. Only Huizhou, Jiujiang, Nanchong, Zhoushan and Dongying are included in Tier III cities

China / Hong Kong

China Property Weekly Digest

Page 11

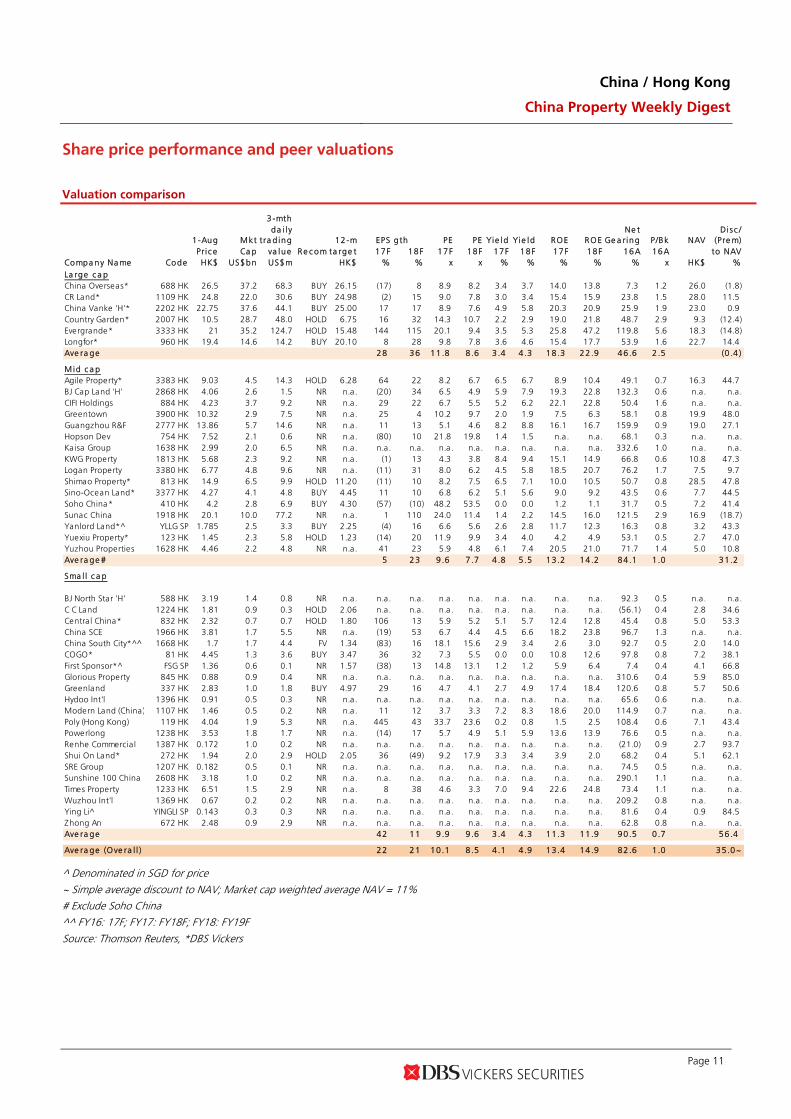

Share price performance and peer valuations

Valuation comparison

3-mthda i l y Ne t Di sc /

Mkt tra d ing 12-m EPS g th PE PE Yie ld Yie ld ROE ROE Ge a ring P/Bk NAV (Pre m)Pri c e Ca p va lue Re c om ta rge t 17F 18F 17F 18F 17F 18F 17F 18F 16A 16A to NAV

Compa ny Na me Code HK$ US$bn US$m HK$ % % x x % % % % % x HK$ %La rge c a pChina Overseas* 688 HK 26.5 37.2 68.3 BUY 26.15 (17) 8 8.9 8.2 3.4 3.7 14.0 13.8 7.3 1.2 26.0 (1.8)CR Land* 1109 HK 24.8 22.0 30.6 BUY 24.98 (2) 15 9.0 7.8 3.0 3.4 15.4 15.9 23.8 1.5 28.0 11.5China Vanke 'H'* 2202 HK 22.75 37.6 44.1 BUY 25.00 17 17 8.9 7.6 4.9 5.8 20.3 20.9 25.9 1.9 23.0 0.9Country Garden* 2007 HK 10.5 28.7 48.0 HOLD 6.75 16 32 14.3 10.7 2.2 2.9 19.0 21.8 48.7 2.9 9.3 (12.4)Evergrande* 3333 HK 21 35.2 124.7 HOLD 15.48 144 115 20.1 9.4 3.5 5.3 25.8 47.2 119.8 5.6 18.3 (14.8)Longfor* 960 HK 19.4 14.6 14.2 BUY 20.10 8 28 9.8 7.8 3.6 4.6 15.4 17.7 53.9 1.6 22.7 14.4Ave ra ge 28 36 11 .8 8 .6 3 .4 4 .3 18 .3 22 .9 46 .6 2 .5 (0 .4 )

M id c a pAgile Property* 3383 HK 9.03 4.5 14.3 HOLD 6.28 64 22 8.2 6.7 6.5 6.7 8.9 10.4 49.1 0.7 16.3 44.7BJ Cap Land 'H' 2868 HK 4.06 2.6 1.5 NR n.a. (20) 34 6.5 4.9 5.9 7.9 19.3 22.8 132.3 0.6 n.a. n.a.CIFI Holdings 884 HK 4.23 3.7 9.2 NR n.a. 29 22 6.7 5.5 5.2 6.2 22.1 22.8 50.4 1.6 n.a. n.a.Greentown 3900 HK 10.32 2.9 7.5 NR n.a. 25 4 10.2 9.7 2.0 1.9 7.5 6.3 58.1 0.8 19.9 48.0Guangzhou R&F 2777 HK 13.86 5.7 14.6 NR n.a. 11 13 5.1 4.6 8.2 8.8 16.1 16.7 159.9 0.9 19.0 27.1Hopson Dev 754 HK 7.52 2.1 0.6 NR n.a. (80) 10 21.8 19.8 1.4 1.5 n.a. n.a. 68.1 0.3 n.a. n.a.Kaisa Group 1638 HK 2.99 2.0 6.5 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 332.6 1.0 n.a. n.a.KWG Property 1813 HK 5.68 2.3 9.2 NR n.a. (1) 13 4.3 3.8 8.4 9.4 15.1 14.9 66.8 0.6 10.8 47.3Logan Property 3380 HK 6.77 4.8 9.6 NR n.a. (11) 31 8.0 6.2 4.5 5.8 18.5 20.7 76.2 1.7 7.5 9.7Shimao Property* 813 HK 14.9 6.5 9.9 HOLD 11.20 (11) 10 8.2 7.5 6.5 7.1 10.0 10.5 50.7 0.8 28.5 47.8Sino-Ocean Land* 3377 HK 4.27 4.1 4.8 BUY 4.45 11 10 6.8 6.2 5.1 5.6 9.0 9.2 43.5 0.6 7.7 44.5Soho China* 410 HK 4.2 2.8 6.9 BUY 4.30 (57) (10) 48.2 53.5 0.0 0.0 1.2 1.1 31.7 0.5 7.2 41.4Sunac China 1918 HK 20.1 10.0 77.2 NR n.a. 1 110 24.0 11.4 1.4 2.2 14.5 16.0 121.5 2.9 16.9 (18.7)Yanlord Land*^ YLLG SP 1.785 2.5 3.3 BUY 2.25 (4) 16 6.6 5.6 2.6 2.8 11.7 12.3 16.3 0.8 3.2 43.3Yuexiu Property* 123 HK 1.45 2.3 5.8 HOLD 1.23 (14) 20 11.9 9.9 3.4 4.0 4.2 4.9 53.1 0.5 2.7 47.0Yuzhou Properties 1628 HK 4.46 2.2 4.8 NR n.a. 41 23 5.9 4.8 6.1 7.4 20.5 21.0 71.7 1.4 5.0 10.8Ave ra ge # 5 23 9 .6 7 .7 4 .8 5 .5 13 .2 14 .2 84 .1 1 .0 31 .2

Sma l l c a p

BJ North Star 'H' 588 HK 3.19 1.4 0.8 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 92.3 0.5 n.a. n.a.C C Land 1224 HK 1.81 0.9 0.3 HOLD 2.06 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. (56.1) 0.4 2.8 34.6Central China* 832 HK 2.32 0.7 0.7 HOLD 1.80 106 13 5.9 5.2 5.1 5.7 12.4 12.8 45.4 0.8 5.0 53.3China SCE 1966 HK 3.81 1.7 5.5 NR n.a. (19) 53 6.7 4.4 4.5 6.6 18.2 23.8 96.7 1.3 n.a. n.a.China South City*^^ 1668 HK 1.7 1.7 4.4 FV 1.34 (83) 16 18.1 15.6 2.9 3.4 2.6 3.0 92.7 0.5 2.0 14.0COGO* 81 HK 4.45 1.3 3.6 BUY 3.47 36 32 7.3 5.5 0.0 0.0 10.8 12.6 97.8 0.8 7.2 38.1First Sponsor*^ FSG SP 1.36 0.6 0.1 NR 1.57 (38) 13 14.8 13.1 1.2 1.2 5.9 6.4 7.4 0.4 4.1 66.8Glorious Property 845 HK 0.88 0.9 0.4 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 310.6 0.4 5.9 85.0Greenland 337 HK 2.83 1.0 1.8 BUY 4.97 29 16 4.7 4.1 2.7 4.9 17.4 18.4 120.6 0.8 5.7 50.6Hydoo Int'l 1396 HK 0.91 0.5 0.3 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 65.6 0.6 n.a. n.a.Modern Land (China) 1107 HK 1.46 0.5 0.2 NR n.a. 11 12 3.7 3.3 7.2 8.3 18.6 20.0 114.9 0.7 n.a. n.a.Poly (Hong Kong) 119 HK 4.04 1.9 5.3 NR n.a. 445 43 33.7 23.6 0.2 0.8 1.5 2.5 108.4 0.6 7.1 43.4Powerlong 1238 HK 3.53 1.8 1.7 NR n.a. (14) 17 5.7 4.9 5.1 5.9 13.6 13.9 76.6 0.5 n.a. n.a.Renhe Commercia l 1387 HK 0.172 1.0 0.2 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. (21.0) 0.9 2.7 93.7Shui On Land* 272 HK 1.94 2.0 2.9 HOLD 2.05 36 (49) 9.2 17.9 3.3 3.4 3.9 2.0 68.2 0.4 5.1 62.1SRE Group 1207 HK 0.182 0.5 0.1 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 74.5 0.5 n.a. n.a.Sunshine 100 China 2608 HK 3.18 1.0 0.2 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 290.1 1.1 n.a. n.a.Times Property 1233 HK 6.51 1.5 2.9 NR n.a. 8 38 4.6 3.3 7.0 9.4 22.6 24.8 73.4 1.1 n.a. n.a.Wuzhou Int'l 1369 HK 0.67 0.2 0.2 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 209.2 0.8 n.a. n.a.Ying Li^ YINGLI SP 0.143 0.3 0.3 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 81.6 0.4 0.9 84.5Zhong An 672 HK 2.48 0.9 2.9 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 62.8 0.8 n.a. n.a.Ave ra ge 42 11 9 .9 9 .6 3 .4 4 .3 11 .3 11 .9 90 .5 0 .7 56 .4

Ave ra ge (Ove ra l l ) 22 21 10 .1 8 .5 4 .1 4 .9 13 .4 14 .9 82 .6 1 .0 35 .0~

1-Aug

^ Denominated in SGD for price

~ Simple average discount to NAV; Market cap weighted average NAV = 11% # Exclude Soho China

^^ FY16: 17F; FY17: FY18F; FY18: FY19F

Source: Thomson Reuters, *DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 12

PE valuations, 2008 to 2016 trough (based on earnings forecasts)

1-Aug Mkt 17F 18F PE (x)

Compa ny Na me CodePri c eHK$

Ca pUS$bn

PEx

PEx

Trough 2008

Trough 2009

Trough 2010

Trough 2011

Trough 2012

Trough 2013

Trough 2014

Trough 2015

Trough 2016

China Overseas* 688 HK 26.50 37.2 8.9 8.2 9.7 11.1 12.8 6.5 7.1 7.8 6.1 6.7 5.8CR Land* 1109 HK 24.80 22.0 9.0 7.8 15.9 13.1 14.4 7.2 10.1 11.9 7.1 8.2 7.0China Vanke 'H'* 2202 HK 22.75 37.6 8.9 7.6 n.a. n.a. n.a. n.a. n.a. n.a. 6.3 6.8 6.5Country Garden* 2007 HK 10.50 28.7 14.3 10.7 3.6 5.2 10.7 5.2 5.8 6.5 4.0 4.2 4.9Evergrande* 3333 HK 21.00 35.2 20.1 9.4 n.a. n.a. 3.8 2.9 3.3 4.2 3.4 4.3 6.4Longfor* 960 HK 19.40 14.6 9.8 7.8 n.a. 17.8 13.8 6.3 5.6 7.4 5.3 5.4 5.5Ave ra ge 11 .8 8 .6 9 .7 11 .8 11 .1 5 .6 6 .4 7 .6 5 .4 5 .9 6 .0

Agile Property* 3383 HK 9.03 4.5 8.2 6.7 1.5 4.2 7.6 2.5 3.4 3.6 2.2 2.7 3.0BJ Cap Land 'H' 2868 HK 4.06 2.6 6.5 4.9 1.6 3.1 5.1 1.9 2.0 3.3 2.6 3.1 3.5CIFI Holdings 884 HK 4.23 3.7 6.7 5.5 n.a. n.a. n.a. n.a. n.a. 3.8 3.2 2.7 2.8Greentown 3900 HK 10.32 2.9 10.2 9.7 1.9 2.3 6.3 2.0 1.5 3.3 2.3 3.1 3.4Guangzhou R&F 2777 HK 13.86 5.7 5.1 4.6 2.4 4.8 6.8 3.2 3.2 4.7 3.8 3.1 3.5Hopson Dev 754 HK 7.52 2.1 21.8 19.8 1.0 2.2 4.9 2.8 2.8 5.6 3.9 10.7 12.1Kaisa Group 1638 HK 2.99 2.0 n.a. n.a. n.a. n.a. 3.5 3.7 2.9 2.8 1.9 1.7 1.9KWG Property 1813 HK 5.68 2.3 4.3 3.8 2.1 2.8 7.8 3.0 2.8 3.6 2.8 3.1 3.0Logan Property 3380 HK 6.77 4.8 8.0 6.2 n.a. n.a. n.a. n.a. n.a. n.a. 3.5 3.6 3.7Shimao Property* 813 HK 14.90 6.5 8.2 7.5 3.7 4.2 8.5 3.6 3.9 6.4 4.3 3.3 3.1Sino-Ocean Land* 3377 HK 4.27 4.1 6.8 6.2 4.7 9.0 11.3 4.1 5.4 6.7 6.0 5.9 5.1Soho China* 410 HK 4.20 2.8 48.2 53.5 4.5 3.1 3.6 7.0 3.5 4.9 6.9 12.3 14.0Sunac China 1918 HK 20.10 10.0 24.0 11.4 n.a. n.a. 4.5 1.4 1.4 3.1 2.2 2.7 3.1Yanlord Land*^ YLLG SP 1.79 2.5 6.6 5.6 4.1 6.6 9.3 5.0 6.7 9.3 7.5 7.1 7.0Yuexiu Property* 123 HK 1.45 2.3 11.9 9.9 1.9 2.9 8.9 4.5 4.5 5.8 5.9 6.3 5.3Yuzhou Properties 1628 HK 4.46 2.2 5.9 4.8 n.a. 9.6 5.5 2.7 3.6 3.6 2.4 2.1 3.3Ave ra ge # 9 .6 7 .7 2 .8 4 .7 7 .2 3 .6 3 .6 4 .9 4 .0 4 .7 5 .0

BJ North Star 'H' 588 HK 3.19 1.4 n.a. n.a. 3.5 5.0 7.5 3.6 6.5 4.0 3.8 5.0 5.6C C Land 1224 HK 1.81 0.9 n.a. n.a. 18.4 n.a. n.a. 5.1 3.9 6.7 3.4 5.2 7.6Central China* 832 HK 2.32 0.7 5.9 5.2 1.3 1.5 3.9 2.8 2.8 3.5 2.6 2.5 2.3China SCE 1966 HK 3.81 1.7 6.7 4.4 n.a. n.a. 4.7 3.7 2.9 2.4 5.6 4.5 3.7China South City*^^ 1668 HK 1.70 1.7 18.1 15.6 n.a. 17.7 6.9 4.3 5.9 4.3 5.1 5.7 5.8COGO* 81 HK 4.45 1.3 7.3 5.5 n.a. n.a. n.a. 3.6 5.0 6.3 3.1 3.1 2.7First Sponsor*^ FSG SP 1.36 0.6 14.8 13.1 n.a. n.a. n.a. n.a. n.a. n.a. 29.9 13.4 13.6Glorious Property 845 HK 0.88 0.9 n.a. n.a. n.a. 12.9 6.4 2.8 2.8 4.8 4.4 3.6 17.3Greenland 337 HK 2.83 1.0 4.7 4.1 0.7 1.1 3.6 1.2 1.0 0.6 11.7 8.0 4.8Hydoo Int'l 1396 HK 0.91 0.5 n.a. n.a. n.a. n.a. n.a. n.a. n.a. 3.6 2.3 2.3 7.0Modern Land (China) 1107 HK 1.46 0.5 3.7 3.3 n.a. n.a. n.a. n.a. n.a. n.a. 2.4 2.4 2.0Poly (Hong Kong) 119 HK 4.04 1.9 33.7 23.6 10.0 3.8 14.9 4.2 4.9 5.2 3.9 5.4 13.0Powerlong 1238 HK 3.53 1.8 5.7 4.9 n.a. 4.7 5.3 1.5 1.6 3.6 2.8 3.2 2.7Renhe Commercia l 1387 HK 0.17 1.0 n.a. n.a. 10.5 5.7 5.4 3.2 2.7 4.7 7.7 7.7 7.7Shui On Land* 272 HK 1.94 2.0 9.2 17.9 1.7 3.4 9.4 5.6 6.5 9.1 10.6 5.8 6.5SRE Group 1207 HK 0.18 0.5 n.a. n.a. 1.0 1.5 2.0 2.3 0.9 1.1 1.1 1.1 1.1Sunshine 100 China 2608 HK 3.18 1.0 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 5.7 5.8 5.3Times Property 1233 HK 6.51 1.5 4.6 3.3 n.a. n.a. n.a. n.a. n.a. n.a. 2.5 2.2 1.9Wuzhou Int'l 1369 HK 0.67 0.2 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 7.3 5.2 22.3Ying Li^ YINGLI SP 0.14 0.3 n.a. n.a. n.a. 64.8 22.4 6.9 4.7 7.8 4.1 5.1 9.5Zhong An 672 HK 2.48 0.9 n.a. n.a. 1.7 2.9 7.8 3.0 9.9 5.3 8.3 8.3 8.3Ave ra ge 9 .9 9 .6 4 .3 9 .0 7 .4 3 .5 3 .8 4 .6 5 .9 5 .0 7 .0

Ave ra ge (Ove ra l l ) 10 .1 8 .5 4 .2 7 .5 7 .8 3 .8 4 .1 5 .1 5 .1 5 .0 6 .1 ^ Denominated in SGD for price # Exclude Soho China

^^ FY16: 17F; FY17: FY18F; FY18: FY19F

Source: Thomson Reuters, *DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 13

PE valuations, 2008 to 2016 peak (based on earnings forecasts)

1-Aug M kt 17F 18F PE (x)

Compa ny Na me CodePr ic eHK$

Ca pUS$bn

PEx

PEx

Pe a k 2008

Pe a k 2009

Pe a k 2010

Pe a k 2011

Pe a k 2012

Pe a k 2013

Pe a k 2014

Pe a k 2015

Pe a k 2016

China Overseas* 688 HK 26.50 37.2 8.9 8.2 22.7 25.0 17.0 12.1 12.4 11.2 8.5 9.9 8.7CR Land* 1109 HK 24.80 22.0 9.0 7.8 28.6 30.4 21.1 15.2 17.6 16.2 10.7 12.8 9.7China Vanke 'H'* 2202 HK 22.75 37.6 8.9 7.6 n.a. n.a. n.a. n.a. n.a. n.a. 9.0 11.8 11.3Country Garden* 2007 HK 10.50 28.7 14.3 10.7 19.8 20.3 16.7 11.6 9.2 10.0 6.4 7.3 8.8Evergrande* 3333 HK 21.00 35.2 20.1 9.4 n.a. n.a. 9.1 8.9 6.1 6.4 4.6 14.2 13.2Longfor* 960 HK 19.40 14.6 9.8 7.8 n.a. 24.4 21.7 14.2 11.9 10.4 6.9 8.7 8.2Ave ra ge 11 .8 8 .6 23 .7 25 .0 17 .1 12 .4 11 .4 10 .8 7 .7 10 .8 10 .0

Agile Property* 3383 HK 9.03 4.5 8.2 6.7 14.5 19.0 12.4 10.0 6.4 6.9 3.9 5.1 5.6BJ Cap Land 'H' 2868 HK 4.06 2.6 6.5 4.9 9.5 15.9 9.6 5.9 4.7 5.3 3.3 6.3 5.9CIFI Holdings 884 HK 4.23 3.7 6.7 5.5 n.a. n.a. n.a. n.a. n.a. 5.9 4.3 5.1 5.4Greentown 3900 HK 10.32 2.9 10.2 9.7 9.7 18.3 10.2 6.1 6.3 6.6 4.5 6.1 7.8Guangzhou R&F 2777 HK 13.86 5.7 5.1 4.6 16.6 17.8 10.5 8.0 7.4 8.1 4.8 4.8 6.0Hopson Dev 754 HK 7.52 2.1 21.8 19.8 9.6 10.3 7.5 6.4 16.0 13.7 16.1 24.6 22.4Kaisa Group 1638 HK 2.99 2.0 n.a. n.a. n.a. n.a. 8.4 10.0 6.9 5.9 3.9 2.3 8.9KWG Property 1813 HK 5.68 2.3 4.3 3.8 12.1 21.6 13.9 9.6 6.4 6.4 5.0 6.0 4.5Logan Property 3380 HK 6.77 4.8 8.0 6.2 n.a. n.a. n.a. n.a. n.a. n.a. 3.8 6.6 6.0Shimao Property* 813 HK 14.90 6.5 8.2 7.5 14.8 18.3 13.2 9.6 9.5 8.8 6.0 6.1 5.6Sino-Ocean Land* 3377 HK 4.27 4.1 6.8 6.2 13.2 24.8 15.7 10.3 12.1 11.4 7.8 9.9 8.0Soho China* 410 HK 4.20 2.8 48.2 53.5 11.4 8.5 6.1 13.7 4.8 6.0 9.1 18.9 46.7Sunac China 1918 HK 20.10 10.0 24.0 11.4 n.a. n.a. 5.8 3.5 5.5 4.9 5.1 6.3 12.4Yanlord Land*^ YLLG SP 1.79 2.5 6.6 5.6 14.5 19.8 14.5 10.5 15.0 14.4 9.8 12.7 9.4Yuexiu Property* 123 HK 1.45 2.3 11.9 9.9 11.0 25.5 15.7 11.0 9.1 9.5 7.9 11.1 10.6Yuzhou Properties 1628 HK 4.46 2.2 5.9 4.8 n.a. 11.7 9.9 5.8 6.5 6.5 3.3 5.2 5.2Ave ra ge # 9 .6 7 .7 13 .2 18 .4 11 .7 8 .8 8 .7 8 .4 6 .1 8 .1 8 .3

BJ North Star 'H' 588 HK 3.19 1.4 n.a. n.a. 20.6 18.0 12.7 10.5 8.9 7.0 8.2 13.0 10.9C C Land 1224 HK 1.81 0.9 n.a. n.a. n.a. n.a. n.a. 17.5 12.7 10.8 6.4 8.6 7.6Central China* 832 HK 2.32 0.7 5.9 5.2 10.8 9.4 6.6 5.6 6.3 5.2 3.8 4.4 3.9China SCE 1966 HK 3.81 1.7 6.7 4.4 n.a. n.a. 6.9 5.5 3.5 6.6 5.6 5.6 7.6China South City*^^ 1668 HK 1.70 1.7 18.1 15.6 n.a. 19.6 20.4 12.3 6.6 6.9 11.8 9.5 10.8COGO* 81 HK 4.45 1.3 7.3 5.5 n.a. n.a. n.a. 9.8 9.8 10.0 5.1 6.1 6.3First Sponsor*^ FSG SP 1.36 0.6 14.8 13.1 n.a. n.a. n.a. n.a. n.a. n.a. 31.3 13.9 13.6Glorious Property 845 HK 0.88 0.9 n.a. n.a. n.a. 17.7 10.8 7.3 6.3 11.0 9.1 41.0 19.0

Greenland 337 HK 2.83 1.0 4.7 4.1 9.3 11.9 6.7 3.2 7.6 44.8 28.2 21.6 8.6Hydoo Int'l 1396 HK 0.91 0.5 n.a. n.a. n.a. n.a. n.a. n.a. n.a. 5.5 5.9 7.8 7.0Modern Land (China) 1107 HK 1.46 0.5 3.7 3.3 n.a. n.a. n.a. n.a. n.a. n.a. 2.9 5.8 5.8Poly (Hong Kong) 119 HK 4.04 1.9 33.7 23.6 30.0 51.0 25.2 16.1 9.8 9.9 6.4 27.9Powerlong 1238 HK 3.53 1.8 5.7 4.9 n.a. 7.0 8.2 6.5 5.6 6.7 3.8 4.6 5.3Renhe Commercia l 1387 HK 0.17 1.0 n.a. n.a. 12.5 10.7 7.2 7.0 9.4 23.9 7.7 7.7 7.7Shui On Land* 272 HK 1.94 2.0 9.2 17.9 16.2 21.3 16.6 17.6 12.6 17.6 13.8 87.1 11.7SRE Group 1207 HK 0.18 0.5 n.a. n.a. 4.2 4.6 3.7 2.9 1.4 1.1 1.1 1.1 1.1Sunshine 100 China 2608 HK 3.18 1.0 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 6.7 7.4 8.0Times Property 1233 HK 6.51 1.5 4.6 3.3 n.a. n.a. n.a. n.a. n.a. n.a. 3.5 3.2 3.6Wuzhou Int'l 1369 HK 0.67 0.2 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 12.4 29.6 22.3Ying Li^ YINGLI SP 0.14 0.3 n.a. n.a. n.a. 196.2 331.2 42.9 13.0 16.1 14.7 16.4 15.3Zhong An 672 HK 2.48 0.9 n.a. n.a. 8.8 22.3 13.8 12.3 14.9 10.3 8.3 8.3 8.3Ave ra ge 9 .9 9 .6 12 .2 28 .1 32 .2 11 .9 8 .2 11 .1 8 .9 14 .5 8 .8

Ave ra ge (Ove ra l l ) 10 .1 8 .5 14 .0 23 .8 21 .6 10 .7 8 .8 10 .0 7 .7 11 .7 8 .8

^ Denominated in SGD for price

# Exclude Soho China

^^ FY16: 17F; FY17: FY18F; FY18: FY19F

Source: Thomson Reuters, *DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 14

PE valuations, 2008 to 2016 trough (based on reported earnings)

3-mth da i l yMkt tra d ing FY17F FY18F

Pric e Ca p va lue PE PE Avg Trough Trough Trough Trough Trough Trough Trough Trough TroughCompa ny Na me Code HK$ US$bn US$m x x PE (x) 2008 2009 2010 2011 2012 2013 2014 2015 2016China Overseas* 688 HK 26.5 37.2 68.3 8.9 8.2 9.6 9.9 10.0 8.9 5.3 5.3 6.4 5.1 6.1 5.6CR Land* 1109 HK 24.8 22.0 30.6 9.0 7.8 11.4 13.1 8.5 10.6 4.9 6.4 7.3 5.3 6.8 6.0China Vanke 'H'* 2202 HK 22.75 37.6 44.1 8.9 7.6 8.8 n.a. n.a. n.a. n.a. n.a. 6.5 6.3 8.6 6.7Country Garden* 2007 HK 10.5 28.7 48.0 14.3 10.7 13.9 11.3 9.2 6.3 4.3 5.2 5.8 4.4 4.9 4.4Evergrande* 3333 HK 21 35.2 124.7 20.1 9.4 5.3 n.a. 42.7 3.0 2.4 3.6 2.7 2.7 3.9 11.0Longfor* 960 HK 19.4 14.6 14.2 9.8 7.8 6.4 n.a. 11.8 7.2 4.5 5.1 5.8 4.7 4.9 5.0Ave ra ge 11.8 8 .6 11 .4 16 .4 7 .2 4 .3 5 .1 5 .7 4 .7 5 .9 6 .4

Agile Property* 3383 HK 9.03 4.5 14.3 8.2 6.7 6.9 1.2 4.2 3.6 2.9 3.5 4.2 2.6 8.6 5.1BJ Cap Land 'H' 2868 HK 4.06 2.6 1.5 6.5 4.9 7.0 2.3 2.4 3.6 2.3 2.0 2.8 2.5 2.7 3.3CIFI Holdings 884 HK 4.23 3.7 9.2 6.7 5.5 3.7 n.a. n.a. n.a. n.a. 2.4 2.9 3.6 3.7 2.8Greentown 3900 HK 10.32 2.9 7.5 10.2 9.7 10.0 4.2 2.8 6.6 1.7 0.9 3.9 6.7 18.8 6.2Guangzhou R&F 2777 HK 13.86 5.7 14.6 5.1 4.6 6.9 3.3 6.3 6.6 3.7 2.7 3.4 4.0 3.3 3.1Hopson Dev 754 HK 7.52 2.1 0.6 21.8 19.8 6.0 1.1 0.8 2.3 4.6 2.1 3.9 5.1 7.0 3.7Kaisa Group 1638 HK 2.99 2.0 6.5 n.a. n.a. 3.4 n.a. 16.2 1.6 2.8 2.5 2.2 n.a. n.a. (11.3)KWG Property 1813 HK 5.68 2.3 9.2 4.3 3.8 6.7 5.8 3.5 6.0 2.2 2.0 2.6 2.2 3.2 3.1Logan Property 3380 HK 6.77 4.8 9.6 8.0 6.2 3.7 n.a. n.a. n.a. n.a. n.a. 3.6 3.6 3.6 2.2Shimao Property* 813 HK 14.90 6.5 9.9 8.2 7.5 9.3 11.4 3.1 6.6 2.7 3.0 4.9 4.8 4.9 4.6Sino-Ocean Land* 3377 HK 4.27 4.1 4.8 6.8 6.2 10.0 4.5 8.3 9.5 5.2 4.1 5.1 5.4 11.6 5.3Soho China* 410 HK 4.2 2.8 6.9 48.2 53.5 15.5 n.a. n.a. n.a. n.a. n.a. n.a. n.a. 25.3 15.0Sunac China 1918 HK 20.1 10.0 77.2 24.0 11.4 4.6 n.a. n.a. n.a. 1.3 1.5 3.8 3.1 3.6 5.3Yanlord Land*^ YLLG SP 1.785 2.5 3.3 6.6 5.6 9.2 4.1 4.2 7.9 4.7 4.9 7.3 6.8 5.8 3.4Yuexiu Property* 123 HK 1.45 2.3 5.8 11.9 9.9 8.0 3.4 (4.6) 8.0 1.1 2.5 4.2 4.9 12.6 6.4Yuzhou Properties 1628 HK 4.46 2.2 4.8 5.9 4.8 4.0 n.a. 2.6 3.6 2.6 4.2 2.8 3.4 3.0 3.0Ave ra ge # 9.6 7 .7 4 .3 4 .7 6 .0 3 .0 2 .8 3 .9 4 .1 6 .4 3 .5

BJ North Star 'H' 588 HK 3.19 1.4 0.8 n.a. n.a. 7.9 1.6 1.9 4.6 2.3 3.1 5.4 5.8 7.8 7.3C C Land 1224 HK 1.81 0.9 0.3 n.a. n.a. 24.7 n.a. n.a. n.a. n.a. n.a. n.a. n.a. 3.2 (14.2)Central China* 832 HK 2.32 0.7 0.7 5.9 5.2 5.2 1.1 2.4 5.1 3.7 3.3 3.8 3.9 3.7 6.6China SCE 1966 HK 3.81 1.7 5.5 6.7 4.4 4.8 n.a. n.a. 4.0 4.1 5.1 4.4 4.5 4.6 2.2China South City*^^ 1668 HK 1.7 1.7 4.4 18.1 15.6 6.1 n.a. n.a. n.a. 3.6 2.9 3.1 4.3 3.6 2.5COGO* 81 HK 4.45 1.3 3.6 7.3 5.5 7.8 32.9 (3.5) 2.9 2.9 4.0 5.3 6.8 5.9 5.0First Sponsor*^ FSG SP 1.36 0.6 0.1 14.8 13.1 2.4 n.a. n.a. n.a. n.a. n.a. n.a. 13.8 8.8 8.1Glorious Property 845 HK 0.88 0.9 0.4 n.a. n.a. 4.5 n.a. 6.7 3.7 2.9 5.7 23.6 (2.2) (1.4) (1.1)Greenland 337 HK 2.83 1.0 1.8 4.7 4.1 9.5 2.4 1.0 2.9 1.2 (1.1) 71.8 22.8 13.0 4.0Hydoo Int'l 1396 HK 0.91 0.5 0.3 n.a. n.a. 11.9 n.a. n.a. n.a. n.a. n.a. n.a. 10.1 5.1 5.0Modern Land (China) 1107 HK 1.46 0.5 0.2 3.7 3.3 3.5 n.a. n.a. n.a. n.a. n.a. 2.5 2.9 3.1 2.4Poly (Hong Kong) 119 HK 4.04 1.9 5.3 33.7 23.6 12.1 11.4 5.0 11.5 2.9 4.2 5.2 11.1 (2.5) 85.5Powerlong 1238 HK 3.53 1.8 1.7 5.7 4.9 2.6 n.a. 2.6 2.8 1.1 1.8 3.2 2.4 1.8 1.8Renhe Commercia l 1387 HK 0.172 1.0 0.2 n.a. n.a. n.a. 7.8 4.8 6.0 2.5 5.2 (3.6) (3.2) (2.3) (0.5)Shui On Land* 272 HK 1.94 2.0 2.9 9.2 17.9 8.9 1.6 2.1 4.2 1.9 5.1 5.9 6.5 13.1 10.4SRE Group 1207 HK 0.182 0.5 0.1 n.a. n.a. 7.0 3.2 1.5 3.6 2.7 3.8 6.7 (10.6) (0.6) (12.9)Sunshine 100 China 2608 HK 3.18 1.0 0.2 n.a. n.a. 12.9 n.a. n.a. n.a. n.a. n.a. n.a. 5.7 8.3 30.8Times Property 1233 HK 6.51 1.5 2.9 4.6 3.3 2.9 n.a. n.a. n.a. n.a. n.a. 3.6 3.2 2.5 2.0Wuzhou Int'l 1369 HK 0.67 0.2 0.2 n.a. n.a. 10.3 n.a. n.a. n.a. n.a. n.a. 3.7 18.4 (5.7) 32.1Ying Li^ YINGLI SP 0.143 0.3 0.3 n.a. n.a. n.a. 1.8 32.6 18.6 7.8 6.8 18.4 9.5 12.1 18.4Zhong An 672 HK 2.48 0.9 2.9 n.a. n.a. 10.8 4.2 3.4 8.6 5.5 4.2 5.1 5.2 3.6 10.1Ave ra ge 9 .9 9 .6 5 .7 4 .7 6 .1 3 .2 4 .0 9 .2 6 .2 4 .3 9 .0

Ave ra ge (Ove ra l l ) 10 .1 8 .5 5 .7 6 .4 6 .2 3 .3 3 .7 6 .6 5 .3 5 .3 6 .7HSI Inde x HSI 9 .1 9 .0 10 .3 7 .8 8 .8 9 .4 9 .3 10 .4 8 .9

1-Aug

^ Denominated in SGD for price

# Exclude Soho China

^^ FY16: 17F; FY17: FY18F; FY18: FY19F

Source: Thomson Reuters, *DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 15

PE valuations, 2008 to 2016 peak (based on reported earnings)

3-mth da i l yM kt tra d ing FY17F FY18F

Pr i c e Ca p va lue PE PE Avg Pe a k Pe a k Pe a k Pe a k Pe a k Pe a k Pe a k Pe a k Pe a kCompa ny Na me Code HK$ US$bn US$m x x PE (x) 2008 2009 2010 2011 2012 2013 2014 2015 2016China Overseas* 688 HK 26.5 37.2 68.3 8.9 8.2 9.6 25.2 20.6 11.6 9.4 10.1 8.7 6.9 9.3 7.6CR Land* 1109 HK 24.8 22.0 30.6 9.0 7.8 11.4 35.6 21.6 14.5 10.2 11.5 9.3 7.8 10.9 8.4China Vanke 'H'* 2202 HK 22.75 37.6 44.1 8.9 7.6 8.8 n.a. n.a. n.a. n.a. n.a. 9.9 10.5 12.5 10.9Country Garden* 2007 HK 10.5 28.7 48.0 14.3 10.7 13.9 86.8 25.3 10.6 9.0 8.2 9.5 7.2 8.6 7.1Evergrande* 3333 HK 21 35.2 124.7 20.1 9.4 5.3 n.a. 52.1 7.0 6.6 6.3 4.5 3.9 9.9 15.9Longfor* 960 HK 19.4 14.6 14.2 9.8 7.8 6.4 n.a. 14.8 11.7 9.2 10.2 8.7 6.3 8.3 7.0Ave ra ge 11.8 8 .6 49 .2 26 .9 11 .1 8 .9 9 .3 8 .4 7 .1 9 .9 9 .5

Agile Property* 3383 HK 9.03 4.5 14.3 8.2 6.7 6.9 7.9 20.9 6.1 9.6 5.9 7.2 5.7 17.3 7.3BJ Cap Land 'H' 2868 HK 4.06 2.6 1.5 6.5 4.9 7.0 21.7 13.2 6.3 5.4 4.7 4.0 3.3 7.1 4.6CIFI Holdings 884 HK 4.23 3.7 9.2 6.7 5.5 3.7 n.a. n.a. n.a. n.a. 2.6 4.6 4.7 7.2 5.5Greentown 3900 HK 10.32 2.9 7.5 10.2 9.7 10.0 30.5 18.9 10.7 5.2 4.3 6.2 12.7 42.0 9.5Guangzhou R&F 2777 HK 13.86 5.7 14.6 5.1 4.6 6.9 28.6 20.6 10.2 8.3 6.0 5.2 6.0 5.3 5.7Hopson Dev 754 HK 7.52 2.1 0.6 21.8 19.8 6.0 16.2 4.1 3.9 11.7 7.3 8.2 7.1 14.0 5.0Kaisa Group 1638 HK 2.99 2.0 6.5 n.a. n.a. 3.4 n.a. 20.2 3.2 7.0 4.8 3.9 n.a. n.a. (11.3)KWG Property 1813 HK 5.68 2.3 9.2 4.3 3.8 6.7 n.a. 18.2 11.0 6.4 4.5 4.5 4.3 5.8 4.2Logan Property 3380 HK 6.77 4.8 9.6 8.0 6.2 5.7 n.a. n.a. n.a. n.a. n.a. 3.7 4.5 5.5 3.8Shimao Property* 813 HK 14.90 6.5 9.9 8.2 7.5 9.3 63.7 14.2 9.6 6.7 7.4 7.6 6.8 10.1 6.8Sino-Ocean Land* 3377 HK 4.27 4.1 4.8 6.8 6.2 10.0 25.5 22.5 16.2 12.8 8.5 8.3 7.3 20.1 8.8Soho China* 410 HK 4.2 2.8 6.9 48.2 53.5 15.5 n.a. 6.7 7.9 8.0 2.4 3.8 7.2 52.1 23.7Sunac China 1918 HK 20.1 10.0 77.2 24.0 11.4 4.6 n.a. n.a. n.a. 3.2 5.4 6.0 6.9 9.8 8.2Yanlord Land*^ YLLG SP 1.785 2.5 3.3 6.6 5.6 9.2 27.4 17.6 11.0 11.6 8.0 10.4 8.1 8.3 5.1Yuexiu Property* 123 HK 1.45 2.3 5.8 11.9 9.9 8.0 20.2 n.a. 12.0 2.5 5.7 6.8 6.5 22.2 9.4Yuzhou Properties 1628 HK 4.46 2.2 4.8 5.9 4.8 4.0 n.a. 3.2 4.7 4.6 7.1 4.1 4.5 5.0 5.5Ave ra ge # 9.6 7 .7 26 .9 16 .3 9 .3 7 .4 6 .1 6 .1 6 .2 12 .5 5 .8

BJ North Star 'H' 588 HK 3.19 1.4 0.8 n.a. n.a. 7.9 12.7 6.1 6.9 5.2 5.7 7.7 9.8 15.5 10.2C C Land 1224 HK 1.81 0.9 0.3 n.a. n.a. 24.7 n.a. n.a. 36.3 26.6 13.5 15.9 4.7 5.8 (18.3)Central China* 832 HK 2.32 0.7 0.7 5.9 5.2 5.2 6.7 11.0 7.4 6.6 6.3 6.1 5.9 7.1 9.9China SCE 1966 HK 3.81 1.7 5.5 6.7 4.4 4.8 n.a. n.a. 5.9 6.1 6.3 5.8 5.9 6.2 3.8China South City*^^ 1668 HK 1.7 1.7 4.4 18.1 15.6 6.1 n.a. n.a. n.a. 5.8 4.3 7.0 9.7 8.6 3.5COGO* 81 HK 4.45 1.3 3.6 7.3 5.5 7.8 188.9 n.a. 4.9 8.0 8.9 9.2 13.3 14.1 7.3First Sponsor*^ FSG SP 1.36 0.6 0.1 14.8 13.1 2.4 n.a. n.a. n.a. n.a. n.a. n.a. 16.6 9.7 9.2Glorious Property 845 HK 0.88 0.9 0.4 n.a. n.a. 4.5 n.a. 8.8 6.3 8.5 10.1 39.2 (3.8) (2.3) (2.2)Greenland 337 HK 2.83 1.0 1.8 4.7 4.1 9.5 39.3 7.2 4.9 4.2 (1.8) 364.4 48.0 36.7 7.2Hydoo Int'l 1396 HK 0.91 0.5 0.3 n.a. n.a. 11.9 n.a. n.a. n.a. n.a. n.a. n.a. 28.2 12.4 11.5Modern Land (China) 1107 HK 1.46 0.5 0.2 3.7 3.3 3.5 n.a. n.a. n.a. n.a. n.a. 3.4 3.7 6.5 6.2Poly (Hong Kong) 119 HK 4.04 1.9 5.3 33.7 23.6 12.1 59.7 40.1 18.6 10.8 8.3 9.1 16.4 (6.8) 121.8Powerlong 1238 HK 3.53 1.8 1.7 5.7 4.9 2.6 n.a. 3.0 3.7 3.2 3.1 5.4 4.0 3.5 3.7Renhe Commercia l 1387 HK 0.172 1.0 0.2 n.a. n.a. n.a. 9.3 9.1 9.4 5.7 17.4 (8.4) (5.5) (7.3) (0.9)Shui On Land* 272 HK 1.94 2.0 2.9 9.2 17.9 8.9 11.7 7.8 6.3 4.7 9.1 10.4 9.6 24.7 14.6SRE Group 1207 HK 0.182 0.5 0.1 n.a. n.a. 7.0 20.7 4.7 4.8 6.7 6.8 13.3 (13.9) (2.7) (24.3)Sunshine 100 China 2608 HK 3.18 1.0 0.2 n.a. n.a. 12.9 n.a. n.a. n.a. n.a. n.a. n.a. 7.9 13.0 38.5Times Property 1233 HK 6.51 1.5 2.9 4.6 3.3 2.9 n.a. n.a. n.a. n.a. n.a. 3.7 3.9 3.8 3.1Wuzhou Int'l 1369 HK 0.67 0.2 0.2 n.a. n.a. 10.3 n.a. n.a. n.a. n.a. n.a. 4.2 32.2 (15.0) 35.8Ying Li^ YINGLI SP 0.143 0.3 0.3 n.a. n.a. n.a. 4.8 112.2 33.8 17.6 11.5 26.6 17.7 27.1 26.6Zhong An 672 HK 2.48 0.9 2.9 n.a. n.a. 10.8 29.4 15.4 12.4 10.4 7.2 9.1 16.6 6.1 13.2Ave ra ge 9.9 9 .6 33 .1 19 .8 11 .2 8 .4 7 .8 26 .5 10 .8 8 .0 12 .2

Ave ra ge (Ove ra l l ) 10 .1 8 .5 32 .4 19 .5 10 .5 8 .1 7 .3 16 .1 8 .7 9 .8 9 .5HSI Inde x HSI 23 .1 18 .2 13 .6 11 .7 11 .0 11 .3 11 .1 14 .3 11 .7

1 -Aug

^ Denominated in SGD for price # Exclude Soho China

^^ FY16: 17F; FY17: FY18F; FY18: FY19F

Source: Thomson Reuters, *DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 16

Share price performance

Price Pe rformance 20071-wk 2-wk 1-mth 2-mth 3-mth 4-mth 5-mth 6-mth YTD 1-yr 2012 2013 2014 2015 2016 high

% % % % % % % % % % % % % % % %Tie r 1 playe rsChina Overseas 688 HK 3.5 3.3 16.0 13.0 17.3 19.4 11.8 14.2 29.0 2.1 78.0 (5.6) 5.7 21.5 (24.4) 41.2CR Land 1109 HK 3.5 1.8 9.0 8.1 14.8 18.1 18.7 26.5 42.2 26.9 69.1 (8.9) 6.4 14.2 (22.8) 19.8China Vanke 'H' 2202 HK 2.9 (1.9) 2.9 11.5 15.2 8.3 15.7 14.9 28.5 26.7 n.a. n.a. n.a. 32.4 (22.7) n.a.Country Garden 2007 HK 10.5 15.5 16.0 12.5 41.9 50.2 85.5 136.5 141.9 227.1 46.4 15.3 (32.8) 2.6 36.5 (18.7)Evergrande 3333 HK 18.6 33.2 49.8 46.6 152.7 191.7 259.6 283.9 334.8 327.7 32.0 (30.4) 6.1 117.2 (29.2) n.a.Longfor Properties 960 HK 3.1 7.1 15.6 21.3 43.9 51.8 55.9 72.3 97.2 79.6 72.9 (28.6) (7.8) 15.7 (14.9) n.a.Ave rage 7.0 9.8 18.2 18.8 47.6 56.6 74.5 91.4 112.3 115.0 59.7 (11.6) (4.5) 33.9 (12.9) 14.1

Tie r 2 playe rsAgile Property 3383 HK 5.0 12.3 26.3 25.1 29.7 34.2 76.0 117.1 128.6 100.7 56.6 (23.8) (46.9) (2.0) (8.6) (54.1)BJ Cap. Land 2868 HK (1.7) (0.2) 9.4 10.9 7.4 15.7 20.8 31.8 39.5 37.2 110.5 (18.0) 11.4 20.7 (18.0) (45.6)CIFI Holdings 884 HK 11.3 14.6 21.9 38.7 50.5 40.1 62.7 88.8 102.4 110.4 n.a. 17.1 (6.1) 12.3 20.8 n.a.Greentown 3900 HK 3.8 5.2 20.0 26.6 38.0 39.5 47.2 61.8 64.3 83.0 321.4 (16.6) (35.0) 0.0 (18.4) (47.2)GZ R&F 2777 HK 2.7 8.8 14.2 9.5 5.8 14.2 28.6 38.3 47.8 19.3 110.1 (12.1) (16.3) 0.6 (1.8) (68.1)Hopson Dev 754 HK (1.1) (2.2) 2.5 2.3 1.3 5.2 8.0 7.9 8.8 5.2 207.2 (24.6) (24.0) 8.7 (10.5) (75.9)Kaisa Group 1638 HK (7.7) (8.6) 21.1 13.7 28.3 8.7 91.7 91.7 91.7 91.7 79.1 4.2 (36.4) (1.9) 0.0 n.a.KWG 1813 HK 1.2 3.6 8.6 (7.9) (3.4) 0.9 18.8 27.6 29.1 19.6 122.2 (26.1) 33.5 13.1 (17.8) (55.2)Logan Property 3380 HK 1.3 6.4 31.5 40.5 51.8 65.1 100.9 108.3 131.1 126.4 n.a. n.a. 10.0 9.1 11.4 n.a.Shimao Property 813 HK 0.7 6.7 11.5 12.0 19.2 20.7 33.5 42.4 46.9 46.1 120.5 21.9 (2.7) (20.5) (26.4) (48.7)Sino-Ocean 3377 HK 2.9 8.4 11.8 10.3 12.4 17.0 9.5 26.0 23.1 28.6 60.8 (12.1) (13.4) 12.7 (30.2) (71.5)SOHO China 410 HK (0.2) 1.9 9.1 8.5 (0.9) 1.0 4.2 6.9 9.9 11.4 20.3 7.4 (18.0) (31.4) 1.6 (64.8)Sunac China 1918 HK 8.1 26.1 23.2 56.8 98.2 99.4 149.1 191.3 211.6 313.6 272.7 (22.5) 69.7 (24.0) 7.5 n.a.Yanlord Land YLLG SP (1.1) 2.0 1.7 (4.0) (4.3) (1.7) 19.0 27.0 35.2 50.0 59.2 (19.4) (15.1) (3.4) 31.3 (57.7)Yuexiu Property 123 HK 0.0 2.8 9.0 6.6 9.8 9.8 15.1 26.1 36.8 43.6 118.8 (22.0) (16.8) (10.1) (20.9) (49.7)Yuzhou Properties 1628 HK (0.9) 1.6 (3.5) 12.6 25.6 37.7 65.2 72.9 65.2 92.2 37.1 2.9 1.0 7.7 28.6 n.a.Ave rage 1.6 5.4 12.9 16.7 22.9 25.2 44.8 57.6 64.3 69.7 119.3 (9.1) (8.1) 4.1 (4.8) (56.6)

Tie r 3 playe rsBJ North Star 588 HK 3.2 1.3 (3.3) 0.0 6.0 10.8 13.5 30.2 34.0 31.8 82.6 (16.7) 41.1 3.6 (7.0) (59.6)C C Land 1224 HK 4.6 2.3 1.7 (6.7) (9.5) (12.1) (22.5) (23.2) (18.8) (10.4) 88.9 (28.3) (30.7) 79.2 (6.6) (89.0)Central China 832 HK (2.9) 10.0 31.1 28.2 22.1 20.8 30.3 35.7 37.3 52.6 76.8 (12.8) (26.8) (7.4) 4.3 n.a.China SCE Property 1966 HK 1.6 3.3 7.3 27.9 29.6 30.0 36.6 53.0 63.5 128.1 20.2 16.2 (12.4) 8.0 33.1 n.a.China South City 1668 HK 0.0 8.3 17.2 15.6 11.8 6.3 5.6 3.0 4.9 5.6 17.0 88.0 60.9 (50.6) (7.4) n.a.COGO 81 HK 0.5 0.9 6.7 7.7 11.5 8.5 56.1 66.7 75.9 98.7 105.6 (20.7) (46.7) (16.8) (22.9) (2.0)First Sponsor FSG SP 0.0 (0.7) 3.0 2.3 2.3 0.0 3.0 1.9 1.9 7.1 n.a. n.a. n.a. 0.8 6.0 n.a.Glorious Property 845 HK (7.4) 2.3 3.5 1.1 (3.3) 1.1 (2.2) 15.8 15.8 18.9 7.4 14.4 (28.1) (25.0) (15.6) n.a.Greenland 337 HK (0.7) (4.4) 5.6 1.4 12.7 35.4 28.6 63.6 46.6 20.9 53.5 90.4 (18.3) (1.9) (36.1) (62.1)Hydoo Int'l 1396 HK 2.2 2.2 0.0 8.3 16.7 35.8 19.7 37.9 56.9 1.1 n.a. n.a. (13.5) (44.0) (46.3) n.a.Modern Land (China) 1107 HK 1.4 9.8 15.9 20.7 15.0 10.6 18.7 25.9 41.7 44.6 n.a. n.a. 1.6 98.4 (53.2) n.a.Poly HK 119 HK 7.4 12.2 17.8 21.3 26.6 24.7 23.9 32.5 57.2 93.3 79.8 (31.7) (22.9) (20.7) 1.6 (64.7)Powerlong 1238 HK (1.9) 0.0 5.1 4.7 (3.6) 19.7 33.7 53.5 54.8 97.2 58.7 0.6 (34.3) 50.5 39.0 n.a.Renhe Commercial 1387 HK (1.1) 6.8 (1.7) (9.9) (13.6) (11.8) (18.9) (14.0) (13.6) (13.6) (8.9) (38.9) (28.1) 5.9 (44.7) n.a.Shui On Land 272 HK 1.0 7.2 2.6 1.0 12.1 10.9 12.8 19.8 16.2 (7.2) 58.9 (31.1) (23.1) 16.4 (21.6) (80.3)SRE Group 1207 HK 0.0 1.7 1.1 (1.6) (3.2) (6.7) (9.0) (8.1) (8.5) (21.2) 24.2 (32.9) (20.8) 73.8 (45.5) (94.7)Sunshine 100 China 2608 HK (0.6) (2.2) 9.7 (3.3) 5.3 (2.8) (7.8) 7.4 (14.1) (3.3) n.a. n.a. n.a. 21.7 4.8 n.a.Times Property 1233 HK 1.7 10.3 33.4 29.2 20.1 18.4 37.9 62.3 71.8 110.0 n.a. n.a. (5.7) (18.2) 40.4 n.a.Wuzhou Int'l 1369 HK (10.7) (16.3) (18.3) (10.7) (15.2) (14.1) (14.1) (14.1) (14.1) (13.0) n.a. n.a. 14.0 (44.9) (3.7) n.a.Ying Li YINGLI SP 2.1 0.7 8.3 6.7 2.1 (7.7) (11.2) (12.8) (4.0) 5.9 45.1 6.8 (38.0) (32.2) (10.2) (88.1)Zhong An 672 HK 0.0 21.6 49.4 254.3 281.5 281.5 281.5 306.6 287.5 259.4 7.5 26.3 (20.8) (28.9) (21.0) (57.1)Ave rage 0.5 3.9 9.6 17.3 18.3 20.5 23.9 34.8 38.2 43.6 48.1 0.8 (13.5) 2.3 (7.9) (63.1)

Ave rage (Ove ra l l ) 1.7 5.2 11.9 17.3 23.7 26.8 38.0 50.4 57.2 62.3 78.8 (4.9) (10.4) 6.9 (7.4) (51.8)

Hang Seng Index 2.6 3.8 6.9 6.7 11.9 14.2 15.8 18.1 25.2 24.5 22.9 2.9 1.3 (7.2) 0.4 (13.0)MSCI China 2.1 3.5 8.4 9.3 15.9 19.1 21.5 26.1 34.7 35.5 18.7 0.4 4.7 (10.1) (1.4) (24.2)

Source: Thomson Reuters

China / Hong Kong

China Property Weekly Digest

Page 17

Historical valuations

1 -Au gCo mp a n y n a me

Co d e Pr i c eHK$

Cu rre n t H i s t a vg

+ 1 s .d .

- 1 s .d .

Cu rre n t(FY1 7 )

H i s t a vg

+ 1 s .d .

- 1 s .d . Cu rre nt

H i s t a vg

+ 1 s .d .

- 1 s .d .

Agile Property 3383 HK 9.03 44.7 54.8 33.7 75.9 8.2 6.9 8.9 4.8 0.7 1.2 2.1 0.4C C Land 1224 HK 1.81 34.6 56.2 35.1 77.4 n.a . 24.7 189.8 (140.5) 0.4 0.8 3.0 (1.4)Centra l China 832 HK 2.32 53.3 67.3 60.5 74.1 5.9 5.2 6.5 3.9 0.8 0.7 0.9 0.5China Overseas 688 HK 26.50 (1.8) 13.8 (2.5) 30.0 8.9 9.6 14.4 4.9 1.2 1.7 2.5 1.0China Vanke-H 2202 HK 22.75 0.9 13.7 5.7 21.7 8.9 5.2 6.5 3.9 1.9 0.7 0.9 0.5China Vanke-A* 000002 CH 23.42 (13.2) (10.4) (33.5) 12.6 10.5 9.6 14.4 4.9 2.3 1.7 2.5 1.0COGO 81 HK 4.45 38.1 52.7 34.9 70.5 7.3 7.8 18.5 (2.9) 0.8 0.8 1.3 0.2Country Garden 2007 HK 10.50 (12.4) 29.4 9.1 49.8 14.3 13.9 31.5 (3.6) 2.9 1.9 3.4 0.3CR Land 1109 HK 24.80 11.5 29.1 15.1 43.0 9.0 11.4 17.9 4.8 1.5 1.3 1.7 0.8China Eve rgrande 3333 HK 21.00 (14.8) 49.4 22.3 76.5 20.1 5.3 7.8 2.9 5.6 1.3 1.7 0.8First Sponsor FSG SP 1.36 66.8 n.a . n.a . n.a . 14.8 2.4 2.7 2.1 0.4 0.4 2.2 (1.4)Longfor 960 HK 19.40 14.4 38.3 30.7 45.9 9.8 6.4 7.5 5.4 1.6 1.3 1.8 0.9Shimao Property 813 HK 14.90 47.8 42.6 25.2 60.0 8.2 9.3 18.1 0.5 0.8 1.2 1.8 0.6Shui On Land 272 HK 1.94 62.1 57.6 47.7 67.5 9.2 8.9 12.4 5.4 0.4 0.6 1.1 0.2Sino-Ocean Land 3377 HK 4.27 44.5 41.3 21.3 61.4 6.8 10.0 14.9 5.0 0.6 0.8 1.2 0.4SOHO China 410 HK 4.20 41.4 38.4 18.3 58.6 48.2 15.5 31.8 (0.9) 0.5 0.8 1.2 0.5Greenland 337 HK 2.83 50.6 44.3 15.2 73.5 4.7 9.5 18.4 0.6 0.8 0.9 1.5 0.4Yanlord Land^ YLLG SP 1.79 43.3 41.9 25.8 58.0 6.6 9.2 14.5 4.0 0.8 1.1 1.9 0.3Yuexiu Property 123 HK 1.45 47.0 57.7 51.7 63.8 11.9 8.0 12.9 3.2 0.5 0.6 0.8 0.4Se c to r a ve ra g e 3 5 .0 * * 4 5 .9 ~ 3 9 .1 ~ 5 2 .8 ~ 1 0 .1 6 .5 ~ 7 .6 ~ 5 .5 ~ 1 .0 0 .8 ~ 0 .9 ~ 0 .6 ~

NAV d i s c o u n t / (p re miu m) (% ) PE (x) PB (x)

* Share price denominated in RMB

^ Share price denominated in SGD

** Exclude Soho China

~ 2010-YTD

Source: Thomson Reuters, DBS Vickers

China / Hong Kong

China Property Weekly Digest

Page 18

DBSVHK recommendations are based an Absolute Total Return* Rating system, defined as follows:

STRONG BUY (>20% total return over the next 3 months, with identifiable share price catalysts within this time frame)

BUY (>15% total return over the next 12 months for small caps, >10% for large caps)

HOLD (-10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps)

FULLY VALUED (negative total return i.e. > -10% over the next 12 months)

SELL (negative total return of > -20% over the next 3 months, with identifiable catalysts within this time frame)

* Share price appreciation + dividends Completed Date: 2 Aug 2017 08:45:36 (HKT) Dissemination Date: 2 Aug 2017 10:09:32 (HKT)

Sources for all charts and tables are DBS Vickers unless otherwise specified.

GENERAL DISCLOSURE/DISCLAIMER This report is prepared by DBS Vickers (Hong Kong) Limited (“DBSV HK”). This report is solely intended for the clients of DBS Bank Ltd., DBS Bank (Hong Kong) Limited (DBS HK), DBSV HK, and DBS Vickers Securities (Singapore) Pte Ltd. (“DBSVS”), its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBSV HK. The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd., DBS HK, DBSV HK, DBSVS, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies. Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report. This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned schedule or frequency for updating research publication relating to any issuer. The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that: (a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and (b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk

assessments stated therein. Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets. Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies) mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the commodity referred to in this report. DBSVUSA, a US-registered broker-dealer, does not have its own investment banking or research department, has not participated in any public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months and does not engage in market-making.

China / Hong Kong

China Property Weekly Digest

Page 19

ANALYST CERTIFICATION The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The research analyst (s) primarily responsible for the content of this research report, in part or in whole, certifies that he or his associate1 does not serve as an officer of the issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the management company of the real estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of the entity who is responsible for the management of the issuer or the new listing applicant) and the research analyst(s) primarily responsible for the content of this research report or his associate does not have financial interests2 in relation to an issuer or a new listing applicant that the analyst reviews. DBS Group has procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of research reports. The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment banking function of the DBS Group and procedures are in place to ensure that confidential information held by either the research or investment banking function is handled appropriately. There is no direct link of DBS Group's compensation to any specific investment banking function of the DBS Group. COMPANY-SPECIFIC / REGULATORY DISCLOSURES 1. DBS Bank Ltd, DBS HK, DBSVS, DBSV HK or their subsidiaries and/or other affiliates have proprietary positions in China Overseas Land

& Investment Limited (688 HK), China Resources Land Limited (1109 HK), China Vanke Company Limited 'H' (2202 HK) and Sino-Ocean Land Holdings Limited (3377 HK) recommended in this report as of 28 Jul 2017. DBS Bank Ltd, DBS HK, DBSVS, DBSV HK or their subsidiaries and/or other affiliates have proprietary positions in Yanlord Land Group Limited (YLLG SP) and Ying Li International Real Estate Limited (YINGLI SP) recommended in this report as of 30 Jun 2017.

2. Neither DBS Bank Ltd, DBS HK nor DBSV HK market makes in equity securities of the issuer(s) or company(ies) mentioned in this Research Report.

3. Compensation for investment banking services: DBS Bank Ltd, DBS HK, DBSVS, DBSV HK, their subsidiaries and/or other affiliates of DBSVUSA have received compensation, within the past 12 months for investment banking services from Yanlord Land Group Limited (YLLG SP), Yuexiu Property Company Limited (123 HK), Central China Real Estate Limited (832 HK), China South City Holdings Limited (1668 HK) and China Overseas Grand Oceans Group (81 HK) as of 30 Jun 2017.

4. DBS Bank Ltd, DBS HK, DBSVS, DBSV HK, their subsidiaries and/or other affiliates of DBSVUSA have managed or co-managed a public offering of securities for Yanlord Land Group Limited (YLLG SP), Yuexiu Property Company Limited (123 HK), China South City Holdings Limited (1668 HK) and China Overseas Grand Oceans Group (81 HK) in the past 12 months, as of 30 Jun 2017. DBSVUSA does not have its own investment banking or research department, nor has it participated in any public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months. Any US persons wishing to obtain further information, including any clarification on disclosures in this disclaimer, or to effect a transaction in any security discussed in this document should contact DBSVUSA exclusively.

5. Disclosure of previous investment recommendation produced: DBS Bank Ltd, DBSVS, DBSVHK, their subsidiaries and/or other affiliates of DBSVUSA may have published other investment recommendations in respect of the same securities / instruments recommended in this research report during the preceding 12 months. Please contact the primary analyst listed in the first page of this report to view previous investment recommendations published by DBS Bank Ltd, DBSVHK, their subsidiaries and/or other affiliates of DBSVUSA in the preceding 12 months.

1 An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of

which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

2 Financial interest is defined as interests that are commonly known financial interest, such as investment in the securities in respect of an issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or analysis. This term does not include commercial lending conducted at arm's length, or investments in any collective investment scheme other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer or a new listing applicant.

China / Hong Kong

China Property Weekly Digest

Page 20

RESTRICTIONS ON DISTRIBUTION

General This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Australia This report is being distributed in Australia by DBS Bank Ltd. (“DBS”) or DBS Vickers Securities (Singapore) Pte Ltd (“DBSVS”). DBS holds Australian Financial Services Licence no. 475946.

DBSVS is exempted from the requirement to hold an Australian Financial Services Licence under the Corporation Act 2001 (“CA”) in respect of financial services provided to the recipients. Both DBS and DBSVS are regulated by the Monetary Authority of Singapore under the laws of Singapore, and DBSVHK is regulated by the Securities and Futures Commission of Hong Kong under the laws of Hong Kong, which differ from Australian laws.

Distribution of this report is intended only for “wholesale investors” within the meaning of the CA.

Hong Kong This report is being distributed in Hong Kong by DBS Bank Ltd, DBS Bank (Hong Kong) Limited and DBS Vickers (Hong Kong) Limited, all of which are registered with or licensed by the Hong Kong Securities and Futures Commission to carry out the regulated activity of advising on securities.

Indonesia This report is being distributed in Indonesia by PT DBS Vickers Sekuritas Indonesia.

Malaysia This report is distributed in Malaysia by AllianceDBS Research Sdn Bhd ("ADBSR"). Recipients of this report, received from ADBSR are to contact the undersigned at 603-2604 3333 in respect of any matters arising from or in connection with this report. In addition to the General Disclosure/Disclaimer found at the preceding page, recipients of this report are advised that ADBSR (the preparer of this report), its holding company Alliance Investment Bank Berhad, their respective connected and associated corporations, affiliates, their directors, officers, employees, agents and parties related or associated with any of them may have positions in, and may effect transactions in the securities mentioned herein and may also perform or seek to perform broking, investment banking/corporate advisory and other services for the subject companies. They may also have received compensation and/or seek to obtain compensation for broking, investment banking/corporate advisory and other services from the subject companies.

Wong Ming Tek, Executive Director, ADBSR

Singapore This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) or DBSVS (Company Regn No. 198600294G), both of which are Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd and/or DBSVS, may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 6327 2288 for matters arising from, or in connection with the report.

Thailand This report is being distributed in Thailand by DBS Vickers Securities (Thailand) Co Ltd. Research reports distributed are only intended for institutional clients only and no other person may act upon it.

United Kingdom

This report is produced by DBSVHK which is regulated by the Hong Kong Securities and Futures Commission This report is disseminated in the United Kingdom by DBS Vickers Securities (UK) Ltd (“DBSVUK”). DBSVUK is authorised and regulated by the Financial Conduct Authority in the United Kingdom. In respect of the United Kingdom, this report is solely intended for the clients of DBSVUK, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBSVUK. This communication is directed at persons having professional experience in matters relating to investments. Any investment activity following from this communication will only be engaged in with such persons. Persons who do not have professional experience in matters relating to investments should not rely on this communication.

Dubai International Financial Centre

This research report is being distributed by DBS Bank Ltd., (DIFC Branch) having its office at PO Box 506538, 3rd Floor, Building 3, East Wing, Gate Precinct, Dubai International Financial Centre (DIFC), Dubai, United Arab Emirates. DBS Bank Ltd., (DIFC Branch) is regulated by The Dubai Financial Services Authority. This research report is intended only for professional clients (as defined in the DFSA rulebook) and no other person may act upon it.

United Arab Emirates

This report is provided by DBS Bank Ltd (Company Regn. No. 196800306E) which is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. This report is for information purposes only and should not be relied upon or acted on by the recipient or considered as a solicitation or inducement to buy or sell any financial product. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situation, or needs of individual clients. You should contact your relationship manager or investment adviser if you need advice on the merits of buying, selling or holding a particular investment. You should note that the information in this report may be out of date and it is not represented or warranted to be accurate, timely or complete. This report or any portion thereof may not be reprinted, sold or redistributed without our written consent.

China / Hong Kong

China Property Weekly Digest

Page 21

United States This report was prepared by DBSVHK. DBSVUSA did not participate in its preparation. The research analyst(s) named on this report are not registered as research analysts with FINRA and are not associated persons of DBSVUSA. The research analyst(s) are not subject to FINRA Rule 2241 restrictions on analyst compensation, communications with a subject company, public appearances and trading securities held by a research analyst. This report is being distributed in the United States by DBSVUSA, which accepts responsibility for its contents. This report may only be distributed to Major U.S. Institutional Investors (as defined in SEC Rule 15a-6) and to such other institutional investors and qualified persons as DBSVUSA may authorize. Any U.S. person receiving this report who wishes to effect transactions in any securities referred to herein should contact DBSVUSA directly and not its affiliate.

Other jurisdictions

In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is intended only for qualified, professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

DBS Vickers (Hong Kong) Limited

18th Floor Man Yee building, 68 Des Voeux Road Central, Central, Hong Kong

Tel: (852) 2820-4888, Fax: (852) 2868-1523

Company Regn. No. 31758