08-30-17 meg 1h2017 ir kit - megaworld corporation best position to capture bpo ......

TRANSCRIPT

IRKit1H2017

ALLIANCEGLOBALSTRUCTUREFocusedconsumercentricbrand

2

81% 44% 49%

RealEstatePioneertownshipdeveloper

andleadingBPO/officelandlordinthePhilippines

LiquorLargestbrandycompanyin

theworld

GamingFirstintegratedresortinthe

Philippines

QSRSecondinthePhilippine

QSRindustry

67%MEGPM

Marketcap:USD3.1b

EMPPMMarketCap:USD2.2b

RWMPMMarketCap:USD1.1b

NotListed

AGIPMMarketCap:USD2.7b

Marketcapfiguresasof08/29/2017

MEGAWORLDSTRUCTUREAstreamlinedvehicleforAGI’spropertyinterests

82% 82% 100%

TownshipDevelopment

Upper-middletohighincomemostlyinMetroManilaPHP3m– 30m(USD75k– 750k)Pricerange(perunit)

OfficeandcommercialMostlyBPOandLifestyleMalls

TourismestatedevelopmentsPHP3m– 12m(USD75k– 300k)Pricerange(perunit)

Middle-incomePHP1.5m– 4m(USD37.5k– 100k)Pricerange(perunit)

Affordable/economicPHP800K– 3m(USD20k– 75k)Pricerange(perunit) 3

GERIPMMarketCap:USD350m

ELIPMMarketCap:USD198m

NotListed

Marketcapfiguresasof08/29/2017

KEYMESSAGES

MEG– USD3.9b

Townshipdominance

Rentalincomegrowth

Strategiclandbank

• Pioneersof“Live-Work-Play-Learn”concept

• Diversifiedroster;inlinewiththedirectionofthegovernmentofregionalgrowth

• 22Townships:• 4inFortBonifacio• 6inMM(ex-FortBoni)• 5inLuzon(ex-MM)• 6inVisayas• 1inMindanao

4

• BestpositiontocaptureBPOindustrygrowth

• #1BPOlandlordinthePH• Highmarginbusiness• P12bnrentalincomein2017• P20bnrentalincomein2020

• Expansivelandbankacross3mainregionsofthecountry

• Nopressuretoacquirelandatunreasonableprices

• Canlastforthenext10-15years

Excellenttrackrecordprovingstabilityandsustainability

Strongfinancials

• Strongbalancesheet• Lowgearingvs industry

standard• Abletowithstand

downturns• Abletoseizeopportunities

Excellentmanagement

RAWLANDBANK

3,356ha

362ha

5

172ha

404ha

2,418ha

105hectares– unmatchedscaleinFortBonifacio,oneofthelargestCBDsinManila

UNMATCHEDTOWNSHIPDEVELOPMENTSINMETROMANILA

6

PHILIPPINE’SPREMIERTOWNSHIPDEVELOPERANDPIONEEROFTHE“LIVE-WORK-PLAY-LEARN”LIFESTYLE

7

50ha

5ha

34.5ha

15.4ha

18.5ha

12.4ha

25ha

350ha

561ha

62ha

1,200ha

150ha

30ha

72ha

11ha

34ha

53ha

173haSta. Barbara Heights

35.6ha

31ha WEST S I D EC I T Y

���������

MegaworldGERI

Suntrust

MapleGrove140ha

Totalof22TownshipsCovering3,704hectares

640ha

*Launchedin2016

*

*

4826

25%bookingthreshold

500k(5%)lumpsum

Month

RESIDENTIALBUSINESSCYCLETriedandtestedmodel

8

12

TypicalPaymentScheme

0Monthlypayments

500k(5%)lumpsum

24 36

500k(5%)lumpsum

500k(5%)lumpsum

0.5%permonth 0.6%permonth 1%permonth 1.2%permonth

ConstructionPeriod

Totalcontractprice:P10m•60%AmortizedPayments:P6m• Monthly:stepupperyear• 5%peranniversarydate:P500k

•40%TurnoverBalance:P4m

30%

RealEstateSalesP10mCostofRES(P6m)GrossProfitP4mDeferredGP(P2.8m)RealizedGPP1.2m

P1.1m(11%) P1.2m(12%) P1.7m(17%) P2m(20%)+P4m(40%)

Annualpayments

P1.1m(11%) P2.3m(23%) P4m(40%) P10m(100%)Cumulativepayment

30

PaymentPeriod

Toberealizedbasedonpercentageofcompletion

100%

1. Affordableandflexible2. Self-funding3. Conservativebooking4. Securedbypostdatedchecks

0%

~70%presold

Completion

0downpayment

50k(0.5%) 60k(0.6%) 120k(1.2%)100k(1%)

Fort MMex-fort Luzonex-MM Vis-Min Total

1H2016

1H2017

MEG 9.1 67% 9.2 67%

Taguig 3.2 24% 2.8 20%

Makati 1.1 8% 1.9 14%

Pasay&Parañaque 2.0 15% 1.0 8%

QuezonCity 0.7 5% 0.8 6%

Manila 0.1 1% 0.2 1%

Cavite >0.1 0% 0.1 0%

Cebu 0.2 1% 0.2 1%

Iloilo 0.5 4% 0.4 3%

Bacolod 0.1 0% 0.1 1%

Other Subs 1.3 10% 1.9 14%

GERI 2.1 16% 2.1 16%

ELI 2.3 17% 2.3 17%

TOTAL 13.4 100% 13.6 100%

DIVERSIFIEDREALESTATESALESMIX

inPHPbillions

9

1H2016(%sales)

MEG67% ELI

17%

GERI16%

Vis-Min12%

FortBonifacio

20%

MMEx-FortBonifacio

53%

LuzonEx-MM15%

1H2017PerBrand 1H2017PerLocation

10%

1%

14%

Year-on-YearGrowthperArea

14%

1H2017(%sales)

9%

STABLEOVERALLRESIDENTIALMARGINS

10

In PHPbillions 1H 2016 1H2017 %change

Real EstateSales(RES) 13.4 13.6 1.4%+InterestincomeonRealEstateSales 0.6 0.6 -0.2%

Total RES 14.0 14.2 1.4%

-CostofRES 7.6 7.7 1.0%

Gross ProfitonRES 6.4 6.5 1.8%

Gross ProfitMargin 45.7% 45.8% +10bps

-DeferredGrossProfit 2.7 2.3 -17.1%

RealizedGrossProfit 3.7 4.3 15.7%

+RealizedGrossProfitOnPriorYears'Sales 2.1 2.2 5.8%

TotalRealizedGrossProfit 5.8 6.5 12.2%

• SteadyhighblendedGPM

• Healthyincreaseintotalrealizedgrossprofitfromcontinuedprojectcompletion

P460/sqm

P480/sqm

P510/sqm

P530/sqm

P560/sqm

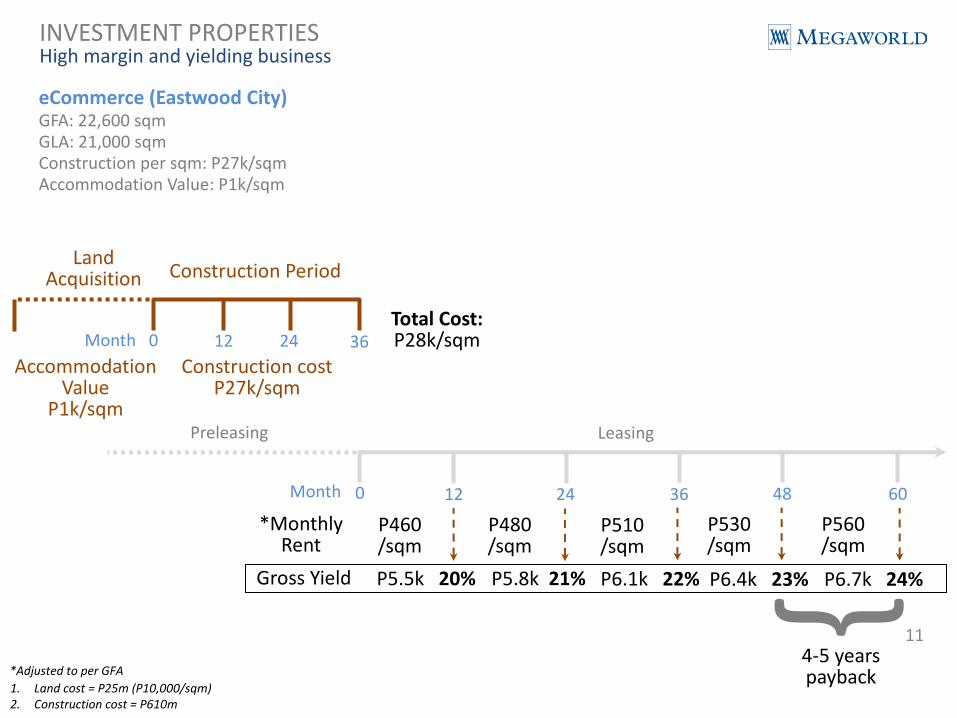

INVESTMENTPROPERTIESHighmarginandyieldingbusiness

11

LandAcquisition ConstructionPeriod

0 12 24 36

0 12 24 36

Preleasing

Month

Month

Leasing

48 60

TotalCost:P28k/sqm

eCommerce (EastwoodCity)GFA:22,600sqmGLA:21,000sqmConstructionpersqm:P27k/sqmAccommodationValue:P1k/sqm

*MonthlyRent

AccommodationValue

P1k/sqm

ConstructioncostP27k/sqm

GrossYield P5.5k20% P5.8k21% P6.1k22% P6.4k23% P6.7k24%}

4-5yearspayback*AdjustedtoperGFA

1. Landcost=P25m(P10,000/sqm)2. Constructioncost=P610m

P520/sqm

P540/sqm

P570/sqm

P600/sqm

P630/sqm

INVESTMENTPROPERTIESHighmarginandyieldingbusiness

12

LandAcquisition ConstructionPeriod

0 12 24 36

0 12 24 36

Preleasing

Month

Month

Leasing

48 60

TotalCost:P30k/sqm

OneWorldSquare(McKinleyHill)GFA:33,000sqmGLA:29,200sqmConstructionpersqm:P27k/sqmAccommodationValue:P2.5k/sqm

*MonthlyRent

AccommodationValue

P2.5k/sqm

ConstructioncostP27k/sqm

GrossYield }

4-5yearspayback*AdjustedtoperGFA

1. Landcost=P83m(P20,000/sqm)2. Constructioncost=P905m

P6.2k21% P6.5k22% P6.8k22% P7.2k24% P7.6k 25%

6.1

0.2 0.2 0.3 0.2 0.22.9 3.6 4.0

2.0 2.3

4.15.1

6.0

2.9 3.6

2014 2015 2016 1H2016 1H2017 2017 2020

166 170 170 237 273 356432 509 621

737 8511,009

2012 2013 2014 2015 2016 2017 2020

Rentalportfolio(‘000sqm)

13

7.2

598 679 791

8.9

20

974

15%

ExcellentTenantBaseQuality&Quantity• Over130tenants• Blue-chipcompanies

HealthyPre-leasing

Office

Commercial

CapturedMarketMegaworld LifestyleMalls

TopRetailers

2,110

IncreasingRentalIncome(inPhP billions)

OfficeCommercial&OthersIntersegment

OfficeCommercial&Others

23%

10.312

1,124

• P10bnin2016• P20bnin2020• Over1millionGLAin

2016• Over2millionGLAin

2020

Rental

1,365

20%

GROWINGRENTALINCOME–DRIVENBYOFFICE&COMMERCIALLEASING

5.1

GROWINGRENTALINCOME– HIGHMARGINBUSINESS

14

In PHPbillions 1H 2016 1H2017 %changeRevenuesRental 4.8 5.8 20.3%

IntersegmentSales 0.2 0.2 0.7%

TotalRentalRevenues 5.0 6.0 19.7%

-Operating Expense 1.3 1.5 16.9%

RentalEBIT 3.7 4.5 20.7%

RentalEBITMargin 74.5% 75.1% +60bps

In PHPbillions 1H2016 %share 1H2017 %shareEBIT Contribution

RealEstate 4.0 51% 4.7 51%Rental 3.7 47% 4.5 49%Hotel 0.1 2% 0.1 1%Corporate&Elimination 0.0 0% -0.1 -1%

TotalEBIT 7.8 100% 9.2 100%

• 50/50splitonEBIT

• StrongandsteadyrentalEBITMargin

• TotalrentalsinlinewithFYtarget

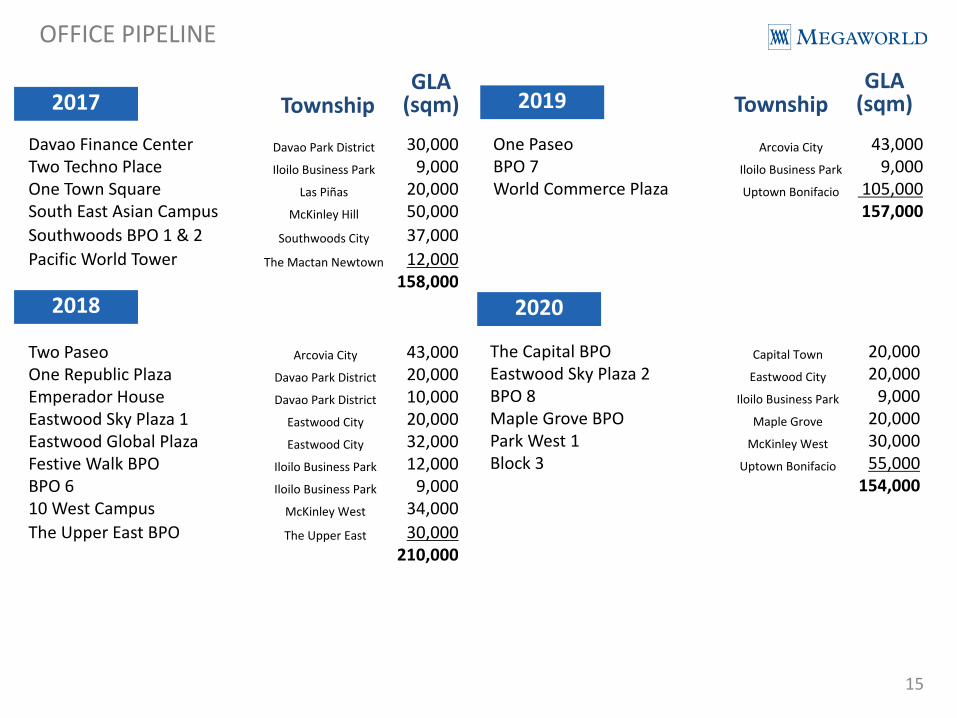

OFFICEPIPELINE

15

DavaoFinanceCenter Davao ParkDistrict 30,000TwoTechnoPlace IloiloBusinessPark 9,000OneTownSquare Las Piñas 20,000SouthEastAsianCampus McKinley Hill 50,000Southwoods BPO1&2 Southwoods City 37,000PacificWorldTower TheMactan Newtown 12,000

158,000

TwoPaseo Arcovia City 43,000OneRepublic Plaza DavaoParkDistrict 20,000Emperador House DavaoParkDistrict 10,000EastwoodSkyPlaza1 Eastwood City 20,000EastwoodGlobalPlaza Eastwood City 32,000FestiveWalkBPO IloiloBusinessPark 12,000BPO6 IloiloBusiness Park 9,00010WestCampus McKinleyWest 34,000TheUpperEastBPO TheUpperEast 30,000

210,000

OnePaseo Arcovia City 43,000BPO7 Iloilo BusinessPark 9,000WorldCommercePlaza UptownBonifacio 105,000

157,000

2017

2018

2019GLA(sqm)Township

GLA(sqm)Township

TheCapitalBPO Capital Town 20,000EastwoodSky Plaza2 EastwoodCity 20,000BPO8 Iloilo BusinessPark 9,000Maple GroveBPO Maple Grove 20,000ParkWest1 McKinleyWest 30,000Block 3 UptownBonifacio 55,000

154,000

2020

COMMERCIALPIPELINE

16

2017

2018

Grossfloorarea(sqm)

Leasablearea(sqm)

Commonarea(sqm)

Township

Arcovia Parade Arcovia CityFestiveWalkAnnex IloiloBusinessParkFestive WalkMall IloiloBusinessParkKing’sPlaza Manila 186,000 82,400 105,600McKinleyWestBPOD,E,F McKinleyWestSouthwoods Mall Southwoods CityUptownResidences UptownBonifacio

Alabang WestRetail Alabang WestBoracay Beach Strip Boracay NewcoastTheCapitalRetail Capital TownDavaoParkRetail DavaoParkDistrict 53,200 28,800 24,800MapleGroveRetail MapleGroveNorthill GatewayRetail Northill GatewayThe UpperEastRetail TheUpperEastMactan NewtownBeach TheMactan Newtown

COMMERCIALPIPELINE

17

2019

2020

Township

Boracay Belmont Boracay NewcostGovernors’Hills Governors’Hills 85,000 26,900 38,600ThePad Shaw

Arcovia Palazzo Arcovia CityBoracay Chancellor Boracay NewcoastRomaCainta CaintaTheCapitalRetail2 CapitalTownBlock20 McKinleyWest 267,700 168,200 99,300Maple GroveRetail2 Maple GroveSanAntonioResidences SanAntonioResorts WorldRetail Westside City

Grossfloorarea(sqm)

Leasablearea(sqm)

Commonarea(sqm)

PERFORMANCEUPDATE

18

In PHPbillions 1H 2016 1H2017 %change

Revenues 23.0 24.3 5.4%Real EstateSales 13.4 13.6 1.4%Rental 4.8 5.8 20.3%Hotel 0.6 0.6 9.8%OtherRevenues 4.2 4.2 0.3%

Cost&Expenses 17.0 17.6 3.4%Cost ofRealEstateSales 7.6 7.7 1.0%Hotel 0.3 0.4 17.1%OPEX& OtherExpenses 6.5 6.7 2.3%OperatingIncome 8.5 9.5 11.2%InterestExpense 0.7 0.8 5.0%Pre-taxIncome 7.8 8.7 11.8%IncomeTax Expense 1.8 2.1 14.5%NetIncome 6.0 6.7 11.0%Minority Interest 0.2 0.2 17.9%NetIncome toOwners 5.8 6.4 10.8%

EBITMargin 37.1% 39.2% +210bpsNetIncomeMargin 26.2% 27.6% +140bps

• Netincomeinlinewithdouble-digitgrowthtarget

• Marginimprovementfromhigherrentalcontribution

• OPEXup8.6%

• Flattishbutdiversifiedmix

• Modestcostexpansion

• Robustgrowthforbothrental&hotels

• DeferredGPdown17.1%

CONSOLIDATEDREVENUEBREAKDOWN

19

1H2017

RentalIncome24%

HotelOperations3%

Interest&Other4%

RealEstate69%

1H2016

RentalIncome21%

HotelOperations3%

Interest&Other5%

RealEstate71%

In PHPbillions 1H 2016 1H2017 %change

Real EstateSales 13.4 13.6 1.4%InterestincomeonRealEstateSales 1.0 1.0 0.1%

RealizedGross ProfitonPriorYears’Sales 2.1 2.2 5.8%

Rental 4.8 5.8 20.3%Hotel 0.6 0.6 9.8%Interest& Otherincome 1.1 1.0 -9.6%

Total Revenues 23.0 24.3 5.4%

• Morerentalcontribution;300bp expansion

• Residentialrevenuesup1.9%drivenbygrowingRGPfromcontinuedprojectcompletion

71.0

61.252.6

33.528.6

20.115.916.4

22.825.131.8

26.8

47% 43% 39%

26% 28% 25%

37% 31%

22%

7%

1H2017FY2016FY2015FY2014FY2013FY2012

TotalBorrowings Cash&CashEquivalents DettoEquity NetDebttoEquity

FY2012 FY2013 FY2014 FY2015 FY2016 1H2017

DebttoEquity 25% 28% 26% 39% 43% 47%

NetDebttoEquity Net Cash NetCash 7% 22% 31% 37%

20

SOLIDBALANCESHEETinPHPbillions

34.622.320.924.824.8

13.6

36.4

38.931.7

8.83.8

6.5

1H2017FY2016FY2015FY2014FY2013FY2012

21

DEBTMATURITYPROFILE

Borrowings Loans

$250,000,000 4.25% April2013 2023$200,000,000 6.75% April2011 2018

₽12,000,000,000 5.35% March2017 2024

Bonds DateIssued MaturityCouponRate

inPHPbillions

BondsLoans

₽36,386,223,575 ~5.00% Various Various

Loans YearIssued MaturityAve.Rate

28.6 33.5

52.6

71.0

20.1FixedRate99%

FloatingRate<1%

61.2

5-YEARCAPEXPLANPHP285.8BUNTIL2019

22

2015PHP54.5B

2016PHP48.8B

2017PHP60B

2018 2019

PHP285.8B

PHP122.5B

Residential/Office/Retail/HotelPHP48B

LandBankingPHP12B

2017CAPEXBudget

20%

80%

1H2017CAPEXSpending

99%

Resi/Office/Retail/HotelPHP21.9B

<1% LandBankingPHP0.9B

67%

49%

76%

47% 48%

FLI ALI MEG RLC SMPH

82% 64% 54%

23% 21%

16% 8%

27%

21% 6%

10% 23% 22%

50% 74%

0% 4% 1% 6% 2%

-8%

1%

-4%

0%

-3% FLI ALI MEG RLC SMPH

Residential Office Retail Hotels Others

ImpactofRentalAssetsonEarnings

23

49%31%

80%

71%

26%

94% 60%

103% 127%

165%

FLI ALI MEG RLC SMPH

EBITContribution

RentalMargins RentalIncomeas%ofOPEX

Basedon2015FSs

KEYTAKEAWAYS

24

• Diversifiedtownshiproster22townshipsacrossthecountryGrowingcontributionsfromoutsideMM

• HighresidentialbaseHighblendedGPMat46%1H2017presalesatP58.3bn(P90bnE2017guidance)1H2017launchesatP18.4bn(P30bnE2017guidance)

• GrowinghighmarginrentalbusinessRentalEBITmarginat75%2017Target:P12bn2020Target:P20bn

EndofPresentation