07 apr 2015 letter to us senate ctee on energy & natural resources

DESCRIPTION

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.TRANSCRIPT

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Lisa Murkowski 709 Hart Senate Office Building Washington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear ENR Chairman Murkowski,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary • XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery

from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. • While the U.S. refining margins are high at the moment, the outcome of this investment is

unpredictable and will largely depend on whether the ban on oil exports is repealed. • The article discusses a series of critical decisions that XOM has made in recent years,

which have been marked by buying high and selling low. .

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Lisa Murkowski April 7, 2015

Page ! of ! 2 3

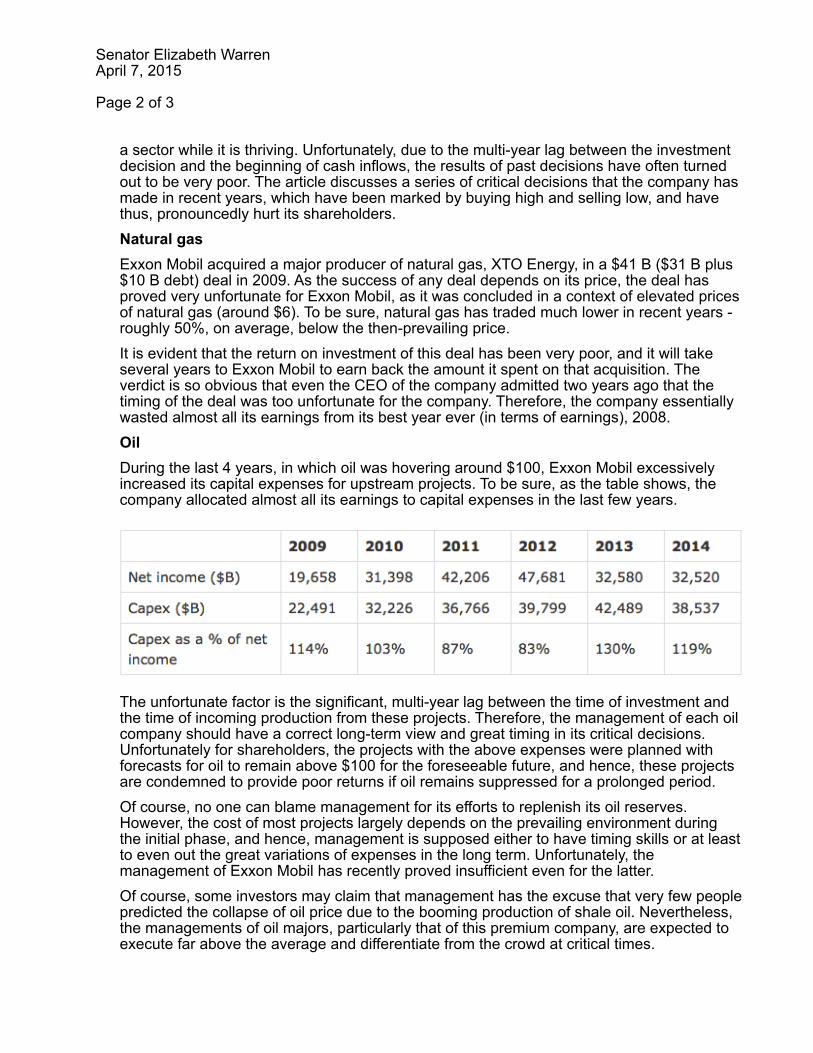

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Lisa Murkowski April 7, 2015

Page ! of ! 3 3

Share repurchases The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that you as Chairman of ENR, convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Lamar Alexander 455 Dirksen Senate Office BuildingWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Alexander,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Lamar Alexander April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Lamar Alexander April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator John Barrasso 307 Dirksen Senate Office BuildingWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Barrasso,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator John Barrasso April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator John Barrasso April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Shelley Capito 5 Russell Senate Office Building CourtyardWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Capito,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Shelley Capito April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Shelley Capito April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Bill Cassidy 703 Hart Senate Office BuildingWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Cassidy,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Bill Cassidy April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Bill Cassidy April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Steve Daines 1 Russell Senate Office Building CourtyardWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Daines,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Steve Daines April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Steve Daines April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Jeff Flake Russell Senate Office Building 368Washington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Flake,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Jeff Flake April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Jeff Flake April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator Cory Gardiner Dirksen Senate Office Building SD-B40BWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Gardiner,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator Cory Gardiner April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.

The unfortunate factor is the significant, multi-year lag between the time of investment and the time of incoming production from these projects. Therefore, the management of each oil company should have a correct long-term view and great timing in its critical decisions. Unfortunately for shareholders, the projects with the above expenses were planned with forecasts for oil to remain above $100 for the foreseeable future, and hence, these projects are condemned to provide poor returns if oil remains suppressed for a prolonged period. Of course, no one can blame management for its efforts to replenish its oil reserves. However, the cost of most projects largely depends on the prevailing environment during the initial phase, and hence, management is supposed either to have timing skills or at least to even out the great variations of expenses in the long term. Unfortunately, the management of Exxon Mobil has recently proved insufficient even for the latter. Of course, some investors may claim that management has the excuse that very few people predicted the collapse of oil price due to the booming production of shale oil. Nevertheless, the managements of oil majors, particularly that of this premium company, are expected to execute far above the average and differentiate from the crowd at critical times.

Senator Cory Gardiner April 7, 2015

Page ! of ! 3 3

Share repurchases

The company has consistently repurchased its shares to enhance shareholder returns. Unfortunately for shareholders, the company funded the acquisition of XTO Energy with the issuance of new shares in 2010, when the stock stood at a decade low. Moreover, now that the oil producers are facing the headwind of cheap oil, the company has drastically reduced the annual rate of share repurchases, from 5% in 2011-2013 to 3% in 2014 and only 1% in 2015. Nevertheless, to be fair to management, the poor timing in share repurchases is the norm for the vast majority of companies. More specifically, as share repurchases are the last priority - after the capital expenses and dividends are paid - most companies tend to repurchase their shares only when they have ample cash. This invariably occurs during booming periods, in which the stock prices are inflated, and hence these share repurchases hardly add any shareholder value. While most companies tend to make the same mistake, the few companies that keep performing buybacks even during rough times make a difference to their shareholders. Downstream

While refiners in most parts of the world have suffered from depressed margins in the last 6 years, their U.S. counterparts have thrived, thanks to the deep discount of WTI vs. Brent, which has resulted from the shale oil boom. It is remarkable that this advantage of U.S. refineries had remained largely unnoticed in the oil majors till recently, as oil majors normally derived about 90% of their earnings from the upstream sector. However, now that the oil price has collapsed, the downstream sector has provided significant support on the earnings of oil majors. Therefore, it makes sense that Exxon Mobil wants to spend billions to expand the capacity of its Beaumont refinery. Nevertheless, as it will take some years to complete the expansion, the profitability of this project will depend on the long-term trajectory of U.S. refining margins. If the ban on U.S. oil exports is repealed, the refining margins will pronouncedly contract, and hence, this project will offer disappointing returns. Therefore, management should carefully evaluate the long-term path of U.S. refining margins, and not just decide based on the recent enthusiasm over U.S. refining margins. Hopefully, they will do their homework this time. Conclusion

Buying high and selling low is a catastrophic strategy for long-term returns. Unfortunately, this is much easier said than done, as it is much easier to follow the herd than go against the flow. To be sure, the herd followers will be easily forgiven if their decision is proven wrong, whereas the ones who decide against public opinion will incur excessive criticism, should they fail. The management of Exxon Mobil has made some poor critical investments in the past, which have punished the company's shareholders. Hopefully, their decision to spend billions on the refinery expansion is based on a solid long-term view.

Again, I suggest that the ENR Committee convene a hearing and ask Rex Tillerson and other CEOs if they will supply fuels when profits fall below breakeven. Ask how they will clean up the toxic infrastructure in the end. Will Risk Management avert worst case scenarios — the unfathomable, shocking to ponder, economic collapse caused by their decisions and hubris?

Sincerely yours,

Doug Grandt

Douglas A. Grandt PO Box 6603 Lincoln, NE 68506 (510) 432-1452

April 7, 2015

Senator John Hoeven 338 Russell Senate Office BuildingWashington, D.C. 20510

Re: Oil Refining - Considering future eventualities versus the myopia of the present (letter #7)

Dear Senator Hoeven,

U.S. ENERGY INDEPENDENT does not come from the likes of ExxonMobil holding us hostage to rectify their having “shot themselves in the foot.” The glut from the shale oil and gas boom was their own miscalculation. Now, they are holding a gun to our collective head, demanding that their cash flow and earnings be protected by allowing the glut of excess production to flood the international markets to fetch higher prices. That, in turn will raise domestic prices.

Where is the industry taking us? Are We the People beholden to the industry for the fossil fuels they provide — are we expected to acquiesce to their experiment with our economy? Who will bale them out when their accumulated miscalculations and hubris result in financial collapse?

We need to manage the industry’s decisions for the sake of public interest and national interest. Please call them to task, develop a strategy to get control, assure true energy independence.

This is no April Fools joke. One analyst had the courage to publish the following assessment, which — when taken in context with countless other assessments that also hint at a precarious future for the fossil fuel industry — points to serious risk for our economy. Read this critically:

Exxon Mobil - The Company That Buys High And Sells Low April 2, 2015 | Aristofanis Papadatos | http://bit.ly/ALPHA2April15

Summary

• XOM is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project.

• While the U.S. refining margins are high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the ban on oil exports is repealed.

• The article discusses a series of critical decisions that XOM has made in recent years, which have been marked by buying high and selling low.

.

Exxon Mobil (NYSE:XOM) is reportedly escalating its plans to expand the capacity of its Beaumont refinery from 344 Kbbl/day to 850 Kbbl/day in a multi-billion dollar project. The management previously intended to double the capacity of its refinery, but it now seems determined to expand its capacity even further. While the U.S. refining margins are particularly high at the moment, the outcome of this investment is unpredictable and will largely depend on whether the U.S. government will continue to ban oil exports in the future. In addition, although it is really hard to evaluate this decision of the management at the moment, it is safe to claim that it has a similar character to some past decisions; investing in

Senator John Hoeven April 7, 2015

Page ! of ! 2 3

a sector while it is thriving. Unfortunately, due to the multi-year lag between the investment decision and the beginning of cash inflows, the results of past decisions have often turned out to be very poor. The article discusses a series of critical decisions that the company has made in recent years, which have been marked by buying high and selling low, and have thus, pronouncedly hurt its shareholders. Natural gas Exxon Mobil acquired a major producer of natural gas, XTO Energy, in a $41 B ($31 B plus $10 B debt) deal in 2009. As the success of any deal depends on its price, the deal has proved very unfortunate for Exxon Mobil, as it was concluded in a context of elevated prices of natural gas (around $6). To be sure, natural gas has traded much lower in recent years - roughly 50%, on average, below the then-prevailing price. It is evident that the return on investment of this deal has been very poor, and it will take several years to Exxon Mobil to earn back the amount it spent on that acquisition. The verdict is so obvious that even the CEO of the company admitted two years ago that the timing of the deal was too unfortunate for the company. Therefore, the company essentially wasted almost all its earnings from its best year ever (in terms of earnings), 2008. Oil During the last 4 years, in which oil was hovering around $100, Exxon Mobil excessively increased its capital expenses for upstream projects. To be sure, as the table shows, the company allocated almost all its earnings to capital expenses in the last few years.