03 june 2013 - the ice · › on 20 december 2012, ice clear europe and liffe administration ... of...

TRANSCRIPT

The Regulatory and Clearing Landscape

Mark Woodward, ICE Clear Europe

03 June 2013

2

Legal Disclaimer

Disclaimer and Cautionary Note Regarding Forward-Looking Statements

This presentation may contain “forward-looking statements” made pursuant to the safe harbor provisions of

the Private Securities Litigation Reform Act of 1995. Statements regarding our businesses that are not

historical facts are forward-looking statements that involve risks, uncertainties and assumptions that are

difficult to predict. These statements are not guarantees of future performance and actual outcomes and

results may differ materially from what is expressed or implied in any forward-looking statement. In some

cases, you can identify forward-looking statements by words such as "may," "hope," "will," "should,"

"expect," "plan," "anticipate," "intend," "believe," "estimate," "predict," "potential," "continue," "could," "future"

or the negative of those terms or other words of similar meaning.

In addition, you should carefully consider the risks and uncertainties and other factors that may affect future

results in ICE's and NYSE Euronext's respective filings with the SEC that are available on the SEC's web

site located at www.sec.gov, including the sections entitled "Risk Factors" in ICE's Form 10−K for the fiscal

year ended December 31, 2012, as filed with the SEC on February 6, 2013, and "Risk Factors" in NYSE

Euronext's Form 10−K for the fiscal year ended December 31, 2011, as filed with the SEC on February 29,

2012. SEC filings are also available in the Investors & Media section of ICE’s website and the Investor

Relations section of NYSE Euronext’s website. You should not place undue reliance on forward-looking

statements, which speak only as of the date of this presentation. Except for any obligations to disclose

material information under the Federal securities laws, ICE and NYSE Euronext undertake no obligation to

publicly update any forward-looking statements to reflect events or circumstances after the date of this

presentation.

3

Agenda

Background to ICE Clear Europe

Regulatory Reform Agenda: Future Impacts and Implications Swaps to Futures Transition

EMIR Requirements

Customer Account Structures

Trade Confirmation and Registration

4

ICE Commodity and Derivatives Markets

Integrated Markets, Clearing and Technology

ICE Regulated Futures Exchanges ICE OTC ICE Data & Services

EUROPE

ENERGY & EMISSIONS

Brent Crude

Brent NX Crude

WTI Crude

Gasoil

Low Sulphur Gasoil

ASCI Crude

Oil and refined products

Natural gas liquids

Liquefied natural gas

European natural gas

U.K. Electricity

Coal

Emissions

Iron Ore

Freight

OTC CONTRACTS

AGS & ENERGY

Cocoa

Coffee

Cotton

Sugar

Orange Juice

Barley

Canola

Wheat

Corn

Soybeans

Financial Gas

Financial Power

FINANCIAL

Currency Pairs

U.S. Dollar Index

Russell Indexes

Real-time prices/screens

Indices and end of day reports

Tick-data, time and sales

Market price validations

Forward Curves

WebICE & ICE Mobile ICE eConfirm ICE Link

ICE Chat

ICE Match

Chatham Energy

Coffee Grading

Trade Vault

OTC Credit – Creditex

CDS – indexes, single names, structured products

BRIX – Brazilian Power Markets

ICE Clear U.S., ICE Clear Canada ICE Clear Europe The Clearing Corp, ICE Clear Credit

Global Clearing Houses

U.S. & CANADA MARKET DATA

SERVICES

5

Overview of ICE Clear Europe › ICE Clear Europe (ICE Clear) regulatory status is as follows:

• Recognised Clearing House supervised by the U.K.’s Financial Services Authority (FSA);

• Designated under the Settlement Finality Directive by the U.K. FSA;

• Systemically important payment system overseen by the Bank of England;

• Derivatives Clearing Organisation supervised by the U.S. Commodity Futures Trading Commission; and

• Securities Clearing Agency supervised by the U.S. Securities and Exchange Commission.

› ICE Clear currently offers clearing and settlement services to: ‒ ICE Futures Europe’s contracts (including the ICE ECX Emissions products)

‒ ICE Futures US Energy Division contracts

‒ iTraxx Europe indices and Single Name OTC CDS contracts

› ICE Clear commenced operations on 03 November 2008 and, in relation to its energy clearing business: ‒ has 57 Energy Clearing Members

‒ clears contracts with a notional value of approximately $40bn per day

‒ can call on a Guaranty Fund of approximately $1.8bn (made up from $650mn cash and collateral deposited in the Fund by ICE and its Members, and powers of assessment)

› CDS clearing was launched on 27 July 2009, and: ‒ currently has 16 CDS Clearing Members and has cleared:

• €10.66trn in notional value across 288,443 CDS Index transactions with an open interest of €193bn (currently 46 indices);

• €1.73trn in notional value across 336,821 CDS Single Name transactions with an open interest of €337bn (currently 121 names);

‒ can call on a Guaranty Fund of over €5bn (made up from cash deposited to the Fund by ICE and its Members, and powers of assessment).

› On 20 December 2012, ICE Clear Europe and LIFFE Administration and Management (“LIFFE A&M”) entered into a clearing services agreement (“CSA”) pursuant to which ICE Clear Europe will provide clearing services to the London market of NYSE Liffe from 01 July 2013.

6

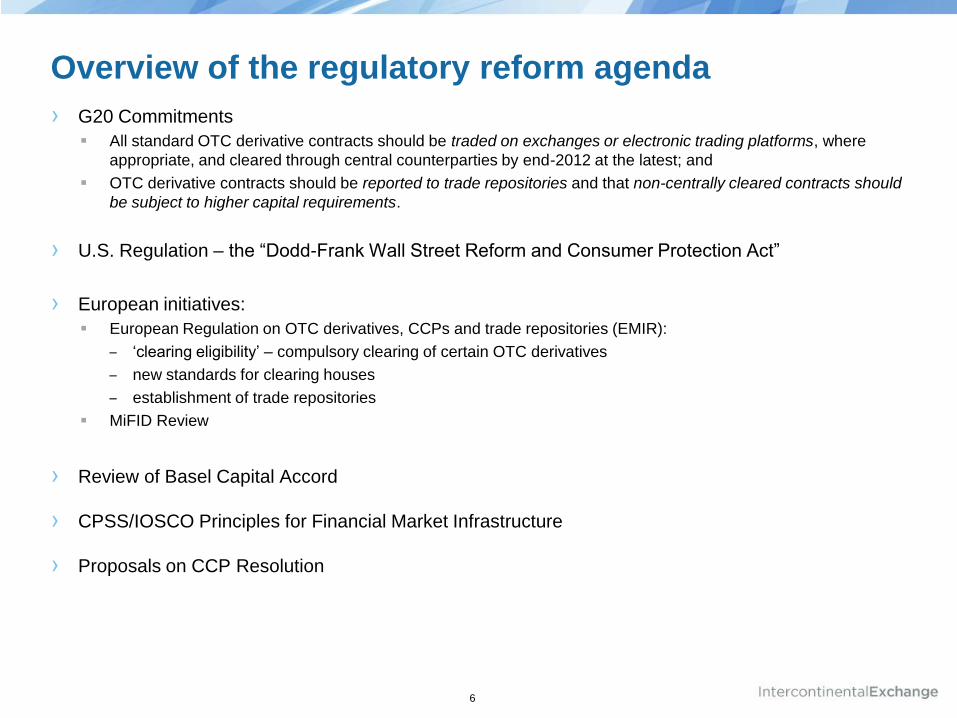

Overview of the regulatory reform agenda

› G20 Commitments

All standard OTC derivative contracts should be traded on exchanges or electronic trading platforms, where

appropriate, and cleared through central counterparties by end-2012 at the latest; and

OTC derivative contracts should be reported to trade repositories and that non-centrally cleared contracts should

be subject to higher capital requirements.

› U.S. Regulation – the “Dodd-Frank Wall Street Reform and Consumer Protection Act”

› European initiatives:

European Regulation on OTC derivatives, CCPs and trade repositories (EMIR):

‒ ‘clearing eligibility’ – compulsory clearing of certain OTC derivatives

‒ new standards for clearing houses

‒ establishment of trade repositories

MiFID Review

› Review of Basel Capital Accord

› CPSS/IOSCO Principles for Financial Market Infrastructure

› Proposals on CCP Resolution

7

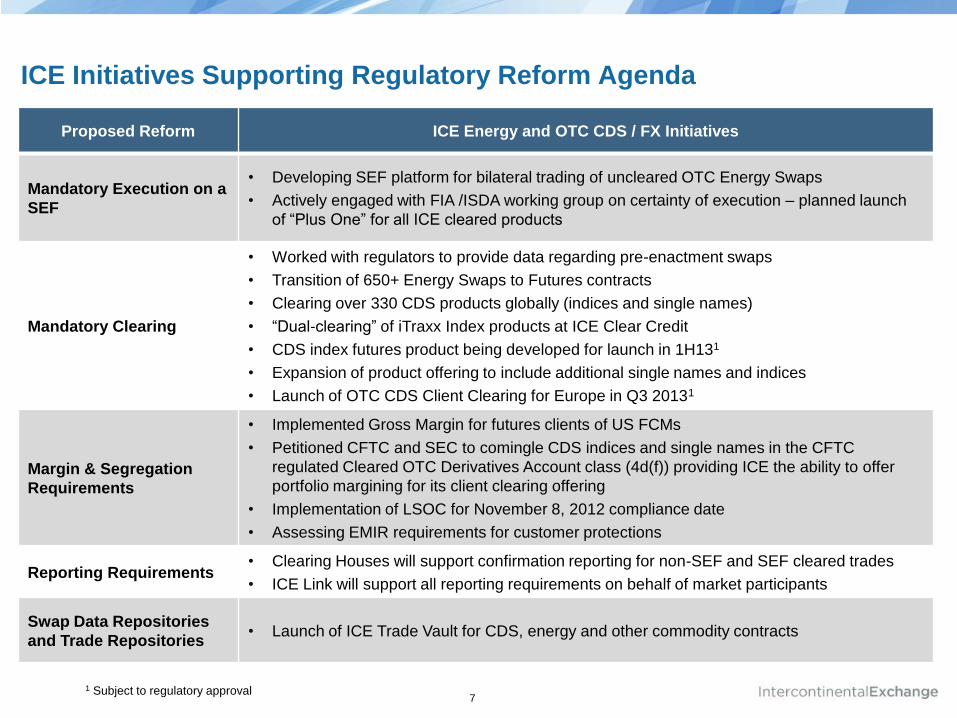

ICE Initiatives Supporting Regulatory Reform Agenda

Proposed Reform ICE Energy and OTC CDS / FX Initiatives

Mandatory Execution on a

SEF

• Developing SEF platform for bilateral trading of uncleared OTC Energy Swaps

• Actively engaged with FIA /ISDA working group on certainty of execution – planned launch

of “Plus One” for all ICE cleared products

Mandatory Clearing

• Worked with regulators to provide data regarding pre-enactment swaps

• Transition of 650+ Energy Swaps to Futures contracts

• Clearing over 330 CDS products globally (indices and single names)

• “Dual-clearing” of iTraxx Index products at ICE Clear Credit

• CDS index futures product being developed for launch in 1H131

• Expansion of product offering to include additional single names and indices

• Launch of OTC CDS Client Clearing for Europe in Q3 20131

Margin & Segregation

Requirements

• Implemented Gross Margin for futures clients of US FCMs

• Petitioned CFTC and SEC to comingle CDS indices and single names in the CFTC

regulated Cleared OTC Derivatives Account class (4d(f)) providing ICE the ability to offer

portfolio margining for its client clearing offering

• Implementation of LSOC for November 8, 2012 compliance date

• Assessing EMIR requirements for customer protections

Reporting Requirements • Clearing Houses will support confirmation reporting for non-SEF and SEF cleared trades

• ICE Link will support all reporting requirements on behalf of market participants

Swap Data Repositories

and Trade Repositories • Launch of ICE Trade Vault for CDS, energy and other commodity contracts

1 Subject to regulatory approval

8

Swaps to Futures Transition

› ICE conducted an extensive review and analysis of the Dodd-Frank Wall Street Reform and Consumer

Protection Act (Dodd-Frank Act) in the U.S. and parallel laws presently being drafted in Europe and Asia. In

order to determine how these rules will affect swaps participants across the U.S., Europe, and Asia and have

also received substantial input from many ICE Participants. Based on this analysis, ICE concluded that, once

implemented, these laws and regulations are likely to increase the cost and complexity for swaps market

participants relative to futures markets participants.

› ICE’s announced its intention to convert each existing OTC cleared Energy swap and option product and open

interest to an economically equivalent future or option contract listed on either the ICE Futures US or ICE

Futures Europe exchange.

› The transition occurred over the weekend of 13/14 October 2012 in line with the implementation of the Swap

Dealer/Swap Market Participant rules.

ICE Futures Europe ICE Futures US Energy Division

Crude Oil U.S. Natural Gas

Refined Products Electric Power

Natural Gas Liquids U.S. Environmental Products

Freight

Iron Ore

9

Impact of EMIR on CCPs and operating processes

› ICE has contributed extensively to the consultation process in relation to global regulatory reform, including

the Dodd-Frank Act, EMIR and CPSS-IOSCO Principles. Core concerns expressed include level of

prescription and possibility of regulatory arbitrage.

› Key areas of change:

1. CCP rules and operating procedures:

Re-authorisation process

Operating structures and Governance

Risk Management standards

Acceptable collateral and liquidity risk management

Customer protection models

2. Trade reporting to Trade Repositories.

3. Implementation Timetable.

4. Impact on capital charges.

5. Impact of areas of regulatory variance.

10

Q3 2013

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

EMIR – Current Implementation Timeline

15 Mar 13 – 15 Sep 13: EU/EEA CCPs have 6 months to submit their application for authorisation under EMIR.

15 Mar 13 – 15 Apr 13: NCAs initial notifications of OTC derivatives already cleared by CCPs in their jurisdiction.

CCP registration

Trade reporting

15 Apr 13 – 15 Mar 14: National competent authorities (NCAs) have 6 months to decide whether to authorise after determining application is complete.

Mandatory clearing

15 Mar 13: First date TR can send application for authorisation to ESMA.

25 Jun 13: First possible registration of TR (ESMA have 20 working days to determine completeness, then 40 working days to make a decision once complete. Registration comes into effect 5 working day after decision).

23 Sep 13: First possible reporting start date for IR and credit (90 calendar days after first TR registered).

1 Jan 14: First possible reporting start date for commodities and other asset classes (assuming TR is registered for the specific asset class before 1 Oct).

15 Mar 14: Last possible registration date for existing CCPs.

16 Apr 13 – 16 Mar 14: NCAs notify of additional OTC derivatives cleared in their jurisdiction as they authorise CCPs.

16 Oct 13 – 16 Sep 14: ESMA will have 6 months to submit draft RTS on the class of OTC derivatives subject to clearing obligation and effective dates.

11

› EMIR requires CCPs to keep separate records and accounts so its Clearing Members can distinguish assets

and positions:

held for the clearing member from those of its clients - "Omnibus Client Segregation"; and

held for one client from those held for other clients – “Individual Client Segregation.”

› Clearing Members are then also required to offer these client protection options to their clients. In relation to

Individual Client Segregation, where a client elects for this level of protection, their positions and margin will

be held in an account at the CCP together with any excess margin.

› ICE is proposing to introduce the following segregation models under EMIR:

Segregated Client Account: Omnibus Client Segregation (Net Margin for ETD);

Non-Segregated Client Account (TTCA): Omnibus Client Segregation (Net Margin for ETD);

Individual Segregation through Sponsored Principal Model.

Alternative (Margin-flow co-mingled) Individual Segregated Account.

› Additionally, ICE Clear Europe is currently discussing with various custody agents and securities

depositories the possibility of enhancing protection of customer assets through tri-party, quad-party or

similar arrangements.

EMIR Customer Account Structure models

12

ICE eConfirm

› Internet-based Electronic Trade Confirmation Services:

Central Web-Based Platform to Submit & Confirm Trades & Resolve Discrepancies

Two-Way Matching between 2 Counterparties OR a Broker & Customer

Three-Way Matching between a Broker & 2 Counterparties

For ALL Standard Trades NOT for “Just ICE Trades”

Confirm Trades Executed via a Voice Broker, Direct, or Online

› Processes trade data from 250+ counterparties & brokers. Utilized Globally by the Largest Banks, Energy

Marketers, Utilities, & Hedge Funds

› Fourteen million trades matched & warehoused since 2002 go live

› Accepts broad range of bilateral swaps, options & physical trades

› Leading Technology and Systems

State of the Art Technology with Physical & Logical Security

Regular External Audit of all Processes and Controls (including Comprehensive SAS 70 Type II Audit

performed Annually by PWC)

Comprehensive Data Retention Policy

› https://www.theice.com/econfirm.jhtml

13

ICE Trade Vault

› ICE Trade Vault, LLC (“ICE Trade Vault”) was the first SDR approved by the CFTC. ICE Trade Vault

is registered in the credit, commodities and FX asset classes. During October 2012, ICE Trade Vault

went live with CDS. Commodities went live on 28 February 2013 for Swap Dealers.

› ICE has established an EU entity domiciled in London, ICE Trade Vault Europe Limited, in order to

best serve our European participants. ICE Trade Vault EU is the legal entity which is seeking TR

registration under EMIR. By operating the TR service via this entity, ICE Trade Vault EU is addressing

concerns expressed by our European participants regarding the extraterritorial reach of Dodd-Frank.

› Reporting Guidance & Trade Flows. ICE Trade Vault has contributed to consultation on Technical

Specs are principal based in regards to trade reporting and trade flows.

› ICE is committed to making the technical integration process streamlined for its customers. Trade

data submission is possible via three easy methods:

XML API enables real time submissions and queries

Tab delimited file upload facilitates batch processing

Trade entry on-screen via simple website features

› https://www.theice.com/trade_vault.jhtml

14

Contacts

Mark Woodward

Director, Corporate Development

ICE Clear Europe

+44 (0)20 7065 7617

ICE Clear Europe

www.theice.com

The Regulatory and Clearing Landscape

Mark Woodward, ICE Clear Europe

03 June 2013