003840 - germania insurance company · pdf filebusiness profile the germania insurance company...

TRANSCRIPT

003840 - Germania Insurance Company

Report Revision Date: 07/15/2013

Rating and Commentary 1

Best's Credit Rating: 12/18/2012

Rating Rationale: 12/18/2012

Report Commentary: 07/15/2013

Financial 2

Time Period: 2nd Quarter - 2013

Last Updated: 08/24/2013

Status:Quality Cross Checked

General Information 3

Corporate Structure: N/A

States Licensed: 01/15/2002

Officers and Directors: 06/04/2012

Best's Credit Rating Methodology Disclaimer Best's Rating Guide

Additional Online Resources

Related News Archived AMB Credit Reports

Rating Activity and Announcements Corporate Changes & Retirements

Company Overview AMB Country Risk Reports - United States

1The Rating and Commentary date outlines the most recent updates to the Company's Rating, Rationale, and Report Commentary for key rating and business changes. Reportcommentary may include significant changes to Business Review, Financial Performance/Earnings, Capitalization, Investment/Liquidity, or Reinsurance sections of the report.2The Financial date reflects the current status of the financial tables found within the body of the Report, including whether the data was loaded as received or had been runthrough our quality control cross-check process.3The General Information date covers key areas that may have changed such as corporate structure, states licensed or officers and directors.

Page 1 of 28 Print Date: September 03, 2013

Ultimate Parent: Germania Farm Mutual Insurance Assn

Germania Insurance Company507 Highway 290 East, Brenham, Texas, United States 77833

Tel.: 979-836-5224 Web: www.germaniainsurance.com Fax: 979-277-1900

AMB #: 003840 Ultimate Parent: 003687 NAIC #: 36854 FEIN#: 74-1991338

Best's Credit RatingsBest's Financial Strength Rating: A- Outlook: Stable

Best's Issuer Credit Rating: a- Outlook: Stable

Rating Effective Date: 12/18/2012

Financial Size Category: VIII

Report Revision Date: 07/15/2013

Rating RationaleRating Rationale: The ratings of Germania Farm Mutual Insurance Association have been extended to Germania InsuranceCompany as it is fully integrated into the Germania group's strategic and operational plans. The company benefits from theGermania group's shared common infrastructure and distribution network, use of the highly recognizable brand, andparticipation in the intercompany reinsurance program. In the group, the company is the sole writer of commercial property andBOP, personal and general liability, as well as standard personal auto, all of which statutorily cannot be written by GermaniaFarm Mutual Insurance Association.

The following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

The ratings are based on the consolidated operating results and financial position of Germania Farm Mutual InsuranceAssociation and its wholly owned subsidiaries, Germania Insurance Company, Germania Select Insurance Company,Germania Fire and Casualty Company, and Texas Heritage Insurance Company (Texas Heritage Insurance Company isseparately rated by A.M. Best). The ratings and outlooks reflect the group's adequate risk-adjusted capitalization, conservativeinvestment philosophy, and its strong and long-standing market presence in Texas. Partially offsetting these positive ratingfactors are the group's underwriting losses in most of the last five years, elevated underwriting leverage measures andgeographic concentration of risk.

The group maintains adequate risk-adjusted capitalization given its current rating level. This is partially due to the group'sconservative investment portfolio, which continues to produce favorable investment earnings that have partially mitigatedunderwriting losses over the last five-year period. The group's operating results have been extremely volatile during the latestfive-year period due primarily to frequent and severe weather-related events. In response, the group has been managing itsproperty book of business to reduce weather-related exposure, especially from hurricane-prone areas. In addition, a separatelyrated stock company, Texas Heritage Insurance Company was created to write dwelling policies previously written byGermania Farm Mutual Insurance Association in a seven-county area, including Harris County (Houston). Subsequently, thegroup has been reducing policy count in that area by implementing significant rate increases, increased deductibles andstricter underwriting guidelines. The group continues to maintain a strong market presence in Texas and its long-standingagency relationships that have been developed in its 100-plus-year history.

Partially offsetting these positive rating factors is the group's unprofitable underwriting performance as well as decline insurplus over the last five years. During the latest five-year period the group has been impacted by a variety of frequent andsevere weather-related events. As a result, the group has reported sizeable underwriting losses and its five-year average pre-tax operating returns on revenue and equity are negative and compare unfavorably to the private passenger standard auto andhomeowners composite. In an effort to improve these results, management has implemented several corrective actions whichinclude, rate increases, tighter policy verbiage, mandatory and increased deductibles, improved rural spread of risk, andenhanced policy forms. In addition, the group transformed its auto book of business to "preferred" and "ultra-preferred"

Page 2 of 28 Print Date: September 03, 2013

Rating Rationale (Continued ...)programs through revised underwriting guidelines. As a single state writer with all of its business produced in Texas, the groupis exposed to frequent and severe weather-related events as well as judicial, economic and legislative concerns.

The parent company, Germania Farm Mutual Insurance Association operates under Chapter 911 of the Texas Insurance Code.As such, it operates with relative rate and form freedom, which offers a significant competitive advantage by allowing it torespond more quickly to changing market conditions.

In future rating cycles, a continuation of adverse operating results coupled with declining capitalization could result in negativepressure on the outlooks or ratings.

Five Year Rating HistoryBEST'S

Date FSR ICR

12/18/2012 A- a-

12/20/2011 A- a-

12/10/2010 A a

11/13/2009 A a

12/16/2008 A a

View 25 Year Rating History

Key Financial Indicators

Statutory Data ($000)

PeriodEnding

Premiums Written Pre-taxOperatingIncome Net Income

Total AdmittedAssets

Policyholder'sSurplusDirect Net

2012 31,503 29,353 8,210 5,865 68,637 32,157

2011 30,377 28,613 5,925 4,525 64,218 26,069

2010 29,324 27,628 5,805 4,254 65,129 36,401

2009 28,271 26,074 5,661 5,501 58,858 32,118

2008 28,450 24,039 18,949 27,264 56,461 26,484

06/2013 16,945 15,837 915 593 68,391 32,844

06/2012 16,213 15,122 2,670 1,704 62,199 27,859

003840 - Germania Insurance Company

Page 3 of 28 Print Date: September 03, 2013

Key Financial Indicators (Continued ...)

Profitability Leverage Liquidity

PeriodEnding

CombinedRatio

InvestmentYield (%)

Pre-TaxROR (%)

Non-AffiliatedInvestmentLeverage

NPW toPHS

NetLeverage

OverallLiquidity

(%)

OperatingCash-flow

(%)

2012 79.0 3.0 28.4 ... 0.9 2.0 188.1 128.9

2011 86.2 3.0 21.0 ... 1.1 2.5 168.3 139.8

2010 87.4 3.9 21.4 0.3 0.8 1.5 226.7 123.1

2009 88.2 4.2 21.4 0.3 0.8 1.6 220.1 117.3

2008 113.0 8.9 30.9 1.8 0.9 2.0 188.4 96.8

5-Yr Avg 90.5 5.0 25.9 ... ... ... ... ...

06/2013 98.9 3.0 6.2 1.3 0.9 2.0 192.5 102.6

06/2012 87.5 3.5 18.7 1.4 1.0 2.3 181.1 118.6

(*) Within several financial tables of this report, this company is compared against the Commercial Casualty Composite.(*) Data reflected within all tables of this report has been compiled from the company-filed statutory statement.

003840 - Germania Insurance Company

Page 4 of 28 Print Date: September 03, 2013

Business ProfileThe Germania Insurance Company (GIC) was originally formed as an accommodation to its parent, Germania Farm Mutual(GFM), which offers only fire policies. GIC originally offered only personal and farm liability coverage to GFM policyholders.Other lines of business now include commercial property, BOP, commercial liability, commercial auto, standard personal auto,farm and personal umbrella, and inland marine coverage. In 2008, GIC began non-renewing its homeowner and dwelling firepolicies with most policies transferring to the GFM property policy. During the third quarter of 2008, GIC was involved in thereorganization of Germania Mutual Group. GIC declared and paid a dividend and returned capital to its parent, GFM. Thedividend and return of capital was settled with common stock of Germania Fire & Casualty Company (GFC) and GermaniaSelect Insurance Company (GSC), thereby effectively terminating the Germania Insurance Group. A limited amount of servicefee income is generated by Germania General Agency (GGA), a wholly owned subsidiary of GSC, which acts as a generalagent allowing Germania agents to place non-standard risks through other carriers. Beginning in November 1999, GermaniaMutual Group began utilizing a county mutual to give it additional pricing tiers for its existing auto market through GGA. Duringthe third quarter of 2008, GIC contributed capital, including the stock of GGA to Germania Select Insurance Company.Business is developed through the same independent agents that represent the parent, GFM.

Scope of Operations

Total Premium Composition & Growth Analysis

PeriodEnding

Direct PremiumsWritten

Reinsurance PremiumsAssumed

Reinsurance PremiumsCeded Net Premiums Written

($000) (%Chg) ($000) (%Chg) ($000) (%Chg) ($000) (%Chg)

2012 31,503 3.7 ... ... 2,150 21.8 29,353 2.6

2011 30,377 3.6 ... ... 1,765 4.1 28,613 3.6

2010 29,324 3.7 ... ... 1,696 -22.8 27,628 6.0

2009 28,271 -0.6 ... -99.9 2,197 -62.8 26,074 8.5

2008 28,450 19.6 1,492 -98.1 5,902 87.5 24,039 -75.7

5-Yr CAGR ... 5.8 ... -99.9 ... -7.3 ... -21.5

06/2013 16,945 4.5 ... ... 1,108 1.6 15,837 4.7

06/2012 16,213 4.3 ... ... 1,091 21.5 15,122 3.3

Territory

The company is licensed in Texas.

Business Trends

003840 - Germania Insurance Company

Page 5 of 28 Print Date: September 03, 2013

Business Trends (Continued ...)2012 By-Line Business ($000)

Product Line

Direct PremiumsWritten

ReinsurancePremiumsAssumed

ReinsurancePremiums Ceded

Net PremiumsWritten Business

Retention%($000) (%) ($000) (%) ($000) (%) ($000) (%)

Oth Liab Occur 15,377 48.8 ... ... 1,034 48.1 14,343 48.9 93.3

Auto Physical 4,108 13.0 ... ... 96 4.5 4,012 13.7 97.7

Priv Pass Auto Liab 2,923 9.3 ... ... 36 1.7 2,886 9.8 98.8

Allied Lines 2,653 8.4 ... ... 385 17.9 2,268 7.7 85.5

Fire 2,354 7.5 ... ... 337 15.7 2,017 6.9 85.7

Comm'l Auto Liab 1,905 6.0 ... ... 23 1.1 1,882 6.4 98.8

Com'l MultiPeril 1,692 5.4 ... ... 221 10.3 1,471 5.0 87.0

All Other 490 1.6 ... ... 16 0.8 474 1.6 96.7

Total 31,503 100.0 ... ... 2,150 100.0 29,353 100.0 93.2

2012 Top Product Lines of Business (Net Premiums Written)

48.9%

13.7%

9.8%

7.7%

6.9%

6.4%5.0%

1.6%

Oth Liab Occur Priv Pass Auto Liab Fire Com'l MultiPeril

Auto Physical Allied Lines Comm'l Auto Liab All Other

5 Years of Net Premiums Written ($000)

0

6,000

12,000

18,000

24,000

30,000

2008

2009

2010

2011

2012

24,03926,074

27,62828,613

29,353

003840 - Germania Insurance Company

Page 6 of 28 Print Date: September 03, 2013

Business Trends (Continued ...)By-Line Reserve ($000)

Product Line 2012 2011 2010 2009 2008

Oth Liab Occur 12,748 11,897 10,215 7,717 7,614

Auto Physical 292 208 215 182 154

Priv Pass Auto Liab 2,034 1,644 1,497 1,128 808

Allied Lines 418 412 288 286 317

Fire 80 391 45 86 95

Comm'l Auto Liab 440 621 778 338 309

Com'l MultiPeril 156 192 166 214 161

All Other 26 43 105 286 616

Total 16,194 15,408 13,308 10,238 10,073

Market Share / Market Presence

Geographical Breakdown By Direct Premium Writings ($000)

2012 2011 2010 2009 2008

Texas 31,503 30,377 29,324 28,271 28,450

Total 31,503 30,377 29,324 28,271 28,450

003840 - Germania Insurance Company

Page 7 of 28 Print Date: September 03, 2013

Risk ManagementThe following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

Enterprise risk management practices are in place and handled by the Board of Directors, Cabinet, and internal auditors. Theyall have various responsibilities which include, identifying the framework, quantifying and managing risks, as well ascommunicating to all employees. Management views volatility in the common stock market and catastrophe exposure as two oftheir top five risks. In response, a conservative investment strategy and an extensive reinsurance program has beenmaintained to protect surplus from weather-related events and stock market crisis. The group's approach to risk managementappears to be in line with expectations for its business profile. However, A.M. Best anticipates that the underwriting volatilitymay continue to be an issue as the group maintains exposure to both frequency and severity related weather experience forevery natural peril other than earthquake.

003840 - Germania Insurance Company

Page 8 of 28 Print Date: September 03, 2013

Operating PerformanceThe following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

Operating Results: Overall earnings have been volatile during the latest five year period. These results are primarily due tosizeable underwriting losses that could not be completely offset by net investment income and other income. As a result, fiveyear average pre-tax returns on revenue and equity are negative and compare unfavorably to the private passenger standardauto and homeowners composite. In addition, pre-tax operating losses have been reported three of the last five years. Theunfavorable operating results are primarily due to varying weather related events, the financial crisis in 2008 and record lowinterest rates which have resulted in sizeable underwriting losses and flat to declining net investment income. The overallresults have improved in 2012 when compared to 2011 as evidenced by positive pre-tax operating income driven by lowerunderwriting losses, while other income and net investment income continued to remain favorable. Management has takenseveral corrective actions which include significant rate increases, de-emphasizing and refining the property book of business,tighter policy verbiage, mandatory and increased deductibles, improved rural spread of risk, enhanced policy forms andimproved insurance to value. Going forward, A.M. Best anticipates continued volatility in results due to the inherent exposure tofrequent and severe weather related events. However, as management's initiatives gain traction the degree of volatility shoulddecrease.

Profitability Analysis

PeriodEnding

Company Industry Composite

Pre-taxOperating

Income

After-taxOperating

Income Net IncomeTotal

Return

Pre-TaxROR

Returnon PHS

OperatingRatio

Pre-TaxROR

Returnon PHS

OperatingRatio

2012 8,210 5,358 5,865 5,903 28.4 20.3 73.1 6.7 7.9 92.4

2011 5,925 3,988 4,525 4,611 21.0 14.8 80.3 6.5 5.6 93.1

2010 5,805 3,967 4,254 4,230 21.4 12.3 79.9 11.1 9.6 88.2

2009 5,661 5,519 5,501 5,657 21.4 19.3 80.5 15.4 11.5 84.6

2008 18,949 15,981 27,264 12,717 30.9 23.5 101.4 16.8 -1.0 83.6

5-Yr Avg/Tot 44,550 34,813 47,411 33,119 25.9 18.6 82.0 11.3 6.8 88.4

06/2013 915 546 593 593 6.2 15.8 93.5 XX XX XX

06/2012 2,670 1,676 1,704 1,705 18.7 21.5 81.4 XX XX XX

003840 - Germania Insurance Company

Page 9 of 28 Print Date: September 03, 2013

Operating Performance (Continued ...)

Pre-Tax ROR Comparison with Industry Composite

0.0

7.5

15.0

22.5

30.0

37.5

2008 2009 2010 2011 2012

30.9

21.4 21.4 21.0

28.4

16.8 15.4

11.1

6.5 6.7

- Company Pre-Tax ROR - Industry Composite Pre-Tax ROR

* Industry Composite - Commercial Casualty Composite

Return on PHS Comparison with Industry Composite

-5.0

0.0

5.0

10.0

15.0

20.0

2008 2009 2010 2011 2012

23.5

19.3

12.314.8

20.3

-1.0

11.59.6

5.67.9

- Company Return on PHS - Industry Composite Return on PHS

* Industry Composite - Commercial Casualty Composite

Underwriting Results

Underwriting Results: Frequent and severe weather related events have plagued the Texas market place over the last fiveyears. As a result, underwriting losses have been reported in most years and the five year average combined ratio is abovebreak-even and compares unfavorably to the private passenger standard auto and homeowners composite. The exception was2010 where milder weather patterns resulted in favorable net underwriting income and combined ratio below break-even. Thenegative underwriting results were driven by a series of differing weather related events which included wildfires, hail stormsand hurricanes. The unfavorable underwriting performance has continued in 2012, but improved when compared to prior year-end. In an effort to improve underwriting results, management has taken several corrective actions which include; significantrate increases, exposure reduction along Tier 1 and Tier 2 coastal counties, increased and mandatory deductibles, andinsurance-to-value initiatives. In addition, an emphasis on increasing the automobile book of business as well as transformingauto to a "preferred auto program" with stricter underwriting guidelines including credit scoring, re-underwriting of renewalbusiness and expanded rate tiers. Going forward, A.M. Best anticipates that underwriting volatility will continue due to theinherent exposure to frequent and severe weather related events. However, continuation of aggressive underwriting correctiveactions may reduce future volatility.

003840 - Germania Insurance Company

Page 10 of 28 Print Date: September 03, 2013

Underwriting Results (Continued ...)Underwriting Experience

YearNet Undrw

Income ($000)

Loss Ratios Expense Ratios

Div. Pol.Comb.Ratio

PureLoss LAE

Loss &LAE

NetComm

OtherExp.

TotalExp.

2012 5,968 45.0 9.3 54.3 14.9 9.7 24.7 ... 79.0

2011 3,773 49.0 11.0 60.0 15.7 10.5 26.3 ... 86.2

2010 3,265 48.1 11.8 59.9 15.4 12.1 27.6 ... 87.4

2009 3,208 48.4 11.6 60.0 15.6 12.6 28.2 ... 88.2

2008 11,320 53.1 8.1 61.2 17.8 34.0 51.9 ... 113.0

5-Yr Avg 27,534 49.5 9.9 59.4 15.8 15.3 31.1 ... 90.5

06/2013 -104 62.8 11.9 74.7 XX XX 24.2 ... 98.9

06/2012 1,560 52.4 10.3 62.7 XX XX 24.8 ... 87.5

Loss Ratio By Line

Product Line 2012 2011 2010 2009 2008 5-Yr. Avg.

Oth Liab Occur 31.5 37.7 47.3 31.2 28.2 35.3

Auto Physical 63.0 57.0 46.9 61.3 62.0 59.9

Priv Pass Auto Liab 75.1 63.2 73.3 64.8 54.1 59.6

Allied Lines 102.4 97.3 68.8 115.1 72.5 91.2

Fire 23.8 61.6 9.4 47.0 49.6 37.9

Comm'l Auto Liab 26.7 32.9 45.7 27.6 28.3 32.4

Com'l MultiPeril 34.5 33.9 45.8 65.8 92.7 53.4

All Other 36.0 45.8 -0.8 57.6 68.3 55.2

Total 45.0 49.0 48.1 48.4 53.1 49.5

Combined Ratio

0.0

30.0

60.0

90.0

120.0

150.0

2008 2009 2010 2011 2012

61.2 60.0 59.9 60.0 54.3

51.9

28.2 27.6 26.3 24.7

113.0

88.2 87.4 86.279.0

- Loss & LAE Ratio - Expense Ratio - Combined Ratio

2012 Pure Loss Ratio by Product Line

0

20

40

60

80

100

Oth Lia

b Occ

ur

Auto P

hysic

al

Priv P

ass A

uto Li

ab

Allied L

ines

Fire

Comm'l A

uto Li

ab

Com'l M

ultiPeri

l

All Othe

r

31.5

63.0

75.1

102.4

23.826.7

34.5 36.0

003840 - Germania Insurance Company

Page 11 of 28 Print Date: September 03, 2013

Underwriting Results (Continued ...)Direct Loss Ratios By State

2012 2011 2010 2009 2008 5-Yr. Avg.

Texas 42.5 50.0 49.2 48.0 62.2 50.1

Total 42.5 50.0 49.2 48.0 62.2 50.1

Investment Results

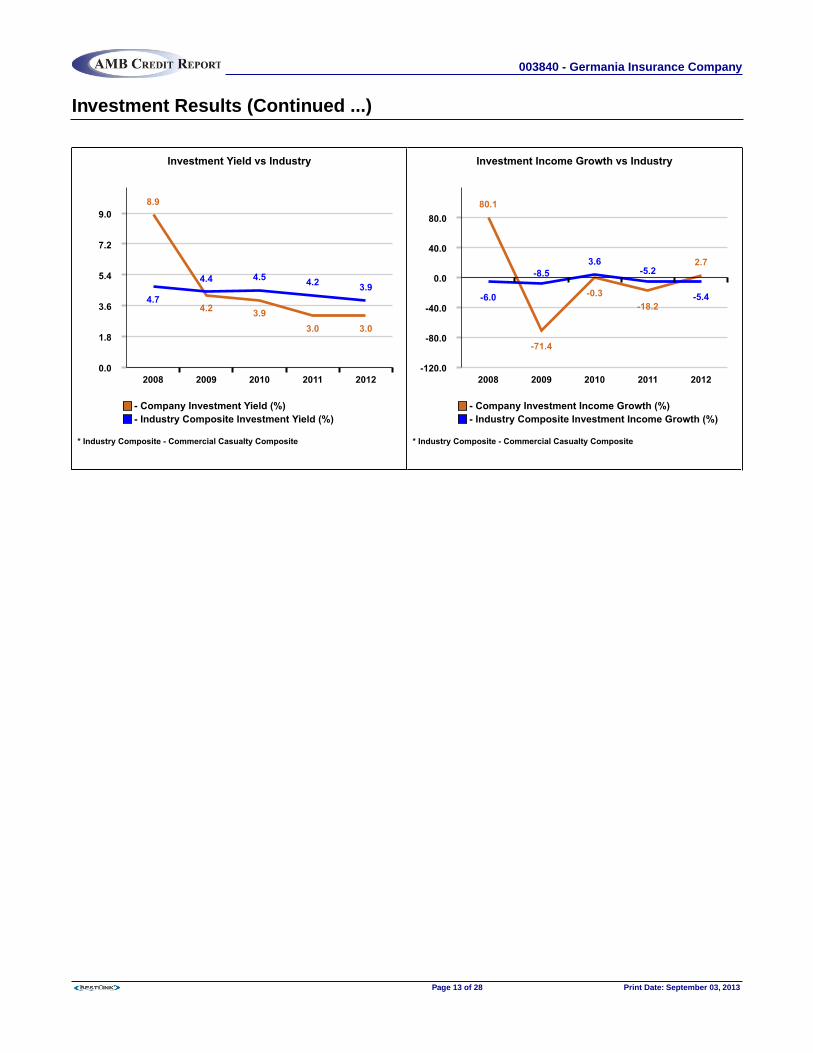

Investment Results: Stable investment earnings have positively contributed to overall operating performance over the pastfive years. The group maintains a conservative investment portfolio with an emphasis on quality, diversification and liquidity. Asa result of record low interest rates, investment yield has declined over the last five years and the five year average is slightlybelow the private passenger standard auto and homeowners composite. Net investment income has generally declined in thelatest five year period, but is favorable and has partially offset sizeable underwriting losses. The current invested asset mix isanchored by its bond portfolio, which represents 87% of total invested assets at year-end 2012, with an emphasis on tax-exempt municipals. The remainder of the current portfolio consists of cash and short-term investments, with a small equityexposure in large cap and value stock funds. In addition, an affiliated life company represents approximately 3% of totalinvested assets at year-end 2012. The portfolio showed moderate effect from the financial market volatility in late 2008.

Investment Gains ($000)

Company Industry Composite

Year

NetInvestment

Income($000)

RealizedCapitalGains($000)

UnrealizedCapitalGains($000)

InvestmentIncome

Growth (%)InvestmentYield (%)

Returnon

InvestedAssets

(%)

TotalReturn

(%)

InvestmentIncome

Growth (%)InvestmentYield (%)

2012 1,709 508 37 2.7 3.0 3.9 4.0 -5.4 3.9

2011 1,664 538 86 -18.2 3.0 4.0 4.2 -5.2 4.2

2010 2,035 287 -24 -0.3 3.9 4.5 4.4 3.6 4.5

2009 2,041 -18 156 -71.4 4.2 4.1 4.5 -8.5 4.4

2008 7,130 11,283 -14,547 80.1 8.9 24.8 4.7 -6.0 4.7

5-Yr Avg/Tot 14,579 12,598 -14,292 -13.4 5.0 9.5 4.4 -4.4 4.4

06/2013 790 47 ... -9.4 3.0 4.1 4.1 XX XX

06/2012 872 28 1 -7.3 3.5 4.4 4.6 XX XX

003840 - Germania Insurance Company

Page 12 of 28 Print Date: September 03, 2013

Investment Results (Continued ...)

Investment Yield vs Industry

0.0

1.8

3.6

5.4

7.2

9.0

2008 2009 2010 2011 2012

8.9

4.2 3.93.0 3.0

4.7

4.4 4.5 4.2 3.9

- Company Investment Yield (%) - Industry Composite Investment Yield (%)

* Industry Composite - Commercial Casualty Composite

Investment Income Growth vs Industry

-120.0

-80.0

-40.0

0.0

40.0

80.0

2008 2009 2010 2011 2012

80.1

-71.4

-0.3-18.2

2.7

-6.0

-8.53.6

-5.2

-5.4

- Company Investment Income Growth (%) - Industry Composite Investment Income Growth (%)

* Industry Composite - Commercial Casualty Composite

003840 - Germania Insurance Company

Page 13 of 28 Print Date: September 03, 2013

Balance Sheet Strength

Capitalization

The following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

Capitalization: Overall risk-adjusted capitalization as measured by Best's Capital Adequacy Ratio (BCAR) is adequate andsupports the current rating. The capital position is reflective of the group's generally favorable reserve development, prudentcatastrophe risk management, and a conservative investment portfolio, which has produced consistent net investment incomeduring the latest five-year period. These factors are partially offset by the group's exposure to weather catastrophe events,elevated underwriting leverage measures, and decline in surplus in three of the last five years. In addition, change in surplusover the last five years has been negative due to significant unrealized capital losses in 2008 as a result of a downturn in thecapital market and unfavorable underwriting performance driven by severe and frequent weather related events along with anextraordinary wildfire event that occurred in 2011. Offsetting this was the realized capital gains and the benefit of favorableincome tax treatment. However, in 2012, surplus appreciation was reported due to improved operating performance coupledwith realized and unrealized capital gains.

Capital Generation Analysis ($000)

Year

Source of Surplus Growth

Pre-taxOperating

Income

RealizedCapitalGains

IncomeTaxes

UnrealizedCapitalGains

NetContributed

CapitalOther

ChangesChange in

PHS

%Changein PHS

2012 8,210 508 2,852 37 ... 185 6,087 23.3

2011 5,925 538 1,937 86 -15,000 57 -10,332 -28.4

2010 5,805 287 1,838 -24 ... 53 4,283 13.3

2009 5,661 -18 142 156 ... -23 5,634 21.3

2008 18,949 11,283 2,968 -14,547 -65,011 -3,168 -55,461 -67.7

5-Yr Total 44,550 12,598 9,737 -14,292 -80,011 -2,897 -49,789 -17.1

06/2013 915 47 370 ... ... 94 688 2.1

06/2012 2,670 28 994 1 ... 84 1,789 6.9

Quality of Surplus ($000)

YearSurplusNotes Other Debt

ContributedCapital

UnassignedSurplus

Year EndPolicyholders

SurplusConditionalReserves

AdjustedPolicyholders

Surplus

2012 ... 9,050 -5,550 28,657 32,157 ... 32,157

2011 ... 9,050 -5,550 22,569 26,069 ... 26,069

2010 ... 9,050 -5,550 32,901 36,401 ... 36,401

2009 ... 9,050 -7,050 30,118 32,118 ... 32,118

2008 ... 9,050 -7,050 24,484 26,484 10 26,494

06/2013 ... 9,050 -5,550 29,344 32,844 25 32,869

06/2012 ... 9,050 -5,550 24,359 27,859 ... 27,859

003840 - Germania Insurance Company

Page 14 of 28 Print Date: September 03, 2013

Underwriting Leverage

Leverage Analysis

Company Industry Composite

YearNPW to

PHSReservesto PHS

NetLeverage

GrossLeverage

NPW toPHS

Reservesto PHS

NetLeverage

GrossLeverage

2012 0.9 0.5 2.0 2.2 0.8 1.5 3.0 3.8

2011 1.1 0.6 2.5 2.7 0.8 1.5 3.0 3.9

2010 0.8 0.4 1.5 1.7 0.7 1.5 2.9 3.7

2009 0.8 0.3 1.6 1.8 0.7 1.5 2.9 3.8

2008 0.9 0.4 2.0 2.3 0.9 1.6 3.3 4.3

06/2013 0.9 0.5 2.0 XX XX XX XX XX

06/2012 1.0 0.6 2.3 XX XX XX XX XX

Current BCAR: 162.4

Net Leverage vs Industry

0.0

0.8

1.6

2.4

3.2

4.0

2008 2009 2010 2011 2012

2.01.6 1.5

2.5

2.0

3.32.9 2.9 3.0 3.0

- Company Net Leverage - Industry Composite Net Leverage

* Industry Composite - Commercial Casualty Composite

Gross Leverage vs Industry

0.0

1.0

2.0

3.0

4.0

5.0

2008 2009 2010 2011 2012

2.31.8 1.7

2.72.2

4.33.8 3.7 3.9 3.8

- Company Gross Leverage - Industry Composite Gross Leverage

* Industry Composite - Commercial Casualty Composite

003840 - Germania Insurance Company

Page 15 of 28 Print Date: September 03, 2013

Underwriting Leverage (Continued ...)Ceded Reinsurance Analysis ($000)

Company Industry Composite

Year

CededReinsurance

Total

BusinessRetention

(%)

ReinsuranceRecoverables

to PHS (%)

CededReinsuranceto PHS (%)

BusinessRetention

(%)

ReinsuranceRecoverables

to PHS (%)

CededReinsuranceto PHS (%)

2012 5,531 93.2 10.5 17.2 82.6 59.1 84.5

2011 5,526 94.2 14.4 21.2 81.6 59.4 84.5

2010 4,615 94.2 8.0 12.7 81.2 57.6 80.4

2009 4,989 92.2 8.7 15.5 82.6 61.2 84.8

2008 6,096 84.2 13.6 23.0 84.6 70.6 97.6

2012 Reinsurance Recoverables ($000)

Paid & UnpaidLosses

Incurred ButNot Reported(IBNR) Losses

UnearnedPremiums

OtherRecoverables *

TotalReinsuranceRecoverables

US Insurers 1,790 1,088 410 ... 3,288

Other Non-Us 5 88 ... ... 93

Total(ex Us Affils) 1,795 1,176 410 ... 3,381

Grand Total 1,795 1,176 410 ... 3,381

* Includes Commissions less Funds Withheld

Loss Reserves

Loss Reserves: Reserves have generally been favorable as evidenced by consistent redundancies on both a calendar andaccident year basis. However, minor deficiencies in accident year of 2008 and 2009, and calendar year of 2009 were reported.Loss reserves are generally short-tailed with duration of approximately 12-24 months. Primary reserve lines include privatepassenger auto and fire, which represent approximately 43% and 32% respectively of total loss reserves at year-end 2012.

Loss and ALAE Reserve Development: Calendar Year ($000)

CalendarYear

OriginalLoss

Reserves

DevelopedReservesThru 2012

Developmentto Original (%)

Developmentto PHS (%)

Developmentto NPE (%)

UnpaidReserves @

12/2012

UnpaidReserves toDevelopment

(%)

2012 14,461 14,461 ... ... 50.0 14,461 100.0

2011 13,674 13,219 -3.3 -1.7 46.9 8,217 62.2

2010 11,856 11,156 -5.9 -1.9 41.1 3,502 31.4

2009 8,986 10,555 17.5 4.9 40.0 1,229 11.6

2008 8,803 9,678 9.9 3.3 15.8 629 6.5

2007 25,922 22,067 -14.9 -4.7 23.8 253 1.1

003840 - Germania Insurance Company

Page 16 of 28 Print Date: September 03, 2013

Loss Reserves (Continued ...)Loss and ALAE Reserve Development: Accident Year ($000)

AccidentYear

Original LossReserves

DevelopedReserves Thru

2012Development to

Original (%)

UnpaidReserves @

12/2012Accident Year

Loss RatioAccident YearComb. Ratio

2012 6,244 6,244 ... 6,244 58.6 83.2

2011 7,336 6,834 -6.8 4,715 61.5 87.7

2010 6,646 5,572 -16.2 2,273 51.4 78.9

2009 4,819 5,432 12.7 600 63.0 91.2

2008 4,944 5,945 20.2 376 70.3 122.1

2007 15,631 13,158 -15.8 63 58.5 89.2

Liquidity

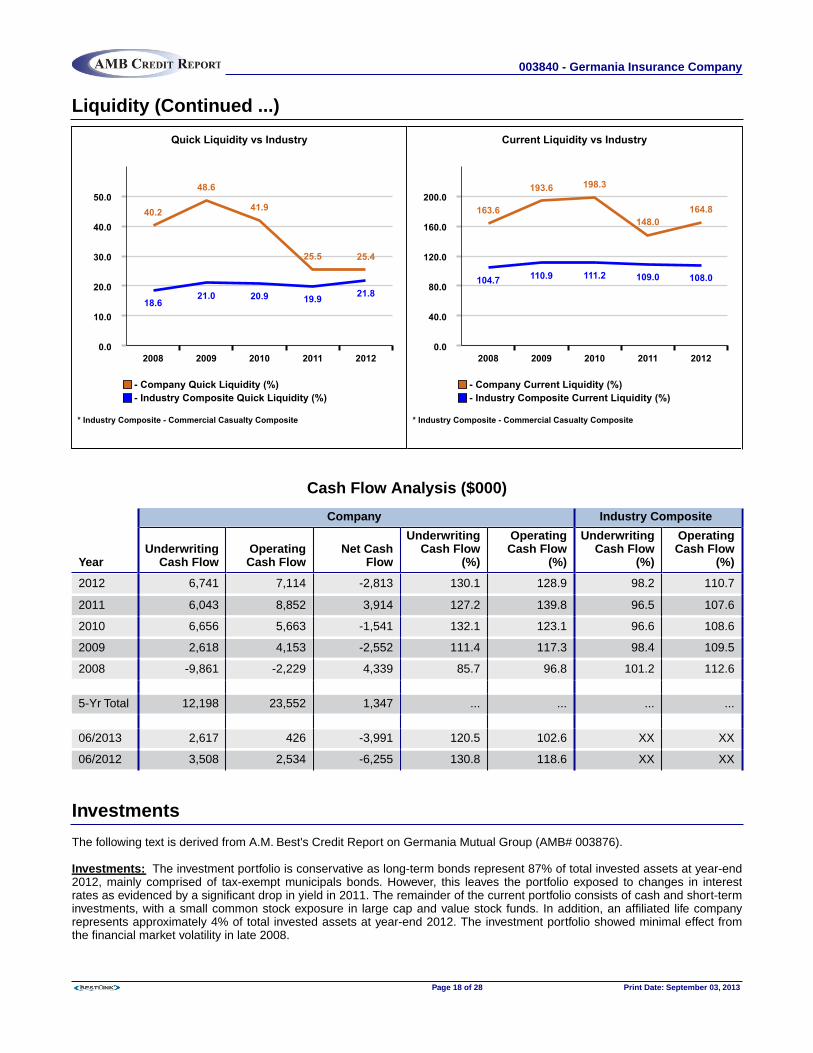

The following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

Liquidity: Liquidity measures are adequate as non-affiliated invested assets exceed overall liabilities. Despite an increase inclaim payouts due to significant weather, fire losses and market volatility in recent years, liquidity measures have been stableand remain comparable to the private passenger standard auto and homeowners composite. Significant negative operatingcash flows were reported in three of the last five years driven by sizeable underwriting losses partially offset by consistentinvestment income. However, operating cash flows were positive in 2010 and 2012 due to favorable underwriting cash flowscoupled with positive investment income.

Liquidity Analysis

Company Industry Composite

Year

QuickLiquidity

(%)

CurrentLiquidity

(%)

OverallLiquidity

(%)

GrossAgents

Balancesto PHS(%)

QuickLiquidity

(%)

CurrentLiquidity

(%)

OverallLiquidity

(%)

GrossAgents

Balancesto PHS (%)

2012 25.4 164.8 188.1 0.5 21.8 108.0 144.9 10.9

2011 25.5 148.0 168.3 0.6 19.9 109.0 144.5 10.3

2010 41.9 198.3 226.7 0.4 20.9 111.2 146.2 9.0

2009 48.6 193.6 220.1 0.5 21.0 110.9 146.0 9.1

2008 40.2 163.6 188.4 0.6 18.6 104.7 140.8 11.9

06/2013 XX 160.1 192.5 0.5 XX XX XX XX

06/2012 XX 150.0 181.1 0.5 XX XX XX XX

003840 - Germania Insurance Company

Page 17 of 28 Print Date: September 03, 2013

Liquidity (Continued ...)

Quick Liquidity vs Industry

0.0

10.0

20.0

30.0

40.0

50.0

2008 2009 2010 2011 2012

40.2

48.6

41.9

25.5 25.4

18.621.0 20.9 19.9 21.8

- Company Quick Liquidity (%) - Industry Composite Quick Liquidity (%)

* Industry Composite - Commercial Casualty Composite

Current Liquidity vs Industry

0.0

40.0

80.0

120.0

160.0

200.0

2008 2009 2010 2011 2012

163.6

193.6 198.3

148.0164.8

104.7 110.9 111.2 109.0 108.0

- Company Current Liquidity (%) - Industry Composite Current Liquidity (%)

* Industry Composite - Commercial Casualty Composite

Cash Flow Analysis ($000)

Company Industry Composite

YearUnderwritingCash Flow

OperatingCash Flow

Net CashFlow

UnderwritingCash Flow

(%)

OperatingCash Flow

(%)

UnderwritingCash Flow

(%)

OperatingCash Flow

(%)

2012 6,741 7,114 -2,813 130.1 128.9 98.2 110.7

2011 6,043 8,852 3,914 127.2 139.8 96.5 107.6

2010 6,656 5,663 -1,541 132.1 123.1 96.6 108.6

2009 2,618 4,153 -2,552 111.4 117.3 98.4 109.5

2008 -9,861 -2,229 4,339 85.7 96.8 101.2 112.6

5-Yr Total 12,198 23,552 1,347 ... ... ... ...

06/2013 2,617 426 -3,991 120.5 102.6 XX XX

06/2012 3,508 2,534 -6,255 130.8 118.6 XX XX

Investments

The following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

Investments: The investment portfolio is conservative as long-term bonds represent 87% of total invested assets at year-end2012, mainly comprised of tax-exempt municipals bonds. However, this leaves the portfolio exposed to changes in interestrates as evidenced by a significant drop in yield in 2011. The remainder of the current portfolio consists of cash and short-terminvestments, with a small common stock exposure in large cap and value stock funds. In addition, an affiliated life companyrepresents approximately 4% of total invested assets at year-end 2012. The investment portfolio showed minimal effect fromthe financial market volatility in late 2008.

003840 - Germania Insurance Company

Page 18 of 28 Print Date: September 03, 2013

Investments (Continued ...)Investment Leverage Analysis (% of PHS)

Company Industry Composite

YearClass 3-6

BondsReal Estate /Mortgages

OtherInvestedAssets

CommonStock

Non -Affiliated

InvestmentLeverage

AffiliatedInvestments

Class 3-6Bonds

CommonStock

2012 ... ... ... ... ... ... 7.1 10.3

2011 ... ... ... ... ... ... 7.4 9.5

2010 0.3 ... ... ... 0.3 ... 7.2 9.0

2009 0.3 ... ... ... 0.3 ... 6.0 8.2

2008 1.8 ... ... ... 1.8 ... 5.4 9.1

Investments - Bond Portfolio

2012 Distribution By Maturity

Years

0-1 1-5 5-10 10-20 20+

YearsAverageMaturity

Government 0.2 3.1 2.6 0.2 ... 5.3

Government Agencies & Muni. 7.7 19.8 26.9 6.3 8.8 8.3

Industrial & Misc. 5.0 13.1 6.0 0.2 ... 3.7

Total 12.9 36.0 35.5 6.7 8.8 7.0

003840 - Germania Insurance Company

Page 19 of 28 Print Date: September 03, 2013

Investments - Bond Portfolio (Continued ...)

Bond Distribution By Issuer Type

2012 2011 2010 2009 2008

Bonds (000) 57,506 50,675 54,698 48,246 43,954

US Government 6.4 1.4 3.9 3.9 2.3

State/Special Revenue-US 72.0 73.2 70.5 74.2 70.4

Industrial and Misc-US 21.7 25.5 25.6 21.9 27.3

2012 Bond Distribution By Issuer Type

6.4%

72.0%

21.7%US GovernmentState/Special Revenue-USIndustrial and Misc-US

Bond Percent Private vs Public

2012 2011 2010 2009 2008

Private Issues 3.1 2.1 0.9 1.0 ...

Public Issues 96.9 97.9 99.1 99.0 100.0

Bond Quality Percent

2012 2011 2010 2009 2008

Class 1 98.8 99.1 98.6 99.0 97.8

Class 2 1.2 0.9 1.2 0.8 1.3

Class 3 ... ... ... ... 0.8

Class 4 ... ... ... ... ...

Class 6 ... ... 0.2 0.2 0.1

003840 - Germania Insurance Company

Page 20 of 28 Print Date: September 03, 2013

Investments - Other Invested Assets

2012 2011 2010 2009 2008

Other Invested Assets(000) 1,707 4,519 606 2,147 4,699

Cash 51.8 81.4 -99.9 -9.6 -77.5

Short-Term 48.2 18.6 249.3 109.6 177.5

Schedule BA Assets ... ... 0.1 ... ...

003840 - Germania Insurance Company

Page 21 of 28 Print Date: September 03, 2013

HistoryThis company was incorporated on April 19, 1978 under the laws of Texas and began business on November 29, 1978.

During the third quarter of 2008, GIC was involved in the reorganization of Germania Mutual Group. GIC declared and paid adividend of $39,565,464 and returned capital of $16,753,500 to its parent, GFM. The dividend and return of capital was settledwith common stock of Germania Fire & Casualty Company (GFC) and Germania Select Insurance Company (GSC). Alsoduring the third quarter of 2008, GIC redeemed 100% of its outstanding preferred stock for $9,050,000. This stock is currentlyin Treasury. GIC also issued another 500,000 shares of $1.00 par common stock to its sole stockholder, GFM. Currently, GIChas 1,000,000 shares of common stock authorized, issued and outstanding. GIC has 181,000 shares of preferred stockauthorized with 90,500 issued and in Treasury.

ManagementAdministration and operations of the company's affairs is under the same management as the parent organization, GermaniaFarm Mutual Insurance Association, and GFM's other subsidiaries, Germania Life Insurance Company (incorporated in late1983), Germania Fire & Casualty Company (incorporated in 1985) and Germania Select Insurance Company (incorporated in2002). All of the officers have been affiliated with the well established parent company for many years.

Management and service contracts and all cost sharing arrangements involving GIC consist of a monthly managementagreement between GIC and its parent, GFM. All previous management and facilities agreements between GIC and GFC orGSC have been cancelled.

Officers And Directors

OfficersPresident Paul EhlertVice President Blake Lovelace

Vice President Gary WeissSecretary and Treasurer Derrell Krebs

DirectorsRalph BeadlePaul EhlertBruce E. GermerFredda Gibbs LemonsDwayne W. Herring

Clarence H. Herring, Jr.Derrell KrebsBlake LovelaceDon McAfeeGary Weiss

Regulatory

An examination of the financial condition was made as of December 31, 2008, by the insurance department of Texas. The2012 annual independent audit of the company was conducted by Jaynes, Reitmeier, Boyd & Therrell, PC. The annualstatement of actuarial opinion is provided by John F. Butcher, FCAS, MAAA, Tillinghast Towers Perrin.

Reinsurance

The following text is derived from A.M. Best's Credit Report on Germania Mutual Group (AMB# 003876).

For 2012, Germania Mutual Group maintains catastrophe coverage through a catastrophe per risk excess of loss that includesGermania Farm Mutual (GFM), Germania Insurance Company (GIC), Germania Fire & Casualty Company (GFC), GermaniaSelect Insurance Company (GSC) and Texas Heritage Insurance Company (THC). This reinsurance program provides $357.5

003840 - Germania Insurance Company

Page 22 of 28 Print Date: September 03, 2013

Reinsurance (Continued ...)

million in coverage excess of a $17.5 million retention, with 100% placement on each layer. One automatic reinstatement is ineffect for each of the first four layers up to the $150 million limit. Concurrently, there is an underlying internal catastrophecontract between GFM and THC covering 100% of $8 million excess of $5.5 million ultimate net loss to THC. Also, there is athree year structured weather aggregate contract to address potential frequency of storm events, other than hurricanes. Thereis a $80 million annual aggredate deductible with a $1 million per occurrence franchise deductible. The per occurrence limit perevent subject to the contract is $17.5 million. Maximum recovery in any one year is $30 million and for the three year period themaximum recovery is $75 million. Property per risk excess of loss reinsurance is maintained for GFM, GIC and THC forrecovery of claims above a retention of $1 million up to $5 million. Facultative arrangements are available for risks in excess of$5 million. Casualty per risk excess of loss reinsurance is maintained for GIC, GFC and GSC with $700,000 of coverage inexcess of a $300,000 net retention for any one casualty risk and which includes an additional $4 million limit for ECO, XPL andclash cover losses. Since 1999, GIC has offered personal and farm umbrella coverage. Limits from $1 million up to $5 millionare offered. These programs are reinsured under a quota share reinsurance agreement. The first million is covered at 95% andthe remaining at 100%.

003840 - Germania Insurance Company

Page 23 of 28 Print Date: September 03, 2013

Balance Sheet ($000)

Admitted Assets 12/31/2012 12/31/2011 2012 % 2011 %

Bonds 57,506 50,675 83.8 78.9

Preferred Stock ... ... ... ...

Common Stock ... ... ... ...

Cash & Short-Term Invest 1,707 4,519 2.5 7.0

Real estate, investment ... ... ... ...

Derivatives ... ... ... ...

Other Non-Affil Inv Asset ... ... ... ...

Investments in Affiliates ... ... ... ...

Real Estate, Offices ... ... ... ...

Total Invested Assets 59,212 55,194 86.3 85.9

Premium Balances 6,899 6,683 10.1 10.4

Accrued Interest 387 346 0.6 0.5

Life department ... ... ... ...

All Other Assets 2,139 1,994 3.1 3.1

Total Assets 68,637 64,218 100.0 100.0

Liabilities & Surplus 12/31/2012 12/31/2011 2012 % 2011 %

Loss & LAE Reserves 16,194 15,408 23.6 24.0

Unearned Premiums 15,020 14,584 21.9 22.7

Conditional Reserve Funds ... ... ... ...

Derivatives ... ... ... ...

Life department ... ... ... ...

All Other Liabilities 5,266 8,156 7.7 12.7

Total Liabilities 36,480 38,148 53.1 59.4

Surplus notes ... ... ... ...

Capital & Assigned Surplus 3,500 3,500 5.1 5.5

Unassigned Surplus 28,657 22,569 41.8 35.1

Total Policyholders' Surplus 32,157 26,069 46.9 40.6

Total Liabilities & Surplus 68,637 64,218 100.0 100.0

003840 - Germania Insurance Company

Page 24 of 28 Print Date: September 03, 2013

Interim Balance Sheet ($000)

Admitted Assets 03/31/2013 06/30/2013

Bonds 60,576 58,716

Cash & Short-Term Invest -3,459 -2,284

Other Investments ... ...

Total Invested Assets 57,118 56,431

Premium Balances 7,049 7,532

Accrued Interest 504 436

Reinsurance Funds 61 134

All Other Assets 3,140 3,858

Total Assets 67,871 68,391

Liabilities & Surplus 03/31/2013 06/30/2013

Loss & LAE Reserves 15,203 17,716

Unearned Premiums 15,190 16,126

Conditional Reserve Funds 22 25

All Other Liabilities 3,208 1,680

Total Liabilities 33,623 35,547

Capital & Assigned Surp 3,500 3,500

Unassigned Surplus 30,749 29,344

Total Policyholders' Surplus 34,249 32,844

Total Liabilities & Surplus 67,871 68,391

003840 - Germania Insurance Company

Page 25 of 28 Print Date: September 03, 2013

Summary Of 2012 Operations ($000)

Statement of Income 12/31/2012 Funds Provided from Operations 12/31/2012

Premiums earned 28,917 Premiums collected 29,159

Losses incurred 13,024 Benefit & loss-related pmts 12,458

LAE incurred 2,683

Undwr expenses incurred 7,242 LAE & undwr expenses paid 9,960

Other expenses incurred ... Other income / expense ...

Dividends to policyholders ... Dividends to policyholders ...

Net underwriting income 5,968 Underwriting cash flow 6,741

Net transfer ...

Net investment income 1,709 Investment income 2,059

Other income/expense 533 Other income/expense 533

Pre-tax operating income 8,210 Pre-tax cash operations 9,333

Realized capital gains 508

Income taxes incurred 2,852 Income taxes pd (recov) 2,220

Net income 5,865 Net oper cash flow 7,114

003840 - Germania Insurance Company

Page 26 of 28 Print Date: September 03, 2013

Interim Income Statement ($000)

Period Ended06/30/2013

Period Ended06/30/2012

Increase /Decrease

Premiums earned 14,731 14,243 488

Losses incurred 9,248 7,459 1,789

LAE incurred 1,752 1,466 286

Undwr expenses incurred 3,835 3,758 77

Other expenses incurred ... ... ...

Dividends to policyholders ... ... ...

Net underwriting income -104 1,560 -1,664

Net investment income 790 872 -82

Other income/expense 229 238 -9

Pre-tax operating income 915 2,670 -1,755

Realized capital gains 47 28 20

Income taxes incurred 370 994 -625

Net income 593 1,704 -1,111

Interim Cash Flow ($000)

Period Ended06/30/2013

Period Ended06/30/2012

Increase /Decrease

Premiums collected 15,401 14,899 502

Benefit & loss-related pmts 7,885 6,541 1,344

LAE & undwr expenses paid 4,899 4,849 50

Dividends to policyholders ... ... ...

Underwriting cash flow 2,617 3,508 -891

Net transfer ... ... ...

Investment income 1,003 1,016 -13

Other income/expense 229 238 -9

Pre-tax cash operations 3,849 4,762 -913

Income taxes pd (recov) 3,423 2,228 1,195

Net oper cash flow 426 2,534 -2,108

003840 - Germania Insurance Company

Page 27 of 28 Print Date: September 03, 2013

A Best's Financial Strength Rating opinion addresses the relative ability of an insurer to meet its ongoing insurance obligations. The ratings are not assigned to specific insurance policies orcontracts and do not address any other risk, including, but not limited to, an insurer's claims-payment policies or procedures; the ability of the insurer to dispute or deny claims payment ongrounds of misrepresentation or fraud; or any specific liability contractually borne by the policy or contract holder. A Financial Strength Rating is not a recommendation to purchase, hold orterminate any insurance policy, contract or any other financial obligation issued by an insurer, nor does it address the suitability of any particular policy or contract for a specific purpose orpurchaser.

A Best's Debt/Issuer Credit Rating is an opinion regarding the relative future credit risk of an entity, a credit commitment or a debt or debt-like security.

Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. These credit ratings do not address any other risk, including but not limited to liquidityrisk, market value risk or price volatility of rated securities. The rating is not a recommendation to buy, sell or hold any securities, insurance policies, contracts or any other financialobligations, nor does it address the suitability of any particular financial obligation for a specific purpose or purchaser.

In arriving at a rating decision, A.M. Best relies on third-party audited financial data and/or other information provided to it. While this information is believed to be reliable, A.M. Best does notindependently verify the accuracy or reliability of the information. Any and all ratings, opinions and information contained herein are provided "as is," without any express or implied warranty.

Visit http://www.ambest.com/ratings/notice.asp for additional information or http://www.ambest.com/terms.html for details on the Terms of Use.

Copyright © 2013 A.M. Best Company, Inc. All rights reserved.

No part of this report may be reproduced, distributed, or stored in a database or retrieval system, or transmitted in any form or by any means without the prior written permission of the A.M.Best Company. While the data in this report was obtained from sources believed to be reliable, its accuracy is not guaranteed.

003840 - Germania Insurance Company

Page 28 of 28 Print Date: September 03, 2013