€¦ · unit 2: saving and ... wisely and lived within their means. ... to learn more. spending...

TRANSCRIPT

Made possible through the generous support of the

National Headquarters1275 Peachtree St. NE

Atlanta, GA 30309www.bgca.org • (404) 487-5700

© 2010 Boys & Girls Clubs of America • 1640-10

www.MoneyMattersMakeItCount.com

Copyright © 2010 Boys & Girls Clubs of America • 1640-10

Teen Personal

Finance Guide

iiiii

Money M

atters: Make it C

ountS

M | Teen GuideM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de

UniT 1: BUdGeTinG and LivinG WiThin YoUr MeanS . . . . . . . . 3

My Savings Goals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

I Want It, I Need It . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Analyzing Spending Habits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Proof of Purchase . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Budget This! . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Budgeting Plus 10 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Put It in the Bank . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

UniT 2: SavinG and inveSTinG: PUT YoUr MoneY To Work . . 17

Comparing Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Stock Scramble . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

UniT 3: PLanninG for CoLLeGe: CoLLeGe aS an inveSTMenT. . 29

Personal Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Career Path . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Ready for College! . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

UniT 4: CrediT and deBT: ProTeCT YoUr fUTUre . . . . . . . . . . 43

UniT 5: enTrePreneUrShiP: MakinG iT on YoUr oWn . . . . . . 47

Entrepreneur Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

anSWer keY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Contents

important Guidelines for Photocopying

Limited permission is granted free of charge to photocopy all pages of this guide that are required for use by Boys & Girls Club staff members. Only the original manual purchaser/owner may make such photocopies. Under no circumstances is it permissible to sell or distribute on a commercial basis multiple copies of material reproduced from this publication.

Copyright © 2010 Boys & Girls Clubs of America

All rights reserved. Printed in the United States of America. Except as expressly provided above, no part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission of the publisher.

Boys & Girls Clubs of America 1275 Peachtree St. NE Atlanta, GA 30309–3506 404–487–5700

1

Money M

atters: Make it C

ount | Teen Guide | IN

TRO

dU

CTIO

N

You’re never too young – or too old – to learn how to manage

money and make smart financial decisions. Some very wealthy

people are wealthy not because they won the lottery or inherited

millions, but because they managed their money well, invested

wisely and lived within their means. And you can, too.

Within this guide are useful tricks, terms and tools you’ll need

to build a solid financial future. You won’t find any get–rich–quick

schemes, but you will find the long–term strategies that will help

you make smart decisions that keep your money safe and, over

time, even help it grow.

There’s more online! When you see one of the icons below, hop over to www.moneymattersmakeitcount.com to learn more.

Spending Plan Saving and Investing

Plan for College Credit and debt Entrepreneurship

Introduction

Legend

3

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

S

BUdGeTinG and LivinG WiThin YoUr MeanS

My Saving goalSList some things in the appropriate category below that you would like to be able to afford.

• Short–term financial Goals: Items that you can save for now or within a few months (e.g., an MP3 player, a cell phone).

• Long–term financial Goals: Items that you can save enough money for in a few years (e.g., a car, college tuition).

Unit 1

Short–Term financial Goals

Short–term goals are those you can put money aside for in a bank account and take the money out when you have

enough for your goal.

item Cost item Cost

Long–Term financial Goals

Long–term goals are those for which you put money aside for a year or more until

you have enough for your goal.

1.

2.

3.

4.

5.

6.

54

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

FocuS on: PerSonal SacriFiceSSaving money is one of the most important steps to achieving financial freedom. By saving money a little at a time, you get the freedom of purchasing big–ticket items like a car, a house or a college education. One paycheck is never enough to pay for one of those big expenses, but by putting a little something away each time you earn, your purchasing power grows and grows. A savings account also gives you peace of mind – because you know you have a cushion in case of unexpected expenses.

There are three good ways to save up money for the important stuff:

• Saving regularly

• Increasing your earnings

• Making smart choices

A budget is a plan you make in advance for how you will spend your income. You can take time to investigate your spending options and carefully decide how to meet your savings goals, pay for your needs and prioritize what you want to buy. In an ideal budget, every penny is spoken for – but that doesn’t mean you never get to have any fun. For example, you can put a certain amount in your monthly budget for entertainment. As long as your needs are being met and money is going toward savings, then it’s a great idea to include things like movies or dining out in your budget.

At some point, you’re going to be in a situation where you will have to make a smart choice and prioritize something you need over something you want. It’s not fun to think about, but figuring out what things you could give up in order to increase your savings can help you avoid a lot of anxiety in the future.

QueStionS:Why is saving important?

_______________________________________

How can you increase your earnings?

_______________________________________

How does a budget help you make smart choices?

_______________________________________

i Want it, i need itTo live within your means, you need to first figure out what’s really important to you. The first step to taking control of your financial future is learning to tell the difference between the things you want and the things you need.

Anticipate items you will want and need during your first year out of high school:

items i Will Want items i Will need

______________ _______________

______________ _______________

______________ _______________

______________ _______________

WantS vS. needSSo what’s the difference between a want and a need? A want is something you would like, but can live without. A need is a necessity — something you can’t live without like food, shelter and clothing.

WanTS needS

Car Groceries

Cell phone Place to live

Music player Clothes

Tv Medical care

Expensive sneakers

QueStionS:When does a want become a need?

_______________________________________

When would a car move from a want to a need?

_______________________________________

ProoF oF PurchaSeAnswer the questions below in the column on the right.

analyzing SPending habitSHave you ever stopped and wondered why you buy the things you do? Think about the last big–ticket purchase you made. Why did you spend your money on that? did a friend suggest it? did you see an ad and feel you had to have it? Were you feeling low and you wanted something that might make you feel better? Understanding your own motivations and spending habits can help you resist unnecessary temptations.

Use this spending tracker to keep track of where you’re spending your money. Make a point of writing down each purchase you make.

You can also find this Spending Tracker on the Money Matters website, so you can track your spending in your Personal Locker.

The last unnecessary purchase (a “want”) I made was:

It cost:

I got the money from:

The main reason that I purchased that item was: Friend suggested

Made me feel good

It was just so cool

don’t know

Other (specify)

If I hadn’t spent $______ on ______ I could:

Clothing Transportation Personal Care

Date Amount Item Date Amount Item Date Amount Item

Food Music/Electronics Other

Date Amount Item Date Amount Item Date Amount Item

76

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

Tips for Managing spending:1. Use direct deposit to have your paycheck automatically put into your account.2. Make a budget and stick to it.3. Purchase items on sale.4. Make a list before going shopping.5. Buy only items that you need.

FocuS on: incoMeIncome is any money that you receive. You can receive income from a full–time or part–time job, birthday gifts, an allowance, scholarships, prizes or from proceeds/profit you make from items you sell – cookies, clothes, etc. Money from a regular job is money you can count on. Some jobs will pay you an hourly rate, and you’ll receive a paycheck every week or every two weeks. Other jobs will pay you an annual salary, and that amount will get divided into regular pay periods, such as one every two weeks. Other jobs are contract work – meaning you get paid for a specific project and a specific amount of time. For example, you might decide to be a painter or hair stylist and get paid for each job you do.

Time + Talents + opportunities = income

during the school year, it’s difficult to find free time after school, homework, sports and other activities. But if you manage your time well, you probably can find some free hours during the week or on the weekend.

When do you have free time during the week or on weekends?

_______________________________________

Instead of hanging out with friends or relaxing at home, you could spend some of those free hours making use of one or more of your talents to earn extra income. Almost anything you’re good at doing or making can be a profitable talent. Some may not seem like a talent to you – but it would be valued by others. For example, maybe you’re great with animals, but you never thought much about it. Fact is you could make extra money walking dogs or pet sitting.

What talents do you have? What are you good at doing or making? What kinds of activities do you enjoy?

____________________ ________________________ _______________________

Now that you’ve identified some windows of time when you’re available and some things you’re good at or like doing, it’s just a matter of finding the right opportunities. If you have time on the weekends you could seek opportunities to work at a movie theater, in a restaurant, at a clothing store or as a tutor. To find these opportunities, you could look in the “Help Wanted” section of the local newspaper or conduct an online job search. Or if you enjoy being outside, and have access to garden tools and a lawnmower, you could make extra money cutting yards or gardening. You can try to find these opportunities by putting up flyers around your neighborhood.

Where will you look for opportunities to earn extra income? What steps will you take to find these opportunities, or to help these opportunities find you?

____________________ ________________________ _______________________

groSS Pay vS. net Pay If you don’t already have one, you soon will have a job. Which means you soon will have a paycheck. There are two ways to look at a paycheck. It comes down to gross vs. net.

Your gross pay or total pay is always larger than your net pay or take–home pay. If you get paid hourly, your gross pay is your hourly rate times the number of hours you worked. But you usually do not receive a paycheck equal to your gross pay. Where does the rest of the money go?

Out of your gross pay, several deductions are removed by your employer (see “Understanding a Paycheck and Deductions” below). Your net pay is the amount that’s actually on the check you receive. Net pay is gross pay minus all of those deductions. When you’re calculating your monthly budget, you should only include net pay as your income.

underStanding a Paycheck and deductionS Everyone’s paycheck and deductions will be slightly different, but the following are the most common deductions:

federal Tax: Federal taxes withheld from each paycheck. This money is spent by the federal government on a wide variety of programs.

Social Security Tax: You pay 6.2 percent* of your salary to FICA. It stands for Federal Insurance Contributions Act. The good news is that your employer contributes an additional 6.2 percent* into FICA. That means a total of 12.4 percent* of your salary is automatically being put into the Social Security system. When you retire, or in case of a disability, you’ll have the opportunity to receive Social Security benefits.

State Tax: State taxes withheld from each paycheck. This money is used by your state. In some locations, but not many, you will also see a deduction of taxes for your city or town. There are also a few states that don’t have a state income tax.

Medicare: Medicare deductions are primarily used to help senior citizens with their medical expenses. 1.45 percent* of your income goes toward Medicare, and your employer matches an additional 1.45 percent*.

401(k): Some employers will automatically deduct a certain amount of your pre–tax paycheck and put it toward a retirement plan. This money is still yours – it’s simply being saved up for you for when you retire, and in some cases, employers will match your 401(k) contributions up to a limit.

insurance: If you receive health insurance from your job, a part of that cost is usually deducted from your paycheck. Your employer typically pays the majority of the cost of your health insurance.

*Percentages indicated above are valid rates at the time of printing.

98

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

Pay yourSelF FirSt! Have you ever heard the expression, “Living paycheck to paycheck?” Unfortunately, many Americans would describe themselves as living exactly that way. Living paycheck to paycheck means that whatever money comes in each month, all of that money is in turn spent just to cover monthly expenses, with nothing left over.

To avoid living this way, you have to do two things. First, as you learned in the last section of this guide, you need to make personal sacrifices by recognizing the difference between Needs and Wants, and cutting back on unnecessary expenses. Second, you must always follow the 10 percent rule and pay yourself first.

the 10 Percent rule The 10 percent rule is easy: when you receive any income at all— whether it’s birthday cash or a paycheck from your job — 10 percent of that amount goes into a savings account. Any budget you make should list savings as your first monthly expense, and 10 percent of your net (after tax) income should be allocated toward it.

Setting aside 10 percent of your net income in a savings account can do even more than help you save up for big long–term expenses; one of the most important benefits is that this 10 percent acts as a safety net. If you are living paycheck to paycheck, without putting anything aside, you will have no money left over in case of emergency or unexpected expenses; for example, if you lose your job, you will not have the safety net of that savings account while you look for a new job.

QueStion: If you took home a net pay of $700 a month, how much money would you immediately set aside for savings?

_______________________________________

FocuS on: exPenSeS Expenses are anything you spend money on: food, transportation, rent, shoes, video games, etc. To make a budget, you need to classify all of your expenses. You don’t have to list every item of food you buy or every grocery store you go to; instead, you can have one category called “Groceries” and budget a certain amount to cover all expenses that pertain to groceries.

Although everyone’s list of expense types might be a bit different, there are some common expense categories that apply to most adults. Here’s a list to get you started when planning your own budget:

Common expense Categories:

Essential Expenses (Money you must spend)

Savings: Set aside 10 percent of your income in a savings account; this should always be your first expense.

home: Monthly rent or mortgage payment, including insurance and any maintenance.

Groceries: Food purchased to be prepared or eaten at home.

Transportation: Gas, cost of public transportation or the cost for maintaining a car, including insurance.

Utilities: Electric bills, water, sewage, cable television, mobile phone and home phone bills.

Medical: doctor visits, prescriptions, urgent care.

Discretionary Expenses (Money that you’d like to spend but don’t have to spend)

eating out: Money spent on food prepared out of the house, including food purchased at restaurants or coffee at coffee shops.

health and fitness: Gym memberships; non-essential doctor, dentist or eye care visits.

entertainment: Movie tickets or dvd rentals, concert tickets or any other money spent on recreation.

Shopping: Clothing, electronics, books or sporting goods.

Personal care: Haircuts or styling, manicures or pedicures.

Gifts and donations: Gifts for friends or family or donations to charity.

1110

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM |

Tee

n G

uide

|

U

NIT

1:

BU

dG

ETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

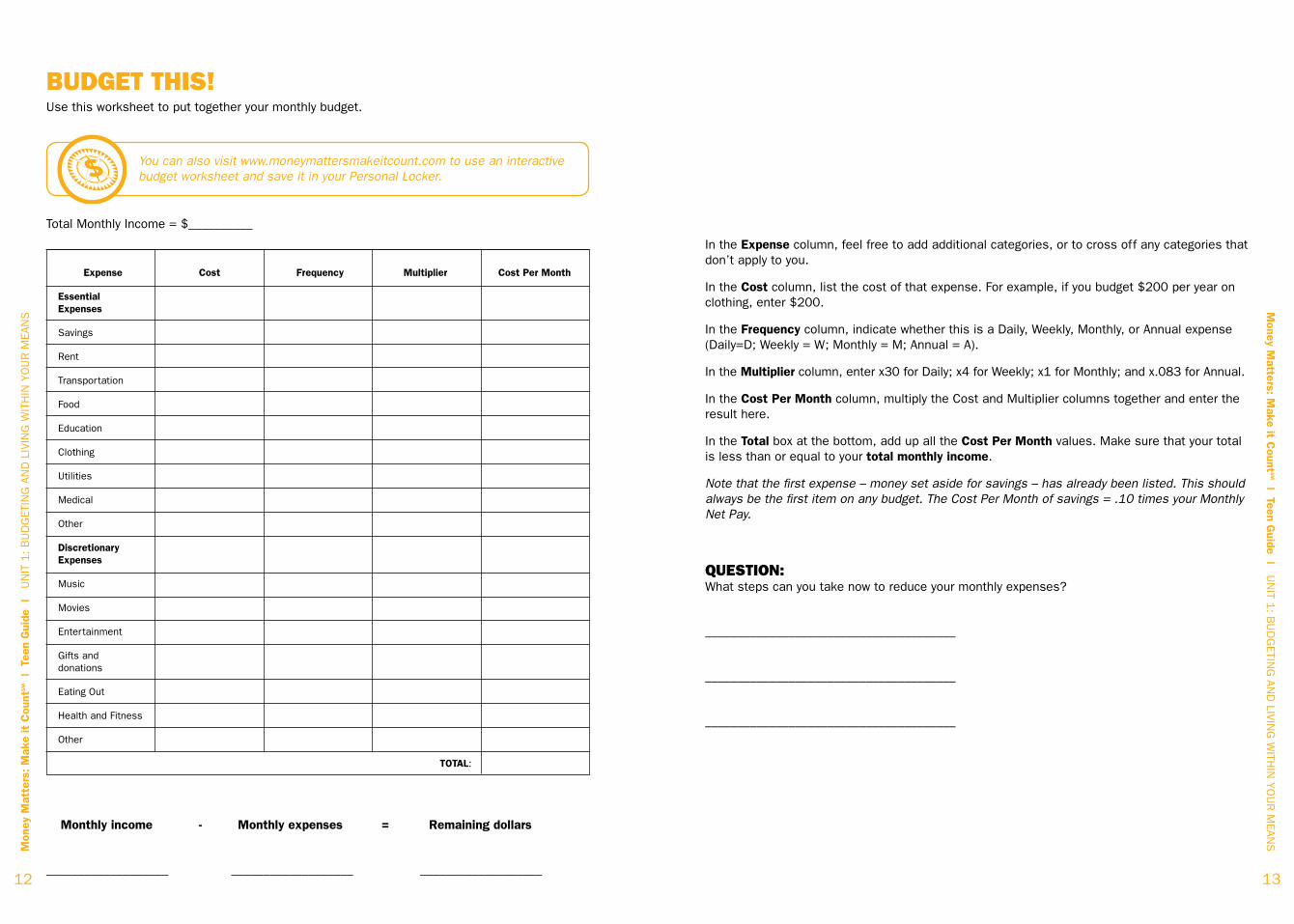

In the expense column, feel free to add additional categories, or to cross off any categories that don’t apply to you.

In the Cost column, list the cost of that expense. For example, if you budget $200 per year on clothing, enter $200.

In the frequency column, indicate whether this is a daily, Weekly, Monthly, or Annual expense (Daily=D; Weekly = W; Monthly = M; Annual = A).

In the Multiplier column, enter x30 for Daily; x4 for Weekly; x1 for Monthly; and x.083 for Annual.

In the Cost Per Month column, multiply the Cost and Multiplier columns together and enter the result here.

In the Total box at the bottom, add up all the Cost Per Month values. Make sure that your total is less than or equal to your total monthly income.

Note that the first expense – money set aside for savings – has already been listed. This should always be the first item on any budget. The Cost Per Month of savings = .10 times your Monthly Net Pay.

QueStion: What steps can you take now to reduce your monthly expenses?

_______________________________________

_______________________________________

_______________________________________

budget thiS! Use this worksheet to put together your monthly budget.

You can also visit www.moneymattersmakeitcount.com to use an interactive budget worksheet and save it in your Personal Locker.

Total Monthly Income = $__________

expense Cost frequency Multiplier Cost Per Month

essential expenses

Savings

Rent

Transportation

Food

Education

Clothing

Utilities

Medical

Other

discretionary expenses

Music

Movies

Entertainment

Gifts and donations

Eating Out

Health and Fitness

Other

ToTaL:

Monthly income - Monthly expenses = remaining dollars

___________________ ___________________ ___________________1312

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

In the expense column, feel free to add an additional category. In the Cost Per expense column, list how much you want to be spending in 10 years. In the Frequency column, indicate whether this is a daily, weekly or monthly expense (Daily = “D”; Weekly = “W”; Monthly = “M”). In the Multiplier column, enter x30 for daily; x4 for weekly; and x1 for monthly. In the Cost Per Month column, multiply the Cost and Multiplier columns together and enter the result here.

Now add up the Cost Per Month column to get your total. That number is how much money you’ll need to be earning as your monthly take-home income in 10 years, in order to cover your 10–year dream budget. If you multiply that number by 12, you’ll get the approximate annual take-home salary you’ll need to earn.

QueStionS: What career path can you follow that will result in approximately that salary?

______________________________________________________________________________

What steps can you take today to start moving toward that long-term goal?

_______________________________________

_______________________________________

_______________________________________

budgeting PluS 10For this activity, you’re going to create another budget. But this time, instead of starting with your current income and deciding how to plan your spending as wisely as possible, you’re going to use a budget as a way of imagining the future.

So, in the budget below, write the amounts of money that you WANT to be spending 10 years from now.

BUdGeT in 10 YearS:

expense Cost frequency Multiplier Cost Per Month

essential expenses

Savings

Rent

Transportation

Food

Education

Clothing

Utilities

Medical

Other

discretionary expenses

Music

Movies

Entertainment

Gifts and donations

Eating Out

Health and Fitness

Other

ToTaL:

1514

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 1: B

Ud

GETIN

G A

Nd

LIvIN

G W

ITHIN

YO

UR

MEAN

SM

oney

Mat

ters

: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

17

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

Put it in the bankbudgeting revieW croSSWord PuzzleCongratulations! You’ve just covered the ins and outs of budgeting. Now let’s see if you really know your stuff. Using the clues below, write the answers in the correct spaces. (Hint: If you get stuck, don’t worry. All the answers can be found throughout the previous pages of this unit.)

aCroSS

1 Something you like but can live without.

4 Money withheld from your paycheck that is used by your state.

8 Many Americans claim that they are living paycheck to ___.

9 Expense category that involves electric bills and cable.

11 Payment type: paid for the completion of a certain project.

13 Payment type: a yearly sum divided and paid out over a series of pay periods.

14 A necessity: something you can’t live without.

15 Expense category that involves monthly rent.

doWn

2 Payment amount after deductions and taxes.

3 Social security tax.

5 Expense category that involves school supplies and tuition.

6 Payment amount before deductions and taxes.

7 Payment type: paid for each hour of work completed.

10 Any type of money you receive, whether it’s from a job, allowance, birthday gift, etc.

12 When saving, try to follow the 10 percent ___.

16

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 1

: B

Ud

GETI

NG

AN

d L

IvIN

G W

ITH

IN Y

OU

R M

EAN

S

SavinG and inveSTinG – PUT YoUr MoneY To WorkWhich would you rather have: a million dollars or a penny? Wait, before you answer, there’s a special deal with that penny. Today you only get a penny, but tomorrow you get two pennies. And the day after you get four pennies. And that penny will keep on doubling each day for a month. So which would you pick? Remember, with the million dollars up front, you can do whatever you’d like with that money – invest it, save it, grow it. So which would you pick?

If you picked the million, congratulations. You’ve got a million dollars.

If you picked the doubling penny, in a week, you’ll have $1.28. Not such a smart choice, huh? Well, after one month you’ll have $10,737,418.24 – almost 11 million dollars!

Unit 2

1918

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 2

: S

AvIN

G A

Nd

IN

vES

TIN

G:

PU

T YO

UR

MO

NEY T

O W

OR

kM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

diFFerent tyPeS oF cardSWhen you open a new bank account, you’ll almost always receive something that looks like a credit card. But look carefully at your card – there’s usually much more than meets the eye.

aTM Card Some banks still issue a card that only lets you get money from their ATM’s (Automated Teller Machines). Withdrawing money from an ATM is the same as writing a check, except that you receive the cash immediately. For almost all banks, using your ATM card at a branch of your own bank is free, but there can be fees if you use a different bank’s ATM machine.

deBiT Card or CheCk Card A debit card and a check card are two names for the same thing. The name “check card” makes more sense, because using a check card is just like writing a check. The difference between an ATM card and a check card is that a check card can be used in stores and online

– wherever a credit card is accepted. But unlike a credit card, you do not run up debt. Instead, when you purchase something with

this kind of card, the money is automatically deducted from your account. If you don’t have enough money in your bank account, the purchase will be declined.

CrediT Card A credit card looks like a check card. But it works completely differently. When you make a purchase with a credit card, the money does not come directly out of your bank account. Instead, you borrow money from a credit card company, and the company sends you a bill. If you don’t pay your credit card bill in full each month, you pay interest, and if your payment is late, you pay a penalty. Credit cards can be useful, but they can also be dangerous.

FocuS on: coMPound intereStOne of the added benefits of saving money in a savings account is that not only are you spending your money wisely and planning for your long–term goals, you are also allowing your money to grow in that savings account. Your money keeps on growing because it is earning compound interest.

Compound interest means that when you put money in a bank account that earns interest, the bank pays you for keeping your money there. If you leave the money sitting in the bank, you start earning interest not only on the money you originally put in, but also on the interest itself. That’s right: the interest earns interest, too!

Be sure to visit www.moneymattersmakeitcount.com to check out the Compound Interest Calculator so you can get a sense of the real power of compounding.

helPFul hint: Write it in the regiSter!When you open a checking account, you’ll receive a small book of starter checks. Then the bank will send several books of checks that have your name and address printed on them. You’ll also receive a little plastic wallet for holding your checks, and it will come with a register — which is a blank form for recording all of your transactions. To avoid ever paying overdraft fees (money the bank charges you if you write a check for more money than you have in your account), or injuring your credit score, it’s critical to get in the habit of always recording every transaction in this register.

•When you deposit money in your account – write it in the register.

•When you take out money from an ATM – write it in the register.

•When you use your debit card to make a purchase – write it in the register.

•When you write a check – write it in the register.

•Are you seeing a pattern here? WriTe iT in The reGiSTer!

Tip: Check your balances two to three times per week. You can check your balance online, but be sure to use a secure computer, and log out and close the browser when you’re finished.

CAUTION!Debit CardsAlthough many ATM cards have credit card logos, they are not credit cards. You must have money in your bank account to use them.

2120

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 2

: S

AvIN

G A

Nd

IN

vES

TIN

G:

PU

T YO

UR

MO

NEY T

O W

OR

kM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

FocuS on: Money in the bankMoney kept in a savings account can earn interest. You can keep making contributions and that money will keep on growing. But even if you keep your money in an account that doesn’t earn interest, like many checking accounts, there are still many incredible advantages. It’s important to know what your goals are, and to learn the fees charged by different institutions for different account types. Only by knowing your goals and these terms can you make the best possible choice for yourself.

Why Should you keeP your Money in a bank or a credit union? Your Money is Safe. Money in the bank is money that only the account holder can access. If you open an account in your name, only you and any other named account holders on the account can touch that money. In fact, most banks require those under 18 years old to have parental consent or joint account status with a parent or guardian.

Your Money is insured. The U.S. government insures the deposits kept in insured banks, credit unions and savings and loans institutions up to $250,000* per account. If the institution closes, or is robbed, your money is still safe. But if someone takes money you have stored at home in a drawer or under your bed, you have no insurance.

a Bank account Builds Good Credit. keeping a bank account active is a step toward borrowing money, which you may need someday to buy a house or a car.

items usually required to open an account with a bank or credit union:

o valid Photo id (driver’s license, state-issued ID card, passport)

o Social Security number

o Proof of current address (a utility bill or phone bill)

o Parent or Guardian (if under 18 years old)

o For non-citizens: proof of alien registration

o an initial deposit (the money you’ll use to open the account; can be cash, a check or money order)

note: Some banks will also ask for a second form of Id. To save yourself time, call the bank first and confirm what you items you’ll need.

*Limits indicated above are effective as of this printing

tyPeS oF Financial inStitutionS

Bank

• Insured by the federal government

• Offer a range of different accounts

• Big banks have branches in lots of locations

• No charge to deposit a check in your account

• Money can earn interest

Credit Union

• Insured by the federal government

• Not–for–profit cooperative financial institution – money is generally kept in the community to help the community

• When you put your money in a credit union, you become part owner of the credit union

• No charge to deposit a check to your account

• Generally lower monthly fees than banks

• Money can earn interest

Check Cashing Store

• Will cash your paychecks for a large fee

• Provide fewer services than a bank, and charge much, much more

• No matter what you hear, there is absolutely no good reason to use a check cashing store

• Money you pay to a check cashing store will never earn interest

QueStion:What type of financial institution is best for you?_______________________________

DID YOU KNOW?

Did you know for your money to

be safe, it has to be in an insured

institution? Look for FDIC banks

and NCUSIF for credit unions.

CAUTION!Payday Loans

Payday loan companies or check

cashing stores have fees associated

with their services. This means that

every time you make money, you lose

money by paying those fees associated

with cashing your check or repaying

the loan. Deposit your checks in a

savings account and the bank pays you

interest. Cash your check as a payday

loan and you pay them.

Visit www.moneymattersmakeitcount.com to learn more.

2322

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 2

: S

AvIN

G A

Nd

IN

vES

TIN

G:

PU

T YO

UR

MO

NEY T

O W

OR

kM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

activity: coMParing accountSAs you investigate different financial institutions – either by visiting websites or by visiting actual branches around town, you can use the form below to compare the different types of accounts available to you. You might also discover that within the financial institutions you visit, they offer different types of accounts that will suit your needs. Remember, it is important to choose a financial institution that is right for you and provides you the most bang for your buck!

CoMParinG aCCoUnTS

The financial institution that is best for me is: ______________________________________

CAUTION! Fees and PenaltiesBanks and credit unions provide many services for free. But if you’re not careful, you can also rack up a lot of penalties and fees. It’s important to be aware of all the fees, charges and penalties your institution might impose. All banks and credit unions have different schedules of fees, so check with yours before opening an account. Here is just a sample of a typical fee schedule of a checking account:

•UsingyourATMcardatanotherbank:$2.50•Stoppaymentonacheck(whenyoumakeapayment with a check and then you change your mind): $25.00

•Non–sufficientfunds(notenoughmoneytocover a check you wrote): $27.00

Name of financial institution

Type of account

Minimum deposit required

Interest rate (if any)

How often is interest compounded?

Number of free withdrawals per month

Service fees

Can you write checks; if so, is there a charge per check?

Can you cash a check for free; if so how many per month?

ATM charge (Same institution)

ATM charge (Other institution)

Distance from my home/school/Club

2524

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 2

: S

AvIN

G A

Nd

IN

vES

TIN

G:

PU

T YO

UR

MO

NEY T

O W

OR

kM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

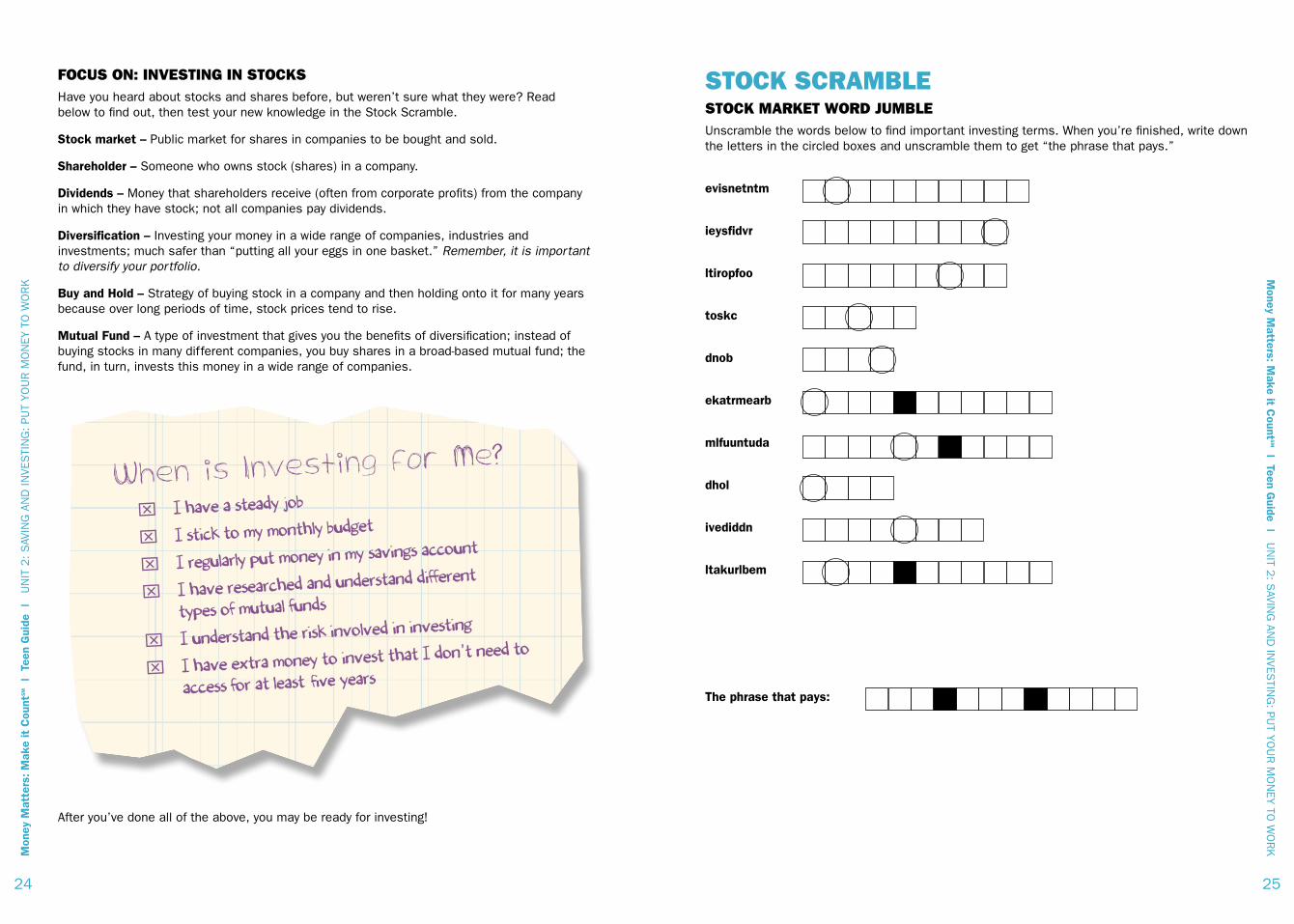

FocuS on: inveSting in StockSHave you heard about stocks and shares before, but weren’t sure what they were? Read below to find out, then test your new knowledge in the Stock Scramble.

Stock market – Public market for shares in companies to be bought and sold.

Shareholder – Someone who owns stock (shares) in a company.

dividends – Money that shareholders receive (often from corporate profits) from the company in which they have stock; not all companies pay dividends.

diversification – Investing your money in a wide range of companies, industries and investments; much safer than “putting all your eggs in one basket.” Remember, it is important to diversify your portfolio.

Buy and hold – Strategy of buying stock in a company and then holding onto it for many years because over long periods of time, stock prices tend to rise.

Mutual fund – A type of investment that gives you the benefits of diversification; instead of buying stocks in many different companies, you buy shares in a broad-based mutual fund; the fund, in turn, invests this money in a wide range of companies.

After you’ve done all of the above, you may be ready for investing!

Stock ScraMbleStock Market Word JuMbleUnscramble the words below to find important investing terms. When you’re finished, write down the letters in the circled boxes and unscramble them to get “the phrase that pays.”

evisnetntm

ieysfidvr

ltiropfoo

toskc

dnob

ekatrmearb

mlfuuntuda

dhol

ivediddn

ltakurlbem

The phrase that pays:

When is Investing for Me?

xi have a steady job

xi stick to my monthly budget

xi regularly put money in my savings account

xi have researched and understand different

types of mutual funds

xi understand the risk involved in investing

x i have extra money to invest that i don’t need to

access for at least years

2726

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 2

: S

AvIN

G A

Nd

IN

vES

TIN

G:

PU

T YO

UR

MO

NEY T

O W

OR

kM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 2: S

AvIN

G A

Nd

INvES

TING

: PU

T YO

UR

MO

NEY TO

WO

Rk

Making your Money groWThe following chart shows how an investment grows over different periods of time. Few people get rich from their wages alone. By taking advantage of the “miracle” of compound interest, anyone can end up with significantly more than their original savings amount and be on the way to meeting long–term financial goals. When the interest earned on an account also earns interest, it is called compound interest. It is growth on top of growth!

Investing small amounts each month may not seem like a lot, but if you start early, even in your teens, it’ll translate into big dollars down the road.

tiMe iS MoneyAssume you’re 16 years old and decide to invest $1,000 a year with money you earn from summer jobs. Your investment grows by 9 percent each year. You set aside the money each year for 10 years, but at age 26 you decide to stop.

Meanwhile, your friends save nothing until they are 25. At 25, they begin to put aside $1,000 every year, and like you, earn 9 percent on their money. At age 50, you have a reunion and compare notes. Who has the most money? The correct answer is the person who began saving at age 16.

The following chart, “The Impact of Time on the Value of Money,” shows the surprising results. The chart shows how time can be a significant factor in helping you achieve your financial goals. Note: Examine the chart with your own situation in mind and take into consideration that saving consistently throughout your life will provide you with the best chance of staying financially secure.

Test your financial knowledge! Visit www.moneymattersmakeitcount.com to play a game. Have your friends play it and see who is the finance whiz!

“show Me The Money!”Cuba Gooding Jr., in the movie Jerry Maguire

the iMPact oF tiMe on the value oF Money (9 Percent rate oF return)

Starting early

age Savings

16 $1,000

17 $1,000

18 $1,000

19 $1,000

20 $1,000

21 $1,000

22 $1,000

23 $1,000

24 $1,000

25 $1,000

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

Total invested $10,000

Amount available by age 50:

$131,010

Starting Later

age Savings

16

17

18

19

20

21

22

23

24

25

26 $1,000

27 $1,000

28 $1,000

29 $1,000

30 $1,000

31 $1,000

32 $1,000

33 $1,000

34 $1,000

35 $1,000

36 $1,000

37 $1,000

38 $1,000

39 $1,000

40 $1,000

41 $1,000

42 $1,000

43 $1,000

44 $1,000

45 $1,000

46 $1,000

47 $1,000

48 $1,000

49 $1,000

50 $1,000

Total invested $25,000

Amount available by age 50:

$84,701

a Lifetime of Saving

age Savings

16 $1,000

17 $1,000

18 $1,000

19 $1,000

20 $1,000

21 $1,000

22 $1,000

23 $1,000

24 $1,000

25 $1,000

26 $1,000

27 $1,000

28 $1,000

29 $1,000

30 $1,000

31 $1,000

32 $1,000

33 $1,000

34 $1,000

35 $1,000

36 $1,000

37 $1,000

38 $1,000

39 $1,000

40 $1,000

41 $1,000

42 $1,000

43 $1,000

44 $1,000

45 $1,000

46 $1,000

47 $1,000

48 $1,000

49 $1,000

50 $1,000

Total invested $50,000

Amount available by age 50:

$215,711

Adapted with permission from National Endowment for Financial Education.

29

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

PLanninG for CoLLeGe: CoLLeGe aS an inveSTMenTYou might already be thinking about a career; but almost all of the most in–demand (and highest paying) careers require some form of post–secondary education: trade school, an associate’s degree, a college degree or a post–graduate degree, like one from medical school or law school. So, taking things one step at a time, that means the next big step after high school will be going to college or a trade school. That’s one of the best ways to increase your career options and your earning potential.

activity: PerSonal inventoryA personal inventory can help you decide on a career path or which subject to major in when you get to college.

Favorite subject(s) in school: ________________________________________________________

Sports or physical activities you enjoy: _______________________________________________

Hobbies: _________________________________________________________________________

Artistic talents: ___________________________________________________________________

Language skills: __________________________________________________________________

Other talents: _____________________________________________________________________

Areas of interest: _________________________________________________________________

Now that you have assessed your interest and talents, what types of careers are best for you?

_________________________________________________________________________________

_________________________________________________________________________________

What type of degree would you need to pursue this type of career?

_________________________________________________________________________________

_________________________________________________________________________________

Unit 3

3130

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

education alternativeSThere are a lot of options for continuing your education after high school, so be sure to talk with your parents, guidance counselor or Club staff to help choose what’s right for you.

Want to see how your level of education can affect your income? Visit www.moneymattersmakeitcount.com and check out the “Planning for College” section to learn more!

activity: career Path Instructions:

1. Write your career destination in the blank below.

2. Add to the list on the left everything else you can think of that you can do to help you reach your career destination.

3. In the right–hand column, indicate how you are going to accomplish these goals. Be specific. For example, for “improve my grades,” you might say “study harder” or “work with a tutor at the Club” or “talk with my teachers during their office hours,” or you might even list all of those things.

MY CAREER dESTINATION IS ___________________.

A BENEFIT OF CHOOSING THIS CAREER IS __________________________.

My Plan for the future

WhaT i WiLL do hoW i WiLL aCCoMPLiSh ThiS

Improve my grades.

Practice for the SAT or ACT.

Join extra–curricular activities.

Perform community service.

Get a job.

Find an internship.

Save money.

Research schools to attend after high school.

Learn more about my career destination.

Improve my interview skills.

Educational Setting

Four-year Universities

Four-year Liberal Arts Colleges

Community and Two-year Colleges

Technical Training or Vocational School

Military Service

Benefits

• Undergraduateandgraduatedegrees• Largechoiceofmajors

• Generalized(notcareer–specific)curriculumwithdeclaredmajors• Generallysmallerclassesthanuniversities• Usuallymorefaculty–studentinteractionthanuniversities

• Opentoeveryone• Maybeagoodchoiceifyouarenotsurewhattomajorin• Economicalwaytotakeclassesandbuildgradepointaverages• Flexiblehourssostudentscanwork• Career–orienteddegreesnotofferedbyfour–yearcolleges(suchasfashiondesign,computerrepair,electronics,foodservice, technology, paralegal studies, etc.)

• Canbeasteppingstonetoafour–yearcollegeoruniversity

• Certificationinparticularskill(suchascosmetology,nursing assistant, computer repair, culinary arts and fashion and design schools, etc.)

• Waytobuildcharacterandgetaneducationwhileserving the country

• GIBillhelpscovercostofhighereducation

3332

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

Financial aid ServiceSThis is a comprehensive suite of assistance that most educational institutions can provide for you, combining loans, grants and work/study programs. Some financial aid does not need to be repaid, but you must qualify to receive it. (Visit www.finaid.org for more information).

note: Loans do require repayment.

fafSa: This is the central application you’ll need to complete, with the assistance of your parents or guardians, to apply for financial aid. (You can find the application and more information here: www.fafsa.ed.gov)

Work/Study programs: A portion of your financial aid package might derive from the Federal Work Study Program, in which schools offer students jobs that allow them to earn up to a certain amount each year. You get paid just like a normal job.

loanS Loans are easier to qualify for than financial aid, but they must be repaid with interest. Repayment usually begins immediately after graduating.

federal Loans: The U.S. government offers Stafford and Perkins student loans, and PLUS Loans for parents. (Visit the Department of Education for their complete guide to repaying loans: http://studentaid.ed.gov)

Private Loans: Many financial institutions, like Sallie Mae, offer private student loans and consolidation loans.

ScholarShiPS & grantS These don’t ever have to be paid back. All you have to do is qualify. And qualifying can sometimes be much easier than you think. Grants and scholarships can come from the federal or state government, a high school, college or university, a business, an individual or even a nonprofit organization.

Merit-based: These are scholarships that you earn, like academic or athletic scholarships.

need-based: Need–based scholarships, like the Federal Pell Grant, are determined by financial need factors.

Visit www.moneymattersmakeitcount.com to use the Scholarship Search tool – you can save all the scholarships you find in your Personal Locker.

toPic: Paying For your education Yes, education can be expensive. But because people with a college education tend to have more opportunities and higher–paying jobs, continuing your education past high school is probably the best investment you can make for yourself.

It’s important to find out all the ways you can pay for college. After all, paying for college is more than just tuition. If you plan to live on campus you’ll have expenses like room and board. Here is an overview of resources to help you pay for your college expenses:

SavingS PlanSConventional Savings account. deposit 10 percent of any money you receive as income or gifts into a conventional savings account at a bank or credit union to start your own education savings program.

Coverdell Savings account. In order to participate, your family must have an adjusted gross income of less than $110,000* ($220,000* if filing a joint return). This money has to be used to pay for school. Non–qualified withdrawals are taxed as ordinary income at donor’s rate and subject to a 10 percent tax penalty. (For more information, visit CFED.org or www.finaid.org)

529 College Plan. Also known as qualified tuition plans, this is named for section 529 of the Internal Revenue Code. You can invest long–term in mutual funds or pay future tuition costs at today’s prices. As with the Coverdell, money has to be used for education or you have to pay a penalty. (For more information, visit CFED.org)

educational Savings Plans. Several companies and organizations now offer educational savings plans as a way to earn enough money to pay for college. Special incentives allow you to put away college savings every time you use a credit card or make specific types of purchases. (For more information, visit www.upromise.com)

An individual development account is a matched savings account that can be used to pay for post–secondary education. A “matched” account means that for every contribution that you or your family makes to the account, additional money is placed into the account by various government and private sources. (For more information visit, CFED.org)

Savings Bonds. You or your family can purchase U.S. Savings Bonds that only cost a fraction of their face value, but over time, they mature and end up being worth more than you paid for them; once they mature, you can cash them in and use them to pay for school. As an added bonus, the government gives you tax credits when savings bonds are used to pay for college. (For more information on how to use Savings Bonds to pay for post–secondary education, visit www.treasurydirect.gov)

*Limits listed above are valid at the time of printing.

WATCh OUT!

Onlyborrowenough

money to pay for

college; try to avoid

any unnecessary debts.

3534

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

getting into college checkliStGetting into college does not mean you need a 4.0 average and perfect scores on the SAT. In fact, colleges look at a wide range of factors when they decide whom to admit into next year’s freshman class. Here’s a checklist of some of the things you’ll need to do to help you get into the college of your choice.

o PSaT – The PSAT is a practice test that you usually take in 10th and 11th grade to prepare for the SAT.

o SaT/aCT – Most schools require that applicants submit their scores on either the SAT or ACT, which are standardized admissions tests.

o GPa – Your grade point average is weighted heavily in college admissions because it reflects your long–term performance in school.

o extra–curricular activities – Involvement in extra–curricular activities, like sports, clubs or student government, show that you are well–rounded and can manage your time well.

o hobbies – Hobbies help to present you as an interesting, well–rounded person.

o Community service – Look for opportunities through your school, church or other organizations to get involved in making a difference in your community.

o Part–time and summer jobs – A job can not only earn you money to pay for college, it can also be used to impress the admissions team by demonstrating your work ethic and responsibility.

o Part–time and summer internships – Internships offer the chance to learn much more about your possible profession.

o College application – Usually includes one long essay and one or more short–answer essays. Some schools participate in the common application process, which has one standard application for some 400 schools. Visit www.commonapp.org for more information.

o College interview – A great opportunity to let the admissions staff get to know the real you.

o Letters of recommendation – These can come from a favorite teacher, coach, guidance counselor, employer or community leader.

o Completed financial aid application – Also known as the FASFA.

o Scholarship search – A chance for you to research additional ways to pay for your college education.

Visit www.moneymattersmakeitcount.com to check out an interactive checklist that you can save to your Personal Locker!

Senior year Financial aid guide and checkliStNote: You can begin your scholarship search during your junior year of high school.

To-do When

o Ask your counselor about local scholarships October available in your community.

o Apply for local scholarships in time to meet deadlines. November

o Get a free application for Federal Student Aid (FAFSA). November

o Gather all the necessary information to complete the FAFSA. december

o determine if your prospective schools require the CSS PROFILE. december

o Get a Personal Identification Number (PIN) from the December U.S. department of Education in order to complete the FAFSA online.

o Get a copy of parents’ or guardians’ tax return. January

o Complete and submit the FAFSA. January

o Complete and submit the CSS PROFILE (if applicable). January

o Receive a copy of your Student Aid Report. February

o Receive aid offers from schools. March

o Accept financial aid offer from the school you will attend. April

how to keep Costs down When applying to Colleges

• Buy used SAT practice books or check out copies from the library.

• Apply for an SAT or ACT fee waiver through your guidance counselor.

• Apply for an application fee waiver.

• Look for school– or Club–sponsored trips to visit colleges.

REMINDER!

Be sure to keep track

of

deadlines for a

ll of your

college applicat

ions.

3736

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

Question: How do you plan to pay for college? Check off the boxes below to indicate which sources you will use.

o Parents/Family

o Scholarships/Grants

o Student Loan/Financial Aid

o Summer Job

o Part-time Job

o Savings Account

inForMation Scavenger hunt

What kinds of scholarships and programs are available in colleges and universities in your community?

do some research about the colleges, universities or campuses in your area. Write, call or use the Internet to identify a contact person at an institution and gather the following information:

• What kinds of high school courses would help prepare you for success?

• Does the school have brochures and program descriptions that outline information helpful to pursing your career?

• What scholarship information is available?

Using the information you’ve gathered, fill in the ready for College! chart below to help you keep your eyes on the goal.

HELPFUL HINT! Visit the Money Matters website (www.moneymattersmakeitcount.com) to research scholarships opportunities and the CareerLaunch website to explore careers or build your resume. Also, www.collegeboard.com is a great site to learn more ways to pay for your college education.

readY for CoLLeGe!Three schools I am interested in attending:

Name of Institution Cost of Tuition + Room & Board

Organizations that offer scholarships and grants take into consideration a wide variety of factors in awarding their financial packages. The following is only a partial list of information that you may need to have on hand to apply for various scholarships. Fill this out as best you can and ask your family to help you with any missing information. Remember, you can save all of this information in your Personal Locker on the Money Matters website (www.moneymattersmakeitcount.com).

DID YOU KNOW?A 2008 study* reveals the following about how students pay for their college education:

•Parents 61percent•Scholarships 40percent•StudentLoans 38percent•SummerJobs 32percent•Part-timejobs 29percentDid you notice that the percentages add up to more than 100 percent? In other words, almost every student reported that their education is being paid for by a combination of the sources listed above.*Source:Mierzwinski,Edumund,andChristineLindstrom.TheCampusCreditCardTrap: A Survey of College Students and Credit Card Marketing. U.S. Public Interest ResearchGroupEducationFund,March2008

GOOD TO KNOW!Did you know that you could

save on the cost of tuition by

getting college credits while you

are still in high school? Not only

will this save on costs, but it

will help ensure that you graduate

on time or even early. Talk to a

guidance counselor about Advanced

Placement(AP)classesthatare

offered at your high school. You

will have to take an AP test or a

CLEP(College–LevelExamination

Program) to gain the credit, but it’s

worth it if you can save a couple

thousand dollars!

3938

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

Not all of the information you collected about yourself and your family may seem relevant when applying for college, but there are scholarships associated with many obscure talents, hobbies, family situations or histories. Now that you have spent some time thinking about the qualities that make you unique, use Internet search tools like Google and Bing to search for scholarships, grants and contests where these qualities may help you to pay for college.

After researching some scholarships online, I think I qualify for the following:

name of Scholarship/Contest/Grant

Money Matters Scholarship

deadline for Submitting application

Ask Club staff for the deadline!

My Scholarship Worksheet

First name:

Last name:

Gender:

Country of birth:

Ethnicity (list all):

Countries where your ancestors came from (list all):

Sports you play:

Musical instruments you play:

GPA:

Majors you’re interested in:

Career objectives:

Organizations you belong to:

Organizations your parents belong to:

Colleges attended by your immediate family members:

did your parents serve in the military:

Parent or Guardian careers:

Fraternities/Sororities for your immediate family members:

Hobbies:

Extra-curricular activities:

Awards:

do you have any disabilities:

Family members with disabilities:

Total household annual income:

Additional information:

4140

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 3: P

LAN

NIN

G FO

R C

OLLE

GE: C

OLLE

GE A

S A

N IN

vES

TMEN

T

Sample College interview Questions Here are some questions you can use to practice and prepare for your college interviews. Use the space below to brainstorm your responses!

Tell me about your experiences at your high school. Is there a particular experience you had there that stands out? _____________________________________________________________

__________________________________________________________________________________

What might your teachers say is your greatest strength as a person and as a student, and what are your weaknesses in each area? ______________________________________________

__________________________________________________________________________________

What sort of things do you like to do outside of school? _________________________________

__________________________________________________________________________________

What do you want to do in the future? _________________________________________________

__________________________________________________________________________________

What do you want out of college? ____________________________________________________

__________________________________________________________________________________

Where do you see yourself in 10 years? _______________________________________________

__________________________________________________________________________________

What are you doing to prepare for college? ____________________________________________

__________________________________________________________________________________

What accomplishment are you most proud of? _________________________________________

__________________________________________________________________________________

Give me three characteristics that describe you. ________________________________________

__________________________________________________________________________________

Tell me about someone who has influenced you in your life. ______________________________

__________________________________________________________________________________

ready For college!Some colleges may require an interview before admission is granted. Here are a few questions that can help you prepare for your face–to–face interview or complete your college application. Review your responses before each interview or before applying to a college of your choice.

College interview Tips and Questions The interview is not an adversarial situation. Admissions folks want to like you, have you like them and like their school. Remember to:

• Have a positive attitude

• Smile and maintain eye contact

• Take a moment to think about an answer before replying

• Ask questions; this shows interest in the college and what the admission officer has to say

• Highlight the good things from your academic past and put a positive spin on your background

• Rehearse for the interview with family, friends or a coach

College Prep Questions Here are some questions you can ask your high school guidance counselor, and also discuss at home with your family:

• Which are the best colleges, universities or trade schools for my interests?

• Are my current grades good enough to get into the schools of my choice?

• What can I do to improve my grades?

• Do those schools have financial aid?

• When should I start researching scholarships and other ways of paying for school?

• What other steps can I take during school and after school to improve my chances of getting into those schools?

• Are there any extra–curricular activities I can participate in that will help me in my acceptance to the school of my choice?

• What do these universities/colleges/schools look for in a student?

• When do I start taking the SAT, PSAT or ACT?

• Are there programs I can use to help me practice for those tests?

43

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 4: C

RED

IT AN

D D

EB

T: PR

OTE

CT Y

OU

R FU

TUR

E

42

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 3

: PLA

NN

ING

FO

R C

OLL

EG

E:

CO

LLEG

E A

S A

N IN

vES

TMEN

T

UniT 4: CrediT and deBT: ProTeCT YoUr fUTUre

credit and debt: Protect your FutureCredit is borrowed money you can use to pay for things. The creditor (also known as the lender) trusts that you (the borrower) will pay them back later, usually with interest.

As teenagers, now is the time to start building up good credit, to prove to future lenders that you are responsible. This will be very important when you eventually apply for other types of credit, when you want to buy a car, rent an apartment or even apply for a business loan, for example.

Every single financial transaction you engage in –– whether you pay your bills on time, if you miss some payments, how much debt you have –– is tracked and recorded in a document known as your credit report. Some simple ways to build a good credit report are paying your bills on time and managing your checking account responsibly. Whether or not you have good credit will affect almost every single aspect of your life.

did YoU knoW?• 80 percent of college students received credit card offers in the mail.

• Students received an average of nearly five credit card offers in the mail per month.

• 66 percent of students have at least one credit card.

• For students paying their own bills, about half reported that they pay their credit card bills in full each month.

• 25 percent reported that they had paid at least one late fee.

• 15 percent reported that they had paid at least one over–limit fee.

Source: Mierzwinski, Edumund, and Christine Lindstrom. The Campus Credit Card Trap: A Survey of College

Students and Credit Card Marketing. U.S. Public Interest Research Group Education Fund, March 2008

Unit 4

CREDIT CARD REMINDERS:o Never charge more on a credit card than you can afford to pay

back right away.o Onlyusecreditcardsforplannedexpenses(useyourbudget!).o Pay off credit card balances in full each month.o Limit the number of credit cards you have.o Carefully evaluate all credit card offers you receive.o If anything ever sounds too good to be true, it probably is.o Late or missing payments can make your credit card interest rates

go up and will have a negative impact on your credit score.

4544

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 4

: C

RED

IT A

ND

D

EB

T: P

RO

TEC

T YO

UR

FU

TUR

EM

oney Matters: M

ake it Count

SM | Teen G

uide | UN

IT 4: C

RED

IT AN

D D

EB

T: PR

OTE

CT Y

OU

R FU

TUR

E

FocuS on: hoW credit aFFectS your liFeYour credit score will be considered by future employers, landlords, bankers, credit card companies, phone companies, utilities. It can mean getting a job or not. It can mean getting an apartment or not. Getting a home loan or not. These are huge and important impacts.

But besides these all–or–nothing situations, your credit score will also have an impact on almost all of your financial dealings. For example, let’s take a look at the situation where you’re going to buy a car and you want to finance $10,000. (In other words, you’re getting a loan of $10,000 to buy the car.)

Your credit score won’t just determine whether or not you get the loan. It will determine the TERMS of the loan –– how favorable the interest rate is. Take a look at the chart below. The person with a really bad credit score ends up paying about $2,200 more for the car than the person with a really good credit score. So even this one transaction, buying a car, cost the financially irresponsible person an extra $2,000. Bad credit is a penalty you pay over and over and over again.

So keep your debts to a minimum – and always pay your bills – and pay them on time!

Amountborrowed:$10,000•Repaymentperiod:36months*

fiCo® score

720-850

690-719

660-689

620-659

590-619

500-589

aPr

5.149%

6.677%

8.610%

12.219%

17.958%

18.957%

Monthly payment

$300

$307

$316

$333

$361

$366

Total paid

$10,800

$11,052

$11,376

$11,988

$12,996

$13,176

Source: MyFico.com. *Based on available rates at the time of printing.

Visit www.moneymattersmakeitcount.com to use an interactive repayment calculator. You will see how quickly interest charges add up!

hoW to Manage your credit ScoreYour credit report is a detailed account of your financial history – it shows you how responsible you have been (or have not been) with your money, especially with paying back money you owe. It shows your payment history, your current credit accounts and other related information.

Your credit score, or FICO score, is a number based on the results of your credit report. It is a number between 300 and 850; the higher the score, the better. Anything above 700 is generally considered to be a good score. Your FICO score is essentially made up of the following*:

1. Payment History – 35 percent

2. Total Amounts Owed – 30 percent

3. Length of Credit History – 15 percent

4. New Credit – 10 percent

5. Type of Credit in Use – 10 percent

*Source: “How Your FICO Credit Score is Calculated.” MyFICO. Fair Isaac Corporation. Web. 04 Feb. 2010.

www.myfico.com/CreditEducation/WhatsInYourScore.aspx

As a teenager, there’s nothing you can do about numbers 3 and 4 above. But as you can see, by using a budget, spending your money wisely and using credit cards responsibly (if you use them at all), you can focus on the #1 and #2 items that make up your credit score. Keep the amount you owe to a minimum, and always pay your bills on time.

Check Your own Credit reports

Your credit report is maintained by three different credit bureaus: TransUnion, Experian and Equifax. There really is no significant difference among these three companies. But if you ever have any problems with your credit, it’s a good idea to contact each of the three bureaus separately in order to correct any inaccuracies you might find on your credit report.

You can order a free credit report from all three credit bureaus for free from the official website that helps consumers keep track of their credit reports:

www.annualcreditreport.com

Once you’ve reviewed your report, www.annualcreditreport.com has a list of frequently asked questions where you can find out how to dispute or correct inadequate information.

CAUTION!Making only the minimum payment

can add a considerable amount to

your original purchase and can take

years to pay off a balance.

47

Money M

atters: Make it C

ountSM | Teen G

uide | UN

IT 5: E

NTR

EPR

EN

EU

RS

HIP

: MAk

ING

IT ON

YO

UR

OW

N

46

Mon

ey M

atte

rs: M

ake

it C

ount

SM | T

een

Gui

de |

UN

IT 4

: C

RED

IT A

ND

D

EB

T: P

RO

TEC

T YO

UR

FU

TUR

E

real coSt oF a coMPuter The way in which you purchase items can have a big effect on your bottom line. Look at the scenarios below to see how improper use of a credit card on a $500 computer purchase can quickly land you in hot water.