+ chapter 2 the accounting equation. + assets, liabilities & owner’s equity the most obvious...

TRANSCRIPT

+

Chapter 2

The Accounting Equation

+The Accounting Equation

Assets, Liabilities & Owner’s Equity The most obvious place to start an assessment of any

business is with its current situation, or if you like, its current financial position. At its most basic, this assessment will consider the economic resources it controls – its assets – and the obligations it has – its liabilities. By preparing a Balance Sheet (which details these assets and liabilities), an owner can assess his or her owner’s equity – the net worth of their investment in the business.

+The Accounting Equation

What liabilities and owner’s equity have in common is that they are both equities – claims on the assets of the business. That is, liabilities are what the business owes to external parties, while owner’s equity is what the business owes to the owner. Both types of claim must be funded from the business’ assets. This relationship – between assets, liabilities and owner’s equity – is described by the Accounting Equation.

The Accounting Equation

Assets = Liabilities + Owner’s Equity

+It must always balance!

Assets must always equal liabilities plus owner’s equity; it is not possible for the equation to be out of balance.

For instance, if a firm has assets of $120 000 and liabilities worth $85 000, its owner’s equity must be the residual (what is left over): $35 000. It is not possible for owner’s equity to equal an amount greater than this, because there would be insufficient assets to fund the claim. Conversely, it is not possible for owner’s equity to equal an amount less than this. If liabilities claimed $85 000, and the owner claimed only $20 000, that would leave an amount not claimed by liabilities, nor by the owner – who would then claim this amount? Who would claim the remaining $15 000? (Surely a donation to the tax office is not on the cards!) Thus, the Accounting equation must always balance.

+The Balance Sheet

The relationship between assets, liabilities and owner’s equity – as described by the Accounting equation – is at the heart of the Balance Sheet. The Balance Sheet is an accounting report that details the business’ assets, liabilities and owner’s equity at a particular point in time, and is a reflection of the firm’s Accounting equation.

Assets = Liabilities + Owner’s equity

Assets Liabilities

plus Owner’s equity

TOTAL ASSETS TOTAL EQUITIES

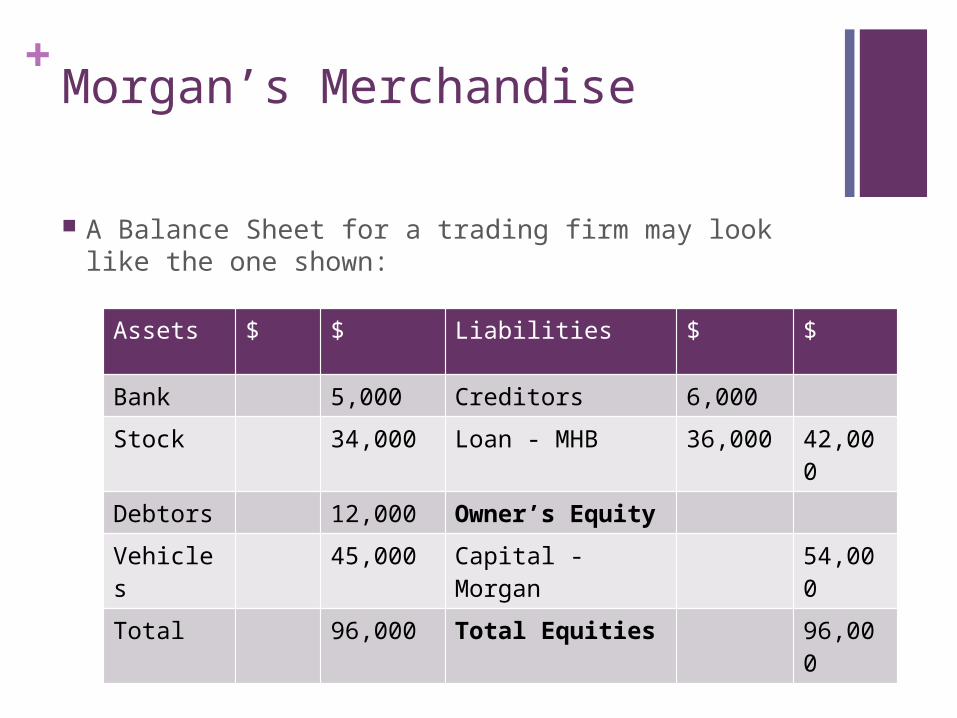

+Morgan’s Merchandise

A Balance Sheet for a trading firm may look like the one shown:

Assets $ $ Liabilities $ $

Bank 5,000 Creditors 6,000

Stock 34,000 Loan - MHB 36,000 42,000

Debtors 12,000 Owner’s Equity

Vehicles 45,000 Capital - Morgan 54,000

Total 96,000 Total Equities 96,000

+Note

The assets are listed on the left-hand side, with the equities – liabilities and owner’s equity – listed on the right, just like the Accounting equation.

The title of the report will normally state who it has been prepared for (Morgan’s Merchandise), what kind of report it is (a Balance Sheet), and when it was prepared (30 June 2010). Because businesses engage in a number of transactions every day, and every transaction changes the Balance Sheet, the Balance Sheet is only ever accurate on the day it is prepared. Thus, the title says ‘as at’ a particular date.

Note also how the term ‘Owner’s Equity’ is used as a heading. The actual item representing the owner’s claim is known as ‘Capital’, with the name of the owner listed next to it. Any profits earned by the business – and thus ‘owed’ to the owner – would also be listed under this heading of ‘Owner’s equity’.

+Assets

Assets are resources controlled by the entity as a result of past events from which future economic benefits are expected to flow to the entity. For an item to be recognised as an asset, it must meet each

part of the definition; an item that fails to meet any of these requirements cannot be considered to be an asset.

+Assets

Resources controlled by the entity Resources are simply items that are capable of generating an economic

gain for the business, such as Bank (the cash held there, not the building!), Debtors, Stock, Vehicles, and Premises. However, not all these items will necessarily qualify as assets: only those items that are under the firm’s control will satisfy the definition. This means that the firm must be in a position to determine how and when the item is used. For instance, it is up to the business to determine how and when the cash in the Bank account will be spent, when the Debtors are expected to pay, and how the Vehicles will be used. Alternatively, the owner’s home cannot be classified as a business asset because it is not under business control. (Don’t forget the Entity principle here: the owner’s home is under the control of the owner, who is considered to be a separate accounting entity from the firm.)

Note that although a business will own many of its assets, ownership itself is not a necessary condition for an item to be classified as a business asset. Control is much broader than ownership, so the firm’s assets will obviously include, but not be restricted to, what it owns.

+Assets

Future economic benefit In addition to falling under business control, assets must be

capable of generating a future economic benefit. That is, they must represent some sort of benefit that is yet to be received. For example, cash in the Bank can be spent, and Stock can be sold, at some point in the future. The amount owed to the business by its Debtors will be received as cash sometime in the next month or so, and items like Premises and Vehicles will usually be used for business activities for a number of years into the future. On the other hand, cash paid for this month’s Wages is not an asset, as there is no future benefit: in order to gain a further benefit, a further payment must be made. Items like this cannot be classified as assets because their benefit does not extend beyond what has already been received.

+Liabilities

Liabilities are present obligations of the entity as a result of past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

This may seem like a lot of jargon, but broken into its components it is easier to understand.

+Present Obligations

If the business has a legal responsibility (or obligation) to settle a debt, then this debt is likely to be a liability. In the case of a bank overdraft or mortgage, the contract with the lender means the business is obliged to repay the amount owing. Contrast these items with the amount that is expected to be paid next year for advertising. This cannot be reported as a liability, as at present there is no obligation to pay – the obligation will only occur once the firm has signed the contract, or the advertising itself has been provided.

+Expected to result in an outflow of economic benefits

The fact that a liability is expected to result in an outflow or sacrifice of economic benefits means that the outflow/sacrifice has not yet occurred. In this way, a liability could be seen as requiring a future economic sacrifice.

In most cases, the economic benefit to be sacrificed will be cash, and the expected outflow will occur when the business pays its debts. However, this is not always the case – there may be an alternative economic benefit that must be sacrificed. For example, a firm may have received cash in advance for a job yet to be completed: it is not a payment that is required to extinguish this liability, but the work itself.

+Owner’s Equity

Owner’s equity is the residual interest in the assets of the entity after the deduction of its liabilities. In effect, owner’s equity is what is left over for the owner once a firm has met all its liabilities. And given that the owner and the firm are considered to be separate entities, it can also be described as the amount the business ‘owes the owner’.

+Funnies

+Performance Indicators & the Balance Sheet

The classification of the items in the Balance Sheet as current or non-current enhances the usefulness of the report because it allows for the calculation of performance indicators. These indicators – or ratios as they are sometimes known – compare items within the Balance Sheet in order to assist management in determining the financial health of their business. Specifically, the Balance Sheet allows for the calculation of indicators to assess the firm’s liquidity and stability.

+Performance Indicators & the Balance Sheet

Indicator A measure that expresses profitability or liquidity in terms of

the relationship between two different elements of performance.

Liquidity Liquidity refers to the ability of a business to meet its

debts as they fall due, which is essential to its survival. One of the most popular measures of liquidity is the Working Capital Ratio (WCR). This indicator compares a firm’s current assets and current liabilities to determine whether the business has sufficient economic resources to cover its present obligations.

+Working Capital Ratio

Working Capital Ratio

Formula

Working Capital Ratio (WCR) = Current Assets

Current Liabilities

Read Figure 2.3 p. 24.

Assessing Working Capital Ratio What is a suitable level for the WCR? As long as the ratio is above a minimum of

1:1 then this would indicate sufficient liquidity, as there are enough current assets to cover the current liabilities of the business. Obviously a Working Capital Ratio of less than 1:1 is worrying, however the owner should also be wary of having a Working Capital Ratio that is too high as this may indicate that the business has an overabundance of current assets that are not being employed effectively.

+Stability

Whereas liquidity focuses on short-term, stability concentrates on the firm’s ability to meet it obligations in the longer term.

A good indicator of stability is Gearing, which measures what percentage of the firm’s assets are funded by external (outside) sources. In this way it measures the firm’s reliance on outside finance.

Formula: Gearing = Total Liabilities X 100

Total Assets

+Assessing Gearing

Assessing Gearing There is no set level at which Gearing is said to be satisfactory,

but it is a good indicator of financial risk. High Gearing means that a high proportion of the firm’s assets are funded by external sources. This in turn means pressure on the firm’s cash flow to meet principal and interest repayments, and therefore a greater risk of the business facing financial collapse.

Gearing will increase from increased borrowing by the business; however, changes in owner’s equity will also affect the Gearing, not just changes in the assets and liabilities. Excessive drawings that decrease owner’s equity will increase the Gearing and the risk the business as well as affecting the level of liquidity. However, capital contributions by the owner can reduce the Gearing and the financial risk of the business as well as providing short-term relief to liquidity.

+You!

Finish note taking.

Read Summary.

Homework! Do a minimum of five exercises at the end of the chapter

(don’t just do the first five).