© 2014 kaufman, hall & associates, inc. all rights reserved. insurance exchanges – public...

TRANSCRIPT

© 2014 Kaufman, Hall & Associates, Inc. All rights reserved.

Insurance Exchanges – Public & Private Implications for Hospitals

GSMC| 2014 Fall Conference and Annual MeetingYoung Harris, GA| October 2, 2014

GSMC 2014 Fall Conference & Annual Meeting 2

Meeting Agenda• Introductions• Private exchanges

– What are private exchanges and how do they work?– Private exchange adoption outlook– Implications for hospitals and health systems

• Public exchange update– National– Georgia

• Narrow network prospects and implications• Summary implications• Questions

GSMC 2014 Fall Conference & Annual Meeting 3

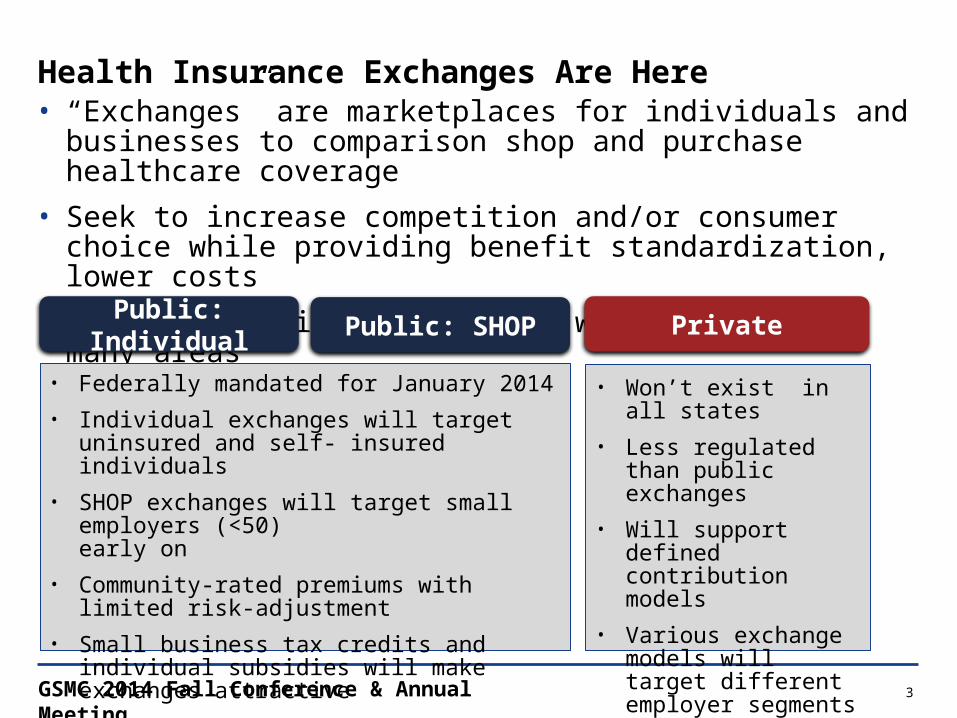

Health Insurance Exchanges Are Here• “Exchanges” are marketplaces for individuals and businesses to

comparison shop and purchase healthcare coverage• Seek to increase competition and/or consumer choice while providing

benefit standardization, lower costs• Public and private exchanges will co-exist in many areas

Public: Individual Public: SHOP Private

• Federally mandated for January 2014 • Individual exchanges will target uninsured and self-

insured individuals • SHOP exchanges will target small employers (<50)

early on• Community-rated premiums with limited risk-

adjustment • Small business tax credits and individual subsidies

will make exchanges attractive

• Won’t exist in all states• Less regulated than

public exchanges• Will support defined

contribution models• Various exchange models

will target different employer segments

GSMC 2014 Fall Conference & Annual Meeting 4

Private Exchanges – What Are They And How Do They Work?

GSMC 2014 Fall Conference & Annual Meeting 5

Private Exchanges – What Are They?As the commercial insurance market continues to move from defined benefit to

defined contribution plans, employers will seek new benefit models to maximize or cap the value of their healthcare benefit subsidies

Private Exchange Sponsors

Defined ContributionDefined Benefit

Private exchanges will support this market shift by offering a broader choice of plan and coverage options sponsored by a variety of organizations

GSMC 2014 Fall Conference & Annual Meeting 6

Private Exchange Adoption Outlook

GSMC 2014 Fall Conference & Annual Meeting 7

Private Exchange Activity Occurs Across a Range of Employer Sizes

Small to Midsize Employers

Large Employers

Midsize to Large Employers

Liazon Forges Partnerships with National Brokers

Mercer Announces 2014 Private Exchange Participants

Walgreens Joins AON Hewitt Private Exchange

BAN/USI have 150 US offices; Liazon exchange

includes 2,000 employers

33 mostly midsize companies across range of industries will

enroll 75K employees

160K Walgreen’s employees will enroll in 2014; total AON 2014 enrollment will be 600K

Note: 600K AON enrollees includes employees and dependents across 18 employers, an increase of 15 employers vs. the 3 employers enrolled in 2013. Sources: Shutan, B: “BAN Partners with Liazon,” Health Insurance Exchange News, Sept 17, 2013. “USI Helps Clients Manage Employee Benefits Through Launch of Private Insurance Exchange,” Fort Mill Times, Oct 17, 2013. McCann, D: “Midsize Companies Move to Private Health Exchanges,” CFO.com, Oct 15, 2013. Armstrong D, “Walgreen Joins in Exodus of Workers to Private Exchanges,” Bloomberg, 18 Sept, 2013. “Private Exchanges Woo More Employers, But Real Traction Won’t Begin Until 2015,” Inside Health Insurance Exchanges, Aug 15, 2013.

GSMC 2014 Fall Conference & Annual Meeting 8

2014 Enrollment Amongst Select Major Private Exchange Operators Has Reached 1.2 Million Commercial Lives

Exchange Operator

# of 2014 Enrollees

# of 2014 Employers

# of Enrollees per Employer

600,000 18 33,333

400,000 14 28,571

100,000 2,400 42

75,000 33 2,273

46,500 3 15,500

Total 1,221,500 2,468 495

Private exchange operators are quickly growing their enrollee bases and appealing to employers of all sizes

Source: Company press releases and investor conference calls.

GSMC 2014 Fall Conference & Annual Meeting 9

Early Adopters Include Many Household Names with Outsized Representation by the Retail and Restaurant Industries

GSMC 2014 Fall Conference & Annual Meeting 10

Drivers That Could Impact Commercial Shift to Private Exchanges

Driver Influence Factors Shift Impact

“Me Too” Effect Secondary wave of “fast followers” will emerge if initial wave of employers demonstrates success

↑Rising Administrative Costs Employers continue to look for ways to lower

administrative expenses of employee benefitsDelivery Cost Favorable insurer network contracts will increase plan

participation and pressure on employers to shiftCadillac Tax Some employers may use private exchanges to avoid

the excise tax stipulated to begin in 2018Exchange Plan Options and Premiums

Plan designs and premiums must be as good or better than current group coverage ↔

Paternalism Employers can be paternalistic and resistant to significant changes in employee benefit design ↓Union and Public Sector Collectively bargained cohorts and public sector employers typically are slower to change

Source: “Sizing Up The Healthcare Exchanges - Big Long-Term Opportunity,” Credit Suisse, Sept 26, 2013.

GSMC 2014 Fall Conference & Annual Meeting 11

Implications for Hospitals and Health Systems

GSMC 2014 Fall Conference & Annual Meeting 12

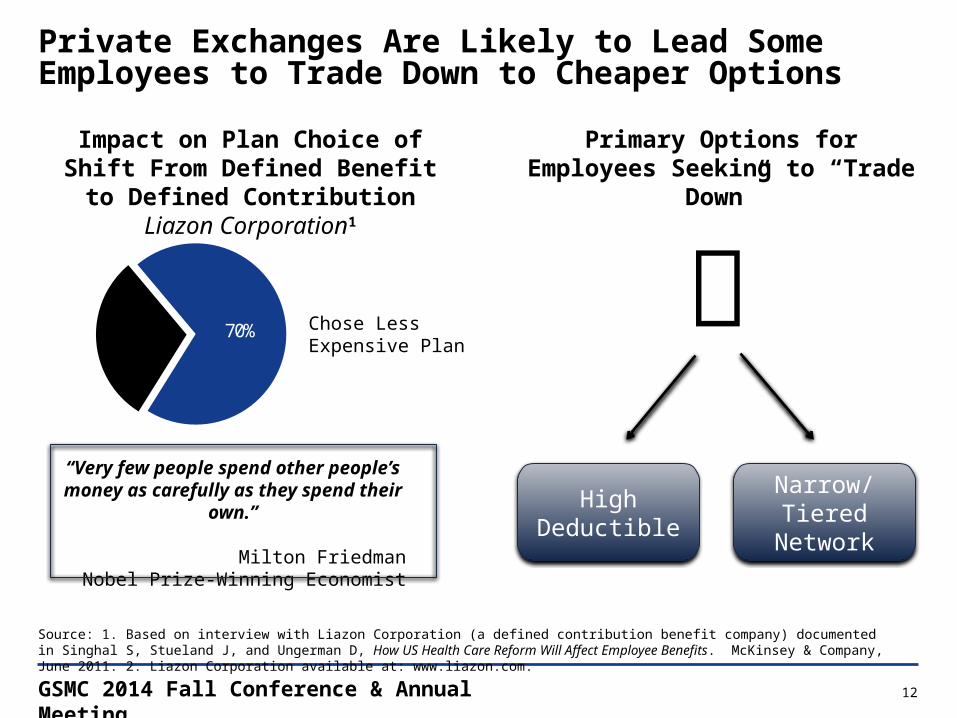

Private Exchanges Are Likely to Lead Some Employees to Trade Down to Cheaper Options

Source: 1. Based on interview with Liazon Corporation (a defined contribution benefit company) documented in Singhal S, Stueland J, and Ungerman D, How US Health Care Reform Will Affect Employee Benefits. McKinsey & Company, June 2011. 2. Liazon Corporation available at: www.liazon.com.

Chose Less Expensive Plan

Primary Options for Employees Seeking to “Trade Down”

High Deductible

Narrow/ Tiered Network

Impact on Plan Choice of Shift From Defined Benefit to Defined Contribution

Liazon Corporation1

70%

“Very few people spend other people’s money as carefully as they spend their own.”

Milton FriedmanNobel Prize-Winning Economist

GSMC 2014 Fall Conference & Annual Meeting 13

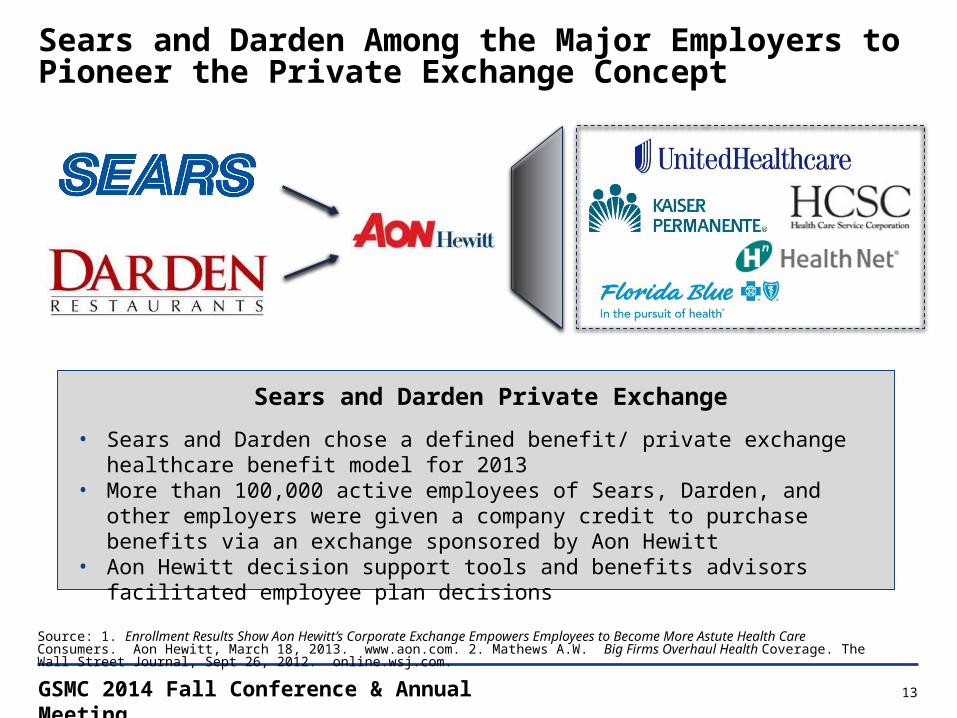

Sears and Darden Among the Major Employers to Pioneer the Private Exchange Concept

Source: 1. Enrollment Results Show Aon Hewitt’s Corporate Exchange Empowers Employees to Become More Astute Health Care Consumers. Aon Hewitt, March 18, 2013. www.aon.com. 2. Mathews A.W. Big Firms Overhaul Health Coverage. The Wall Street Journal, Sept 26, 2012. online.wsj.com.

Sears and Darden Private Exchange

• Sears and Darden chose a defined benefit/ private exchange healthcare benefit model for 2013

• More than 100,000 active employees of Sears, Darden, and other employers were given a company credit to purchase benefits via an exchange sponsored by Aon Hewitt

• Aon Hewitt decision support tools and benefits advisors facilitated employee plan decisions

GSMC 2014 Fall Conference & Annual Meeting 14

Many Participants Shifted to CDHPs in the First Year of the Sears and Darden Private Exchange

Sears and Darden found that choice of plans changed when employees were presented with expanded plan options and control over employer subsidy

Source: Mathews A.W. To Save, Workers Take on Health-Cost Risk. The Wall Street Journal, Mar 17 2013. online.wsj.com.

2012 2013

70%

47%

18%

14%

12%

39%

Consumer-Directed Health PlanHMOPPO

Distribution of Sears and Darden Employee Health Benefits by Type of Plan

GSMC 2014 Fall Conference & Annual Meeting 15

Transparency Tools Are a Key Catalyst for High Deductible Impact

• Growth in high deductible plans has prompted payers and employers to develop price transparency tools revealing cost and quality data to members

• Informed patients are likely to choose the “low-cost/high-quality” providers when faced with increased cost sharing

• Providers in competitive markets are at risk of revenue and market share erosion as payers and patients become aware of reimbursement variance

• Improving cost structure and competing on value is the only viable long-term option

Select Companies Offering Transparency Tools

GSMC 2014 Fall Conference & Annual Meeting 16

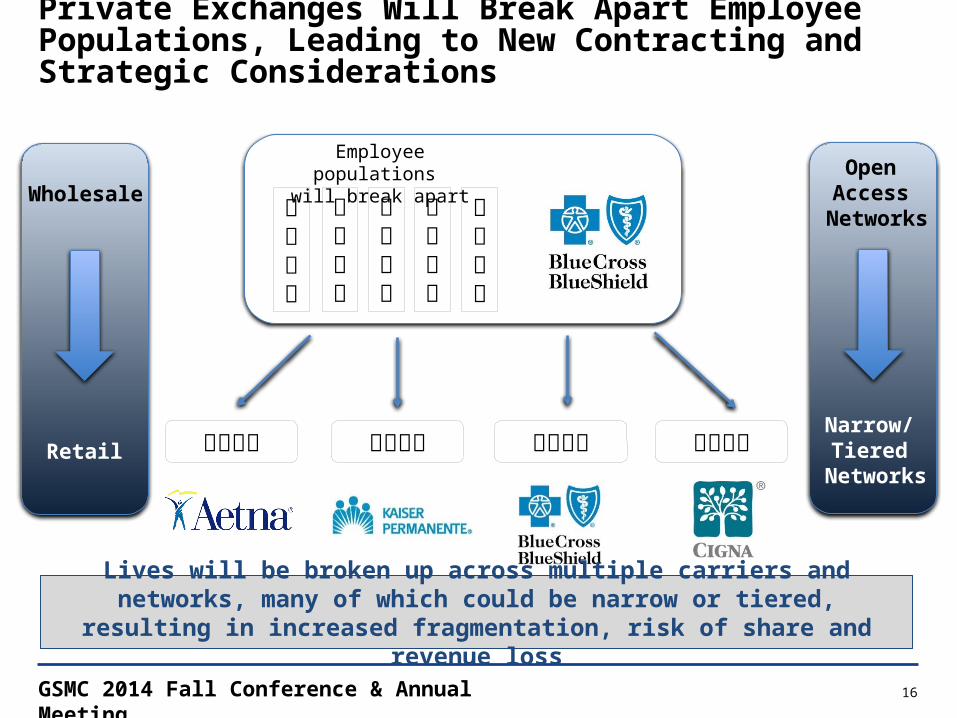

Private Exchanges Will Break Apart Employee Populations, Leading to New Contracting and Strategic Considerations

Employee populations will break apart

Lives will be broken up across multiple carriers and networks, many of which could be narrow or tiered, resulting in increased fragmentation, risk of share and revenue loss

Open Access

Networks

Narrow/ Tiered

Networks

Wholesale

Retail

GSMC 2014 Fall Conference & Annual Meeting 17

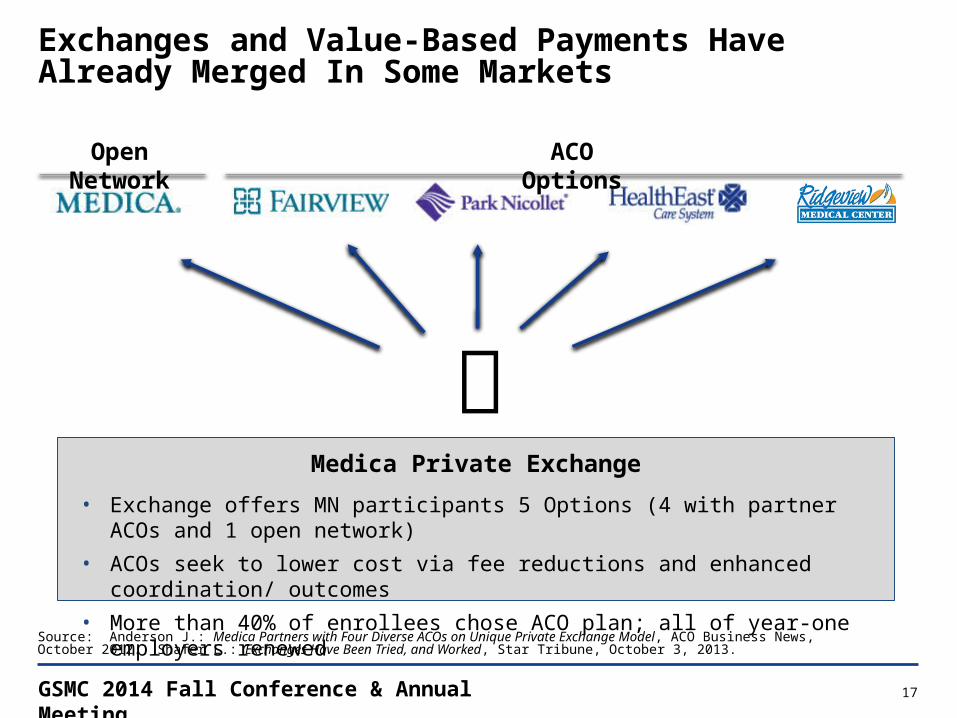

Exchanges and Value-Based Payments Have Already Merged In Some Markets

Medica Private Exchange

• Exchange offers MN participants 5 Options (4 with partner ACOs and 1 open network)• ACOs seek to lower cost via fee reductions and enhanced coordination/ outcomes• More than 40% of enrollees chose ACO plan; all of year-one employers renewed

Open Network ACO Options

Source: Anderson J.: Medica Partners with Four Diverse ACOs on Unique Private Exchange Model, ACO Business News, October 2012. Shafer L.: Exchanges Have Been Tried, and Worked, Star Tribune, October 3, 2013.

GSMC 2014 Fall Conference & Annual Meeting 18

Today’s Model Emerging Models

Implications

Expected to decline over time

Likely near-term model of choice

Expected to increase over time as narrow/tiered networks mature

Risk of Share Loss

Price Pressure

Bad Debt

Use Rate Pressure

Private Exchanges

Limited Threat Significant Threat

Open Access PPO High Deductible Narrow/Tiered

Private Exchanges Will Accelerate the Transition to Emerging Payment Models and Create New Strategic/ Financial Challenges

GSMC 2014 Fall Conference & Annual Meeting 19

Public Exchange Update

GSMC 2014 Fall Conference & Annual Meeting 20

Public Exchange Update and Analysis – National

GSMC 2014 Fall Conference & Annual Meeting 21

Public Exchange Enrollment Surpassed both Incremental and Cumulative Administration Targets for March

Notes: (1) HHS definition of enrollment (those who have “selected a plan”) (2) March data includes Special Enrollment Period through 19 April 2014 (3)Percentage of HHS enrollment target. Sources: ASPE, Health Insurance Marketplace Enrollment Reports, 13 Nov 2013, 11 Dec 2013, 13 Jan 2014, 12 Feb 2014, 11 Mar 2014, and 1 May 2014. Tavenner M, Projected Monthly Enrollment Targets for Health Insurance Marketplaces in 2014, 5 Sept 2013.

Public Exchange Enrollment

• National public exchange enrollment increased to 8.0M during the initial enrollment period

• Administration 2014 enrollment goal was 7.1M

% Target3 21% 65%30%

Cumulative U.S. Public Exchange Enrollment1

Thousands

Oct Nov Dec Jan Feb Mar106 364

2,153

3,300 4,242

8,020

75% 75% 113%

2

GSMC 2014 Fall Conference & Annual Meeting 22

The Vast Majority of Those Enrolled Nationally Chose Silver and Bronze Plans

Plan Choice Trends• 85% of those enrolled nationally

chose cheaper Bronze or Silver plans• Silver plans (eligible for cost-sharing

subsidies) are the most popular and account for 65% of all enrollment

National Plan Selection by Metal Level Initial Enrollment Period1

20%

65%9%

5%

2% Silver

Bronze

Gold

Platinum

Cat. (2%)2

Notes: (1) Includes additional special enrollment period activity through 19 April 2014. (2) Catastrophic plan. Source: ASPE, Health Insurance Marketplace Enrollment Report, 1 May 2014.

GSMC 2014 Fall Conference & Annual Meeting 23

Initial National Public Exchange Enrollment Skews Older Than Administration Targets

National6%

28%

17%

23%

25%

55 - 64

45 - 54

35 - 44

18 - 34

<18

National Exchange Age DistributionInitial Enrollment Period1

• Enrolling young and healthy people is critical to a stable risk pool• Age 18-34 enrollment lags the 39% administration target• How enrollment compares to health plan expectations will dictate plan profitability• The “3Rs” will mitigate premium changes in the near to medium term

Note: (1) Includes additional special enrollment period activity through 19 April 2014. Source: ASPE, Health Insurance Marketplace Enrollment Report, 1 May 2014.

Well below national HHS 18-34 target of 39%

GSMC 2014 Fall Conference & Annual Meeting 24

Despite Recent Improvements, the Previously Uninsured Represent Only About Half of the National Enrollment

Notes: McKinsey data from 11/25 to 1/10 survey, Feb 4 to Feb 13 survey, and April 7 to April 16 survey; Broker/consultant estimates from 1/17 WSJ article. Sources: Weaver C and Mathews A, Exchange See Little Progress on Uninsured, WSJ, 17 Jan, 2014; Demko P, 27% of 2014 Individual Market Enrollees Previously Lacked Coverage, Study Says, Modern Healthcare, March 2014: Hamel L, Rao M, Levitt L, Claxton G, Cox C, Pollitz K, Brodie M, Survey of Non-Group Health Insurance Enrollees, Kaiser Family Foundation, 19 June, 2014..

% of Public Exchange Enrollment by UninsuredNational Surveys

Nov 25 - Jan 10McKinsey

Feb 4 - Feb 13McKinsey

April 7 - April 16 McKinsey

June 19 Kaiser

11%

27% 26%

57%

• McKinsey surveys suggest that a majority of those enrolled nationally previously had individual or employer coverage

• Broker/ consultant data from mid-January found that 33% were previously uninsured• Kaiser Family Foundation Survey of small sampling suggests that 57% were previously uninsured

GSMC 2014 Fall Conference & Annual Meeting 25

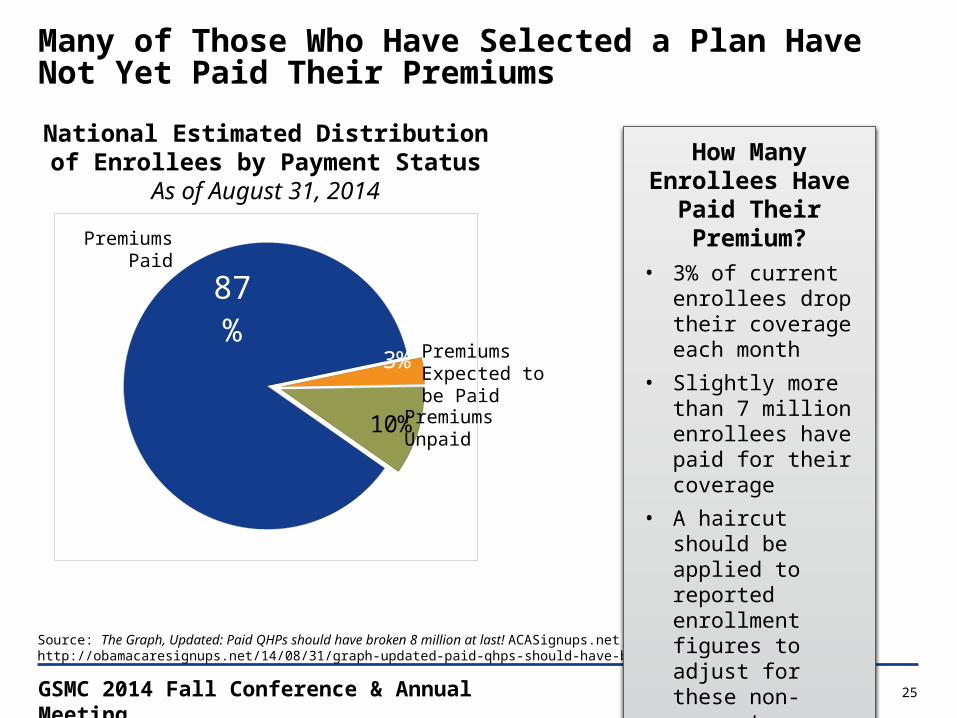

Many of Those Who Have Selected a Plan Have Not Yet Paid Their Premiums

Source: The Graph, Updated: Paid QHPs should have broken 8 million at last! ACASignups.net, August 31, 2014, http://obamacaresignups.net/14/08/31/graph-updated-paid-qhps-should-have-broken-8-million-last-92m-total

How Many Enrollees Have Paid Their

Premium?• 3% of current

enrollees drop their coverage each month

• Slightly more than 7 million enrollees have paid for their coverage

• A haircut should be applied to reported enrollment figures to adjust for these non-payments

National Estimated Distribution of Enrollees by Payment Status

As of August 31, 2014

87%

3%

10%PremiumsUnpaid

Premiums Paid

Premiums Expected to be Paid

GSMC 2014 Fall Conference & Annual Meeting 26

Public Exchange Update and Analysis – Georgia

GSMC 2014 Fall Conference & Annual Meeting 27

Georgia Is One of 28 Federally Facilitated Exchanges

Source: Kaiser Family Foundation, www.statehealthfacts.org. State Decisions For Creating Health Insurance Exchanges as of Oct. 2013.

177

GSMC 2014 Fall Conference & Annual Meeting 28

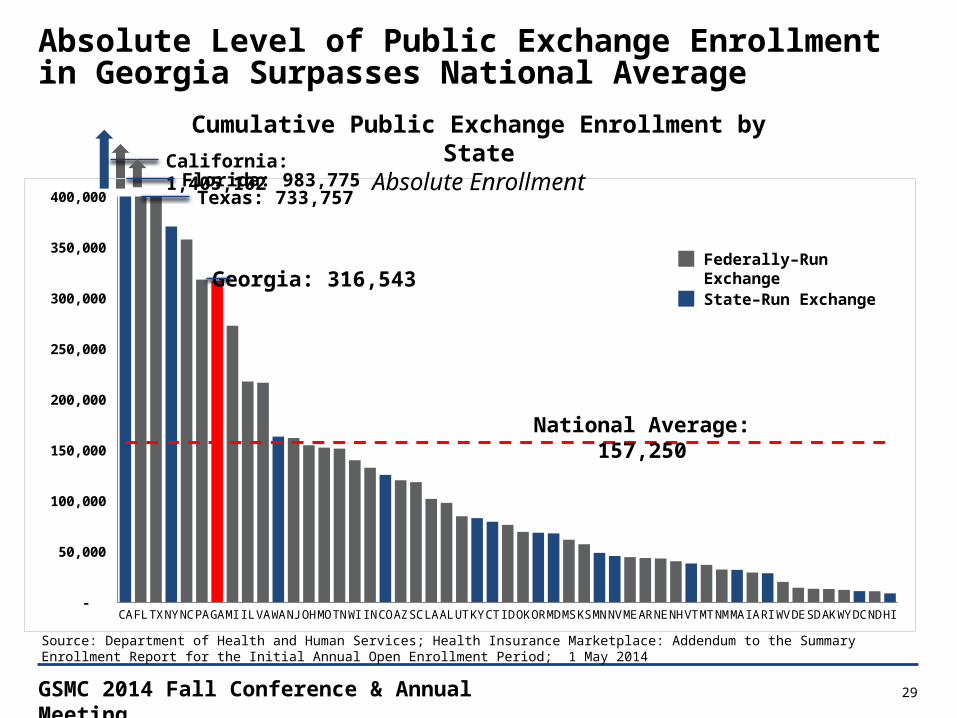

Public Exchange Enrollment in Georgia Surpassed Administration Targets

Notes: (1) HHS definition of enrollment (those who have “selected a plan”) (2) March data includes Special Enrollment Period through 19 April 2014 (3)Percentage of HHS enrollment target. Sources: ASPE, Health Insurance Marketplace Enrollment Reports, 13 Nov 2013, 11 Dec 2013, 13 Jan 2014, 12 Feb 2014, 11 Mar 2014, and 1 May 2014. Tavenner M, Projected Monthly Enrollment Targets for Health Insurance Marketplaces in 2014, 5 Sept 2013.

Public Exchange Enrollment

• GA public exchange enrollment increased to 316,543

• Full year HHS target was 204,000

• Enrollment in GA reached 155% of HHS initial enrollment target% Target3 10% 61%20%

Cumulative Georgia Enrollment1

Oct Nov Dec Jan Feb Mar1,390 6,859

58,611

101,276 139,371

316,543

80% 85% 155%

2

GSMC 2014 Fall Conference & Annual Meeting 29

CA TX NC GA IL WA OH TN IN AZ LA UT CT OK

MD KS NV AR NH MTMA RI DE AK DC HI

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Cumulative Public Exchange Enrollment by StateAbsolute Enrollment

Florida: 983,775

Absolute Level of Public Exchange Enrollment in Georgia Surpasses National Average

Federally–Run Exchange

State–Run Exchange

Source: Department of Health and Human Services; Health Insurance Marketplace: Addendum to the Summary Enrollment Report for the Initial Annual Open Enrollment Period; 1 May 2014

Georgia: 316,543

National Average: 157,250

California: 1,405,102

Texas: 733,757

GSMC 2014 Fall Conference & Annual Meeting 30

CT NH ME NC DE NY NJ PA UTMO TN MT LA CA NE IN HI

AR OKMN SD AK

MDNM OR MA

0%

50%

100%

150%

200%

250%

Georgia Also Surpasses National Averages as a Percentage of HHS Targets

Federally–Run Exchange

State–Run ExchangeGeorgia: 155%

National Average: 113%

Cumulative Public Exchange Enrollment by State% of HHS Targets

Source: Department of Health and Human Services; Health Insurance Marketplace: Addendum to the Summary Enrollment Report for the Initial Annual Open Enrollment Period; 1 May 2014

GSMC 2014 Fall Conference & Annual Meeting 31

20%

65%9%

5%2%

Bronze and Silver Plans Make Up 82% of Public Exchange Enrollment in Georgia

• Plan selection in Georgia skews toward low cost Silver and Bronze plans but slightly less so than the national average

Georgia

11%71%

7%

10%2%

Gold

Cat. (2%) 2 Silver

Bronze

Gold

Platinum

Cat. (2%)

Note: (1) Includes additional special enrollment period activity through 19 April 2014. (2) Catastrophic plan Source: ASPE, Health Insurance Marketplace Enrollment Report, 1 May 2014.

Plan Selection by Metal Level Initial Annual Open Enrollment Period1

National

Silver

Bronze

Platinum

GSMC 2014 Fall Conference & Annual Meeting 32

Age Distribution of Georgia and National Enrollment Are Similar

Georgia National5% 6%

32% 28%

20%17%

23%23%

21%25%

55 – 64

45 – 54

35 – 44

18 – 34

<18

• Georgia has a slightly lower percentage of enrollees between the ages of 55 and 64 than the national average

• 32% of Georgia enrollees are in the pivotal 18–34 cohort, which is slightly higher than the national average (28%) and well below the administration target (39%)

Note: (1) Includes additional special enrollment period activity through 19 April 2014. Source: ASPE, Health Insurance Marketplace Enrollment Report, 1 May 2014.

Exchange Age DistributionInitial Enrollment Period1

GSMC 2014 Fall Conference & Annual Meeting 33

Georgia Bronze Premiums Are Slightly Higher than the National Average

WY AK MS CT VT NJ ME DE IN SD WI NH NC ND WV CA NY AR SC GA LA RI WA OH FL MTAvg. AL MO NE VA CO PA ID NV MI NM AZ IA TX OR DC IL UT KS MD TN OK MN$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$265

Monthly Premium of Lowest Cost Individual Bronze Plan in State1

National Avg: $249

Note: 1) Age weighting for all states is based on expected age distribution in the Marketplaces, estimated by the RAND Corporation.Source: APSE Issue Brief, Health Insurance Marketplace Premiums for 2014, Health and Human Services, avail able at: aspe.hhs.gov (accessed Oct 1, 2013).

$144

$425

GSMC 2014 Fall Conference & Annual Meeting 34

Georgia’s Five Individual Market Plans Puts the State Toward the Middle of the Pack

Source: Avalere Health, Analysis on Health Plan Offerings on the Federally-Facilitated Marketplace, 3 Oct 2013.

Insurer Competition by StateIndividual Market

GSMC 2014 Fall Conference & Annual Meeting 35

Georgia Health Insurance Exchange Participants – Blue Cross Blue Shield of Georgia Plans are Available State Wide

Georgia Public Individual Exchange Participants

Georgia Public SHOP Exchange Participants

Source: Miller, A.: UnitedHealthcare to be fourth company to offer insurance in State Exchange next year, The Augusta Chronicle, July 14, 2014

GSMC 2014 Fall Conference & Annual Meeting 36

Drivers That Could Impact Commercial Shift and Employer “Dumping” to Public Exchanges

Driver Influence Factors Shift Impact

Firm Size Small firms are more likely to choose SHOP exchanges or dump to HIX

↑Subsidy/ Tax Credits Subsidy and tax credit availability will stimulate exchange uptake

Delivery Cost Favorable insurer network contracts will increase plan participation and pressure on employers to shift

Wages/ Part-Time Workforce/ Retirees

Low-wage geographies will have greater subsidy availability; part-time employees and pre-65 retirees more apt to shift

Exchange Implementation and Promotion

Good communication, promotion, and receptivity will stimulate enrollment ↔

Timing Uptake could initially be slow but increase over time once the market settles out, particularly if the “me too” effect takes hold

Recruitment and Retention

Higher skilled/ wage employers who prioritize recruitment and retention may not be willing to shift to public exchanges

↓Exchange Plan Options and Premiums Fewer plan options and higher premiums will delay uptake

Penalties Employer responsibility penalties a key deterrent for larger employers; fear among some that penalties could be increased in the future

GSMC 2014 Fall Conference & Annual Meeting 37

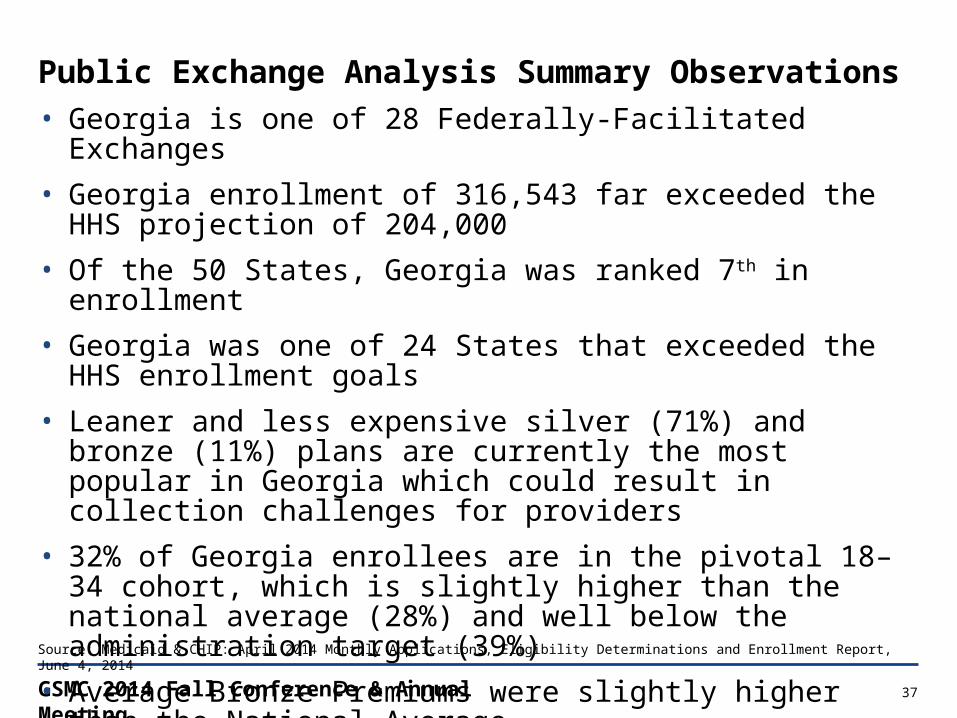

Public Exchange Analysis Summary Observations• Georgia is one of 28 Federally-Facilitated Exchanges• Georgia enrollment of 316,543 far exceeded the HHS projection of

204,000• Of the 50 States, Georgia was ranked 7th in enrollment• Georgia was one of 24 States that exceeded the HHS enrollment goals• Leaner and less expensive silver (71%) and bronze (11%) plans are

currently the most popular in Georgia which could result in collection challenges for providers

• 32% of Georgia enrollees are in the pivotal 18–34 cohort, which is slightly higher than the national average (28%) and well below the administration target (39%)

• Average Bronze Premiums were slightly higher than the National Average

• There was a decent selection of plans available in GeorgiaSource: Medicaid & CHIP: April 2014 Monthly Applications, Eligibility Determinations and Enrollment Report, June 4, 2014

GSMC 2014 Fall Conference & Annual Meeting 38

Narrow Network Considerations

GSMC 2014 Fall Conference & Annual Meeting 39

0%

20%

40%

60%

80%

100%

120%

72%

2014 Limited Network Percentage of Plan Offerings By StateFederal Exchange States

Note: Limited network defined as EPO and HMO plans. Survey results exclude the 49% of respondents who indicated that they “did not know” their exchange contract network plan design.Source: Health Insurance Marketplace Premiums for 2014 Databook (Information Current as of Sept 18, 2013); MHA member survey.

Limited Network Penetration

• Network adequacy regulations, hospital competition, spare capacity will influence prevalence

• 72% of plans offered on Georgia’s exchange were narrow network plans

Limited Networks Will Have a Significant Presence on the Georgia Public Exchange

GSMC 2014 Fall Conference & Annual Meeting 40

Commercial Market Share by Service Area

PSA SSA PSA + SSA0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

52%

29%46%

23%

6%

18%

25%

65%

36%

Other CompetitorsCompetitor 1Client

Mar

ket S

hare

Tot. Discharges

Tot. Discharges

Tot. Discharges

Conceptual Illustration

GSMC 2014 Fall Conference & Annual Meeting 41

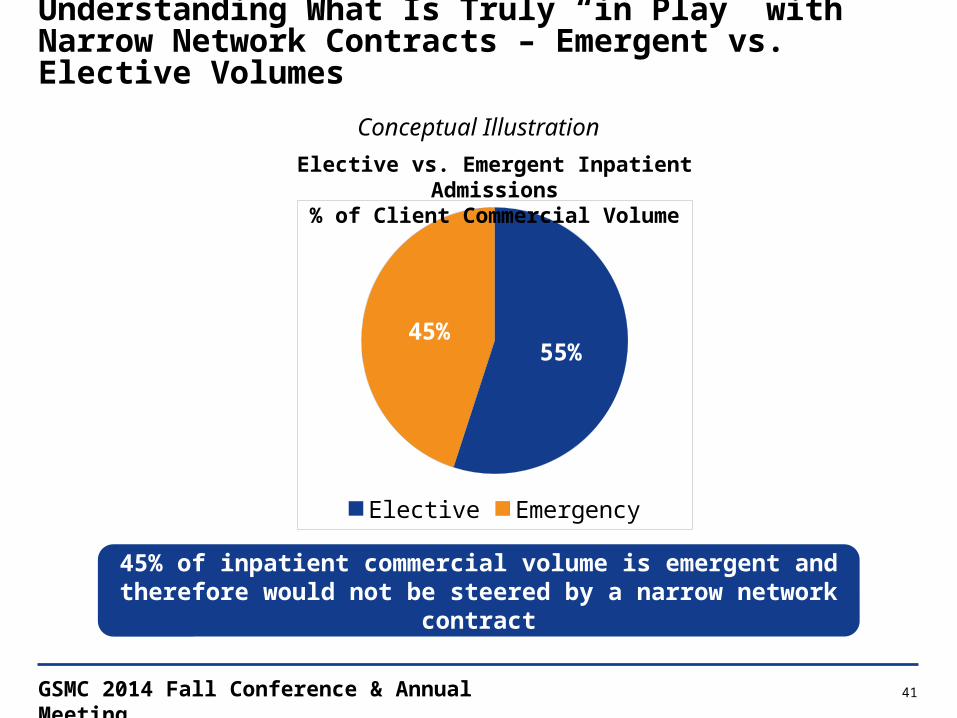

Understanding What Is Truly “in Play” with Narrow Network Contracts – Emergent vs. Elective Volumes

45% of inpatient commercial volume is emergent and therefore would not be steered by a narrow network contract

55%45%

Elective Emergency

Elective vs. Emergent Inpatient Admissions% of Client Commercial Volume

Conceptual Illustration

GSMC 2014 Fall Conference & Annual Meeting 42

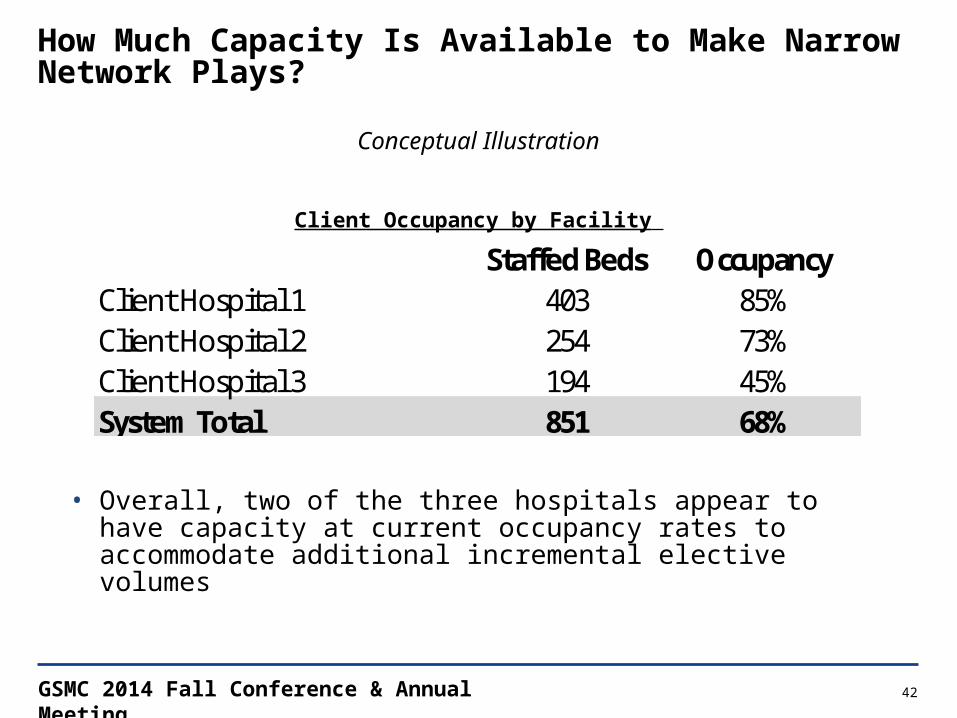

How Much Capacity Is Available to Make Narrow Network Plays?

Client Occupancy by Facility

Staffed Beds OccupancyClient Hospital 1 403 85%Client Hospital 2 254 73%Client Hospital 3 194 45%System Total 851 68%

• Overall, two of the three hospitals appear to have capacity at current occupancy rates to accommodate additional incremental elective volumes

Conceptual Illustration

GSMC 2014 Fall Conference & Annual Meeting 43

Key Considerations for Narrow Network ParticipationKey Consideration Steps:

1. Evaluate market share of local competitors to quantify if additional share can be gained • How much volume is potentially at risk if you do not participate?

2. Based on available market share, evaluate elective vs. emergent split – how much elective volume can you expect to gain?

3. Does the organization have the capacity to handle the additional volume?

4. What discounts will be required to participate in narrow networks and are individuals likely to choose narrow networks?

In pursuing a narrow network contract, is it worth discounting rates to obtain additional volume, and if so, by how much?

GSMC 2014 Fall Conference & Annual Meeting 44

Summary Implications

GSMC 2014 Fall Conference & Annual Meeting 45

What is the optimal way to balance these threats and opportunities?

Balancing New Revenue Opportunities and Cannibalizing the Existing Commercial Business

Uninsured Exchange

Commercial

Exchange

New Rev. Lost Rev.

GSMC 2014 Fall Conference & Annual Meeting 46

Summary Implications• Exchanges will catalyze the shift of purchasing healthcare benefits from

the wholesale to the retail channel• This channel shift will change the behavioral economics of plan

purchasing decisions and increase the prevalence of high deductible and narrow network plans

• Value-based reimbursement will increase over the long-term as pricing and cost pressures grow, which will require improved cross-continuum care coordination

• Competing on value and improving cost structure are the only viable long-term options for continued growth

GSMC 2014 Fall Conference & Annual Meeting 47

How Do You Prepare for the Increasing Shift to Public and Private Exchanges?Kaufman Hall believes that operational and financial success with healthcare exchanges requires an integrated planning framework

• Strategic Planning: A Health Insurance Exchange Strategy will be necessary to compete in the changing market environment. New reimbursement and contract models, in addition to FFS, will be used for exchange-based products, most likely requiring providers to assess and acquire new strategies and tactics

• Financial Planning: Many health systems and providers are in the early stages or have not yet begun to plan for how health insurance exchanges will impact their current and future patient populations and revenue base. A thorough analysis and plan to quantify the implications and potential financial impact should be completed

• Tactical Planning: New skills and capabilities will certainly be required for financial and operational success when working with health insurance exchanges. Developing the right tactical plan, resources, and investments while taking into consideration specific opportunities, priorities, risks, and benefits will be necessary

Exchanges are expanding; make sure your organization is prepared

GSMC 2014 Fall Conference & Annual Meeting 48

Discussion/ Questions

GSMC 2014 Fall Conference & Annual Meeting 49

COMPREHENSIVE SOFTWARE SUITE

Over 1,400 software licenses are in place

nationwide. The ENUFF Software Suite uses

corporate finance principles to directly support the

financial management cycle

CAPITAL ALLOCATIONKaufman Hall helps

organizations design and implement capital allocation

processes which provide consistent and rigorous

methodologies to guide the capital decision-making

process

MERGERS, ACQUISITIONS, AND DIVESTITURES

Kaufman Hall has advised on hundreds of M&A-related

engagements including analyzing, structuring,

negotiating and executing mergers, acquisitions,

divestitures, joint ventures, strategic partnerships and

affiliations

FINANCIAL AND CAPITAL PLANNING

Introduced concept of strategic financial planning to

healthcare field in 1983. Kaufman Hall has prepared

financial and capital plans for over 800 hospitals and

healthcare systems

STRATEGIC SERVICES

Kaufman Hall provides a broad range of strategy-

related services to support organizational management

and decision making. Kaufman Hall pioneered the

development of the integrated strategic financial

plan

CAPITAL MARKETS

Since 1985, Kaufman Hall has acted as financial advisor to more than 1050 healthcare debt transactions. Total debt and swaps issued on behalf of our clients exceeds $105

billion and $50 billion, respectively

Kaufman Hall Services at a Glance

GSMC 2014 Fall Conference & Annual Meeting 50

Kalani Redmayne, Assistant Vice PresidentKalani Redmayne is an Assistant Vice President at Kaufman Hall and a member of the firm’s Strategy practice. In this role, she provides strategic planning advisory services for a wide range of clients, including healthcare systems, academic medical centers, and community hospitals. Ms. Redmayne’s responsibilities focus on payer-provider strategies, alternative reimbursement methodologies, health plan and service operations, healthcare reform, payer relations and product development.

Ms. Redmayne has more than 20 years of experience in the healthcare industry. Prior to joining Kaufman Hall, Ms. Redmayne was Vice President of Product Development and Management for UnitedHealthcare, Inc., where she focused on Medicare Advantage, Medicare Supplement, Prescription Drug Plans and UnitedHealthcare’s private exchange products. During her 15 year tenure with UnitedHealthcare, Inc, Ms. Redmayne held other senior positions in Sales Operations, Sales and Marketing, and Marketing Operations. Before UnitedHealthcare, she spent five years as a sales executive with Downey Community Hospital/HealthFirst Medical Group.

Contact Ms. Redmayne at 310.227.8988 or [email protected]

GSMC 2014 Fall Conference & Annual Meeting 51

Qualifi cati ons, Assumpti ons and Limiti ng Conditi ons (v.12.08.06):This Report is not intended for general circulati on or publicati on, nor is it to be used, reproduced, quoted or distributed for any purpose other than those that may be set forth herein without the prior writt en consent of Kaufman, Hall & Associates, Inc. (“Kaufman Hall”).All informati on, analysis and conclusions contained in this Report are provided “as-is/where-is” and “with all faults and defects”. Informati on furnished by others, upon which all or porti ons of this report are based, is believed to reliable but has not been verifi ed by Kaufman Hall. No warranty is given as to the accuracy of such informati on. Public informati on and industry and stati sti cal data, including without limitati on, data are from sources Kaufman Hall deems to be reliable; however, neither Kaufman Hall nor any third party sourced make any representati on or warranty to you, whether express or implied, or arising by trade usage, course of dealing, or otherwise. This disclaimer includes, without limitati on, any implied warranti es of merchantability or fi tness for a parti cular purpose (whether in respect of the data or the accuracy, ti meliness or completeness of any informati on or conclusions contained in or obtained from, through, or in connecti on with this report), any warranti es of non-infringement or any implied indemniti es.The fi ndings contained in this report may contain predicti ons based on current data and historical trends. Any such predicti ons are subject to inherent risks and uncertainti es. In parti cular, actual results could be impacted by future events which cannot be predicted or controlled, including, without limitati on, changes in business strategies, the development of future products and services, changes in market and industry conditi ons, the outcome of conti ngencies, changes in management, changes in law or regulati ons. Kaufman Hall accepts no responsibility for actual results or future events.The opinions expressed in this report are valid only for the purpose stated herein and as of the date of this report.All decisions in connecti on with the implementati on or use of advice or recommendati ons contained in this report are the sole responsibility of the client.In no event will Kaufman Hall or any third party sourced by Kaufman Hall be liable to you for damages of any type arising out of the delivery or use of this Report or any of the data contained herein, whether known or unknown, foreseeable or unforeseeable.

5202 Old Orchard Road, Suite N700, Skokie, Illinois 60077847.441.8780 phone | 847.965.3511 fax

www.kaufmanhall.com

© 2014 Kaufman, Hall & Associates, Inc. All rights reserved.