© 2005 by robert f. halsey, all rights reserved inter-corporate investments market value...

Post on 20-Dec-2015

217 views

TRANSCRIPT

© 2005 by Robert F. Halsey, all rights reserved

Inter-corporate investments

Market value accounting (minority passive investments) Accounting Met Life mini-case

Equity method accounting (significant influence) Accounting Coca Cola mini-case

© 2005 by Robert F. Halsey, all rights reserved

Degree of Ownership

Minority

Majority

Passive - market method

Securities available for sale (Unrealized gains and losses to stockholder's equity)

Trading securities (Unrealized gains and losses to Income Statement)

Significant Influence - Equity method

Consolidate

Purchase method

The following is a general roadmap of the accounting for marketable securities:

>50%

<50%>20%

<20%

Ownership percentage

Required accounting

methodBalance sheet Income statement

Held-to-maturity bonds or equities w/ no public market

Cost Report investments at cost plus (less) unamortized premium (discount)

Income is interest received minus (plus) amortization of premium (discount)

< 20% and marketable“Passive”

Market Investment reported at FMV

Change in FMV is either in OCI (AFS) Income (Trading)Dividends are income

20 – 50 %“Significant Influence”

Equity Report investments at cost – dividends received proportionate chare of investee income

Dividends reported as reduction of investmentReport income equal to proportionate share of investee profits

> 50%“Control”

Consolidate Report balance sheet of subsidiary together w/ parent

Report income statement of subsidiary together w/ parent

© 2005 by Robert F. Halsey, all rights reserved

Minority Passive Investments –

Market Method Investor owns < 20% of investee Classify portfolio as “available-for-sale” or “trading.”

This classification dictates the accounting treatment Record dividends received as income Mark investments to market at each statement

date A = L + E ΔA = L + ΔE Q: Is ΔE income? A: AFS, no – record in OCI Trading, yes – record in net income Equity increases either way. The issue is

whether profit is affected.

© 2005 by Robert F. Halsey, all rights reserved

Met Life mini-case

Met Life B/S

Met Life Income Statement

Met Life’s

Statement of Stockholders’ Equity

Met Life’s

Investment Footnote

© 2005 by Robert F. Halsey, all rights reserved

Significant influence – Equity Method Investor owns > 20% and less than 50%.

The key is the ability to exert “significant influence.”

Dividends treated as a return of investment (reduce investment balance) rather than income

Report income equal to percentage interest in investee profits

Investment recorded at cost + profit recognized – dividends received.

Assume that HP acquires a 30% interest in Mitel Networks. On the date of acquisition, Mitel reports $1,000 of stockholders’ equity, and HP purchases its 30% stake for $300 (at book value).

Transaction or event Balance Sheet Income Statement

Cash Asset

+Other Assets

= Liabs +Cont. cap

Ret. Earn

Revenues Exp

1. 30% investment in Mitel

(300) 300

2. Mitel reports $100 income

30 3030

3. Mitel pays $20 dividends, $6 to HP

6 (6)

4. HP’s ending balance of its investment account

324

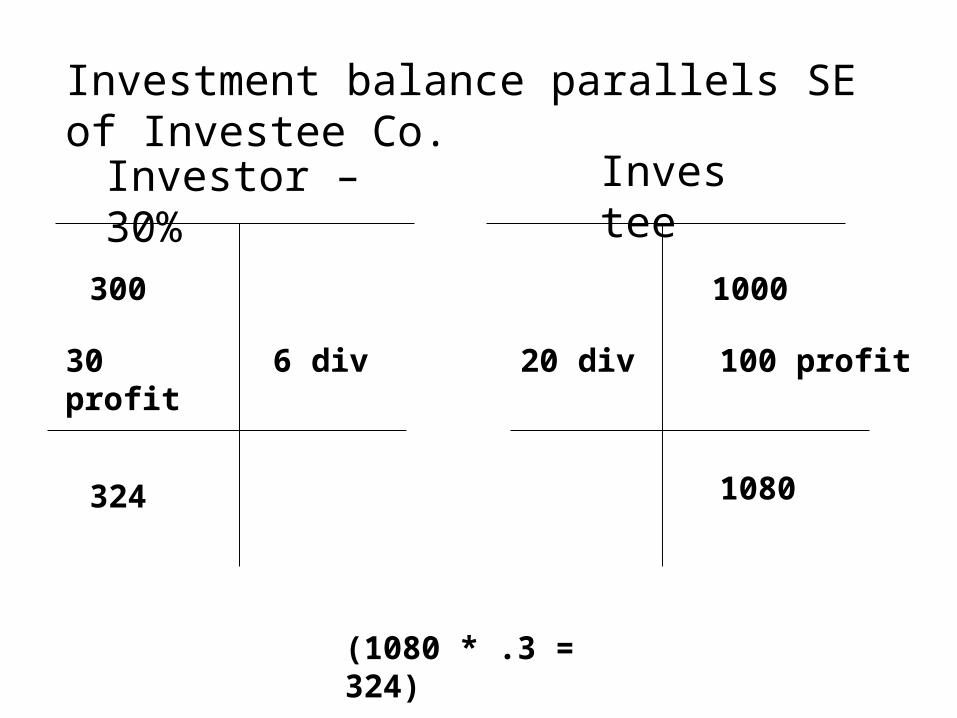

Investment balance parallels SE of Investee Co.

Investor – 30% Investee

1000300

100 profit30 profit 20 div6 div

1080324

(1080 * .3 = 324)

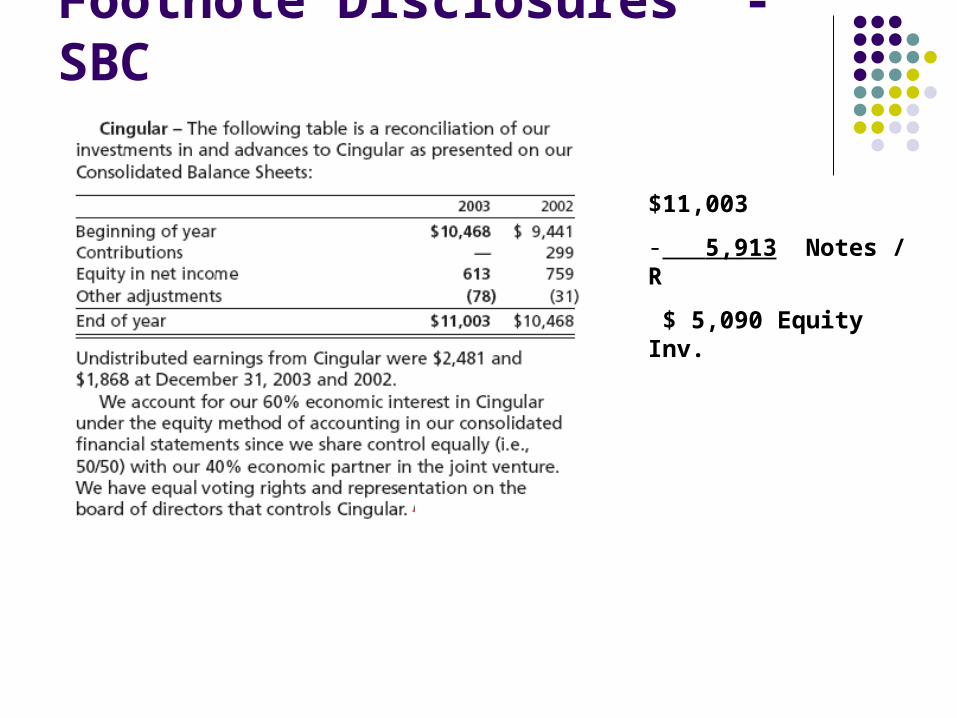

Footnote Disclosures - SBC

$11,003

- 5,913 Notes / R

$ 5,090 Equity Inv.

$3,300 + $22,226 - $3,187 - $13,855 = $8,484 x 60% = $5,090

$1,022 x 60% = $613

© 2005 by Robert F. Halsey, all rights reserved

Coca-Cola mini-case

© 2005 by Robert F. Halsey, all rights reserved

© 2005 by Robert F. Halsey, all rights reserved

© 2005 by Robert F. Halsey, all rights reserved

© 2005 by Robert F. Halsey, all rights reserved

© 2005 by Robert F. Halsey, all rights reserved

© 2005 by Robert F. Halsey, all rights reserved

Analysis Implications of Equity Method Investments Income does not equal Cash Flow

Regulations. Regulatory authorities can sometimes intervene in an investee company’s dividend policy.

International. An investee company may operate in a country where restrictions exist on remittance of earnings or where the value of currency can deteriorate rapidly. Political risks can further inhibit access to earnings.

Restrictions. Dividend restrictions in loan agreements can limit the ability of the investee company to make dividend payments from retained earnings.

Power. Presence of a stable or powerful minority interest can reduce the investor company’s ability to set dividend or other policies of the investee company.

© 2005 by Robert F. Halsey, all rights reserved

Analysis Implications of Equity Method Investments Net operating profit margin (NOPM NOPAT/Sales). Most analysts

include equity income in NOPAT since it relates to operating investments. The reported NOPM is, thus, overstated due to nonrecognition of investee sales and the recognition of investee income.

Net operating asset turnover (NOAT Sales/Average NOA). The equity investment balance is typically included in operating assets. This means that NOAT is understated due to nonrecognition of investee sales and overstated by nonrecognition of investee assets in excess of the investment balance. The net effect is, therefore, indeterminate (NOAT is overstated provided NOA exceeds sales, and understated otherwise.)

Financial leverage (FLEV Net financial obligations/Average equity). Financial leverage is understated due to nonrecognition of investee liabilities and the recognition of investee equity (the proportionate share of investee earnings is included in SBC’s income).

Although ROE components are affected, ROE is unaffected since income and equity are unaffected.

Book value does not equal market value. There can be significant unrealized gains in the equity method investment.

© 2005 by Robert F. Halsey, all rights reserved

Summary: exclusion of debt from B/S

Operating leases Leased asset/liability not recorded on B/S

Equity method investments Only record percentage of equity owned as an investment,

not full or proportionate assets and liabilities SPEs

A/R securitization / synthetic leases Executory contracts (product financing agreements)

Transfer of manufacturing assets to a SPE or other party with purchase agreement for output

© 2005 by Robert F. Halsey, all rights reserved

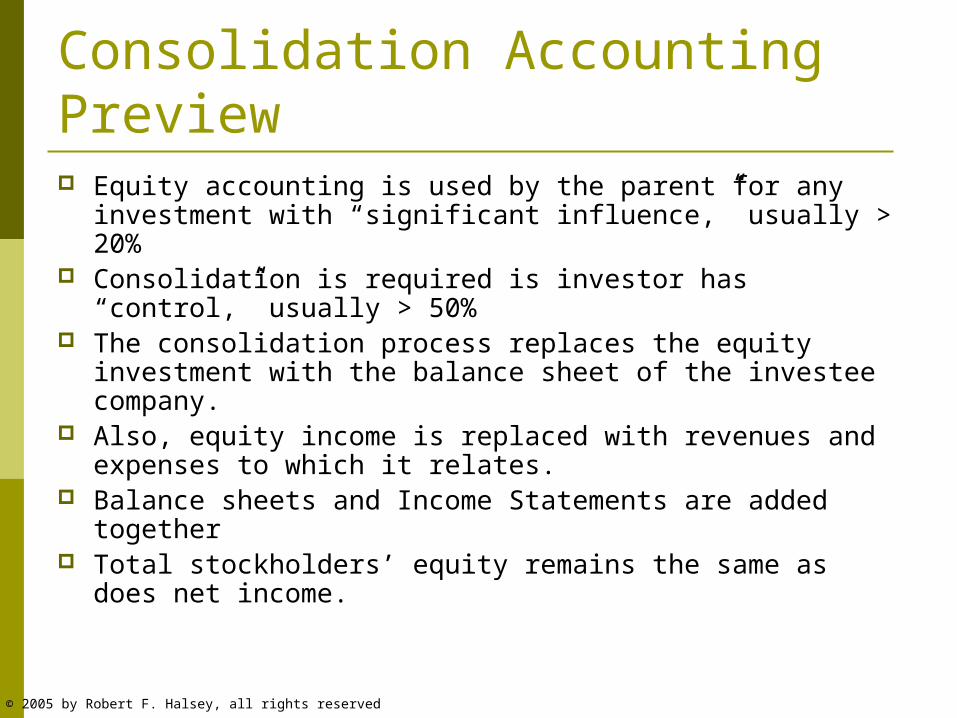

Consolidation Accounting Preview Equity accounting is used by the parent for any investment

with “significant influence,” usually > 20% Consolidation is required is investor has “control,” usually >

50% The consolidation process replaces the equity investment

with the balance sheet of the investee company. Also, equity income is replaced with revenues and

expenses to which it relates. Balance sheets and Income Statements are added together Total stockholders’ equity remains the same as does net

income.

© 2005 by Robert F. Halsey, all rights reserved