© 2004 south-western publishing 1 chapter 13 swaps and interest rate options

TRANSCRIPT

© 2004 South-Western Publishing 1

Chapter 13

Swaps and Interest Rate Options

2

Outline

Introduction Interest rate swaps Foreign currency swaps Circus swap Interest rate options

3

Introduction

Both swaps and interest rate options are relatively new, but very large– In mid-2000, there was over $60 trillion

outstanding in interest rate swaps, foreign currency swaps, and other interest rate options

4

Interest Rate Swaps

Introduction Immunizing with interest rate swapsExploiting comparative advantage in

the credit market

5

Introduction

Popular with bankers, corporate treasurers, and portfolio managers who need to manage interest rate risk

A swap enables you to alter the level of risk without disrupting the underlying portfolio

6

Introduction (cont’d)

The most common type of interest rate swap is the fixed for floating rate swap– One party makes a fixed interest rate payment to

another party making a floating interest rate payment

– Only the net payment is made (difference check)– The firm paying the floating rate is the swap seller– The firm paying the fixed rate is the swap buyer

7

Introduction (cont’d)

Typically, the floating interest rate is linked to a market rate such as LIBOR or T-bill rates

The swap market is standardized partly by the International Swaps and Derivatives Association (ISDA)– ISDA provisions are master agreements

8

Introduction (cont’d)

A plain vanilla swap refers to a standard contract with no unusual features or bells and whistles

The swap facilitator will find a counterparty to a desired swap for a fee or take the other side– A facilitator acting as an agent is a swap broker– A swap facilitator taking the other side is a swap

dealer (swap bank)

9

Introduction (cont’d)

Plain Vanilla Swap Example

A large firm pays a fixed interest rate to its bondholders, while a smaller firm pays a floating interest rate to its bondholders.

The two firms could engage in a swap transaction which results in the larger firm paying floating interest rates to the smaller firm, and the smaller firm paying fixed interest rates to the larger firm.

10

Introduction (cont’d)

Plain Vanilla Swap Example (cont’d)

Big Firm Smaller Firm

Bondholders Bondholders

LIBOR – 50 bp

8.05%

8.05% LIBOR +100 bp

11

Introduction (cont’d)

Plain Vanilla Swap Example (cont’d)

A facilitator might act as an agent in the transaction and

charge a 15 bp fee for the service.

12

Introduction (cont’d)

Plain Vanilla Swap Example (cont’d)

Big Firm Smaller Firm

Bondholders Bondholders

8.05% LIBOR +100 bp

Facilitator

LIBOR -50 bp

8.05% 8.20%

LIBOR -50 bp

13

Introduction (cont’d)

The swap price is the fixed rate that the two parties agree upon

The tenor is the term of the swap The notional value determines the size of

the interest rate payments Counterparty risk refers to the risk that one

party to the swap will not honor its part of the agreement

14

Immunizing With Interest Rate Swaps

Interest rate swaps can be used by corporate treasurers to adjust their exposure to interest rate risk

The duration gap is:

sliabilitieassetgap Dassets Total

sLiabilitie TotalDD

15

Immunizing With Interest Rate Swaps (cont’d)

A positive duration gap means a bank’s net worth will suffer if interest rates rise– The treasurer may choose to move the duration

gap to zero This could be accomplished by selling some of the

bank’s loans and holding cash equivalent securities instead

16

Immunizing With Interest Rate Swaps (cont’d)

Using the bank’s balance sheet, we can algebraically solve for the proportion of the firm’s assets to be held in cash so that the duration gap is zero:

0Dassets Total

sLiabilitie Total

-durationasset loan averagex100.0xD

sliabilitie

cashcashgap

17

Exploiting Comparative Advantage in the Credit Market

Interest rate swaps can be used to exploit differentials in the credit market

18

Exploiting Comparative Advantage in the Credit Market

Credit Market Example

AAA Bank and BBB Bank currently face the following borrowing possibilities:

Firm Fixed Rate Floating Rate

AAA Current 5-yr

T-bond + 25 bp

LIBOR

BBB Current 5-yr

T-bond + 85 bp

LIBOR + 30 bp

Quality Spread 60 bp 30 bp

19

Exploiting Comparative Advantage in the Credit Market

Credit Market Example (cont’d)

AAA Bank has an absolute advantage over BBB in both the fixed and the floating rate markets. AAA has a comparative advantage in the fixed rate market.

The total gain available to be shared among the swap participants is the differential in the fixed rate market minus the differential in the variable rate market, or 30 bps.

20

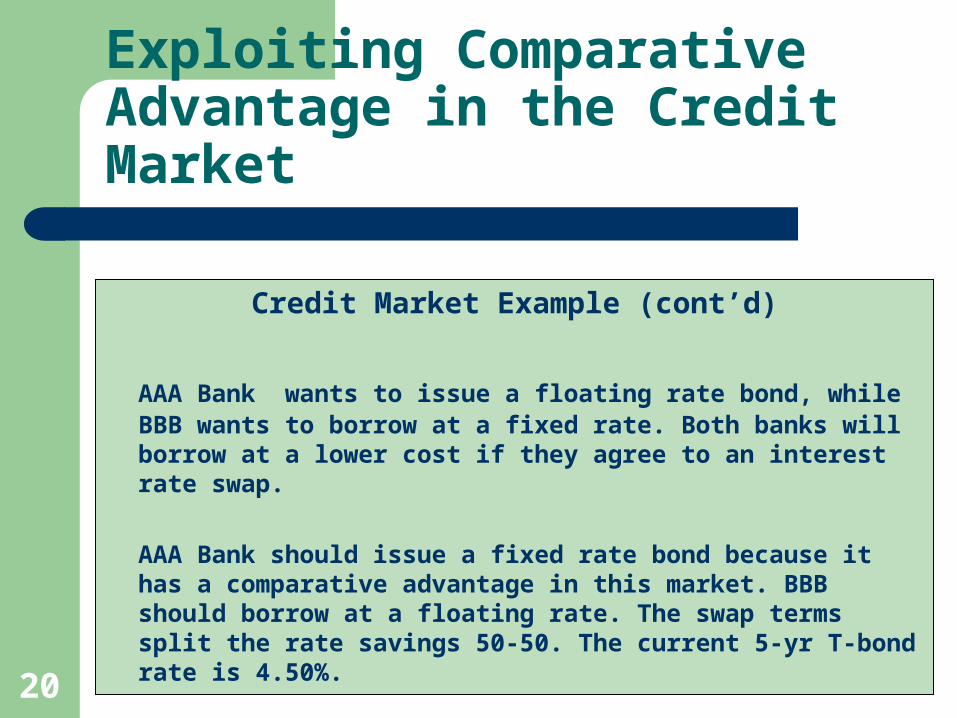

Exploiting Comparative Advantage in the Credit Market

Credit Market Example (cont’d)

AAA Bank wants to issue a floating rate bond, while BBB wants to borrow at a fixed rate. Both banks will borrow at a lower cost if they agree to an interest rate swap.

AAA Bank should issue a fixed rate bond because it has a comparative advantage in this market. BBB should borrow at a floating rate. The swap terms split the rate savings 50-50. The current 5-yr T-bond rate is 4.50%.

21

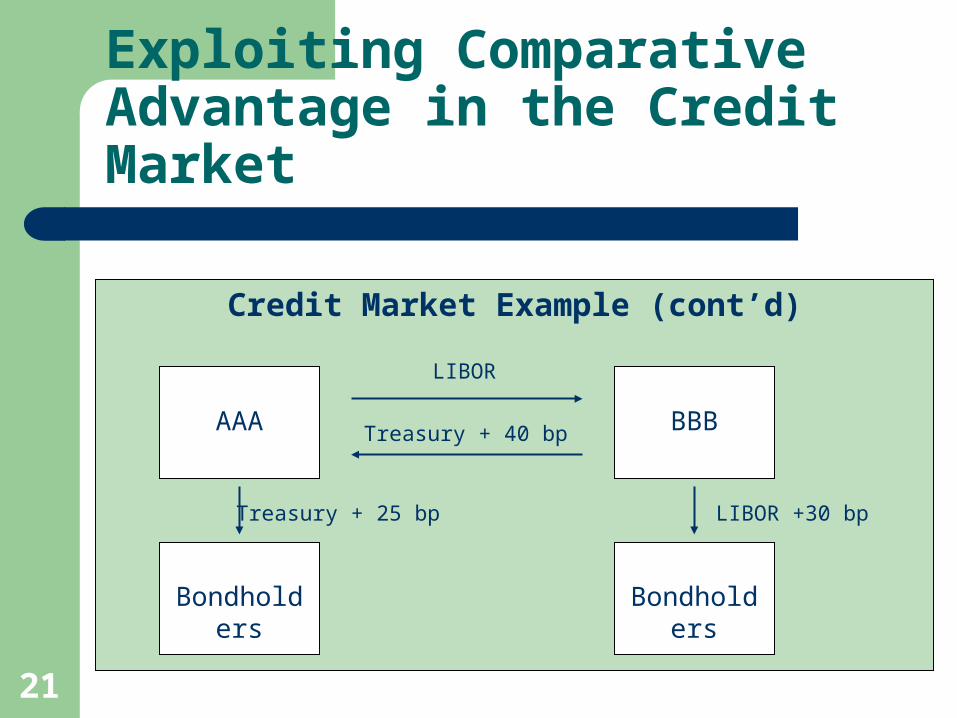

Exploiting Comparative Advantage in the Credit Market

Credit Market Example (cont’d)

AAA BBB

Bondholders Bondholders

LIBOR

Treasury + 40 bp

Treasury + 25 bp LIBOR +30 bp

22

Exploiting Comparative Advantage in the Credit Market

Credit Market Example (cont’d)

The net borrowing rate for AAA is LIBOR – 15 bps

The net borrowing rate for BBB is Treasury + 70 bps

The net rate for both parties is 15 bps less than without the swap.

23

Foreign Currency Swaps

In a currency swap, two parties– Exchange currencies at the prevailing exchange

rate – Then make periodic interest payments to each

other based on a predetermined pair of interest rates, and

– Re-exchange the original currencies at the conclusion of the swap

24

Foreign Currency Swaps (cont’d)

Cash flows at origination:

FX Principal

US $ PrincipalParty 1 Party 2

25

Foreign Currency Swaps (cont’d)

Cash flows at each settlement:

$ LIBOR

FX Fixed RateParty 1 Party 2

26

Foreign Currency Swaps (cont’d)

Cash flows at maturity:

US $ Principal

FX PrincipalParty 1 Party 2

27

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example

A multinational US corporation has a subsidiary in Germany. It just signed a 3-year contract with a German firm. The German firm will provide raw materials, with the US firm paying 1 million Euros every 6 months for the 3-year period. The current exchange rate is $0.90/Euro.

The contract is fixed in Euro terms, but if the dollar depreciates against the Euro, dollar accounts payable would increase.

28

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example (cont’d)

A currency swap is possible with the following terms:

Tenor = 3 years Notional value = 25 million Euros ($22.5 million) Floating rate = $ LIBOR Fixed rate = 8.00% on Euros

29

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example (cont’d)

The swap will result in the following payments every six months:

Fixed rate payment = 25,000,000 Euros x 8.00% x 0.5 = 1,000,000 Euros

Floating rate payment = $22.5 million x 0.5 x LIBOR

30

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example (cont’d)

Cash Flows at Origination

25 million euros

$22.5 million

Party 1 Party 2

31

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example (cont’d)

Cash Flows at Each Settlement

$ LIBOR

1 million euros

Party 1 Party 2

32

Foreign Currency Swaps (cont’d)

Foreign Currency Swap Example (cont’d)

Cash Flows at Maturity

$22.5 million

25 million euros

Party 1 Party 2

33

Circus Swap

Introduction Swap variations

34

Introduction

A circus swap combines an interest rate and a currency swap– Involves a plain vanilla interest rate swap and an

ordinary currency swap– Both swaps might be with the same

counterparty or with different counterparties

35

Introduction (cont’d)

Circus swap with two counterparties:

8% on Euros

$ LIBOR

Party 1 Party 2

36

Introduction (cont’d)

Circus swap with two counterparties (cont’d):

$ LIBOR

6.50% US

Party 1 Party 3

37

Introduction (cont’d)

Circus swap with two counterparties (cont’d):

8% on Euros

6.50% US

Party 1 Net

38

Introduction (cont’d)

Circus swap with two counterparties (cont’d):– Party 1 is effectively paying 8% on Euros and

receiving 6.5% in U.S. dollars

39

Swap Variations

Deferred swap Floating for floating swap Amortizing swap Accreting swap

40

Deferred Swap

In a deferred swap (forward start swap), the cash flows do not begin until sometime after the initiation of the swap agreement– If the swap begins now, the deferred swap is

called a spot start swap

41

Floating for Floating Swap

In a floating for floating swap, both parties pay a floating rate, but with different benchmark indices

42

Amortizing Swap

In an amortizing swap, the notional value declines over time according to some schedule

43

Accreting Swap

In an accreting swap, the notional value increases through time according to some schedule

44

Interest Rate Options

Introduction Interest rate cap Interest rate floor Calculating cap and floor payoffs Interest rate collar Swaption

45

Introduction

Most of the trading done off the exchange floors

The interest rate options market is– Very large– Highly efficient– Highly liquid– Easy to use

46

Introduction (cont’d)

Growth in Interest Rate OptionsNotional Value

0

5

10

15

1992 1993 1994 1995 1996 1997 1998 1999 2000

(Tril

lions

)

47

Interest Rate Cap

An interest rate cap– Is like a portfolio of European call options

(caplets) on an interest rate On each interest payment date over the life of the cap,

one option in the portfolio expires

– Is useful to firms with floating rate liabilities– Caps the periodic interest payments at the

caplet’s exercise price

48

Interest Rate Cap (cont’d)

Long interest rate cap (exercise price 7%)

$ Payoff

Option expires worthless

7%Floating Rate

Payoff

49

Interest Rate Cap (cont’d)

Short interest rate cap (exercise price 7%)

$ Payoff

Option expires worthless

7%Floating Rate

Payout

50

Interest Rate Floor

An interest rate floor– Is related to a cap in the same way that a put is

related to a call– Like a portfolio of European put options

(floorlets) on an interest rate On each interest payment date over the life of the cap,

one option in the portfolio expires

– Is useful to firms with floating rate assets– Puts a lower limit on the periodic interest

payments at the floorlet’s exercise price

51

Interest Rate Floor (cont’d)

Long interest rate floor (exercise price 6.5%)

$ Payoff

Option expires worthless

6.5%Floating Rate

Payoff

52

Interest Rate Floor (cont’d)

Short interest rate floor (exercise price 6.5%)

$ Payoff

Option expires worthless

6.5%Floating Rate

Payout

53

Calculating Cap and Floor Payoffs

There are no universally acceptable terms to caps and floors

However, frequently the terms provide for the cash payment on an in-the-money caplet or floorlet to be based on a 360-day year

54

Calculating Cap and Floor Payoffs (cont’d)

Cap payout formula:

If the benchmark rate is less than the exercise price, the payout is zero

price) striking-rate (benchmark360

periodpayment in Days value)(notionalpayout Cap

55

Calculating Cap and Floor Payoffs (cont’d)

Floor payout formula:

rate)benchmark - price (striking360

periodpayment in Days value)(notionalpayoutFloor

56

Interest Rate Collar

An interest rate collar is simultaneously long an interest rate cap and short an interest rate floor

Sacrifices some upside potential in exchange for a lower position cost– Premium from writing the floorlets reduces

position costs

57

Interest Rate Collar (cont’d)

$ Payoff

K2

Floating RateInflow

Outflow K1

No payout

Long cap

Short floor

58

Swaption

A swaption is an option on a swap Can be either American or European style A payer swaption (put swaption) gives its

owner the right to pay the fixed interest rate on a swap

A receiver swaption (call swaption) gives its owner the right to receive the fixed rate and pay the floating rate