© 2002 mouhamet diop national ict forum « towards full utilization of ict potential » banjul...

TRANSCRIPT

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 1

National ICT Forum« Towards full utilization

of ICT potential »ICT Development: Senegal Experience

National ICT Forum« Towards full utilization

of ICT potential »ICT Development: Senegal Experience

Mouhamet DIOPCEO NEXT SA

E-mail: [email protected]

Mouhamet DIOPCEO NEXT SA

E-mail: [email protected]

May 21st-22nd 2002May 21st-22nd 2002

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 2

AGENDAAGENDA

• National ICT Vision : The Internet Market, Needs & ambitions

• The regulatory environment: The market, the key players & the consumer

• Key Players Evolution & attitude: Telcos , ISP, Government

• National Infrastructure Evolution

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 3

Snapshot of the ICT SectorSnapshot of the ICT SectorPopulation : 9 037 106 htsSuperficie : 196 712 km2Currency : Franc CFAPIB : 550 USDNumber of villages : > 13.000

Data at Decembre 31 2000Land Line : 205 888Mobile Subscribers

Sonatel Mobiles : 195 508Sentel : 57 000

Villages connected : ~ 660«Rural Téléphony » ~ 5 %Internet Users > 100 000 Telecentres : 8 181 Telecentres lines: 11 773 Concentration Dakar : > 50 %

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 4

4

157 171

5

181

25

0

50

100

150

200

(in

Mill

ion

s)

Africa

Asia/P

acific

Europ

e

Mid

dle E

ast

Canad

a & U

SA

Latin

Am

erica

Internet Users (NUA Estimation )

Worldwide Internet UsersWorldwide Internet Users

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 5

Senegal National IndicatorsSenegal National Indicators

• Human Development 2000 (UNDP ranking) 152

• Population 1999 (millions) 9

• Population Density 1999 people per sq km 48

• Urbanization 1999 % of Population 47%

• Per Capita GNP 1999 $510.00

• Adult Literacy 1997 34.5%

• Gross Enrolment Rate for eligible age groups, 1997 (all levels of education) 35%

ECA/IDRC Pan-African initiative in e-Commerce -Regional Report on West Africa(UNDP Human Development Report 2000 - The World Bank World Development Report 2000/2001.)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 6

Senegal ICT Vision ProcessSenegal ICT Vision Process

• Senegal Vision 2015 – Survey in 1989• Survey on Teleservices• Closer approach on ICT• Interministerial council on ICT.• The 9th Economic and Social Development

Plan (1996-2001)• Special committee on ICT in the preparation of

the Economic and Social Development Plan• Survey for the implementation of an ICT

national strategy - 2001

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 7

National Development PlanNational Development Plan• Development of telecommunications infrastructure

Enable every Senegalese to communicate at a very low cost

• Access to information resources to every school, village, public office and private enterprise

• Promote new generation of Senegalese ICT userscapable of fostering the economic development

• Internet local Content content widely accessible to all Senegalese

• Elimination or reductionTaxes

Duties

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 8

ICT Survey and Strategic visionICT Survey and Strategic vision

• Strategic Objectives within activity sectors

• Telecom Sector Development

• Rural Services, Social improvements

• Radio & Broadcasters development for Democracy

• Short-term & Mid-term consumers needs

• Satisfactory conditions for the demand (technologies, human resources, investment, institutional & government measures,…)

• Analysis of Telecom Infrastructure Development

• Priority Projects

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 9

Regulatory: Some fundamental truthsRegulatory: Some fundamental truths

1. Competition is good for the Internet

2. Regulation is usually bad for the Internet

3. Internet development is GOOD for existing telecommunications operators

4. The customer will gain better services, more services and to lower prices !!

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 10

OFFRE SONATEL 1996:TARIFFS VAT Excluded

Leased Line Internet Access 64 Kbit/s Set Up fee = 650 000 FCFA (~ 900 USD) Monthly charge = 1 060 000 FCFA (~1,400 USD)

PSTN Dial UP access Set Up fee = 25 000 FCFA (~ 35 USD) Monthly Charge = 10 000 FCFA

including 4 hours of Internet connexion 1 Hour of connexion = 1 200 FCFA (~ 1.80 USD)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 11

SONATEL Internet Tariff 2000SONATEL Internet Tariff 2000

285 310 325600

996

1550

2550

3200

3600

0500

1000150020002500300035004000

Tarifs

19,2 28,8 33,6 64 128 256 512 1024 2048

Débit

Courbe Révisée Tarif/Débit

900 USD

PS: A recent discount of 30% has been applied en 2002 ($ 600)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 12

The African contextThe African context

• Fixed Wire Network for monopoly (DSL included)• Explosion of the Cellular network for new telcos

competitor• Many evolutions in the Wireless market

New media for incoming competitorsWireless Local Loop for the telcosCorporate solutions for VPNsInterconnexion of ISP POPLocal Loop for the ISP customers

• Voice services still the bigger and main service• Voice/Data Integration for Telcos and Corporate• VSAT solutions for Telcos and ISPs• Slow change in the Corporate customers environment• The actors: Telcos, ISP and Integrators.

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 13

Problem PointsProblem Points

• The PSTN battleground (revenue sharing model)large scale ISDN demand without associated call revenue

PSTN modem access models are stressing ISDN investment and revenue model

Second PSTN line demand in the surburbs stressing copper plant

Wholesale dial access yet to be accepted

• The Leased Line battleground DC copper pairs, ISDN PVCs, Frame Relay PVCs, High speed

DDS services

dark fibre

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 14

Problem PointsProblem Points

• The IP Battlegroundlack of wholesale tariff point

bundled IP vs unbundled IP

settlements (or the lack thereof)

competitive interest in the customer

competitive distraction of limited expertiseTelco’s own ISP absorbs all available clue!

Clue density is a continuing problem

• The Voice BattlegroundVOIP is viable in competition to existing voice pricing

Voice revenue leakage to the ISP sector is emerging

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 15

The ProblemThe Problem

• Data over Voice is Exhausted• Access (Modem) market

Slow, Inefficient, Complicated, UnreliableCall Characteristics:

voice vs modem access callCall Concentrations move out to the surburbsCopper loop quality problems

• Data over Voice• Leased Line market

increasing bandwidthdifferent load patterndifferent circuit characteristics required

• Digital Subscriber Line – DSL technology• Wireless Local Loop (licensed and unlicensed solutions)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 16

Key Players:Policy, economy & regulation

Key Players:Policy, economy & regulation

1. Government & Regulatory Body

2. Traditional Operators (Sonatel)

3. Mobile Operators (Sonatel Alize, Sentel)

4. Data Operators (Sonatel, SITA, etc)

5. ISPs & ASPs (Metissacana, WAIT, Arc Info, CYG, …)

6. New Telcos (Termination, Prepaid Cards, Origination, etc.)

7. Telecentres (Phone Service)

8. Cyber-cafes (Internet Services )

9. Multipurpose community Telecenters

10. Consumers – Local Internet Community11. NGOs & Donors ( ISOC, ACCT, PNUD, USAID, CRDI, ONUDI, World Bank…)

Approach Limit : Weakeness of the Foreign Direct Investmentdes (IED) in Africa (- de 2%)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 17

Government Policy focusGovernment Policy focus

• Improve ICT indicators

• Focus on Employment creation

• Focus on welfare improvement

• Push to set up the Regulatory environmentUniform tariff nationaly applied

Numbering Plan for Internet Access Server

Assist and help in the Domain Name Registration with the Senegal NIC (ESP)

• Liberalize the Internet Market for local playersNo license for Internet ISP

Development of Cyber-cafes & Multiservice Centers

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 18

Growth & InvestmentGrowth & Investment

Senegalese Telecom drive competitivity and growth to companies:

•Technology

•Cost Effective solutions

•Advanced Network Services

•Quality

•Promote Foreign Direct Investments (IED)(investissements étrangers directs)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 19

The Four Layers of the Internet EconomyThe Four Layers of

the Internet Economy

Internet InfrastructureInternet InfrastructureLayer 1

Application InfrastructureApplication InfrastructureLayer 2

Intermediairy/Market MakerIntermediairy/Market MakerLayer 3

Internet CommerceInternet CommerceLayer 4

Source Cisco

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 20

EvolutionEvolution

• Telco Evolution

• Post

• Telegraph

• Telephone…

• Common Carrier roleone service, one policy, one

operator

Regulatory barriers to competitive entry

indirect taxation base

• ISP, Mobile & Integrated services...

• ISP Evolution• From...Private corporate

networks

• To...LANs, WLANs

• To...Packet Switched Networks

• To...Telco Market and services, IP intelligent services

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 21

ISP EvolutionISP Evolution

• Service Internet ProvidersInter-Corporate connectivity

Public Email service network

• Dial Access ProvidersRetail dial access model - email, web services

• Full Service ISPsDial Access, Web Publishing, Email, VPNs …

Carrier services:ISDN primary rate access services

Leased Line services

Private 4 wire services

Radio Spectrum services

IPLs

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 22

WHY did ISPs appear?WHY did ISPs appear?

• Classic Market Opportunity :Deregulated communications environment

No license fees

No high capital requirement

No infrastructure build required - overlay

No incumbent monopoly operator

No market resistance (quite the opposite)

NEW customer NEED !!! New services required and new suppliers (ISP)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 23

Internet Service Provider (ISP) & ASPInternet Service Provider (ISP) & ASP

• Education-research and NGOESP (UCAD), ORSTOM, AUPELF, ENDA,IRD...

• Health : ???

• InstitutionnalPrimature, Conseil Eco et Social, Minist. Intérieur

• CommercialMetissacana, Arc Informatique, ABM, Point NET, Cyber Center,

Telecom Plus (SONATEL), ICNS, WAIT, ATI, etc ….

• ASP - eCommerce Trade Point Senegal, Silicon Valley, GSIE, etc.

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 24

Area of potential Growth for the ISPArea of potential Growth for the ISP• IP Telephony and Data/Voice Integration

Quality of serviceBandwidth

shortage still a problem in developing countries

Regulatory prohibition or authorization ?But, more than 70% of int’l traffic flows between markets where VoIP already

liberalised

Regulatory: liberalising or “turning a blind eye”

Competence – Skills to run a good network for IP Telephony

• Wireless Network (Voice and Data)Easy to installBandwidthUnlicensed technology & licensed technology

Security is a big concern but solutions exist

• Security Solutions for Network and applications

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 25

The Telco PerspectiveThe Telco Perspective

• One view is that the Telco serviced the data market to prevent private-wired corporate voice systems gaining market impetus

• It is likely that the Telco did not foresee a competitive data service industry due to:competing data standards

low value data transactions

• Usually, the data market was serviced using the margins of oversupply of voiceVoice provisioning uses long-term investment models

Voice service architecture relies on over-provisioned network

• Additional infrastructure investment to provide DSL services

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 26

The Telco PerspectiveThe Telco Perspective

• Voice is good business... But just for themInstalled asset baseStatic service modelHistorical monopoly incumbentHigh revenue potential

• Data is good business for ISP but …WITHOUT Voice• Data business should become part of the Telco

business• Voice Protect Mode

Barriers to voice entry decreasingProtect core voice assets from competitionService the data market at voice bypass prevention pricingRestrict resale access

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 27

The ISPs view of the TelcoThe ISPs view of the Telco

• SUPPLIER, COMPETITOR, CUSTOMER OR PARTNER ?

• incompetence or malice?• Critical path supplier

Incoming callsISDN primary rate accessesDigital circuitsIPLsUpstream Wholesale IP

• New market: New competitor or customer ???

• CONSULTANCY business to be developped in:

IP network Design

IP services (Adressing, Numbering Plan, Security, etc)

• competitorlarger

more capitalmore staffcustomer relationshipsbilling capabilitylarger network

Cheaper• But also a CUSTOMER for

Service provisionningIP infrastructure managementLocal Internet Registry

IP services :

Design , market and sales

Network Design

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 28

ISP Market StrategyISP Market Strategy

• Telco partnership ExpertiseFacilities ManagementIP network services managementSLA for the IP infrastructure

• Versus Telco competitorDSL market introductionWireless Network WLLVoice Over IP businessBuilding network infrastructureBuilding Application InfrastructuresDevelop the portal as the main and only access to the

customer

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 29

The ISP view of the TelcoThe ISP view of the Telco

• The BAD TELCO

• ISP Killer !!!

• dissatisfaction

• suspicion

• forced relationship

• gorilla competitor

• Potential Customer with the biggest customer base

• The GOOD TELCO• good, fast, accurate,

cheap

• fast service provisioning

• wide portfolio of data services

• low prices

• high quality

• high service accuracy

• non-competitive retail services

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 30

The Telco view …ConfusedThe Telco view …Confused

• under-capitalized

• poor service quality

• poor business foundation

• limited role

• limited future

• distracting competitor

• Short term perspective

• ISPs are a potential revenue stream

call revenue

services revenue

circuit revenue

wholesale IP revenue

• In a competitive carrier world, this market cannot be ignored

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 31

Customer dilemma :Customer dilemma :

X25

Frame Relay

ATM

InternetAPPLICATIONS(TransactionnelMultimediaWeb Based Applications)

INTERCONNEXION(Remote sites, Broadband , Virtual Private

Network VPN, Security and Mobility)

IntranetExtranet

ISDN LeasedLines

Teleservices

“A customer is not looking for technology but for Solutions”

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 32

A Common NeedA Common Need

• IntranetCentralized Resources in term of servers Explosion of internal WEB servers Internal Process Management: ERP, etc…

• Extranet Give access to the internal resources for partners (WEB serevrs, FTP, Support AV, ...) Integration of Suppliers in the process.

• Internet Serveurs WEB

E-Commerce

E-mail, ….

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 33

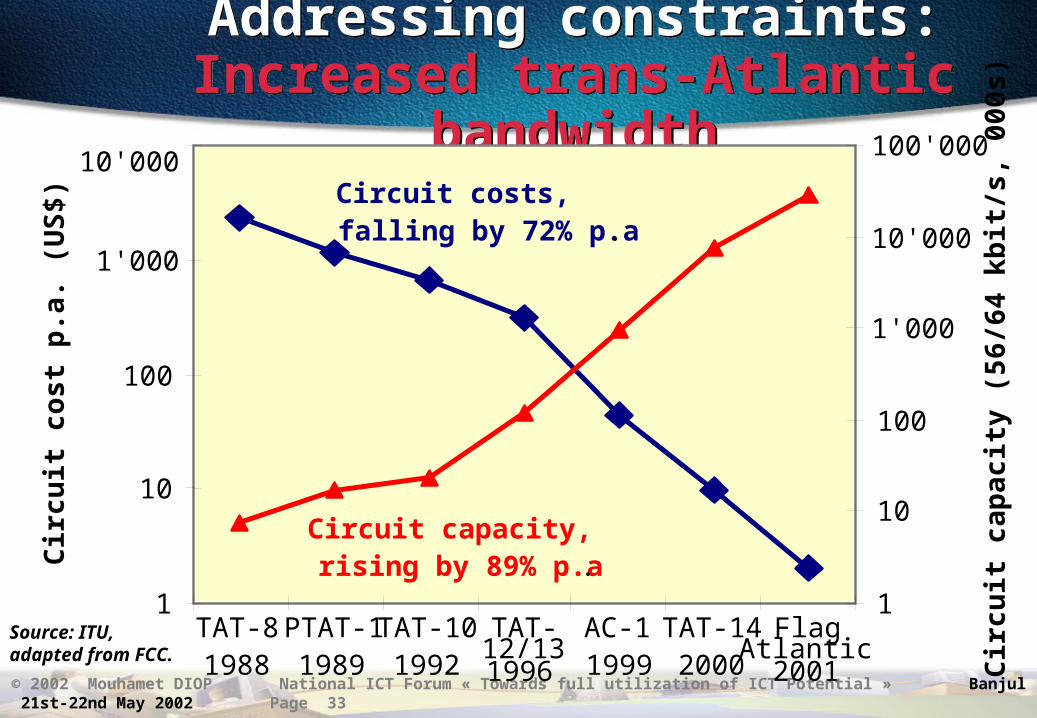

Addressing constraints: Increased trans-Atlantic bandwidth

Addressing constraints: Increased trans-Atlantic bandwidth

1

10

100

1'000

10'000

TAT-81988

PTAT-11989

TAT-101992

TAT-12/131996

AC-11999

TAT-142000

FlagAtlantic2001

Cir

cuit

co

st p

.a.

(US

$)

1

10

100

1'000

10'000

100'000

Cir

cuit

cap

acit

y (5

6/64

kb

it/s

, 00

0s)

Circuit capacity, rising by 89% p.a .

Circuit costs, falling by 72% p.a .

Source: ITU, adapted from FCC.

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 34

6,66,89,07,47,73,57,0

30,0

21,8

0

10

20

30

40

50

60

70

80

90

100

1996 1999 2001

Level 3FrontierQwestGTE (Qwest fiber)IXCWilliamsSprintMCI WorldComAT&T

Network Capacity in U.S. explode over 8,000%In Senegal , it was over 65,600%

Bandwidth IS a KEY ISSUE !!!

Network Capacity in U.S. explode over 8,000%In Senegal , it was over 65,600%

Bandwidth IS a KEY ISSUE !!!

Total Total Bandwidth:Bandwidth:

99.8 terabits/second

21.7 terabits/second

1.2 terabits/second

Fortune Magazine, 3/15/99

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 35

National Infrastructure Networks…

National Infrastructure Networks…

• National Network

• International Network

• Cellular GSM Network

• Rural Telephony Network

• VAN & VAS

• Data Networks

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 36

Telco Infrastructure :The International Network

Telco Infrastructure :The International Network

• Digital Transit Center CTI-M & CTI-T• Earth Station at Gandoul with Standard A

pointant sur le 335,5° EST d ’Intelsat• CLRI with Switches, compression DCME, LRE

witth satellite technologies IDR, DAMA• Over 2100 international circuits • Sub-marine Station at Medina :

Antinea (Juin 1977) between Senegal and MaroccoFraternité (Avril 1978) between Dakar and AbidjanAtlantis-1 (1982) between Bresil-Senegal & Senegal-

Portugal

• Sub-marine Centre : Terminaison Point• Dakar Transmission Center

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 37

Telco’s infrastructureTelco’s infrastructure

• Digitalization of Exchanges 100 % (ISDN/PSTN) with SS7 signalling

• Intelligent Network and New Services (Diamono, Eko, Contact, les Numéros Verts, Vocal Kiosk, Carte NOPALE)

• Digitalization of all transmission trunks FO & MW (4.732 Km)• SDH (Synchronous Digital Hierarchy) introduction

• Optical Fiber over 2.560 Km• IDR for Satellites

• Regional sub-marine cable project

• GSM Ntework (Alizé, SENTEL)

• IP Network

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 38

Telecom Infrastructure :Emerging Projects

Telecom Infrastructure :Emerging Projects

• ATLANTIS-2(2000) Sub-marine cable between America, Africa and Europe EU

• SAT3 (2002) West African Integration Cable

• WLL (Wireless Local Loop) CDMA, etc.

• Satellite Radiocommunications (Globalstar, Iridium, Skybridge, etc.)

• Hub VSAT (Hughes Network) for Voice and Data services

• xDSL(ADSL, HDSL, etc.) : High Digital Subcriber line over copper cable

• Web/TV, VideoConferencing, etc.

• National IP-based Network for Internet, Intranet & Extranet.

• Voice over IP (VOIP)

• Convergence fixe/Mobile/Internet (SENTEL)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 39Mai 98 2

The X25 Network (1988-1997)

Thies

St-Louis

Kaolack

Yoff

Thiaroye

NTI Paris et autres réseaux

X25

DPS6 DPS25

PASS25

PASS25

PASS25

Grand-Dakar

PASS25

Louga

Noeuds X25 redondants

19,2 Kbit/s

PASS25

9,6 Kbit/s

9,6 Kbit/s

19,2 Kbit/s

9,6 Kbit/s9,6 Kbit/s

9,6 Kbit/s

liaisons X75(9,6 Kbit/s)

Centre deGestion

DPS25

DPS25DPS25

48 Kbit/s

MEDINA

19,2 Kbit/s

9,6 Kbit/s

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 40

ISP Network in 1995

FastHub 108T

FastHub 108T

AS5100

Hub 10 Mbit/s

UTPUTP

AS5100SV2

SV3 Tacacs Plus Server(Base de données Clients)

10 Mbit/s

POP 3 ServerSMTP ServerDNS Server

etc ...

AdministrationDNS- SPIN

MCI

Firewall(Check Point)

64 Kbit/s Satellite connexion

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 41

ISP Network in 1997

FastHub 108T

FastHub 108T

AS5100

Catalyst 2924or other

UTPUTP

AS5200

AS5100SV2

SV4

SV3 Cisco SecureUnix Server

(Customer Database)

10 Mbit/s100 Mbit/s

Proxy et backup POP3

POP 3 ServerSMTP ServerDNS Server

etc ...

AdministrationDNS- SPIN

CISCO 7000

Téléglobe128 Kbt/sMCI

64Kbit/s

Firewall(Check Point)

•BGP 4 Running

•10 Leased Lines

•Common Rate for ISPs

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 42

Internet Point of Presence (POP) Extension Thiaroye & Medina - 1998

2 Mbit/s

Serveur Cisco Secure (Account Management Server)

SV2(Serveur Mail, Web, ftp, News, ...)

SV4(Serveur Proxy, News, ...)

Cisco 4700

Access ServerAS5300

Cisco 7000

FirewallEthernet 100

SV3

Access ServerAS5200

MEDINA

THIAROYE

Cisco 2522

Accès RNIS T2 ou PRIDial-Up Access

TéléglobeMCI

•BGP 4 Running

•22 Leased Lines

•Common Rate for ISPs

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 43

The IP Network 98Medina

Thies

St-Louis

Kaolack

4700

7000

7206

7206

7206

Yoff

7204

Hann

2522

Touba7206

Thiaroye

MCI(64 kbit/s)

Téléglobe(2 Mbit/s)

AS5301

AS5200 AS5301

3640

Grand-Dakar

7206

7204Sud-Foire

AS5301

3640

3640

7206

Ziguinchor

Tamba

Kolda

Louga

3640

3640

3640

3640

3640

3640LS1010

7204

LS1010

7206

AS5301

LS1010

LS1010

ATM E3

ATM E1E1 G.703 PPPATM OC-3

Mouhamet DIOP – CEO NEXT

CISCO 7000

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 44

The IP Network 2001

Medina

Thies

St-Louis

Kaolack

4700

7000

7206

7206

7206

Yoff

7204

Hann

2522

Touba7206

Thiaroye

MCI(64 kbit/s)

Téléglobe(2 Mbit/s)

AS5301

AS5200 AS5301

3640

Grand-Dakar

7206

7204Sud-Foire

AS5301

3640

3640

7206

Ziguinchor

Tamba

Kolda

Louga

3640

3640

3640

3640

3640

3640LS1010

7204

LS1010

7206

AS5301

LS1010

LS1010

ATM E3

ATM E1E1 G.703 PPPATM OC-3

Mouhamet DIOP – CEO NEXT

CISCO 7000

FT(34 Mbit/s)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 45

Main steps…Main steps…

• 2 Mbit/s with France Telecom – Quarter 2, 2000

• 8 Mbit/s with Teleglobe – Third Quarter, 2000

• 34 Mbit/s with France Telecom - 2001• Backbone open to other ISPs in term of sharing access

• Regional Initiatives ...Manantali project (Mali, Mauritania, Senegal,…)SAT3/WASC/SAFE sub-marin cableOMVG projectNew Panaftel

• New Tariff evolution 2002 50 % for Education

20% - 30 % reduction on the Internet Leased Line tariffs

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 46

Internet users ...Internet users ...

Part de marché1998

Telecomplus 36%

Autres ISP64%

Part de marché1999

Telecomplus 34%

Autres ISPs66%

70 % of the Internet Traffic is Telecom Plus customers.

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 47

Data Network Revenue - 1998Data Network Revenue - 1998

• X25 Market (SENPAC)Revenue ~ 850 Millions

• Analog & Digital Leased LinesRevenue ~ 1.7 Milliards

• Internet Market (LS + E-mail)

Revenue ~ 615 Millions

• Internet Servers (3000 et 3011)

CA ~ 590 Millions (Télécom Plus)

CA ~ 100 millions (autres serveurs)

• Total Internet ~ 1,3 Milliards

SENPAC26%

LS42%

Internet32%

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 48

Data Network MarketX25 (Senpac) Network revenueData Network MarketX25 (Senpac) Network revenue

0,0 0,0 0,3 0,2 0,5 0,6 0,6 0,7 0,6 0,7 0,8 0,8

19 2024

2730

3538

5754

62

78

91

0

10

20

30

40

50

60

70

80

90

100

Année

Chiffre d'Affaires (en Milliards de F CFA)

© 2002 Mouhamet DIOP National ICT Forum « Towards full utilization of ICT Potential » Banjul 21st-22nd May 2002 Page 49

Questions ?Questions ?