www.worldbank.org/ict/strategy [email protected] strategy consultations 2011 connect...

TRANSCRIPT

www.worldbank.org/ict/[email protected]

Strategy Consultations 2011CONNECT • INNOVATE • TRANSFORM

CommunicationTechnologies

Information &

World Bank Group

ICTObjective

The World Bank Group is developing a new ICT Sector strategy.

We seek views from stakeholders on where and howto focus our financial and advisory services

www.worldbank.org/ict/[email protected]

2

3

20102000

Phone

Smart Grids

Green Technology

Video on Internet

Social Networking

Mobile Banking

3

ICT Going Forward

Climate Change

Ed

ucatio

n &

Health

Governance &

Social Develop.

Urb

an

Finance

Rur

al

Social Protection

Infrastructu

re

Largest Ever Delivery Platform:> 3 Billion Mobile Phones in Developing Countries

4

2001 ICT Sector Strategy

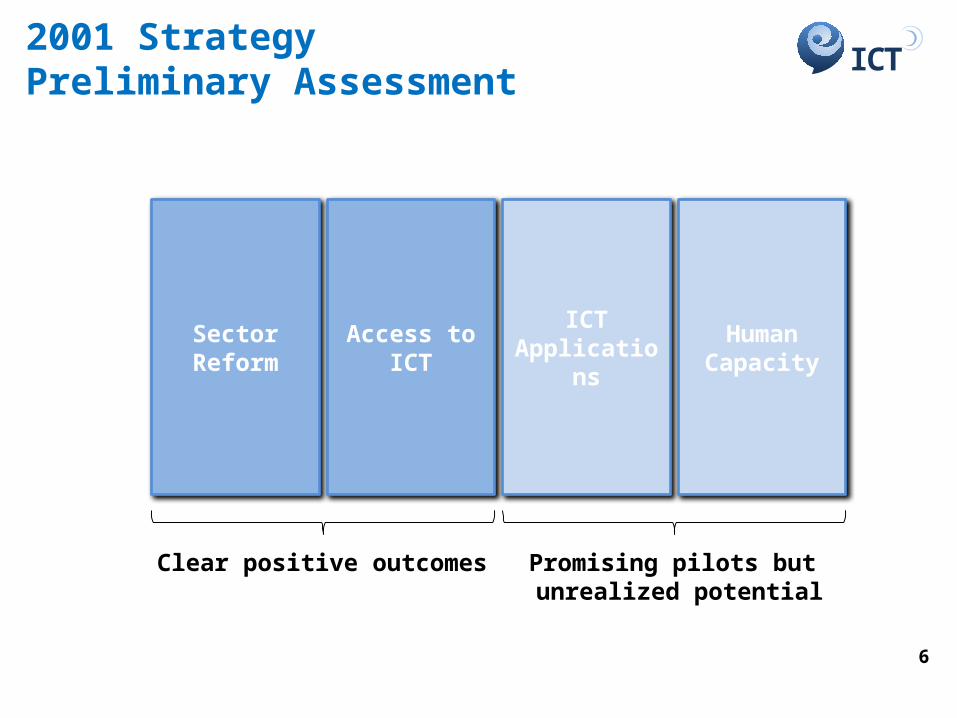

ICT2001 Strategy Preliminary Assessment

6

Sector Reform Access to ICT ICT Applications

Human Capacity

Clear positive outcomes Promising pilots but unrealized potential

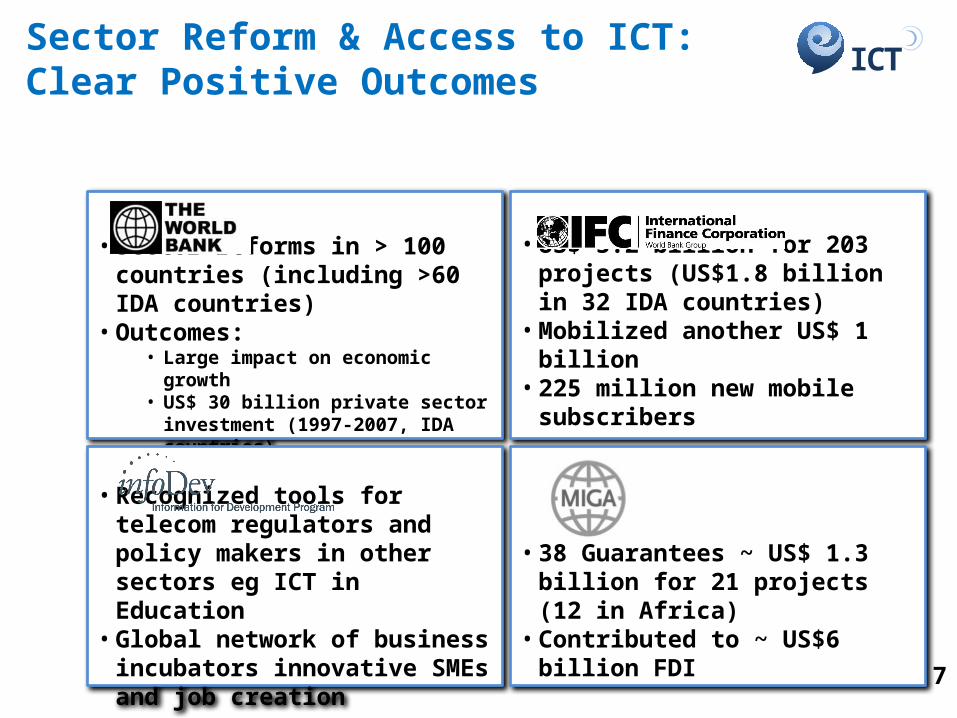

ICTSector Reform & Access to ICT: Clear Positive Outcomes

• Sector reforms in > 100 countries (including >60 IDA countries)

• Outcomes: • Large impact on economic growth• US$ 30 billion private sector investment

(1997-2007, IDA countries)

• US$ 3.2 billion for 203 projects (US$1.8 billion in 32 IDA countries)

• Mobilized another US$ 1 billion• 225 million new mobile subscribers

• Recognized tools for telecom regulators and policy makers in other sectors eg ICT in Education

• Global network of business incubators innovative SMEs and job creation

• 38 Guarantees ~ US$ 1.3 billion for 21 projects (12 in Africa)

• Contributed to ~ US$6 billion FDI7

ICT Applications: Unrealized Potential but Promising Pilots

Examples of Promising Pilots

• IFC:– Mobile banking in South Africa– Mobile health in Rwanda

• Bank:– Ghana: e-Customs PPP– Afghanistan: Use of geo-referenced photos

for verification of project outputs– Sri Lanka: Satellite imagery for fisherman

communities– Tunisia & Ethiopia: Access to Internet for

disabled

Unrealized Potential

QAG Assessment: • Low quality of ICT components• ICT inputs insufficient in most cases• Focus on automation, recent focus on

transformation

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 20060%

10%

20%

30%

40%

50%

60%

70%

0% 1% 2% 8%11%

22%

40%

47%

55%61%

51%

57%

More than half of WB projects include active ICT components (US$ 7.7 billion, FY07)

8

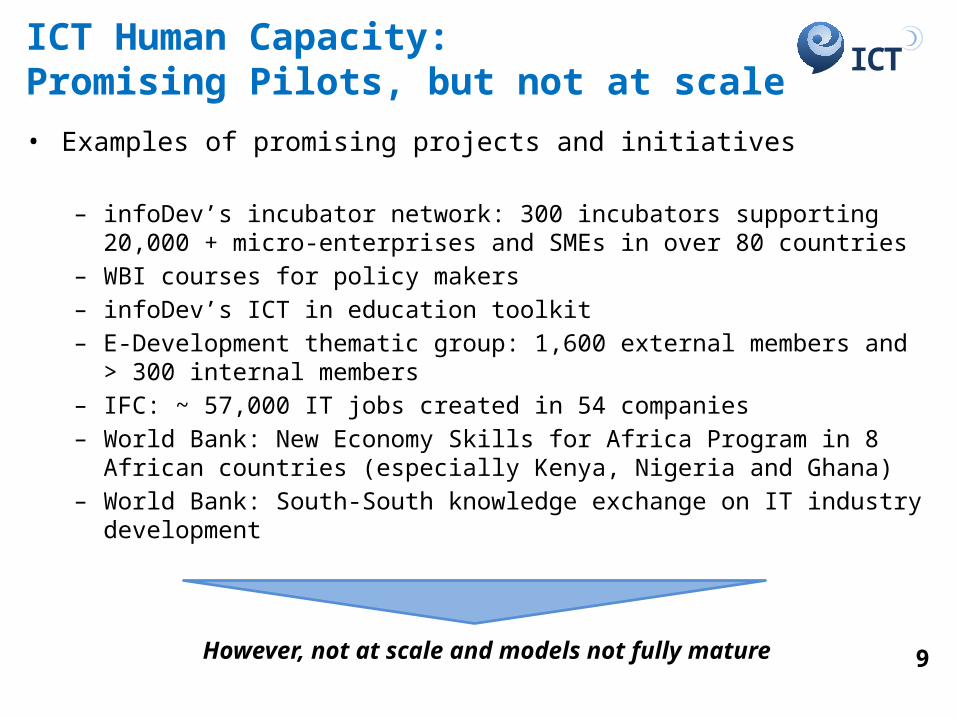

ICTICT Human Capacity: Promising Pilots, but not at scale• Examples of promising projects and initiatives

– infoDev’s incubator network: 300 incubators supporting 20,000 + micro-enterprises and SMEs in over 80 countries

– WBI courses for policy makers– infoDev’s ICT in education toolkit– E-Development thematic group: 1,600 external members and > 300 internal

members– IFC: ~ 57,000 IT jobs created in 54 companies– World Bank: New Economy Skills for Africa Program in 8 African countries (especially

Kenya, Nigeria and Ghana)– World Bank: South-South knowledge exchange on IT industry development

However, not at scale and models not fully mature 9

ICTWBG in ICT Sector: 2000 - 2010

Sect

or R

efor

m /

Ac

cess

to IC

TIC

T Ap

plic

ation

sH

uman

Cap

acity

an

d In

nova

tion

• Sector reform: Bank active in 105 countries in last 10 years, infoDev’s regulatory toolkit and Open Access research• PPPs for backbone infrastructure: IFC-led EASSy Project (22 countries, 30 operators, 4 other DFIs) in Africa – Bank-led Regional

Communications Infrastructure Program (RCIP)• Wireless: IFC financing have so far contributed to 225 million mobile subs • Infrastructure: IFC financing for Shared towers (Turkey and Brazil); Bank support for rural infrastructure (India, Sri Lanka);• New broadband solutions: WiMax (Ukraine, Uruguay), Cameroon / Central Africa (Pipeline), West Africa (Electricity Transmission),

Broadband wireless (Afghanistan)

• Banking the unbanked: IFC support to m-banking - WIZZIT (South Africa), Digicel in Caribbean, Millicom; infoDev’s m-banking knowledge map and research

• e-Government: Bank support in Vietnam, Ghana, Mongolia, Kenya; IFC support to Sonda (Chile), IBS (Russia), Meteksan (Turkey), Chinasoft; infoDev’s egovernment toolkit

• e-Health: Investing in cellular-based health systems, Voxiva (Africa – LAC), health data management• Education: IFC support to Socket Works (Nigeria), new Bank-led ICT Skills development Initiative, infoDev’s ICT in education

toolkit in partnership with UNESCO• Partnerships and Knowledge: M-Banking Conference (GSM Assoc., DfID, CGAP), Industry Partnerships, Government

Transformation Initiative

• Supporting the growth of IT/IT enabled service industry: Bank’s support in Ghana, Mexico, Kenya, Sri Lanka; infoDev’s research on ITES industry and IT parks

• Cellular Distribution Facility: IFC- financed working capital facility program offering local banks creditline to cellular distributors to buy bulk airtime aimed for retail market

• Supporting the development of an ICT-Enabled innovation network: Leveraging infoDev’s business incubator initiative, which provides financing and TA to over 300 incubators for 20,000 MSME businesses in over 80 countries

• Supporting the development of holistic ICT policy frameworks: Increasingly developing countries are recognizing the linkage between innovation and economic development and GICT is working with several countries

• Creating systems of innovations: DFID Low Carbon Innovation Centers, clean energy innovation centers

10

The ICT Sector in 2010

ICTTrends in ICT Sector

• Growing role of high-speed internet in developing countries

• Information and content available at high-speeds on phones

• Mobile phones as the single largest service delivery platform in the world

• IT-enabled services industry an engine of growth and employment generation

• Convergence causing disruptions in government policies and business models

12

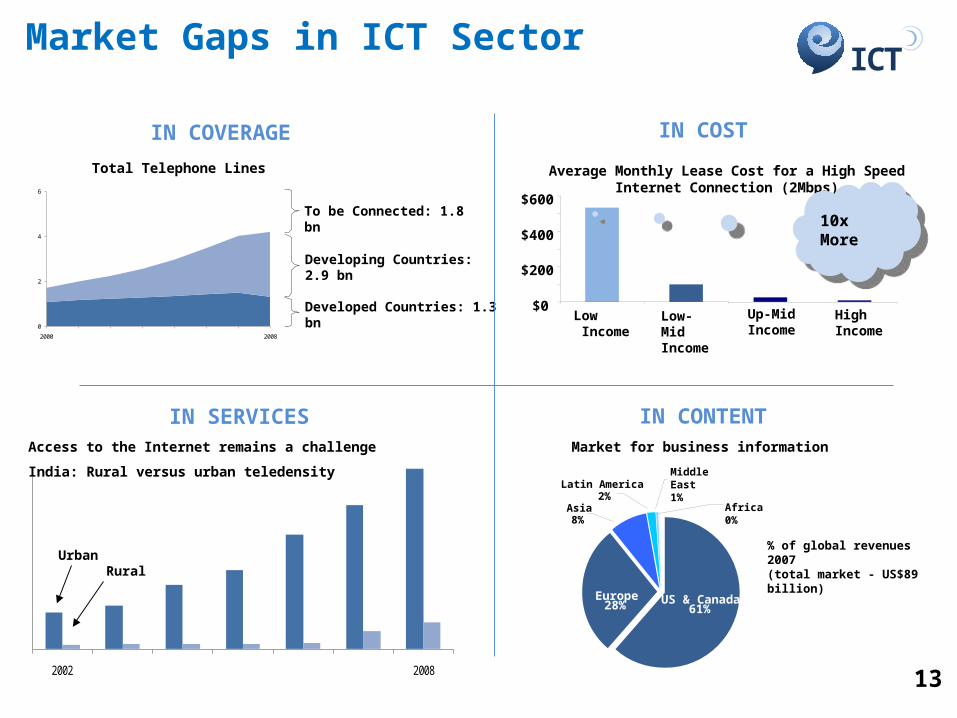

ICTMarket Gaps in ICT Sector

IN COVERAGE

2002 2008

India: Rural versus urban teledensity

RuralUrban

Access to the Internet remains a challenge

IN SERVICES

IN COST

% of global revenues 2007(total market - US$89 billion)

US & Canada61%

Middle East1%

Latin America2%

Asia8%

Europe28%

Africa0%

Market for business information

IN CONTENT

$0

$200

$400

$600

Low Income

Low-MidIncome

Up-MidIncome

HighIncome

Average Monthly Lease Cost for a High Speed Internet Connection (2Mbps)

10x More

10x More

0

2

4

6

2000 2008

Total Telephone Lines

To be Connected: 1.8 bn

Developing Countries: 2.9 bn

Developed Countries: 1.3 bn

13

ICTLessons Learned

• The role of private sector continues to be paramount

• The level of connectivity in client countries varies and requires a differentiated approach to ICT sector development in client countries

• Skills are a binding constraint in developing local IT-enabled service industries and supporting ICT applications

• ICT applications present high-risk, high-reward opportunities, and require selectivity and greater checks and balances

• IT coordination across sectors of government can help lower costs and create operational efficiencies

• Deliberate policies are needed to promote social inclusion and gender equality

• IT-enabled service industries are capable of creating opportunities for youth and women

14

Proposed ICT Sector Strategy

ICT

Transform Innovate

Connect

Emerging Directions for the New StrategySe

ctor

Ref

orm

Acce

ss to

ICT

Hum

an C

apac

ity

ICT

Appl

icati

ons

2001 Strategy Emerging Directions

CONNECT – Maintain a focus on the connectivity agenda with an emphasis on high-speed Internet

INNOVATE - Increase support for the use of ICT to unleash innovation across the economy and for the growth of local ICT industries

TRANSFORM – Scale up support to client countries to use ICT to transform all areas of the economy 16

Connect: Maintain Focus with an Emphasis on High-Speed Internet

ICT and Growth• 10% point increase in high-speed Internet

connections accounts for 15-25% of a country’s growth

Significant gaps remain in High-Speed Internet• Only 250 million subscribers in developing

countries• Private sector investments lagging behind

policy objectives

Areas of WBG Interventions• Continue reform agenda for more private

sector investment• Need for public-private partnerships• Public sector financing interventions ramping

up across country segments. Examples: Finland, Australia, Germany, USA, Russia, Brazil, Uganda, Ghana, Rwanda, etc.

Policy and Regulation

(WB, infoDev)

Private sector investments (IFC)

Guarantees (MIGA)

Catalytic public sector investments (WB)

17

Policy and Regulation Infrastructure R&D and Skills

Ecosystem for Innovationand ICT Industry Development

Start-up Growth Established

Venture Capital Public Equity Markets

Credit (Debt) Markets

Stages of Enterprise Development

Finance

Policy, Infrastructure and Skills

• 300 incubators of ICT-enabled enterprises in over 80 developing countries supported by

infoDev • 20,000+ enterprises creating over 220,000 jobs

INNOVATION AT THE GRASS ROOTS

Innovation at the Micro-Enterprise and SME level

Innovate: Promote innovation across the economy and grow local ICT industries

18

SME Development & Job Creation

Young firms contribute to over 60% of job creationOver 80% of incubated SMEs stay in local communities50 jobs created by an incubator client generate 25 in community

Transform: Increase Support to Leverage ICT Across All Sectors

Cross-Sector Agenda Strategic Template

Sector / Theme

Outcomes

Climate Change

Infra-structure

Human Develop-

ment

Gover-nance

Mobile and Other

e-Services Government Private Sector & NGOs

Back-end Applications (MIS, FMS, Procurement, etc.)

Enabling Environment:• Regulatory framework (sector-specific)

• Policies and standards• Shared infrastructure

• Interoperability framework• Cyber security

Foundations

Environment &Climate Change

Ed

ucatio

n &

Health

Governance &

Social Develop.

Urb

an

Finance

Rur

al

Social Protection

Infrastru

cture

Largest Ever Delivery Platform:> 3 Billion Mobile Phones In Developing Countries

Need for Sector/Theme Specific Strategies (Annexes) – for Sector-Led Implementation

19

20

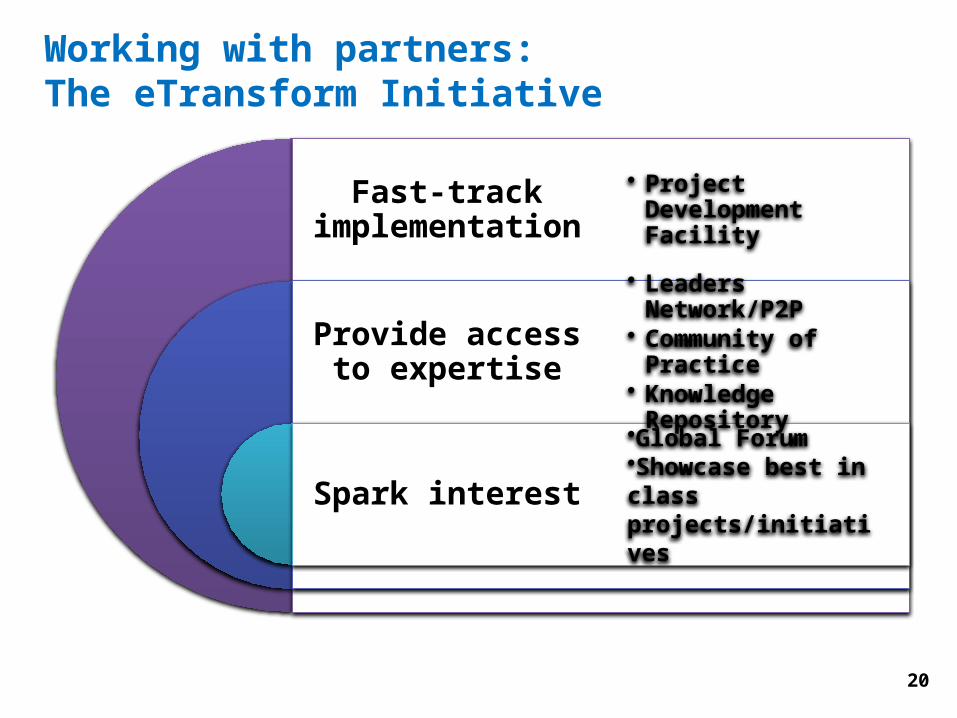

Working with partners: The eTransform Initiative

COMPONENTS

Fast-track implementation

Provide access to expertise

Spark interest

• Project Development Facility

• Leaders Network/P2P• Community of Practice• Knowledge Repository

•Global Forum•Showcase best in class projects/initiatives

Consultations

ICTConsultations & Strategy Preparation

Internal and External Consultations for

Strategy Preparation

November 2010 – February 2011

Analytical Work• Broadband policy• ICT and Climate Change• Mobile applications for development• ICT for Innovation, ICT in Agric• AFR ICT-enabled Transformation,

AFR ICT in Health

Global Consultationson Full Draft

Strategy

July2011

Internal Management

Reviews

PreliminaryBoard review

June 2011

Board Discussion

September 2011

Strategy drafting

November 2010 – May 2011

www.worldbank.org/ict/strategy22

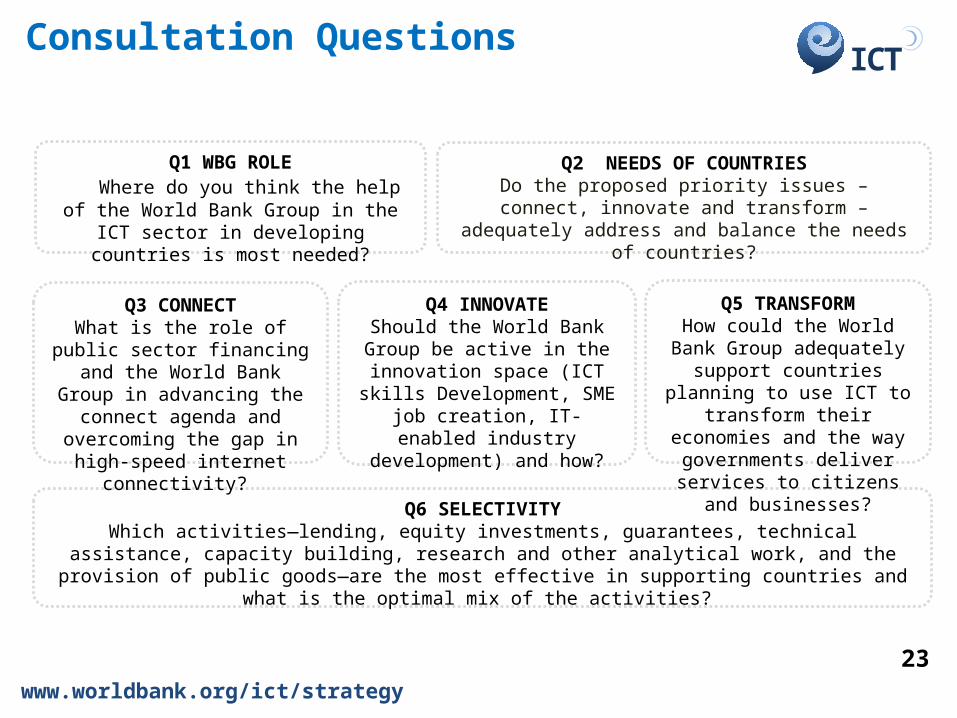

ICTConsultation Questions

Q6 SELECTIVITYWhich activities—lending, equity investments, guarantees, technical assistance, capacity building, research and

other analytical work, and the provision of public goods—are the most effective in supporting countries and what is the optimal mix of the activities?

Q1 WBG ROLEin Where do you think the help of the World Bank Group in the ICT sector in developing

countries is most needed?

Q2 NEEDS OF COUNTRIESDo the proposed priority issues – connect, innovate and

transform – adequately address and balance the needs of countries?

Q3 CONNECTWhat is the role of public sector

financing and the World Bank Group in advancing the connect

agenda and overcoming the gap in high-speed internet connectivity?

Q4 INNOVATEShould the World Bank Group be

active in the innovation space (ICT skills Development, SME job creation, IT-enabled industry

development) and how?

Q5 TRANSFORMHow could the World Bank Group

adequately support countries planning to use ICT to transform

their economies and the way governments deliver services to

citizens and businesses?

www.worldbank.org/ict/strategy

23