world insurance report 2015

TRANSCRIPT

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 1/60

WORLD

INSURANCEREPORT

2015

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 2/60

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 3/60

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 4/60

4

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 5/60

5

2015 WORLD INSURANCE REPORT PREFACE

Capgemini and Efma are pleased to present the 2015 World Insurance Report (WIR). This

year’s edition, presented in three chapters, provides a comprehensive overview of the current

status of the insurance industry, including detailed assessments of financial performance and

customer experience, as well as an overview of looming challenges. An appendix offers a high-

level overview of the performance of the non-life insurance industry in 15 countries around the

world.

In the first chapter, we analyzed publicly available financial information to see how insurers are

faring against a range of industry-standard efficiency ratios. We found that a healthy reductionin claims-related expenses helped boost profits throughout most regions globally, despite the

resistance of important levers, such as operational and acquisition ratios, to improvement.

Extensive consumer research, based on surveys of more than 15,500 respondents across 30

countries in five regions throughout the world, form the second chapter of our report. In this

section, we documented a disquieting drop in the volume of positive experiences customers are

having as they interact with their insurance providers. This trend is especially troubling given

the strong link we quantified between positive customer experience and advocacy, an important

source of loyalty and profitability.

In the third chapter of our report, we outlined the many changes that threaten to negatively

impact stability in the insurance industry. Some of these forces of change come from unexpected

quarters, while others have been in the works for some time. Alongside this picture of a

changing landscape, we highlighted the tools and strategies available to insurers as they seek to

maintain their competitiveness.

We hope you will find our 2015 WIR useful in helping you understand the challenges and

opportunities facing global insurers. Armed with details related to peer-level performance and

customer attitudes and perceptions, we expect insurers will be better prepared to develop and

implement ongoing strategies for continued profitability.

Preface

Jean LassignardieGlobal Head of Sales and Marketing

Global Financial Services

Capgemini

Introducing the Eighth Annual World Insurance Report

Patrick DesmarèsSecretary General

Efma

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 6/60

6

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 7/60

2015 WORLD INSURANCE REPORT CHAPTER 1

7

C H A P T E

R 1

Non-Life Insurers in Most

Markets DemonstrateImproved UnderwritingPerformance

C H A

P T E R 1

INSURERS RECORDED HIGHER PROFITS AIDEDBY DROP IN CLAIMS EXPENSES

Non-life insurers in most countries recorded healthyprofits, aided by a significant drop in claims payoutexpenses. Global insured losses in 2013 droppedby nearly half to US$45 billion, from US$81 billionin 2012. At the same time, global firms exhibitedproficiency in managing the basic risks of the non-lifebusiness, showing more improvement than not in the

claims ratio, which measures their ability to balancethe volumes and prices of premiums against payouts.Other business basics, such as managing operationaland customer acquisition costs, proved more resistantto improvement, as operational and acquisition ratiosremained largely unchanged or deteriorated slightlyin 2013. Despite those difficulties, profitability in thesector was substantial, with insurers in more than halfthe countries posting double-digit margins.

The global volume of non-life gross writtenpremiums (GWP) increased by 3.3% in 2013, to

reach US$2.03 trillion.1

While the 3.3% increase

was a sizable jump over the very slight increaseposted between 2011 and 2012, it fell short of thecompound annual growth of 4.0% experiencedbetween 2010 and 2012 (see Figure 1.1).

1 “Natural catastrophes and man-made disasters in 2013”, Swiss Re sigma 1/2014, March 2014

Figure 1.1 Global Non-Life Gross Written Premium Volumes (US$ Billion), 2010-2013

1,819.31,968.2 1,968.7 2,032.9

0

600

1,200

1,800

2,400

2010 2011 2012 2013

G r o s s W r i t t e n P r e m i u m

( U S $ b i l l i o n )

CAGR 2010-2012

4.0 %

Growth 2012–2013

3.3%

Source: Capgemini Financial Services Analysis, 2014; Swiss Re sigma Reports

2010-2014

KEY FINDINGS

Non-life insurers in most regions witnessed improved underwriting ratios due to asignificant drop in claims expenses. Australia, Germany, Japan, and Italy recorded thehighest improvements, while Netherlands and Switzerland deteriorated the most. The lowerclaims payouts contrasted with operating and acquisition costs, which were more resistant topositive change. Overall, the improvement in underwriting ratios led to robust profit marginsfor non-life insurers in most markets.

Global non-life premium volume grew by 3.3% aided by strong growth in emergingmarkets and marginal improvement in some of the mature markets. Of the marketsanalyzed, Brazil in Latin America and India in Asia-Pacific witnessed the highest growthin their non-life premiums. Among the developed markets, Sweden and Switzerland postedthe highest growth rates while other countries, such as Australia, Japan, Spain and Italy,experienced declines in their premium growth. Given advancements in technology andwidespread adoption of different risk mitigation measures, especially in developed markets, it

is expected that premium volumes will drop even further in the near future.

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 8/60

8

While emerging markets witnessed robust growthrates, developed markets found it tough to increasetheir premium volumes. Brazil in Latin Americaand India in Asia-Pacific posted the highest increases

in gross written premium volumes, at compoundedannual growth rates of 8.4% and 8.8% respectively.The more mature markets, beset by stiff competition,experienced more modest growth. The United Statesand Germany, for example, expanded only in the

3 percentage point range. Several other advancedmarkets such as Australia, Japan, Spain,and Italy experienced declines in premium growth(see Figure 1.2). This trend is likely to continue further

as adoption of advanced risk mitigation technologiessuch as telematics and automated home systems,mostly in developed markets increases, resultingin lower incidents and likely lead to a reduction inpremiums charged.

Figure 1.2 Non-Life Insurance GWP Volumes by Country (US$ Million), 2010–2013

Gross Written Premium (US$ million) Gross WrittenPremium

(US$ million)

CAGR2010-2013

(2.0%)

(2.5%)

4.8%

5.9%

3.2%

3.5%

2.3%

0.6%

(0.2%)

(1.1%)

5.8%

1.6%

8.4%

8.8%

6.4%

Australia

Japan

Canada

Belgium

Germany

U.S.

U.K.

Netherlands

Spain

Italy

Switzerland

France

Brazil

India

Sweden

32.732.348.434.7

108.8127.7130.7117.2

73.072.269.063.4

16.615.315.114.0

132.8125.8131.3120.8

726.4703.8667.1

655.5

106.8107.4109.5

99.7

75.171.579.773.7

38.638.440.738.9

50.650.955.452.3

28.427.628.523.9

94.689.798.490.1

39.537.437.231.0

13.413.112.210.4

10.69.8

10.2

8.8

2013

2012

2011

2010

200 400 600 8000

Source: Capgemini Financial Services Analysis, 2014; Swiss Re sigma Reports 2010-2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 9/60

9

2015 WORLD INSURANCE REPORT CHAPTER 1

Underwriting ratios mostly improved, with reducedclaims costs acting as the most significant lever. In nearly two-thirds of the countries, underwritingratios improved or stayed the same (see Figure 1.3).

The largest improvements in underwriting ratios

occurred in Australia, Germany, Japan, and Italy. Onlyin Germany did a significant decrease in operationalexpense play a role in enhancing the underwritingratio. In all other countries, operating and acquisition

ratios stayed about the same or deteriorated slightly.

Figure 1.3 Non-Life Insurance Underwriting Ratios (Combined Expenses as a Percentage of GWP) %, 2010–2013

(16.9)

(6.6)

(1.5)

(1.1)

(7.6)

(2.2)

1.4

6.7

3.3

(5.6)

7.2

(0.3)

0.0

NA

1.0

70.5

97.6

82.8

65.2

11.1

10.6

9.0

8.6

13.1

13.0

12.6

13.7

201061.0

71.4

64.8

58.8

18.5

17.6

16.6

16.0

16.7

16.4

16.3

16.3

77.4

72.2

65.5

64.9

10.9

11.1

11.9

11.5

17.3

16.3

16.1

15.6

66.0

60.3

56.6

55.0

9.7

14.3

14.2

14.3

15.1

20.4

20.4

20.8

70.6

71.7

68.5

66.0

13.2

15.4

15.8

10.6

12.2

11.2

10.3

10.4

69.1

74.2

69.6

66.6

18.9

19.0

20.9

22.1

17.9

17.3

16.3

15.9

67.2

63.1

63.8

63.1

12.9

13.2

11.1

11.7

19.7

18.9

20.3

21.8

68.0

70.1

68.6

76.0

8.2

8.5

8.6

8.6

15.4

14.9

14.5

13.9

74.7

72.8

72.8

66.3

8.4

8.2

8.5

9.1

16.1

15.9

15.6

15.9

69.0

68.4

66.9

69.8

9.4

9.7

8.3

9.6

16.3

16.3

12.8

15.8

77.0

67.5

76.0

75.7

7.2

7.7

6.7

6.7

15.9

16.4

15.4

15.4

64.5

58.9

60.6

59.3

13.1

14.4

16.9

17.6

16.6

14.2

20.4

21.3

95.3

89.7

67.7

31.8

26.2

21.2

5.7

6.3

3.9

NA

78.8

75.5

73.9

75.0

16.6

13.7

13.4

13.4

4.7

9.6

10.2

10.1

0 20 40 60 80 100 120 140

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

2010201120122013

Underwriting Ratio (%)

Claims ratio Operational Ratio Acquisition ratio

Australia

Japan

Canada

Belgium

Germany

U.S.

U.K.

Netherlands

Spain

Italy

Switzerland

France

Brazil

India

Sweden

% Point Change

2012–13

9.6

1.4

(12.1)

0.4

(1.3)

0.9

(4.6)

0.1

(2.1)

(2.2)

(6.8)

(2.0)

(3.6)

(40.1)

(2.5)

2010–12

70.9

68.4

68.0

70.9

3.7

3.6

3.5

3.7

17.4

17.7

18.4

18.6

Note: The ratios are valid only for non-life insurance; The ratios reflect non-life data as reported by the countries themselves, and hence include health insurance for Italy,

Spain, Switzerland, and Netherlands; At the time of analysis, 2013 data was not available for India; The previous year ratios may have changed based on the refresh of

results for some of the companies; PP refers to Percentage Point Change.

Source: Capgemini Financial Services Analysis, 2014; Company Annual Reports, 2010-2013

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 10/60

10

Coming after a $12.5 billion underwriting loss in2012, the global underwriting profit of $8.52 billion in2013 was a welcome turnaround. The profits were thethird best of the past decade, following $28.9 billion

in 2006 and $23.0 billion in 2007. Fewer naturaldisasters combined with premium rate revision led toimproved claims ratios, which in turn helped propelthe underwriting profits.

Most countries were successful in lowering theirclaims ratio significantly (see Figure 1.4). Australiaexperienced the largest decrease in the claims ratio bya wide margin, thanks to premium rate increases andportfolio remediation measures, as well as decreasedloss and loss adjustment expenses. In Japan, areduction in direct claim payments for fire insurance

helped pull down the claims ratio, while the Italiannon-life insurance market benefited from the decreasein claim frequency and from the major attention onfraudulent claims mitigation (subsidized by newregulations).

In Spain and Netherlands, where claims ratiosexperienced significant degradation, competitionhampered the ability of non-life insurers to employpremium pricing as a tool to improve claims ratios.In both markets, insurers lowered premium prices asa means of gaining share in tough markets. Spanish

motor insurers, for example, reduced premiums by10% to 20%. Such price reductions had the effect ofincreasing claims expenses.

Despite ongoing efforts to drive productivity andimprove the bottom line through automation,little change occurred in the operational ratios ofnon-life insurers in most countries. Companies are

striving to make wise investments in technology andautomation, yet most are still struggling to achievethe types of operational benefits that would give thema clear competitive advantage. Only in Germany,where non-life insurers have successfully deployednumerous cost-reduction measures, did operationalratios improve in a significant manner. In the UnitedStates, where the expenses of supporting the world’slargest insurance market are already high, regulatoryrequirements, anti-fraud measures, and legacyreplacement costs drove operational expenses up evenfurther. The industry as a whole needs to continue

to make technology investments aimed at tamingthe inefficiencies and complexities of basic insuranceunderwriting.

Acquisition ratios remained mostly f lat, even asinsurers embraced the use of alternate channelsto distribute products. The burden of supportingmultiple distribution methods may explain thedifficulty insurers have encountered in bringingdown acquisition ratios. Even though digital channelsoffer enormous upside to enhancing the customerexperience and improving profitability by helpinginsurers lower their commission costs, entrencheddelivery channels are likely to continue to play a rolein product distribution for some time. As insurerscontinue to make gains in moving customers toalternate channels, they will begin to reap the benefitsof more streamlined distribution.

Figure 1.4 Non-Life Insurance Performance in Key Ratios, (percentage point change), 2012–2013

Countries / % Point

Change in Ratios,

(2012-13) A u s t r a l i a

J a p a n

C a n a d a

B e l g i u m

G e r m a n y

U . S .

U . K .

N e t h e r l a n d s

S p a i n

I t a l y

S w i t z e r l a n d

F r a n c e

B r a z i l

Claims Ratio

High Deteriorat ion Medium Deter iorat ion Low Change No change Medium Improvement High Improvement

Operational Ratio

Acquisition Ratio

Underwriting Ratio

-6.5 2.9 -0.3 -1.3-17.6 -6.0 -0.6 -1.6 -2.5 -3.0 -0.7 7.4 2.9

0.6 1.3 0.0 0.7-0.4 -0.6 -0.4 0.1 -5.2 1.2 0.6 0.0 0.2

0.3 3.0 0.0 0.61.1 0.0 -0.5 0.4 0.1 -0.4 1.5 -0.6 0.2

-5.6 7.2 -0.3 0.0

S w e d e n

1.1

0.0

-0.1

1.0-16.9 -6.6 -1.5 -1.1 -7.6 -2.2 1.4 6.7 3.3

Note: PP refers to percentage point change; 2013 data for India is unavailable since the consolidated data for Indian insurance firms has not been published yet

▲ refers to changeSource: Capgemini Financial Services Analysis, 2014; Industry Reports from Insurance Associations and Regulators

2 AM Best Reports

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 11/60

11

2015 WORLD INSURANCE REPORT CHAPTER 1

Profit margins for non-life insurers around theworld mostly rose on the strength of improvedunderwriting ratios. Fewer natural disasters,combined with premium rate revisions, led to better

claims ratios. These improved ratios in turn boostedunderwriting ratios, a measure reflecting the overallefficiency of insurance companies. Operationaland acquisition ratios remained mostly unchanged,causing little impact on underwriting ratios or overallprofitability.

U.S. and Australian non-life insurers witnessed thehighest growth in profit margins. The Australianmarket benefited from a massive improvement in theclaims ratio, while the United States experienced amajor decline in natural disasters following a series of

them the previous year. Canada suffered the highestlosses. Despite growth of 3.2% in premium volumes,a large number of natural disasters took its toll onprofitability. The only other country to experiencelosses was Germany, where severe hailstorms struckheavily populated areas.

CONCLUSION

Though non-life insurers experienced the benefits ofa relatively quiet year in 2013, some of our findingsportend growing difficulties in expanding the business

going forward. For one, the volume of premiumsis growing more slowly in developed markets thanemerging ones. Insurers also face a challenge indeveloping an accurate pricing model to assess theimpact of newer risks such as cyber security andincreasing terror threats, which could have a negativeimpact on claims ratio. In addition, insurers continueto leave profits on the table by largely failing to bringdown operational and acquisition costs. With risingglobal temperatures expected to increase the frequencyand intensity of natural calamities, the non-lifeinsurance business is only going to get tougher. Global

non-life insurers will need to tighten up all aspects oftheir businesses to be prepared for this shift.

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 12/60

12

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 13/60

2015 WORLD INSURANCE REPORT CHAPTER 2

13

Alarming Drop in

Customer ExperienceUnderscores RisingCustomer Expectations

C H A

P T E R 2

KEY FINDINGS

Globally, positive customer experiences decreased significantly in 2014, indicating thatsteps taken by insurers are not matching rising customer expectations. North Americawitnessed the largest drop of 8.3 percentage points, followed by Latin America with 5.3percentage points. A steep drop in positive customer experience by the Gen Y segmentcontributed to the large decline in North America. The huge drop in positive experience levelsof U.S. customers enabled Austria to overtake it and emerge as the country with the highestpercentage of customers citing positive experiences.

The agent channel delivered positive experience levels that were almost double thoseof digital channels, suggesting that digital channels are dragging down global customerexperience levels. Customer expectations of digital channels such as mobile and socialmedia are rising rapidly along with their usage and importance. However, more than 40%of customers cited positive experiences through the agency channel, while less than 30% ofcustomers had positive experiences through digital channels such as mobile and social media.

Claims servicing is still an area of concern for most insurers when it comes to enhancingcustomer experience. This process had the lowest percentage of customers with positiveexperiences. In most regions, customers who made a claim in the past year reported positiveexperience levels that were significantly lower than customers who did not make a claim. Forexample, North American customers who made a property claim in the past year reported apositive experience level of 24%, compared to 47% for customers who did not make a claim.

The drop in positive experience levels was much steeper for the Gen Y segmentcompared to other age groups across all regions, especially in the developed markets. In North America, the drop in experience levels for Gen Y customers was approximately10 percentage points steeper than other age segments, while in developed Asia-Pacific the

difference was around five percentage points.

Positive experiences led to better customer advocacy, however advocacy levels variedacross regions. Developing Asia-Pacific (Developing APAC), Latin America, and North

America displayed higher advocacy levels, while those in developed Asia-Pacific (Developed APAC) and Europe were quite low. Only delighted customers (those with very positiveexperiences) displayed positive advocacy.

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 14/60

14

DROP IN POSITIVE CUSTOMER EXPERIENCEWAS PERVASIVE ACROSS THE WORLD

Despite ongoing efforts to improve service, positivecustomer experience levels decreased significantly

across the world in 2014 (see Figure 2.1). The globallevel, already low in 2013 at 32.6%, decreased byanother 3.7 percentage points to 28.9%. Of the 30countries surveyed, 80% recorded a decline in thepercentage of customers with positive experiences.Furthermore, about one-third of these customerswitnessed a decrease of more than 5 percentagepoints.This was the first time we observed such a drasticdrop since we began tracking customer experiencethree years ago.

North America, which in 2013 had the highest levelof positive customer experience at 47.9%, experiencedthe largest decrease (8.3 percentage points), followedby Latin America with a 5.3 percentage point drop.The United States had been the only country in 2013to record positive customer experiences in excess of50.0%. But a large decline of 10.5 percentage pointsresulted in only 40.8% of U.S. customers citing a

positive experience in 2014. As a result of this drop,the United States dropped down to the secondplace behind Austria (see Figure 2.2). This decreasemay have to do with a decline in satisfaction with

digital channels. Positive experience levels for digitalchannels such as mobile and social media was around30%, compared to 50%+ rates for the traditional agentchannel for both life and non-life.

Positive customer experience levels in Europedecreased by 3.4 percentage points to 30.0%,reflecting large declines in countries throughout theregion. Netherlands, France, Germany, Poland, andSpain witnessed the largest declines in Europe, eachrecording decreases in positive customer experience ofmore than 5 percentage points. Portugal was the only

country that had a significant increase (4.8 percentagepoints) in the number of customers with positiveexperiences. However, this increase reflected alreadylow levels of positive customer experience in thecountry and existing room for improvement.

Figure 2.1 Customers with Positive Experience, by Region (%), 2013–2014

22.0%

23.6%

28.7%

30.0%

39.7%

28.9%

24.3%

25.8%

34.0%

33.4%

47.9%

32.6%

Developing APAC

Developed APAC

Latin America

Europe

North America

Global

2013 2014

% Point Change

2013-14

(8.3%)

(3.4%)

(5.3%)

(2.2%)

(2.3%)

(3.7%)

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 15/60

15

2015 WORLD INSURANCE REPORT CHAPTER 2

In developed and emerging Asia-Pacific, wherepositive customer experience remained the lowest inthe world, the levels decreased further, by 2.2 and2.3 percentage points, respectively. Seven of the tencountries with the least amount of customers havinga positive experience were located in Asia-Pacific in2014. The inability of insurers to meet the constantlyevolving expectations of the tech-savvy populationsthey serve appeared to play a role, particularly in thedeveloped Asia-Pacific markets of Hong Kong, Japan,and Singapore.

POSITIVE EXPERIENCE DROPPED ACROSS ALL CHANNELS, THOUGH AGENT CHANNELSTANDS TALL

The agent channel continued to be most important tocustomers of all ages across all regions. In addition,

it provided the highest levels of positive customerexperience across all markets for both life and non-life insurers (see Figure 2.3). The agent channel was

the most successful in North America with morethan 50% of customers claiming a positive customerexperience. In all other regions, positive experiencelevels through the agent channel were well ahead ofthe remaining channels.

Digital channels, particularly mobile and socialmedia, were found to drag down experience levelsacross the globe, with less than 30% of customersciting positive experiences from these channels inmost markets. Most customers are now accustomed toreceiving exemplary services via the digital channelsfor sectors such as retail, travel, and to a certainextent, banking. Hence their expectations from thesedigital channels are quite high even while receivinginsurance services. As such, the experience levelsfrom digital channels are lower when compared to the

agent channel. The ongoing importance of agents inthe channel mix and their ability to deliver consistent

Figure 2.2 Top 10 and Bottom 10 Countries with Positive Experience (%), 2014

Top 10 Countries for Customers with a Positive Customer Experience (%), 2014

Bottom 10 Countries for Customers with a Positive Customer Experience (%), 2014

44.5%

39.5%

40.6%

38.6%

43.1%

31.3%

39.8%

41.2%

51.3%

43.6%

32.0%

33.0%

33.3%

35.2%

35.7%

36.1%

36.7%

37.3%

40.8%

43.0%

U.S.

Netherlands

Germany

Australia

Switzerland

South Africa

Portugal

Belgium

Canada

Austria

32.2%

29.7%

25.9%

20.4%

21.1%

19.8%

17.5%

22.2%

16.4%

15.0%

24.6%

20132014

23.6%

22.8%

20.6%

20.5%

20.0%

19.7%

19.6%

19.5%

15.2%

India

Poland

Sweden

Russia

Taiwan

Singapore

Hong Kong

Japan

China

South Korea

2014Rank

2013Rank

01

02

03

04

05

06

07

08

09

10

03

01

05

07

16

04

10

06

08

02

2014Rank

2013Rank

30

29

24

28

27

25

26

23

20

13

30

29

28

27

26

25

24

23

22

21

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2013, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 16/60

16

positive experiences dictates a moderated approach tochannel management. While insurers need to continueenhancing mobile and social media channels, theyshould take care to ensure that these enhancements

are not carried out at the expense of the agencychannel. Rather, ongoing investments need to supportall types of channels, at least for the foreseeable future.

In addition, insurers should strive to bring some ofthe qualities that define traditional channels to thenewer channels, and vice versa. For example, insurersshould try to replicate the intimacy and personalservice that characterize the agent channel as theydevelop more modern channels. Similarly, they shouldempower their agents with digital tools that advancethe convenience and availability found in newer types

of channels.

In the future, usage of Internet-mobile and socialmedia channels are expected to increase more thanusage of traditional channels. Furthermore, the

Internet-PC may challenge the agent channel as themost frequently used channel. It is currently the mostfrequently used channel during pre-sale (informationgathering and quote search) and insurers need to

enhance their seamless integration capabilities in orderto meet expectations in one of the more prevalentcustomer journeys of research online-purchase offline.Customers will continue to place high importanceacross the full range of channels for their insuranceneeds. Insurers thus need to focus on deliveringexcellent service across all channels. Currently, thefrequency of interactions with their insurers is muchhigher for digital channels such as the Internet-PC,mobile, and social media over traditional channelssuch as agent and phone (see Figure 2.4). Insurersalso have more opportunities to provide positive

experiences to Gen Y customers as they interact withtheir insurer on a more frequent basis, especially usingmobile and social media channels. As the popularity

Figure 2.3 Positive Experience Levels by Channel and Region (%), 2014

38%

34%

36%

35%

43%

34%

30%

29%

31%

38%

Agent Phone Internet-PC

Internet-PC

35%

31%

29%

36%

40%

Agent Phone Internet-Mobile

Internet-Mobile

Social Media

Social Media

35%

30%

33%

38%

43%

Latin America

Developing

APAC

Developed

APAC

Europe

North America

Latin America

Developing

APAC

Developed

APAC

Europe

North America

32%

28%

22%

25%

33%

31%

29%

26%

22%

32%

29%

30%

23%

26%

30%

31%

32%

29%

27%

35%

Non-Life

Life

43%

38%

35%

40%

51%

49%

42%

41%

47%

57%

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 17/60

17

2015 WORLD INSURANCE REPORT CHAPTER 2

of digital channels continues to rise, insurers can usethem to increase the frequency of touch points and thenumber of opportunities to wow customers.

CLAIMS SERVICING STILL A CONCERN, BUTEFFORTS TO ENHANCE CLAIMS EXPERIENCERESULTED IN MARGINAL IMPROVEMENTS

The multi-faceted insurance lifecycle offers numerousopportunities for insurers to provide positiveexperiences to customers. Yet across almost everydimension of the lifecycle, insurers struggled to do so.

The level of positive customer experience declined fornearly all types of activities related to purchasing andholding all types of insurance policies (see Figure 2.5).

Non-life insurance customers recorded the biggestdeclines in positive experience compared tolife customers. Positive experience in the policyacquisition phase of non-life insurance declined by 5.1percentage points, followed by policy servicing, with adecline of 5.0 percentage points, and quote gatheringwith a decline of 3.6 percentage points. Despitethese large decreases, the level of positive customer

experience in non-life insurance is still considerablyhigher than in the life insurance sector, where year-to-year declines were smaller.

Figure 2.4 Frequency of Channel Usage – Gen Y Customers vs. Others (%), 2014

0%

25%

50%

75%

100%

Gen Y Others Gen Y Others Gen Y Others Gen Y Others Gen Y Others

Agent Phone Internet - PC Internet - Mobile Social Media

YearlyTwice a Year Once in Three MonthsOnce a MonthWeekly Never

11%

3%

15%

8%

12%

10%

14%

17%

19%

33%

28% 29%

17%

7%

18%

11%

15%

14%

13%

19%

14%

25%

23% 24%

25%

14%

20%

16%

14%

14%

11%

15%

12%

19%

19%22%

20%

10%

18%

10%

11%

9%

8%

8%

9%

10%

34%

54%

18%

8%

13%

7%

9%

6%

7%

5%

8%

8%

44%

66%

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

Claims servicing remains the lifecycle stage with thelowest levels of positive experience for both life andnon-life customers; however, the decline in experiencelevels was lowest for claims servicing. The lower rateof decline indicates that insurers are taking stepsto enhance the claims experience. Nevertheless,customers still view these efforts as inadequate.Effectively leveraging technology to minimize theimpact of risk and deliver faster processing can helpenhance the overall claims experience of customers.

A close look at the data related to claims servicingunderscores the difficulty of delivering positivecustomer experiences in that area (see Figure 2.6).

Auto and property insurance customers who made anyclaim in the past year had significantly lower positiveexperience levels than customers who did not makea claim. In North America, for example, only 24% ofproperty insurance customers who made a claim inthe past year reported a positive experience, comparedto 47% of customers who did not make a claim.

The lower levels of positive experience related to

claims servicing were pervasive, despite ongoingefforts insurers have made to automate the claimsprocess. For customers increasingly accustomed

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 18/60

18

Figure 2.6 Impact of Claims on Positive Customer Experience

Customers with Positive Experience for

Auto Insurance, by Region (%), 2014

Customers with Positive Experience for

Property Insurance, by Region (%), 2014

Customers who haven’t made any claim in the past yearCustomers who have made a claim in the past year

Developed

APAC

32%

31%

27%

33%

Europe31%

39%

30%

40%

31%

38%Latin America

34%

34%

North America37%

46%

24%

47%

Developing

APAC

26%

29%

20%

29%

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

Figure 2.5 Insurance Customers with Positive Experience, by Lifecycle Stage (%), 2013–2014

Life Non-Life

20142013

% Point Change

2013–14

(1.2%)

(1.8%)

(0.1%)

0.7%

% Point Change

2013–14

(3.6%)

(5.1%)

(5.0%)

(2.3%)35.1%

34.4%

37.0%

37.1%

38.6%

40.4%

37.3%

38.5%

40.7%

43.0%

42.8%

47.8%

44.3%

49.5%

44.6%

48.2%

Claims Servicing

Policy Servicing

Policy Acquisition

Quote Gathering

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

to conducting a wide range of personal activityvia streamlined, frictionless internet and mobiletransactions, the insurance claims process likelyfeels inconvenient and cumbersome. The pressure

for insurers to provide a quick and efficient response

is even greater, given that claims are typically tied toan undesirable incident. Additionally, faster claimsprocessing can save significant costs for the insurer.The longer a claim remains open, the more it is

going to cost the insurer. Insurers’ performance in

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 19/60

19

2015 WORLD INSURANCE REPORT CHAPTER 2

claims servicing is probably the result of customerexpectations that have been set beyond most insurers’current capabilities.

GEN Y SEGMENT PRESENTS HUGE CHALLENGEFOR INSURERS, ESPECIALLY IN DEVELOPEDMARKETS, AS THEY STRIVE TO MATCH RISINGEXPECTATIONS

Generation Y, the customer segment aged between18 and 34, is said to be comprised of individualswho are confident, ambitious and most important,tech-savvy. Having never experienced adult lifewithout the aid of the internet or smart devices,digital technology is essential to the Gen Y lifestyle.

With Gen Y comprising one-quarter to one-third ofthe population in many markets, this segment is of

high importance to insurance firms, especially giventhe high potential of their lifetime values. Insurersmust devise strategies that can attract and retainthis valuable age segment. The downside is that Gen

Y expectations are quite lofty. Any failure to matchthese expectations will result in a negative impact onexperience, as witnessed in our findings this year.

Especially in developed markets, the drop in customerexperience levels for Gen Y customers was very steep(see Figure 2.7). For life customers in developed Asia-Pacific, for example, the positive experiences of Gen

Yers decreased by 5.4 percentage points, compared

to an increase of 1.5 percentage points for those older

Figure 2.7 Change in Customers with Positive Experience, by Age and Region (%), 2013 –14

Life Non-Life

(1.6%)

(1.4%)

(0.6%)

1.5%

1.3%

(2.3%)

(3.0%)

(3.1%)

(5.4%)

(10.9%)

(6.0%)

(6.4%)

(3.8%)

(2.5%)

(7.9%)

(6.7%)

(2.7%)

(7.2%)

(7.3%)

(14.6%)North America

18-34 Years 34+ Years

Developed APAC

Europe

Developing APAC

Latin America

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

than 34. In North America, the difference was evenmore marked, with positive experiences decliningby 10.9 percentage points for Gen Yers, comparedto an increase of 1.3 percentage points for older

respondents.

This decrease in positive experience for Gen Ycustomers contributed significantly to the overalldecline in positive experience levels throughout theindustry. The largest Gen Y-related decreases occurredin North America among life and non-life customers,as well as in developed Asia-Pacific and Europe amongnon-life customers. These results underscore the veryhigh service expectations that Gen Yers have cultivatedas a result of having grown up on a full array of digitalmedia and servicing from a wide range of providers.

As a result, insurers must continue to adapt the qualityof their automated digital services to cater to thehigher expectations of Gen Yers, or risk losing them tonewer, more agile competitors.

Gen Y Customers Place Much Higher Importanceon Mobile, Social Media ChannelsGen Y customers, given their affinity for technologyand their expectations around instant access toinformation and service convenience, are far moreinterested than older customers in using advancedalternate channels (see Figure 2.8). In North America,

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 20/60

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 21/60

21

2015 WORLD INSURANCE REPORT CHAPTER 2

The majority of customers, no matter their age, hadfewer positive experiences regardless of the channelthey used. This widespread dissatisfaction may be areflection of the difficulties providers are having asthey maintain existing channels while also addingnew ones. The most significant difference betweenGen Y and non-Gen Y customers came in theirassessment of social media. More than 50% of Gen

Yers cited social media as an important channel,compared to only 30% of older customers.

CUSTOMER ADVOCACY LAGS IN EUROPE AND DEVELOPED ASIA-PACIFIC

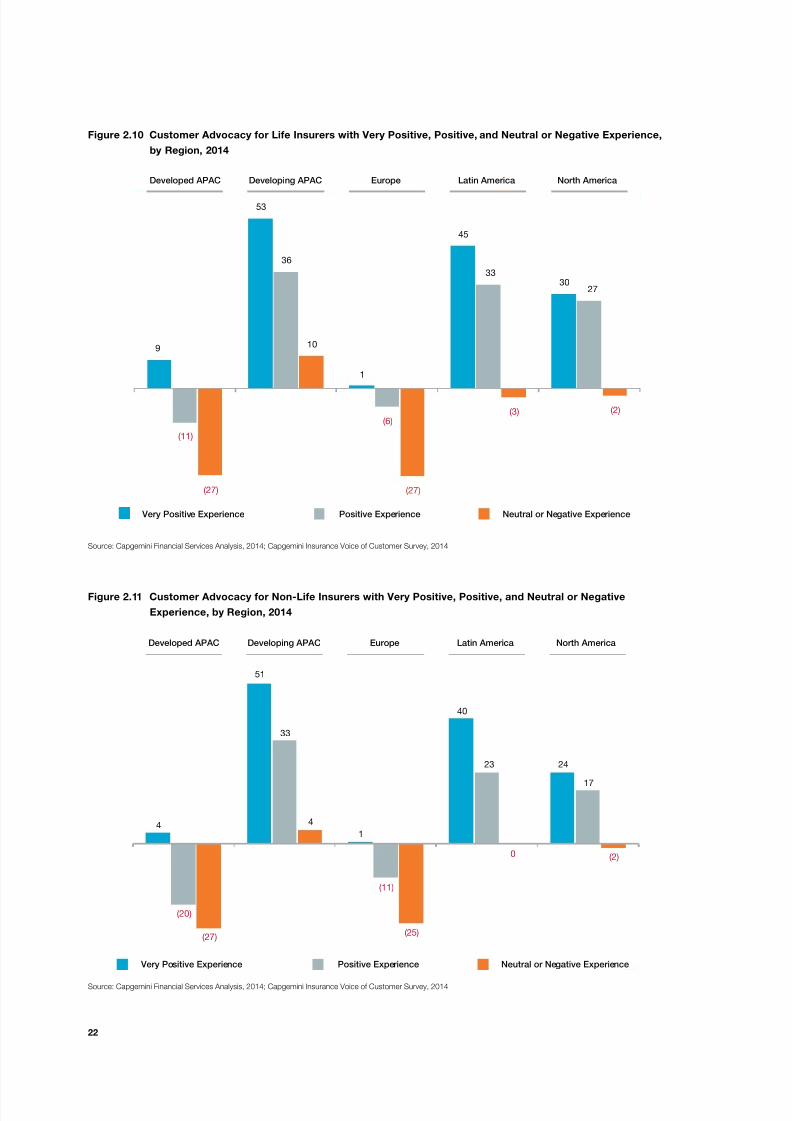

For insurers interested in acquiring new customersand strengthening their market position, there is nobetter ally than the customer advocate. Our findingsrelated to customer advocacy3 proved that positivecustomer experience is fundamental to increasingcustomer advocacy (see Figure 2.10 and Figure 2.11).Further, some regions have much higher advocacylevels than others.

Figure 2.9 Importance vs. Positive Experience with Channel for Gen Y Customers and Others, 2012–2014

Customers with positive experience with channel (%)

C h a n n e l I m p o r t a n c e ( % )

2012 2014Gen Y Others

Agent

Phone

Bank

BrokerInternet-Mobile Internet-Mobile

Internet-Mobile

Internet-Mobile

Agent

Broker

Bank

Phone

Internet-PC

Internet-PC Internet-PC

Internet-PC

Social Media

Agent

Broker

Bank

Phone

Agent

BrokerBank

Phone

Social Media

30%

40%

50%

60%

70%

80%

10% 20% 30% 40% 50%

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

In developing Asia-Pacific, Latin America, and North America, customers with very positive and positiveexperiences displayed much higher advocacy levelsthan customers with neutral or negative experiences.In developing Asia-Pacific and Latin America,customers who had very positive experiencesrecorded the highest advocacy levels-53 and45, respectively, for life customers, and 51 and 40,respectively, for non-life customers

Meanwhile, customer advocacy levels in developed

Asia-Pacific and Europe were much lower than inother regions. Though delighted customers (i.e., thosewith very positive experiences) in developed Asia-Pacific and Europe had higher levels of customeradvocacy, the levels did not reach nearly the sameheights as in other regions. In effect, insurers mustaim very high in providing a delightful experience.

3 “Customer advocacy rates were calculated by asking customers how likely they were to refer a friend, family member, or colleague, and

determining the difference between the percentage of customers likely to refer and those not likely"

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 22/60

22

Figure 2.10 Customer Advocacy for Life Insurers with Very Positive, Positive, and Neutral or Negative Experience,

by Region, 2014

(27)

9

53

1

45

30

(11)

36

(6)

33

27

10

(27)

(3) (2)

Developed APAC Developing APAC Europe Latin America North America

Very Positive Experience Positive Experience Neutral or Negative Experience

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

Figure 2.11 Customer Advocacy for Non-Life Insurers with Very Positive, Positive, and Neutral or Negative

Experience, by Region, 2014

(27)

4

51

1

40

24

(20)

33

(11)

23

17

4

(25)

0 (2)

Developed APAC Developing APAC Europe Latin America North America

Very Positive Experience Positive Experience Neutral or Negative Experience

Source: Capgemini Financial Services Analysis, 2014; Capgemini Insurance Voice of Customer Survey, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 23/60

23

2015 WORLD INSURANCE REPORT CHAPTER 2

Especially for customers in Europe and developed Asia-Pacific, the delivery of a very positive experiencehas become a bare minimum necessity.

An important point to note is that even for thosecustomers who had a positive experience, theadvocacy levels were negative in the regions of Europeand developed Asia-Pacific (-6 and -11, respectively forlife insurance and -11 and -20, respectively, for non-lifecustomers).

CONCLUSION

Expectations are one of many factors that lead topositive customer experiences in the insuranceindustry. As customers have become increasinglyexposed to advanced digital services from a wide

range of providers, their expectations with respectto insurers have become heightened. Insurers havehad a hard time meeting these higher expectations,particularly when it comes to the complicatedmatter of settling claims, or interacting with digitallydemanding Gen Yers.

Insurers can take a number of steps to counteract thenegative impact that heightened expectations havehad on the level of positive customer experiences.Given the strong affinity that customers have toward

traditional channels like agents, and the growingpopularity of alternate channels, insurers shouldstrive to blend the most beneficial qualities of each.

Agents can be empowered with digital tools, whilealternate channels can become more customized andpersonalized.

Hitting upon a winning formula for service deliverycan help insurers move back up the scale in creatingpositive customer experiences. Such experiencesare crucial to building customer advocacy, an all-important measure of customer loyalty, engagement,

and profitability.

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 24/60

24

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 25/60

2015 WORLD INSURANCE REPORT CHAPTER 3

25

C H A P T E

R 1

Disruptive Change

Requires Insurers of theFuture to SharpenStrategic, Analytic Skills

C H A

P T E R 3

2015 WORLD INSURANCE REPORT CHAPTER 3

WIDE VARIETY OF DISRUPTORS LOOM

For decades, even centuries, the classic insurancesale has involved a warm handshake. Agentsselling traditional products focused on deliveringpersonalized service through face-to-face visits, oftenin a customer’s own home or office. The consultativeselling process, which hinged on lengthy relationshipbuilding, could take weeks.

When the internet entered onto the scene in the late1990s, communication that was once dependenton human interaction found a new outlet. Though

agents and brokers continued to be the preferred saleschannel, the internet began to attract greater numbersof users, while the addition of other alternate channelsfragmented distribution even more. Internet-PC hasnow become the second most preferred channel forinsurance customers and is fast catching up with thetraditional channel of agent.

Though the internet’s influence has been significant, itwas only the first of several disruptors impacting theinsurance industry in a significant manner (see Figure3.1). Insurers are going to be impacted significantly

KEY FINDINGS

Big Data analytics is expected to have the biggest impact by far on the insurance industry,with 78% of executives citing it as a key disruptive force. Regulatory change was rankedsecond at 46% and economic uncertainty ranked third at 42%.

These top three disruptive forces represent only a small portion of the many factorsexpected to dramatically affect the insurance landscape. Other disruptive agents includedemographic shifts, extreme weather events, new competition from non-insurers, andadvanced technology.

Insurers globally are falling short of their desired maturity levels in every one of sevencore capabilities identified in our Insurance Capability Maturity Model (see Figure 3.7). Tobetter prepare for the many changes looming ahead, insurers must assess their current strengthsand weaknesses, and develop a strategic plan for moving forward.

Insurers globally are performing at the lowest maturity levels when it comes to capabilitiesrelated to customer interactions. These include connecting elegantly with customers, engagingregularly with them, and having a complete view of customer data and relationships.

Regional differences are exhibited by insurers in their maturity levels related to variouscapabilities. Insurers in North America operated at much higher maturity levels across all corecapabilities when compared to those in other regions.

To move from the current states of mostly basic and median competency to leading-edgeand advanced practices, insurers must adopt a more customer-centric approach. The useof analytics to assimilate customer data, view relationships as a whole, and deliver personalizedproducts through appropriate channels will be essential to succeeding as a customer-oriented

insurer of the future.

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 26/60

26

in the very near future and in some cases they arealready facing the impact. This series of rifts will affectthe industry’s traditional products, processes, andchannels, forcing insurers to innovate or lose out on

new opportunities.

The disruptors on the horizon encompass a widerange of change.

Demographic ShiftsGlobally, the population of people aged 65 years andolder is expected to triple to 1.5 billion by mid-century4, presenting a host of economic and socialburdens. For insurers, the aging population will likelytrigger higher demand for products related to anolder customer base, such as retirement income and

long-term care insurance. Increasing rate of urbanmigration, especially in emerging markets, is alsoleading to change in the demand for different insuranceproducts. The shifting population will also affect theprocesses insurers use to calculate vital rates, as well asassumptions about future ranges of uncertainty, whichwill inf luence product pricing and underwriting.

Aside from an aging population, the number of teendrivers and single-parent families are expected torise in the future. The longevity of the world’s olderpopulation, combined with growing numbers of

younger customers, will put pressure on insurersto offer a full suite of robust delivery channels thatcan meet the broad range of customer distributionpreferences. In effect, from a demographic perspective,insurers have opportunities to offer new products foran aging population, as well as multi-faceted deliverychannels for an increasingly diverse customer set.

Increased Frequency of Extreme Weather EventsGrowing rates of natural calamities, combined withincreasing urbanization of disaster-prone areas,is causing the economic costs of calamities to rise

precipitously. Three times as many natural disastersoccurred from 2000 through 2009, as did from 1980through 1989, with growth in climate-related eventsaccounting for nearly 80% of the increase.5 From 1980to 2011, estimated damages caused by natural disastersrose from about $25 billion to about $350 billion.6

4 “Attitudes about Aging: A Global Perspective”, Pew Research Global Attitudes Project Januar y 30, 2014.

5 “Natural Disasters, Armed Confl ict and Public Health”,The New England Journal of Medicine, Jennifer Leaning, MD and Debarati Guha-Sapir,

PhD, November 13, 2013

6 EM-DAT, The International Disaster Database, www.emdat.be/natural-disasters-trends

Figure 3.1 Key Disruptors for Insurers

Disruptors

Where Are

My New

Customer

Segments?

Why Aren’t

My Investment

Returns

Attractive?

What’s the

Reason for

Rising Claims

Expenses?

Who’sEating

My Pie?

Is Big

Brother’s

Supervision

Increasing?

How Is

It All

Connected?

Demographic Changes

Demographic changesinfluence product pricing,

underwriting as life

expectancy continues to

increase across major

markets along with

increasing urbanization

Financial and Economic

Conditions

Insurance industry

continues to operate in an

uncertain macroeconomic

environment which might

negatively impact

investment returns

Regulatory Intervention

and Scrutiny

Insurers now have to

comply with higher number

of regulations leading to

increased data storage and

reporting; regulators are

pushing insurers toward

improved transparency

Extreme Environmental

Conditions and

CatastrophesRecently recurring

catastrophic events in

places without prior history

such as tsunami, storm,

floods, etc have resulted in

increased costs for insurers

New Entrants (Non-Core

Insurance Players)

New competition has

emerged from non-core

insurance players such as

Walmart and Google, as

they enter the insurance

arena

Technology

Advancements

The connectivity of devices

has led to an age of

Internet of Things making it

necessary to invest in

social media, mobile,

analytics, and cloud

computing

Source: Capgemini Financial Services Analysis, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 27/60

27

2015 WORLD INSURANCE REPORT CHAPTER 3

The rising cost of claims associated with disasters ischanging the landscape of the insurance business.From a product perspective, insurers need to consideradding riders to their policies, as well as new products,

to address co-insurance needs. In terms of processes,insurers have an immediate need to expand theiruse of advanced modeling tools to better predictcatastrophes and expected losses. From a channelpoint of view, disasters offer insurers the opportunityto move more customers to alternate channels. In anemergency, more customers may be impelled to turnto alternate channels such as mobile and social mediato receive faster turnarounds on claims. Insurerscould also use these channels to warn customersabout impending disasters, as a way of mitigatingrisk. Though extreme weather poses serious threats,

insurers have tools at their disposal, such as analytics,to predict catastrophic events and the incidence ofclaims, which help them better manage the eventand overcome risks, positioning the company with acompetitive advantage.

New Entrants

Many companies with little or no backgroundin insurance see opportunity to bring greatertransparency and simplicity to the processes ofresearching and purchasing insurance. Thesecompanies have inherent advantages that may positionthem as threats to existing insurers. The U.S. discountretailer Walmart, for example, plans to market healthinsurance plans online and through its stores to itsmassive existing loyal customer base7, an effort thatcould fracture existing ties insurers have with theircustomers and distributors. Insurers are also waryof high-tech firms like Google or Amazon, whichcould parlay their expertise in areas such as searchengines and one-click shopping to the insurancearena. Google has in fact made some inroads in thisdirection with the acquisition of an aggregator websiteBeatThatQuote.com in the U.K. region. Other pursuitsof Google such as driverless cars, Google Glass, and

automated home technology are likely to have hugeimplications on the insurance industry.

The threat of competition from new, innovativeentrants should propel insurers to aim higher interms of developing more personalized productsand delivering them through convenient, digitalchannels. Opportunities exist for insurers to take

advantage of in-house customer data to developproducts that reflect improved risk profiling and theimpact of customer life events. Insurers may also wantto consider forming strategic alliances with non-

traditional players to broaden their expertise in areassuch as product distribution and development andgain access to better risk profiling.

Economic UncertaintyFive years on from the financial crisis, the globaleconomy still is not back to its pre-crisis form, raisingthe specter of an ongoing strain on insurance profitmargins. In addition, the persistent global financialpressure may cause consumers to curtail theirpurchases of cars and homes, thus lessening demandfor basic insurance products. Near-zero interest rates

in several developed markets also have a significantimpact on insurers’ investment returns.

Increasing uncertainty about profit margins couldhave a significant impact on product line-ups. Insurersmay want to simplify their existing product lines sothat it becomes easy for customers to understandthese products better and thereby enable sales throughdirect channels or develop niche products for whichthey can charge higher premiums. In addition,consumer demand for various products may shiftbased on prevailing economic conditions, creating the

need for insurers to flexibly respond with both saferfixed-income products and higher-return, equity-linked products. Finally, dampened buying behaviorby consumers may lead insurers to develop newproducts built around evolving consumer models.

An example of one such model is the car-sharingservice, Zipcar.

With rising economic uncertainty, insurers will feelgreater pressure to increase operational efficienciesand reduce the time to market for new products. Theymay also want to optimize their distribution channelsby pushing simpler products toward alternate

channels as a way of reducing costs, while utilizingthe agency network to leverage the potential for cross-selling and up-selling. All in all, financial pressureswill likely encourage insurers to become bolder aboutchoosing and executing upon a particular strategy-beit in product innovation, operational improvement, orchannel distribution-to overcome the profit pressuresof financial instability.

7 “You Can Now Get Health Insurance at WalMart”, Huff Post Business, Anne D’Innocenzio, October 6, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 28/60

28

Regulatory Change

One outcome of the global financial crisis hasbeen a comprehensive examination of supervisorypractices, accompanied by a raft of new guidelines

and requirements for insurance firms and theirholding companies. New sets of complex regulatoryand reporting standards are affecting all aspects ofthe business, including financial reporting, capitalfinancing, consumer protection, risk management,exposure, transparency, and others. This regulatorychange is occurring at the national, global, andregional levels.

In some cases, the regulatory burden could be onerousenough to cause insurers to alter existing products oreven stop offering certain ones altogether. At the very

least, many insurers expect to introduce changes inproduct design and pricing in response to impendingregulatory requirements. Insurers will need tounderstand how regulatory changes will impactthe business and long-held processes, and ensurethey have the technical knowledge and expertiseto properly implement the new rules, as well as putin place appropriate measures for ongoing control

and governance. They will need to have systems anddistribution channels that are flexible enough toincorporate the regulatory changes and also adapt tofuture ones. For well-prepared insurers, the massive

amount of regulatory change offers an opportunityto assess and upgrade current reporting functionsand enterprise risk management, as well as evaluatewhether new talent is needed.

Internet of Things

The internet, already a source of lasting impact onthe insurance industry, will continue to act as a majordisruptor as it evolves to incorporate the Internet ofThings (IoT). Any type of natural or man-made objectcan become part of the IoT network and have theability to transfer data over it. Under such a scenario,

devices such as heart monitors, car engines, and stressgauges on bridges, will be able to transmit real-timestatus information to data stores where it can beanalyzed.

Access to all this data could fundamentally alter theinsurance business by providing a much more detailedview of an insurer’s exposures and risks. Insurers

Figure 3.2 Disruptors with Maximum Impact on Insurance Industry (%), 2014

1%

1%

4%

2%

7%

8%

18%

14%

25%

20%

5%

6%

7%

7%

10%

7%

7%

7%

16%

27%

3%

3%

4%

12%

5%

8%

10%

21%

5%

31%

9%

10%

15%

21%

22%

23%

35%

42%

46%

78%

0% 20% 40% 60% 80%

New Risk Perceptions

Social Media

Extreme Weather Events

Internet of Things

New Entrants

Mobile Applications

Changing Demographics

& Millennials

Financial / Economic

conditions

Increased Regulatory

Oversight

Big Data Analytics

Rank 1 Rank 2

Disruptors with Maximum Impact on Insurance Industry (%), 2014

Rank 3

“Regulators aim to protect

the consumer, which is

laudable, but there are now

multiple regulators with

sometimes conflicting

agendas. This creates much

difficulty for us.”

- CIO of a Leading

Insurance Firm in Europe.

“Statistics, better risk

profiling and the huge

amount of information

that can be retrieved from

users’ experience or

obtained from the web

and social networks will

enable a change in the

logic of the definition of

pricing: from static

conventional variables todynamic behavioral

variables” - Filippo

Sirotti (CEO, Quixa)

“Changing demographics

change the expectations of

what is required from

insurance cover. Newer

generations and the impactof austerity have created a

different attitude to risk and

what customers may be

happy to cover for them

selves. Customers are more

savvy and more willing to

trade. New generations in

particular have different

values and priorities.

Insurance is not as high a

priority – but once they buy

it then they expect to get

more in return.”

- Matthew Thomas

Director Strategy and

Planning Ageas UK

Source: Capgemini Financial Services Analysis, 2014; Capgemini WIR 2015 Executive Interviews

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 29/60

29

2015 WORLD INSURANCE REPORT CHAPTER 3

could use this data to redesign or re-price products tomake them less risky and more profitable. Further, bydeveloping a robust, multi-channel feedback loop withcustomers, insurers will be able to act upon the data

they receive and potentially reduce losses. The IoT willno doubt tax the ability of insurers to store, model, andanalyze all the data it generates. Privacy issues willalso likely arise, perhaps leading to more burdensomeregulations. But for insurers who embrace thesechallenges, the IoT offers the potential to expand thelevel of detail related to every aspect of the business,from product design and pricing, to underwriting,service, and claims.

Largest Disruptor of All is Analytics A common denominator in all of these forces is the

powerful impact that data analytics can have onilluminating both the risks and opportunities relevantto each disruptor. In every case, analytics based on BigData can be used to identify threats and minimize theincidence of loss. In fact, industry executives identifiedBig Data analytics as having the greatest impact onthe insurance industry, with 78% ranking it as one ofthe top 3 disruptors, well above increased regulatoryoversight, which was ranked by 46% of executives(see Figure 3.2). In North America, insurers believeanalytics will have more impact on the insuranceindustry than any other disruptor. In Europe and Asia-Pacific, insurers ranked it as a close second. Because ofits reach, analytics has the potential to change the verynature of the business. Several insurance executives

expect analytics to enable a change in their pricingmodels that are currently based on static conventionalvariables to more accurate and dynamic behavioralvariables. Given its expected impact on pricing,

underwriting, and the business in general, insurersmust begin sharpening their expertise and skills inanalytics in short order.

QUICKENING TRENDS POINT TO ADDITIONAL VULNERABILITIES

Insurers may be in the business of identifying andminimizing risks, but that does not make themimmune to outside forces. The disruptors outlinedin the previous section make insurers vulnerableto several trends in the near future, all of whichhave the potential to undermine the business, if no

counterbalancing measures are taken.

Rising Consumer Expectations

Consumers have become accustomed to the idea ofinstant gratification through the web, as capabilitieslike one-click shopping, instant downloads, andimmediate access to a person’s full social networkbecome the norm. The rapid-response serviceconsumers receive from other providers hasheightened the expectations they have of theirinsurers, making it only natural that they should startto demand capabilities like personalized insuranceproducts and location-based awareness. Among otherdemands, customers expect simpler procedures forchoosing, paying for, and renewing policies, and

Figure 3.3 Importance of Seamless Channel Experience (%), 2014

2.0% - Not Important at all

4.2% - Somewhat Unimportant

1.3% - Unimportant

22.2%

Important

14.7%

Very Important

26.8%

Neutral

28.8%

Somewhat Important

Source: Capgemini Financial Services Analysis, 2014

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 30/60

30

quicker claims processing through improvementssuch as photo and video estimating, ease of uploadingdocuments and proofs, mobile-based paymentsand receipts, automated assignment of claims to an

adjuster, and straight-through processing.

Meeting the higher expectations of consumers willrequire insurers to place greater value on customerperceptions. Insurers will need to review, andpotentially revamp, every angle of the insuranceprocess from the customer perspective. Better visibilityon pricing, quicker problem resolution, improvedprivacy protections, and greater product choice willbe among the priorities of customers in this newenvironment. To better compete, insurers mustbe prepared to make the necessary investments to

becoming fully customer centric.

Changing Channel Preferences

Non-traditional channels, not only the internet, butalso mobile and social media have already had a largeimpact on insurance sales and distribution. Overtime, growth in these alternate channels is expectedto continue to expand, both organically and at theexpense of traditional channels. And even though in-person agents will remain relevant to the sales process,alternate channels, such as video, e-mail, text, andsocial media, will increasingly be used to supplement

their interactions.

Currently, social media accounts for a small portionof insurer transactions. Most insurers (85%) view itmore as a vehicle for improving and building theirbrand image. But many other value-added focus areasexist, including connecting agents with customers andproviding a feedback loop for customer opinions.

Aside from supporting a wide range of channels,insurers need to ensure customers can moveseamlessly between channels and receive consistentservice across all of them. More than two-thirds of thecustomers noted that it is important for their insurerto offer a seamless channel experience (see Figure3.3). Among the customers who received a seamlesschannel experience from their insurer, 51.3% of themwere satisfied with the level of service being offered.The positive experience levels of customers who weresatisfied with the seamless channel experience offeredby their insurer are quite high at 72%. Offering high-quality, seamless channel service is a highly effectivestrategy that can enhance customer experiencesignificantly.

Entry of Non-core Insurance PlayersConsumer companies that have built up largecustomer bases through their online or digital

platforms have the ability to enter the insurancespace free from the burden of legacy platforms. Suchcompanies could lure away potential new customers,presenting a considerable threat. The Japanese

shopping site, Rakuten, for example, is leveraging itswell-established customer connections and advanceddigital servicing capabilities to offer insurance policiesover the internet at very low premiums. Alternatively,insurers could band with new types of competitors,entering into strategic alliances that would draw uponthe strengths of each firm. Already, such alliances havetaken on multiple forms. American Family Insurancein the United States has teamed with Microsoft tosupport startups that specialize in advancementsleading to safer and smarter homes. Allstate Canadahas teamed with a provider of home monitoring and

security to offer a 25% discount to customers whoinstall the system.

Coles, one of the largest supermarket chains in Australia, which began offering car insurance in2010, has recently entered the life insurance space aswell. While its car insurance is issued by Wesfarmersinsurance, the life insurance partnership is withMetLife. Due to its vast customer reach, Coles hasbeen successful in increasing the number of insurancepolicies sold on a regular basis. As of May 2014, Coleshas signed up more than 330,000 insurance customerswhile its rival supermarket, Woolworths, has close to125,000 insurance customers. Such alliances illustratethe need of insurers to be open to the possibilities ofthe services that outside providers can offer.

Emergence of Niche Insurance Products

New business models and markets are leading to theemergence of unknown risks. The advent of driverlesscars, for example, raises questions around liability. Inthe event of driverless accidents, liability could shiftto manufacturers and software providers, creating theneed for a new type of insurance product. Similarly,growing cyber-security threats are increasing the

need for new types of cyber insurance. Other factors,like rising air pollution and the expanding use ofe-cigarettes, may potentially trigger liability claimsin the future, though the exact level of risk related tothese factors is still unknown. Insurance firms thatcan accurately assess and price these new types ofrisks will have a competitive advantage as these nicheinsurance products emerge.

Risk Mitigation TechnologiesIndustries including automotive, health care, andhome security are exploring the use of various

technologies to help them reduce consumer risks.Over the next several years, carmakers are expectedto develop and make available a wide range of risk-

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 31/60

31

2015 WORLD INSURANCE REPORT CHAPTER 3

mitigating technologies, including telematics aimed atdelivering safety services directly to cars, and collisionavoidance systems aimed at reducing the severity ofaccidents (see Figure 3.4). These technologies have

the multiple benefits of minimizing risks, while alsoproviding insurers with information that can beused to sell more personalized products and increasecustomer intimacy. Our research found that 65% ofcustomers would let insurers monitor their drivingbehavior in exchange for reduced premiums based onpositive risk assessments.

Advancements in health care are similarly makingit possible for insurers to monitor the health of theircustomers. For example, fitness bands and other typesof wearable technology can be used to detect physical

changes or unhealthy behaviors. Despite data privacyconcerns, a majority of customers (56%) are willingto allow insurers to track their health conditions inreturn for reduced premiums in the case of a positive

risk assessment. The Vitality Group, a member ofSouth Africa based Discovery Holdings Limited, isan early innovator in this field, granting customerspremium discounts and other rewards for improving

their health and fitness.

More than 50% of non-life customers are willing toallow insurers to monitor their driving habits in returnfor better risk assessment and personalized advice,while nearly two-thirds of them would allow insurersto do so in return for a reduced premium for a positiverisk assessment (see Figure 3.5). Several insurers havealready begun to leverage telematics for this purposewhile others are likely to follow suit in the near future.

Finally, technology in the form of smart home

systems is also affecting insurers. Such systems detectthe risks of f loods, fires, gas leaks, and burglaries,triggering real-time alerts to customers and insurers.Ideally, such systems will work on a proactive basis to

Figure 3.4 Expected Timelines for Adoption of Risk Mitigation Technologies in Auto Industry

2012 2013–2017

Mandatory a

Telematics

Robot/Driverless

Cars

Robot/Driverless

Cars

Collision Avoidance

Automated TrafficLaw Enforcement

Collision Avoidance

Automated Traffic

Law Enforcement

Preferredb

Voluntary c

Availabled

2018–2020 2023–2027

Telematics

Collision Avoidance

Automated Traffic

Law Enforcement

Robot/Driverless

Cars

Automation of enforcement of traffic laws

(obeying stoplights and stop signs, driving

within posted speed limits or according to

prevailing conditions, etc.) is being done by

technologies such as automatic red light

cameras and stoplight cameras

Automated

Traffic Law

Enforcement

With the introduction of robot or driverless

cars, insurance industry is likely to experience

a major shift in product designing as number

of accidents could come down. This is likely to

have a huge impact on motor insurance

industry

Auto manufacturers have built several different

collision avoidance systems and identified the

ones that have had a significant impact on

reducing the amount, and severity of accidents

Usage based insurance for the wireless

technology that delivers safety services, route

information, and entertainment to motor

vehicles

TelematicsCollision

Avoidance

System

Robot /

Driverless

Cars

Note: a. Government requires new vehicles and retrofitted older vehicles to have telematics and/or various collision avoidance technologies, and installs the environmental

hardware/systems to make automated traffic law enforcement work; b: Positive or negative incentives promote use; c: Decision based on individual vehicle owners; d: The

technology exists

Source: Capgemini Financial Services Analysis, 2014; “A Scenario: The end of Auto Insurance", Donald Light, Celent, May 8, 2012

8/19/2019 World Insurance Report 2015

http://slidepdf.com/reader/full/world-insurance-report-2015 32/60

32

prevent the occurrence of damage in the first place.Insurers should seek out partnerships with smarthome technology providers to support innovativeproducts and more flexible pricing. In the United

States, for example, State Farm has teamed up witha home security provider to offer discounts onhome monitoring systems, as well as homeownersinsurance.

Regulatory Standardization A push for more regulations and greater rulesuniformity across regions will impose a significantburden on insurance firms in the coming years. TheCommon Framework or ComFrame subjects activeinsurers internationally to more stringent capitalrequirements and imposes additional governance

and compliance guidelines related to enterprise riskmanagement. As a result, global insurers can expectincreased costs related to capital adequacy andgreater reporting complexity. Regionally, insurerswill also have to adhere to various directives. InEurope, Solvency II proposes a uniform approach formeasuring assets and liabilities, requiring insurersto demonstrate a greater understanding of the risksinherent in their business operations and products.In North America, solvency, corporate governance,accounting standards, and consumer protection are

all subject to more stringent regulation. In Asia-Pacific, the China Insurance Regulatory Commissionis shifting its focus from rules concerning productsand pricing to solvency and reporting, placing greater

importance on enhanced enterprise risk management.