wood pellets and co firing - how to compensate generators

TRANSCRIPT

Wood Pellets – Co‐Firing With Coal How to Compensate Generators for the

Higher Cost of Generation

Eric KingsleyInnovative Natural Resource Solutions LLC

[email protected] 207‐233‐9910

June 2015

Innovative Natural Resource Solutions LLC• Based in New Hampshire and Maine, a region with 25+ years of continuous biomass power experience, and pellet mills for 15+ years

• Based in the forest industry – work at the intersection of forest industry, energy and economic development

• My focus is on feedstock supply for biomass electric, thermal, pellet and liquid fuel projects

• Structured over a dozen long‐term supply agreements• Clients include utilities, merchant generators, investors, developers, and industries

• Supported conversion of four coal plants to biomass, and currently working with a coal and wood co‐fired unit

• Conduct work in all regions of North America• www.inrsllc.com

Ways to support additional cost of co‐firing or conversion to wood pellets

•Renewable Energy Certificates (recap)•Carbon Credits•Other emissions credits•Production Tax Credit (Section 45)

Ways to support additional cost of co‐firing or conversion to wood pellets

•Renewable Energy Certificates (recap)•Carbon Credits•Other emissions credits•Production Tax Credit (Section 45)

Renewable Power1 MWH

Electricity1 MWH

Renewable Energy Certificate1 REC

Renewable Portfolio Standard Policieswww.dsireusa.org / June 2015

WA: 15% x 2020*

OR: 25%x 2025* (large utilities)

CA: 33% x 2020

MT: 15% x 2015

NV: 25% x2025* UT: 20% x

2025*†

AZ: 15% x 2025*

ND: 10% x 2015

NM: 20%x 2020 (IOUs)

HI: 100% x 2045

CO: 30% by 2020 (IOUs) *†

OK: 15% x 2015

MN:26.5% x 2025 (IOUs)

31.5% x 2020 (Xcel)

MI: 10% x 2015*†WI: 10%

2015

MO:15% x 2021

IA: 105 MW IN:10% x 2025†

IL: 25% x 2026

OH: 12.5% x 2026

NC: 12.5% x 2021 (IOUs)

VA: 15% x 2025†KS: 20% x 2020

ME: 40% x 2017

28 States + Washington DC + 3 territories have a Renewable Portfolio Standard (9 states and 1 territories have renewable portfolio goals)

Renewable portfolio standard

Renewable portfolio goal Includes non-renewable alternative resources* Extra credit for solar or customer-sited renewables†

U.S. Territories

DC

TX: 5,880 MW x 2015*

SD: 10% x 2015

SC: 2% 2021

NMI: 20% x 2016

PR: 20% x 2035

Guam: 25% x 2035

USVI: 30% x 2025

NH: 24.8 x 2025VT: 20% x 2017MA: 15% x 2020(new resources) 6.03% x 2016 (existing resources)

RI: 14.5% x 2019CT: 27% x 2020

NY: 29% x 2015

PA: 18% x 2021†

NJ: 20.38% RE x 2020 + 4.1% solar by 2027

DE: 25% x 2026*MD: 20% x 2022DC: 20% x 2020

What is a Renewable Energy Certificate?

From NH PUC rules (most states have something similar)

A renewable energy certificate encompasses all “non‐price characteristics of the electrical…energy output of a unit including, but not limited to, the unit's location, fuel type, actual emissions, vintage, and portfolio standard eligibility.”

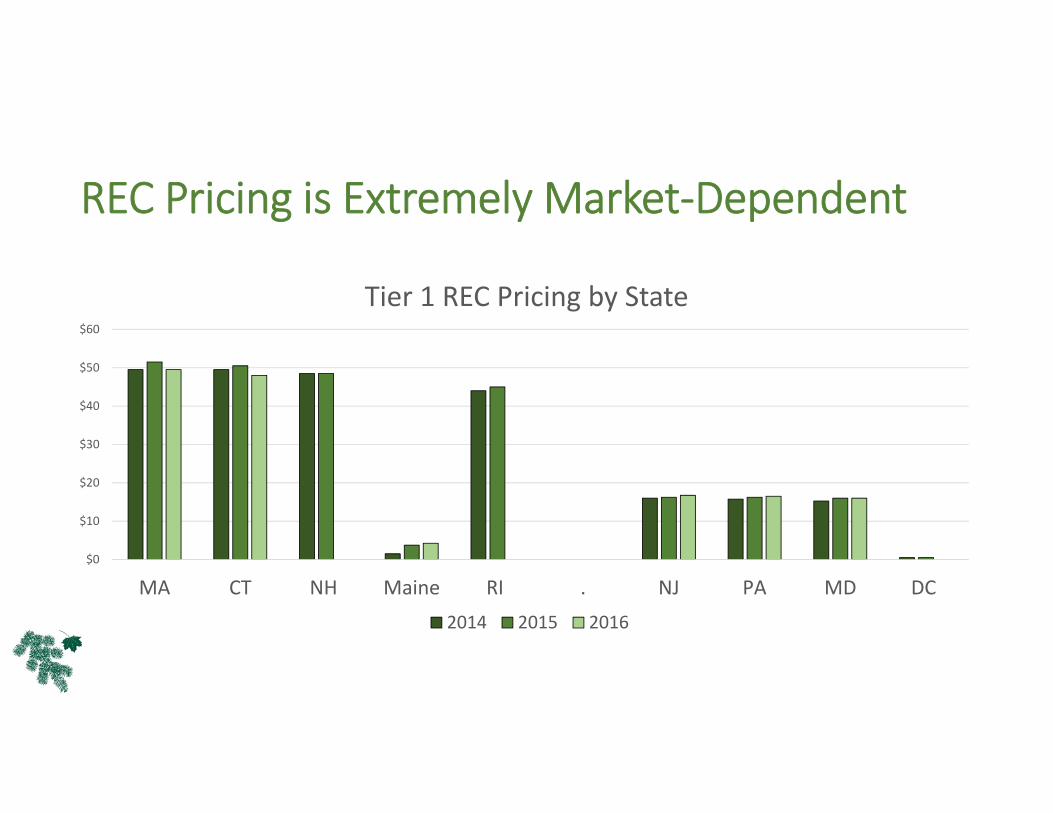

REC Pricing is Extremely Market‐Dependent

$0

$10

$20

$30

$40

$50

$60

MA CT NH Maine RI . NJ PA MD DC

Tier 1 REC Pricing by State

2014 2015 2016

Things to know about RECs

• Every state RPS is unique – know the language in and out (NH example)

• Qualification is usually binary

• The market is not just your state, but usually any state you can deliver to (e.g., ISO‐New, or PJM)

• Policies created by legislatures can be abolished by legislatures

Ways to support additional cost of co‐firing or conversion to wood pellets

•Renewable Energy Certificates (recap)•Carbon Credits•Other emissions credits•Production Tax Credit (Section 45)

Carbon is an emerging market in the U.S.

• Current function carbon markets are:• RGGI (at right)• California (CARB)

• More will come – but it will be a slow process, heavily lobbied and litigated

Two Basic Ways to Value Carbon

Positive• Get paid for doing something• If you reduce carbon, you get paid

• May be incompatible with REC sales, because the emissions attributes have already been sold bundled with the REC

Negative• Get charged (“fined” in the press release) for each unit of carbon emitted

• Puts biomass at a competitive advantage if it does not get charged (forest carbon accounting question)

• Compatible with the sale of RECs

Carbon Accounting for Biomass• Not the subject of this presentation, and a complex and disputed matter

• All sides have “100 scientists” on their side• Appears that EPA will be issuing opinion soon

• Expect most biomass – maybe all – to be considered “carbon neutral” for power plant emissions accounting

• Likely to involve state or regional sustainability oversight• Even then, some states will mess things up

• Incomplete at this time• Recognition of carbon neutrality of biomass important for accounting

Ways to support additional cost of co‐firing or conversion to wood pellets

•Renewable Energy Certificates (recap)•Carbon Credits•Other emissions credits•Production Tax Credit (Section 45)

Other (not carbon) Emissions Credits• Pretty thin market right now

• Market‐based reductions are not how most pollutants are regulated in most areas

• Have same positive / negative issue as seen in carbon• Because the REC already had the emissions attributes embedded in them

• If they existed, could be monetized uniquely (so, carbon + NOx + SO2 + …)

• Also, if unicorns existed, they could be monetized uniquely

Ways to support additional cost of co‐firing or conversion to wood pellets

•Renewable Energy Certificates (recap)•Carbon Credits•Other emissions credits•Production Tax Credit (Section 45)

Production Tax Credits (Section 45)• A federal tax credit

• Currently expired, but that happens with astounding regularity• Provides a $0.015 / kwh tax credit for qualifying technologies

• Solar• Wind• Closed‐loop biomass (including co‐firing with closed‐loop biomass)• Anaerobic digestion

• Credit lasts for 10 years• Adjusted annually for inflation

• Current value $0.022 / kwh• Open‐Loop Biomass receives credit at half rate

• Current value $0.011 / kwh• No co‐firing allowance

Closed Loop Biomass• Biomass grown specifically to be used in energy production

• “Dedicated Energy Crop”• Usually short‐rotation• Long the fascination of universities around the country

• Very challenging economics• Does not exist at meaningful scale in the wood pellet or biomass electric industry

Open Loop Biomass• Available in the real world• What almost all wood pellets are made from

• Generates as co‐product (or by‐product) of other operations

• Sawdust and chips from lumber manufacturing

• Tops and branches from logging• Unmerchantable stems during logging

• Not eligible for PTC

When using RECs and PTC, biomass can be competitive baseload generation

Testimony of Diane Lupold, DominionCASE NO. PUE‐2011‐00073 http://www.scc.virginia.gov/docketsearch/DOCS/2fzn01!.PDF

Ways to support additional cost of co‐firing or conversion to wood pellets• Regulatory systems do not yet (fully) consider co‐firing with wood pellets

• A number of programs designed when co‐firing with wood existing only in Power Point

• Some significant ways to support or incent generation, but regulatory support systems need to be modified to allow (or even encourage) the use of wood pellets in coal plants –either for co‐firing or full re‐powering