women participation in islamic microfinance in bangladesh...

TRANSCRIPT

Dr. Md. Mizanur RahmanJaiz bank, nigeria

Women Participation in Islamic Microfinance in Bangladesh and their Role to Share Prosperity: An Empirical Study

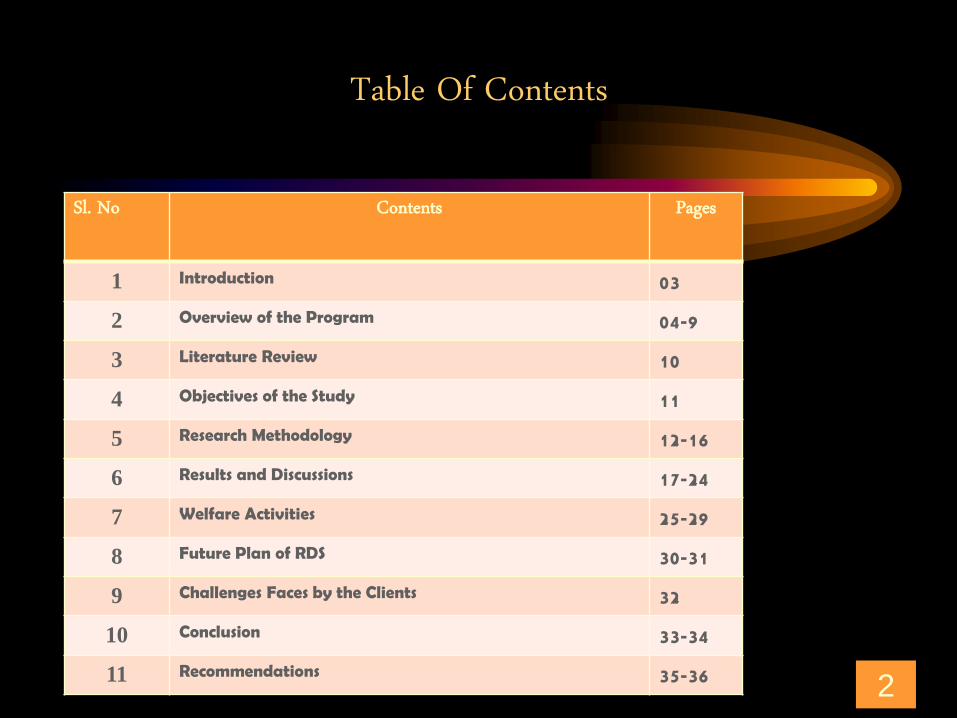

Table Of Contents

Sl. No Contents Pages

1 Introduction 03

2 Overview of the Program 04-9

3 Literature Review 10

4 Objectives of the Study 11

5 Research Methodology 12-16

6 Results and Discussions 17-24

7 Welfare Activities 25-29

8 Future Plan of RDS 30-31

9 Challenges Faces by the Clients 32

10 Conclusion 33-34

11 Recommendations 35-36 2

Introduction

• From the primitive society, women have

been marginalized;

• In Bangladesh 50% of the total population

are women, those were solely housewife;

• Dr. Mohammad Younus, developed the

collateral free institutional loan system;

• It was interest based credits and rate of

interest is very high to commensurate with

the risk in micro-finance lending;

• Clients ethics were not taken care off;

• So, RDS was developed in 1995, which

also has integrated welfare programs;

• Only a little impact assessment study was

so far been conducted.

3

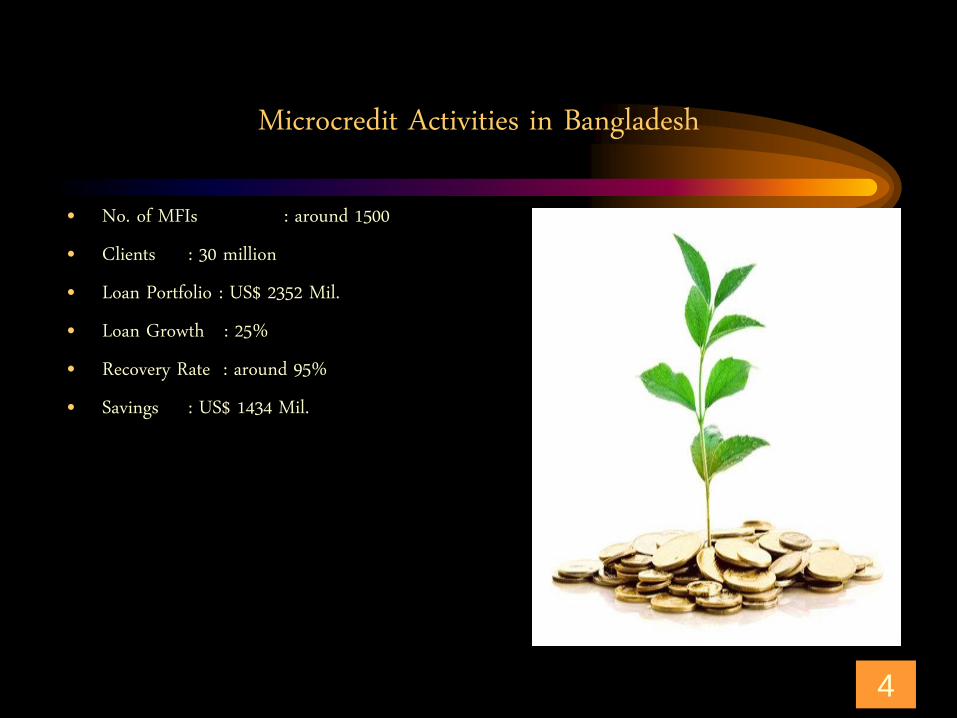

Microcredit Activities in Bangladesh

• No. of MFIs : around 1500• Clients : 30 million• Loan Portfolio : US$ 2352 Mil. • Loan Growth : 25%• Recovery Rate : around 95%• Savings : US$ 1434 Mil.

4

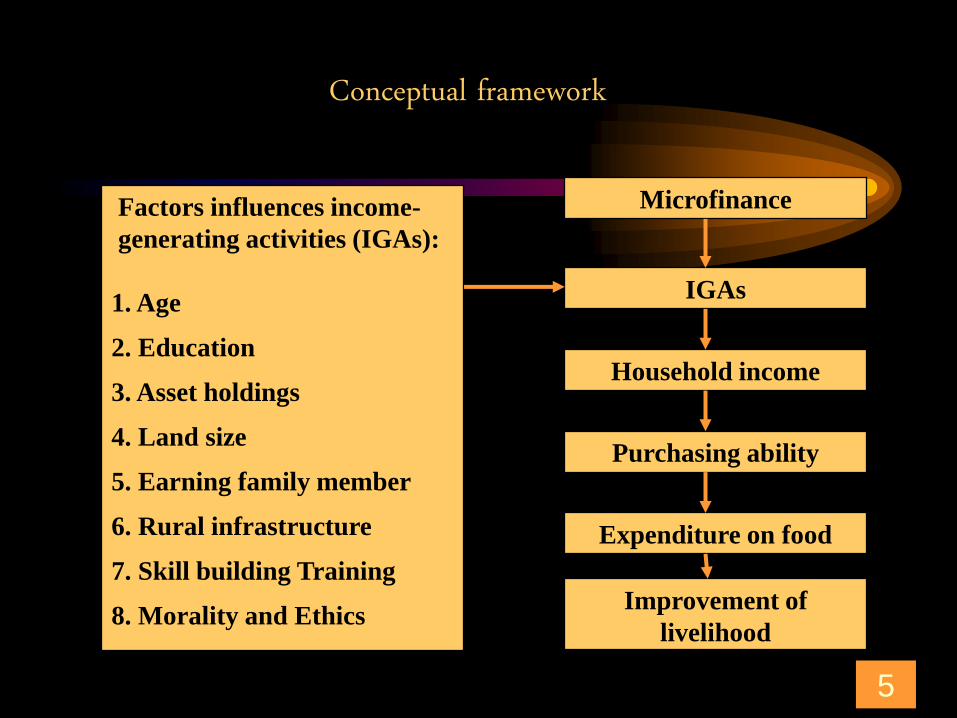

Microfinance

IGAs

Household income

Purchasing ability

Expenditure on food

Improvement of

livelihood

Factors influences income-

generating activities (IGAs):

1. Age

2. Education

3. Asset holdings

4. Land size

5. Earning family member

6. Rural infrastructure

7. Skill building Training

8. Morality and Ethics

Conceptual framework

5

RDS: Special Features

• Shariah based Islamic micro-finance;

• Collateral free investment;

• Finance farming and off-farming

activities;

• Generate Self-employment and

income;

• Provides Welfare, moral and ethical

services;

• Quard facilities for tube-wells,

sanitary latrines;

• Lowest profit rates.

6

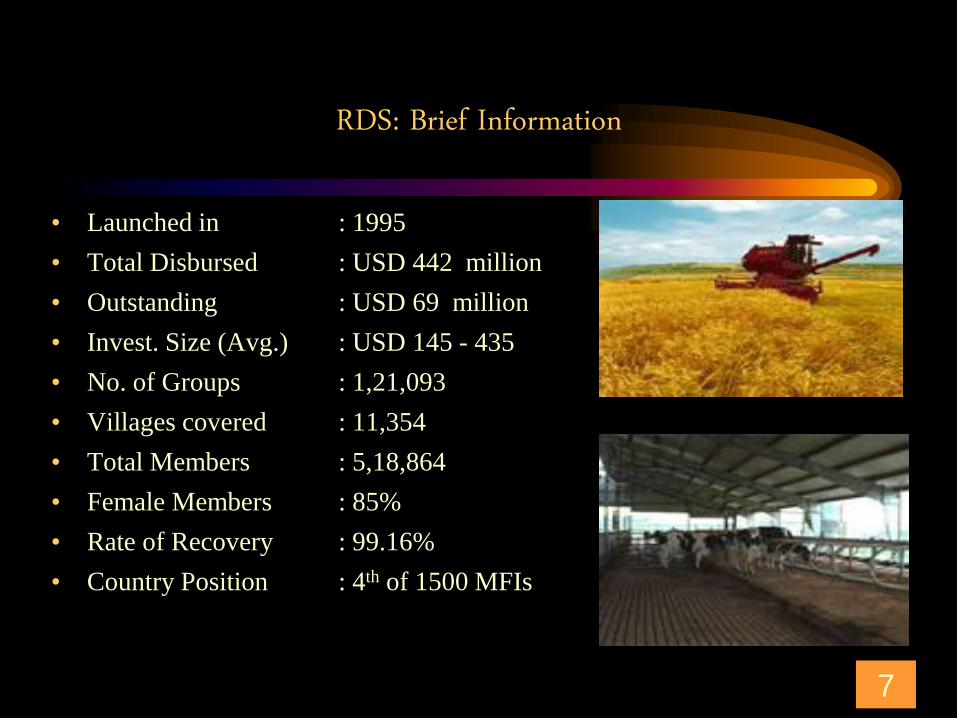

RDS: Brief Information

• Launched in : 1995

• Total Disbursed : USD 442 million

• Outstanding : USD 69 million

• Invest. Size (Avg.) : USD 145 - 435

• No. of Groups : 1,21,093

• Villages covered : 11,354

• Total Members : 5,18,864

• Female Members : 85%

• Rate of Recovery : 99.16%

• Country Position : 4th of 1500 MFIs

7

Target Groups of RDS

• Farmers

• Sharecroppers

• Person engaged in off-farm activities

• Fishermen

• Women and distressed people

8

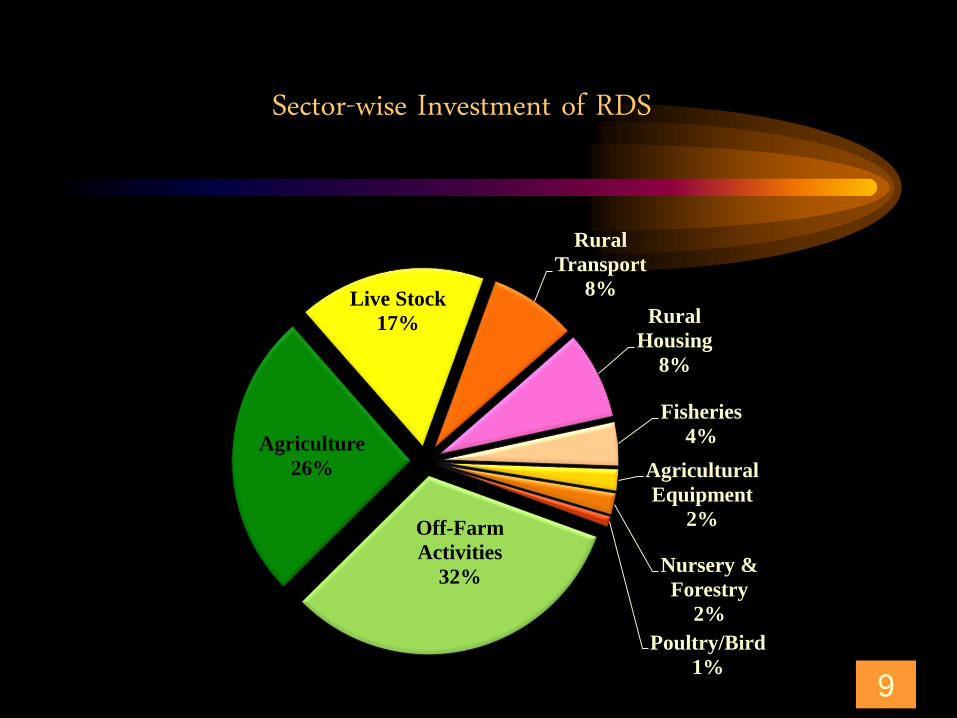

Sector-wise Investment of RDS

Off-Farm

Activities

32%

Agriculture

26%

Live Stock

17%

Rural

Transport

8%

Rural

Housing

8%

Fisheries

4%

Agricultural

Equipment

2%

Nursery &

Forestry

2%

Poultry/Bird

1%9

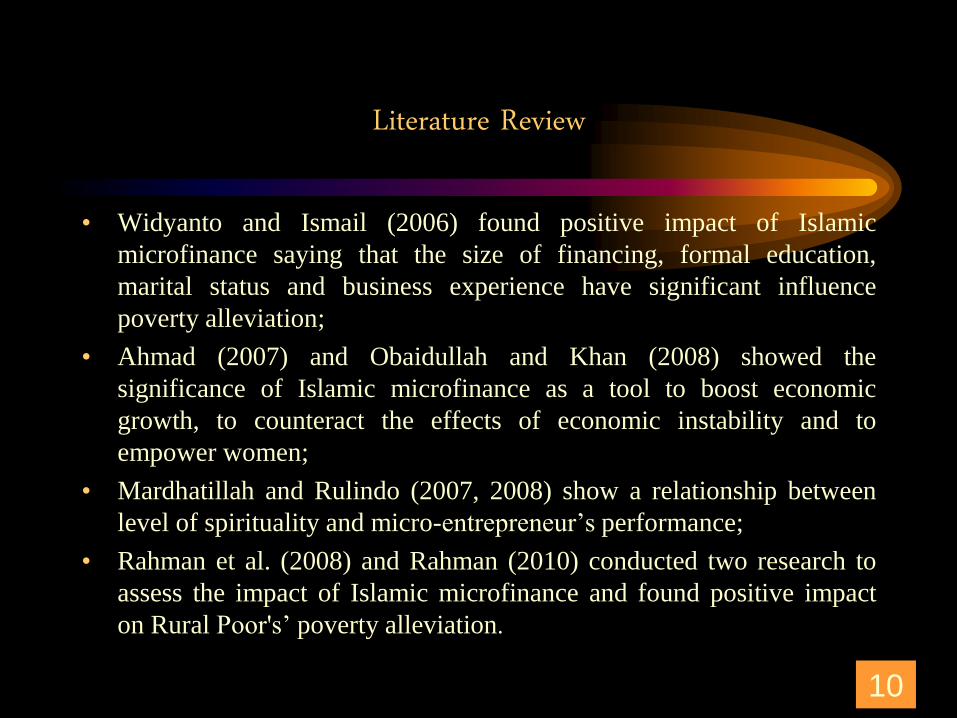

Literature Review

• Widyanto and Ismail (2006) found positive impact of Islamic

microfinance saying that the size of financing, formal education,

marital status and business experience have significant influence

poverty alleviation;

• Ahmad (2007) and Obaidullah and Khan (2008) showed the

significance of Islamic microfinance as a tool to boost economic

growth, to counteract the effects of economic instability and to

empower women;

• Mardhatillah and Rulindo (2007, 2008) show a relationship between

level of spirituality and micro-entrepreneur’s performance;

• Rahman et al. (2008) and Rahman (2010) conducted two research to

assess the impact of Islamic microfinance and found positive impact

on Rural Poor's’ poverty alleviation.

10

Objectives Of The Study

• to assess the impact of Islamic microfinance on their income and

livelihood with especial emphasise on women share to the prosperity;

• to determine the moral and ethical changes of the clients and its impact

of on their income and livelihood;

• to confirm a positive link between Islamic microfinance and socio-

economic well-being of women;

• and also to explore the context in which Islamic microfinance programs

function in Bangladesh and the way their performance can be improved.

11

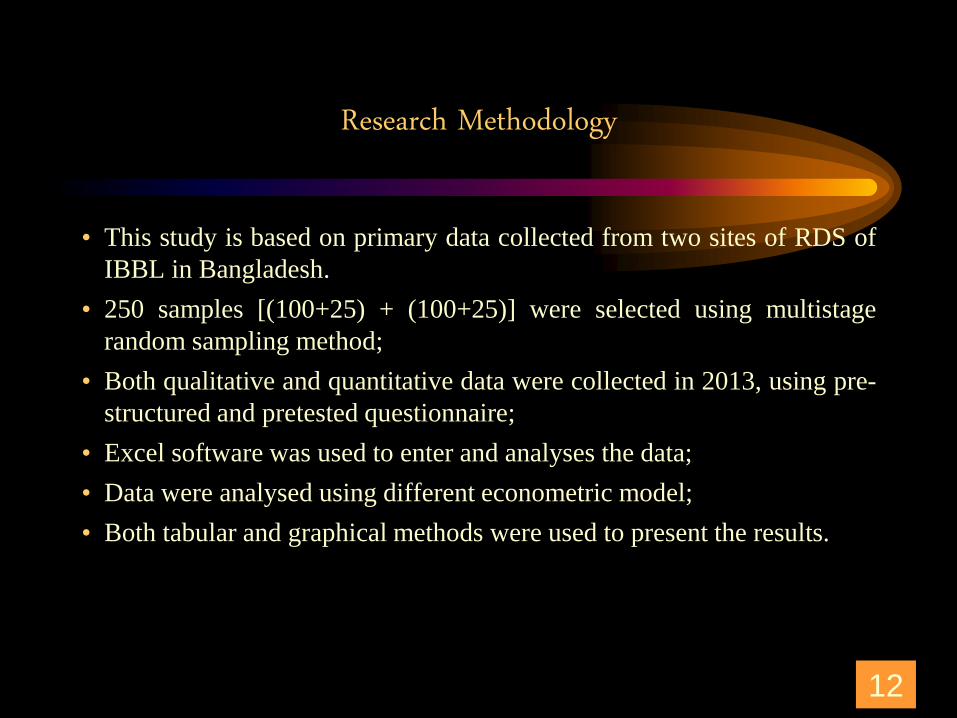

Research Methodology

• This study is based on primary data collected from two sites of RDS of

IBBL in Bangladesh.

• 250 samples [(100+25) + (100+25)] were selected using multistage

random sampling method;

• Both qualitative and quantitative data were collected in 2013, using pre-

structured and pretested questionnaire;

• Excel software was used to enter and analyses the data;

• Data were analysed using different econometric model;

• Both tabular and graphical methods were used to present the results.

12

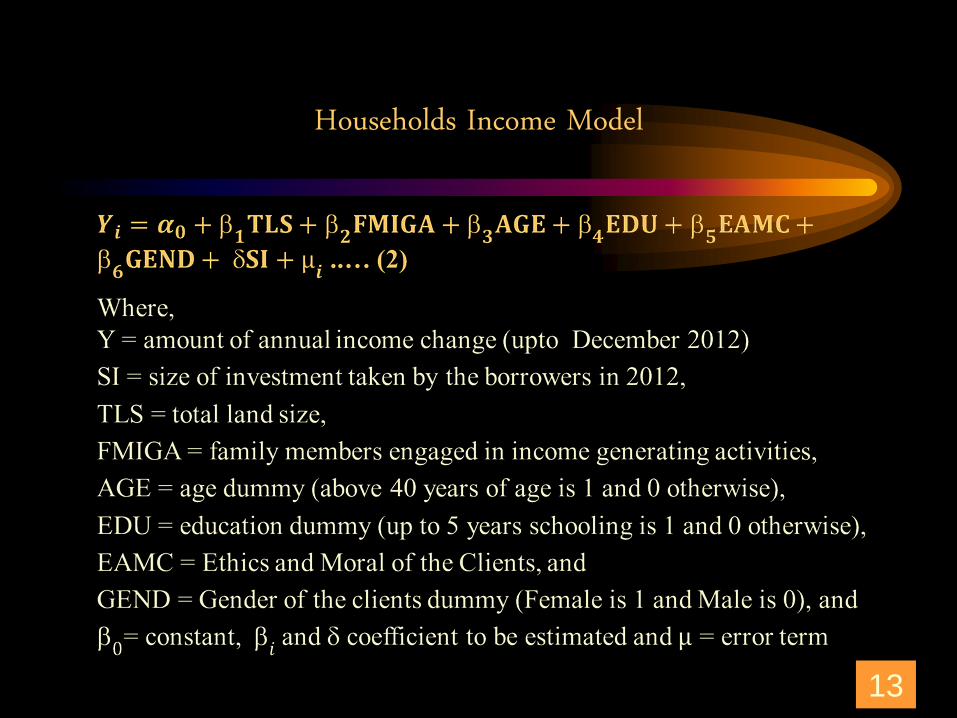

Households Income Model

13

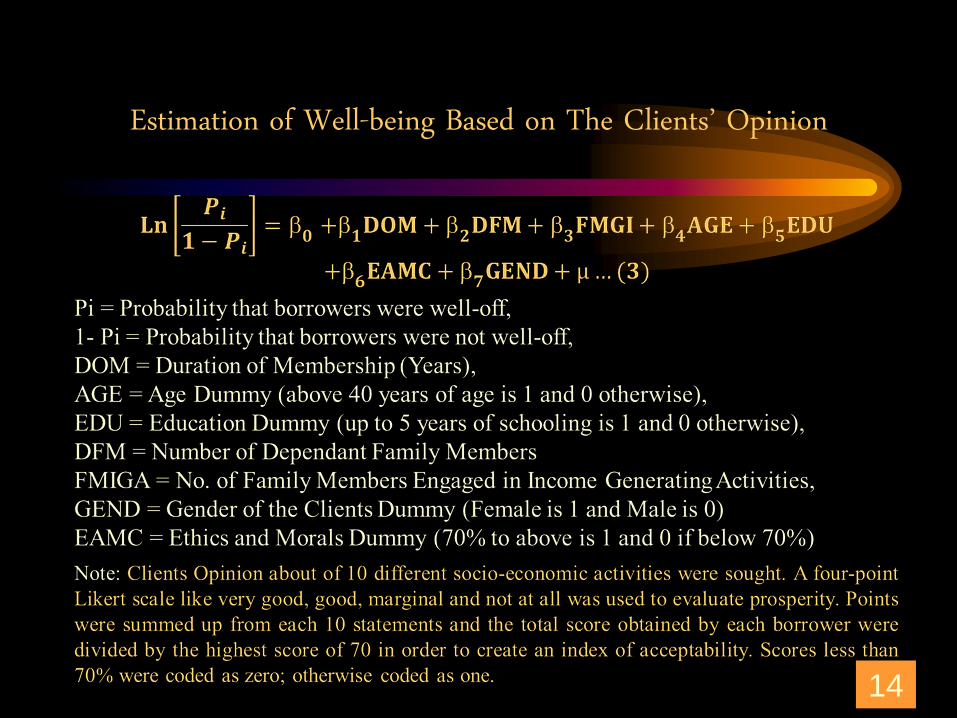

Estimation of Well-being Based on The Clients’ Opinion

14

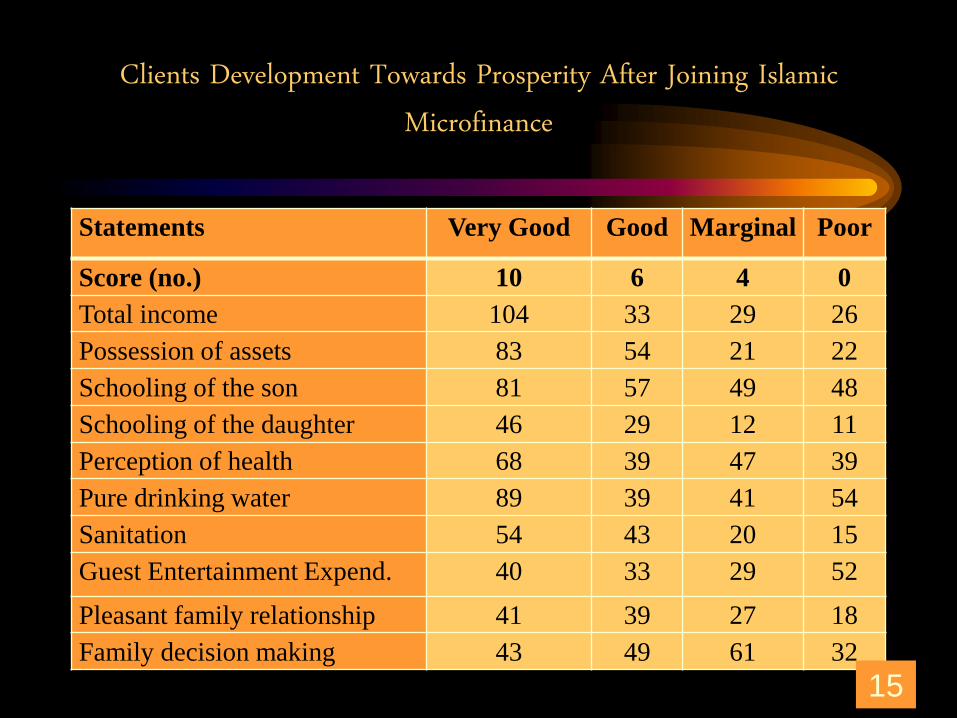

Clients Development Towards Prosperity After Joining Islamic Microfinance

Statements Very Good Good Marginal Poor

Score (no.) 10 6 4 0

Total income 104 33 29 26

Possession of assets 83 54 21 22

Schooling of the son 81 57 49 48

Schooling of the daughter 46 29 12 11

Perception of health 68 39 47 39

Pure drinking water 89 39 41 54

Sanitation 54 43 20 15

Guest Entertainment Expend. 40 33 29 52

Pleasant family relationship 41 39 27 18

Family decision making 43 49 61 32

15

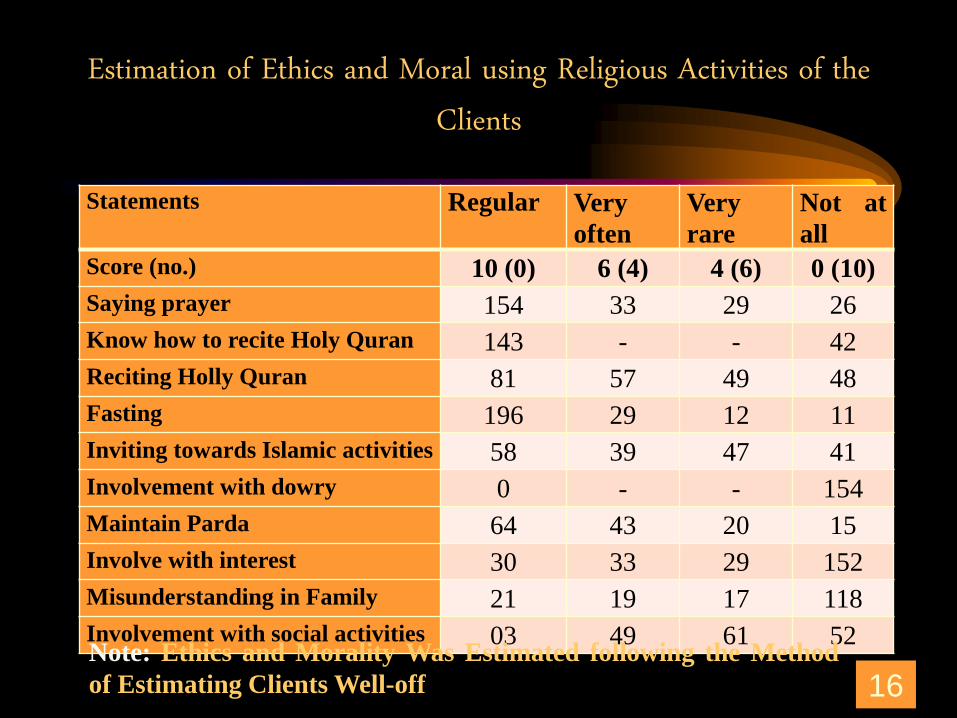

Estimation of Ethics and Moral using Religious Activities of the Clients

Statements Regular Very

often

Very

rare

Not at

all

Score (no.) 10 (0) 6 (4) 4 (6) 0 (10)

Saying prayer 154 33 29 26

Know how to recite Holy Quran 143 - - 42

Reciting Holly Quran 81 57 49 48

Fasting 196 29 12 11

Inviting towards Islamic activities 58 39 47 41

Involvement with dowry 0 - - 154

Maintain Parda 64 43 20 15

Involve with interest 30 33 29 152

Misunderstanding in Family 21 19 17 118

Involvement with social activities 03 49 61 52

16Note: Ethics and Morality Was Estimated following the Method

of Estimating Clients Well-off

Results and Discussions

17

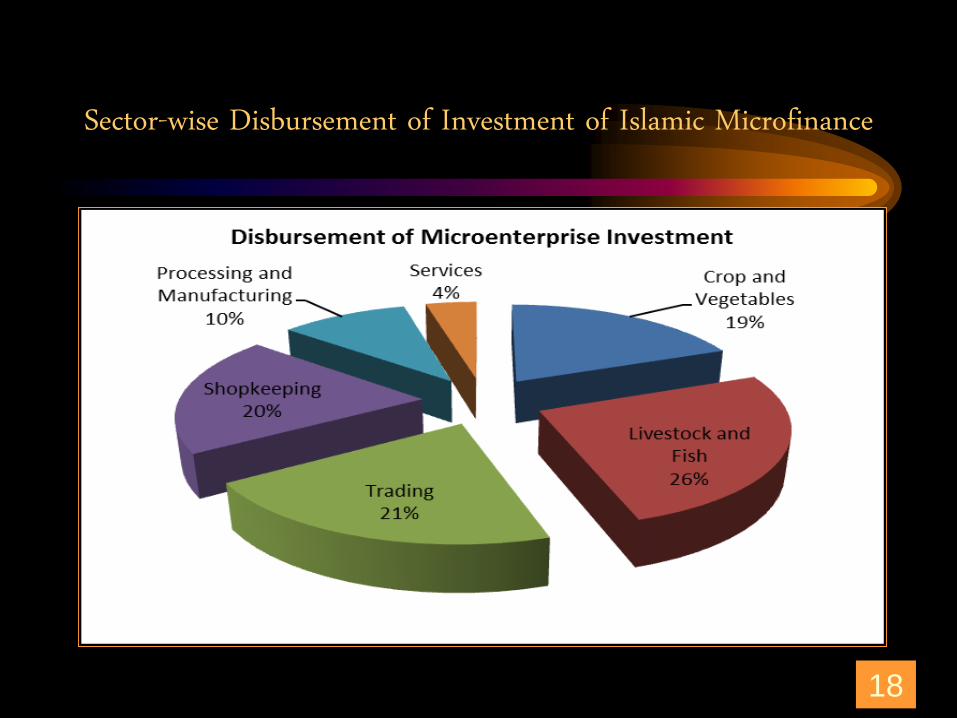

Sector-wise Disbursement of Investment of Islamic Microfinance

18

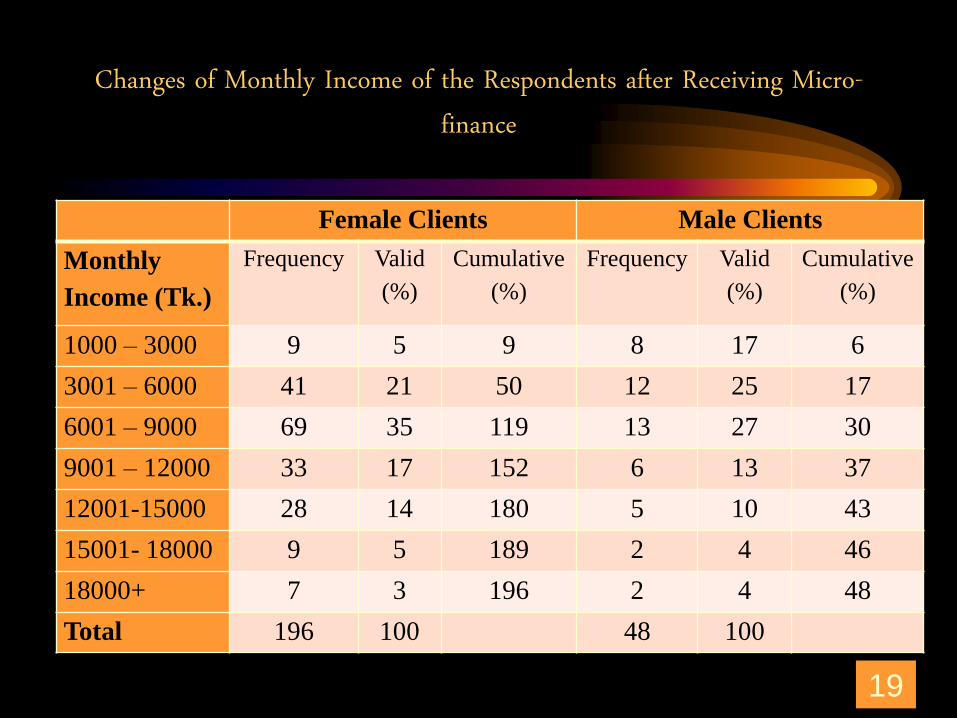

Changes of Monthly Income of the Respondents after Receiving Micro-finance

Female Clients Male Clients

Monthly

Income (Tk.)

Frequency Valid

(%)

Cumulative

(%)

Frequency Valid

(%)

Cumulative

(%)

1000 – 3000 9 5 9 8 17 6

3001 – 6000 41 21 50 12 25 17

6001 – 9000 69 35 119 13 27 30

9001 – 12000 33 17 152 6 13 37

12001-15000 28 14 180 5 10 43

15001- 18000 9 5 189 2 4 46

18000+ 7 3 196 2 4 48

Total 196 100 48 100

19

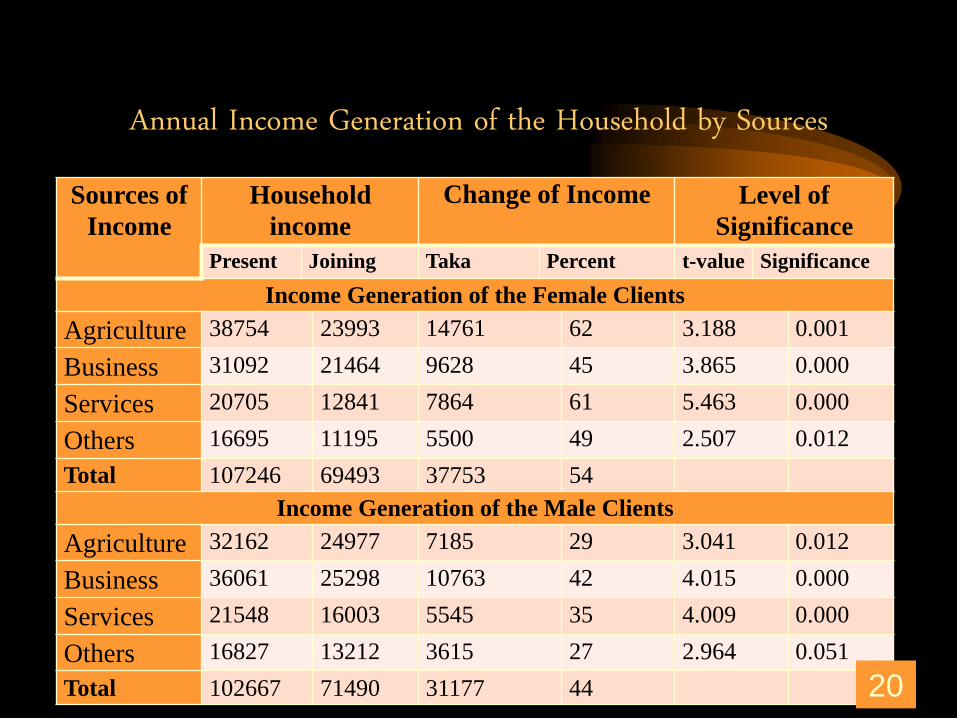

Annual Income Generation of the Household by Sources

Sources of

Income

Household

income

Change of Income Level of

Significance

Present Joining Taka Percent t-value Significance

Income Generation of the Female Clients

Agriculture 38754 23993 14761 62 3.188 0.001

Business 31092 21464 9628 45 3.865 0.000

Services 20705 12841 7864 61 5.463 0.000

Others 16695 11195 5500 49 2.507 0.012

Total 107246 69493 37753 54

Income Generation of the Male Clients

Agriculture 32162 24977 7185 29 3.041 0.012

Business 36061 25298 10763 42 4.015 0.000

Services 21548 16003 5545 35 4.009 0.000

Others 16827 13212 3615 27 2.964 0.051

Total 102667 71490 31177 44 20

OLS Results of the Household Income Model

Variables Coefficient t-value Sig.

Constant 2.789 21.314 0.000**

Log of Investment taken in December 2012 1.210 2.301 0.020**

Log of total land size 0.221 0.528 0.693

Log Number of earning family members 1.110 2.010 0.028**

Borrower’s age dummy (above 40 years 0.332 1.616 0.069

Education dummy (up to 5 years schooling

is 1 and 0 otherwise)

0.210 0.7283 0.470

Ethics and Moral (Dummy) 0.110 2.817 0.045*

Gender Dummy (Female is 1 and Male 0) 0.0215 2.794 0.039*

R-squared: 0.712

21

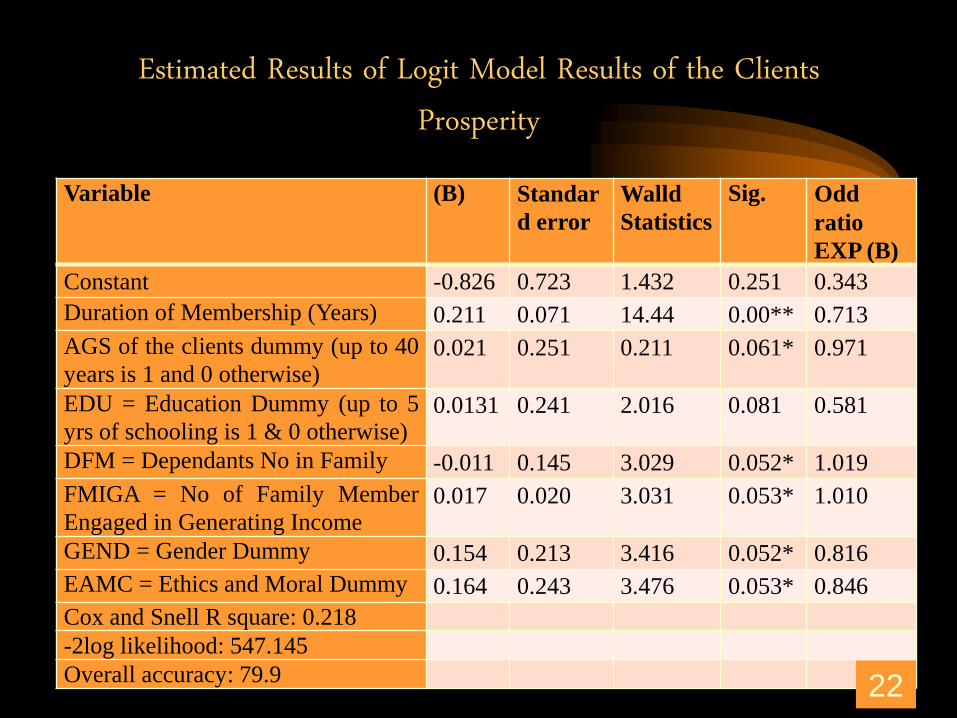

Estimated Results of Logit Model Results of the Clients Prosperity

Variable (B) Standar

d error

Walld

Statistics

Sig. Odd

ratio

EXP (B)

Constant -0.826 0.723 1.432 0.251 0.343

Duration of Membership (Years) 0.211 0.071 14.44 0.00** 0.713

AGS of the clients dummy (up to 40

years is 1 and 0 otherwise)0.021 0.251 0.211 0.061* 0.971

EDU = Education Dummy (up to 5

yrs of schooling is 1 & 0 otherwise)0.0131 0.241 2.016 0.081 0.581

DFM = Dependants No in Family -0.011 0.145 3.029 0.052* 1.019

FMIGA = No of Family Member

Engaged in Generating Income0.017 0.020 3.031 0.053* 1.010

GEND = Gender Dummy 0.154 0.213 3.416 0.052* 0.816

EAMC = Ethics and Moral Dummy 0.164 0.243 3.476 0.053* 0.846

Cox and Snell R square: 0.218

-2log likelihood: 547.145

Overall accuracy: 79.9 22

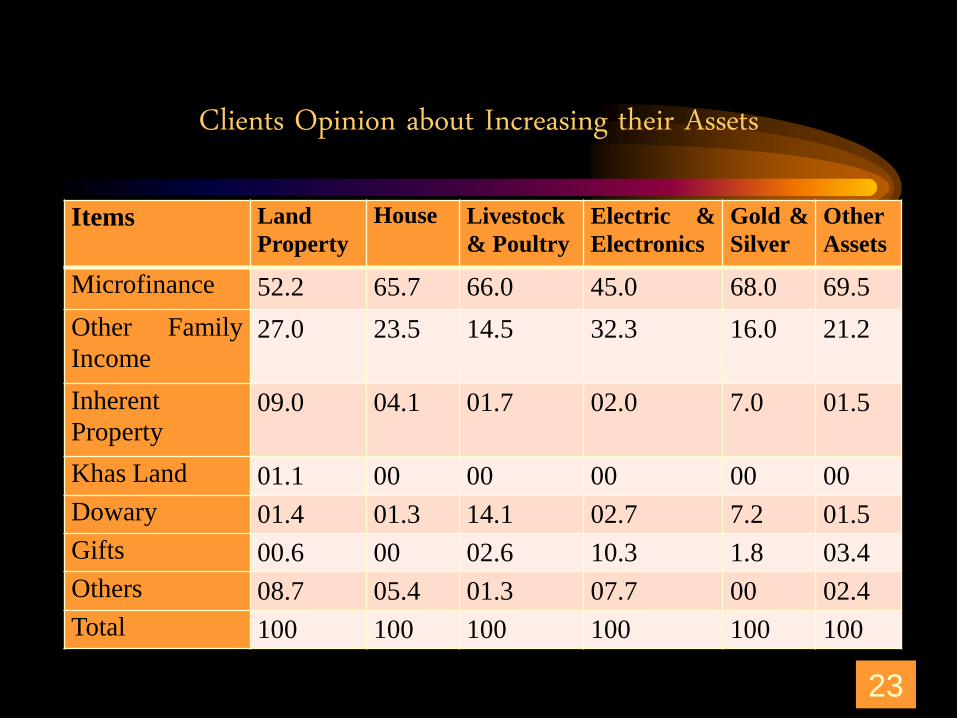

Clients Opinion about Increasing their Assets

Items Land

Property

House Livestock

& Poultry

Electric &

Electronics

Gold &

Silver

Other

Assets

Microfinance 52.2 65.7 66.0 45.0 68.0 69.5

Other Family

Income27.0 23.5 14.5 32.3 16.0 21.2

Inherent

Property09.0 04.1 01.7 02.0 7.0 01.5

Khas Land 01.1 00 00 00 00 00

Dowary 01.4 01.3 14.1 02.7 7.2 01.5

Gifts 00.6 00 02.6 10.3 1.8 03.4

Others 08.7 05.4 01.3 07.7 00 02.4

Total 100 100 100 100 100 100

23

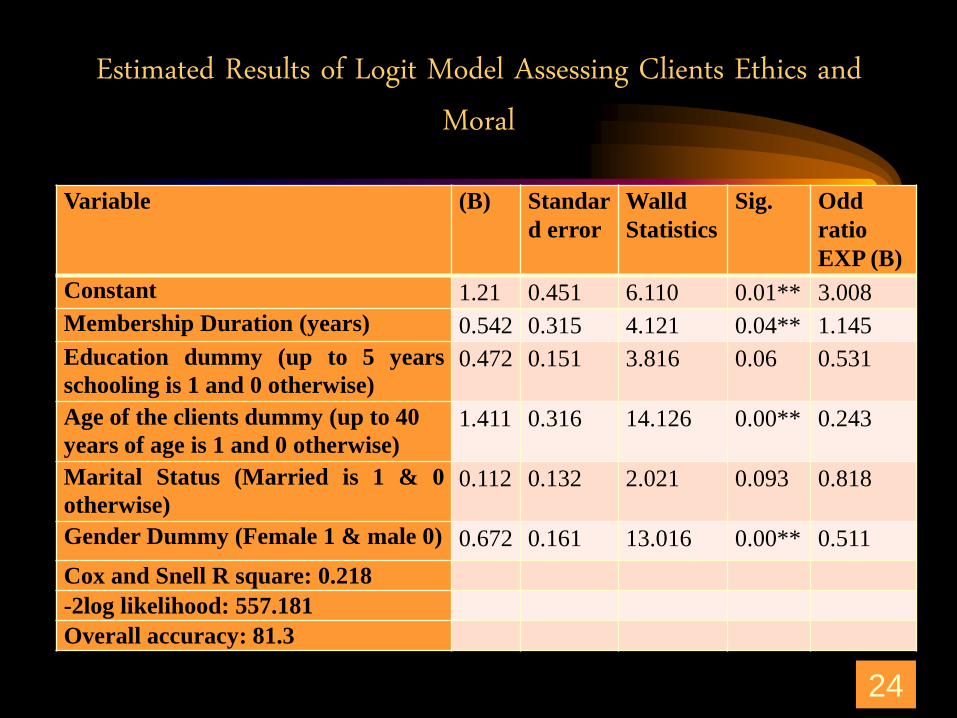

Estimated Results of Logit Model Assessing Clients Ethics and Moral

Variable (B) Standar

d error

Walld

Statistics

Sig. Odd

ratio

EXP (B)

Constant 1.21 0.451 6.110 0.01** 3.008

Membership Duration (years) 0.542 0.315 4.121 0.04** 1.145

Education dummy (up to 5 years

schooling is 1 and 0 otherwise)0.472 0.151 3.816 0.06 0.531

Age of the clients dummy (up to 40

years of age is 1 and 0 otherwise)1.411 0.316 14.126 0.00** 0.243

Marital Status (Married is 1 & 0

otherwise)0.112 0.132 2.021 0.093 0.818

Gender Dummy (Female 1 & male 0) 0.672 0.161 13.016 0.00** 0.511

Cox and Snell R square: 0.218

-2log likelihood: 557.181

Overall accuracy: 81.3

24

Non-financial Services (Welfare activities)

Ethical Discussion for the Clients Annual Get-together

25

Non-financial Services (Welfare activities)

Pure Drinking Water Program Relief Distribution Program

26

Non-financial Services (Welfare activities)

Scholarship Award Program Plant Distribution Program

27

Non-Financial Services (Welfare activities)

RDS Operating School RDS Facilitated Health Camp

28

IDB – RDS Partnership

IDB has chosen IBBL as

strategic partner for its

proposed micro-investment

program in Bangladesh.

29

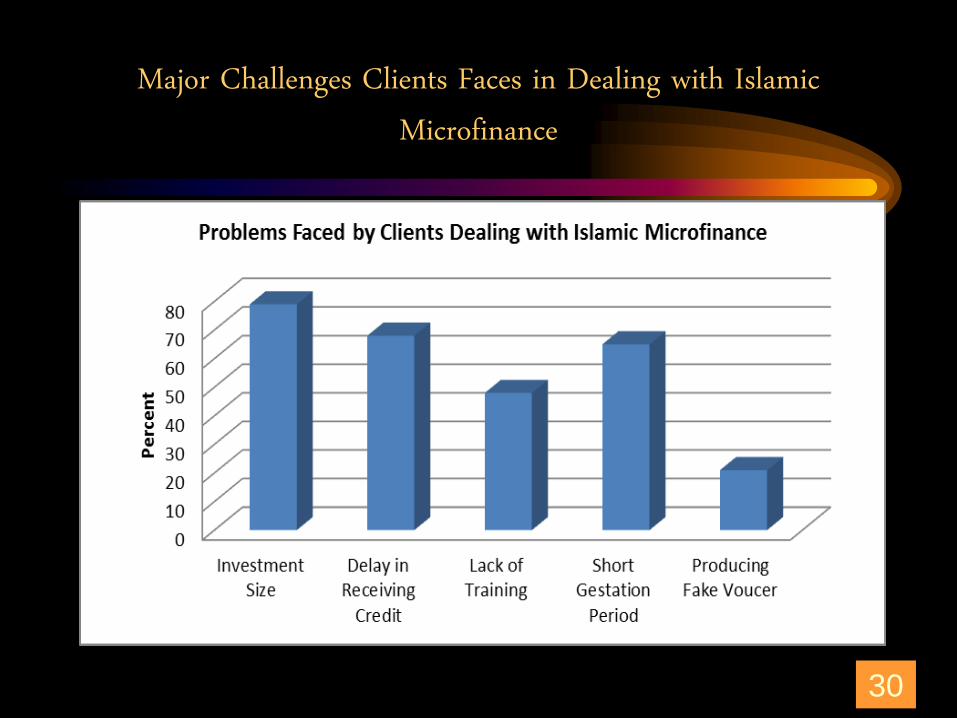

Major Challenges Clients Faces in Dealing with Islamic Microfinance

3030

Future Plan of RDS

Expanding activities to all the

86,000 villages of the country;

Addressing the ultra poor by

developing Quard Fund;

Extensive investment in SME

sector in rural areas for Job

creation;

Financing in bio-gas and solar

panel in the rural house-holds;

Establishing primary schools;

31

Future Plan Of RDS

• Attaining 100% coverage of pure

drinking water and sanitation in

its project areas;

• Ensuring health safety-net of

beneficiaries;

• Extending massive plantation

especially in the coastal areas;

• Alleviate poverty from the

country.

32

Conclusion

• Nearly 50% populations in Bangladesh are women had no income generating

activities and also had no confidence to contribute in their family decision

making.

• Islamic microfinance has been used, to combat poverty and enhance the social

and economic prosperity;

• Findings show that the program has increased women’s income and assets,

which played a very important role in enhancing women’s economic

independence and sense of self-confidence.

• It also helped in breaking the cycle of poverty they live in and allowed them to

have more control over their lives and economic decisions.

• It has enhanced their security giving them access to assets and rights and

augmented their self-respect providing them choice and independence.

33

Conclusion (Cont.)

• It has enabled the poor women to undertake diversified economic activities

which generate flow of stable income round the year and thus has strengthened

survival strategy of the poor women.

• With microinvestment, the poor households now own assets, which can use to

meet contingencies without having to sacrifice their independence, security and

peace of mind by getting into debt.

• It has also empowered the beneficiaries by raising their social consciousness

and importance in family decision making and has also increased their mobility.

• The most important result is the link between receiving an Islamic microfinance

investment and the increase in schooling of the recipients’ children education,

health hygenity and pure drinking water sanitation conscious.

• It can be concluded from the study that Islamic microinvestment program has

benefited the clients in more than one way and women clients were more

benefitted than men.

34

Recommendations

• Some of the clients spent their investment in non-productive sector like, house

repairing, children’s marriage ceremony and furniture purchase etc. So, proper

monitoring and supervision should be made to develop their morals and ethics

so that they use their money in income generating activities;

• Studied RDS touches people having minimum 0.50 acres of land and also has

the working capacity but do not touch the ultra-poor. To alleviate ultra-poor’s

poverty, an integrated approach including zakat and awqaf would be needed.

• Government efforts to employment generation, infrastructure development and

electricity generation can also contribute alleviating ultra-poor’s’ poverty;

• Illiterate and poor borrowers are not aware of the modern technology so they

depend much on the traditional method of farming resulting in low production,

so needs based entrepreneurship training and services is needed;

35

Recommendations (cont.)

• It was noted in focus group discussion that clients often face problems

in marketing products. RDS can play a role to guide to perform the

marketing functions in organizing groups especially in case of selling

and promoting the products to the target people with fair price;

• Some field supervisors do not properly follow the Islamic investment

mode; which is Shariah violation so, monitoring should be strengthen

to develop their moral and ethics so that they do not violate Shariah.

• Besides, Only Bai-muajjal product is used, which is Shariah violation

prone but, Musharaka has comparatively less chances of Shariah

violation, so Musharaka mode of investment can be practiced.

36

THANK YOU

That is the End