wire transfer & ach origination - epcor.org · wire transfer & ach origination ... receipt...

TRANSCRIPT

Wire Transfer &

ACH Origination

Regional Payments Associations, through their Direct Membership in NACHA, are specially

recognized and licensed providers of ACH education, publications and support. Regional

Payments Associations are directly engaged in the NACHA rulemaking process and Accredited

ACH Professional (AAP) program. NACHA owns the copyright for the NACHA Operating Rules &

Guidelines. The Accredited ACH Professional (AAP) is a service mark of NACHA.

©2015, EPCOR®. All Rights Reserved.

What will you learn?

• Discuss the importance of commercially

reasonable security procedures

• Explain the consequences of not being

compliant with UCC 4A

• Given an ACH origination scenario:• Identify the prerequisite rules required for ACH origination

• Identify appropriate actions necessary for exception processing

while complying with the ACH Rules

After this course, you will be able to:

Wire Transfer Origination

©2015, EPCOR®. All Rights Reserved.

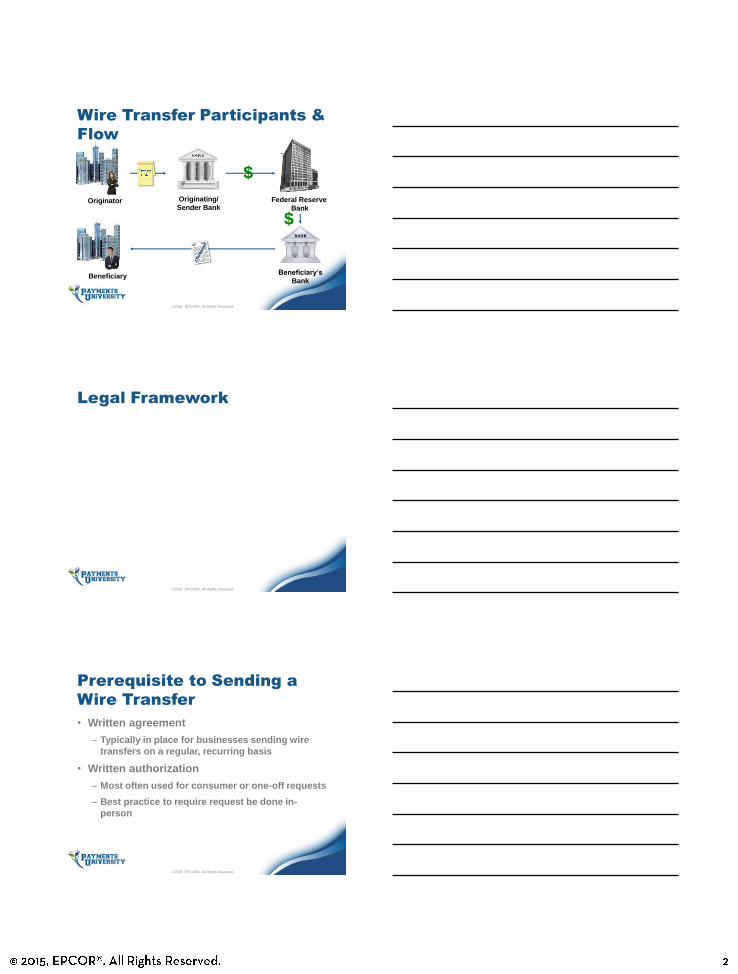

Wire Transfer Participants &

Flow

©2015, EPCOR®. All Rights Reserved.

Originator Originating/

Sender BankFederal Reserve

Bank

Beneficiary’s

BankBeneficiary

$

$

Legal Framework

©2015, EPCOR®. All Rights Reserved.

Prerequisite to Sending a

Wire Transfer

• Written agreement

– Typically in place for businesses sending wire

transfers on a regular, recurring basis

• Written authorization

– Most often used for consumer or one-off requests

– Best practice to require request be done in-

person

©2015, EPCOR®. All Rights Reserved.

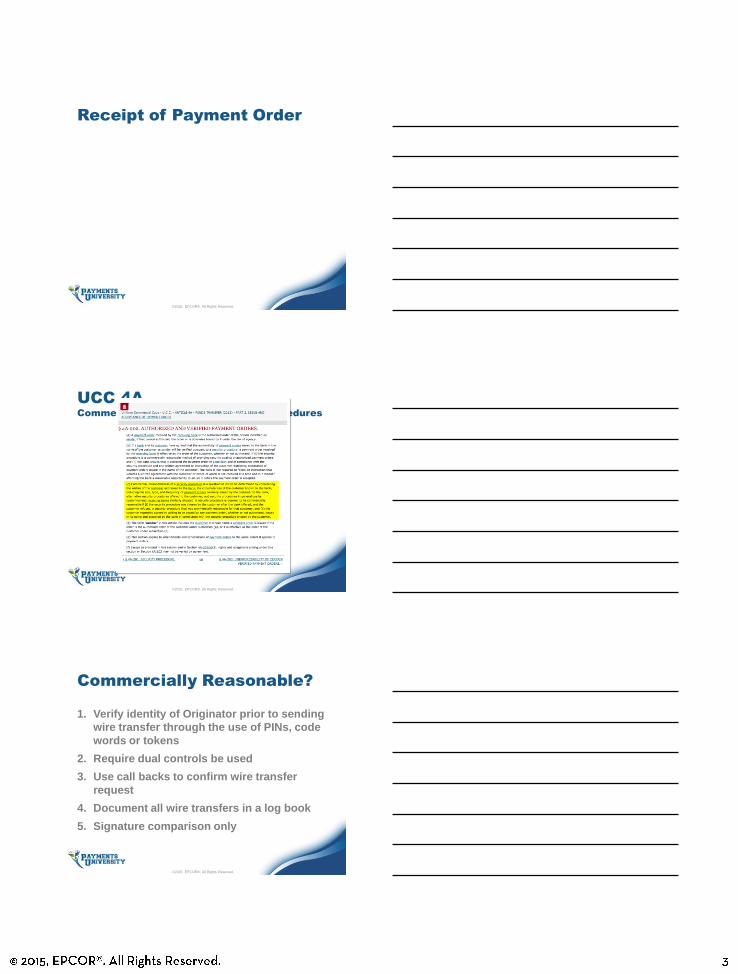

Receipt of Payment Order

©2015, EPCOR®. All Rights Reserved.

UCC 4A

Commercially Reasonable Security Procedures

©2015, EPCOR®. All Rights Reserved.

Commercially Reasonable?

1. Verify identity of Originator prior to sending

wire transfer through the use of PINs, code

words or tokens

2. Require dual controls be used

3. Use call backs to confirm wire transfer

request

4. Document all wire transfers in a log book

5. Signature comparison only

©2015, EPCOR®. All Rights Reserved.

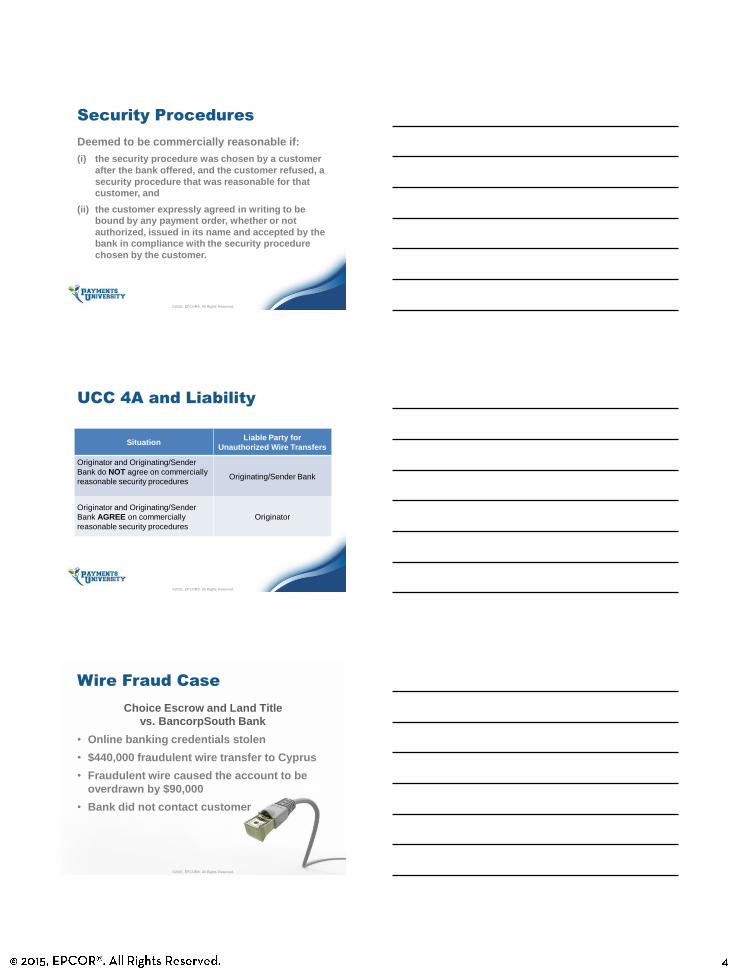

Security Procedures

Deemed to be commercially reasonable if:

(i) the security procedure was chosen by a customer

after the bank offered, and the customer refused, a

security procedure that was reasonable for that

customer, and

(ii) the customer expressly agreed in writing to be

bound by any payment order, whether or not

authorized, issued in its name and accepted by the

bank in compliance with the security procedure

chosen by the customer.

©2015, EPCOR®. All Rights Reserved.

UCC 4A and Liability

SituationLiable Party for

Unauthorized Wire Transfers

Originator and Originating/Sender

Bank do NOT agree on commercially

reasonable security proceduresOriginating/Sender Bank

Originator and Originating/Sender

Bank AGREE on commercially

reasonable security procedures

Originator

©2015, EPCOR®. All Rights Reserved.

Wire Fraud Case

©2015, EPCOR®. All Rights Reserved.

Choice Escrow and Land Title

vs. BancorpSouth Bank

• Online banking credentials stolen

• $440,000 fraudulent wire transfer to Cyprus

• Fraudulent wire caused the account to be

overdrawn by $90,000

• Bank did not contact customer

Wire Fraud Case

©2015, EPCOR®. All Rights Reserved.

Choice Escrow and Land Title

vs. BancorpSouth Bank

“They said they didn’t want to use it because they were concerned

that one of the designated authorized users might be out of the

office when they needed to do a wire.”

~ Defendant's Attorney

Limiting Liability

• Use commercially reasonable security

procedures,

• Ensure both parties agree to the security

procedures to be used, and

• Follow your security policies and

procedures!

©2015, EPCOR®. All Rights Reserved.

ACH Origination

©2015, EPCOR®. All Rights Reserved.

ACH Participants & Flow

©2015, EPCOR®. All Rights Reserved.

Legal Framework

©2015, EPCOR®. All Rights Reserved.

Bank of Lake Superior

• $500 million in assets

• Recently began offering ACH origination

services

– PPD credits

– PPD debits

– CCD credits

– CCD debits

©2015, EPCOR®. All Rights Reserved.

Quality Public Water Supply

District (PWSD)

• Services 4,600 water

customers

• Bill on a monthly basis

• Employ 25 staff

• Payroll is paid bi-monthly

©2015, EPCOR®. All Rights Reserved.

Would they be a good candidate for

ACH origination services?

The Sales Call

• Bank of Lake Superior meets with

Quality PWSD to discuss ACH

origination

• After reviewing the Bank’s ACH

origination service, Quality PWSD

decides to begin with payroll of

its employees

Identify the steps within Section 2.2, page OR 5,

that the Bank must take prior to sending

Quality PWSD’s payroll file.

©2015, EPCOR®. All Rights Reserved.

Prerequisites to Origination

©2015, EPCOR®. All Rights Reserved.

Staff Meeting

• Quality PWSD holds an all-staff meeting

to announce the move to Direct Deposit of payroll

• They also discuss the benefits and answer

questions from staff

©2015, EPCOR®. All Rights Reserved.

Under Section 2.3, page OR 6, is Quality PWSD

required to obtain a written authorization

from each employee before sending his/her payroll?

Authorization Requirements

©2015, EPCOR®. All Rights Reserved.

File Delivery

How might Quality PWSD deliver its payroll file

to the Bank of Lake Superior?

A. Upload to online banking

B. Upload to FTP server

C. Bring a CD or USB drive to the ODFI

D. Bring a paper listing so the Bank can manually

enter for them

©2015, EPCOR®. All Rights Reserved.

Important file be delivered by an authorized user

and by the cutoff times specified

in the Origination Agreement.

ACH Risk

1. What risk(s) are reduced by ensuring the file is delivered by an authorized user?

©2015, EPCOR®. All Rights Reserved.

2. What risk(s) are reduced by setting a

cutoff time?

ODFI Warranties

• Section 2.4, page OR 9

– Entry is properly authorized

– Entry complies with the ACH Rules

– Entry contains the Receiver’s correct

information

– Credit entry is timely

– Debit entry is due and owing

– Banking information is securely

transmitted

©2015, EPCOR®. All Rights Reserved.

Prenotes

• Bank of Lake Superior requires all payroll

Originators to send prenotes prior to

sending a “live” entry

©2015, EPCOR®. All Rights Reserved.

1. Are prenotes required to be sent under the

ACH Rules, Section 2.6, page OR 26?

2. How can the Bank require

prenotes be sent?

Waiting Period for Prenotes

• Subsection 2.6.2, page OR 26

– Quality PWSD may initiate the live entry as soon

as the third banking day following the Settlement

Date of the prenote, provided it has not received a

return or Notification of Change (NOC)

©2015, EPCOR®. All Rights Reserved.

Settlement

Date

Third

Banking Day

Notification of Change

(NOC)

• Joe Drinkwater, an employee of

Quality PWSD, provided

erroneous account information

in his authorization

©2015, EPCOR®. All Rights Reserved.

• Credit Union of Wealth

has sent an NOC with

Joe’s correct account

number

NOC

1. Describe what the Bank is required to do

upon receiving an NOC.

2. Describe Quality PWSD’s responsibilities

related to receipt of an NOC.

©2015, EPCOR®. All Rights Reserved.

Subsection 2.11.1, page OR 29

NOC Responsibilities:

Bank of Lake Superior

©2015, EPCOR®. All Rights Reserved.

NOC Responsibilities:

Quality PWSD

©2015, EPCOR®. All Rights Reserved.

Returns

• Joe closes his account at

Credit Union of Wealth

©2015, EPCOR®. All Rights Reserved.

• Joe opens an account at Nuttin’

Left Bank, but fails to notify Human

Resources of the change

• Credit Union of Wealth returns Joe’s payroll as account closed within 2 banking days of the Settlement Date of the payroll

Returns

1. Describe what the Bank is required to

do when it receives a return entry.

2. What must Quality PWSD do to

resolve this issue?

©2015, EPCOR®. All Rights Reserved.

Subsection 2.12.1, page OR 29

Return Responsibilities:

Bank of Lake Superior

©2015, EPCOR®. All Rights Reserved.

Return Responsiblities:

Quality PWSD

©2015, EPCOR®. All Rights Reserved.

©2015, EPCOR®. All Rights Reserved.