wilary winn university breakout session #2 mortgage ... winn university breakout session #2 mortgage...

TRANSCRIPT

Wilary Winn UniversityBreakout Session #2

Mortgage Servicing RightsEric Nokken, Director

September 23, 2014

Mortgage Servicing Rights

Topics Covered• Release versus retain

• Valuation of retained servicing

• Accounting and regulatory reporting for retained servicing

Mortgage Servicing Rights

2

Mortgage Servicing Rights

3

Once an institution has committed to making residential mortgage

loans it has two choices:

• Hold the loans

• Sell the loans

Mortgage Servicing Rights

4

Benefits of holding the loan• Relatively low credit risk

• Higher yield than MBS

• GSE loans are fungible

• GSE loan is a Qualified Mortgage

Mortgage Servicing Rights

5

Interest rate risk for residential mortgages

• Potential for a gap or mismatch between assets and liabilities because of the longer term and market volatility

• Difficult to estimate prepayment speeds and understand the optional component in residential mortgages

Mortgage Servicing Rights

6

Option risk

• High coupon residential mortgage loans have more call risk

• Low coupon mortgage loans have more extension risk

Regulatory Views of the Banking Regulators

Inter-Agency Advisory Mortgage Banking February 2003

• Need to comply with rules on interest rate risk• Need to consider how mortgage banking affects

strategic, business and asset/liability plans• Establish asset/capital limits for mortgage banking

Mortgage Servicing Rights

Page 23

30

Mortgage Servicing Rights

7

Sales have benefits and risks• Benefits

◦ Reduce interest rate and credit risks◦ Generate potential gains

• Risks◦ Reinvestment risk◦ Generate potential losses if the loan sales are not

hedged or loans have been priced incorrectly◦ Potential loss of customer relationships if the loan is

sold servicing released

Servicing Released

• Receive servicing released premium at time of origination

• Transfer of customer information to potential competitor

Mortgage Servicing RightsMortgage Servicing Rights

8

Retained Mortgage Servicing Rights (MSRs)

• MSRs are a modified interest only strip• Many types of underlying loans• Value varies significantly by type of MSR

Mortgage Servicing Rights

9

Major Valuation Components

• Loan amount• Servicing fee percentage – varies by investor and

type of loan• Ancillary income• Expected loan life – prepayment and loan term• Discount rate• Costs to service – market costs• Delinquency rate and foreclosure losses – recourse

versus non-recourse

Mortgage Servicing Rights

10

Valuation Components Detail

• Servicing fees are earned monthly based on remaining principal balance.

• Servicing costs should be calculated in dollars per loan.

• Ancillary income includes late fees, insurance income and other fees earned.

• Float and escrows (impounds) add value.

Mortgage Servicing Rights

11

Other Key Valuation Variables

• Production channel – retail versus wholesale• Current economic conditions in the region• Recent changes in home prices

Mortgage Servicing Rights

12

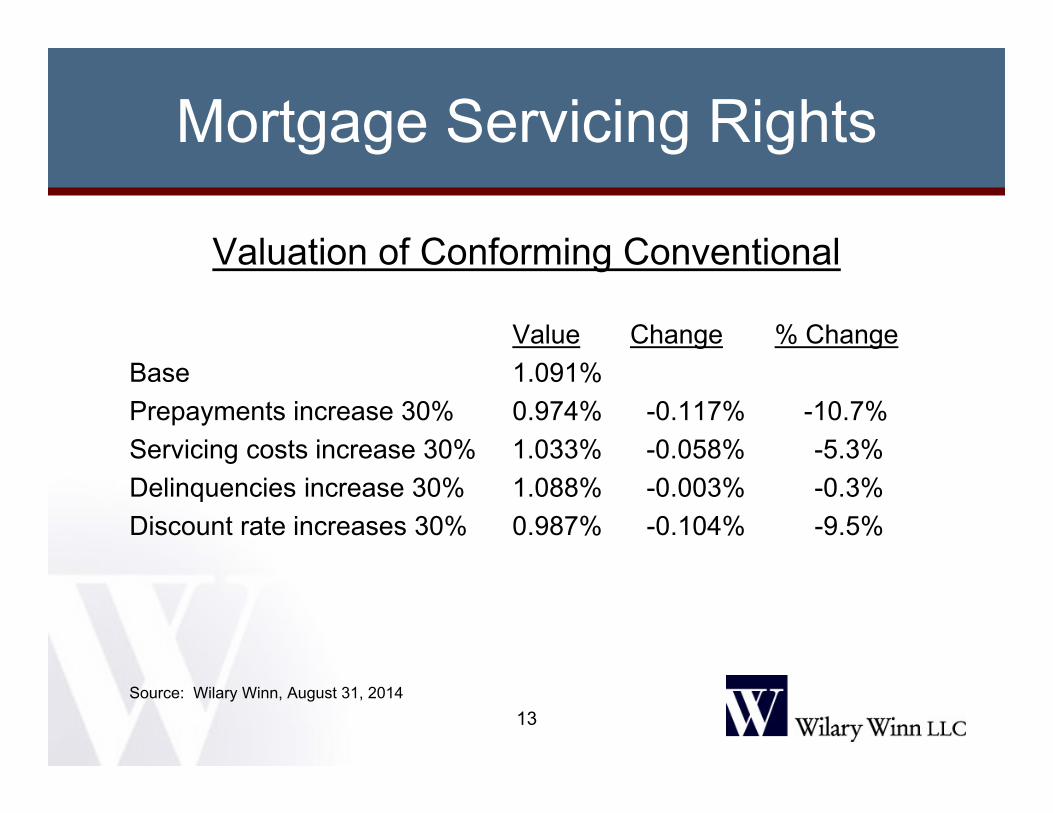

Valuation of Conforming Conventional

Value Change % ChangeBase 1.091%Prepayments increase 30% 0.974% -0.117% -10.7%Servicing costs increase 30% 1.033% -0.058% -5.3%Delinquencies increase 30% 1.088% -0.003% -0.3%Discount rate increases 30% 0.987% -0.104% -9.5%

Source: Wilary Winn, August 31, 2014

Mortgage Servicing Rights

13

Mortgage Servicing Rights

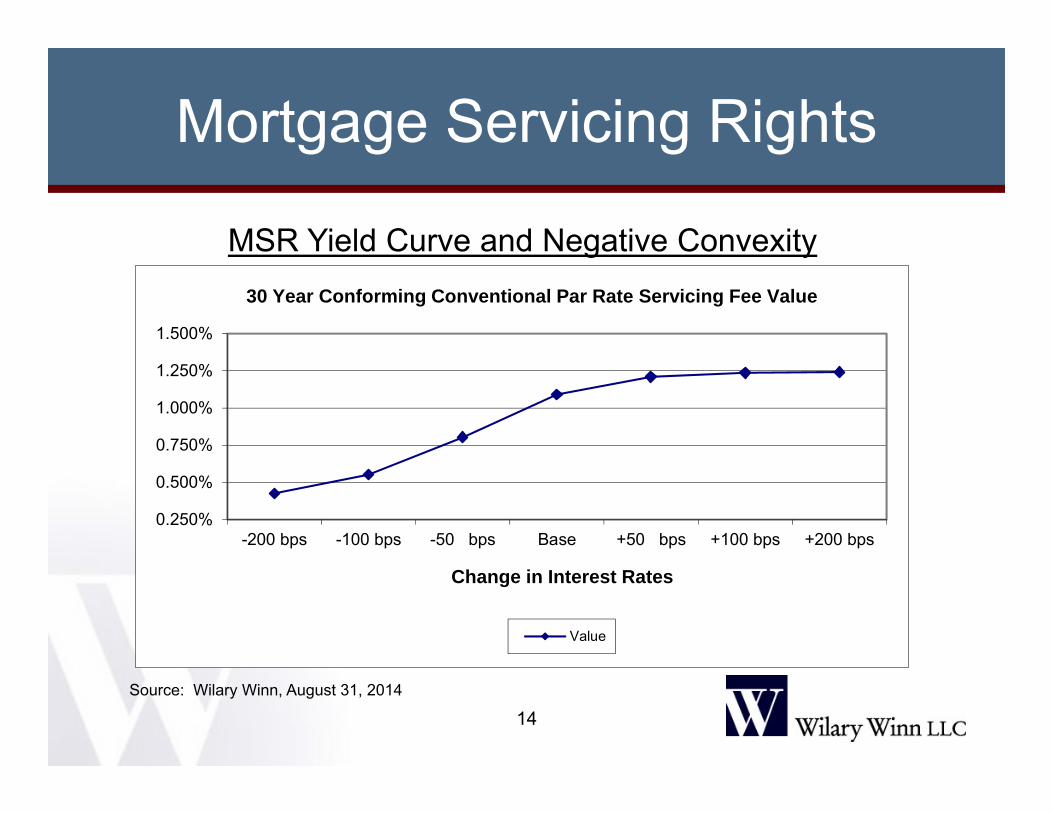

MSR Yield Curve and Negative Convexity

Source: Wilary Winn, August 31, 2014

14

0.250%

0.500%

0.750%

1.000%

1.250%

1.500%

-200 bps -100 bps -50 bps Base +50 bps +100 bps +200 bps

Change in Interest Rates

30 Year Conforming Conventional Par Rate Servicing Fee Value

Value

Mortgage Servicing Rights

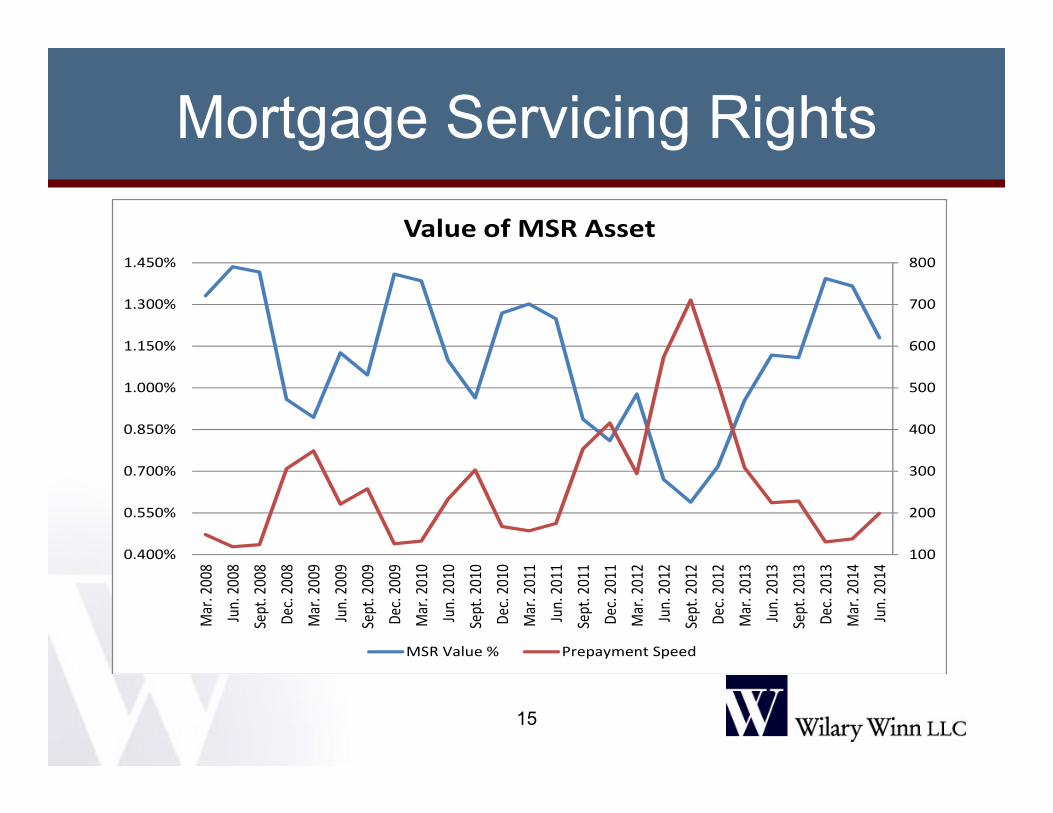

15

100

200

300

400

500

600

700

800

0.400%

0.550%

0.700%

0.850%

1.000%

1.150%

1.300%

1.450%

Mar. 200

8Jun. 20

08Sept. 2008

Dec. 2008

Mar. 200

9Jun. 20

09Sept. 2009

Dec. 2009

Mar. 201

0Jun. 20

10Sept. 2010

Dec. 2010

Mar. 201

1Jun. 20

11Sept. 2011

Dec. 2011

Mar. 201

2Jun. 20

12Sept. 2012

Dec. 2012

Mar. 201

3Jun. 20

13Sept. 2013

Dec. 2013

Mar. 201

4Jun. 20

14

Value of MSR Asset

MSR Value % Prepayment Speed

Managing Run-Off Risk

• The operational / macro hedge• Hedge with positive convexity instruments• Utilize appropriate amortization methodology

Mortgage Servicing Rights

16

Servicing Economics• Smaller servicers can compete with the giant

servicers on cost by keeping it simple – limit the number of investors, use one remittance method, service fixed rate loans only and use existing employees to service the loans.

• Smaller servicers have historically generated less ancillary income per loan than the giant servicers, providing them with an opportunity to increase income and broaden their customer relationships on retained loans.

Mortgage Servicing Rights

17

Potential Strategic Alliances

• Have loans sub-serviced as financial institution builds scale

• Ability to Pay / Qualified Mortgage compliance review• Contract with others to generate ancillary income • Consider outsourcing specialized functions such as

foreclosure – especially given recently released CFPB rules

• Join industry alliances• Hire an expert to assist with hedge

Mortgage Servicing Rights

18

Accounting Implications

Accounting and reporting for MSRs is set forth in FAS ASC 860-50

Mortgage Servicing Rights

19

Existence of Servicing - FAS ASC 860-50-25-1

• A servicing asset or liability arises each time an institution undertakes an obligation to service a financial asset by entering into a servicing contract in connection with –1) a transfer that meets the requirements for true sale or 2) the acquisition or assumption of a servicing obligation not

related to the financial assets of the servicer.

Mortgage Servicing Rights

20

MSR Asset or Liability - FAS ASC 860-50-30

The benefits of the servicing, including the servicing fees, ancillary income, float, etc. must exceed “adequate compensation” in order to have a servicing asset. If not, the servicer has a liability. Adequate compensation includes a profit and is determined by the marketplace. It is based on marketplace costs, not the servicer’s internal costs.

Mortgage Servicing Rights

21

Initial Recording

• Servicing assets and liabilities must be reported separately

• A servicing asset can become a servicing liability over its life and vice versa

Mortgage Servicing Rights

22

Initial Recording

• Record MSR at fair value – quoted price for exact or similar asset would be best – discounted cash flow can be used in the absence of trade information

• Industry believes MSRs are Level 2 or Level 3 assets based on a discounted cash flow model

• Value excess servicing separately - true IO– Creation of the IO does not violate true sale, if part of overall

consideration for the 100% sale of the loan

Mortgage Servicing Rights

23

How to account for the MSR after initial recording?FAS ASC paragraph 860-50-35-1 allows the asset to be measured and reported in one of two ways:

1) Amortization Method2) Fair Value Method

A servicer can select either method, but cannot switch methodologies unless it moves to the Fair Value method at the beginning of the fiscal year before interim financial statements have been released. A servicer cannot go back to the amortization method after it has elected Fair Value.

Mortgage Servicing Rights

24

Amortization MethodAmortize the MSR in proportion and over the period of estimated net servicing income (level yield method) and assess servicing assets for impairment based on fair value at each reporting date.

Mortgage Servicing Rights

25

Amortization Methodologies

• Level yield• Sum of the years digits• Straight line with actual write-offs

Mortgage Servicing Rights

26

Impairment

• Impairment is best measured at the loan level and is reported at the predominant risk characteristic stratum

• There is a difference between temporary impairment, which is accounted for through an allowance and permanent impairment, which requires a direct write-off

Mortgage Servicing Rights

27

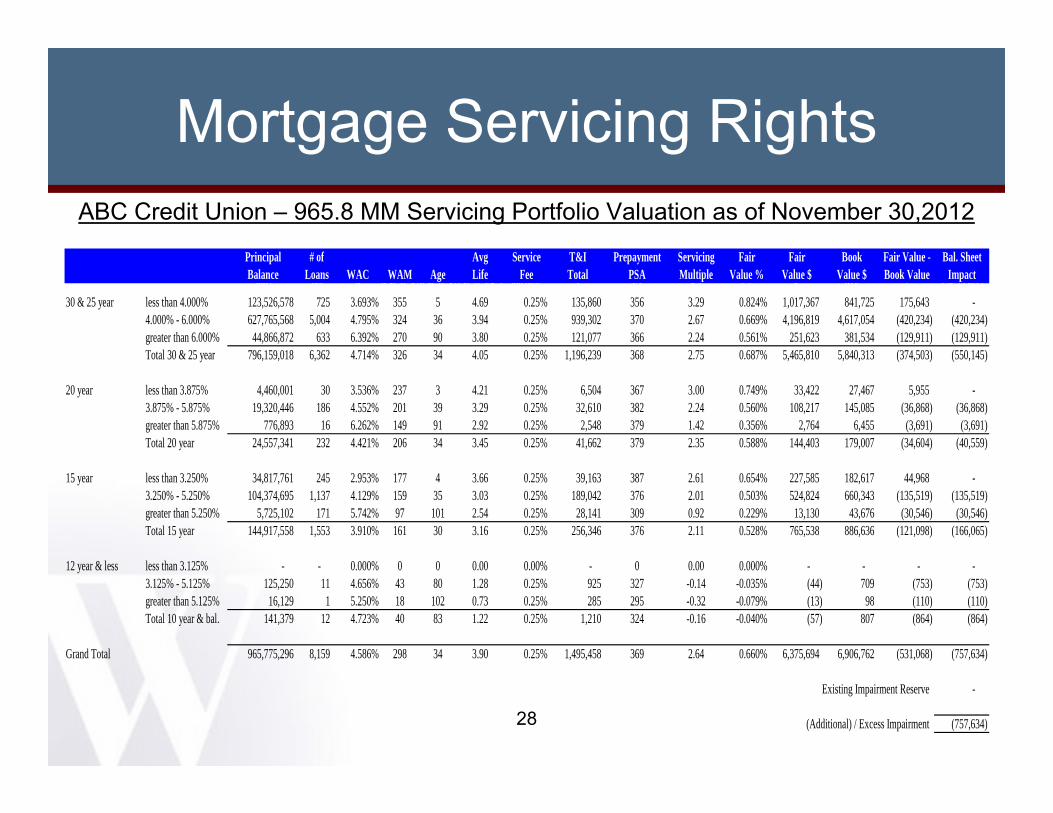

ABC Credit Union – 965.8 MM Servicing Portfolio Valuation as of November 30,2012

Mortgage Servicing Rights

28

Principal # of Avg Service T&I Prepayment Servicing Fair Fair Book Fair Value - Bal. SheetBalance Loans WAC WAM Age Life Fee Total PSA Multiple Value % Value $ Value $ Book Value Impact

2007 360 0 30 & 25 Yr0 & 25 Yr0 & 25 Yr.-F 200.00% 1 F3 K3 5.5 6 914 1 376.72203730 & 25 year less than 4.000% 123,526,578 725 3.693% 355 5 4.69 0.25% 135,860 356 3.29 0.824% 1,017,367 841,725 175,643 -

4.000% - 6.000% 627,765,568 5,004 4.795% 324 36 3.94 0.25% 939,302 370 2.67 0.669% 4,196,819 4,617,054 (420,234) (420,234) greater than 6.000% 44,866,872 633 6.392% 270 90 3.80 0.25% 121,077 366 2.24 0.561% 251,623 381,534 (129,911) (129,911) Total 30 & 25 year 796,159,018 6,362 4.714% 326 34 4.05 0.25% 1,196,239 368 2.75 0.687% 5,465,810 5,840,313 (374,503) (550,145)

20 year less than 3.875% 4,460,001 30 3.536% 237 3 4.21 0.25% 6,504 367 3.00 0.749% 33,422 27,467 5,955 - 3.875% - 5.875% 19,320,446 186 4.552% 201 39 3.29 0.25% 32,610 382 2.24 0.560% 108,217 145,085 (36,868) (36,868) greater than 5.875% 776,893 16 6.262% 149 91 2.92 0.25% 2,548 379 1.42 0.356% 2,764 6,455 (3,691) (3,691) Total 20 year 24,557,341 232 4.421% 206 34 3.45 0.25% 41,662 379 2.35 0.588% 144,403 179,007 (34,604) (40,559)

15 year less than 3.250% 34,817,761 245 2.953% 177 4 3.66 0.25% 39,163 387 2.61 0.654% 227,585 182,617 44,968 - 3.250% - 5.250% 104,374,695 1,137 4.129% 159 35 3.03 0.25% 189,042 376 2.01 0.503% 524,824 660,343 (135,519) (135,519) greater than 5.250% 5,725,102 171 5.742% 97 101 2.54 0.25% 28,141 309 0.92 0.229% 13,130 43,676 (30,546) (30,546) Total 15 year 144,917,558 1,553 3.910% 161 30 3.16 0.25% 256,346 376 2.11 0.528% 765,538 886,636 (121,098) (166,065)

12 year & less less than 3.125% - - 0.000% 0 0 0.00 0.00% - 0 0.00 0.000% - - - - 3.125% - 5.125% 125,250 11 4.656% 43 80 1.28 0.25% 925 327 -0.14 -0.035% (44) 709 (753) (753) greater than 5.125% 16,129 1 5.250% 18 102 0.73 0.25% 285 295 -0.32 -0.079% (13) 98 (110) (110) Total 10 year & bal. 141,379 12 4.723% 40 83 1.22 0.25% 1,210 324 -0.16 -0.040% (57) 807 (864) (864)

Grand Total 965,775,296 8,159 4.586% 298 34 3.90 0.25% 1,495,458 369 2.64 0.660% 6,375,694 6,906,762 (531,068) (757,634)

Existing Impairment Reserve -

(Additional) / Excess Impairment (757,634)

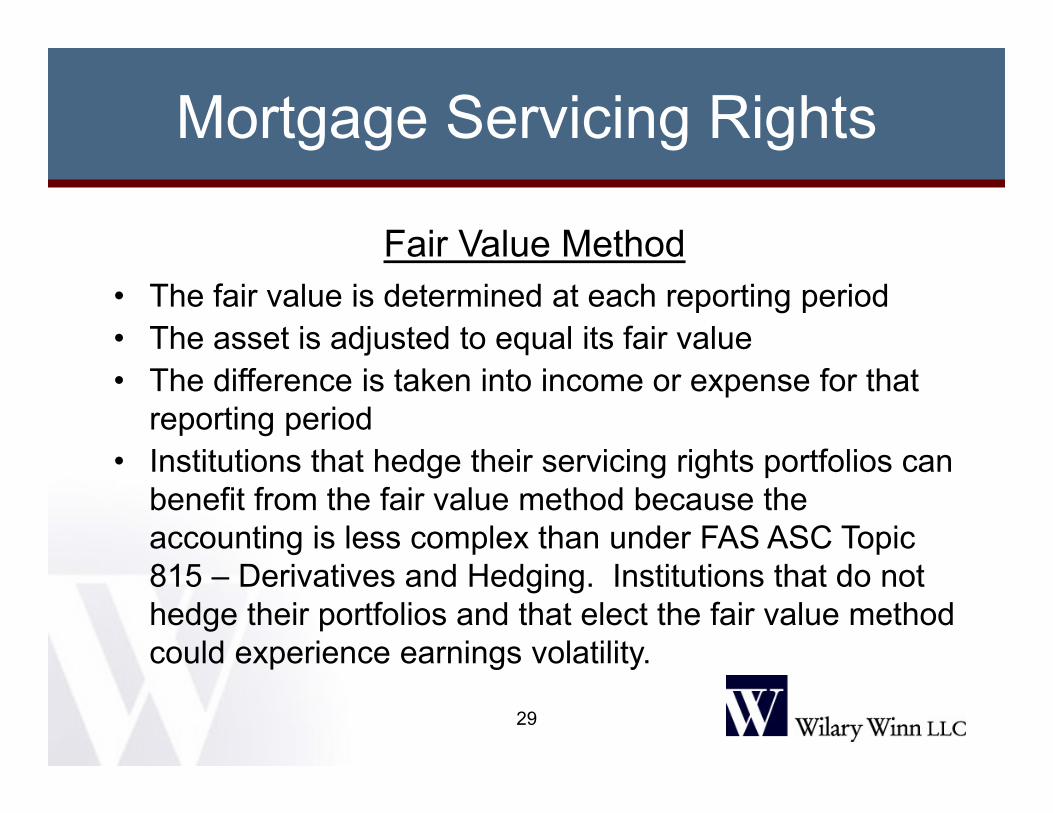

Fair Value Method• The fair value is determined at each reporting period• The asset is adjusted to equal its fair value• The difference is taken into income or expense for that

reporting period• Institutions that hedge their servicing rights portfolios can

benefit from the fair value method because the accounting is less complex than under FAS ASC Topic 815 – Derivatives and Hedging. Institutions that do not hedge their portfolios and that elect the fair value method could experience earnings volatility.

Mortgage Servicing Rights

29

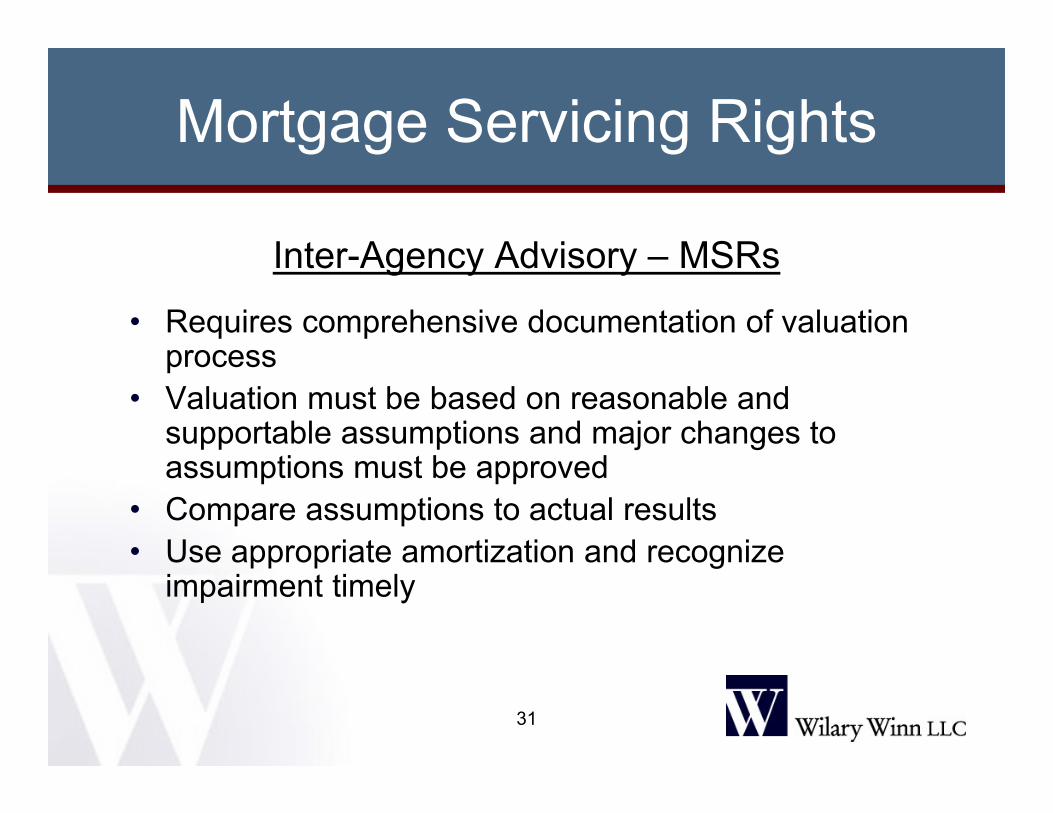

Inter-Agency Advisory – MSRs

• Requires comprehensive documentation of valuation process

• Valuation must be based on reasonable and supportable assumptions and major changes to assumptions must be approved

• Compare assumptions to actual results• Use appropriate amortization and recognize

impairment timely

Mortgage Servicing Rights

31

32

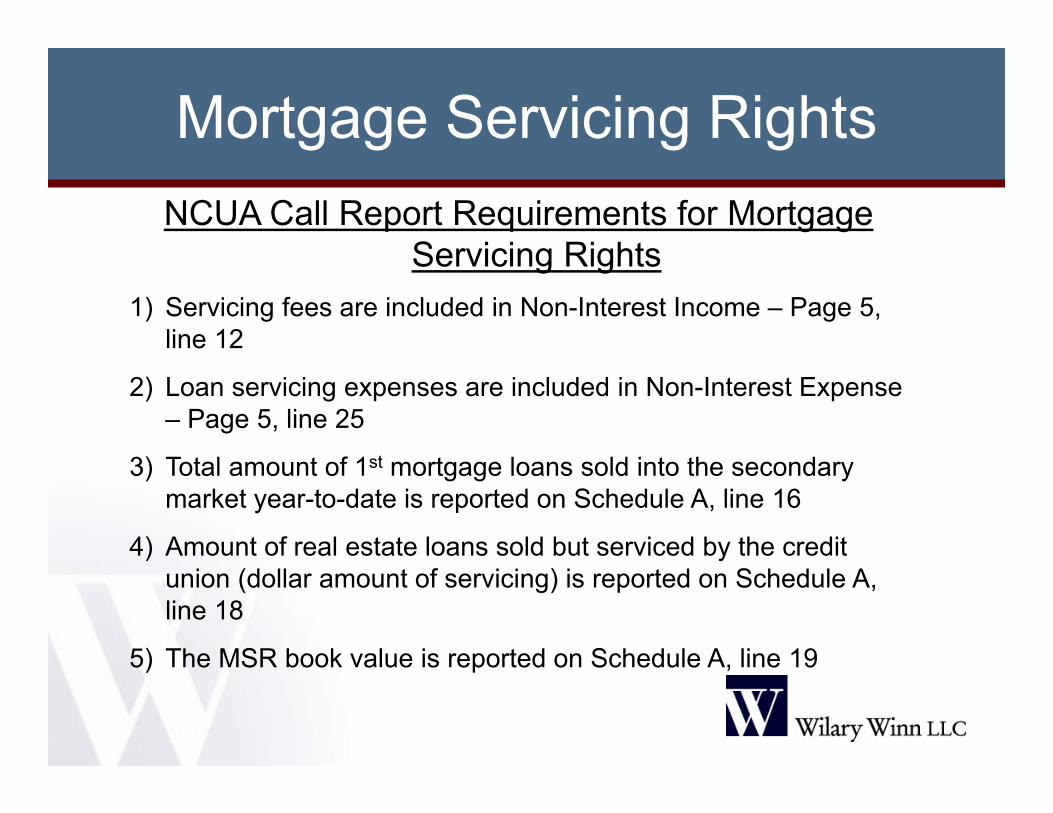

NCUA Call Report Requirements for Mortgage Servicing Rights

1) Servicing fees are included in Non-Interest Income – Page 5, line 12

2) Loan servicing expenses are included in Non-Interest Expense – Page 5, line 25

3) Total amount of 1st mortgage loans sold into the secondary market year-to-date is reported on Schedule A, line 16

4) Amount of real estate loans sold but serviced by the credit union (dollar amount of servicing) is reported on Schedule A, line 18

5) The MSR book value is reported on Schedule A, line 19

Mortgage Servicing Rights

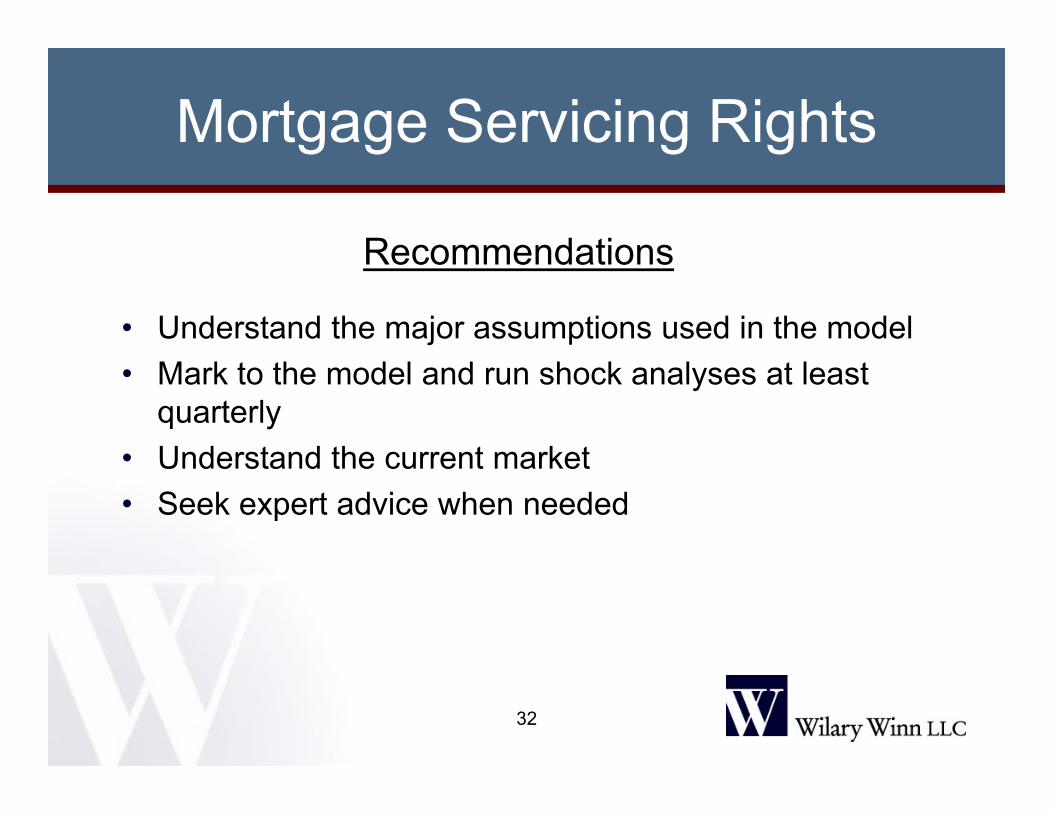

Recommendations

• Understand the major assumptions used in the model• Mark to the model and run shock analyses at least

quarterly• Understand the current market• Seek expert advice when needed

Mortgage Servicing Rights

32

Mortgage Servicing Rights

34

CFPB National Servicing Standards

• Effective January 10, 2014

• Exempts small servicers - - under 5,000 loans

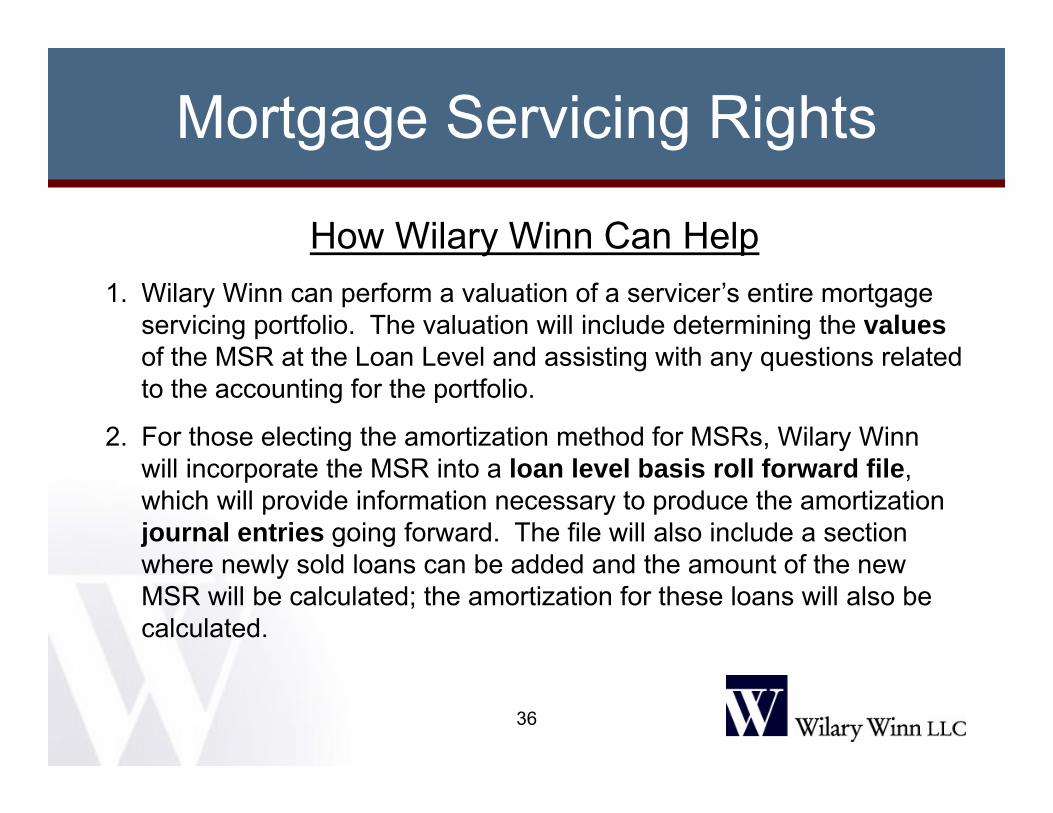

How Wilary Winn Can Help1. Wilary Winn can perform a valuation of a servicer’s entire mortgage

servicing portfolio. The valuation will include determining the valuesof the MSR at the Loan Level and assisting with any questions related to the accounting for the portfolio.

2. For those electing the amortization method for MSRs, Wilary Winn will incorporate the MSR into a loan level basis roll forward file, which will provide information necessary to produce the amortization journal entries going forward. The file will also include a section where newly sold loans can be added and the amount of the new MSR will be calculated; the amortization for these loans will also be calculated.

Mortgage Servicing Rights

36

34

INSERT WEB PAGE SCREENSHOT

34

INSERT WEB PAGE SCREENSHOT

Mortgage Servicing Rights

34

BASIS ROLLFORWARD

DEMONSTRATION

Wilary Winn LLCFirst National Bank Building

332 Minnesota Street, Suite W1750St. Paul, MN 55101

651-224-1200

www.wilwinn.com

Mortgage Servicing Rights

38

Mortgage Servicing Rights

Services and Contact Information

Private Label MBS/CMOs and Asset Liability Management:Frank Wilary [email protected]

Mergers and Acquisitions, Fair Value Footnotes, ASC 310-30, and TDRs:Brenda Lidke [email protected]

Mortgage Servicing Rights and Mortgage Banking Derivatives:Eric Nokken [email protected]

37