what do i need to know about the affordable care act & the health insurance marketplace?

TRANSCRIPT

What do I Need to Know about the Affordable Care Act &

The Health Insurance Marketplace?

What is the Marketplace?

•Offers new, affordable insurance options•Website: www.GetCoveredIllinois.gov•Offers financial help so you can find a plan that

fits your budget•Cannot deny you coverage because of pre-

existing conditions•Cannot charge more because of your health or

gender

Who can benefit?

Marketplace is for: • Uninsured • Underinsured• Those who have individual plans • Those who are a dependent on someone else’s plan

Marketplace is NOT for:•Medicaid eligible•Medicare eligible•Military insurance

Qualified Health Plans cover Essential Health Benefits Qualified Health Plans cover Essential Health Benefits Qualified Health Plans cover Essential Health Benefits, Qualified Health Plans cover Essential Health Benefits,

which include at least these 10 categorieswhich include at least these 10 categories these 10 these 10 categoriescategories

• Ambulatory patient services• Emergency services• Hospitalization• Maternity and newborn care• Mental health and substance use disorder services, including behavioral

health treatment• Prescription drugs• Rehabilitative and habilitative services and devices• Laboratory services• Preventive and wellness services and chronic disease management• Pediatric services, including oral and vision care

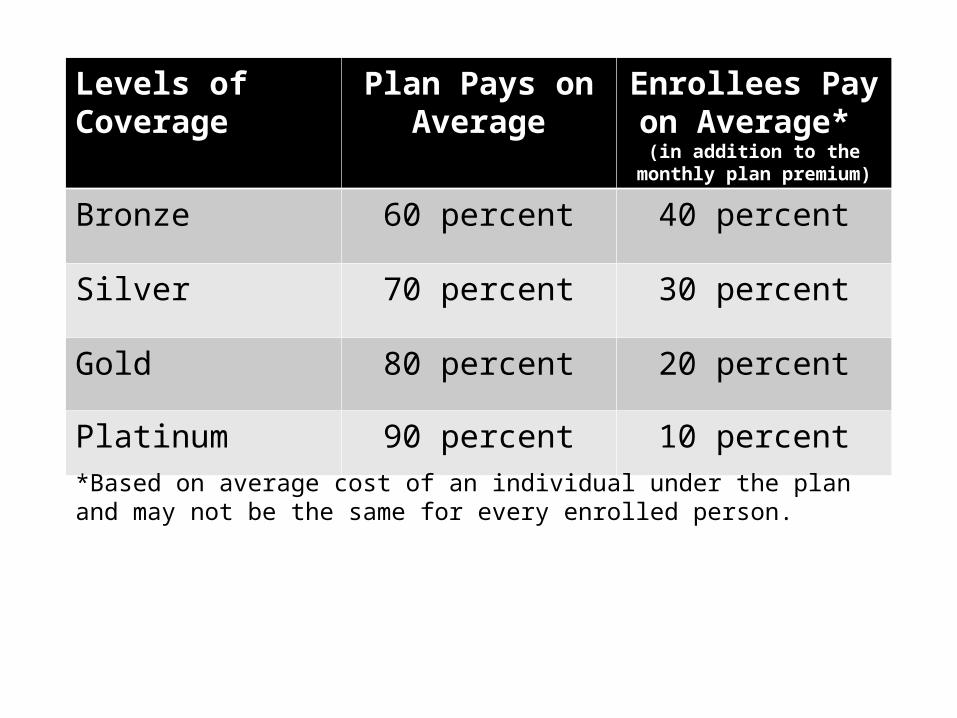

Levels of Coverage Plan Pays on Average

Enrollees Pay on Average*

(in addition to the monthly plan premium)

Bronze 60 percent 40 percent

Silver 70 percent 30 percent

Gold 80 percent 20 percent

Platinum 90 percent 10 percent*Based on average cost of an individual under the plan and may not be the same for every enrolled person.

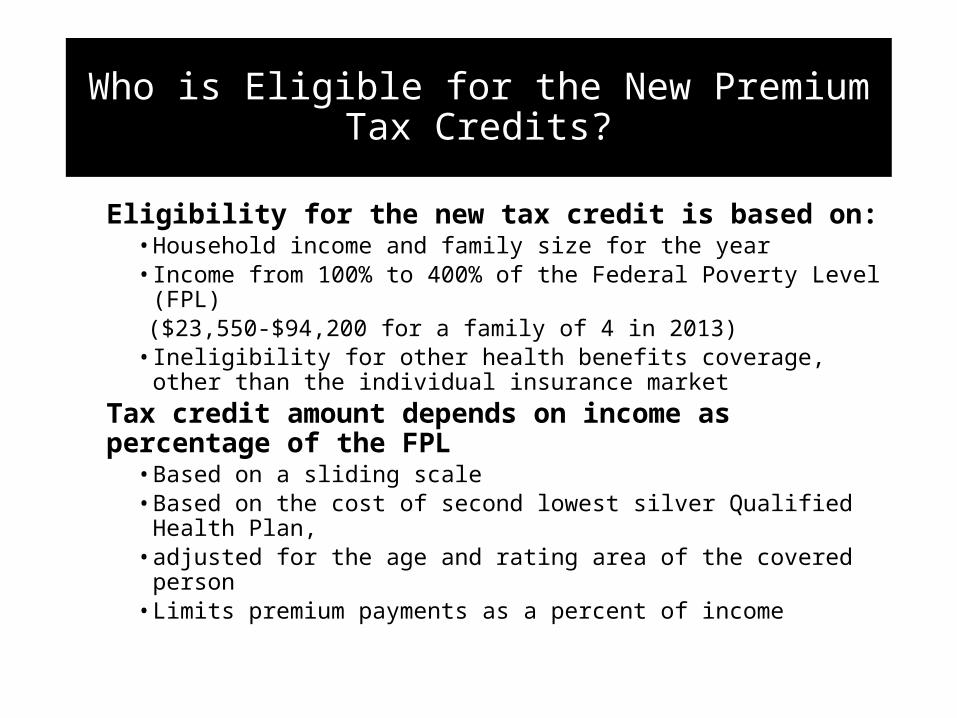

Who is Eligible for the New Premium Tax Credits?

Eligibility for the new tax credit is based on:• Household income and family size for the year• Income from 100% to 400% of the Federal Poverty Level (FPL)

($23,550-$94,200 for a family of 4 in 2013)• Ineligibility for other health benefits coverage, other than the

individual insurance marketTax credit amount depends on income as percentage of the FPL• Based on a sliding scale• Based on the cost of second lowest silver Qualified Health Plan, • adjusted for the age and rating area of the covered person• Limits premium payments as a percent of income

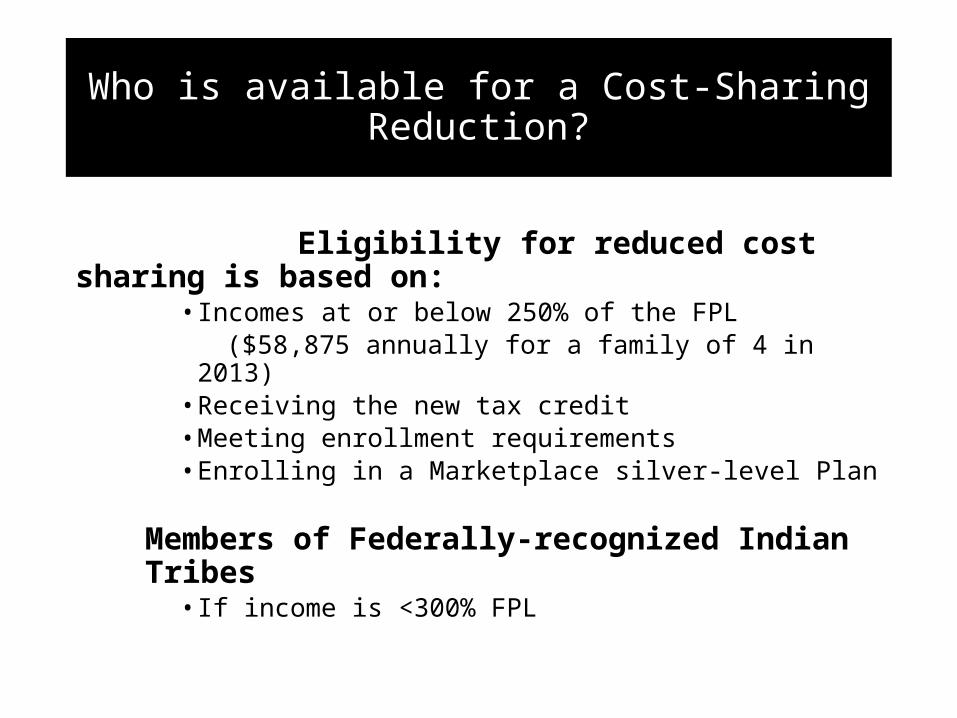

Who is available for a Cost-Sharing Reduction?

Eligibility for reduced cost sharing is based on:• Incomes at or below 250% of the FPL ($58,875 annually for a family of 4 in 2013)• Receiving the new tax credit• Meeting enrollment requirements• Enrolling in a Marketplace silver-level Plan

Members of Federally-recognized Indian Tribes• If income is <300% FPL

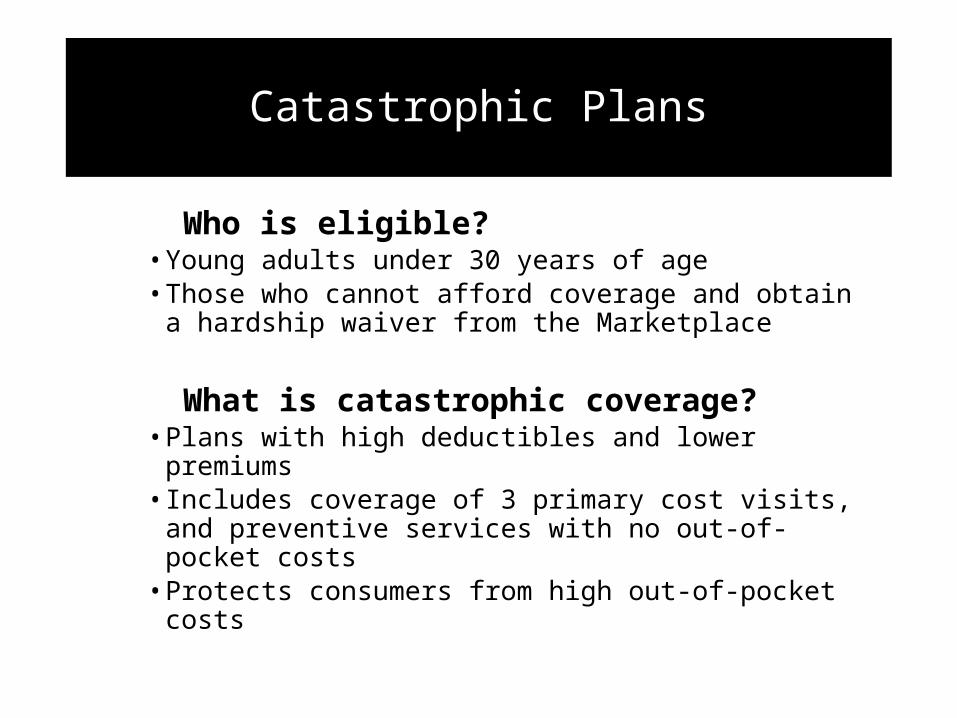

Catastrophic Plans

Who is eligible?• Young adults under 30 years of age• Those who cannot afford coverage and obtain a hardship waiver

from the Marketplace

What is catastrophic coverage?• Plans with high deductibles and lower premiums• Includes coverage of 3 primary cost visits, and preventive services

with no out-of-pocket costs• Protects consumers from high out-of-pocket costs

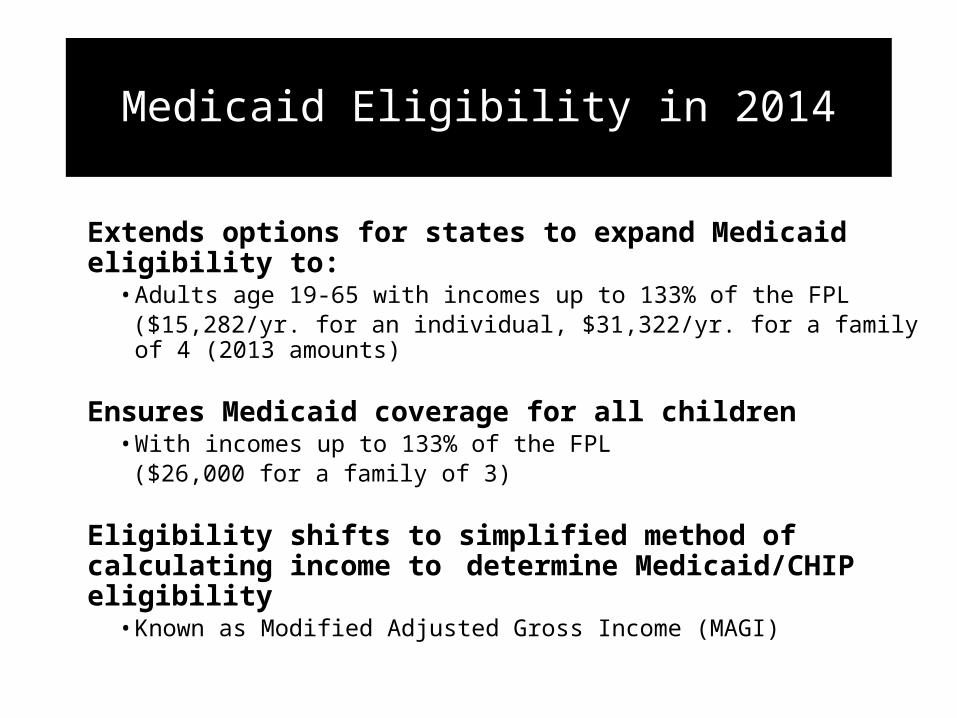

Medicaid Eligibility in 2014

Extends options for states to expand Medicaid eligibility to:• Adults age 19-65 with incomes up to 133% of the FPL ($15,282/yr. for an individual, $31,322/yr. for a family of 4 (2013

amounts)

Ensures Medicaid coverage for all children• With incomes up to 133% of the FPL ($26,000 for a family of 3)

Eligibility shifts to simplified method of calculating income to determine Medicaid/CHIP eligibility

• Known as Modified Adjusted Gross Income (MAGI)

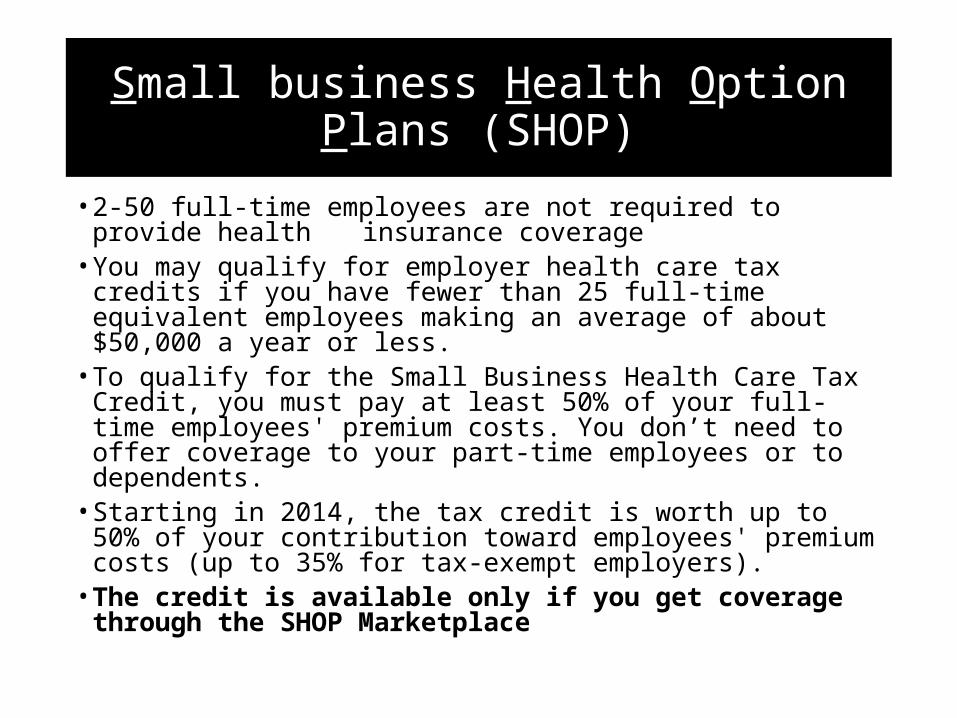

Small business Health Option Plans (SHOP)

• 2-50 full-time employees are not required to provide health insurance coverage• You may qualify for employer health care tax credits if you have

fewer than 25 full-time equivalent employees making an average of about $50,000 a year or less.• To qualify for the Small Business Health Care Tax Credit, you must pay

at least 50% of your full-time employees' premium costs. You don’t need to offer coverage to your part-time employees or to dependents.• Starting in 2014, the tax credit is worth up to 50% of your

contribution toward employees' premium costs (up to 35% for tax-exempt employers).• The credit is available only if you get coverage through the SHOP

Marketplace

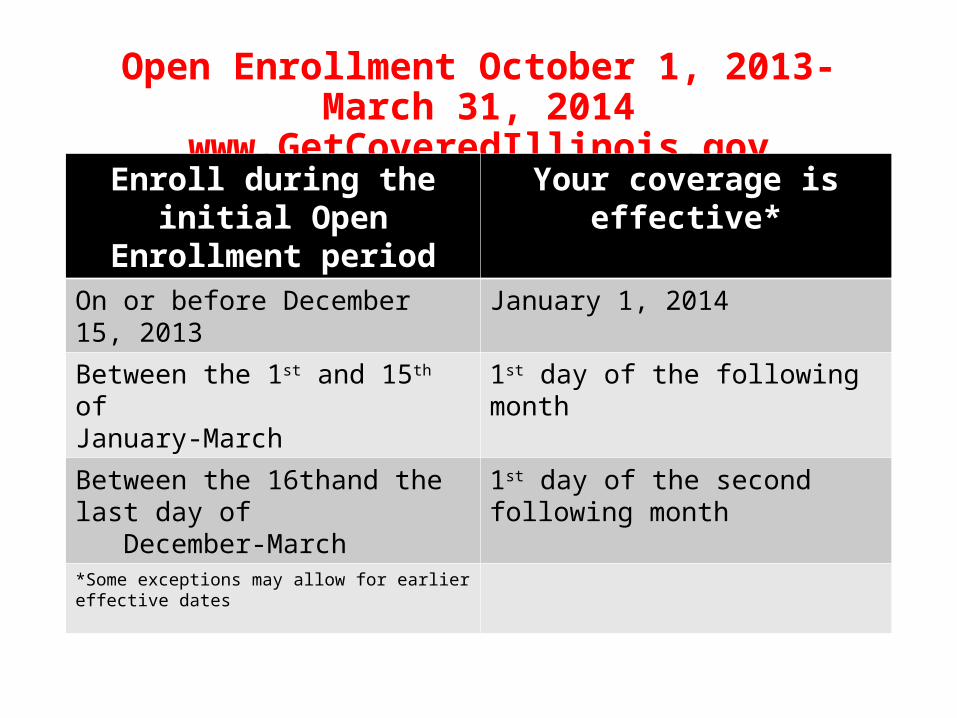

Open Enrollment October 1, 2013-March 31, 2014

www.GetCoveredIllinois.govEnroll during the initial Open

Enrollment periodYour coverage is effective*

On or before December 15, 2013 January 1, 2014

Between the 1st and 15th of January-March

1st day of the following month

Between the 16thand the last day of December-March

1st day of the second following month

*Some exceptions may allow for earlier effective dates

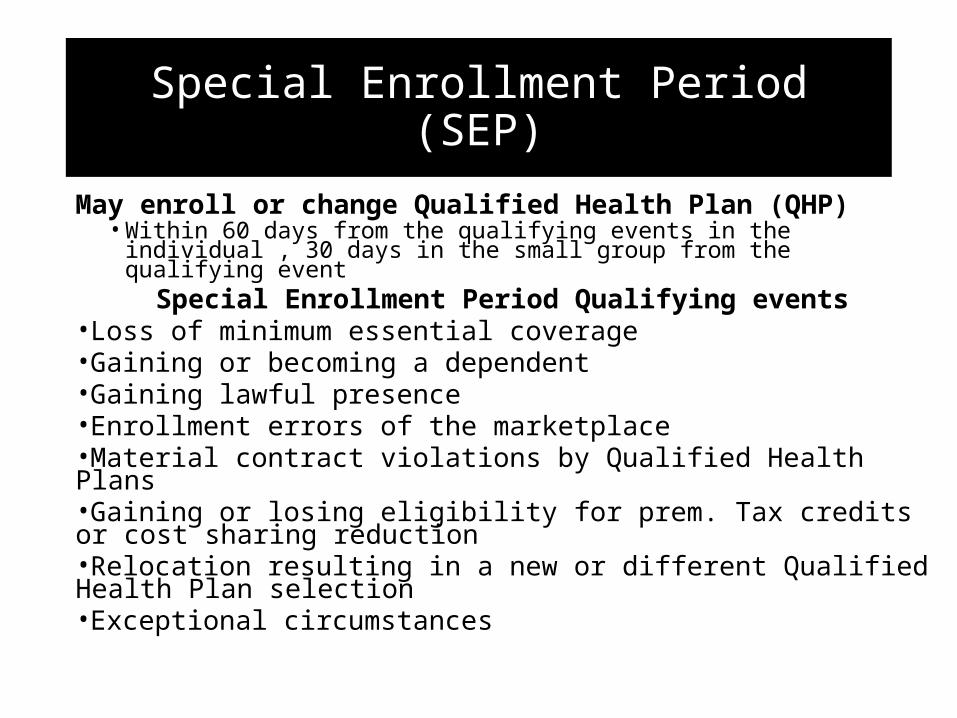

Special Enrollment Period (SEP)

May enroll or change Qualified Health Plan (QHP)• Within 60 days from the qualifying events in the individual , 30 days in the

small group from the qualifying eventSpecial Enrollment Period Qualifying events

•Loss of minimum essential coverage•Gaining or becoming a dependent•Gaining lawful presence•Enrollment errors of the marketplace•Material contract violations by Qualified Health Plans•Gaining or losing eligibility for prem. Tax credits or cost sharing reduction•Relocation resulting in a new or different Qualified Health Plan selection•Exceptional circumstances

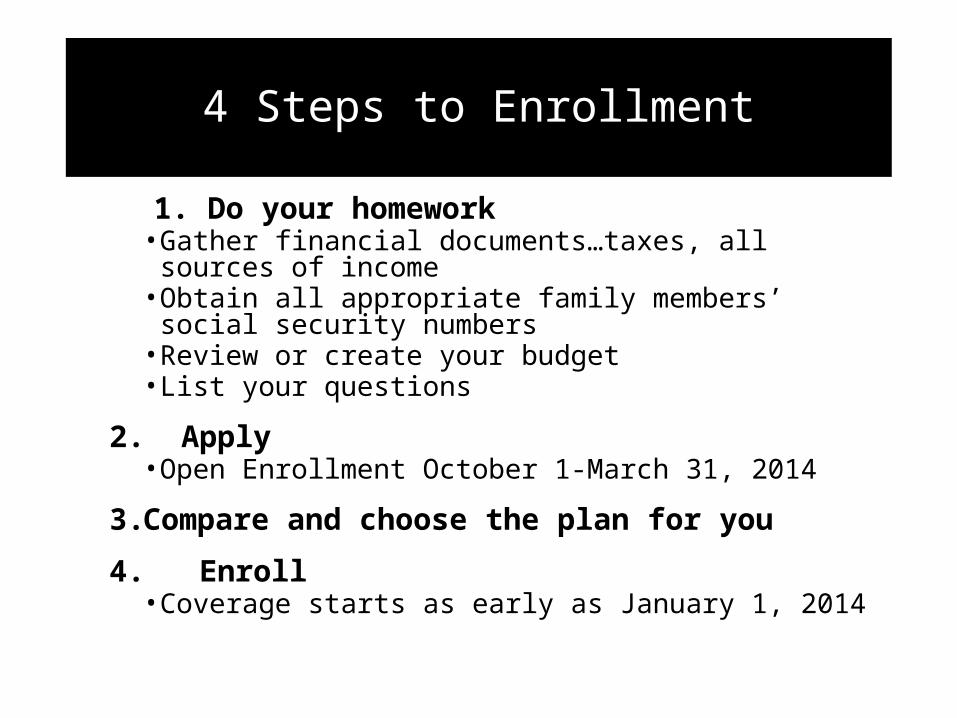

4 Steps to Enrollment

1. Do your homework• Gather financial documents…taxes, all sources of income• Obtain all appropriate family members’ social security

numbers• Review or create your budget• List your questions

2. Apply• Open Enrollment October 1-March 31, 2014

3.Compare and choose the plan for you

4. Enroll• Coverage starts as early as January 1, 2014

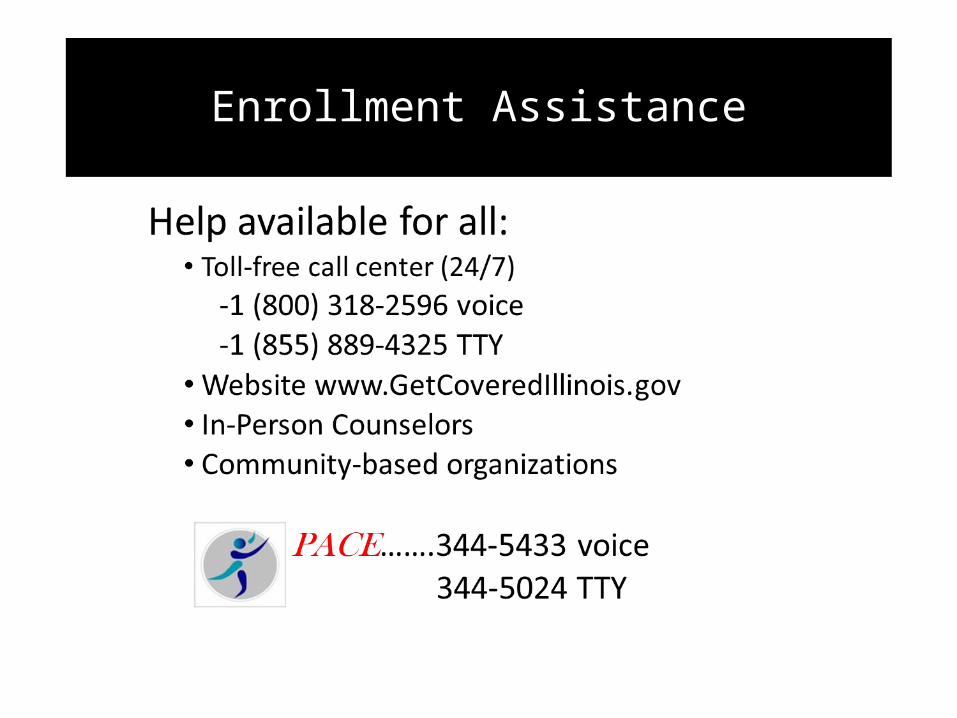

Enrollment Assistance

Questions?