what do caribbean ifcs need to do to survive and prosper ... · what do caribbean ifcs need to do...

TRANSCRIPT

© Z/Yen Group 2010

© Z/Yen Group 2012

Z/Yen Group Limited

Risk/Reward Managers

90 Basinghall Street

London EC2V 5AY

United Kingdom

tel: +44 (20) 7562-9562

Professor Michael Mainelli

2nd CARIFORUM Conference on the International

Financial Services Sector in the Caribbean Region

What Do Caribbean IFCs Need To Do To

Survive And Prosper In The 21st Century?

© Z/Yen Group 2010

© Z/Yen Group 2012

Z/Yen Overview

♦ Special – City of London‟s leading commercial think-tank

♦ Services – projects, coaching/training, expertise on

demand, research

♦ Sectors – technology, finance, voluntary, professional

services, outsourcing All major investment banks as clients, as well as insurers,

reinsurers, exchanges, brokers, information and ICT firms

British Computer Society IT Director of the Year 2004 for

PropheZy and VizZy

DTI Smart Award 2003 for PropheZy

Sunday Times Book of the Week, Clean Business Cuisine

£1.9M Foresight Challenge Award for Financial £aboratory

visualising financial risk 1997

© Z/Yen Group 2010

© Z/Yen Group 2012

What We Already Know

Areas of Competitiveness: ♦ People

♦ Business Environment

♦ Market Access

♦ Infrastructure

♦ General Competitiveness

© Z/Yen Group 2010

© Z/Yen Group 2012

ةيمالعال ةيالمال زكارمال رشؤم

Índice de Centros Financieros Globales

Indice dei Centri Financieri Globali

Indice du Centres Financiers Globaux

世界的な金融

センターインデックス

Σφαιρικός οικονομικός κεντρικός δείκτης

Глобальный индекс финансовых центров

Wskaźnik Globalnych Finansowych Centrów

Индекс на Световните Финансови Центрове

Goelydh Nírnaeth Arnoediad Blebithar

Globaler Finanzzentrenindex

全球金融中心指数

全(quán) 球(qiú) 金(jīn) 融(róng) 中(zhōng) 心(xīn) 指(zhǐ) 数(shù)

A Global Phenomenon

© Z/Yen Group 2010

© Z/Yen Group 2012

A Global Phenomenon

© Z/Yen Group 2010

© Z/Yen Group 2012

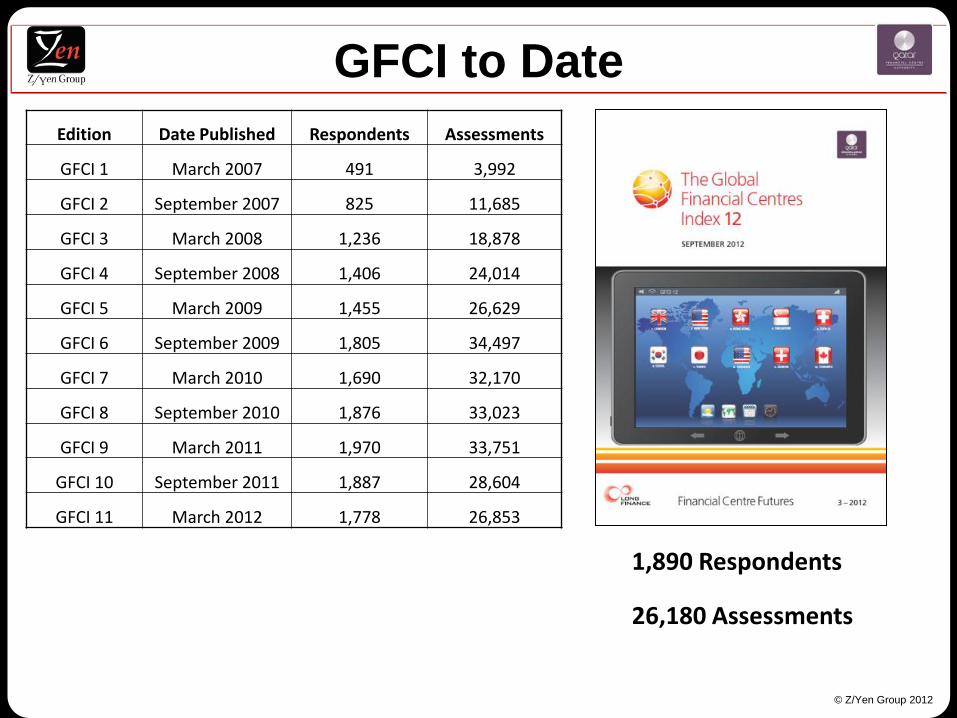

GFCI to Date

Edition Date Published Respondents Assessments

GFCI 1 March 2007 491 3,992

GFCI 2 September 2007 825 11,685

GFCI 3 March 2008 1,236 18,878

GFCI 4 September 2008 1,406 24,014

GFCI 5 March 2009 1,455 26,629

GFCI 6 September 2009 1,805 34,497

GFCI 7 March 2010 1,690 32,170

GFCI 8 September 2010 1,876 33,023

GFCI 9 March 2011 1,970 33,751

GFCI 10 September 2011 1,887 28,604

GFCI 11 March 2012 1,778 26,853

1,890 Respondents

26,180 Assessments

© Z/Yen Group 2010

© Z/Yen Group 2012

The GFCI Process

GFCI 12 uses 26,180

assessments from

1,890 respondents

GFCI 12 uses 86

Instrumental

Factors

© Z/Yen Group 2010

© Z/Yen Group 2012

The GFCI World

© Z/Yen Group 2010

© Z/Yen Group 2012

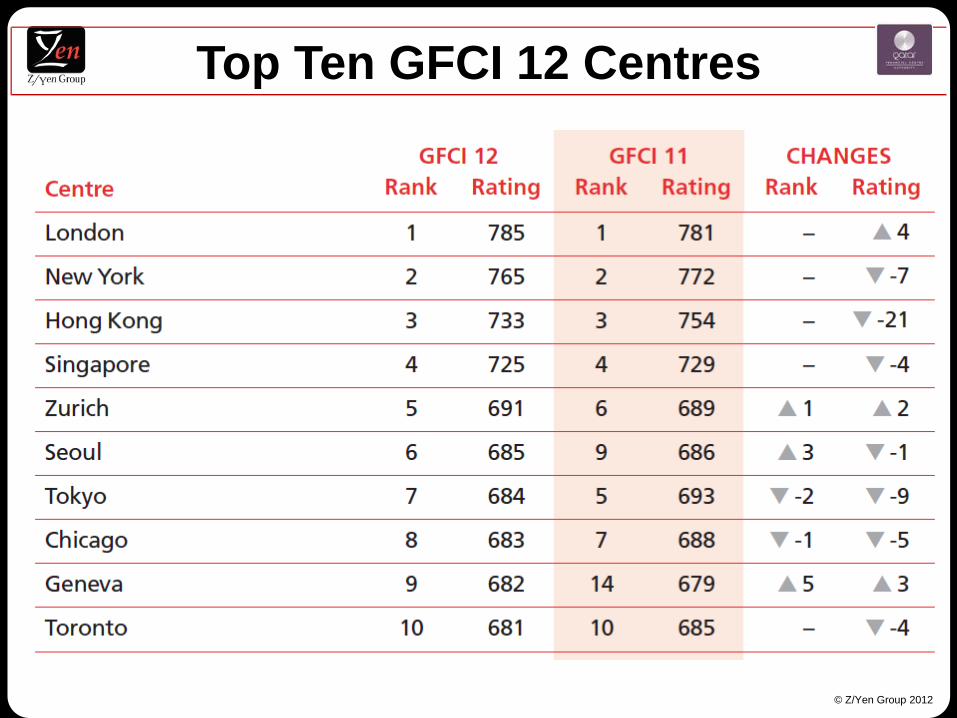

Top Ten GFCI 12 Centres

© Z/Yen Group 2010

© Z/Yen Group 2012

♦ Greater confidence and lower standard deviation

GFCI 12 Headlines (1)

© Z/Yen Group 2010

© Z/Yen Group 2012

♦ Hong Kong slips below London and New York

GFCI 12 Headlines (2)

London / New York Trend Line

Hong Kong / Singapore Trend Line

© Z/Yen Group 2010

© Z/Yen Group 2012

GFCI 12 Headlines (3)

Europe: Capital Cities at the heart of the Eurozone crisis are hit

© Z/Yen Group 2010

© Z/Yen Group 2012

GFCI 12 Headlines (4)

Asian centres Large rises in the ratings of Asia/Pacific centres appears to have stalled:

© Z/Yen Group 2010

© Z/Yen Group 2012

GFCI 12 Headlines (5)

Offshore Centres having suffered significant reputational damage in the past four years, regained ground in GFCI 10 and

GFCI 11. GFCI 12 shows a mixed picture with no significant moves

© Z/Yen Group 2010

© Z/Yen Group 2012

GFCI 12 Headlines (6)

© Z/Yen Group 2010

© Z/Yen Group 2012

More Significant?

© Z/Yen Group 2010

© Z/Yen Group 2012

Profile of Financial Centres

© Z/Yen Group 2010

© Z/Yen Group 2012

Profile of Global Centres

© Z/Yen Group 2010

© Z/Yen Group 2012

Profile of Transnational Centres

© Z/Yen Group 2010

© Z/Yen Group 2012

Profile of Local Centres

© Z/Yen Group 2010

© Z/Yen Group 2012

Assessments by Region – London

© Z/Yen Group 2010

© Z/Yen Group 2012

Assessments by Region – New York

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Progress – Caribbean IFCs

450

470

490

510

530

550

570

590

610

630

650

GFCI 1 GFCI 2 GFCI 3 GFCI 4 GFCI 5 GFCI 6 GFCI 7 GFCI 8 GFCI 9 GFCI 10 GFCI 11 GFCI 12

GFCI Over Time

Cayman Islands British Virgin Islands Hamilton Bahamas

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Progress – European IFCs

450

500

550

600

650

700

GFCI 1 GFCI 2 GFCI 3 GFCI 4 GFCI 5 GFCI 6 GFCI 7 GFCI 8 GFCI 9 GFCI 10 GFCI 11 GFCI 12

GFCI Over Time

Jersey Luxembourg Guernsey Isle of Man Monaco Gibraltar Malta

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Progress – Asian IFCs

450

500

550

600

650

700

GFCI 1 GFCI 2 GFCI 3 GFCI 4 GFCI 5 GFCI 6 GFCI 7 GFCI 8 GFCI 9 GFCI 10 GFCI 11 GFCI 12

GFCI Over Time

Jakarta Manila Kuala Lumpur Taipei Mauritius

© Z/Yen Group 2010

© Z/Yen Group 2012

Assessments by Region

-150 -100 -50 0 50 100 150

Europe (26.2%)

Offshore (60.9%)

North America (2.9%)

Latin America (0.2%)

Middle East/Africa (1.1%)

Asia/Pacific (8.6%)

British Virgin Islands

-150 -100 -50 0 50 100 150

Europe (31.6%)

Offshore (52.1%)

North America (6.1%)

Latin America (0.2%)

Middle East/Africa (0.9%)

Asia/Pacific (9.2%)

Cayman Islands

Caribbean IFCs

-150 -100 -50 0 50 100 150

Europe (26%)

Offshore (55.9%)

North America (9.4%)

Latin America (0.4%)

Middle East/Africa (0.8%)

Asia/Pacific (7.5%)

Bahamas

© Z/Yen Group 2010

© Z/Yen Group 2012

Assessments by Region

-150 -100 -50 0 50 100 150

Europe (33.7%)

Offshore (55.8%)

North America (4.3%)

Latin America (0.2%)

Middle East/Africa (1.4%)

Asia/Pacific (4.8%)

Jersey (Guernsey is very similar)

-150 -100 -50 0 50 100 150

Europe (47.1%)

Offshore (35%)

North America (6.5%)

Latin America (0.3%)

Middle East/Africa (1%)

Asia/Pacific (10.2%)

Luxembourg

European IFCs

-150 -100 -50 0 50 100 150

Europe (43.6%)

Offshore (41.6%)

North America (2.7%)

Latin America (0.4%)

Middle East/Africa (1.9%)

Asia/Pacific (9.7%)

Monaco

© Z/Yen Group 2010

© Z/Yen Group 2012

Assessments by Region

Asian IFCs

-150 -100 -50 0 50 100 150

Europe (19.5%)

Offshore (8.9%)

North America (8.9%)

Middle East/Africa (1.6%)

Asia/Pacific (61%)

Jakarta

-150 -100 -50 0 50 100 150

Europe (30%)

Offshore (11.6%)

North America (6.8%)

Middle East/Africa (3.2%)

Asia/Pacific (48.4%)

Kuala Lumpur

-150 -100 -50 0 50 100 150

Europe (25.3%)

Offshore (7.5%)

North America (12.3%)

Latin America (0.7%)

Middle East/Africa (2.1%)

Asia/Pacific (52.1%)

Taipei

© Z/Yen Group 2010

© Z/Yen Group 2012

Stability – Top 40 Centres

British Virgin Islands

Isle of Man

Hamilton

Monaco

Jakata

Gibraltar

Mauritius

Manila

Malta

Bahamas

© Z/Yen Group 2010

© Z/Yen Group 2012

Areas of Competitiveness

© Z/Yen Group 2010

© Z/Yen Group 2012

Industry Sectors

© Z/Yen Group 2010

© Z/Yen Group 2012

Reputational “Advantage”

© Z/Yen Group 2010

© Z/Yen Group 2012

Reputational “Disadvantage”

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Reputations

Centre Average

Assessment GFCI 12 Rating

Reputational

Advantage

Kuala Lumpur 670 644 26

Jersey 672 654 18

Luxembourg 652 646 6

Guernsey 642 641 1

Isle of Man 616 629 -13

Taipei 614 628 -14

Jakarta 547 573 -26

Monaco 569 597 -28

Malta 532 575 -43

Mauritius 530 579 -49

Gibraltar 527 599 -72

Manila 481 570 -89

© Z/Yen Group 2010

© Z/Yen Group 2012

Caribbean Reputations

Centre Average

Assessment

GFCI 12

Rating

Reputational

Advantage

Cayman

Islands 626 625 1

British Virgin

Islands 624 624 0

Hamilton 621 621 0

Bahamas 521 572 -51

© Z/Yen Group 2010

© Z/Yen Group 2012

We Will Sur-Thrive!

(with apologies to Gloria Gaynor)

© Z/Yen Group 2010

© Z/Yen Group 2012

Anna Karenina Principle

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Generalities

♦ Strong in Wealth Management

♦ Strong in Professional Services

♦ Weak in Government & Regulatory

♦ Weak in Insurance

© Z/Yen Group 2010

© Z/Yen Group 2012

IFC Challenges

♦ Larger nations – applying ongoing pressure trying to

prevent tax competition

♦ OECD – TIEAs, continuing peer reviews of regulatory

framework and implementation and sanctions for non

compliance

♦ OECD members – e.g. US, UK France - plans to limit

use of „havens‟ for tax minimisation

♦ Publicity around aggressive tax planning schemes

♦ FATF/IMF – increased focus on AML and terrorist

finance

♦ Financial Stability Board – information sharing

standards

♦ Foreign Account Tax Compliance Act (FATCA)

© Z/Yen Group 2010

© Z/Yen Group 2012

Connectivity Matters

© Z/Yen Group 2010

© Z/Yen Group 2012

♦ Secrecy ♦ Tax evasion

♦ Conduits √

tax simplicity – fighting back

simple rule zones

long-term “store and release”

zones

♦ Long finance √

signalling stability and rules of

change

„selling‟ regulation

regulatory standards, e.g. ISO

♦ Working together √

corporates, professional services,

IFCs ...

Thoughts for IFCs

© Z/Yen Group 2010

© Z/Yen Group 2012

GFCI 13 – March 2013

Participate yourself at:

www.financialcentrefutures.net