western australia's agricultural bank

TRANSCRIPT

WESTERN ATJSTRALIA’S AGRICULTURAL BANK

I. Introductory. 11. Inception and Development of the Agricultural Bank.

111. The Commission of 1933-4. (a) Conclusions and recommendations. (b) General criticisms.

IV. Future Policy-The New Act.

I During the last forty years remarkable progress has been

achieved in wheat-growing in Western Australia. The total area under wheat in 1895 was only 23,000 acres, which yielded 188,000 bushels. I n the ’nineties the colony was a heavy impor- ter of flour and wheat. By the year 1930 she had built up a very large wheat-esporting trade. Clearly, great efforts had been made t o counteract the diminishing gold yield and t o prevent a decline in population. These efforts began in the days when “ Big John ” Forrest controlled the destinies of Western Aus- tralia. By a combination of liberal land lams and credit foncier, he strove to build up the long languishing agricultural industry t o feed the rapidly increasing population. The Agricultural Bank was his foundation. 1906 saw the State self-sufficient as far as wheat and flour were concerned, and entering the ranks of wheat exporting countries. In that year 250,283 acres were sown with wheat and the yield was 2,758,567 bushels. A new phase in the development of Western Australia began with the advent of the enthusiast, James lIitchel1, t o the Ministry for Lands. Settlement was pushed eastward and northm-ard from the existing agricultural districts. A considerable increase of population of the pioneering type was anricipated. The moderate prices prevailing just before the Great War, together with the onset of drought suggested the likelihood of a break- down in this policy. The farming community mas in particu- larly bad trim, when a new Government Department issuing seasonal credit to wheat-growers was established-the Industries Assistance Board. The industry mas saved-at considerable expense, it is true. But it mas ready to take advantage; of the better times for wheat-growers, one might almost say, “ the halcyon days,” when wheat reached 7s. 6d. a bushel and main- tained an average of we11 over 5s. So in the peak year, 1930-1,

45

46 THE ECONOMIC RECORD J U N E

3,850,000 acres were sown with =heat for a harvest of 53,500,000 bushels. But all good things must come to an end. The very year which mas marked by this record harvest saw a world production of 5,000,000,000 bushels superimposed on a heavy carry-over. The slump in prices mas immediate, inevitable and overwhelming.

There can be no doubt that the vigorous policy of land settlement pursued from 1906 onward had brought about accelerated development. As early as 1920 the writer expressed considerable doubt as to the economic soundness of this development,’ based as i t was as much upon lavish credit as upon liberal land re,dations. The magnificence of the develop- ment in so short a period cannot be gainsaid. Its soundness is another question when consideration is given to the financial burden laid upon the farming community in order to achieve it.

A Royal Commission in 1931 inquired into the disabilities affecting the agricultural industry.2 For the first time the magnitude of the indebtedness =as revealed to the public. The 12,000 clients of the Agricultural Bank owed E14,000,000 to the State. But the total indebtedness of the 20,559 wheat farmers of the State was over E31,000,000. The Commissioners, in con- cluding their Report, said, “ The whole industry was pyramided upon good prices and lavish credit without due inquiry being made into production costs, world production of wheat and the value of assets upon which such credit was being extended. The Government . . . together with all classes of the community, including the Associated Banks, are responsible for the accele- rated and uneconomical development of the farming industry in Western Australia.’’ This I Y ~ , indeed, a comprehensive indictment. Another Royal Commission mas soon a t work investigating dairy-farming in the South-Vest where Sir James Mitchell’s Group Settlement Scheme had broken down badly.s In 1934, as a par t of its Commonwealth-wide inquiry, the Federal Royal Commission on the Wheat Industry reached the State. So that, it may with t rnth be said that the general condition of the farming community in Western Australia has lately been the subject of extensive inquiry.

Par t IV of the 1931 Disabilities Commission’s Report con- sidered the position of thq Agricultural Bank and made certain suggestions in reference thereto. A s a consequence, the Agri- cultural Bank Royal Commission was created under date the

1. I F The Agricultural Bank and Induatriec Asrbtanca Soard (Maernillan). 1921. 2. See Economic Record (Nov.. 1931). 3. See Economic Record (Nov.. 1925. and Map. 1930). and The Peopling of

Awtrdiu (Furthe7 Studier). 1933. Ch. II (b).

1935 W.A.3 AGRICULTURAL BANK 47

3rd October, 1933, and issued its Report 25th DiIay, 1934. The Report has been the subject of lengthy debate in Parliament and the basis of fresh legislation, the Agricultural Bank Act, 1934, assented t o at the beginning of this year and proclaim@ to come into operation on 18th March, 1935. The Report is a document of considerable importance in the history of Australa- sian rural credit policy. The sweeping nature of the Commission’s conclusions and recommendations were in part a t least a cause of some delay in its publication. Much discussion and some criticism were evoked by the Report. The Trustees who were indicted in the document issued Replies as did the Auditor- General. The Collier Government, however, pledged itself to introduce legislation giving effect to the Commission’s main recommendations. This has been done. New management has been given to the reconstituted Bank. It is anticipated that i t will now work along lines indicated by the economic position of the wheat-growing industry.

I1 Before giving consideration to the findings and recommenda-

tions of the Commission, it seems desirable to dwell briefly upon the foundation and previous history of the Bank. The Com- mission aIso deemed this course advisable and Part I of the Report covers this ground.

The Agricultural Bank of Western Australia mas a cherished measure of John Forrest in his policy of development in the early ’nineties. The Bank was established by a Statute of 1894 at a time when control of banking by private enterprise was more than a little discredited throughout Australia. Based upon thq European model of Credit Foncier, it mas designed, in conjunction with liberal land legislation, to help the farmer in the early stages of developing his holding. The Bank was empowered to advance on a 50 per cent. basis only, against a limit,ed category of hprovements-clearing, cultivating and ring-barking. 5400 was the maximum advance. The rate of interest charged was 5 per cent. The Bank was financed by the Government Savings Bank to which it issued mortgage bonds a t 4 per cent. to a total amount, under the Act, of 5100,000. For five years the borrower had only to pay interest. Then repap- ments had t o commence and be completed by half-yearly pay- ments, spread over 25 years.

The institution opened its doors for business on these modest lines early in 1895. Amendments in 1896, 1899 and 1902 widened the scope of the Bank. Fencing, water conservation,

48 THE ECONOMIC RECORD JUNE

buildings, adding to existing improvements, and development of orchards and vineyards, became objects for which money could be advanced. The maximum advance was increased to €1,000 and a 665 per cent. basis rep lacd the 50 per cent. one. In 1904 the capital of the Bank was fixed a t €400,000. The progress of the Bank which up to 30th June, 1906, had lent $394,164 was steady during its first decade. Jus t over €70,000 had been repaid. The decline in the gold yield which marked the new century was offset to some extent by the improved agricultural position. It mas generally acknowledged that the Agricultural Bank, with its financial aid to development, had been a decisive factor in this work of establishing agriculture.

Imports of other foodstuffs hod, however, considerably increased over the same period, a fact which made Rlinisters anxious to foster further and more diversified development. In 1906 the Moore Government, conscious of the diminishing gold yield, decided upon a more vigorous policy. In charge of t h e Lands Department xas an unusually energetic Bliniste# who sponsored a consolidating Agricultural Bank Act. For about two-thirds of its clauses the new Act was identical with the parent legislation. But in certain essential points of policy it departed from the Forrest tradition. For the first time advances were sanctioned t o the full vdne of improvements. This was for B O O of a maximum advance limit of €300, the balance being on a 50 per cent. basis. Advances for the purchase of stock were allowed5. A change of great importance was made at this time, too, in the Bank management. The institution was now declared to be a body corporate with control vested in a Managing Trustee, holding office during the Governor’s pleasure, and t w o co-Trustees (part-time) appointed f o r two years by the Governor-in-Council. The Bank’s capital in view of the “libcr- alizing” tendency of the measure was increased to €1,000,000. Funds continued, until 1912, to be prol-ided by the Government Savings Bank against the issue of mortgage bonds.

I t was, apparently, the aim of the 1906 Act to strengthen the Bank’s position while inau,wating a more liberal policy. But the position of the management seems to have become more amenable to political influences, more dependent upon the Minister for Lands. Failure to preserve a margin of security in making improvement loans appeared likely to result in losses, since risks were nmv to be taken n-ith the land (i.e., from a rainPzll point of vielr) and wheat-growing ~vould iiom be

4. J x n c r (now Sir Jxrne3) Jlitchcll. 8. Up LU a rather rnm:re limit of .€LOO.

1935 W.A.’s AGRICULTURAL BANK 49

recompensed by a world market price. The Moore Government began a wild “ booming ) ) of land settlement. So freely did money flow to the new farming communities that 1909 witnessed the doubling of the Bank’s capital.

I n 1911 came the first check-a partial drought-to the policy of vigorous development. The Scadden (Labour) Government felt itself obliged to set up a Seed Wheat Board, to which was entrusted the work of supplying seed wheat, fertil- isers and fodder to some 1,600 distressed farmers of certain drought-stricken areas. In most instances the only security they could offer was that of the prospective crop. A year later came an amending Act of considerable importance sometimes styled (after the then Minister for Lands) the “Bath amend- ment,” which was a great departure from the original policy of Forrest in establishing the Bank on credit foncier lines, to supply long term credit with a reasonable margin of security. The 1906 Act had done away to some extent with the margin of security. The 1912 Act authorized the Trustees t o make advances to an amount not exceeding 62,000 to persons engaged in the business of farming or grazing or in agricultural or pastoral pursuits for any pwrpose, incidental to or in aid of such industry, including the erection of a dwelling house. The Act is silent about margin of security relative to value of improvements. af ter 1906 there is noticeable a tendency to utilize improvement loans f o r seasonal purposes. From 1912, with the precedent of the Seed Wheat Board, the tendency to find seasonal credit was quickened. The necessity which now esisted to increase the Bank’s capital to S4,00O10O0 shows the extent to which money was being expended at this time.6

In 1914 the yield fell away, owing to drought, practically to nothing. Let the Commission Report speak as to the position:- “It is apparent that 80 per cent. of the newly-settled farmers in Western Australia were not sufficiently established to stand a bad season.” The precedent of 1911 was folloxed. The Government set up the Industries Assistance Board7 t o supply seasonal credit (even sustenence) to the thousands of drought- stricken farmers. Concerning this institution, the Royal Com-

6. These are comparative figurea :- Year Ending Amount Total Amount Total Area Total Area

30th June Advanced Outatandinr under-Crop under Whect Yield € E acres acres bushels _ _ .. . _. ..-..

1906 .. .. 394364 323.466 460.825 250.233 2,759,567 1911 .. .. 1,540,241 976.812 1,072,653 612.104 4,836,904 1913 . . . . 2.582.937 1.883.957 1.537.923 1.097.193 13.331.350 . .. i;3,6;01a ~.~ 1914 ._ .. 3 . 0 8 9 . m 2;331;959 i;s67;54? 2,624,190

‘7. When the Eoard was set up in 1915. it was confidently espected that it would

D function for only one or two seasons at most. It is still operative.

50 THE ECONOMIC RECORD JUNE

mission of 1917, which investigated the position of the agricul- tural industry, observed that it undoubtedly saved the wheat belt, but in doing so was guilty of every sin in the agricultural and administrative calendar. ”

This Royal Commission found the affairs of the Agricultural Bank and Industries Assistance Board in a most unsatisfactory state. It recommended a revision of the Bank’s methods and the removal of the Trustees from political control. It also favoured the appointment of Trustees for life, an increase in the Bank’s capital, and a policy for the future of making money available for farmers a t the lowest possible rate of interest on sound business lines. The recommendations of this Commission were ignored. By 1931 the scheme of Group Settlement in the South West was nndel; way. Neanwhile, the financing of the wheat farmers through thq medium of both Agricultural Bank and Industries Assistance Board went on apace. High wheat prices encouraged extension of settlement. since secondary production was hampered by Eastern States control of the home market. The areas utilized were, however, known t o be precarious for wheat-growing, either because of unreliable rainfall o r poorness of soil. It is hard to justify the Bank’s further extensive operations from an economic viewpoint in view of the position disclosed in 1917. But the pioneering spirit was strong. Apparently the view taken after 1912 was that selection of a block carried with it an improvement loan, even to the full value of improvements, regardless of the fitness or experience of the selector.

I11 (a ) The Commission, which was comprised of a lawyer, a

banker and a farmer, representative, as i t were, of the three- fold nexus between the Bank and its clients, set out its conclusions and recommendations in the last two parts of the Report. It may be convenient to state here the main conclusions and recommendations before dealing generally with the Report in the nest section. It should be noted that the farming representative, while concnrring with his colleagues in their main findings. issued a Xinority Report as to two phases of the Report-the estimate of future losses and the matter of debt adjustment. The main conclusions are twelve in number.

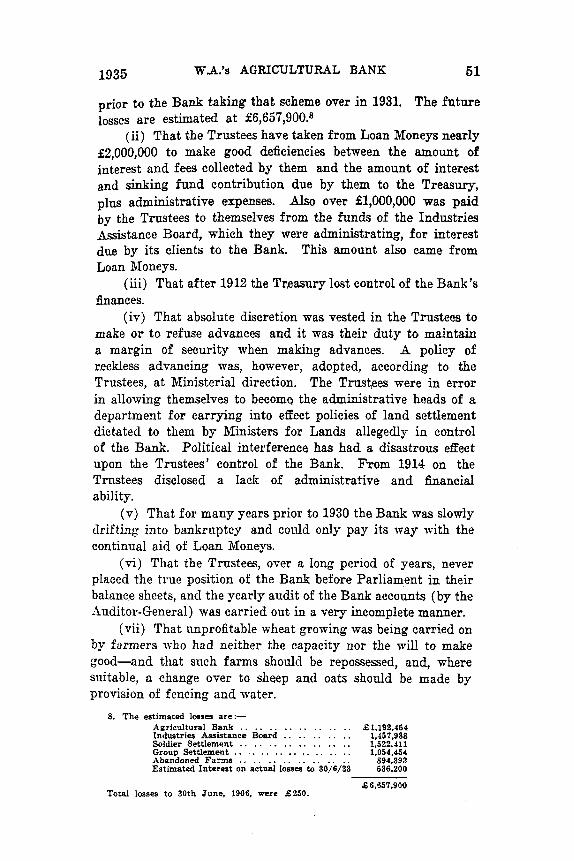

( i ) That large losses of capitnl have already been made by the Bank and allied institutions. In the future, further large losses will have to be faced. The loss to date is estimated at f5,646.700. which includes E4,G95,653 on Group Settlements

1935 W A ’ s AGRICULTURAL BANK 51

prior to the Bank taking that scheme over in 1931. The future losses are estimated at f6,657,900.8

(ii) That the Trustees have taken from Loan Moneys nearly f2,000,000 to make good deficiencies between the amount of interest and fees collected by them and the amount of interest and sinking fund contribution due by them to the Treasury,

Also over €1,000,000 was paid by the Trustees to themselves from the funds of the Industries Assistance Board, which they were administrating, for interest due by its clients to the Bank. This amount also came from Loan Moneys.

(iii) That after 1912 the Tr,easury lost control of the Bank’s finances.

(iv) That absolute discretion was vested in the Trustees to make o r to refuse advances and it was their duty to maintain a margin of security when making advances. A policy of r,eckless advancing was, however, adopted, according to the Trustees, at Ministerial direction. The Trustees were in error in allowing themselves to become the administrative heads of a department for carrying into eEect policies of land settlement dictated to them by Ministers for Lands allegedly in control of the Bank. Political interference has had a disastrous effect upon the Trustees’ control of the Bank. From 1914 on the Trustees disclosed a Iack of administrative and financial ability.

(v) That for many years prior to 1930 the Bank was slowly drifting into bankrnptcy and conld only pay its may with the continual aid of Loan Noneys.

(vi) That the Trustees, over a long period of years, never placed the true position of the Bank before Parliament in their balance sheets, and the yearly audit of the Bank accounts (by the Auditor-General) was carried out in a very incomplete manner.

(vii) That unprofitable wheat growing was being carried on by farmers who had neither the capacity nor the will to make good-and that such farms should be repossessed, and, where suitable, a change over to sheep and oats should be made by provision of fencing and water.

administrative espenses.

8. The estimated losses are:- Agricultural Bank . . . . . . . . . . . . . . . . € 1.192.454 Industries Assistance Board . . . . . . . . . . 1.i57.988 Soldier Settlement . . . . . . . . . . . . . . . . 1,522,411 Group Settlement . . . . . . . . . . . . . . . . . . 1,054,454 Abandoned Farms . . . . . . . . . . . . . . . . S94.393 Estimated Interest on actual losses to 30/6/33 536.200

B 6,667,900 Total losses t o 30th June, 1906, were €250.

52 THE ECONOMIC RECORD JUNE

(viii) That the amounts due to the Bank by many clients are f a r in excess of the real value of the properties, and that such debts should be adjusted.

( i s ) That the Trustees had undertaken too much work, and overloaded themselves with detail, thereby neglecting the finance and organization of the Bank, which should have been their especiaI care. That new management is required and complete reorganization is essential.

(s) That the cost of administering the Bank is excessive. (si) That all political interference in the management of

the Bank and the control of its policy must be abolished. (sii) That the provision of seasonal credit by the Industries

Assistance Eoard v a s a costly mistake and should be dis- continued as soon as possible.

Following these conclusions come the recommenclations, the chief of which are :-

(i) That the present Trustees be retired and control of the Bank be given to a Board of Management, to be free from all political control, to be appointed for 7 years, one member to be representative of the Treasury. Xembers of this Board should devote the whole of their time to the Bank’s business and be removable only on the joint vote of both Houses of Parliament.

( i i j That finance be so arranged that the Bank cannot use principal r e p a p e n t s f o r payment of interest to the Treasury. That each year any deficiency be paid by moneys appropriated by Parliament for that purpose, and that Treasury control of the finances of the Bank be resumed.

(iii) That in view of the unsatisfactory audit in the past by the Ahuditor-General a continuous internal audit be carried out by the Bank’s own audit staff. That the Bank’s balance sheet, profit and loss account, and the Trustees’ Raport, together with a statement of receipts and payments, be laid before Parliament as required by the 1906 Act.

( ivj That the Bank staff should be reorganized and put out- side the Public Service Act. There is need for stricter control and more prompt attention to correspondence, etc.

(v) That discretion should be exercised in making advances both as to the applicant and as to the land.

(vi) That inefficient farmers should be eliminated and good settlers, where adTisable, transferred to other properties, while unproductive wheat lands should be converted to sheep and oats where possible.

W.A.’B AGRICULTURAL BANK 53

(vii) That greater powers should be granted the new Board for the liquidation of securities, including power to spend moneys in making properties repossessed more saleable.

(viii) That accrued interest on many of the Bank’s securities must be written off and the principal moneys be lvritten down.

(is) That the Bank should cease making advances for future land development and pursue a policy of consolidation and liquidation. Advances will have to be made for continuance, changing over to sheep and oats, and croppiug requisites A separate body should be created for the purpose of providing seasonal credit to the Bank’s ~ l i e n t s . ~

(s) That various additional powers should be given the new Board for the continuance of its existing operations and its new policy of collsolidation and liquidation, including power to advance for purchase of sheep, cattle, horses and p ig , and for the construction of Fells and dam.

(xi) That power should be given to the new Board to revalue its securities on the basis of the realsonable capitalization, which a given property can carry, and to release mortgagors from indebtedness, as well as to enter into voluntary arrange- ment with outside creditors for the adjustment of their debts.

(Xi;) That all the assets of the Agricultural Bank, Soldiers’ Settlement Scheme, Industries Assistance Board, Group Settle- ment Board, Finance and Development Board, and special settlements be taken over by the new management which should be given power to borrow by mortgaging such assets or issuing debentures charged upon them.

Such are the main conclusions and recommendations led up to by the previous parts of the Report, which is given general consideration in the next section. They evoked Replies from the Trustees and from the Auditor-General. These m-ere, hom- ever, so weak and ineffective in the face of the position disclosed that they might as well never have been published. The Trustees’ Reply confirmed the conclusion of the Commission that the Trustees had Pelt themselves bound to carry out Ministerial policy. The inescapable facts were that a t the time when the Commission reported the 12,838 accounts of the Bad- showed a total indebtedness of over €16,000,00010 of which it mas estimated that over €6,000,000 mould be lost in addition to the large sums already lost. There were 1,215 abandoned farms, and of

1035

9. Thin haa not no far (March. 19%). been done. 10. Of this i!13,700.000 rr!DmIentl D n n C i D d outstanding and €2,300,000 rapre-

scnta inbraat outltanding.

54 THE ECONOMIC RECORD JUNE

the farmers still on the land many would never, in the opinion of the Commission, make good. It mould appear that whether the losses escezd or fall short of the estimate depends upon the movement of Theat prices. In any case the figure must be a v e v high one. The Conimission discovered that, altogether, f35,251,661 of State money had been advanced to the farmers of Western Australia through the medium of the Agricultural Bank, Industries Assistance Board, Soldiers’ Settlement Scheme and Group S:ttlement. Practically dl this money has been advanced since 1906. Later, when dealing with Disabilities, the Commissioners rather naively open their treatment with the remark : “The main disability of the Agricultural Bank clients is want of money.”

(b) The Report opens b r stating the position in general t e r m n “ T h e financial position of the Agricultural Bank is iilarrning ” because “the Trustees have, for some twenty years, in order to meet the commitments of the Bank, been drawing upoii capital and,‘or losn moneys to make up deficiencies. ” After rejecting the excuses of the Trustees that if the present position of the Bank is attributable to a mistaken policy of land settlement, they were merely carrying out the policy dictated to them by Parliament, the Commission declares: “new management is required. ” They also dismiss the allegation of the Trustees, that in so far as the Bank’s position is attribut- able to the fall in wheat prices, the Bank’s affairs were in no worse position in respect of farming advances in the State than those of other financial institutions (i.e., the private Bank). The t axpap- , observes the Commission, is vell entitled to ask what it has cost the State to establish, or attempt to establish, the farmers on the land through the ageucy of the Agricultural Bank. He had, under the Rank Act, certain safeguards. These were the exercise of absolute discretion by the Trustees to make or withhold advances as the nature of the security demanded and to maintain a safe margin, the Auditor-General’s esamina- tion of the Bank accounts each year and Parliamentary control of Loan Funds after such examination. But the absolute discretion, which the Commission insists was reposed in the Trustees, was not exercised, the Auditor-General failed in his duty and Parliament was never in a position to know the true facts of land- settlement policy. It appears that the Trustees, as a matter of fact, regarded the clause in the Act authorizing aclvances to tho f u l l vultre of improvements as mandatory rather tnan permissive. After 1912 the sdection of a block of land

1935 W.A.3 AGRICULTURAL BANK 55

under the aegis of the Lands Department was treated as carrying \ ~ t h it an Agricultural Bank loan. Even though the applicant had neither means, experience, nor aptitude, the policy of development centred round the idea of “ getting the man on to the land. ’’ The Bank was espected to do its share.

The Trustees, say the Commissioners, might have refused t o implement the Government’s policy. What could Parliament ]lave done in that case? It could have refused to vote moneys for the purposes of the Bank, or, in the alternative, have passed legislation making the Bank as the Managing Trustee said It became, a Government Department for carrying out the Government’s policy of land development. The fact may have been overlooke$ by the Commission, and is affirmed in the Trustees’ Reply, that the Bank has been treated as being under the control of the Minister for Lands. Trustees who were unwilling to carry out a given policy could soon be replaced by those who would be less independent. At the conclusion of the General Report me read: “ There appears to be something radically wrong with the administration of the Bank.” It is more than hinted that the Bank has outlived its usefulness.

We may agree with the Commissioners when they describe the Forrest measure of 1894 as well-conceived and the policy as an admirable and sound one. The 1912 amendment is styled

revolutionary,” changing the character of the Bank from an improvement bank into a mortgage bank. I n spite of the changes which Parliament made in 1912 it never intend&, comment the Commissioners, to interfere with the discretion of the Trustees in making advances. They were expected to maintain a fair margin between advances and the value of the security just as any private banker would do. The difference between an improvement bank, which the Agricultural Bank on its credit foncier fonndation undoubtedly was, and the mortgage bank, which, it is contended, the 1912 legislation aimed at, appears to lie in this. On the one hand, me have long term credit advanced against the security of the land itself and intended to assist its economic development. On the other, we have seasonal credit issued against a more personal security- the prospects of the borrower sometimes reinforced by a crop lien-and intended to facilitate the current farming operations. The former is to be paid by instalments over a long term, the latter out of the crop and/or stock proceeds. In the early days of the Agricultural Bank the borrower was expected to have some means of his own and be capable of making his own

& L

56 THE ECONOMIC RECORD JUNE

arrangements for seasonal supplies. m i e n the settlement of men without means began, the problem became a twofold one. Greater care was necessary in obseriing a safe margin f o r the advance. The Bank, however, carried on, in form a t least, as an improvement b2nk,11 but soon beelme, ns the Managing Trustee admitted, ‘a philanthropic institution. ” The change made was from a policy whereby a settler built up a farm for himself with the niinimum of capitalization (as during the period, 1895-1906) to one of “liberalization’-acceleration with really no limit to the amount to be advanced in one year. Clients mere invited t o apply for more money for additional clearing- to create emplojment in acute times when thousands of men in the cities were workless. “Had the Bank,” remarks the Commission, “not been a State instrumentality it n-odd have been forced into liquidation long ago.”

The Trustees are strongly censured for continuing to advance large sums to open new accounts during the greater part of n period %-hen they were using principal repayments and loan moneys (i.e., capital) to make up the deficiency in interest which they could not collect from their clients. Since 1914 the Trustees have taken from the capital of the Bank an average yearly sum of €104,391 (€1,983,436 in all) t o make np deficien- cies. The Commissioners describe the situation: ‘‘ a continual drift in collection (of interest) yet a progressive policy of advances.” From 1912 onwards the operations of the Bank gathered speed. Until 1929 the Bank’s policy reflected an obsession for expansion. It was in the opinion of the Commis- sion a negation of the cardinal principle upon which the Bank was founded. The Bank, ‘ I becoming the willing instrument of reckless governmental policies of land development, encouraged extravagance in its clients, correspondingly increased its own difficulties, and created a burden of capitalization which the industry cannot c q . ”

Thi l e the lax control of the Trustees is regarded as contributing greatly to the Bank’s present financial condition, the main cause is found in the policy of development of the wheat areas. Two periods of development are indicated; in the first, a cautious policy, founded on the experience gained from pioneering new lands, was pursued; the second period was one of “boom”-rush of survey and classification and indiscriminate allotment of advances t o applicants. The Com- missioners think that even had there been no collapse in Theat

11. Of the total amount of over €9,000,000 expended to 30/6/33. nearly P 7,250.000 was spent upon improvements.

1935 W A ’ s AGRICULTURAL BANK 57

prices the operations o€ the Agricultural Bank would have resulted in considerable loss to the State. The economic development of Western Australia, it is said, owing t o the absence of a uniform quality of land, demanded the closest consideration of State instrumentalities. This attention was not given, with resultant loss to the State.

The Commission says: “From the year 1913 onn-arLs the Eank never paid its way. Ca t we find the Trutees, oblivious of the Bank’s financial affairs, taking on the control of millions oQ money for the Indnstries Assistance Board and Soldier Settlement.” As the same financial muddle is found in connec- tion with Bank, Board and Soldier Settlement, the Commissioners are forced to the canclusion that the Trustees had not the capac- ity to do the work. The Trustees were overwhelmed by a mass of detail and routine matters which should never have bwn referred to Head Office.

IV Future policy in reference to the Bank’s affairs is disclosed

in the recently-enacted Agricultural Bank Act 1934 which embodies the main recommendations of the Royal Commission. 4 brief outline of the Act is now given.

All previous legislation, including the Act of 1906, is repealed. The measure then constitutes the management, of the Bank a body corporate nnder the name, “ The Commissioners of the Agricultural Bank of Western Australia.” These will be t h e e in number-one being the Under-Treasurer o r his deputy, the remaining two members being appointed by the Governor, to hold office for seven years and to be eligible for re-appoint- ment, to devote the whole of their time to the Bank‘s business. The Governor may suspend any Commissioner appointed by hini for misbehavior or incompetence. It is provided. however, that the grounds of suspension shall be put before Parliament within seven days. The votes of both Houses then determine the fate of the suspended Commissioner. If the resolution that he be dismissed from office be not passed by both Houses, he is restored to office automatically. This seems a rather involved way of providing that he shall not forfeit office save on the votes of both Houses.

The Commissioners are empomered to take over the assets and liabilities of the Bank and its allied institutions and all special settlements. The Governor may, on the Treasurer’s recommendation, reduce the Bank’s indebtedness by sums which, after investigation and audit, are found to represent lost capital

58 THE ECONOMIC RECORD J U N E

of the Bank. The same power is given t o suspend liability towards the Treasury and relief is provided from interest payments in respect of such indebtedness whether reduced or suspended. All moneys received by the Commissioners under the new Act are to be paid into a special account a t the Treasury on which they alone may draw. They are given power to borrow money by issue of debentures deemed to be a charge on the assets and revenue of the Commissioners. The amount is limited in the first instance to €1,000,000 with a proviso that they may appl3- for leave to borrow additional amounts when furnish- ing their annual report to the JIinister. They are tinder a liability to make regular sinking fund payments even when other liabilities towards the Treasury may be suspended. Apart from moneys realised by issue of debentnres, Parliament may appropriate moneys to supply funds for the Bank’s operations. Various provisions safeguard the legal position of the debenture holders. Then comes a series of clauses dealing with the position of the Bank staff. They are placed under the immediate control of the Commissioners and excluded from the operation of the Public Service Act. Legislative form is given to the important principle which the Royal Commission found to have been transgressed in the past that no officer or servant of the Com- missioners shall be eligible f o r advances under the Act.

Advances under the new Act are to be made to persons engaged in rural industry, on the security of lands owned and used by them in such industry for the following purposes:-

(a) The effecting of permanent improvements to increase the productivity of the land.

(b) The purchase of machinery, stock and/or plant to work the said lands.

( c ) To enable the applicant to use the said lands in another branch of rural industry (e.g., transfer from wheat- gron<ng to sheep and oats).

(d ) To enable the applicant to erect a dn-elling house on the said laud.

(el To conserve o r protect the Bank’s securities. But, before making any advance the Commissioners have

( i ) That the advance is required for all or any of such purposes.

( i i ) Thar; the applicant has reasonable prospects of developing his lands successfully, and

(iii) That he is deserving of such advance.

ta be satisfied :-

W.A.'s AGRICULTURAL BANK

If this provision had been inserted in the 1912 Act and acted upon it might have saved the State many thousands of pounds.

No advance is to exceed €2,000. Borrowers already indebted to the Bank are entitled to receive the dif€erence between their existing debt and f2,000. Where their debt exceeds f2,000, they lllay receive further advances, where the Commissioners think it necessary, to facilitate a transfer, either to another form of rural industry which mill enhance the value of the security, or to other lands of the Commissioners, or for the purchase of machinery, stock and/or plant. In such cases, advances are made with the approval of the Governor only.

A margin of secnrity is established since the Act limits the advance to 70 per cent. of the reasonable cost of improve- ments in the case of improvement loans, and the value or reasonable cost of the stock or machinerr, etc., in the case of other loans. Advances may be made in progress payments, and if the Commissioners are not satisfied that the moneys advanced are being applied to the proper purpose, or are not being carefully and economically expended, they may refuse further instalments and call up the loan a t once. This is also a provision which might have been very useful in previous Acts if strictly enforced. A mortgage over the land and improvements must be given to the Commissioners. Repapen t s are to be in half-pearly instalments, either equal or graduated, according to the determination of the Commissioners, and to commence not later than 10 yvrs after the date of the advance. The period for repayment is not to exceed 20 years and the borrower may pay off sooner if he so wishes. Interest is payable half-yearly a t a rate fixed by the Commissioners who are given power t o r d u c e the rate at their discretion.

An important section which met with considerable opposition in the House is the 51st xhich gives a statutory lien over crops, wool, wool-clip, butter fa t produce, and the increase in progeny of all live stock, There any interest is due by borrower or where an instalment of principal or interest has been refunded to the borrower (porer to do this is given by a succeeding section) or where advances have been made for other purposes than improvement or purchase of machinery, plant or stock. This lien takes priority eyer all other encumbrances and is for one year's interest where more than that amount of interest is owing. Despite the assertion of the main sub-section that it is a statutory charge in prioritr to all othcr encumbrances

1935

60 THE ECONOMIC RECORD JUNE

it must give place, according to later sections, t o any charge under the Industries Assistance Act and also, as the result of an amendment in Parliament, to the rights of holders of bona fide registered stock mortgages. Power is given to the Commissioners to waive such charge where it may appear desirable. This would be in cases where the stock o r machinery firms refuse further transactions because of the lien.

So that the Commissioners may enforce their securities vari- ous additional powers are given, including a power of distress, il

power of sale, po\yer to maintain the property and to crop and work the same, and to spend money for such purposes, which sums, with interest, shall be payable by the borrower and become a charge on the property. Improvements uiay be effected to make the land more saleable. There is also poll-er given t o allow time for payment of purchase money, to lease, and to enter into share cropping agreements. Money map be advanced to the lessees, and repayment thereof with interest shall consti- tute a charge on the fee simple or other estate of the original borrorer. Power is given to eject forcibly borrowers who are recalcitrant.

The Commissioners may, with the consent of the Treasurer, where a borrower is unable to meet his indebtedness and interest suspend or postpone payment of the whole or any part of the indebtedness f o r such period as theF may think fit, and during such period the borrower is relieved from payment of interest. Such suspensions or postponements are to be reviewed from time to time. at least once in every two years. The Commissioners may, as a condition of such suspension or postponement, require the other creditors of the borrower to enter into a mutually binding scheme or arrangement f o r the suspension o r postponement of their claims on such terms and conditions as the Commissioners may consider reasonable.

Pow-er is given the Commissioners to write of€ and reduce the aggregate indebtedness of any borrower to such sum as the security may be reasonably expected to carry. This can be done where :-

( a , The debt on all accounts exceeds the value of the security, and

( b ) there is no reasonable likelihood of the security appreciating in valrie and the borrower being able t o meet his indebtedness, and

( c j the borrower is deserving of assistance on his past record.

1935 W.A.3 AGRICULTURAL BANK 61

The same power is given to the Commissioners as in the case of suspension o r postponement to require other creditors to enter into a mutually binding scheme, this time for debt adjns:ment. a s a condition of a reduction and adjustment.

The concluding sections require the Commissioners to have prepared and placed before Parliament proper balance sheet.;, revenue accounts, and analysed cash accounts showing receipts and payments. TVhile provision is made for a continual internal audit, the Auditor-General is required to appoint an officer to make audits, and the reports of his officer, with his own coin- ments, are to be placed before Parliament. In addition to these requirements the Commissioners have to furnish an nmual report o€ their operations, also to be laid before Parliament.

While the Act appears to he an honest attempt on the part of the Collier Government to give effect to the recommendations of the Royal Commission and to deal with a very difficult situation due to blundering policy in the past, there are still signs that the Bank may not be so easily freed from political control. It is under a Minister, presumably the Minister for Lands, and, in the case of the Minister causing the suspension of a Commissioner, voting in the Houses might follow party lines. Apart from this weakness in the new Act the appointment of a politician to the important position of Managing or Chief Commissioner hardly awakens that confidence in the freedom from political control in the future of the Bank which is most desirable.

GORDON TAYLOR. University of Melbourne.