welcome. workshop objectives introduce introduce educate educate illustrate illustrate

TRANSCRIPT

Welcome

Workshop ObjectivesWorkshop Objectives

IntroduceIntroduce EducateEducate IllustrateIllustrate

Our CommitmentOur Commitment

Provide sound financialProvide sound financialinformationinformation

Help you identify goalsHelp you identify goals Offer complimentaryOffer complimentary

consultationconsultation

Evaluation FormEvaluation Form

About Your WorkbookAbout Your Workbook

Informative Informative

graphicsgraphics

Wide marginsWide margins

Helpful Helpful

exercisesexercises

4

Your Financial FutureYour Financial Future

Lifetime Earnings

$ 40,000 $ 70,000 $ 100,000per year per year per year

10 years $ 480,244 $ 840,427 $1,200,611

20 years $1,191,123 $2,084,466 $2,977,808

30 years $2,243,398 $3,925,946 $5,608,494

Assumes a 4% annual salary increase

Your Financial Your Financial FutureFuture

Overcome obstacles to successOvercome obstacles to success Practice sound financial managementPractice sound financial management

Lack of DirectionLack of Direction

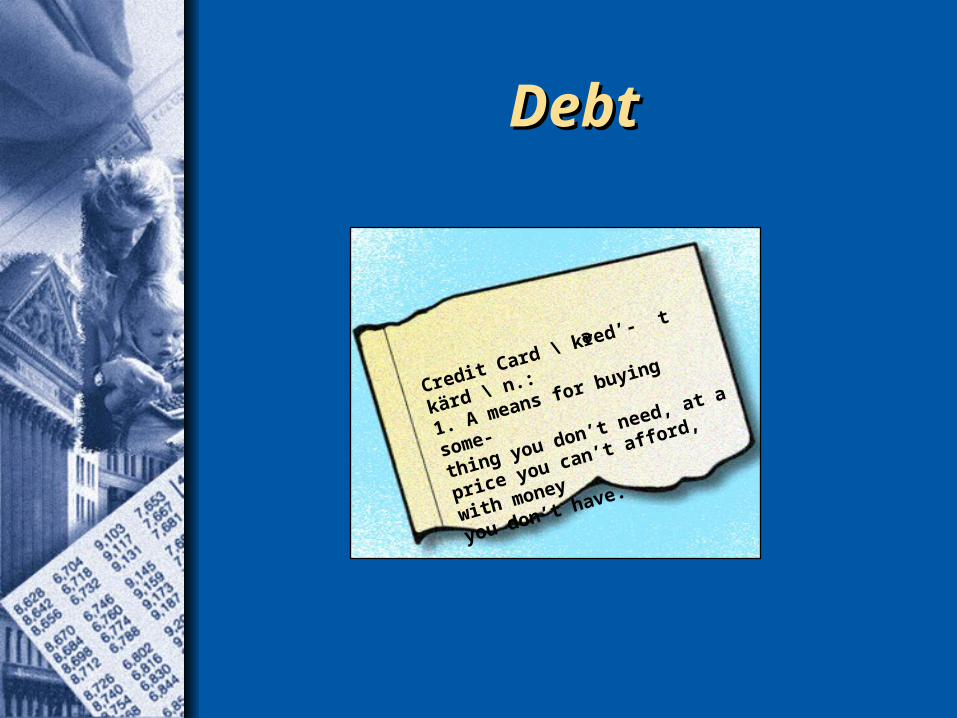

DebtDebt

Credit Card \ kred’- t kärd \ n.:

1. A means for buying some-

thing you don’t need, at a price

you can’t afford, with money

you don’t have.

e

InflationInflation

The Rule of 72The Rule of 72

72Inflation Rate

6% Inflation72 ÷ 6 = 12 years

4% Inflation72 ÷ 4 = 18 years

6

TaxesTaxes

The average The average person will person will work until work until late April to pay late April to pay all federal, state, all federal, state, and local taxes.and local taxes.

Tax Freedom DayTax Freedom Day

Source: Tax FoundationSource: Tax Foundation

Yield After Taxes Yield After Taxes and Inflationand Inflation

Investment $ 10,000

8% interest + 800Taxes (27% tax bracket) – 216Net interest $ 584

Total after taxes $ 10,584

Adjusted for inflation (4%) 1.04

Net after taxes and inflation $ 10,177

Net return = 1.77%

6

What Is Financial What Is Financial Management?Management?

E

N

W

S

ESTATE PLANNING

INVESTMENTPLANNING

RETIREMENTPLANNING

TAX PLANNINGCASH

MANAGEMENT

RISKMANAGEMENT

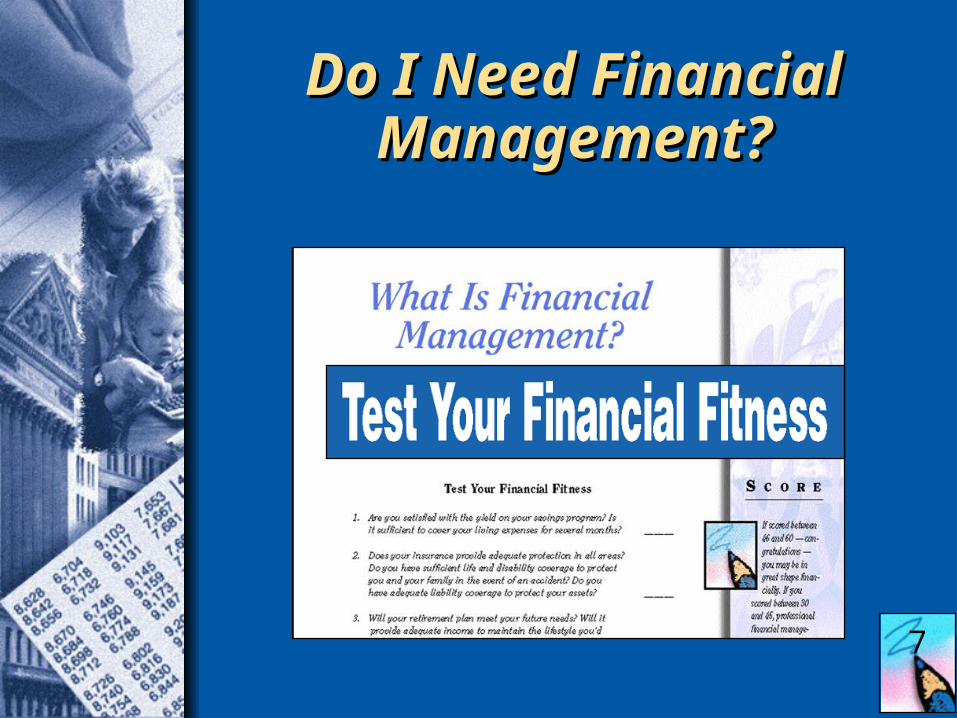

Do I Need Financial Do I Need Financial Management?Management?

7

Cash Cash ManagementManagement

CASHMANAGEMENT

Cash FlowCash Flow

Total Income $ ________

Total Expenses – $ ________

Net Cash Flow = $ ________

8

Liquidity FundLiquidity Fund

Savings = Liquidity Ratio Monthly Expenses

Reposition Assets Reposition Assets and Liabilitiesand Liabilities

Risk Risk ManagementManagement

RISKMANAGEMENT

Risk ManagementRisk Management

LifeLife DisabilityDisability Medical andMedical and

long-term carelong-term care AutoAuto HomeHome LiabilityLiability

Protect YourselfProtect Yourself

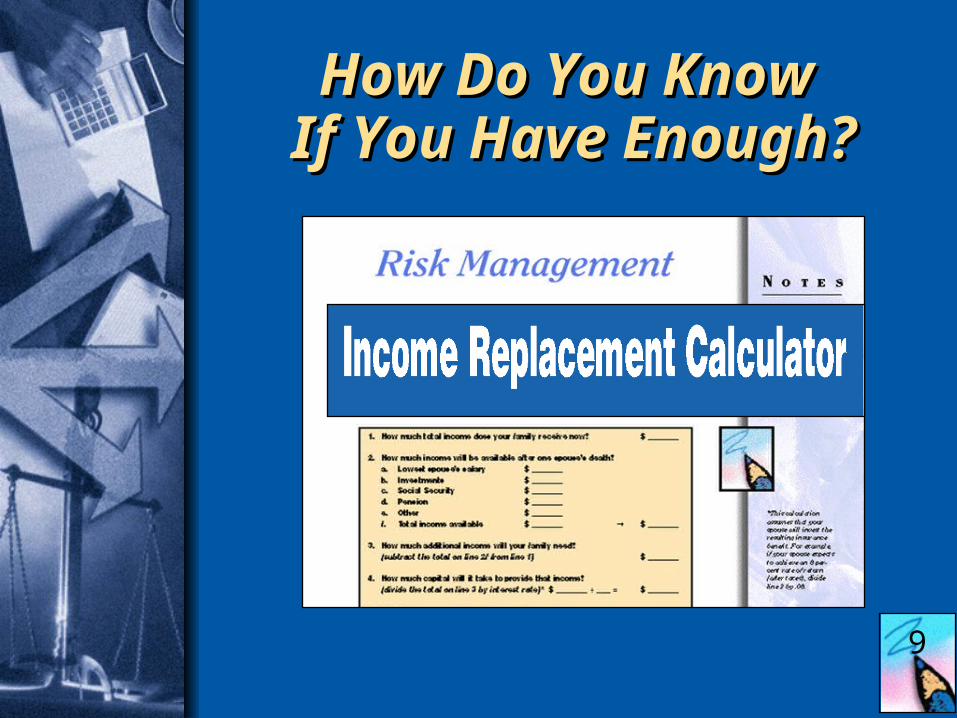

How Do You Know How Do You Know If You Have Enough?If You Have Enough?

9

IncomeIncomeReplacement CalculatorReplacement Calculator

1. Total income now $ 80,000

2. Total income available $ 40,000

3. Additional income needed $ 40,000

4. Capital required $500,000

5. Additional cash requirements $125,000

6. Life insurance needed $625,000

Mr. and Mrs. Harrick

Investment Investment PlanningPlanning

INVESTMENTPLANNING

Investment ObjectivesInvestment Objectives

GrowthGrowth

SafetySafety

IncomeIncome

The Investment SpectrumThe Investment Spectrum

CASHCASHEQUIVALENTSEQUIVALENTS

FIXEDFIXEDINTERESTINTEREST BONDSBONDS STOCKSSTOCKS

HIGHER RISKHIGHER POTENTIAL RETURN

LOWER RISKLOWER POTENTIAL RETURN

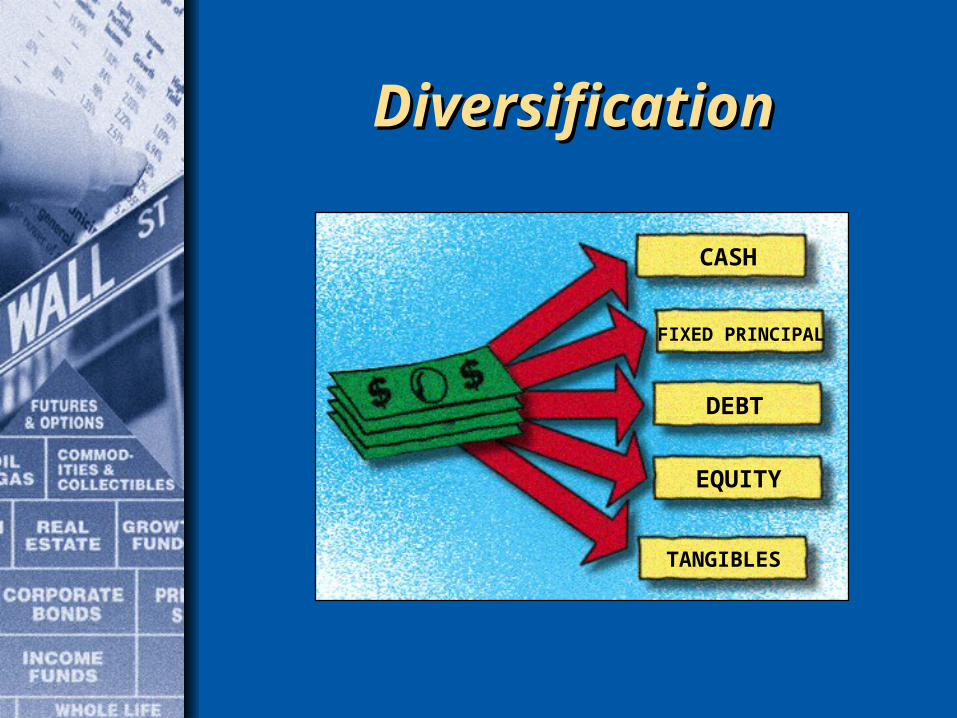

DiversificationDiversification

CASH

FIXED PRINCIPAL

DEBT

EQUITY

TANGIBLES

Diversification ExampleDiversification Example

BILL JILL

$50,000$50,000 $50,000$50,000

Diversification ExampleDiversification Example

Bill and Jill after 20 years

Bill 7% $193,485

Jill (loss) $ 05% $ 26,5337% $ 38,697

10% $ 67,27512% $ 96,463

Jill’s Total $228,968

Difference = $ 35,483

This is a hypothetical example. Actual results will vary.This is a hypothetical example. Actual results will vary.

College PlanningCollege Planning

• Combined income: $48,000

• One child: Robby, age 5

• College cost: $10,000

Mr. and Mrs. Thompson

College SavingsCollege SavingsCalculatorCalculator

• Estimated future collegecost: $107,000 for 4 years

• Annual savings required:$5,671 a year for 13 years

Mr. and Mrs. Thompson

12

Dollar Cost AveragingDollar Cost Averaging

Dollar Cost AveragingDollar Cost Averaging

PRICE PER SHARES

INVESTMENT SHARE PURCHASED

This is a hypothetical example. Actual results will vary.This is a hypothetical example. Actual results will vary.

MONTH 1 $ 200 $ 10.00 20MONTH 2 $ 200 $ 8.00 25MONTH 3 $ 200 $ 5.00 40MONTH 4 $ 200 $ 8.00 25MONTH 5 $ 200 $ 10.00 20

TOTAL $1,000 130 SHARES

AVERAGE PRICE: $8.20AVERAGE COST: $7.69

Tax Tax PlanningPlanning

TAX PLANNING

Tax StrategiesTax Strategies

Tax DeferralTax Deferral

Mr. Washington

• 45 years old

• $70,000 salary

• $85,000 investment portfolioInterest income: $6,800

Taxes: $2,040

Tax DeferralTax Deferral

Mr. Washington

Taxable (30% tax bracket)

Tax deferred

Tax deferred after taxes

5 years 10 years 15 years 20 years

$111,619

$124,891

$145,574

$183,507

$192,476

$269,637$252,754

$396,185

$302,827

Mortality and expense charges, sales charges, and administrative fees are not taken into account and would reduce the performance shown if they were included.

$85,000 initial portfolio8% annual rate of return

Tax-Free InvestmentsTax-Free InvestmentsCalculating the Taxable Equivalent YieldCalculating the Taxable Equivalent Yield

13

EXAMPLEEXAMPLE EXAMPLEEXAMPLE YOU YOU

1.1. Take the tax-exempt yieldTake the tax-exempt yield 7% 7% 7% 7% _____%_____%

2.2. Your marginal federalYour marginal federal

tax ratetax rate 27% 27% 35% 35% _____%_____%

3.3. Subtract your rate fromSubtract your rate from

100% (1.00 – line 2)100% (1.00 – line 2) 73% 73% 65% 65% _____%_____%

4.4. Taxable equivalent yieldTaxable equivalent yield 9.59%9.59% 10.77%10.77% _____%_____%

(line 1 ÷ line 3)(line 1 ÷ line 3)

Retirement Retirement PlanningPlanning

RETIREMENTPLANNING

Sources ofSources ofRetirement IncomeRetirement Income

Social SecuritySocial Security

Employer-sponsored plansEmployer-sponsored plans

Personal savings andPersonal savings andinvestmentsinvestments

Other Retirement Other Retirement Planning ConsiderationsPlanning Considerations

Distribution optionsDistribution options

Tax considerationsTax considerations

Changing JobsChanging Jobs

Ms. Martin

Total distribution amount $40,000

20% withholding – $ 8,000

Early withdrawal penalty – $ 4,000

Additional income tax due – $ 2,800

After-tax distribution $25,200

RolloverRollover

Ms. MartinTax-deferred growth @ 8%

$40,000

$58,773

START 5 10 15 20 25 30

$86,357

$126,887

$186,438

$273,939

$402,506

YEARS

Mr. and Mrs. Tucker

Retirement Retirement DistributionDistribution

Annuity

• Single-life annuity

• Joint and survivor annuity

Mr. and Mrs. Tucker

Increasing YourIncreasing YourPensionPension

$1,000

$1,200

$200

SurvivingSpouse

DeathBenefit

Mr. and Mrs. Tucker

Lump-sum distribution — $220,000

Tax alternatives

Ordinary income tax $58,500

10-year averaging $42,100

Capital gains + 10-year averaging $38,300

Potential tax savings $20,200

RetirementRetirementDistributionDistribution

Estate Estate PlanningPlanning

ESTATE PLANNING

John WayneJohn Wayne

Estate PlanningEstate PlanningConcernsConcerns

DistributionDistribution WillsWills TrustsTrusts GiftingGifting ProbateProbate Taxes and feesTaxes and fees

Reducing Reducing Estate TaxesEstate Taxes

Mr. and Mrs. Hudson

• Two grown children

• Estate value: $1,500,000

• Estimated tax: $210,000

Reducing Reducing Estate TaxesEstate Taxes

Assets Trust

A Trust

Death ofSecondSpouse

Children

B Trust

Death ofFirst

Spouse

Mr. and Mrs. Hudson — Estate value: $1.5 million

ESTATE TAX SAVINGS: $210,000ESTATE TAX SAVINGS: $210,000

Reducing Reducing Estate TaxesEstate Taxes

Mr. and Mrs. Hudson — Estate value: $2.5 million

ESTATE TAX SAVINGS: $470,000ESTATE TAX SAVINGS: $470,000

Premiums

InsuranceTrust

Children

DeathBenefit

Deathof Second

Spouse

ReviewReview

Cash managementCash management Risk managementRisk management Investment planningInvestment planning Tax planningTax planning Retirement planningRetirement planning Estate planningEstate planning

Financial Financial Management ProcessManagement Process

1.1. Gather informationGather information2.2. Identify objectivesIdentify objectives3.3. Determine present positionDetermine present position4.4. Develop strategiesDevelop strategies5.5. Implement strategiesImplement strategies6.6. Review periodicallyReview periodically

17

Where Do Where Do You Go You Go

from Here?from Here?

Where Do You Where Do You Go from Here?Go from Here?

Do it yourselfDo it yourself Work with othersWork with others

Work with usWork with us ProcrastinateProcrastinate

Evaluation FormEvaluation Form

What to BringWhat to Bring

Thank You