volaris: the leading ultra-low-cost airline serving...

TRANSCRIPT

Volaris: the leading ultra-low-cost airline

serving Mexico, USA and Central America

January 2018

The information ("Confidential Information") contained in this presentation is confidential and is provided by

Controladora Vuela Compañía de Aviación, S.A.B. de C.V., (d/b/a Volaris, the "Company") confidentially to you solely

for your reference and may not be retransmitted or distributed to any other persons for any purpose whatsoever.

The Confidential Information is subject to change without notice, its accuracy is not guaranteed, it has not been

independently verified and it may not contain all material information concerning the Company. Neither the Company,

nor any of their respective directors makes any representation or warranty (express or implied) regarding, or

assumes any responsibility or liability for, the accuracy or completeness of, or any errors or omissions in, any

information or opinions contained herein. None of the Company nor any of their respective directors, officers,

employees, stockholders or affiliates nor any other person accepts any liability (in negligence, or otherwise)

whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in

connection therewith. No reliance may be placed for any purposes whatsoever on the information set forth in this

presentation or on its completeness.

This presentation does not constitute or form part of any offer or invitation for sale or subscription of or solicitation or

invitation of any offer to buy or subscribe for any securities, nor shall it or any part of it form the basis of or be relied

on in connection with any contract or commitment whatsoever. Recipients of this presentation are not to construe the

contents of this presentation as legal, tax or investment advice and should consult their own advisers in this regard.

This presentation contains statements that constitute forward-looking statements which involve risks and

uncertainties. These statements include descriptions regarding the intent, belief or current expectations of the

Company or its officers with respect to the consolidated results of operations and financial condition, and future

events and plans of the Company. These statements can be recognized by the use of words such as "expects,"

"plans," "will," "estimates," "projects," or words of similar meaning. Such forward-looking statements are not

guarantees of future performance and actual results may differ significantly from those in the forward-looking

statements as a result of various factors and assumptions. You are cautioned not to place undue reliance on these

forward looking statements, which are based on the current view of the management of the Company on future

events. The Company does not undertake to revise forward-looking statements to reflect future events orcircumstances.

Disclaimer

2

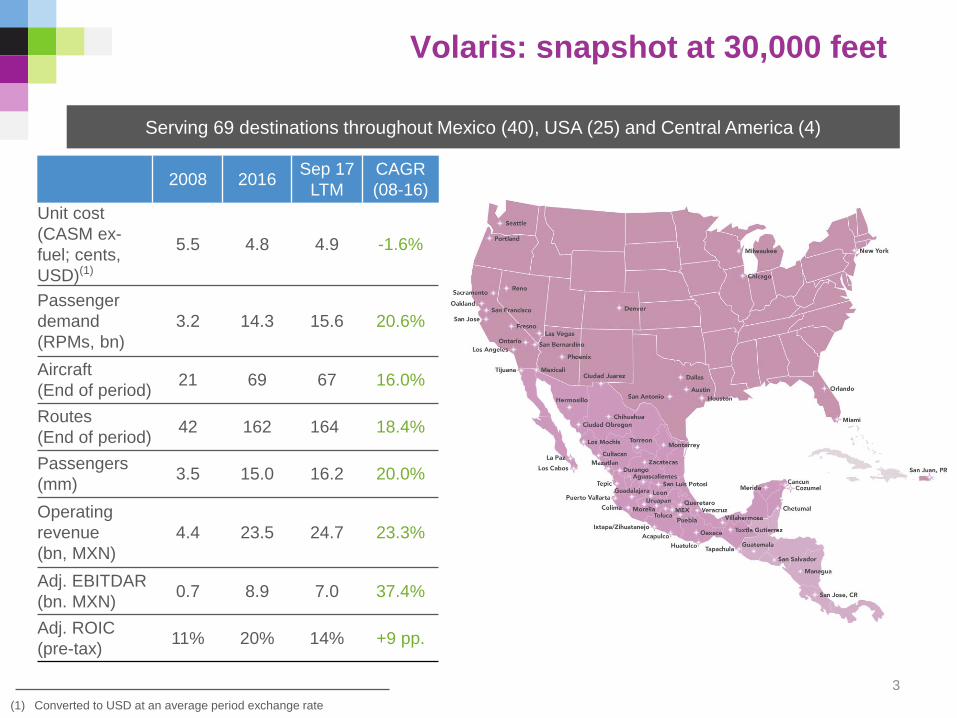

Serving 69 destinations throughout Mexico (40), USA (25) and Central America (4)

(1) Converted to USD at an average period exchange rate

Volaris: snapshot at 30,000 feet

2008 2016Sep 17

LTM

CAGR

(08-16)

Unit cost

(CASM ex-

fuel; cents,

USD)(1)

5.5 4.8 4.9 -1.6%

Passenger

demand

(RPMs, bn)

3.2 14.3 15.6 20.6%

Aircraft

(End of period) 21 69 67 16.0%

Routes

(End of period) 42 162 164 18.4%

Passengers

(mm)3.5 15.0 16.2 20.0%

Operating

revenue

(bn, MXN)

4.4 23.5 24.7 23.3%

Adj. EBITDAR

(bn. MXN)0.7 8.9 7.0 37.4%

Adj. ROIC

(pre-tax)11% 20% 14% +9 pp.

3

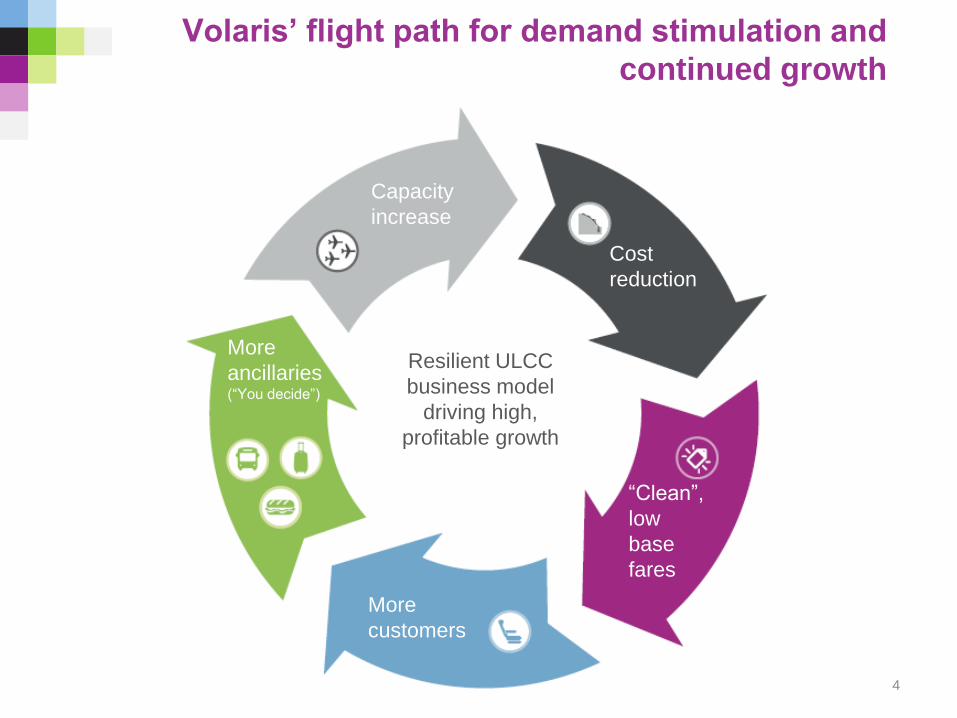

Volaris’ flight path for demand stimulation and

continued growth

Capacity

increase

Cost

reduction

“Clean”,

low

base

fares

More

customers

More

ancillaries(“You decide”)

Resilient ULCC

business model

driving high,

profitable growth

4

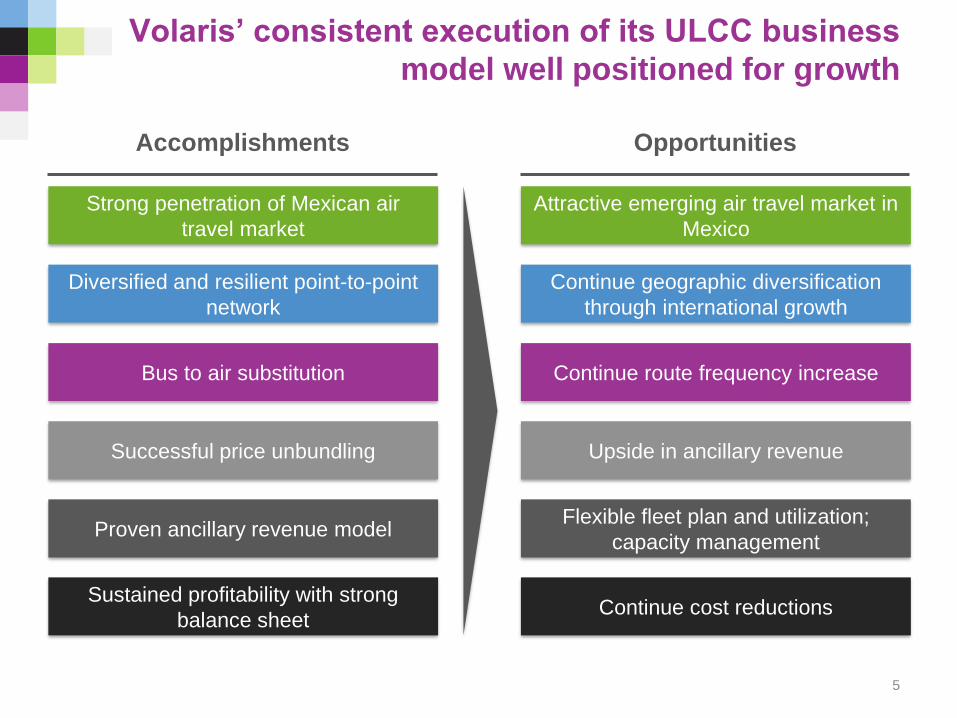

Volaris’ consistent execution of its ULCC business

model well positioned for growth

Diversified and resilient point-to-point

network

Successful price unbundling

Strong penetration of Mexican air

travel market

Proven ancillary revenue model

Bus to air substitution

Upside in ancillary revenue

Continue geographic diversification

through international growth

Attractive emerging air travel market in

Mexico

Flexible fleet plan and utilization;

capacity management

Sustained profitability with strong

balance sheet Continue cost reductions

Continue route frequency increase

OpportunitiesAccomplishments

5

Accomplishments

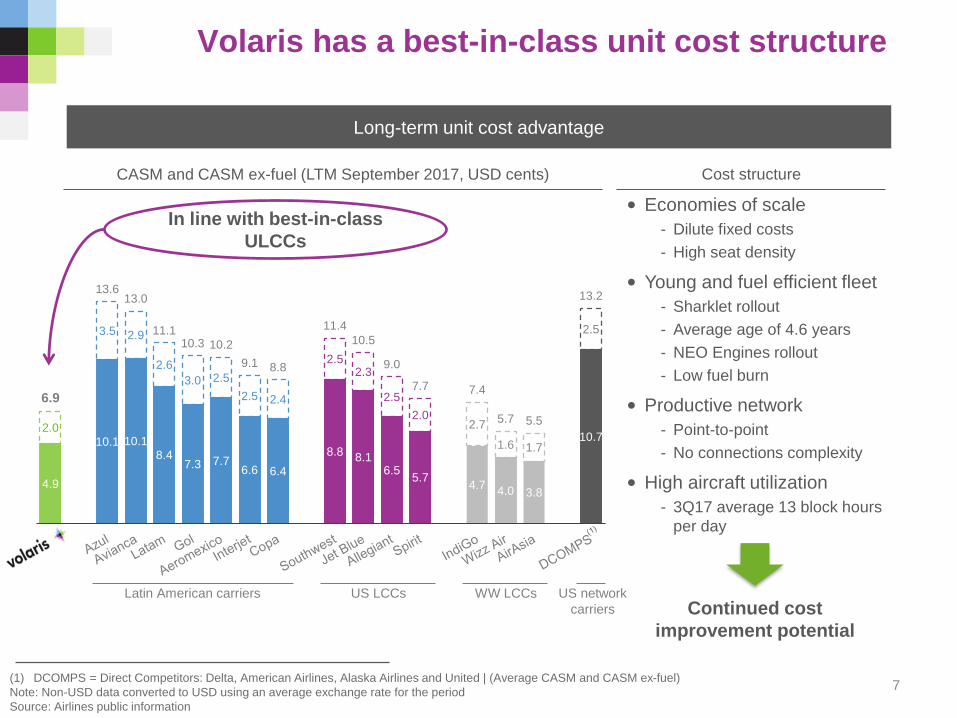

Volaris has a best-in-class unit cost structure

Long-term unit cost advantage

(1) DCOMPS = Direct Competitors: Delta, American Airlines, Alaska Airlines and United | (Average CASM and CASM ex-fuel)

Note: Non-USD data converted to USD using an average exchange rate for the period

Source: Airlines public information

CASM and CASM ex-fuel (LTM September 2017, USD cents) Cost structure

• Economies of scale

- Dilute fixed costs

- High seat density

• Young and fuel efficient fleet

- Sharklet rollout

- Average age of 4.6 years

- NEO Engines rollout

- Low fuel burn

• Productive network

- Point-to-point

- No connections complexity

• High aircraft utilization

- 3Q17 average 13 block hours

per day

Continued cost

improvement potential

7

4.9

10.1 10.18.4

7.3 7.76.6 6.4

8.8 8.16.5

5.74.7

4.0 3.8

10.72.0

3.5 2.9

2.6

3.0 2.5

2.5 2.4

2.52.3

2.5

2.02.7

1.6 1.7

2.5

6.9

13.613.0

11.110.3 10.2

9.1 8.8

11.4

10.5

9.0

7.7 7.4

5.7 5.5

13.2

In line with best-in-class

ULCCs

Latin American carriers US LCCs US network

carriers

WW LCCs

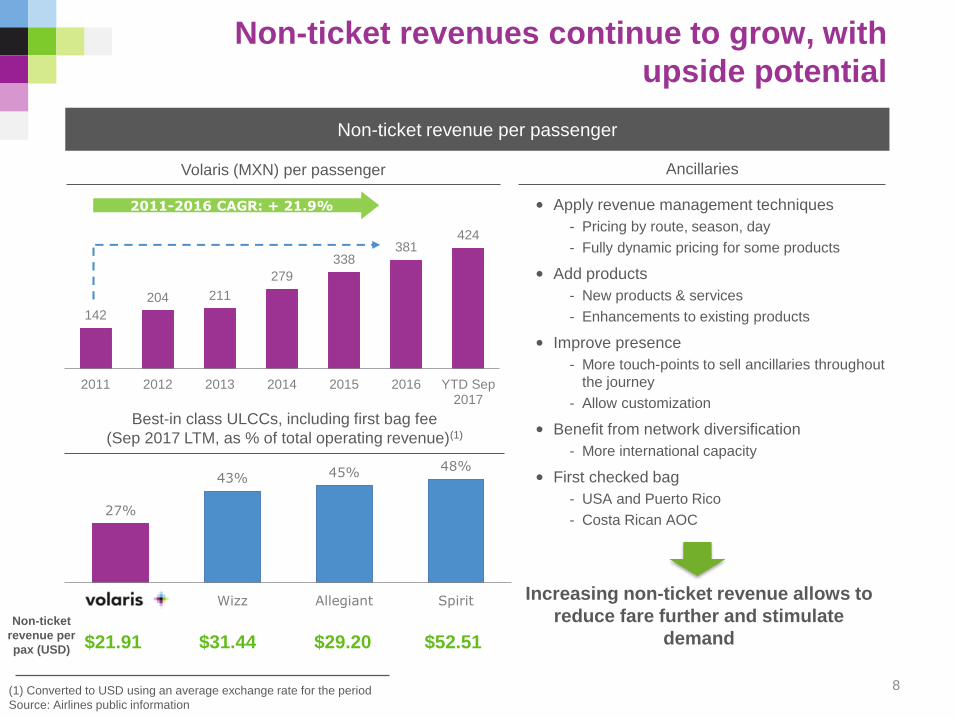

142

204 211

279

338381

424

2011 2012 2013 2014 2015 2016 YTD Sep2017

2011-2016 CAGR: + 21.9%

Non-ticket revenues continue to grow, with

upside potential

8(1) Converted to USD using an average exchange rate for the period

Source: Airlines public information

Non-ticket revenue per passenger

Volaris (MXN) per passenger

Best-in class ULCCs, including first bag fee

(Sep 2017 LTM, as % of total operating revenue)(1)

Ancillaries

• Apply revenue management techniques

- Pricing by route, season, day

- Fully dynamic pricing for some products

• Add products

- New products & services

- Enhancements to existing products

• Improve presence

- More touch-points to sell ancillaries throughout

the journey

- Allow customization

• Benefit from network diversification

- More international capacity

• First checked bag

- USA and Puerto Rico

- Costa Rican AOC

Increasing non-ticket revenue allows to

reduce fare further and stimulate

demandNon-ticket

revenue per

pax (USD) $21.91 $31.44 $29.20 $52.51

27%

43% 45% 48%

Volaris Wizz Allegiant Spirit

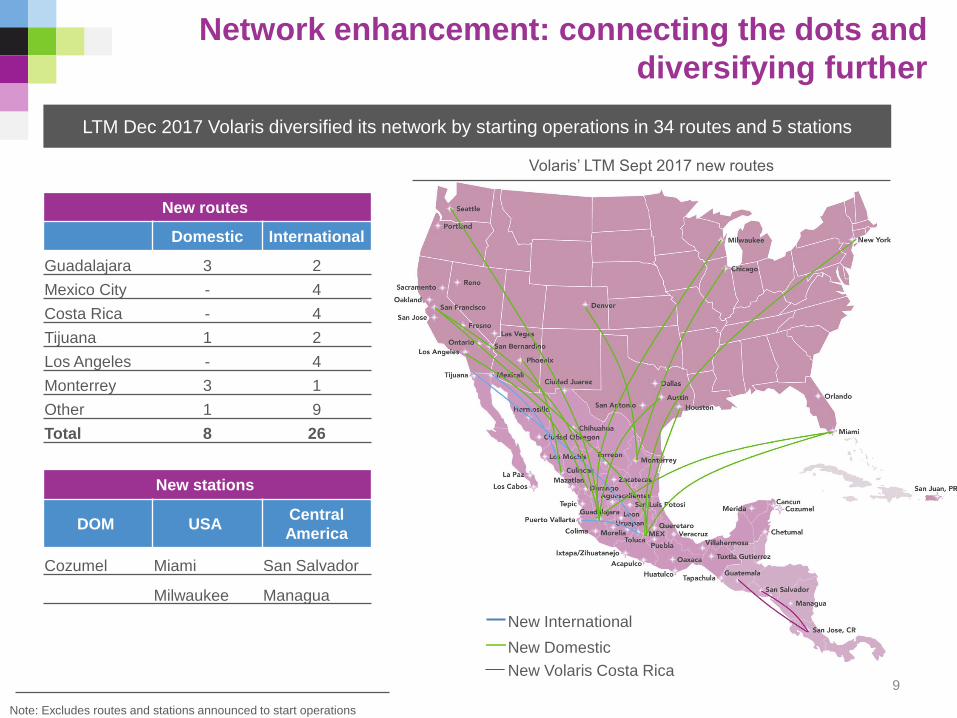

Network enhancement: connecting the dots and

diversifying further

Note: Excludes routes and stations announced to start operations

New routes

Domestic International

Guadalajara 3 2

Mexico City - 4

Costa Rica - 4

Tijuana 1 2

Los Angeles - 4

Monterrey 3 1

Other 1 9

Total 8 26

New stations

DOM USACentral

America

Cozumel Miami San Salvador

Milwaukee Managua

LTM Dec 2017 Volaris diversified its network by starting operations in 34 routes and 5 stations

Volaris’ LTM Sept 2017 new routes

9

New International

New Domestic

New Volaris Costa Rica

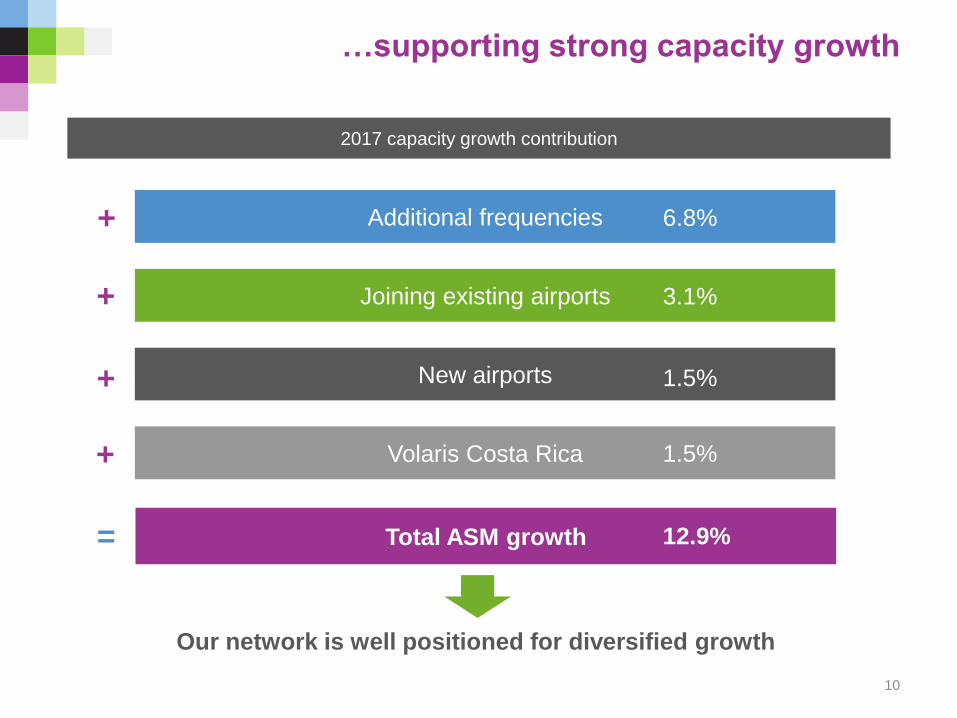

…supporting strong capacity growth

Joining existing airports

Additional frequencies

New airports

6.8%

3.1%

1.5%

Total ASM growth

2017 capacity growth contribution

12.9%

Our network is well positioned for diversified growth

=

+

+

+

Volaris Costa Rica 1.5%+

10

Growth opportunities

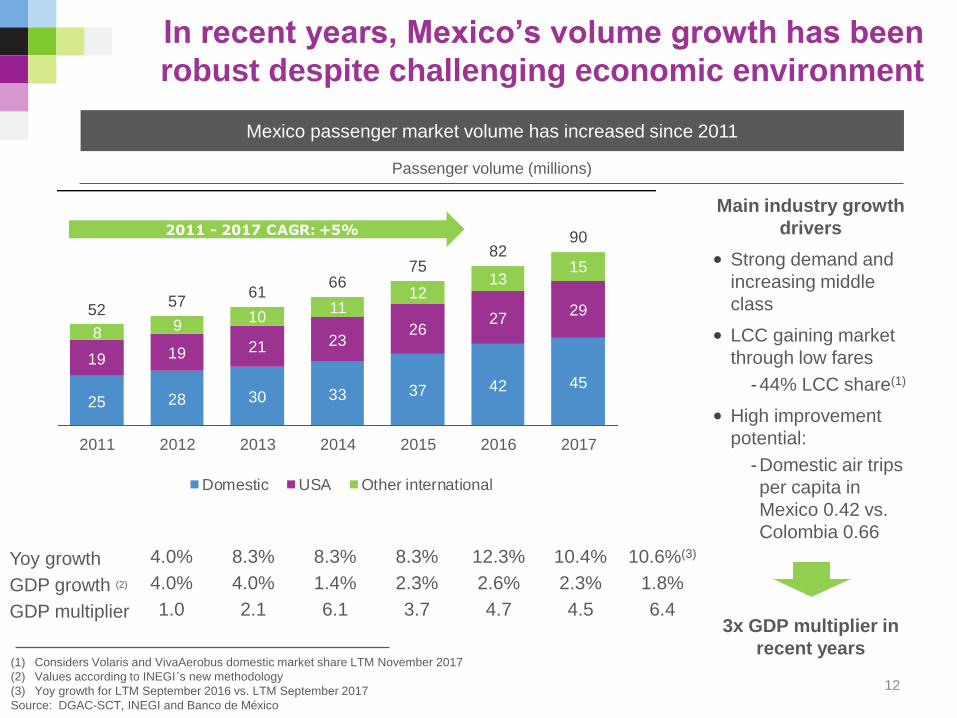

Yoy growth 4.0% 8.3% 8.3% 8.3% 12.3% 10.4% 10.6%(3)

GDP growth (2) 4.0% 4.0% 1.4% 2.3% 2.6% 2.3% 1.8%

GDP multiplier 1.0 2.1 6.1 3.7 4.7 4.5 6.4

In recent years, Mexico’s volume growth has been

robust despite challenging economic environment

(1) Considers Volaris and VivaAerobus domestic market share LTM November 2017

(2) Values according to INEGI´s new methodology

(3) Yoy growth for LTM September 2016 vs. LTM September 2017

Source: DGAC-SCT, INEGI and Banco de México

Mexico passenger market volume has increased since 2011

Passenger volume (millions)

12

Main industry growth

drivers

• Strong demand and

increasing middle

class

• LCC gaining market

through low fares

-44% LCC share(1)

• High improvement

potential:

-Domestic air trips

per capita in

Mexico 0.42 vs.

Colombia 0.66

3x GDP multiplier in

recent years

25 28 30 33 37 42 45

19 19 21 2326

2729

89

1011

1213

15

5257

6166

7582

90

2011 2012 2013 2014 2015 2016 2017

Domestic USA Other international

2011 - 2017 CAGR: +5%

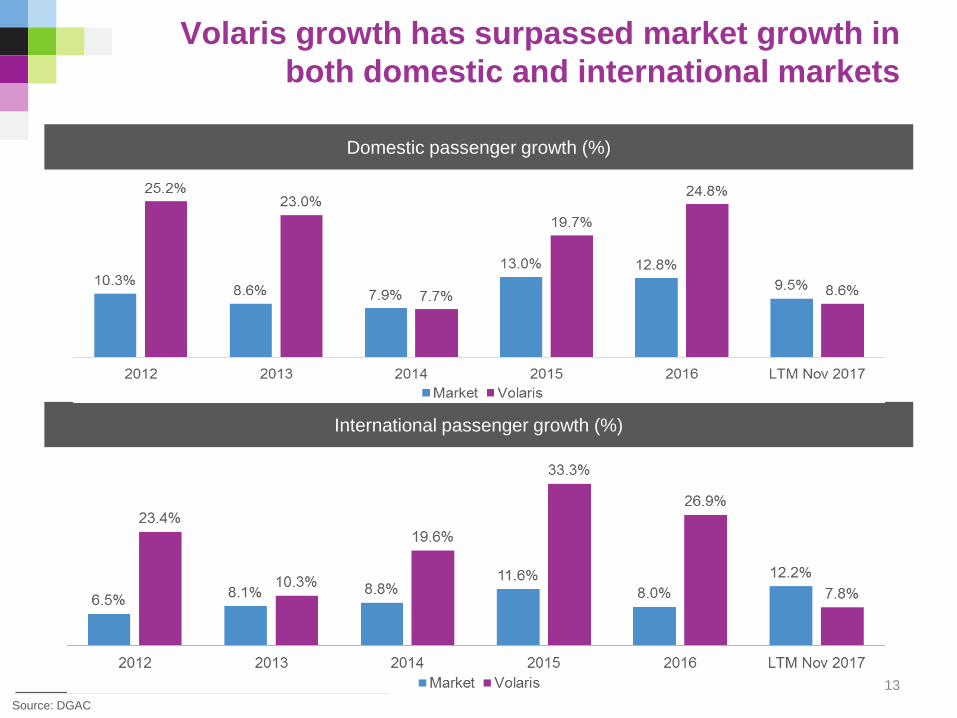

Domestic passenger growth (%)

Source: DGAC

Volaris growth has surpassed market growth in

both domestic and international markets

13

International passenger growth (%)

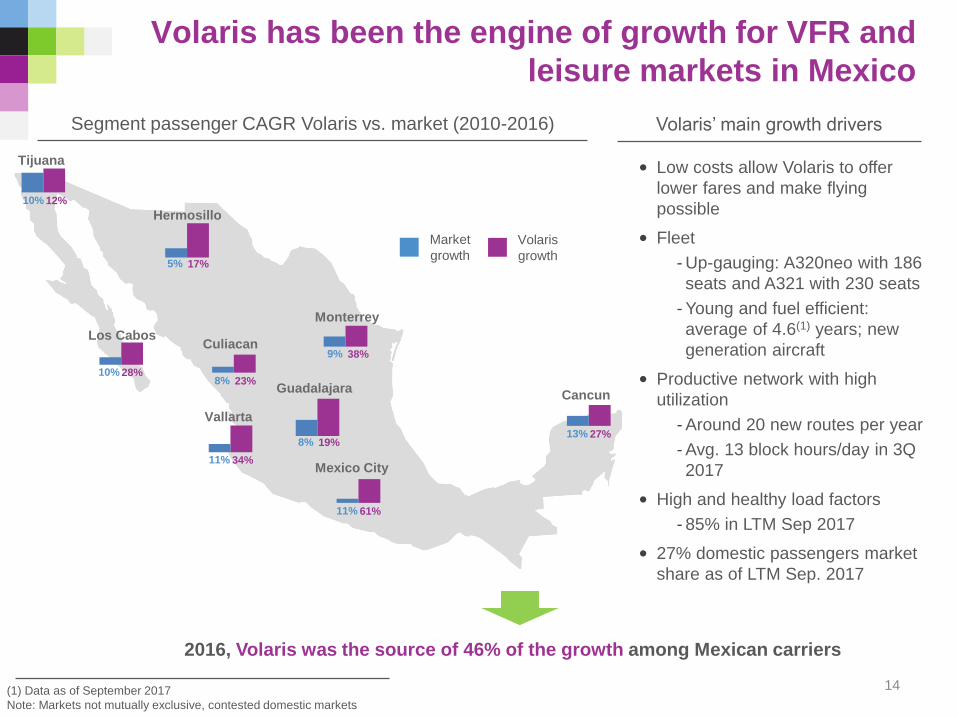

• Low costs allow Volaris to offer

lower fares and make flying

possible

• Fleet

- Up-gauging: A320neo with 186

seats and A321 with 230 seats

- Young and fuel efficient:

average of 4.6(1) years; new

generation aircraft

• Productive network with high

utilization

- Around 20 new routes per year

- Avg. 13 block hours/day in 3Q

2017

• High and healthy load factors

- 85% in LTM Sep 2017

• 27% domestic passengers market

share as of LTM Sep. 2017

Volaris has been the engine of growth for VFR and

leisure markets in Mexico

Market

growth

Volaris

growth

2016, Volaris was the source of 46% of the growth among Mexican carriers

(1) Data as of September 2017

Note: Markets not mutually exclusive, contested domestic markets

Volaris’ main growth driversSegment passenger CAGR Volaris vs. market (2010-2016)

14

Tijuana

Hermosillo

Los CabosCuliacan

Vallarta

Guadalajara

Mexico City

Cancun

Monterrey

10% 12%

5% 17%

10% 28%8% 23%

11% 34%

9% 38%

8% 19%

11% 61%

13% 27%

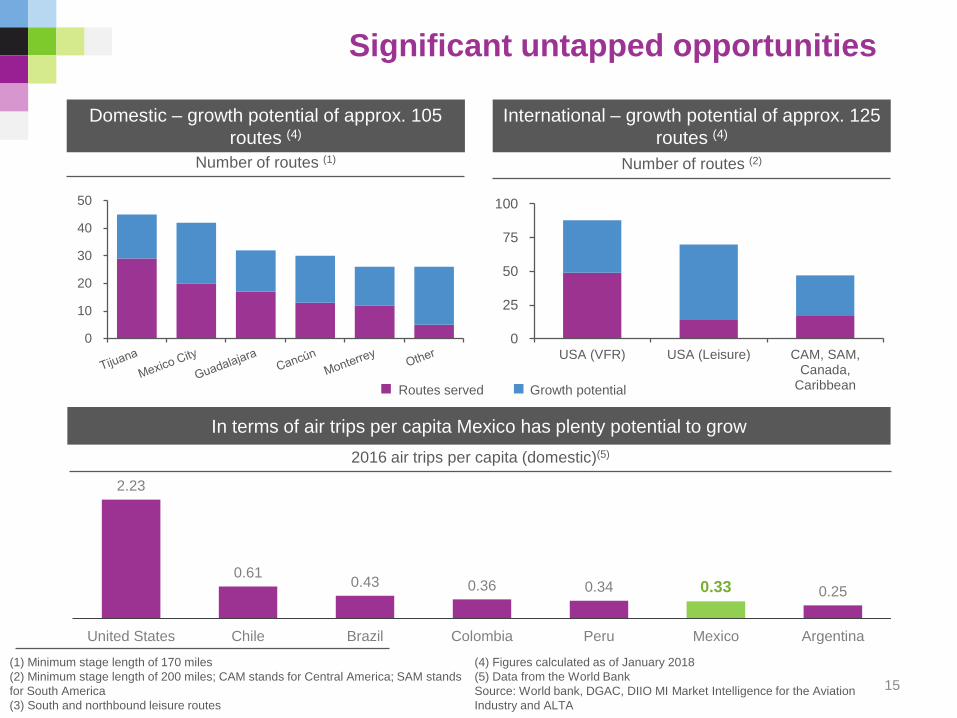

2.23

0.610.43 0.36 0.34 0.33 0.25

United States Chile Brazil Colombia Peru Mexico Argentina

Significant untapped opportunities

15

0

25

50

75

100

USA (VFR) USA (Leisure) CAM, SAM,Canada,

Caribbean

(1) Minimum stage length of 170 miles

(2) Minimum stage length of 200 miles; CAM stands for Central America; SAM stands

for South America

(3) South and northbound leisure routes

Domestic – growth potential of approx. 105

routes (4)

International – growth potential of approx. 125

routes (4)

Number of routes (1) Number of routes (2)

Routes served Growth potential

In terms of air trips per capita Mexico has plenty potential to grow

2016 air trips per capita (domestic)(5)

0

10

20

30

40

50

(4) Figures calculated as of January 2018

(5) Data from the World Bank

Source: World bank, DGAC, DIIO MI Market Intelligence for the Aviation

Industry and ALTA

28 42

2940

2012 2016

Domestic

International

2012 2016

First, economy and other

Executive and luxury

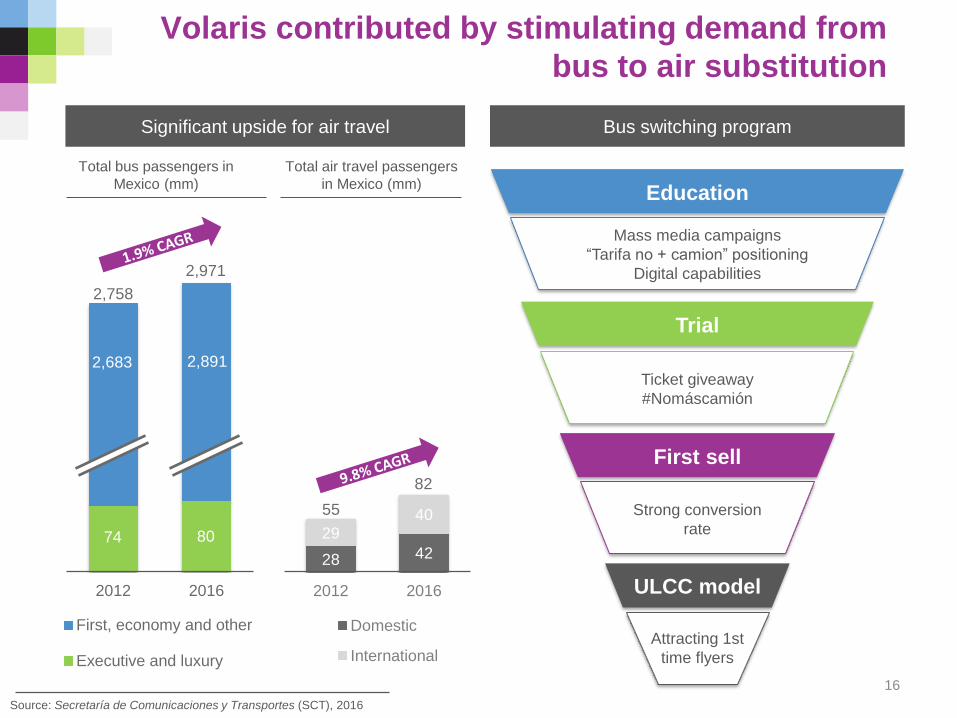

Volaris contributed by stimulating demand from

bus to air substitution

Source: Secretaría de Comunicaciones y Transportes (SCT), 2016

Bus switching programSignificant upside for air travel

Total air travel passengers

in Mexico (mm)

Total bus passengers in

Mexico (mm)

2,758

33

16

Trial

Ticket giveaway

#Nomáscamión

First sell

Strong conversion

rate

ULCC model

Attracting 1st

time flyers

Mass media campaigns

“Tarifa no + camion” positioning

Digital capabilities

Education

2,971

2,683 2,891

74 80

55

82

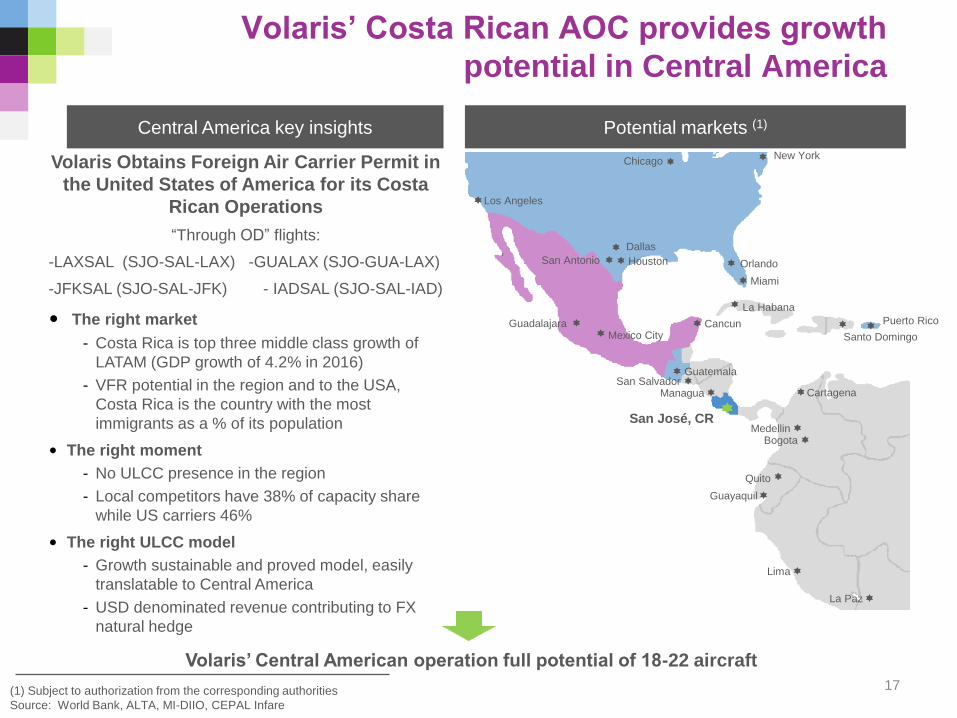

Volaris Obtains Foreign Air Carrier Permit in

the United States of America for its Costa

Rican Operations

“Through OD” flights:

-LAXSAL (SJO-SAL-LAX) -GUALAX (SJO-GUA-LAX)

-JFKSAL (SJO-SAL-JFK) - IADSAL (SJO-SAL-IAD)

• The right market

- Costa Rica is top three middle class growth of

LATAM (GDP growth of 4.2% in 2016)

- VFR potential in the region and to the USA,

Costa Rica is the country with the most

immigrants as a % of its population

• The right moment

- No ULCC presence in the region

- Local competitors have 38% of capacity share

while US carriers 46%

• The right ULCC model

- Growth sustainable and proved model, easily

translatable to Central America

- USD denominated revenue contributing to FX

natural hedge

Volaris’ Costa Rican AOC provides growth

potential in Central America

(1) Subject to authorization from the corresponding authorities

Source: World Bank, ALTA, MI-DIIO, CEPAL Infare

Potential markets (1)Central America key insights

17

Volaris’ Central American operation full potential of 18-22 aircraft

ChicagoNew York

Los Angeles

Dallas

HoustonSan Antonio Orlando

Miami

GuadalajaraMexico City

Cancun

Guatemala

San José, CR

Managua

MedellinBogota

Cartagena

Quito

Guayaquil

Lima

La Paz

San Salvador

La Habana

Santo Domingo

Puerto Rico

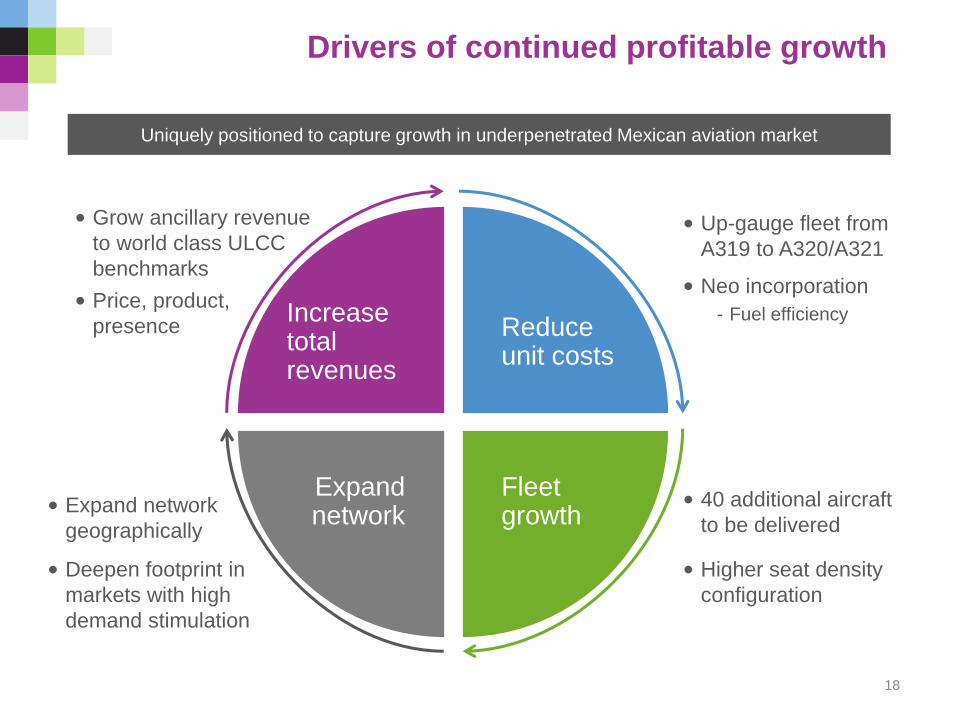

Drivers of continued profitable growth

Uniquely positioned to capture growth in underpenetrated Mexican aviation market

Reduce unit costs

Fleet growth

Expand network

Increase total revenues

• Deepen footprint in

markets with high

demand stimulation

• Grow ancillary revenue

to world class ULCC

benchmarks

• 40 additional aircraft

to be delivered

• Up-gauge fleet from

A319 to A320/A321

• Higher seat density

configuration

• Expand network

geographically

• Neo incorporation

- Fuel efficiency

18

• Price, product,

presence

Fleet and financials

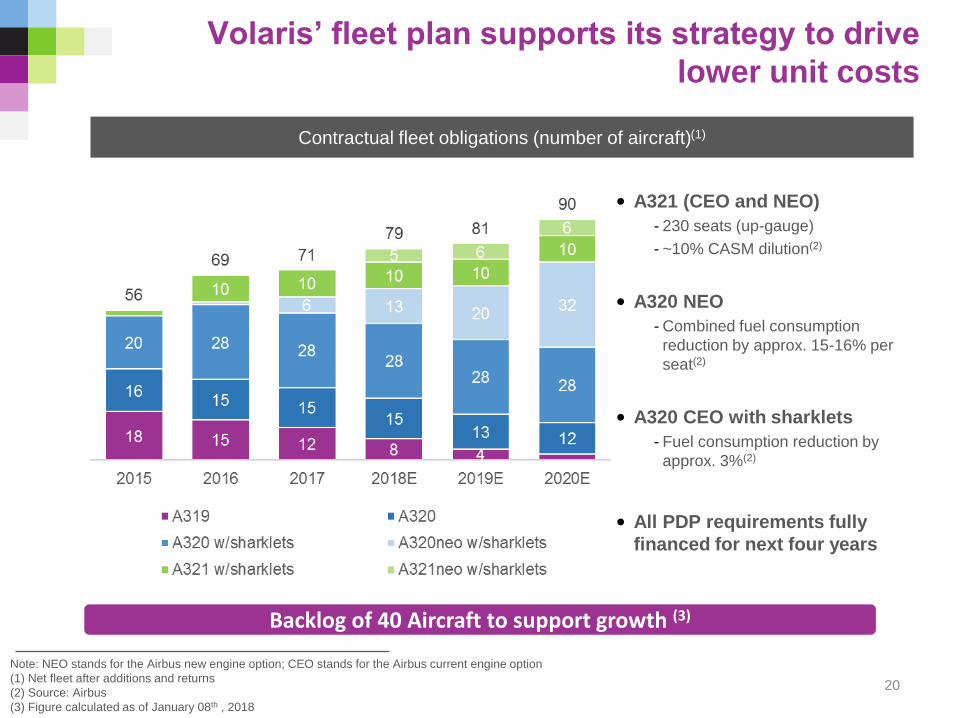

Volaris’ fleet plan supports its strategy to drive

lower unit costs

20

Note: NEO stands for the Airbus new engine option; CEO stands for the Airbus current engine option

(1) Net fleet after additions and returns

(2) Source: Airbus

(3) Figure calculated as of January 08th , 2018

• A321 (CEO and NEO)

- 230 seats (up-gauge)

- ~10% CASM dilution(2)

• A320 NEO

- Combined fuel consumption

reduction by approx. 15-16% per

seat(2)

• A320 CEO with sharklets

- Fuel consumption reduction by

approx. 3%(2)

• All PDP requirements fully

financed for next four years

Contractual fleet obligations (number of aircraft)(1)

Backlog of 40 Aircraft to support growth (3)

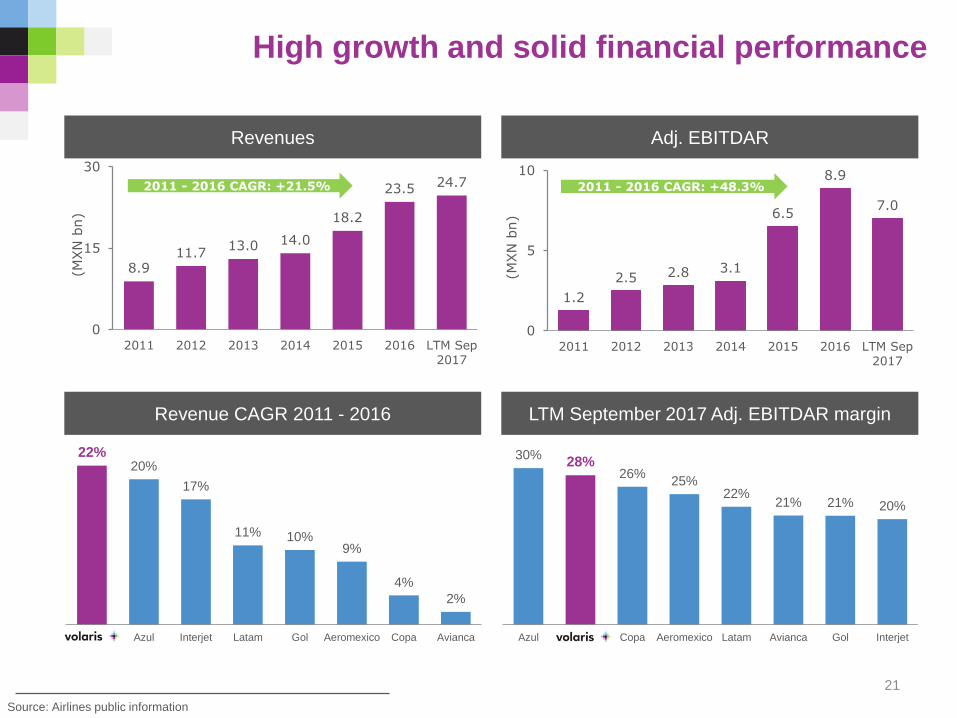

High growth and solid financial performance

21

Source: Airlines public information

Revenue CAGR 2011 - 2016

Revenues Adj. EBITDAR

LTM September 2017 Adj. EBITDAR margin

22%20%

17%

11% 10%9%

4%

2%

Volaris Azul Interjet Latam Gol Aeromexico Copa Avianca

8.911.7

13.0 14.0

18.2

23.5 24.7

0

15

30

2011 2012 2013 2014 2015 2016 LTM Sep

2017

(MXN

bn)

2011 - 2016 CAGR: +21.5%

1.2

2.5 2.8 3.1

6.5

8.9

7.0

0

5

10

2011 2012 2013 2014 2015 2016 LTM Sep

2017

(MXN

bn)

2011 - 2016 CAGR: +48.3%

30%28%

26%25%

22%21% 21% 20%

Azul Volaris Copa Aeromexico Latam Avianca Gol Interjet

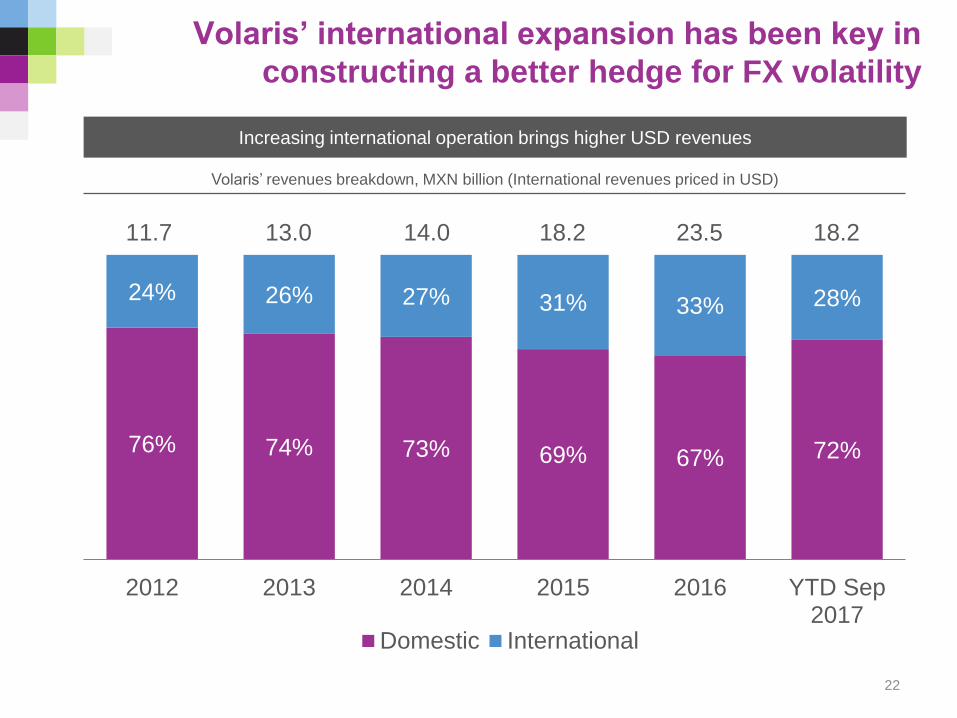

76% 74% 73% 69% 67% 72%

24% 26% 27% 31% 33% 28%

2012 2013 2014 2015 2016 YTD Sep2017

Domestic International

11.7 13.0 14.0 18.2 23.5 18.2

Increasing international operation brings higher USD revenues

Volaris’ international expansion has been key in

constructing a better hedge for FX volatility

22

Volaris’ revenues breakdown, MXN billion (International revenues priced in USD)

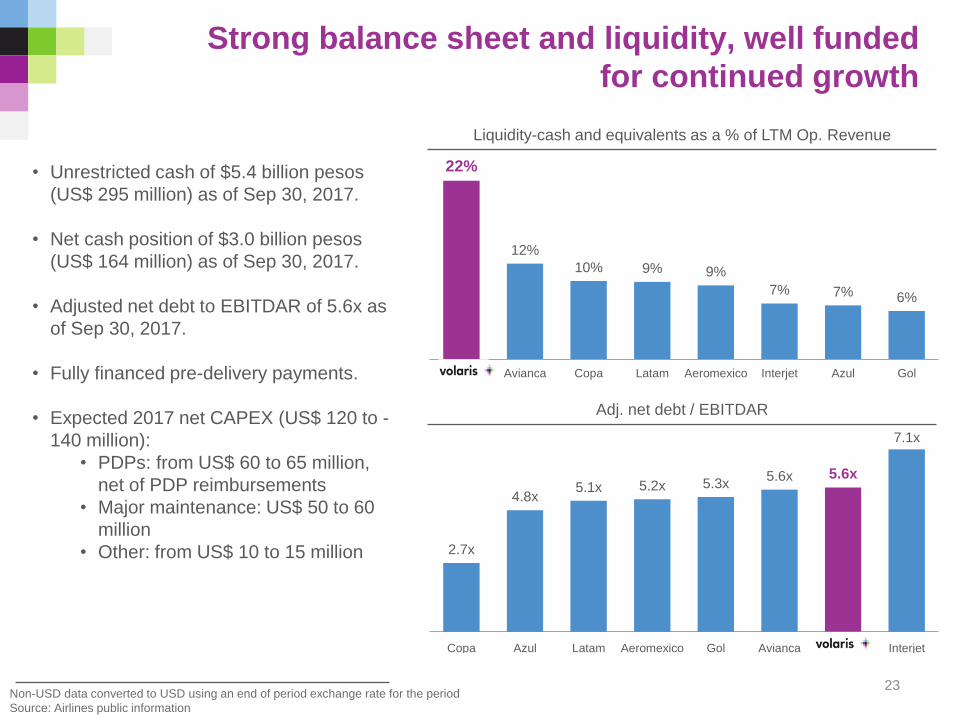

2.7x

4.8x5.1x 5.2x 5.3x

5.6x 5.6x

7.1x

Copa Azul Latam Aeromexico Gol Avianca Volaris Interjet

22%

12%

10% 9% 9%

7% 7% 6%

Volaris Avianca Copa Latam Aeromexico Interjet Azul Gol

Strong balance sheet and liquidity, well funded

for continued growth

23

Adj. net debt / EBITDAR

Liquidity-cash and equivalents as a % of LTM Op. Revenue

• Unrestricted cash of $5.4 billion pesos

(US$ 295 million) as of Sep 30, 2017.

• Net cash position of $3.0 billion pesos

(US$ 164 million) as of Sep 30, 2017.

• Adjusted net debt to EBITDAR of 5.6x as

of Sep 30, 2017.

• Fully financed pre-delivery payments.

• Expected 2017 net CAPEX (US$ 120 to -

140 million):

• PDPs: from US$ 60 to 65 million,

net of PDP reimbursements

• Major maintenance: US$ 50 to 60

million

• Other: from US$ 10 to 15 million

Non-USD data converted to USD using an end of period exchange rate for the period

Source: Airlines public information

Appendix

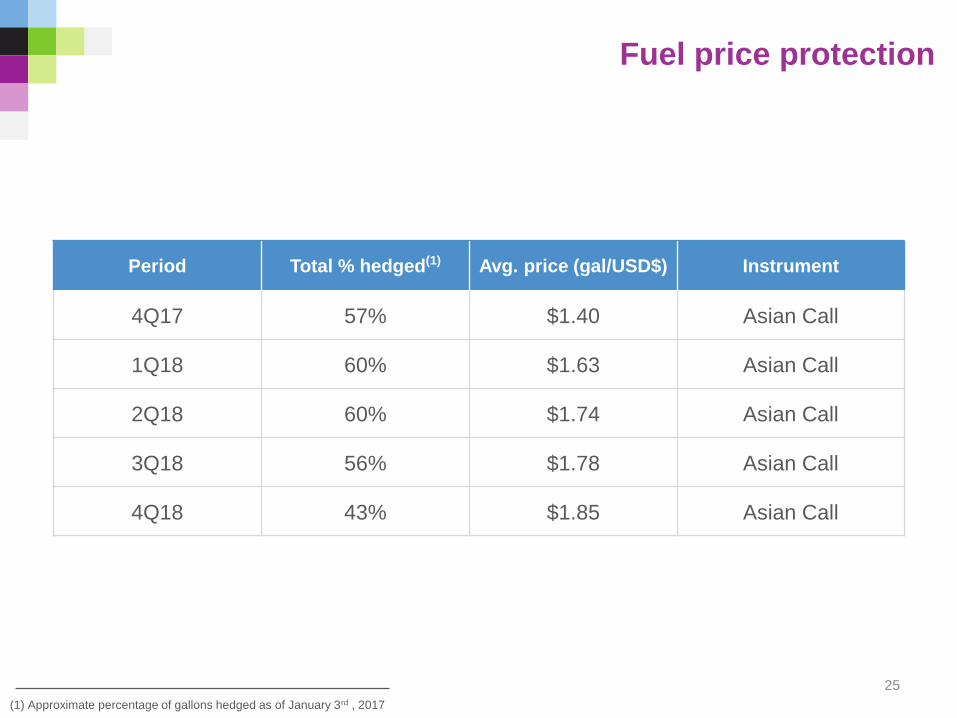

Fuel price protection

25

(1) Approximate percentage of gallons hedged as of January 3rd , 2017

Period Total % hedged(1) Avg. price (gal/USD$) Instrument

4Q17 57% $1.40 Asian Call

1Q18 60% $1.63 Asian Call

2Q18 60% $1.74 Asian Call

3Q18 56% $1.78 Asian Call

4Q18 43% $1.85 Asian Call

(1) Full year 2016 figures converted to USD at December end of the period spot exchange rate $20.6640 for convenience purposes only

(2) 3Q 2017 figures converted to USD at September end of the period spot exchange rate $18.20 for convenience purposes only

(3) Audited financial information 2014A – 2016A

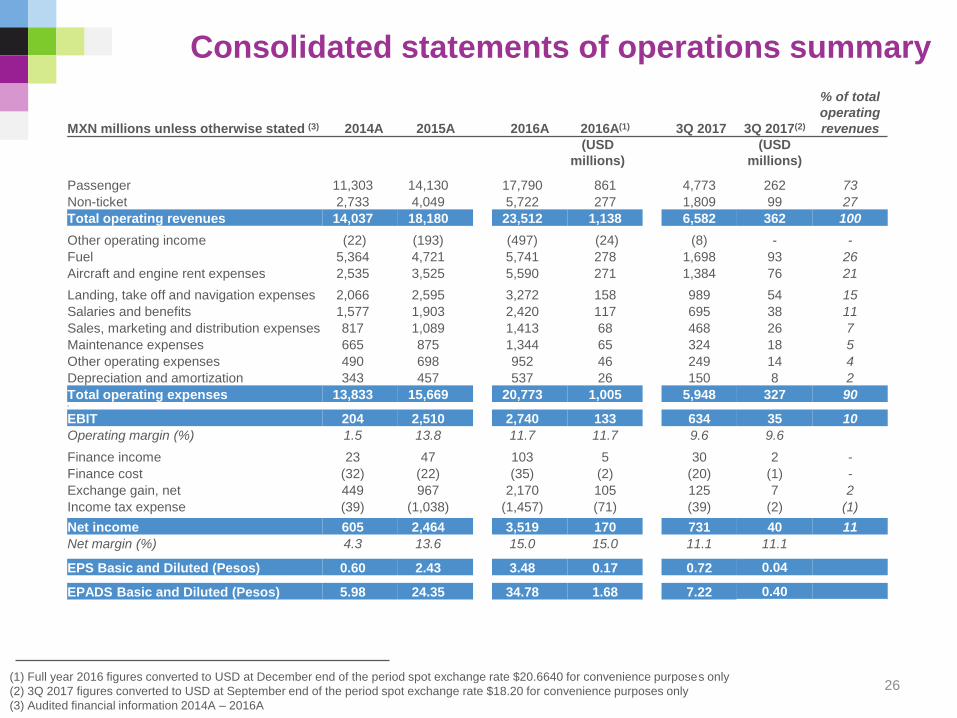

Consolidated statements of operations summary

MXN millions unless otherwise stated (3) 2014A 2015A 2016A 2016A(1) 3Q 2017 3Q 2017(2)

% of total

operating

revenues

(USD

millions)

(USD

millions)

Passenger 11,303 14,130 17,790 861 4,773 262 73

Non-ticket 2,733 4,049 5,722 277 1,809 99 27

Total operating revenues 14,037 18,180 23,512 1,138 6,582 362 100

Other operating income (22) (193) (497) (24) (8) - -

Fuel 5,364 4,721 5,741 278 1,698 93 26

Aircraft and engine rent expenses 2,535 3,525 5,590 271 1,384 76 21

Landing, take off and navigation expenses 2,066 2,595 3,272 158 989 54 15

Salaries and benefits 1,577 1,903 2,420 117 695 38 11

Sales, marketing and distribution expenses 817 1,089 1,413 68 468 26 7

Maintenance expenses 665 875 1,344 65 324 18 5

Other operating expenses 490 698 952 46 249 14 4

Depreciation and amortization 343 457 537 26 150 8 2

Total operating expenses 13,833 15,669 20,773 1,005 5,948 327 906

EBIT 204 2,510 2,740 133 634 35 10

Operating margin (%) 1.5 13.8 11.7 11.7 9.6 9.6

Finance income 23 47 103 5 30 2 -

Finance cost (32) (22) (35) (2) (20) (1) -

Exchange gain, net 449 967 2,170 105 125 7 2

Income tax expense (39) (1,038) (1,457) (71) (39) (2) (1)

Net income 605 2,464 3,519 170 731 40 11

Net margin (%) 4.3 13.6 15.0 15.0 11.1 11.1

EPS Basic and Diluted (Pesos) 0.60 2.43 3.48 0.17 0.72 0.04

EPADS Basic and Diluted (Pesos) 5.98 24.35 34.78 1.68 7.22 0.40

26

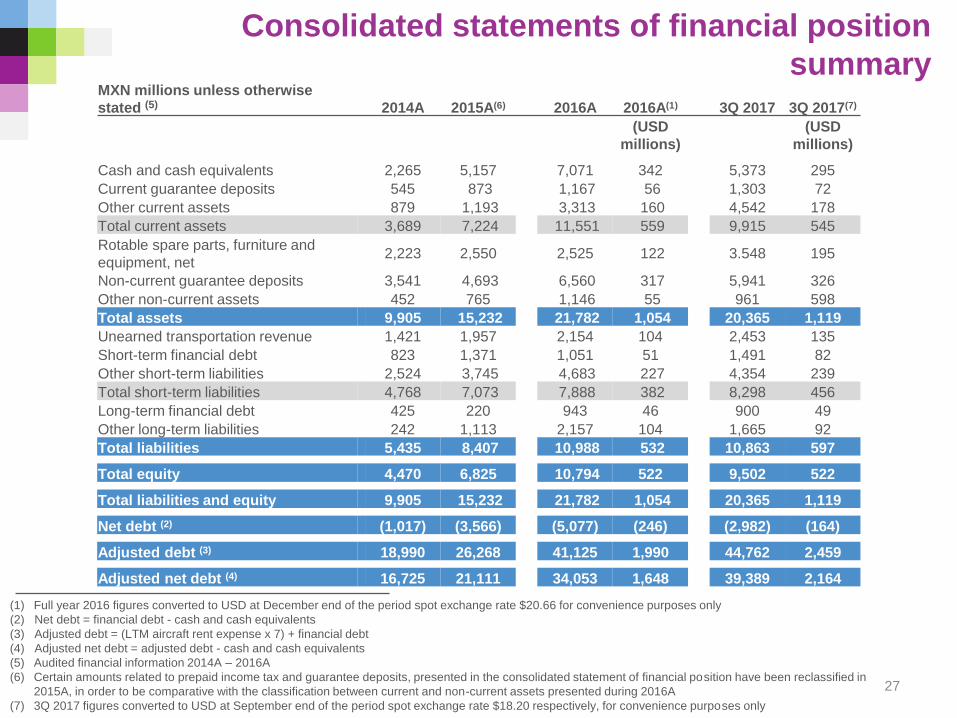

Consolidated statements of financial position

summary

(1) Full year 2016 figures converted to USD at December end of the period spot exchange rate $20.66 for convenience purposes only

(2) Net debt = financial debt - cash and cash equivalents

(3) Adjusted debt = (LTM aircraft rent expense x 7) + financial debt

(4) Adjusted net debt = adjusted debt - cash and cash equivalents

(5) Audited financial information 2014A – 2016A

(6) Certain amounts related to prepaid income tax and guarantee deposits, presented in the consolidated statement of financial position have been reclassified in

2015A, in order to be comparative with the classification between current and non-current assets presented during 2016A

(7) 3Q 2017 figures converted to USD at September end of the period spot exchange rate $18.20 respectively, for convenience purposes only

MXN millions unless otherwise

stated (5) 2014A 2015A(6) 2016A 2016A(1) 3Q 2017 3Q 2017(7)

(USD

millions)

(USD

millions)

Cash and cash equivalents 2,265 5,157 7,071 342 5,373 295

Current guarantee deposits 545 873 1,167 56 1,303 72

Other current assets 879 1,193 3,313 160 4,542 178

Total current assets 3,689 7,224 11,551 559 9,915 545

Rotable spare parts, furniture and

equipment, net2,223 2,550 2,525 122 3.548 195

Non-current guarantee deposits 3,541 4,693 6,560 317 5,941 326

Other non-current assets 452 765 1,146 55 961 598

Total assets 9,905 15,232 21,782 1,054 20,365 1,119

Unearned transportation revenue 1,421 1,957 2,154 104 2,453 135

Short-term financial debt 823 1,371 1,051 51 1,491 82

Other short-term liabilities 2,524 3,745 4,683 227 4,354 239

Total short-term liabilities 4,768 7,073 7,888 382 8,298 456

Long-term financial debt 425 220 943 46 900 49

Other long-term liabilities 242 1,113 2,157 104 1,665 92

Total liabilities 5,435 8,407 10,988 532 10,863 597

Total equity 4,470 6,825 10,794 522 9,502 522

Total liabilities and equity 9,905 15,232 21,782 1,054 20,365 1,119

Net debt (2) (1,017) (3,566) (5,077) (246) (2,982) (164)

Adjusted debt (3) 18,990 26,268 41,125 1,990 44,762 2,459

Adjusted net debt (4) 16,725 21,111 34,053 1,648 39,389 2,164

27

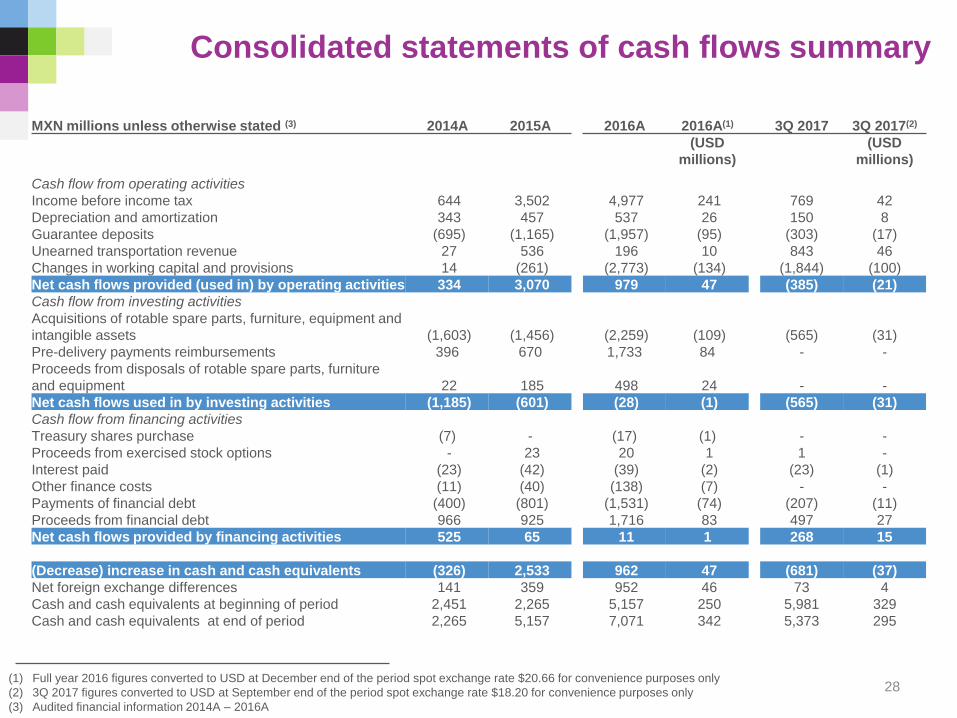

Consolidated statements of cash flows summary

(1) Full year 2016 figures converted to USD at December end of the period spot exchange rate $20.66 for convenience purposes only

(2) 3Q 2017 figures converted to USD at September end of the period spot exchange rate $18.20 for convenience purposes only

(3) Audited financial information 2014A – 2016A

MXN millions unless otherwise stated (3) 2014A 2015A 2016A 2016A(1) 3Q 2017 3Q 2017(2)

(USD

millions)

(USD

millions)

Cash flow from operating activities

Income before income tax 644 3,502 4,977 241 769 42

Depreciation and amortization 343 457 537 26 150 8

Guarantee deposits (695) (1,165) (1,957) (95) (303) (17)

Unearned transportation revenue 27 536 196 10 843 46

Changes in working capital and provisions 14 (261) (2,773) (134) (1,844) (100)

Net cash flows provided (used in) by operating activities 334 3,070 979 47 (385) (21)

Cash flow from investing activities

Acquisitions of rotable spare parts, furniture, equipment and

intangible assets (1,603) (1,456) (2,259) (109) (565) (31)

Pre-delivery payments reimbursements 396 670 1,733 84 - -

Proceeds from disposals of rotable spare parts, furniture

and equipment 22 185 498 24 - -

Net cash flows used in by investing activities (1,185) (601) (28) (1) (565) (31)

Cash flow from financing activities

Treasury shares purchase (7) - (17) (1) - -

Proceeds from exercised stock options - 23 20 1 1 -

Interest paid (23) (42) (39) (2) (23) (1)

Other finance costs (11) (40) (138) (7) - -

Payments of financial debt (400) (801) (1,531) (74) (207) (11)

Proceeds from financial debt 966 925 1,716 83 497 27

Net cash flows provided by financing activities 525 65 11 1 268 15

(Decrease) increase in cash and cash equivalents (326) 2,533 962 47 (681) (37)

Net foreign exchange differences 141 359 952 46 73 4

Cash and cash equivalents at beginning of period 2,451 2,265 5,157 250 5,981 329

Cash and cash equivalents at end of period 2,265 5,157 7,071 342 5,373 295

28