vietnam tax guide 2012 - pkf | assurance, audit, tax ... · vietnam tax guide 2012. ... regardless...

TRANSCRIPT

VietnamTax Guide

2012

PKF Worldwide Tax Guide 2012I

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for 100 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication. I would also like thank Richard Jones, PKF (UK) LLP, Kevin Reilly, PKF Witt Mares, and Kaarji Vaughan, PKF Melbourne for co-ordinating and checking the entries from countries within their regions.

The WWTG continues to expand each year reflecting both the growth of the PKF network and the strength of the tax capability offered by member firms throughout the world.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Jon HillsPKF (UK) LLPChairman, PKF International Tax Committee [email protected]

PKF Worldwide Tax Guide 2012 II

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.

This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2012III

preface

The PKF Worldwide Tax Guide 2012 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of 100 of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current as of 30 September 2011, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDAPRIL 2012

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2012 IV

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,200 partners and more than 21,400 staff.

PKFI is the 10th largest global accountancy network and its member firms have $2.6 billion aggregate fee income (year end June 2011). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryCorporate FinanceFinancial PlanningForensic AccountingHotel ConsultancyInsolvency – Corporate & PersonalIT ConsultancyManagement ConsultancyTaxation

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy, insolvency and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2012V

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2012 VI

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCroatia . . . . . . . . . . . . . . . . . . . .1 pmCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGeorgia . . . . . . . . . . . . . . . . . . . .3 pmGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJersey . . . . . . . . . . . . . . . . . . 12 noonJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKazakhstan . . . . . . . . . . . . . . . . .5 pmKenya . . . . . . . . . . . . . . . . . . . . .3 pmKorea . . . . . . . . . . . . . . . . . . . . .9 pmKuwait . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLiberia . . . . . . . . . . . . . . . . . . 12 noonLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMauritius . . . . . . . . . . . . . . . . . . .4 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmPuerto Rico . . . . . . . . . . . . . . . . .8 am

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE sTANDARD TIME ELsEwHERE Is:

PKF Worldwide Tax Guide 2012VII

QQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pmRussia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

sSierra Leone . . . . . . . . . . . . . 12 noonSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 amVietnam . . . . . . . . . . . . . . . . . . . .7 pm

PKF Worldwide Tax Guide 2012 1

Vietnam

Vietnam

Currency: Vietnam Dong Dial Code To: 84 Dial Code Out: 84 (VND)

Member Firm:City: Name: Contact Information:Hanoi Hung Pham (84) 989 194 898 [email protected] www.pkf.com.vn

Ho Chi Minh City Nga Nguyen (84.8) 54491 476/477 [email protected]

Da Nang Hung Pham (84.511) 3531 399 [email protected]

a. taXes payable

TAXEs AND LEVIEsCOMPANY TAXThe Corporate Income Tax (CIT) rate applicable is 25%, except for business establishments involved in the prospecting, exploration and exploitation of petroleum and gas and other precious natural resources, where the applicable tax rate is 32% -50%.

Enterprises shall make a self-declaration of CIT payable. For each quarter, the enterprise shall determine the amount of CIT provisionally payable for the quarter and the tax finalization for the whole year shall be determined within 90 days after the year end.

The total income generated by Vietnamese enterprises shall be subjected to CIT, regardless of whether the income is generated in Vietnam or overseas, comprising income earned from production except income earned from:• productsofcultivation,husbandryandaquaculturebyco-operatives• performanceoftechnicalservicecontractsdirectlyservingagriculturalproduction• performanceofcontractsforscientificresearchanddevelopment• productionofandtradingingoodsandservicesbybusinessestablishments

specially reserved for disabled employees or persons involved in crime.

The CIT payable shall be determined by applying the applicable tax rate on the taxable income, which is the total turnover less reasonable expenses. Reasonable expenses which are deductible for the purpose of calculating taxable income include expenses actually used for the production or trading in goods and services, and expenses incurred with receipts or source documents issued in accordance with the law.

Tax year: A tax year for the purpose of tax finalization shall be the calendar year (from 01 January to 31 December annually). Where a business establishment is permitted to apply a tax year other than the calendar year, tax finalization shall be conducted in accordance with such a year.

CAPITAL GAINs TAX The capital gains tax rate applicable is 20%.

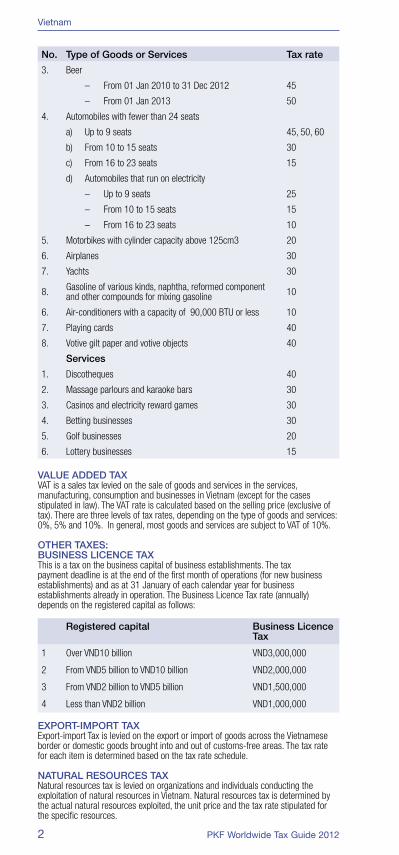

sPECIAL sALEs TAXSpecial Sales Tax is applicable to special goods and services (luxury). The basis for calculating Special Sales Tax shall be based on the quantity of taxable goods sold, their taxable value and the applicable tax rates.

Taxable goods and their applicable tax rates are set out in the following schedule:

No. Type of Goods or services Tax rate

Goods

1. Tobacco products

Cigarettes, cigars and other tobacco products 65

2. Spirits

a) over 20 degrees proof

– From 01 Jan 2010 to 31 Dec 2012 45

– From 01 Jan 2013 50

b) under 20 degrees proof 25

PKF Worldwide Tax Guide 20122

No. Type of Goods or services Tax rate

3. Beer

– From 01 Jan 2010 to 31 Dec 2012 45

– From 01 Jan 2013 50

4. Automobiles with fewer than 24 seats

a) Up to 9 seats 45, 50, 60

b) From 10 to 15 seats 30

c) From 16 to 23 seats 15

d) Automobiles that run on electricity

– Up to 9 seats 25

– From 10 to 15 seats 15

– From 16 to 23 seats 10

5. Motorbikes with cylinder capacity above 125cm3 20

6. Airplanes 30

7. Yachts 30

8. Gasoline of various kinds, naphtha, reformed component and other compounds for mixing gasoline 10

6. Air-conditioners with a capacity of 90,000 BTU or less 10

7. Playing cards 40

8. Votive gilt paper and votive objects 40

services

1. Discotheques 40

2. Massage parlours and karaoke bars 30

3. Casinos and electricity reward games 30

4. Betting businesses 30

5. Golf businesses 20

6. Lottery businesses 15

VALUE ADDED TAXVAT is a sales tax levied on the sale of goods and services in the services, manufacturing, consumption and businesses in Vietnam (except for the cases stipulated in law). The VAT rate is calculated based on the selling price (exclusive of tax). There are three levels of tax rates, depending on the type of goods and services: 0%, 5% and 10%. In general, most goods and services are subject to VAT of 10%.

OTHER TAXEs:BUsINEss LICENCE TAXThis is a tax on the business capital of business establishments. The tax payment deadline is at the end of the first month of operations (for new business establishments) and as at 31 January of each calendar year for business establishments already in operation. The Business Licence Tax rate (annually) depends on the registered capital as follows:

Registered capital Business Licence Tax

1 Over VND10 billion VND3,000,000

2 From VND5 billion to VND10 billion VND2,000,000

3 From VND2 billion to VND5 billion VND1,500,000

4 Less than VND2 billion VND1,000,000

EXPORT-IMPORT TAXExport-import Tax is levied on the export or import of goods across the Vietnamese border or domestic goods brought into and out of customs-free areas. The tax rate for each item is determined based on the tax rate schedule.

NATURAL REsOURCEs TAXNatural resources tax is levied on organizations and individuals conducting the exploitation of natural resources in Vietnam. Natural resources tax is determined by the actual natural resources exploited, the unit price and the tax rate stipulated for the specific resources.

Vietnam

PKF Worldwide Tax Guide 2012 3

b. determination of taXable income

CIT payable = (Assessable income - Allocation to R&D fund) x CIT rate

(R&D fund is Science and Technology Development Fund)

Assessable income equalstaxable income less exempt income andlosses carried forward in accordance with law. Taxable income equals turnover less deductible expenses plus other income items. Generally, to be deductible, the expenses must be related to the activities of production and business of the enterprise and accompanied by legal and complete invoices and source vouchers as required by law.

TAX LOssEsEnterprises which suffer losses after tax finalization shall be entitled to carry forward these losses to taxable income of the following years. Losses may be carried forward for a maximum period of five years from the year following the year in which the loss arose.

FOREIGN sOURCED INCOMEA Vietnamese enterprise which makes an offshore investment and derives income from production and business activities overseas must declare and pay CIT in accordance with the current law on CIT of Vietnam, including when the enterprise is entitled to a tax reduction or exemption under the law of the foreign country.

INCENTIVEsSpecific incentives are provided for high technology fields.

c. foreiGn taX relief

If income from an investment project overseas has been subject to CIT (or any other type of tax which is basically similar to CIT) overseas, then when assessing CIT payable in Vietnam, the Vietnamese enterprise shall be entitled to deduct the amount of tax paid overseas or paid on its behalf by the foreign party accepting such investment (including tax payable on interest on shareholding), but the amount of tax deductible must not exceed the amount of tax payable pursuant to the law on CIT of Vietnam.

e. related party transactions

Related party transactions are subjected to the transfer pricing rules.

f. witHHoldinG taXes

Income from foreign contractors and sub-contractors are taxed at source and tax must be paid to the tax office within 20 business days from the date of signing the contract.

Withholding tax is levied on goods and services provided by a foreign contractor to generate income in Vietnam. Tax applicable to foreign contractors comprises:• VATand• CIT.

VAT is levied on any value-add to a product or service, as follows:

1 Lease of insurance machinery, or equipment 50%

2a Construction with supply of material 30%

2b Construction without supply of material 50%

3 Manufacturing and other business activities 50%

CIT is calculated by ratio over taxable income based on the following table:

1 Trading: distribution, supply of goods, materials, machinery and equipment, together with the provision of services in Vietnam

1%

2 Lease of machinery and equipment, and insurance 5%

3 Construction 2%

4 Manufacturing, transport and other businesses 2%

5 Lease of aircraft and vessels (including components) 2%

6 Overseas reinsurance 2%

7 Transfer of securities 0.1%

8 Borrowing cost 10%

9 Royalties 10%

Vietnam

PKF Worldwide Tax Guide 20124

H. personal income taX

All residents and non-residents are subject to Personal Income Tax.

A resident is liable to pay tax on income sourced in Vietnam as well as on the portion of income from foreign sources (except for non-taxable income, including income from real estate transferred between a husband and wife and blood-relations, scholarships, and overseas remittances).

Deductions are available for family considerations for residents, comprising children under 18, unemployed spouses and elderly and unemployed parents.

Individuals are responsible for self-declaration and payment of tax.

A non-resident is subject to tax only on income sourced in Vietnam.

The applicable Personal Income Tax rates are as follows:

Resident

I Income from salaries and wages, business and production (million dong)

Level Taxable income/year(million VND)

Taxable income/month(million VND)

Tax rate (%)

1 Up to 60 Up to 5 5

2 From 60 to 120 From 5 to 10 10

3 From 120 to 216 From 10 to 18 15

4 From 216 to 384 From 18 to 32 20

5 From 384 to 624 From 32 to 52 25

6 From 624 to 960 From 52 to 80 30

7 Over 960 Over 80 35

II Income from capital investment, copyright and franchise activities 5

III Income from transfer of capital 20

IV Income from transfer of real estate 25

Non-residents

I Income from business and production

1 Income from business and production of goods 1

2 Income from business and production of services 5

3 Manufacturing, construction, transport and other activities 2

II Salary and wages 20

III Income from capital investment 5

Non-residents

IV Transfer of capital 0.1

V Transfer of real estate 2

VI Copyright and franchise activities 5

VII Lottery winning, inheritance and gifts which are securities, capital or assets 10

i. treaty and non-treaty witHHoldinG taX rates

Withholding tax rates for dividend, interest and royalties are as follow:

Dividend(%)

Interest(%)

Royalties(%)

Country:

Algeria 15 15 15

Australia 10 10 10

Vietnam

PKF Worldwide Tax Guide 2012 5

Dividend(%)

Interest(%)

Royalties(%)

Bangladesh 15 15 15

Belarus 15 10 15

Belgium 5, 7, 10 or 15 10 5, 10 or 15

Bulgaria 15 10 15

Canada 5, 10 or 15 10 7.5 or 10

China 10 10 10

Cuba 5, 10 or 15 10 10

Czech Republic 10 10 10

Denmark 5, 10 or 15 10 5 or 15

Finland 5, 10 or 15 10 10

France 7, 10 or 15 Nil 10

Germany 5, 10 or 15 10 7.5 or 10

Hungary 10 10 10

Iceland 10 or 15 10 10

India 10 10 10

Indonesia 15 15 15

Italy 5, 10 or 15 10 7.5 or 10

Japan 10 10 10

Korea 10 10 5 or 15

Laos 10 10 10

Luxembourg 5, 10 or 15 10 10

Malaysia 10 10 10

Mongolia 10 10 10

Myanmar 10 10 10

Netherlands 5, 7, 10 or 15 7 or 10 5, 10 or 15

North Korea 10 10 10

Norway 5, 10 or 15 10 10

Pakistan 15 15 15

Philippines 10 or 15 15 15

Poland 10 or 15 10 1, 10 or 15

Romania 15 10 15

Russian 10 or 15 10 15

Seychelles 10 10 10

Singapore 5, 7 or 12.5 10 5 or 15

Spain 7, 10 or 15 10 10

Sri Lanka 10 10 15

Sweden 5, 10 or 15 10 5 or 15

Switzerland 7, 10 or 15 10 10

Thailand 15 10 or 15 15

Ukraine 10 10 10

United Kingdom 7, 10 or 15 10 10

Uzbekistan 15 10 15

Vietnam

PKF Worldwide Tax Guide 2012 565

www.pkf.com$100