venture capitalandprivate equity research at vlerick/media/corporate/pdf-brochures/events/4... ·...

TRANSCRIPT

20/10/2011

1

Venture Capital and Private EquityResearch at Vlerick

Prof. Sophie Manigart / Prof. Miguel Meuleman / David Devigne / Bart Van Hoe

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Overview presentation

Intro to venture capital and private equity

Why interesting as a research setting?

Theoretical perspectives

Overview datasets

Current research projects

Discussion

2

20/10/2011

2

Intro to venture capital and private equity

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Facebook’s valuation (January 4, 2011)

Goldman Sachs and Digital Sky Technologies (Usmanov’sRussian investment fund) pay $500 mio for 1% stake in Facebook – Facebook value = $50 bio

3 times more than what Microsoft paid three years ago

Company is 7 years old

500 mio users (valuing each user at $100 !)

Huge growth

Comscore: Q3 2010: showed 300 bio ads

Cooperation with Zynga (Farmville game) is very valuable

2010: sales 2 bio, profits 400 mio (P/E: 125!)

IPO is expected...

4

20/10/2011

3

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Facebook’s valuation (January 4, 2011)

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

What do private equity players and venture capitalists do?

Private Equity• Invests in equity

instruments of private companies

• Invests in equity related instruments

• Invests in equity instruments of private

companies• Invests in equity

related instruments

• Replaces existing shareholders:

• Completely• Buyouts• Buyins

• Partially• Replacement capital

• Brings additional resources• Growth capital

Venture capital• Joins with other venture

capitalist to provide risk capital in successive rounds

The objective is to create value through capital gains.

•Take the risks on a business plan and on the growth of the

firm•Mobilize and allocate capital in the economy

6

20/10/2011

4

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

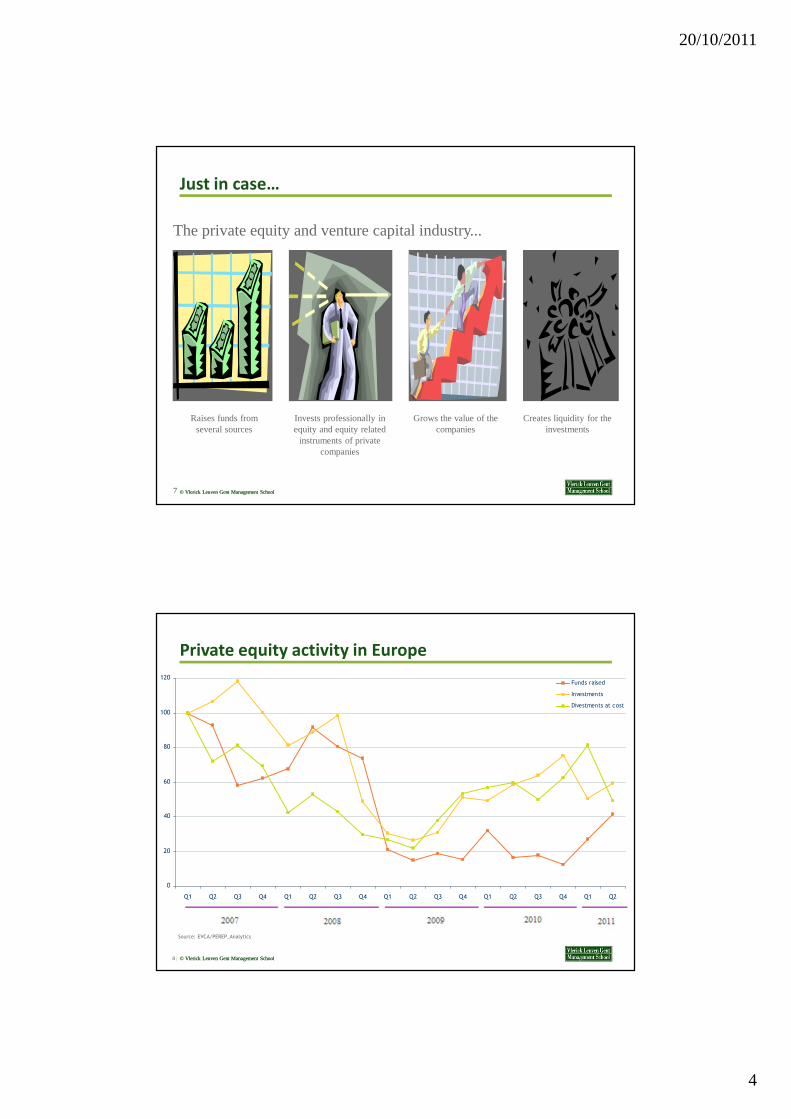

Just in case…

The private equity and venture capital industry...

Raises funds from several sources

Invests professionally in equity and equity related

instruments of private companies

Grows the value of the companies

Creates liquidity for the investments

7

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Private equity activity in Europe

8 |

0

20

40

60

80

100

120

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Funds raised

Investments

Divestments at cost

Source: EVCA/PEREP_Analytics

20/10/2011

5

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

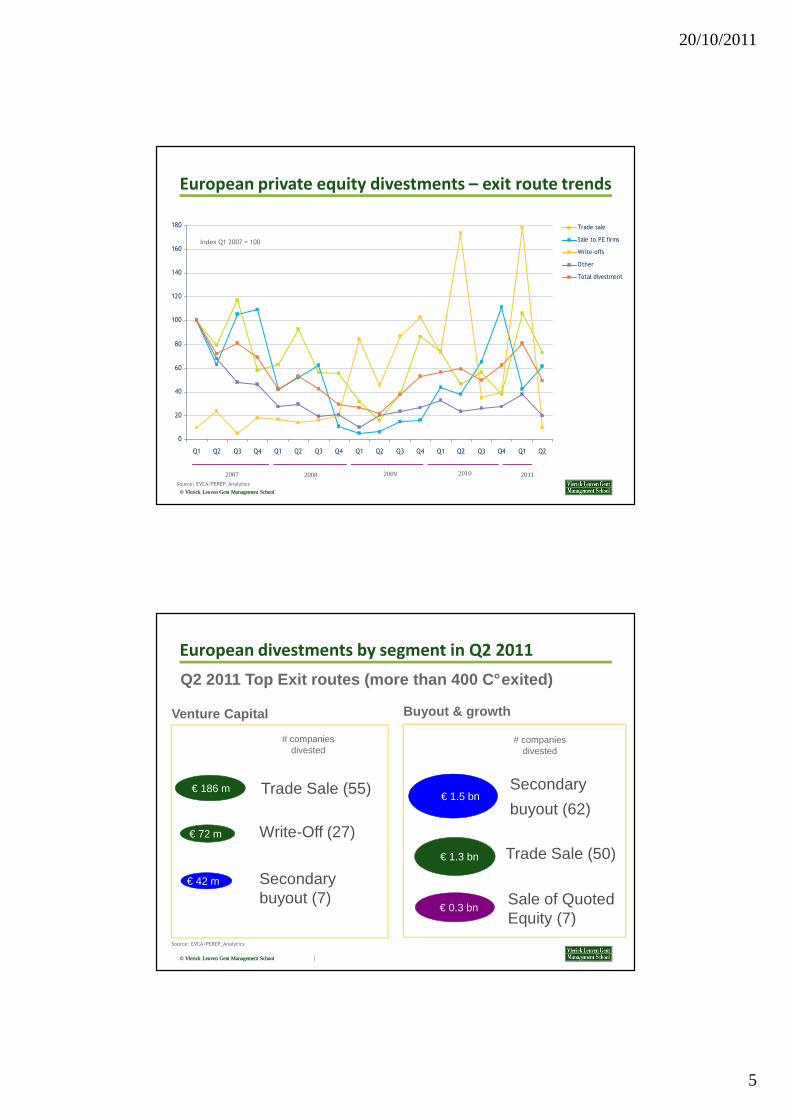

European private equity divestments – exit route trends

Index Q1 2007 = 100

Source: EVCA/PEREP_Analytics

0

20

40

60

80

100

120

140

160

180

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Trade sale

Sale to PE firms

Write-offs

Other

Total divestment

2007 2008 2009 2010 2011

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School |

European divestments by segment in Q2 2011

Venture Capital

€ 186 m

# companies divested

€ 72 m

€ 42 m

Buyout & growth

# companies divested

€ 1.3 bn

€ 1.5 bn

€ 0.3 bn

Q2 2011 Top Exit routes (more than 400 C°exited)

Secondary

buyout (62)

Trade Sale (50)Write-Off (27)

Source: EVCA/PEREP_Analytics

Sale of QuotedEquity (7)

Trade Sale (55)

Secondarybuyout (7)

20/10/2011

6

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

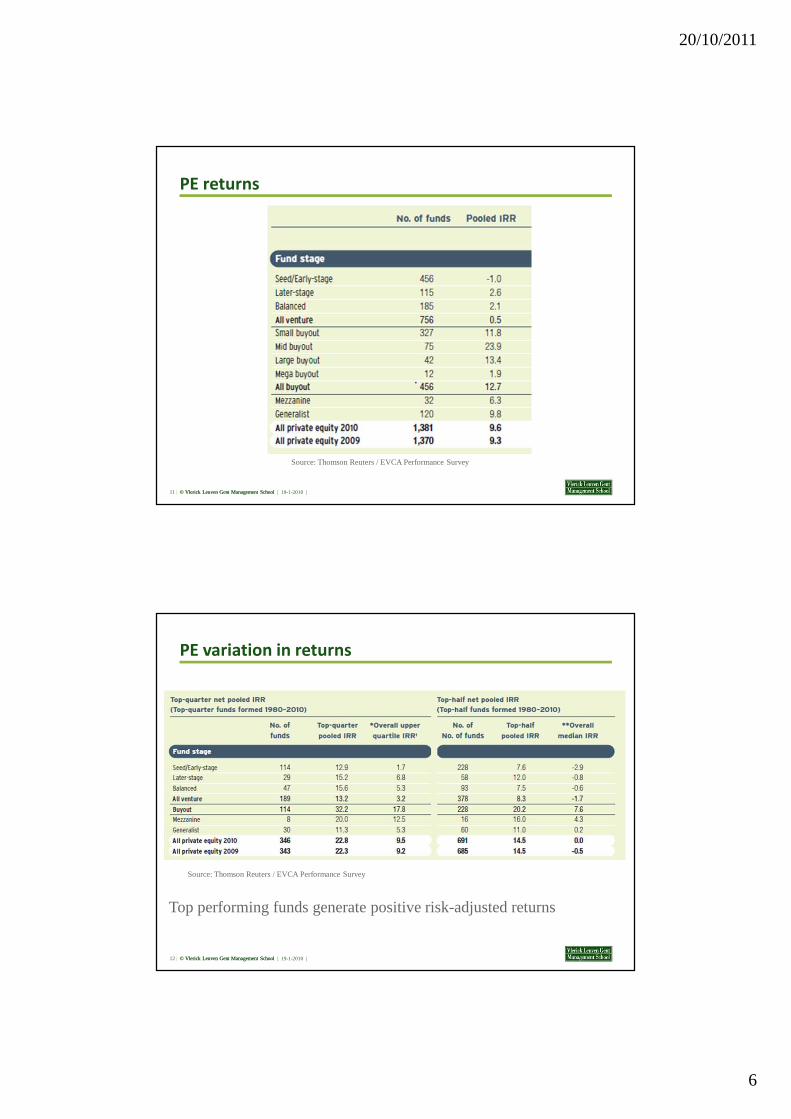

PE returns

| 19-1-2010 |11 |

Source: Thomson Reuters / EVCA Performance Survey

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

PE variation in returns

| 19-1-2010 |12 |

Source: Thomson Reuters / EVCA Performance Survey

Top performing funds generate positive risk-adjusted returns

20/10/2011

7

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

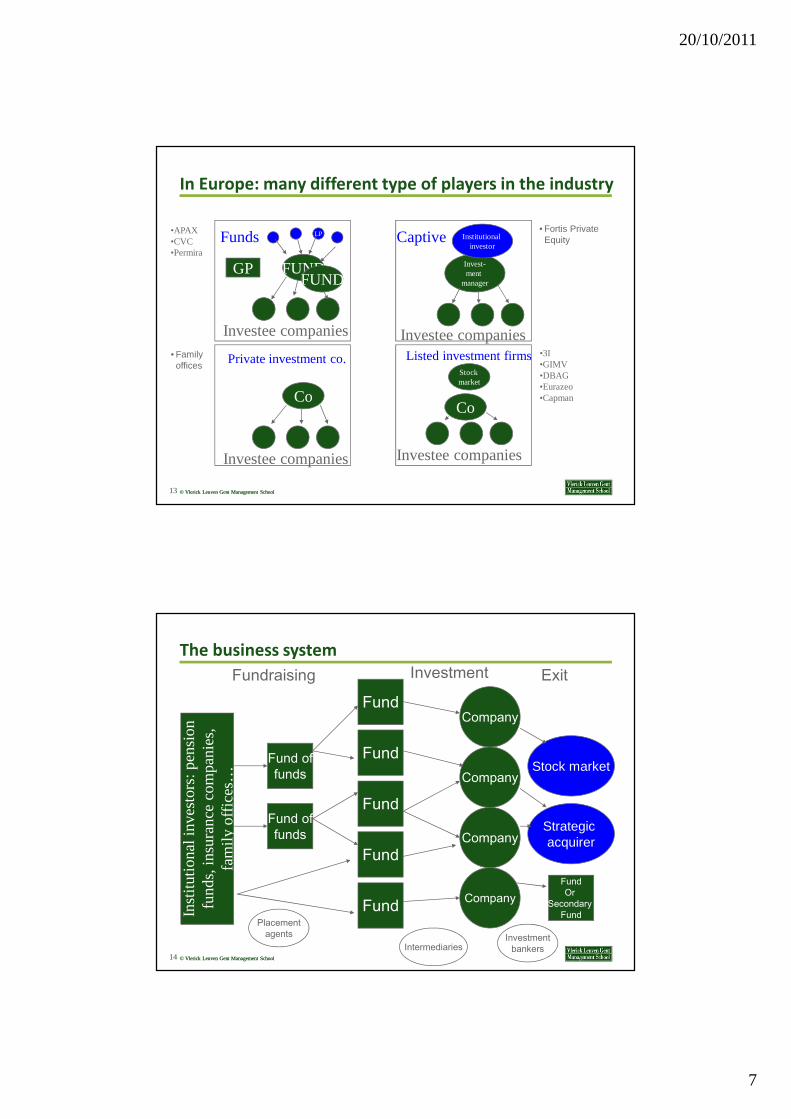

In Europe: many different type of players in the industry

Funds

FUND

LP

GP

Investee companies

Captive

Invest-ment

manager

Investee companies

Private investment co.

Co

Investee companies

FUND

Institutionalinvestor

Listed investment firms

Co

Investee companies

Stock market

•APAX•CVC•Permira

•3I•GIMV•DBAG•Eurazeo•Capman

• Fortis Private Equity

• Family offices

13

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

The business system

Inst

itutio

nal i

nves

tors

: pen

sion

fu

nds,

insu

ranc

e co

mpa

nies

, fa

mily

offi

ces…

Fund offunds

Fund offunds

Fund

Fund

Fund

Fund

Fund

Company

Company

Company

Company

Stock market

Strategic acquirer

FundOr

Secondary Fund

Fundraising Investment Exit

Placementagents

IntermediariesInvestment

bankers14

20/10/2011

8

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Interesting research setting

1. Information on (almost) full population

a) Over 1 (Europe) to 2 (US) decades, currently also Asia and RoW

b) Numerous linkages between actors

2. Individual projects

a) Clear begin and end dates

b) No confounding factors: individual performance observed

3. Extreme risk

4. Numerous different actors, different roles,…

15

Theoretical perspectives

20/10/2011

9

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Theoretical perspectives

Agency theory / multiple agency theory

Social netwerk theory

Human capital theory

Resource-based theory

Decision making theory

Conflict theory

Institutional theory

Finance and law

Contracting theory

Ethics

…

17

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Agency theory / multiple agency theory

18

20/10/2011

10

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Agency theory / reputation

19

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Social netwerk theory

20

20/10/2011

11

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Social netwerk theory/agency theory

21

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Human capital theory

22

20/10/2011

12

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Resource-based theory/agency theory

23

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Decision making theory

24

20/10/2011

13

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Decision making

25

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Finance and law

26

20/10/2011

14

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Governance

27

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Learning theory / institutional theory

28

20/10/2011

15

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Contracting theory

29

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Conflict theory

30

20/10/2011

16

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Ethics

31

Datasets used

20/10/2011

17

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

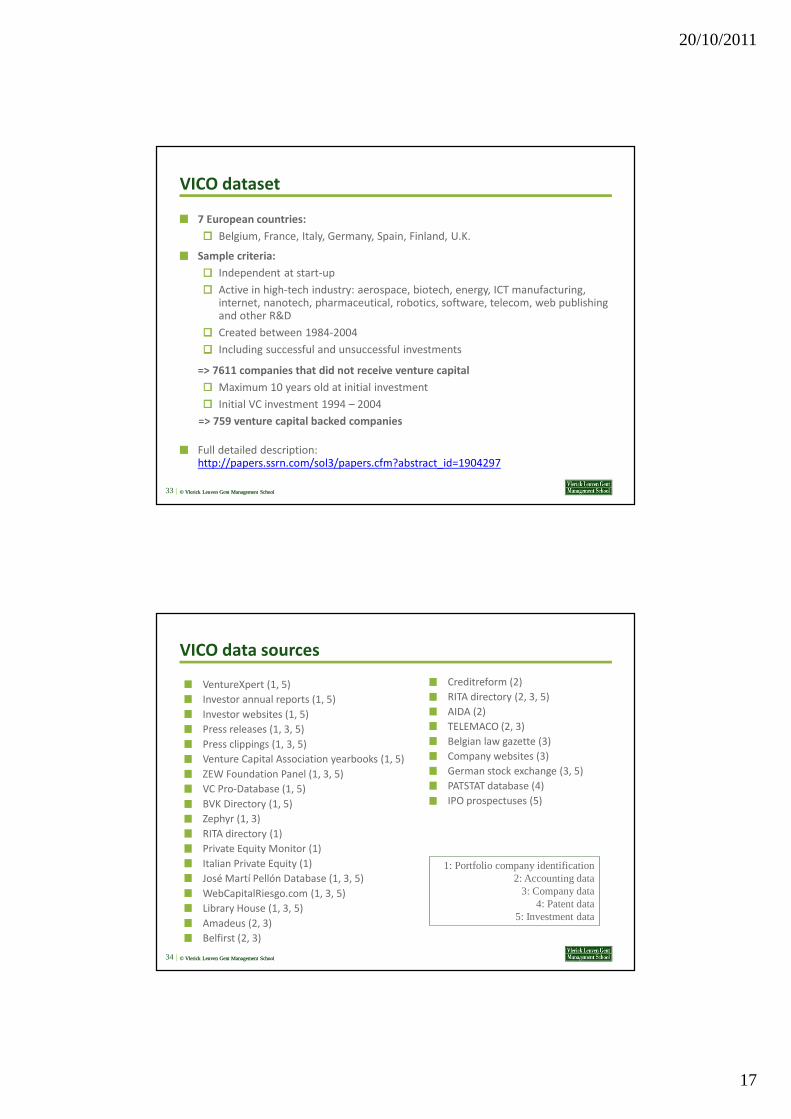

VICO dataset

7 European countries:

Belgium, France, Italy, Germany, Spain, Finland, U.K.

Sample criteria:

Independent at start-up

Active in high-tech industry: aerospace, biotech, energy, ICT manufacturing, internet, nanotech, pharmaceutical, robotics, software, telecom, web publishing and other R&D

Created between 1984-2004

Including successful and unsuccessful investments

=> 7611 companies that did not receive venture capital

Maximum 10 years old at initial investment

Initial VC investment 1994 – 2004

=> 759 venture capital backed companies

Full detailed description: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1904297

33 |

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

VICO data sources

VentureXpert (1, 5)

Investor annual reports (1, 5)

Investor websites (1, 5)

Press releases (1, 3, 5)

Press clippings (1, 3, 5)

Venture Capital Association yearbooks (1, 5)

ZEW Foundation Panel (1, 3, 5)

VC Pro-Database (1, 5)

BVK Directory (1, 5)

Zephyr (1, 3)

RITA directory (1)

Private Equity Monitor (1)

Italian Private Equity (1)

José Martí Pellón Database (1, 3, 5)

WebCapitalRiesgo.com (1, 3, 5)

Library House (1, 3, 5)

Amadeus (2, 3)

Belfirst (2, 3)

34 |

Creditreform (2)

RITA directory (2, 3, 5)

AIDA (2)

TELEMACO (2, 3)

Belgian law gazette (3)

Company websites (3)

German stock exchange (3, 5)

PATSTAT database (4)

IPO prospectuses (5)

1: Portfolio company identification 2: Accounting data

3: Company data 4: Patent data

5: Investment data

20/10/2011

18

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

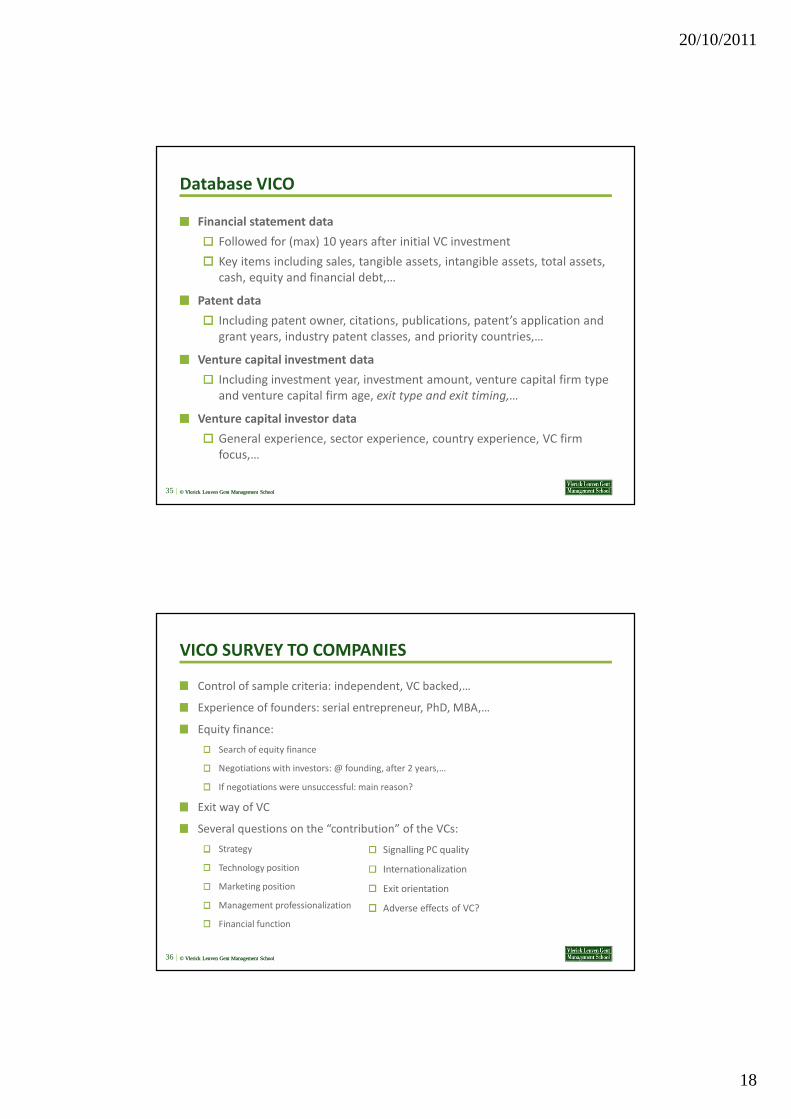

Database VICO

Financial statement data

Followed for (max) 10 years after initial VC investment

Key items including sales, tangible assets, intangible assets, total assets,

cash, equity and financial debt,…

Patent data

Including patent owner, citations, publications, patent’s application and

grant years, industry patent classes, and priority countries,…

Venture capital investment data

Including investment year, investment amount, venture capital firm type

and venture capital firm age, exit type and exit timing,…

Venture capital investor data

General experience, sector experience, country experience, VC firm

focus,…

35 |

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

VICO SURVEY TO COMPANIES

Control of sample criteria: independent, VC backed,…

Experience of founders: serial entrepreneur, PhD, MBA,…

Equity finance:

Search of equity finance

Negotiations with investors: @ founding, after 2 years,…

If negotiations were unsuccessful: main reason?

Exit way of VC

Several questions on the “contribution” of the VCs:

Strategy

Technology position

Marketing position

Management professionalization

Financial function

36 |

Signalling PC quality

Internationalization

Exit orientation

Adverse effects of VC?

20/10/2011

19

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

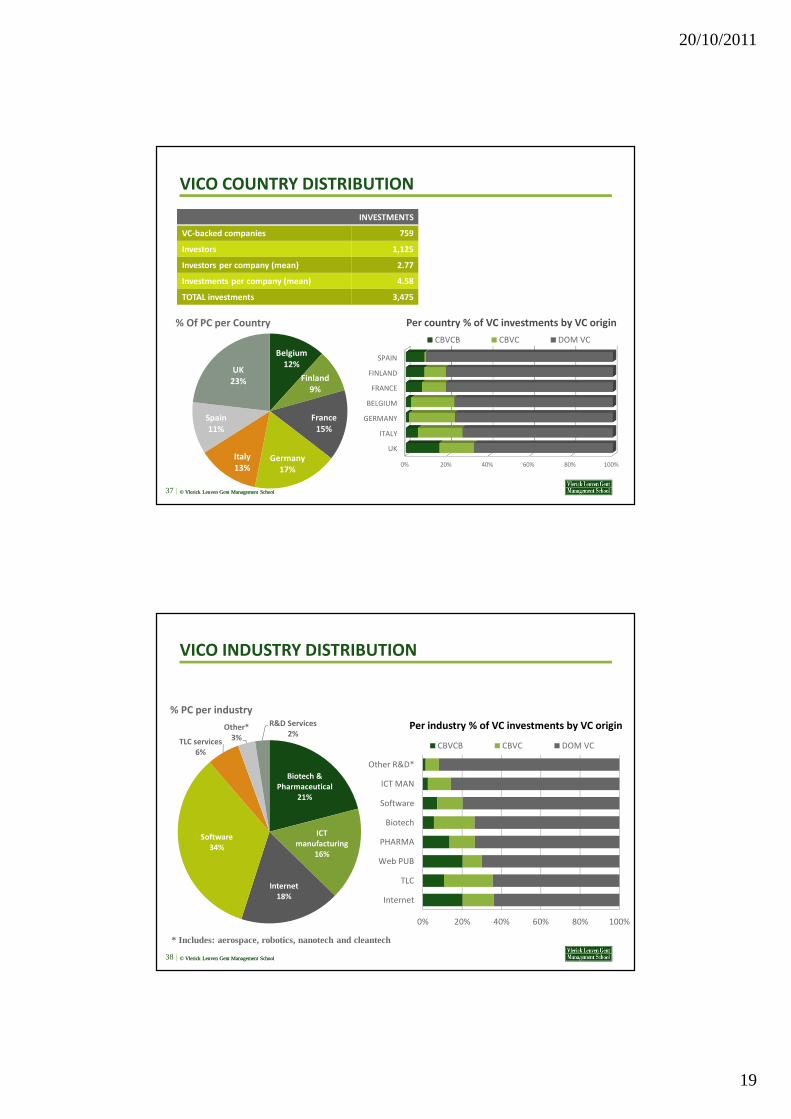

VICO COUNTRY DISTRIBUTION

37 |

INVESTMENTS

VC-backed companies 759

Investors 1,125

Investors per company (mean) 2.77

Investments per company (mean) 4.58

TOTAL investments 3,475

Belgium

12%

Finland

9%

France

15%

Germany

17%

Italy

13%

Spain

11%

UK

23%

% Of PC per Country

0% 20% 40% 60% 80% 100%

UK

ITALY

GERMANY

BELGIUM

FRANCE

FINLAND

SPAIN

Per country % of VC investments by VC origin

CBVCB CBVC DOM VC

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

VICO INDUSTRY DISTRIBUTION

38 |

Biotech &

Pharmaceutical

21%

ICT

manufacturing

16%

Internet

18%

Software

34%

TLC services

6%

Other*

3%

R&D Services

2%

% PC per industry

* Includes: aerospace, robotics, nanotech and cleantech

0% 20% 40% 60% 80% 100%

Internet

TLC

Web PUB

PHARMA

Biotech

Software

ICT MAN

Other R&D*

Per industry % of VC investments by VC origin

CBVCB CBVC DOM VC

20/10/2011

20

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

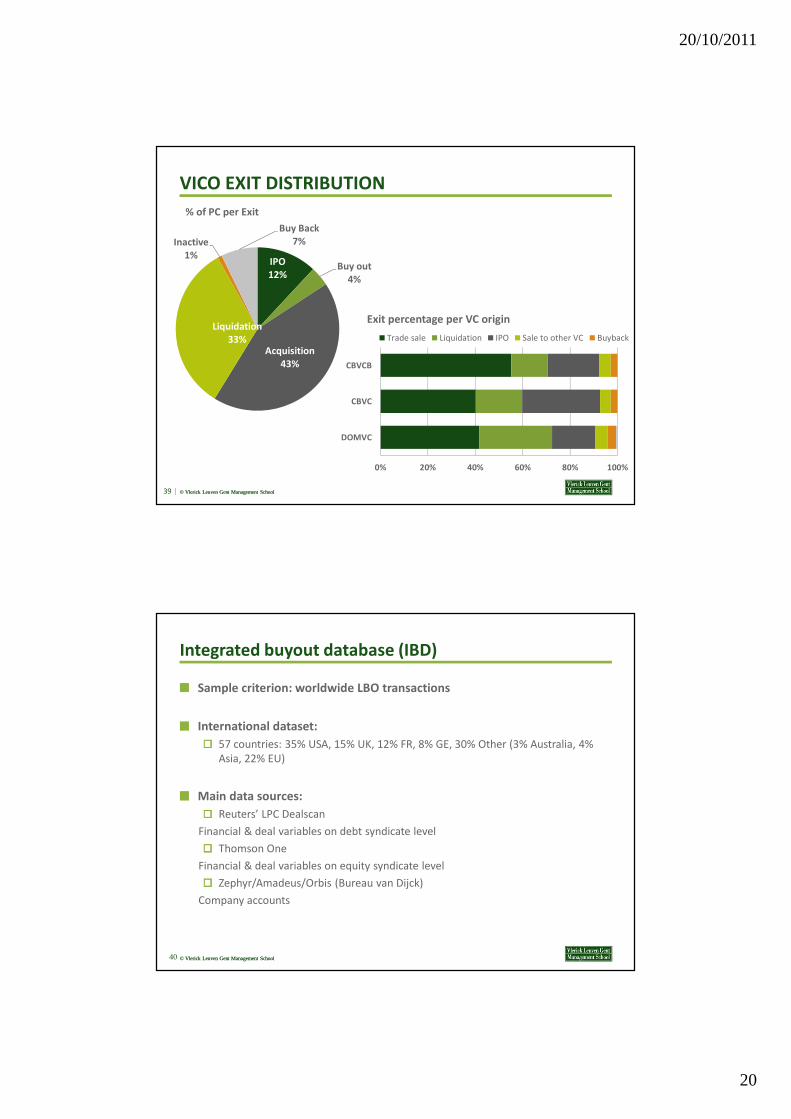

VICO EXIT DISTRIBUTION

39 |

IPO

12%Buy out

4%

Acquisition

43%

Liquidation

33%

Inactive

1%

Buy Back

7%

% of PC per Exit

0% 20% 40% 60% 80% 100%

DOMVC

CBVC

CBVCB

Exit percentage per VC origin

Trade sale Liquidation IPO Sale to other VC Buyback

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Integrated buyout database (IBD)

Sample criterion: worldwide LBO transactions

International dataset:

57 countries: 35% USA, 15% UK, 12% FR, 8% GE, 30% Other (3% Australia, 4%

Asia, 22% EU)

Main data sources:

Reuters’ LPC Dealscan

Financial & deal variables on debt syndicate level

Thomson One

Financial & deal variables on equity syndicate level

Zephyr/Amadeus/Orbis (Bureau van Dijck)

Company accounts

40

20/10/2011

21

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

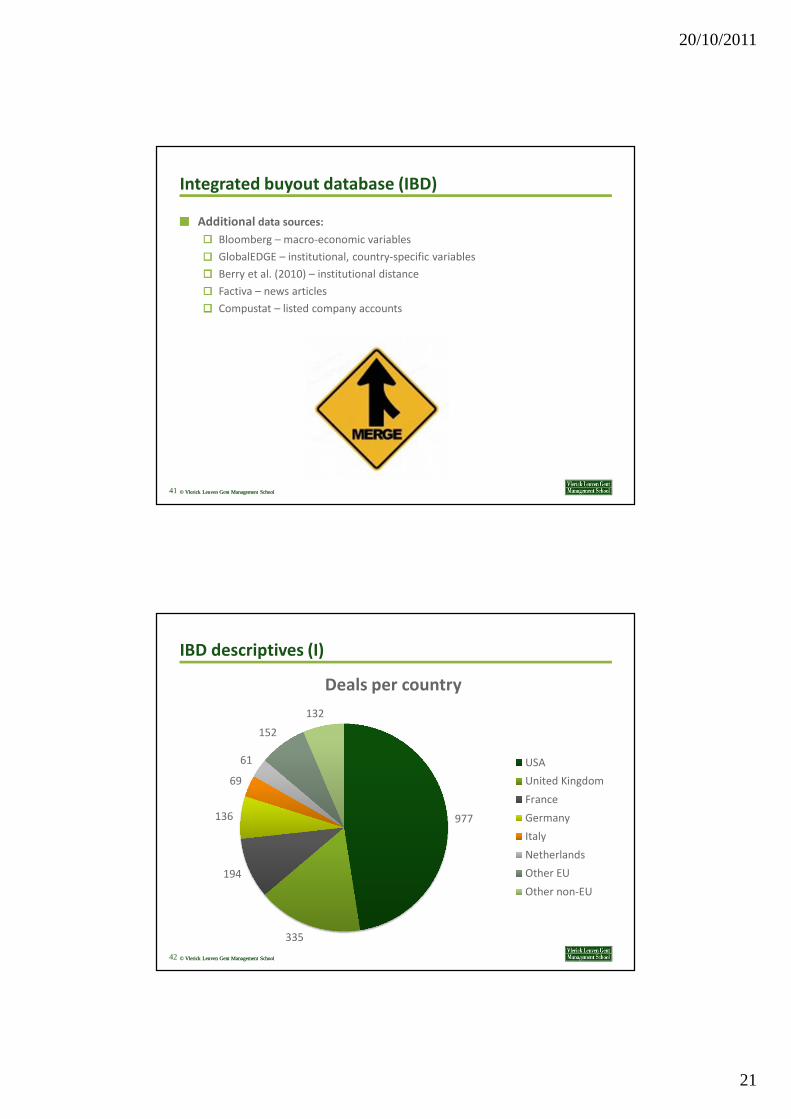

Integrated buyout database (IBD)

Additional data sources:

Bloomberg – macro-economic variables

GlobalEDGE – institutional, country-specific variables

Berry et al. (2010) – institutional distance

Factiva – news articles

Compustat – listed company accounts

41

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

IBD descriptives (I)

977

335

194

136

69

61

152

132

Deals per country

USA

United Kingdom

France

Germany

Italy

Netherlands

Other EU

Other non-EU

42

20/10/2011

22

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

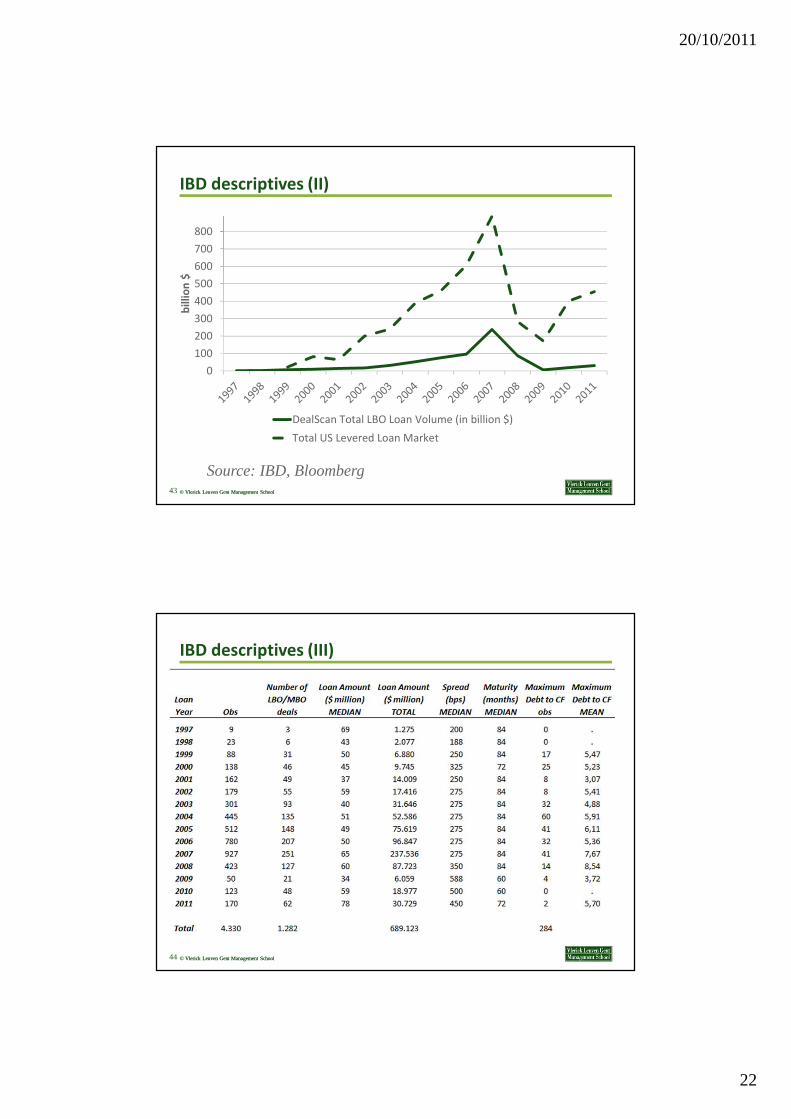

IBD descriptives (II)

0

100

200

300

400

500

600

700

800

bil

lio

n $

DealScan Total LBO Loan Volume (in billion $)

Total US Levered Loan Market

Source: IBD, Bloomberg43

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

IBD descriptives (III)

44

20/10/2011

23

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

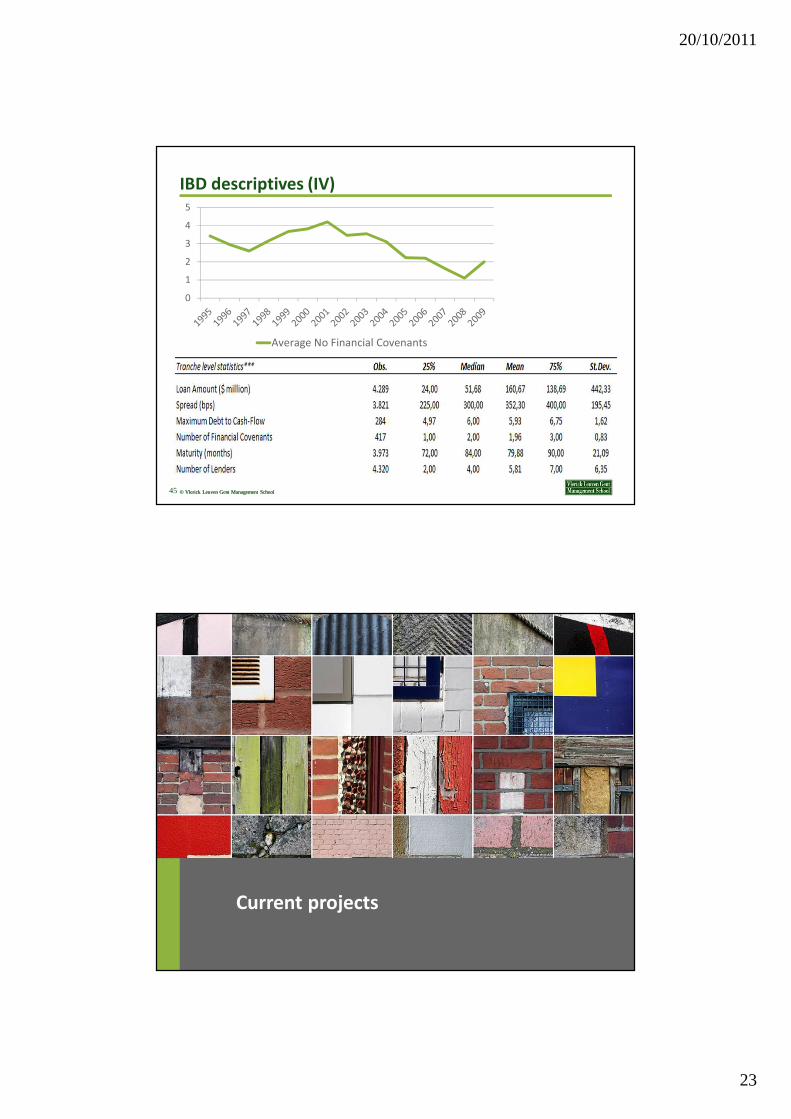

IBD descriptives (IV)

0

1

2

3

4

5

Average No Financial Covenants

45

Current projects

20/10/2011

24

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

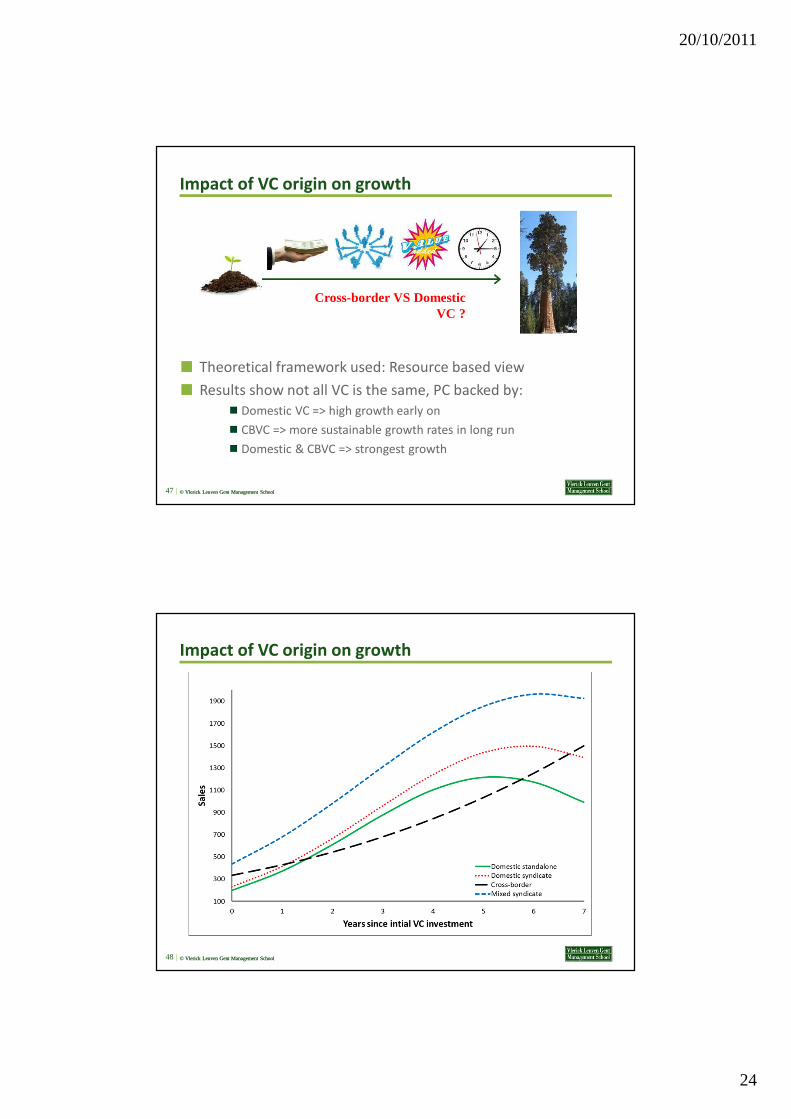

Impact of VC origin on growth

Theoretical framework used: Resource based view

Results show not all VC is the same, PC backed by:

Domestic VC => high growth early on

CBVC => more sustainable growth rates in long run

Domestic & CBVC => strongest growth

47 |

Cross-border VS Domestic VC ?

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Impact of VC origin on growth

48 |

20/10/2011

25

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Impact of VC origin on write-off exit

49 |

To achieve good performance VCs need to:

Nurture the promising PC

Avoid throwing good money after bad

VCs face “liquidation dilemma”

Further finance company => option of improvement

Terminating => sure losses

Theoretical framework used: escalation of commitment

CBVCs can both have advantages or disadvantages for PC:Provide access to specific international resources, networks and experience

Have a lower emotion commitment and face higher transaction costs and as they face larger geographic and cultural distances

=> RQ: “How does CBVC as opposed to domestic VC impact the speed and probability of a write-off exit”

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Belspo

Cost and terms of funding are key in (leveraged) buyout

transactions

Leverage, maturity, loan spreads

Covenants

Research question: How do PE firm characteristics and

institutional environment impact the cost and terms of funding

PE firm heterogeneity: reputation, experience, firm type, bank

relationships

Institutional environment: legal/fiscal framework

50

20/10/2011

26

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Belspo

Many LBO transactions end up in financial distress

Type and timing of exit are crucial to PE investors

History shows high levels of buyout company bankruptcies after peak

deal activity

Research question: How do PE firm characteristics and

institutional environment impact outcomes of financial distress

in buyouts

Impact of reputation, experience, firm type, syndicate structure,

institutional environment

Exit type (liquidation, bankruptcy, trade sale, …) / timing

51

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Ongoing research projects

VICO database

Impact of slack resources on company growth, differentiating between VC-

and non-VC backed firms (Ine Paeleman, Tom Vanacker)

Financing strategies of VC-backed firms (with Andy Heughebaert and Tom

Vanacker)

Differentiating between different types of VC firms

Which VC firms are able to raise follow-on VC funds?

With Mirjam Knockaert, Tom Vanacker

Preqin database

Focus on realised and unrealised returns, age, investment strategy,…

Management or finance paper

52

20/10/2011

27

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Do institutions helps VCs trust new partners?

What are drivers of partner selection decisions in cross-border

VC syndicates

Interaction of relational and institutional embeddedness

Normative, cognitive and legal institutions

European dataset with 1021 transcactions covering period 1997

till 2008

53

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

Buyouts and distress

Impact of multiple agency problems on outcomes of financial

distress in buyouts

Independent variables

Fundraising PE firm

Experience PE firms

Management teams

Banks

UK dataset with 416 distressed transactions

54

20/10/2011

28

Discussion

© Vlerick Leuven Gent Management School© Vlerick Leuven Gent Management School

How can your research berelevant for a VC/PE

context? What could youdo with our data?

20/10/2011

29

Thanks for listening

Feel free to send a mail for more questions / suggestions!