use of interest rate swaps by commercial banks: an ...spidi2.iimb.ernet.in/~networth/ccs/2006/121...

TRANSCRIPT

Use of Interest Rate Swaps by Commercial Banks: An Analysis of Determinants

Contemporary Course Study

Submitted To

Prof. Jayadev M.

ON August 28, 2007

BY

Chirag Thakral (0611016)

Sandeep Kumar (0611042)

INDIAN INSTITUTE OF MANAGEMENT, BANGALORE

ACKNOWLEDGEMENT

We express our sincere thanks to Prof. Jayadev M. (Finance & Control Area) for his

guidance and support extended to us in preparation of the study on “USE OF INTEREST

RATE SWAPS BY COMMERCIAL BANKS: AN ANALYSIS OF DETERMINANTS”. He has been

very helpful throughout the project and co-operated and guided us in the best possible way.

We have benefited a lot from the depth of his knowledge.

We are also extremely grateful to Mr. Srivatsan Sudersan, Bloomberg, Singapore, for being

so helpful and cooperative to us in procuring the data required for the project.

Finally we would like to express our heartfelt thanks to all those who have helped us in this

project.

1

Use of Interest Rate Swaps by Commercial Banks:

An Analysis of Determinants Chirag Thakral (0611016) Sandeep Kumar (0611042)

Prof. Jayadev M.

Indian Institute of Management Bangalore

August 28, 2007

Abstract

Banks like any profit making organisation face a variety of macroeconomic and microeconomic risks and

need to manage all these risks using different methods for their efficient functioning. In this study we develop an

analysis on hedging of the most significant of financial risks faced by the commercial banks i.e. interest rate risk, us-

ing the interest rate swaps. We also look at the revenue generation of banks by trading in interest rate swaps. Banks

interest rate exposure associated with a mismatch between assets and liabilities can be measured using traditional

GAP and duration GAP analysis. To fill this GAP a commercial bank uses derivatives instruments to adjust the

amount of assumed interest rate.

Interest rate swaps are the most popular financial derivatives used by the commercial banks. In this study the

effect of various bank specific parameters (size, profitability, capitalization, interest rate risk profile, creditworthiness,

Stock Price etc.) and economy specific parameters (interest rate volatility, market index etc.) on the interest rate swap

positions of the bank are examined. The study used the annual data of about 20 banks (from India, Singapore, Hong

Kong and Brazil) for a period of over 5 years from 2002-2006 and tried to find out the pattern of interest rate swap

usage for asset liability management by these banks. The various bank specific and economy wide parameters are re-

gressed using Panel Regression, against the notional amount of interest rate swaps obtained from the annual reports of

the bank.

The results suggest that the size, profitability, creditworthiness and interest rate risk profile of the bank are the

bank specific factors that play a major role in the banker’s decision to take interest rate swap position in the market

and the extent of the notional amount is dependent on these. The interest rate volatility is a result of the economy of

the country in which the bank operates and banks take position in the interest rate swap market accordingly to tackle

this factor. The stock market conditions for the bank as well as for the index are not a significant determinant.

Keywords: Interest Rate Swaps, Panel Regression, Commercial Banks, Interest Rate Risk

2

Introduction There are a number of risks banks face that are

typical of non financial firms. According to Hem-

pel et al (1994), financial risks are considered to

be the most critical risks faced by the banks. The

main concern of this study is the analysis of hedg-

ing used by commercial banks for financial risk,

in particular interest rate risk. Interest rate risk is

the risk that the market value of a bank‘s asset

declines due to a change in interest rates.

Looking at financial risks and in particular

interest rate risks from the management perspec-

tive, there are two different approaches managers

may adopt in controlling interest rate risk, namely

on-balance sheet adjustments and off-balance

sheet adjustments. Each has particular strengths

and weaknesses, and should be viewed not as

competing methodologies, but as alternatives

which might be appropriate in certain circum-

stances. On balance sheet adjustment involves the

adjustment of some of the bank‘s assets and li-

abilities in a way that the net effect of an interest

rate movement will not harm the market value of

these components and as a result the overall prof-

itability of the bank. The off-balance sheet ap-

proach involves the use of various non-traditional

financial products, widely known as derivative

instruments. These instruments appear neither on

asset nor on liability side.

In recent years, use of interest rate deriva-

tive products has increased significantly. The

Bank for International Settlements (BIS)

publishes statistics on the notional amounts

outstanding in the OTC (Over the Counter)

Derivatives market. The notional amount

outstanding as of December 2006 in OTC interest

rate swaps was $229.8 trillion, up $60.7 trillion

(35.9%) from December 2005. These contracts

account for 55.4% of the entire $415 trillion OTC

derivative market1.

Swaps based on Interest rate are mostly

used for hedging and speculation. All major

banks in world now have an active Derivatives

structuring desk for corporate wherein they offer

various swap products like Caps, Floors, Digitals,

LIBOR Range Accrual, CMS Spread Range

Accrual, Knock out swap, CMS Blade Range and

Snow range runner etc. for hedging and

speculation.

Figure 1.1 classifications of Bank Risks

1 http://en.wikipedia.org/wiki/Interest_rate_swap

3

An interest rate swap is a contractual agreement

entered into between two counterparties under

which each agrees to make periodic payment to

the other for an agreed period of time on the basis

of a notional amount of principal. Interest Rate

Swaps are typically used to create either synthetic

fixed or floating rate liabilities or assets in an ef-

fort to hedge against adverse movements in inter-

est rates. The floating rate index is usually pegged

to short-term interest rates, such as LIBOR or

one-month commercial paper.

Vanilla interest rate swaps are quoted in

terms of the fixed rate to be paid against the float-

ing index. The fixed rate is usually quoted as an

absolute rate, so a quote of 3% against 3-month

Libor would indicate that the fixed rate would be

3% pa. The fixed rates on vanilla swaps are called

swap rates. The swap curve is a yield curve com-

prising swap rates for different maturities. In

highly liquid USD swap market, the swap curve

has emerged as an alternative to Treasuries as a

benchmark for USD interest rates at maturities

exceeding a year. Swap markets serve as a link

between government debt, corporate debt and

money markets, across currencies and maturities.

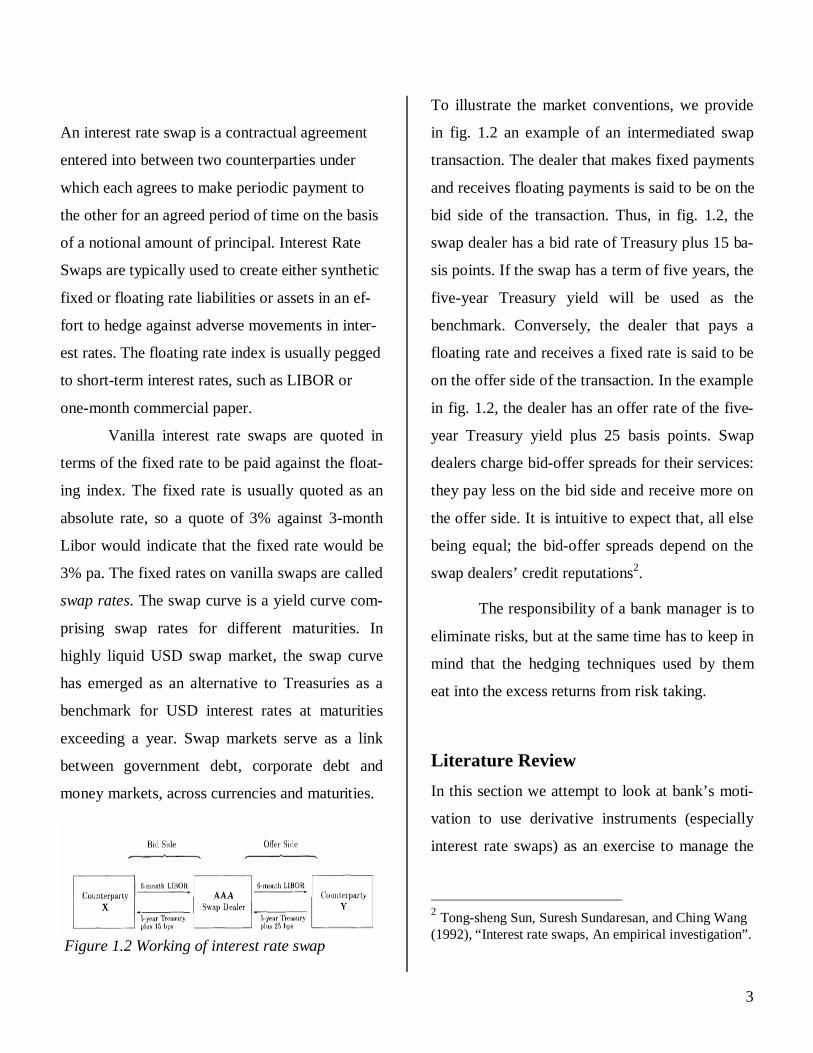

Figure 1.2 Working of interest rate swap

To illustrate the market conventions, we provide

in fig. 1.2 an example of an intermediated swap

transaction. The dealer that makes fixed payments

and receives floating payments is said to be on the

bid side of the transaction. Thus, in fig. 1.2, the

swap dealer has a bid rate of Treasury plus 15 ba-

sis points. If the swap has a term of five years, the

five-year Treasury yield will be used as the

benchmark. Conversely, the dealer that pays a

floating rate and receives a fixed rate is said to be

on the offer side of the transaction. In the example

in fig. 1.2, the dealer has an offer rate of the five-

year Treasury yield plus 25 basis points. Swap

dealers charge bid-offer spreads for their services:

they pay less on the bid side and receive more on

the offer side. It is intuitive to expect that, all else

being equal; the bid-offer spreads depend on the

swap dealers’ credit reputations2.

The responsibility of a bank manager is to

eliminate risks, but at the same time has to keep in

mind that the hedging techniques used by them

eat into the excess returns from risk taking.

Literature Review In this section we attempt to look at bank’s moti-

vation to use derivative instruments (especially

interest rate swaps) as an exercise to manage the

2 Tong-sheng Sun, Suresh Sundaresan, and Ching Wang (1992), “Interest rate swaps, An empirical investigation”.

4

asset liability mismatch by reviewing work done

in this area.

1) Generation of Income

The generation of fee income is a major incentive

for banks to provide risk-management services to

corporate clients. Smith (1993) argues that bank-

ers must recognize the potential benefits of selling

risk-management services. The obvious benefits

come from the generation of fee income and the

opportunities for bankers to create value through

cross-selling and enhanced customer relation-

ships. Less obviously, since hedging with deriva-

tives can reduce the probability of financial dis-

tress for client firms, banks also benefit by reduc-

ing their risk exposure to their customers.

2) Hedging activities

Most of the big banks use interest rate swaps for

income generation but the bank at lower end of

the spectrum use it to hedge against, or speculate

on, the movement of economic variables. Smith

and Stulz (1985) argue that hedging can reduce

the probability of bankruptcy by reducing the

variance of cash flows. Banks with a higher prob-

ability of financial distress would be most likely

to benefit from a hedging program. This implies

that banks with greater leverage, and hence a

greater probability of experiencing bankruptcy,

are more likely to use derivatives to hedge. The

business of banking includes a number of impor-

tant risk factors (for example, default or credit

risk, interest-rate risk, and foreign-exchange risk)

that may be related to the use of derivatives for

hedging purposes. An important consideration is

the interaction between interest-rate risk and

credit risk. Schrand and Unal (1998) investigate

hedging and coordinated risk management used

by thrifts to control both credit risk and interest-

rate risk. If banks are practicing coordinated risk

management, then the use of derivatives to hedge

interest-rate risk should also be related to a bank's

credit exposure. If banks use derivatives (to hedge

or speculate) in response to credit risk, a positive

relationship is expected to exist between loan

losses and derivatives use.

In addition to above papers we looked at the fol-

lowing papers:

Wall and Pringle (1989)

Wall and Pringle (1989) surveyed a set of 250

firms which had reported the use of interest rate

swaps. This study tried to find out the different

motives for using interest rate swaps. They found

that no single explanation is adequate in explain-

ing the behavior of all swap users. They found out

that the motives for using interest rate swaps dif-

fer between banks and other financial institutions

and the non financial institutions.

5

Song (2005)

Song (2005) examined the use of interest rate

swaps to manage earnings in the banking sector.

He finds that banks enter into swap arrangements

to increase (decrease) earnings when they would

have otherwise missed (exceeded) their target. In

a follow up analysis, he finds no evidence that

banks enter into offsetting swap arrangements in

subsequent periods to offset the interest rate risk

taken on by the initial swap arrangement.

Kim and Koppenhaver (1992)

Kim and Koppenhaver (1992) analysis focused on

whether interest rate exposure is a sufficient de-

terminant of a bank to engage in interest rate

swaps transactions. Thus, the authors tried to re-

late the interest rate swap position of the banks to

their interest rate risk profile. However, as Simons

(1995) mentioned in her study the very broad na-

ture of the data in the banks call reports make it

impossible to define such relationships with any

degree of precision. According to the findings of

the study the authors reported a positive relation-

ship between the long term interest rate exposure

of the bank and the extent of swap market partici-

pation. Thus, the study supported the hedging ar-

gument which requires the bank to increase its

hedging position along with the increase of its in-

terest rate exposure.

Moreover the study found that “the size of

interest rate swap positions, as measured by re-

ported notional values, is positively related to the

balance sheet mismatch one to five years forward,

the competitiveness of the bank's deposit market,

the bank's total asset size, primary capitalization

given the bank is a swap dealer, the relative size

of its commercial and industrial loans portfolio,

and futures trading. The study by Kim and Kop-

penhaver (1992) forms the first attempt to shed

some light on the pattern of interest rate swaps

use by commercial banks. It used the method of

regression but the factors used were not much.

L. Shanker (1996)

Shanker (1996) studied the effect that the use of

interest rate derivatives (futures, options, and

swaps) may have in hedging the interest rate risk

of large US commercial banks. Complete data on

stock returns and interest rate sensitive assets and

liabilities were collected for 360 banks over the

period 1986-1993. The study suggested that de-

rivatives usage by banks can effectively reduce

their interest rate risk. However, the study found

that when balance-sheet exposure is considered

the GAP measure is either the same or greater for

the group of banks that uses derivatives than for

the group of banks that does not use derivatives.

Thus, the above result was only supported when

the sensitivity of bank's stock returns to interest

rate changes was considered.

6

Sinkey and Carter (1997)

Sinkey and Carter (1997) examine cross-sectional

differences in the use of derivatives by banks in

an effort to identify the factors that cause banks to

use derivatives. The results of their study suggest

that many of banks' derivative activities can be

explained by the arguments of contemporary fi-

nance theory. Consistent with avoidance of the

costs of financial distress, they find that banks

with greater leverage (and lower capital-to-asset

ratios) are more likely to use derivatives. Incon-

sistent with this argument, however, they find that

banks with greater on-balance-sheet sources of

risk exposure, as reflected in large maturity gaps,

are less likely to use derivatives.

Lyes Boukrami (2002)

The Paper “The Use of Interest Rate Swaps by

Commercial Banks” by Lyes Boukrami, Graduate

Business School, and Manchester analyzed and

illustrated the relationship between one of the

most significant financial risks faced by banks i.e.

interest rate risk, and the interest rate swap. This

study developed a fixed effect model using cross

section data from US banks Annual Reports for

the Year 2001. The paper defined the Bank’s mo-

tives of using derivatives by giving variety of rea-

sons as were mentioned in various papers written

before this paper. The paper used annual data for

a number of US commercial banks and analyzed

the determinants of interest rate swap as a mean

of hedging the interest rate risk of the banks' port-

folios. The objective of this study was to deter-

mine which bank's characteristics best explain the

use of interest rate swaps by commercial banks in

order to hedge the interest rate risk of their portfo-

lios? These characteristics may include the bank's

size, capitalization, assets quality, interest rate

risk profile and the firm's revenue performance

(these were decided based on previous work done

on these topics). Moreover, the degree to which

these characteristics can explain the extent of that

use was also examined. The empirical result was

derived using hypothesis formulation and per-

forming regression on the data available. The re-

sults disclose a positive relationship between the

size of banks and the use of interest rate swaps. In

addition, the study has found that banks with bet-

ter asset quality tend to use interest rate swaps

more intensively than banks with weaker assets

quality.

Aim and Scope of the Study Although interest rate swaps have been the fastest

growing off-balance sheet product in emerging

markets, very less research has been conducted on

the analysis of which specific characteristics best

describe the use of interest rate swaps by banks

and which of these can describe the extent of that

use. Other than the bank specific factors like size,

profitability, stock price, creditworthiness and in-

terest rate risk profile of the bank, the economy

7

wide factors used are financial market index and

interest rate volatility. Although banks don’t dis-

close much about their strategy of portfolio man-

agement, this study analyses the relationship be-

tween various factors of bank and economy and

the position of bank in an interest rate swap.

Hence, the problem is to “Find out the determi-

nants and their extent of influence on the interest

rate swap positions of a commercial bank as a part

of their strategy of asset liability management.”

Methodology of Study and Motivation

In order to solve the above problem our study de-

velops a fixed effect model with the cross section

data for 5 years. The data used in this study was

obtained from annual reports of commercial banks

in India, Hong Kong, Singapore and Brazil for the

year 2002 to 2006. The sample size has been re-

stricted to include only the large banks from a

country as per Simons (1995) paper, which

proved that interest rate swap use is much more

widespread among large banks. The resulting

sample includes 20 banks. The notional amount of

the interest rate swaps used for asset-liability pur-

poses is regressed against the specific characteris-

tics of the banks and economies. The computing

software used for the calculation of the results is

EViews 5.0.

Selection of the variables

In order to select factors which should be exam-

ined to find out the dependence of interest rate

swap exposure of a bank the model developed by

Simons (1995) was employed. The study by

Simons was selected since it provides similar re-

search issues with one of the aims of this study.

This study deals with the emerging markets as

compared to the study by Simons. Moreover, this

study deals with a smaller dataset than Simons

attributed to the limited period of time available

during the face of data collection.

The limited number of studies conducted in the

area of derivatives use by commercial banks sug-

gests that all the authors have more or less used

the same parameters in order to explain the use of

these activities by banks, each one using different

proxies to capture the effects of these parameters.

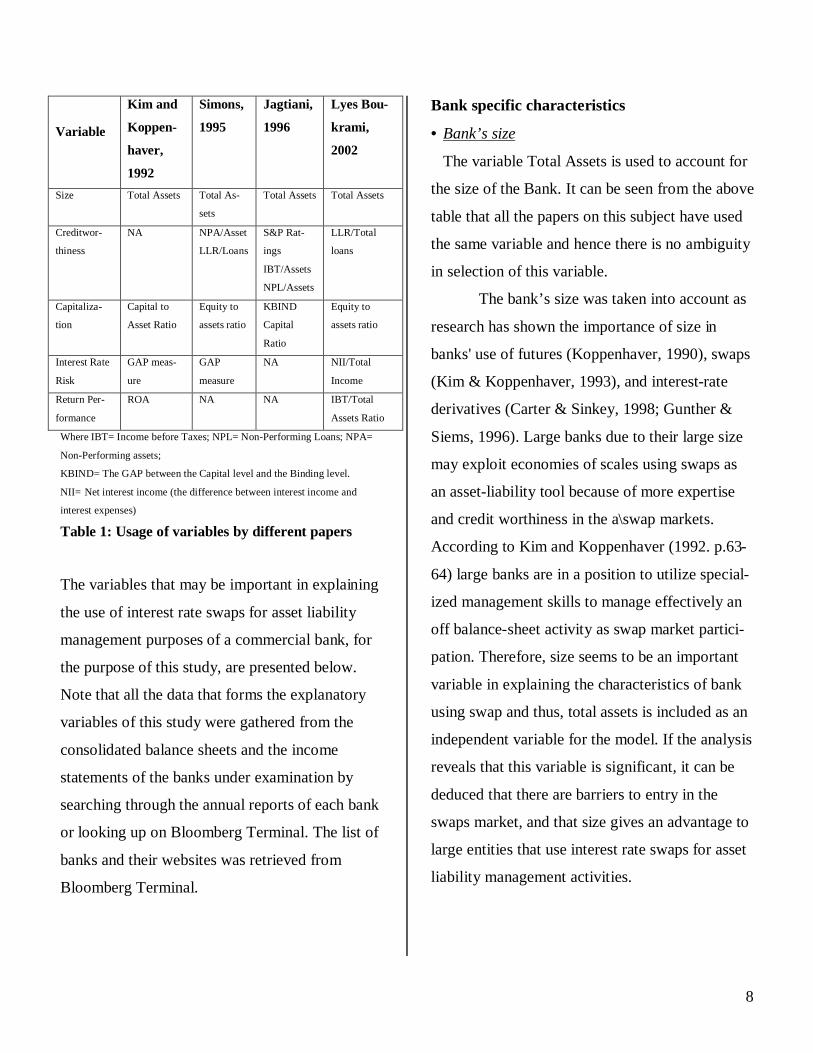

The most common variables that appear in most

of these studies are (i) the bank's size, (ii) the

bank‘s capital position, (iii) the bank‘s credit wor-

thiness and, (iv) bank‘s interest rate risk profile

(v) and the bank revenue performance. The table

given below provides the most commonly used

parameters by some of the most recent studies on

derivatives use by commercial banks

8

Variable

Kim and

Koppen-

haver,

1992

Simons,

1995

Jagtiani,

1996

Lyes Bou-

krami,

2002

Size Total Assets Total As-

sets

Total Assets Total Assets

Creditwor-

thiness

NA NPA/Asset

LLR/Loans

S&P Rat-

ings

IBT/Assets

NPL/Assets

LLR/Total

loans

Capitaliza-

tion Capital to

Asset Ratio

Equity to

assets ratio KBIND

Capital

Ratio

Equity to

assets ratio

Interest Rate

Risk

GAP meas-

ure

GAP

measure

NA NII/Total

Income

Return Per-

formance

ROA NA NA IBT/Total

Assets Ratio Where IBT= Income before Taxes; NPL= Non-Performing Loans; NPA=

Non-Performing assets;

KBIND= The GAP between the Capital level and the Binding level. NII= Net interest income (the difference between interest income and

interest expenses)

Table 1: Usage of variables by different papers

The variables that may be important in explaining

the use of interest rate swaps for asset liability

management purposes of a commercial bank, for

the purpose of this study, are presented below.

Note that all the data that forms the explanatory

variables of this study were gathered from the

consolidated balance sheets and the income

statements of the banks under examination by

searching through the annual reports of each bank

or looking up on Bloomberg Terminal. The list of

banks and their websites was retrieved from

Bloomberg Terminal.

Bank specific characteristics

• Bank’s size

The variable Total Assets is used to account for

the size of the Bank. It can be seen from the above

table that all the papers on this subject have used

the same variable and hence there is no ambiguity

in selection of this variable.

The bank’s size was taken into account as

research has shown the importance of size in

banks' use of futures (Koppenhaver, 1990), swaps

(Kim & Koppenhaver, 1993), and interest-rate

derivatives (Carter & Sinkey, 1998; Gunther &

Siems, 1996). Large banks due to their large size

may exploit economies of scales using swaps as

an asset-liability tool because of more expertise

and credit worthiness in the a\swap markets.

According to Kim and Koppenhaver (1992. p.63-

64) large banks are in a position to utilize special-

ized management skills to manage effectively an

off balance-sheet activity as swap market partici-

pation. Therefore, size seems to be an important

variable in explaining the characteristics of bank

using swap and thus, total assets is included as an

independent variable for the model. If the analysis

reveals that this variable is significant, it can be

deduced that there are barriers to entry in the

swaps market, and that size gives an advantage to

large entities that use interest rate swaps for asset

liability management activities.

9

Hypothesis

H10: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool and the size of the bank.

H11: A significant relationship exists between the

usage of interest rate swaps as an asset liability

management tool and the size of the bank.

• Bank’s Creditworthiness

The ratio of the Non Performing Assets (NPA)

to the total assets, accounts for the creditworthi-

ness or asset quality of a given bank. This ratio

gives the percentage of bad loans with respect to

the total loans given. Banks with relatively poor

asset quality (as measured by high levels of Non

Performing Assets to total assets), will need to

conserve capital and may find interest rate swaps

as a more desirable, capital efficient way to man-

age their balance sheet.

Hypothesis

H20: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool and the NPA ratio of the bank.

H21: There is a significant relationship between

the usage of interest rate swaps an asset liability

management tool and the NPA Ratio of the bank.

• Bank’s Capitalization

The equity to assets ratio is used to find out the

capitalization for a bank. This is in accordance

with most of the papers on this subject as can be

seen in the table given above. As the capital of a

bank increases, the bank’s risk handling ability

increases and hence the need for use of interest

rate swap (for hedging purposes) decreases.

Hence to investigate this relationship the variable

equity to assets ratio has been included in the

model. Moreover, Kim and Koppenhaver (1992)

also point out bank capital is an important dimen-

sion that has to be considered when choosing to

participate in swaps market.

Hypothesis

H30: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool and the equity to assets ratio of the

bank.

H31: There is a significant relationship between

the usage of interest rate swaps an asset liability

management tool and the equity to assets ratio of

the bank.

• Bank’s Interest rate risk exposure

The ratio of net interest income (the difference

between interest income and interest expenses) to

total income (appears in the income statement as

net income: the sum of net interest income and net

non-interest income) is used to measure the inter-

est rate risk exposure of the bank without taking

the interest rate swap into consideration. This

measure is included unlike the GAP measures

used by other studies (Kim and Koppenhaver,

1992; Simons, 1995) in order to avoid a major

11

match a bank may open a position in the interest

rate swaps.

Hypothesis

H60: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool and the Stock Price of the bank.

H61: A significant relationship exists between the

usage of interest rate swaps as an asset liability

management tool and the Stock Price of the bank.

Economy specific characteristics

• Stock Market index performance

The market index of the most prominent stock

exchange of a country is used as a measure of the

market performance of the country. With the

change in the market performance of the econ-

omy, the assets side of the bank’s balance sheet

may change. This may cause an asset liability

mismatch in the bank’s balance sheet. To care of

this mismatch a bank may open a position in the

interest rate swaps.

Hypothesis

H70: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool for a bank and the market index of

the stock exchange of the country.

H71: A significant relationship exists between the

usage of interest rate swaps as an asset liability

management tool for a bank and the market index

of the stock exchange of the country.

• Interest rate volatility

The ratio of standard deviation to mean of the

interest rate of an economy is used as a measure

of the market performance of the country. The

measure of the deviation of the interest rate with

respect to the mean interest rate is a safe measure

for the volatility of the markets (or interest rates).

Frequent changes in the interest rate of an econ-

omy will affect the positions of various banks in

the interest rate swaps.

Hypothesis

H80: There is no relationship between the usage

of interest rate swaps as an asset liability man-

agement tool for a bank and the interest rate vola-

tility of the country.

H81: A significant relationship exists between the

usage of interest rate swaps as an asset liability

management tool for a bank and the interest rate

volatility of the stock exchange of the country.

The summarization of all the above selection of

variables is done in the table given below:

Variable Used Representative for Total assets Size NPA/Total Assets Creditworthiness/Asset

Quality Equity-to-Assets Ratio Capitalization Net Interest Income / Total Income

Interest Rate Risk exposure

Profit before Tax / Total Assets

Profitability

Stock Price of Bank Bank’s Market Performance Market Index of stock ex-change of country

Market’s performance

Standard deviation/mean of the interest rate of country

Market Volatility

Table 2: Variables used for various parameters

12

Results

Descriptive statistics All the data is collected and converted into USD

for consistent results. Table given below provides

some preliminary descriptive statistics for the

variables used in the empirical analysis. A total of

80 observations of the banks have been used. The

notional principal of swaps used for asset liability

management averaged $505,209.69 million and

ranged from $911 million to $6,749,847 million.

The Bank size as measured by the assets size had

an average of $127,974 million, but most of the

banks in the sample have a lower amount of as-

sets. The largest bank in the sample is HSBC with

a total amount of assets of $1,860,758 million,

whereas the smallest bank was UTI Bank with

total assets of $4,049 million.

The Asset quality on an average is 1.22%

with a variation of 1.27%, representing the variety

in the types of the banks in the sample. The prof-

itability of BANCO ITAU bank is highest at

4.875% with the average profitability of the sam-

ple of the banks at only 1.56%.

In terms of Market index performance of each

country, the sample is very much varied with a

standard deviation of 4949.45 and with the best

valued index of Brazil at 20,818.6 in 2006 and

worst valued index of India at 70.39 in 2002.

Table 3: Descriptive summary of Bank Data

Vari-able

N Min Max Mean Std. Devia-tion

Total as-sets (Mil-lion USD)

80 4,049 1,860,758 127,974 294508.9684

NPA/Total Assets 80 0 0.05284 0.01223 0.012729715

Equity-to-Assets Ratio

80 0.00093 0.11928 0.04913 0.045089438

Net Inter-est Income / Total Income

80 0 0.75758 0.39461 0.192685056

Profit be-fore Tax / Total As-sets

80 0.00439 0.04875 0.01563 0.007468489

Stock Price of Bank

80 0.26264 36.23170 7.07589 6.86613013

Market Index of stock ex-change of country

80 70.3967 20,818.6 2,708.278 4949.453003

Standard devia-tion/mean of the in-terest rate of country

80 0.01870 0.21045 0.14132 0.056806605

13

Regression Results The data we have used to do regression is a time-

series data available for around 5 years for differ-

ent banks, which makes the sample data as cross-

sectional data. So we have used the Panel Regres-

sion to regress the interest rate swap notional val-

ues of the banks against the bank and economy

specific factors. Following Results were obtained:

Table 4: Regression Results Summary Table The R-square of the model equals 74.3% and the

R-square adjusted of the model equals to 71.5%,

which are both consistent. This means that 71.5%

of the changes in the interest rate swaps are due to

the variations of the independent variable used in

the model. This supports the good selection of the

proxies.

Analysis of Hypothesis Size of the Bank

The regression results in table shows that there is

a positive relationship between the use of interest

rate swaps and size. The variable's total asset co-

efficient has a positive sign and equals to 0.4325

in its regression coefficient and is a significant

variable. So we must reject the null hypothesis

and accept that ‘a significant relationship exists

between the usage of interest rate swaps as an

asset liability management tool and the size of

the bank’. It can be deduced that the size and the

expertise, as well as skill, that may be implicitly

available to large banks, give a comparative ad-

vantage to these entities in using interest rate

swaps for hedging and trading applications.

Creditworthiness

By using the NPA to total assets ratio as the vari-

able of the asset quality of the bank, the regres-

sion results in table shows that there is a negative

relationship between the use of interest rate swaps

and asset quality of the banks assets. The vari-

able's coefficient has a negative sign and equals to

Dependent Variable: INTEREST RATE SWAP

Method: Least Squares

White Heteroskedasticity - Consistent Standard Errors & Covariance

Included observations: 80

Variable Coefficient Std. Error t-Statistic Prob.

TOTALASS 0.432594 0.055559 7.786160 0.0000

CAPITAIS 1557281. 1048973. 1.484577 0.1424

PROFITAB 7096655. 3075197. 2.307708 0.0242

INTERSTR 219241.0 94472.64 2.320683 0.0234

CREDITWO -5576091. 1414314. -3.942612 0.0002

STOCKPRI -1704.937 2134.464 -0.798766 0.4273

MARKETIN -56.81285 54.22311 -1.047761 0.2986

INTERE_A -799486.7 363000.8 -2.202438 0.0311

R-squared 0.742724 Mean dependent var 76707.22

Adjusted R-squared 0.715437 S.D. dependent var 176841.9

S.E. of regression 94335.31 Akaike info criterion 25.84890

Sum squared resid 5.87E+11 Schwarz criterion 26.09799

Log likelihood -948.4095 Durbin-Watson stat 0.922159

14

-5576091 in its regression coefficient and is a sig-

nificant variable with p-value equal to 0.0002. So

we must reject the null hypothesis and accept that

‘There is a significant relationship between the

usage of interest rate swaps an asset liability

management tool and the NPA Ratio of the

bank’.

This suggests that banks with stronger asset qual-

ity tend to be a bigger user of interest rate swaps

than banks with relatively weaker asset quality.

Therefore, our study is in line with earlier studies

to conclude that swaps are perceived by regulators

as risky and banks with weak assets quality are

subject to more scrutiny by regulators when they

attempt to use swaps.

Capitalisation

The regression results in table shows that there is

no relationship between the use of interest rate

swaps and capitalisation. The variable's total asset

coefficient has a positive sign and equals to

1557281 in its regression coefficient, but the p-

value of 0.14 suggests that it is not a significant

variable to determine the interest rate swap posi-

tion. So we must accept the null hypothesis and

accept that ‘There is no relationship between the

usage of interest rate swaps as an asset liability

management tool and the equity to assets ratio of

the bank’.

Inconsistent with the findings from the

Lyes Boukrami (2002) study for the US banks,

the view that Bank capital significantly enhances

the swaps participation is refuted in our sample.

These findings highlight the importance of distin-

guishing the determinants of swaps participation

from the factors influencing the extent of swaps

participation.

Interest rate risk exposure

As per Kim and Koppenhaver, 1992 there is ex-

pected to be a positive relationship that would sat-

isfy the hedging argument that higher the interest

rate risk profile of the bank, the higher would be

its interest rate swap hedging position. The re-

gression results in table shows that there is a posi-

tive relationship between the use of interest rate

swaps and the interest rate risk profile. The vari-

able's coefficient has a positive sign and equals to

219241.0 in its regression coefficient and is a sig-

nificant variable with p-value of 0.0234. So we

must reject the null hypothesis and accept that

‘There is a significant relationship between the

usage of interest rate swaps an asset liability

management tool and the bank’s interest rate

risk exposure (Net Interest Income to Total In-

come ratio) of the bank.’

Profitability

The regression results in table shows that there is

a positive relationship between the use of interest

rate swaps and profitability of the bank. The vari-

15

able's coefficient has a positive sign and equals to

7096655 in its regression coefficient. Profitability

of a bank comes out to be a significant variable in

the usage of interest rate swap with p-value

0.0242. So we must reject the null hypothesis and

accept that ‘A significant relationship exists be-

tween the usage of interest rate swaps as an asset

liability management tool and the Income before

Taxes to Total Assets ratio of the bank’.

Bank’s Stock market performance

The regression results in table shows that there is

no relationship between the use of interest rate

swaps and Stock Price of the bank. The variable's

coefficient has a negative sign and equals to -

1704.937 in its regression coefficient, but the p-

value of 0.4276 suggests that it is not a significant

variable to determine the interest rate swap posi-

tion. So we must accept the null hypothesis and

accept that ‘There is no relationship between the

usage of interest rate swaps as an asset liability

management tool and the Stock Price of the

bank’.

Country’s Stock Market index performance

The regression results in table shows that there is

no relationship between the use of interest rate

swaps and Stock Market index. The variable's co-

efficient has a negative sign and equals to -56.81

in its regression coefficient, but the p-value of

0.2986 suggests that it is not a significant variable

to determine the interest rate swap position. So

we must accept the null hypothesis and accept that

‘There is no relationship between the usage of

interest rate swaps as an asset liability manage-

ment tool and the market index of the stock ex-

change of the country’.

Interest rate volatility

The regression results in table shows that there is

a negative relationship between the use of interest

rate swaps and interest rate volatility of the coun-

try. The variable's coefficient has a negative sign

and equals to 799486.7 in its regression coeffi-

cient. Interest rate volatility of a country comes

out to be a significant variable in the usage of in-

terest rate swap with p-value 0.0311. So we must

reject the null hypothesis and accept that ‘A sig-

nificant relationship exists between the usage of

interest rate swaps as an asset liability manage-

ment tool for a bank and the interest rate volatil-

ity of the stock exchange of the country.’

16

Key Interpretations & conclusions After analyzing the data of 20 top commercial

banks of some of the emerging markets, our study

sheds some light on the factors which influence

the use of interest rate swaps for asset liability

purpose by the banks. The study has found that

larger the bank, higher will be their position in the

interest rate swap market. This can also be attrib-

uted to the fact that larger the banks, better are the

technical expertise and better the customer rela-

tionship and hence easier for them to get involved

in swaps and derivative activities.

In addition, the study has found that banks with

better asset quality tend to be more intensive users

of interest rate swaps, than those with weaker as-

set quality. There is very little publicly available

information on the swap positions of banks. This

means that it is very difficult to estimate the expo-

sure of interest rate movements.

As per the earlier studies as the capital of a

bank increases, the bank’s risk handling ability

increases and hence the need for use of interest

rate swap (for hedging purposes) decreases. But

our study concludes that capitalization of the bank

is not much related to the interest rate swap posi-

tion in the market. The Study also concludes that

banks with higher profitability manage their risk

better than other banks and hence take bigger po-

sitions in the interest rate swap market. The con-

clusion that interest rate risk profile of the bank

has a consistent relationship with the use of inter-

est rate swaps came as per our expectations.

From the economic factors considered to

play an important role in the interest rate swap

positions of the banks, only the interest rate vola-

tility proved out to be a significant factor as fre-

quent changes in the interest rate of an economy

will have to be managed by banks, which affect

the positions of various banks in the interest rate

swaps. The stock price or stock market index are

not a factor in the banker’s decision to take posi-

tions in the interest rate swap market.

Irrespective of whether swaps are for

hedging or speculating, the positive relationship

between interest rate exposure and swap activity,

if it exists, may not imply that the market does not

care about the bank's risk and allow risky banks to

be more active as guarantors in the swap market.

Depending on the risk propensity of the institu-

tion, risk can be controlled using a wide variety of

techniques that fall into two broad categories,

namely direct and synthetic methods. Direct re-

structuring of the balance sheet involves the

changing of the contractual characteristics of the

bank‘s assets and liabilities in a way that a par-

ticular duration or maturity can be achieved. Since

direct restructuring may not be always possible or

desired, the synthetic method comes to comple-

ment the drawbacks of the direct method and to

add a certain degree of flexibility to the asset li-

ability management process. The synthetic

17

method relies on the use of capital markets in-

struments; such as interest rate swaps, interest rate

futures and interest rate options; and customized

agreements to alter the balance sheet risk expo-

sure. Among these instruments, interest rate

swaps are considered to be the most widely

used instrument for hedging against interest rate

risk.

Limitations One problem that we encountered during the

study is the limited disclosure of interest rate

swap information by the banks. Most of the banks

only disclose the notional amount of swaps in

their annual reports, which doesn’t provide com-

plete information about the risks of interest rate

swap transactions. Russian banks don’t disclose

their interest rate swap positions in their annual

reports. So there is a need of a more detailed dis-

closure by the banks.

Another limitation was the difficulty in

identifying the interest rate swap from other

swaps mentioned in the annual reports. In many

cases, interest rate swaps include plain vanilla

fixed for floating swaps, basis swaps, index-

amortizing swaps, and other, more exotic types of

swaps contracts. Different countries have different

disclosure norms and hence different level of in-

terest rate swap disclosure.

Studying the commercial banks of emerg-

ing markets made the information extraction a

little more difficult as the data disclosure is not

very high outside US banks. The language in

which banks in different countries disclose their

annual reports also limited the scope of our study.

For Example the Chinese banks couldn’t be stud-

ied because of annual reports being published in

Chinese language. We believe that in future more

disclosure information will be available in public

domain for interest rate swaps, which will make

the empirical study of the interest rate swap issues

by researchers more interesting and reliable.

About the Authors Prof. Jayadev M is a professor in the Finance

and Control at the Indian Institute of Management

Bangalore.

Chirag Thakral is a second-year student at the

Indian Institute of Management, Bangalore.

Sandeep Kumar is a second-year student at the

Indian Institute of Management, Bangalore

18

References 1. Ahmed . A S Beatty. A, Takeda . C , (1997),

"Evidence on Interest risk management and derivatives usage by commercial banks", working paper, University of Rochester, NY.

2. Arnold, T.S. (1984). “How To Do Interest

Rate Swaps”, Harvard Business Review. Sep-tember/October, pp. 96-101.

3. Aspinwall, R. (1982). “Managing Interest

Rate Risk.“ In: Proceedings of a Conference on bank structure and Competition. Chicago: Federal Reserve Bank of Chicago, pp.463-470.

4. Badger, P. (1995), “Financial insurance, Inter-

est Rate Risk, and Derivatives”, Bankers Magazine, volume 178, number 3, May/June. p.32-37.

5. Barton, J. “Doe the Use of Financial Deriva-

tives Affect Earnings Management Deci-sions?" The Accounting Review 76 (2005): 1-26.

6. Bicksler, J. and Chen, A.H. (1986). “An Eco-

nomic Analysis of Interest Rate Swaps“. Jour-nal of Finance, volume 41, July, pp. 645-655.

7. Carter.D.A & Sinkey J.F , (1996); " An em-

pirical investigation into the use of interest rate derivatives by US commercial banks. Working paper. Athens, GA: University of Georgia.

8. Carter.D.A & Sinkey J.F , (1998); " The use

of interest rate derivative by end users: the case of large community banks, Journal of Fi-nancial Services Research 14 pp17-34.

9. Colquitt. L.L & Hoyt. R.E, (1997), "Determi-

nants of corporate hedging behaviour," Jour-nal of Risk and Insurance, Vol 64

10. Flannery. M.J & James. C.M, (1984), "The effects of interest rate changes on the common stock returns of financial institutions," Journal of Finance, Vol 39, pp 1141-1153.

11. Felgran, S.D. (1987). “Interest Rate Swaps:

Use, Risk. and Prices”, New England Eco-nomic Review. November/December, pp. 22-32.

12. Geczy. C, Minton. B.A, and Schrand. C,

(1997), "Why firms use currency derivatives," Journal of Finance, Vol 52, pp1323-1354.

13. Goodman, Laurie S., (1990) “The use of in-

terest rate swaps in managing corporate li-abilities”, Journal of Applied Corporate Fi-nance, 2 (4), 35-47.

14. Gunther. J.W, & Siems. T.F, (1996), "the like-

lihood and extent of bank participation in de-rivatives activities," Financial Industry Stud-ies, Federal Reserve Bank of Dallas, Dallas, TX.

15. Haight, T.G. and Kehly, J.C.Jr. (1995). “The

Role of Derivatives as an Asset/Liability Management Tool”. Bankers Magazine, vol-ume 178, number 3, May/June, p.22-26.

16. Jagtiani, J. (1996). “Characteristics of Banks

that are More Active in the Swap Market”. Journal of Financial Services Research, vol-ume 10, pp. 131-141.

17. Jong and Driessen (1999) "LIBOR versus

Swap Market Models: An Empirical Compari-son", European Finance Review, 5(3), 201-237.

18. Kim, S. and Koppenhaver, G.D. (1992). ‘An Empirical Analysis of Bank Interest Rate Swaps”. Journal of Financial Services Re-search. volume 7. number 1. pp. 57-72

19. Kangis. P, Elgar. J and Haar L, (1998), "The

use of Derivatives Instruments for Hedging

19

Purposes," Journal of Financial Services Mar-keting, Vol 3, No 1, p 81.

20. Kuprianov, Anatoli. (Summer 1994) The role

of interest rate swaps in corporate finance, Economic Quarterly, 80, 49-68.

21. Kwan. S.H, (1991), "Re-examination of inter-

est rate sensitivity of commercial banks stock returns using of random-coefficient model," Journal of Financial Services Research, Vol 5, pp 61-76.

22. Litzenberger, R.H. (1992). “Swaps: Plain and

Fanciful”. Journal of Finance, volume 47, number 3, pp. 831-850.

23. Loeys, G.J. (1985). “Interest Rate Swaps: A

New Tool for Managing Risk“. Federal Re-serve Bank of Philadelphia, Business Review, May/June, pp. 17-25.

24. Lyes, Boukrami (2002), “The Use of Interest

Rate Swaps by Commercial Banks”, Man-chester Metropolitan University

25. Remolona E.M. and P.D. Wooldridge (2003)

‘The Euro Interest Rate Swap Market’, BIS Quarterly Review, March.

26. Ronn.E.L, Verma. A.K, (1986)," Pricing the risk adjusted: An option based model," Jour-nal of Finance, Vol 41, pp 871-896.

27. Rudnick, L.T. (1987). “Discussion of Practical

Aspects of Interest Rate Swaps”. In Proceed-ings of a Conference on Bank Structure and Competition. Chicago: Federal Reserve Bank of Chicago, pp. 206-213.

28. Sinkey. J.F and Carter. D.A, (1997), " Evi-

dence on Financial Characteristics of banks that do and do not use derivatives," Working Paper, University of Georgia, Athens.

29. Smith Clifford W and Rene Stulz, (1985), "

The Determinants of Firms' Hedging Poli-

cies", Journal of Financial and Quantitative Analysis 20 , No . 4, pp. 583-601.

30. Shanker, L. (1996). “Derivatives Usage and

Interest Rate Risk of Large Banking Firms”. The Journal of Futures Markets, volume 16, number 4, pp. 459-474.

31. Simons, K. (1993). “Interest Rate Structure

and the Credit Risk of Swaps”. New England Economic Review, July/August, pp. 23-34.

32. Simons, K. (1995). “Interest Rate Derivatives

and Asset-Liability Management by Commer-cial Banks”. New England Economic Review, January, February, p.l7-28.

33. Smith, C. W., Smithson, C.W., Wakeman,

L.M. (1988). “The market for interest rate swaps”. Financial Management 17, (4), 34 -44, Winter.

34. Song, C. J. “Are Interest Rate Swaps Used to

Manage Bank Earnings?" Working paper, Michigan State University, 2005.

35. Sun, T.S., Sundaresan, S., and Wang, C.

(1993). “Interest Rate Swaps: An empirical Investigation”. Journal of Financial Econom-ics, volume 34, number 1, pp. 77-99.

36. Venkatachalam M. “Value-Relevance of

Banks’ Derivatives Disclosures.” Journal of Accounting and Economics 22 (1996)

37. Wright, W.M. and Houpt, J.V. (1996). “An

Analysis of Commercial Bank Exposure to in-terest Rate Risk”. Federal Reserve Bulletin, volume 82, number 2, February, p.l15-128.

38. Yu, W.T. and Pang, W.K. and Li, L.K. (2002)

“Borrowing cost reduction by interest rate swaps––an option pricing analysis,” Euro-pean Journal of Operational Research 154 (2004) 764–778.

39. Bloomberg Database