u.s. insurance industry outlook trends to look out for · u.s. insurance industry outlook trends to...

TRANSCRIPT

0Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Presented by

Stephan Christiansen, FCAS, MAAAManaging Director

U.S. Insurance Industry OutlookTrends to Look Out For

Placeholder for Head Shot if desired

1Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

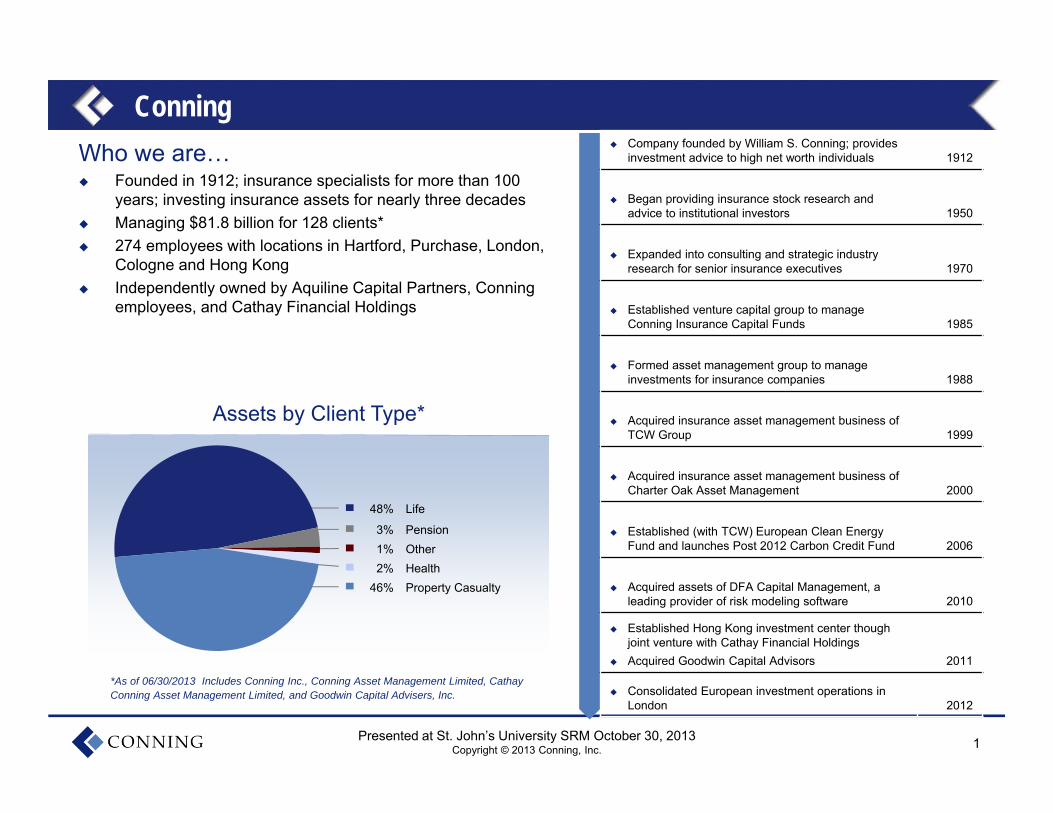

Who we are… Founded in 1912; insurance specialists for more than 100

years; investing insurance assets for nearly three decades Managing $81.8 billion for 128 clients* 274 employees with locations in Hartford, Purchase, London,

Cologne and Hong Kong Independently owned by Aquiline Capital Partners, Conning

employees, and Cathay Financial Holdings

Conning

*As of 06/30/2013 Includes Conning Inc., Conning Asset Management Limited, Cathay Conning Asset Management Limited, and Goodwin Capital Advisers, Inc.

Company founded by William S. Conning; provides investment advice to high net worth individuals 1912

Began providing insurance stock research and advice to institutional investors 1950

Expanded into consulting and strategic industry research for senior insurance executives 1970

Established venture capital group to manage Conning Insurance Capital Funds 1985

Formed asset management group to manage investments for insurance companies 1988

Acquired insurance asset management business of TCW Group 1999

Acquired insurance asset management business of Charter Oak Asset Management 2000

Established (with TCW) European Clean Energy Fund and launches Post 2012 Carbon Credit Fund 2006

Acquired assets of DFA Capital Management, a leading provider of risk modeling software 2010

Established Hong Kong investment center though joint venture with Cathay Financial Holdings

Acquired Goodwin Capital Advisors 2011

Consolidated European investment operations in London 2012

48% Life

3% Pension1% Other2% Health

46% Property Casualty

Assets by Client Type*

2Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

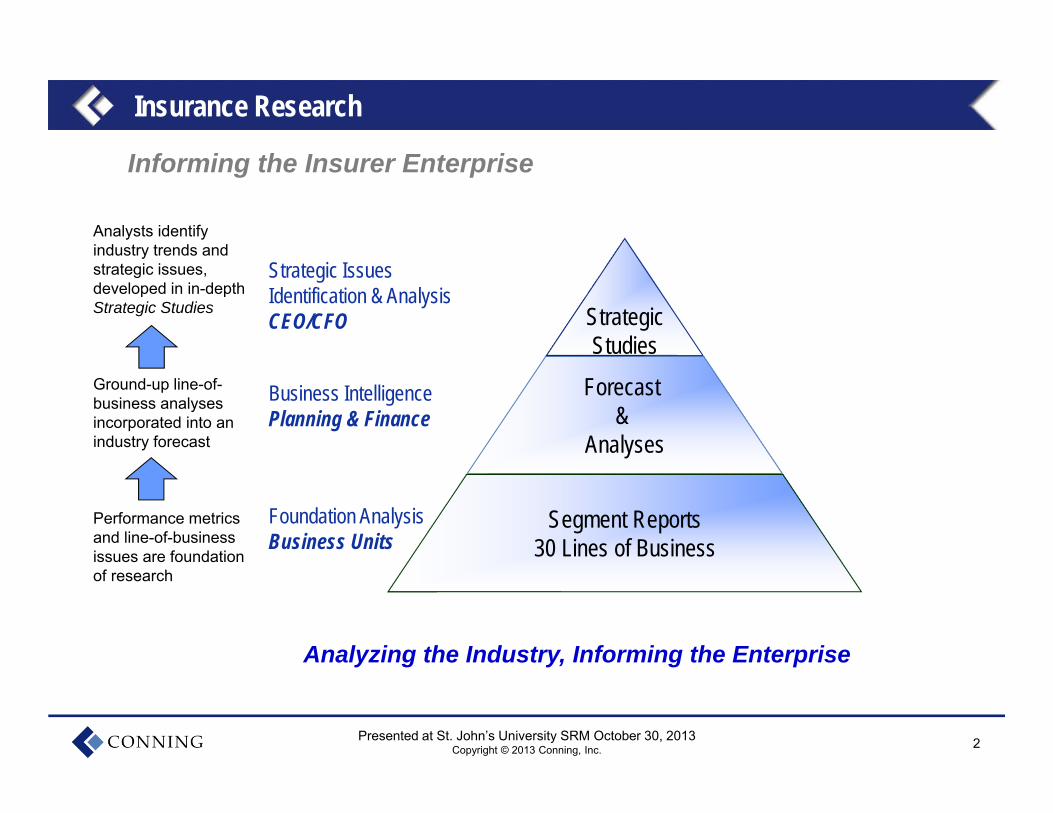

Insurance Research

Analysts identify industry trends and strategic issues, developed in in-depth Strategic Studies

Ground-up line-of-business analyses incorporated into an industry forecast

Performance metrics and line-of-business issues are foundation of research

Informing the Insurer Enterprise

StrategicStudies

Forecast &

Analyses

Segment Reports30 Lines of Business

Business IntelligencePlanning & Finance

Strategic Issues Identification & AnalysisCEO/CFO

Foundation AnalysisBusiness Units

Analyzing the Industry, Informing the Enterprise

3Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Insurance Research

Projects in Support of Client Strategic Planning Proprietary Executive Surveys and Analysis Peer Analyses

Business Development Support Quantitative Analysis of Market Segments Acquisition Target Identification Detailed Company Analyses

State-Level Premium Forecasting Analysis of State Regulatory Environment Review of State-Level Drivers and Indicators Premium History and Forecast by Segment by State

Proprietary Research and Strategic Advisory

4Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

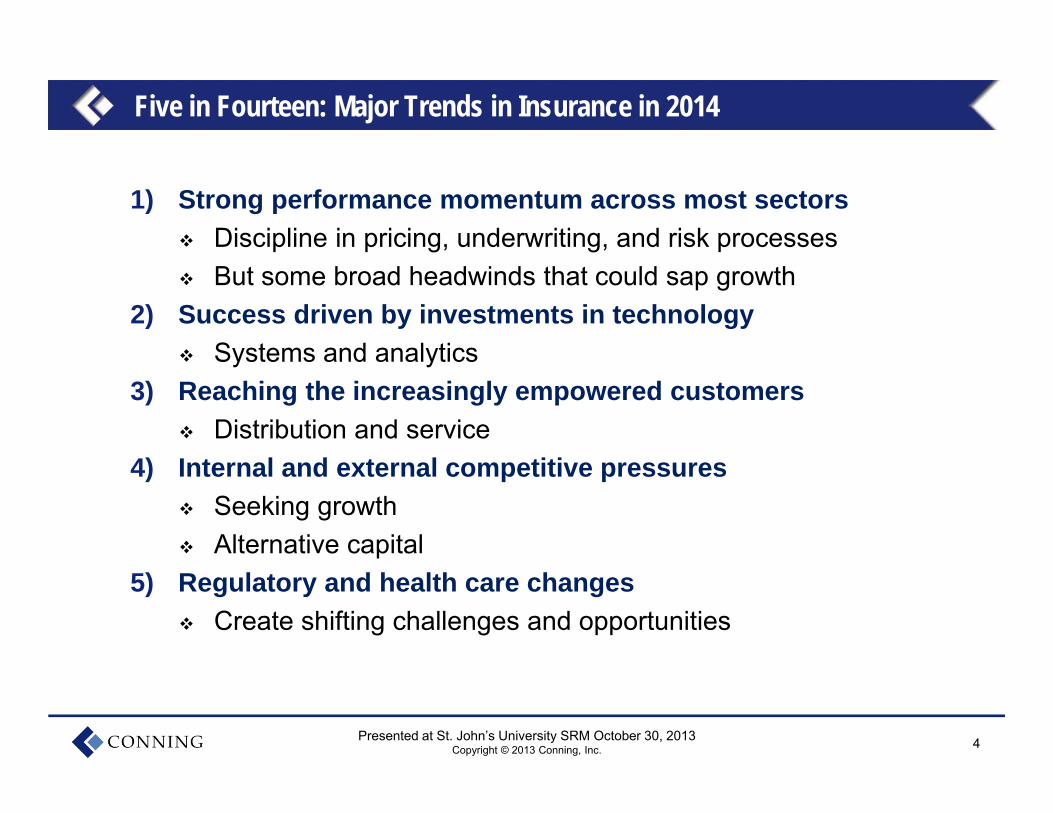

Five in Fourteen: Major Trends in Insurance in 2014

1) Strong performance momentum across most sectors Discipline in pricing, underwriting, and risk processes But some broad headwinds that could sap growth

2) Success driven by investments in technology Systems and analytics

3) Reaching the increasingly empowered customers Distribution and service

4) Internal and external competitive pressures Seeking growth Alternative capital

5) Regulatory and health care changes Create shifting challenges and opportunities

5Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Strong Performance Heading Into 2014

Discipline in pricing, underwriting, and risk processes

But some broad headwinds that could sap growth

6Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

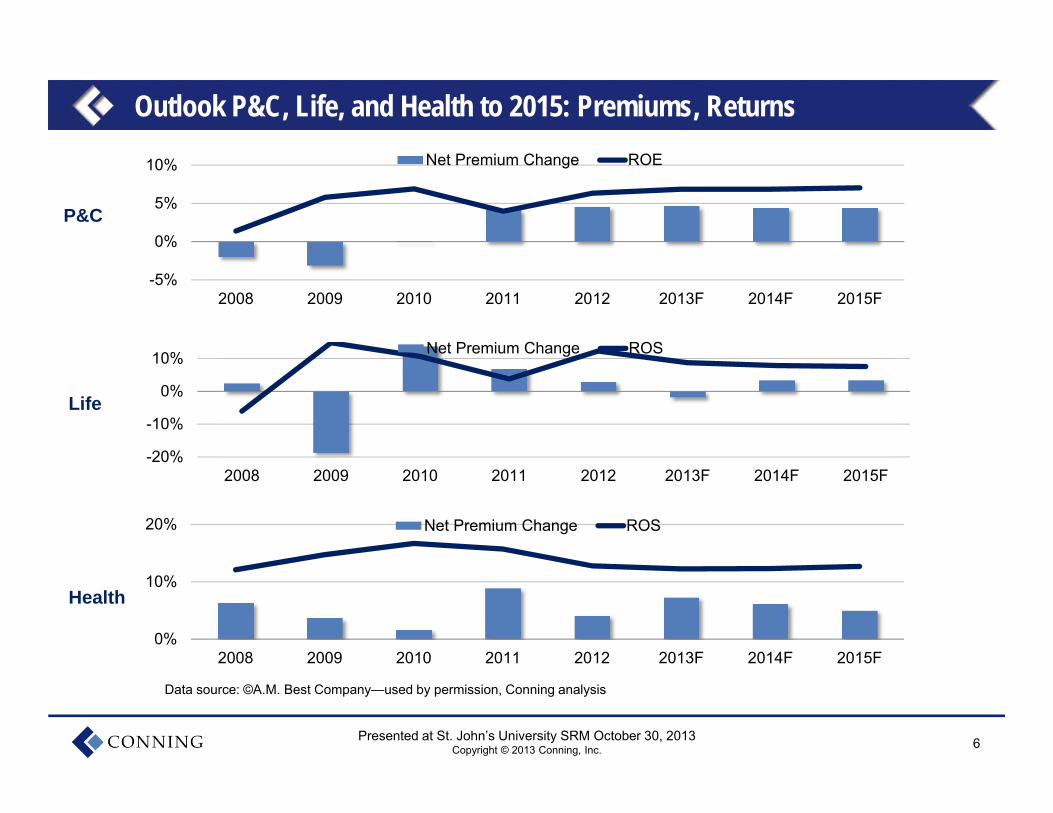

Outlook P&C, Life, and Health to 2015: Premiums, Returns

-5%

0%

5%

10%

2008 2009 2010 2011 2012 2013F 2014F 2015F

Net Premium Change ROE

P&C

Life

Health

-20%

-10%

0%

10%

2008 2009 2010 2011 2012 2013F 2014F 2015F

Net Premium Change ROS

0%

10%

20%

2008 2009 2010 2011 2012 2013F 2014F 2015F

Net Premium Change ROS

Data source: ©A.M. Best Company—used by permission, Conning analysis

7Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

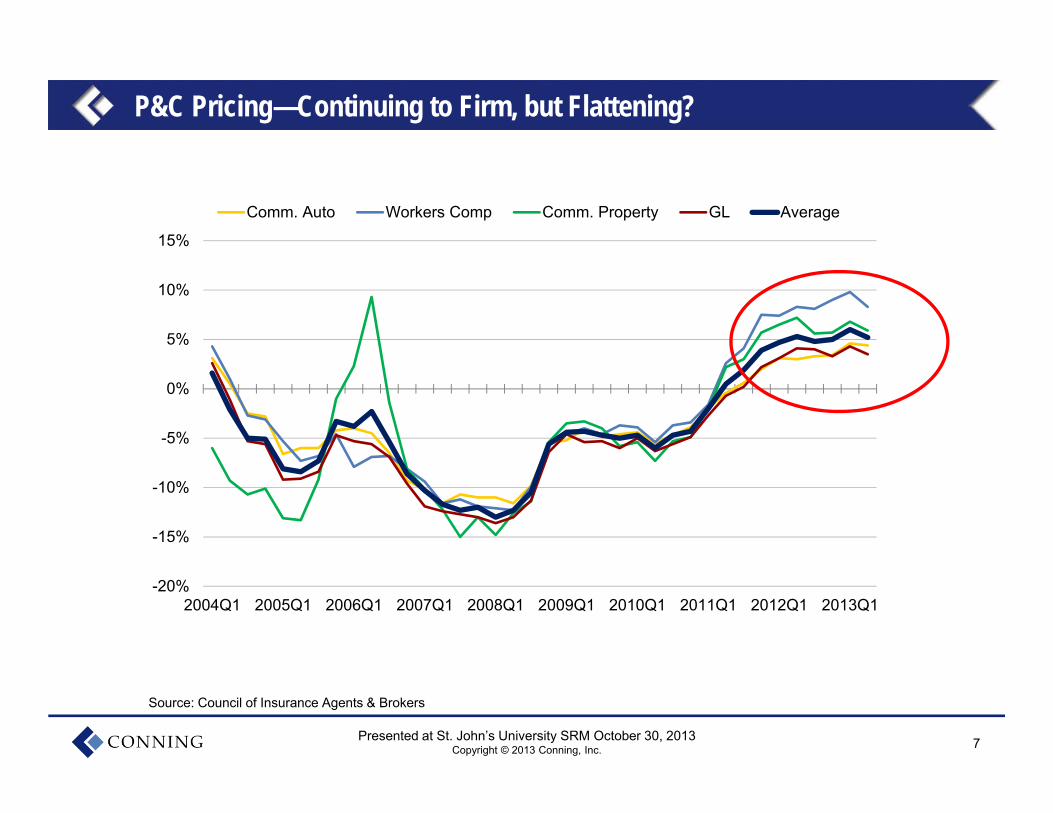

P&C Pricing—Continuing to Firm, but Flattening?

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2004Q1 2005Q1 2006Q1 2007Q1 2008Q1 2009Q1 2010Q1 2011Q1 2012Q1 2013Q1

Comm. Auto Workers Comp Comm. Property GL Average

Source: Council of Insurance Agents & Brokers

8Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

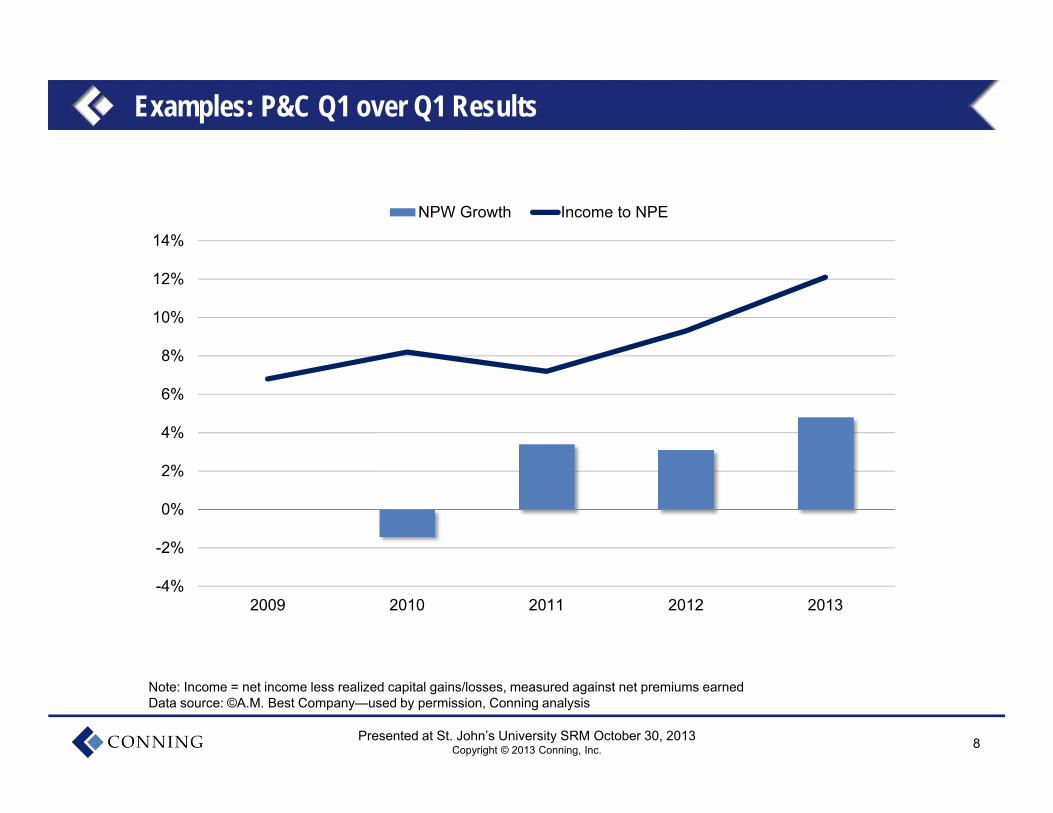

Examples: P&C Q1 over Q1 Results

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2009 2010 2011 2012 2013

NPW Growth Income to NPE

Note: Income = net income less realized capital gains/losses, measured against net premiums earnedData source: ©A.M. Best Company—used by permission, Conning analysis

9Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

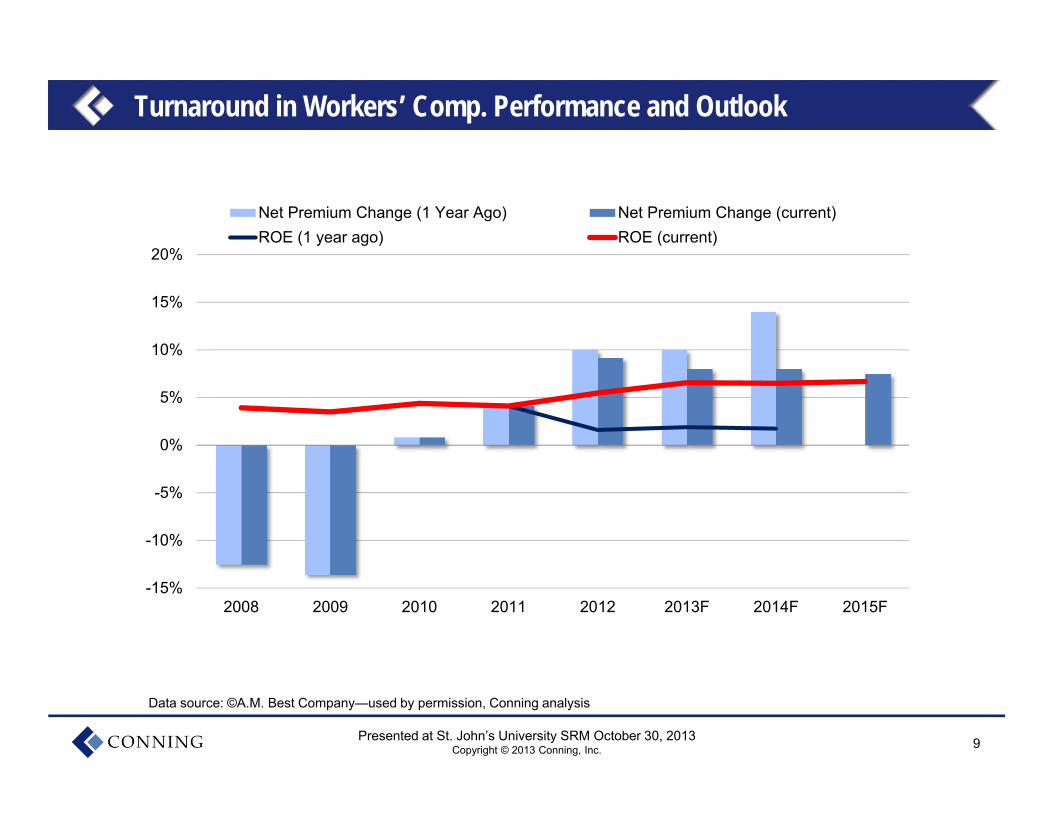

Turnaround in Workers’ Comp. Performance and Outlook

-15%

-10%

-5%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012 2013F 2014F 2015F

Net Premium Change (1 Year Ago) Net Premium Change (current)ROE (1 year ago) ROE (current)

Data source: ©A.M. Best Company—used by permission, Conning analysis

10Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

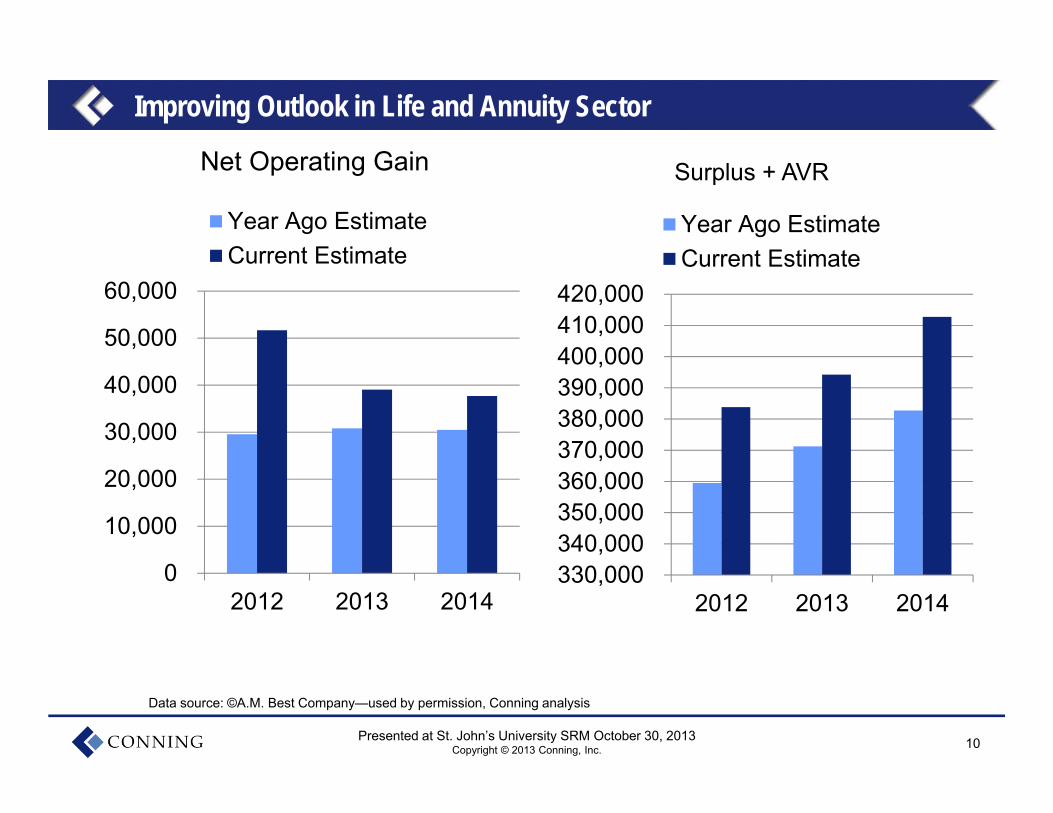

Improving Outlook in Life and Annuity Sector

Data source: ©A.M. Best Company—used by permission, Conning analysis

0

10,000

20,000

30,000

40,000

50,000

60,000

2012 2013 2014

Year Ago EstimateCurrent Estimate

Net Operating Gain

330,000340,000350,000360,000370,000380,000390,000400,000410,000420,000

2012 2013 2014

Year Ago EstimateCurrent Estimate

Surplus + AVR

11Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

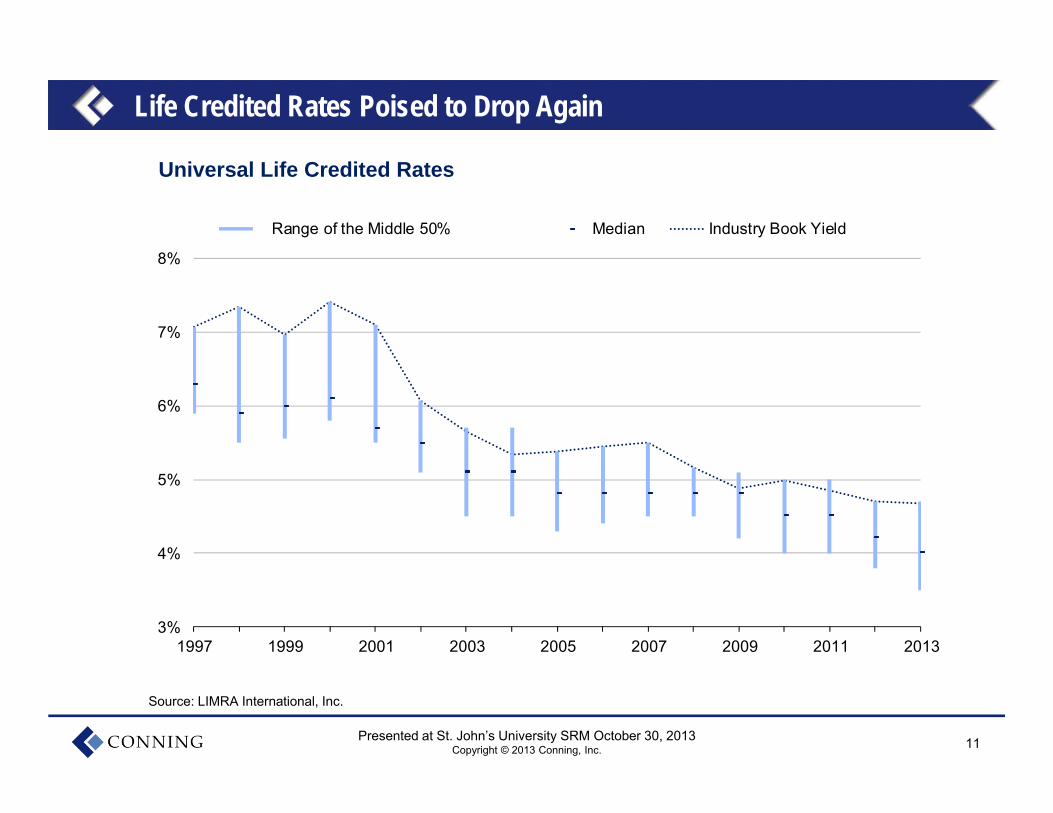

3%

4%

5%

6%

7%

8%

1997 1999 2001 2003 2005 2007 2009 2011 2013

Range of the Middle 50% Median Industry Book Yield

Life Credited Rates Poised to Drop Again

Source: LIMRA International, Inc.

Universal Life Credited Rates

12Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

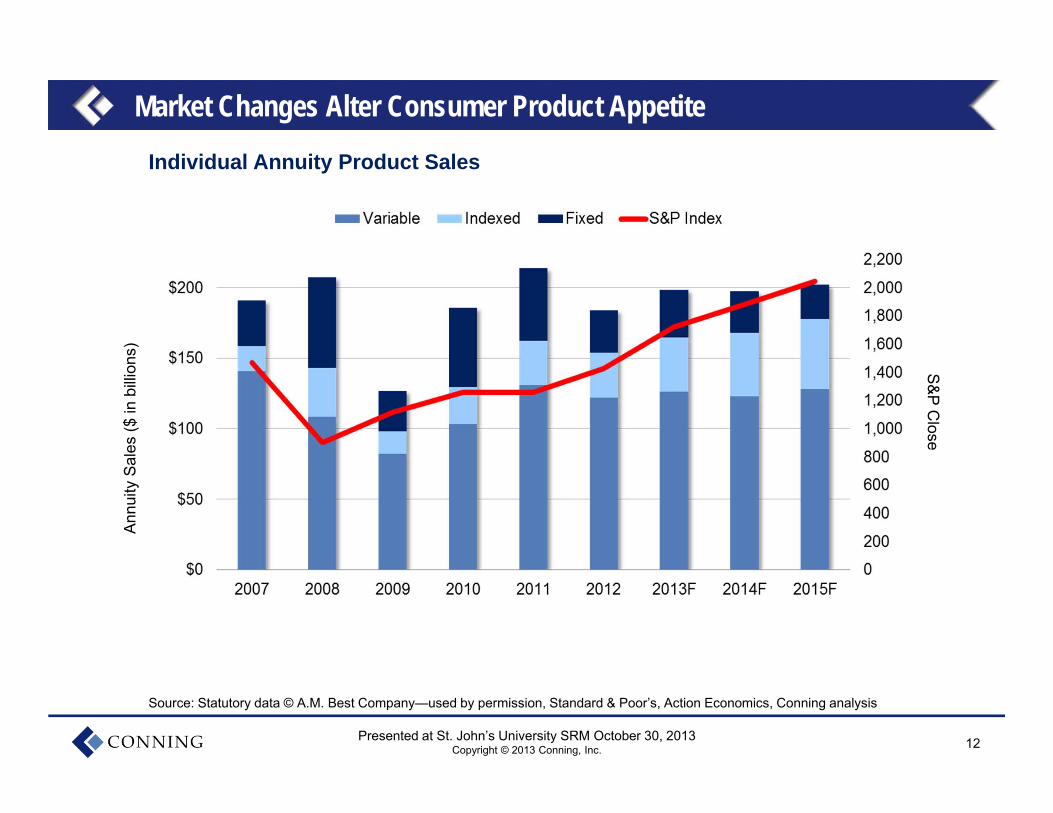

Market Changes Alter Consumer Product AppetiteA

nnui

ty S

ales

($ in

billi

ons)

S&P Close

Individual Annuity Product Sales

Source: Statutory data © A.M. Best Company—used by permission, Standard & Poor’s, Action Economics, Conning analysis

13Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

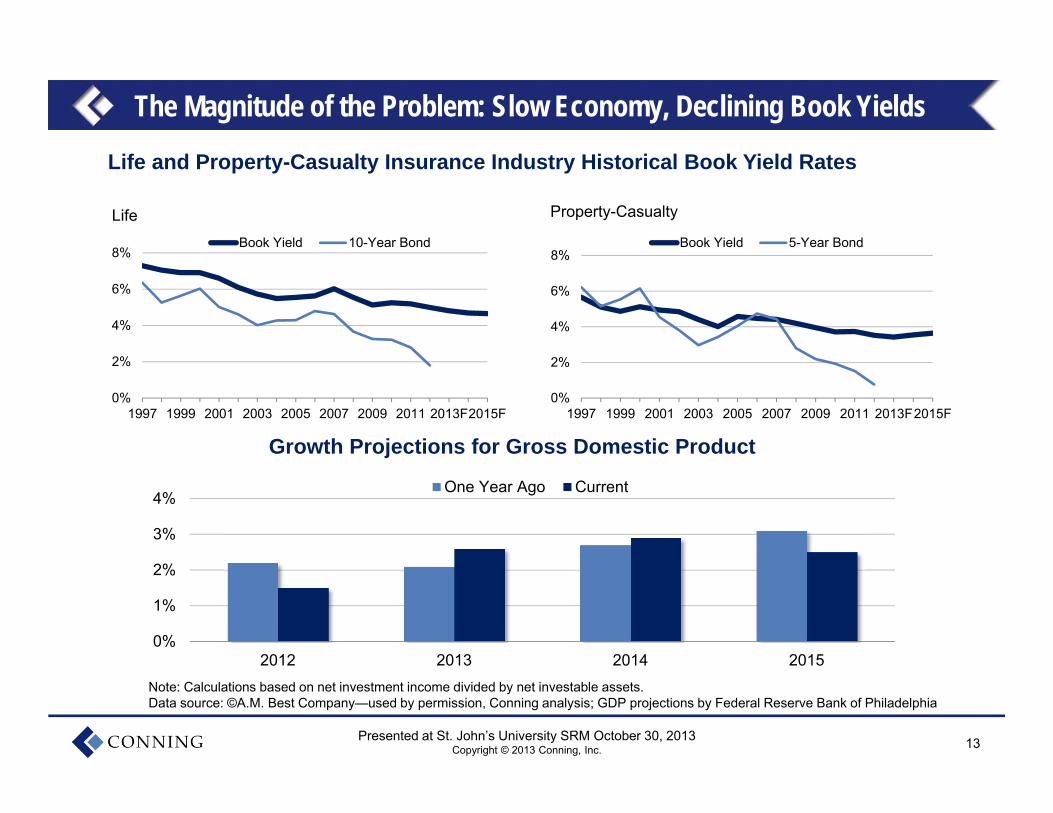

The Magnitude of the Problem: Slow Economy, Declining Book Yields

Life and Property-Casualty Insurance Industry Historical Book Yield Rates

Life Property-Casualty

0%

2%

4%

6%

8%

1997 1999 2001 2003 2005 2007 2009 2011 2013F2015F

Book Yield 5-Year Bond

0%

2%

4%

6%

8%

1997 1999 2001 2003 2005 2007 2009 2011 2013F2015F

Book Yield 10-Year Bond

Note: Calculations based on net investment income divided by net investable assets.Data source: ©A.M. Best Company—used by permission, Conning analysis; GDP projections by Federal Reserve Bank of Philadelphia

0%

1%

2%

3%

4%

2012 2013 2014 2015

One Year Ago Current

Growth Projections for Gross Domestic Product

14Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

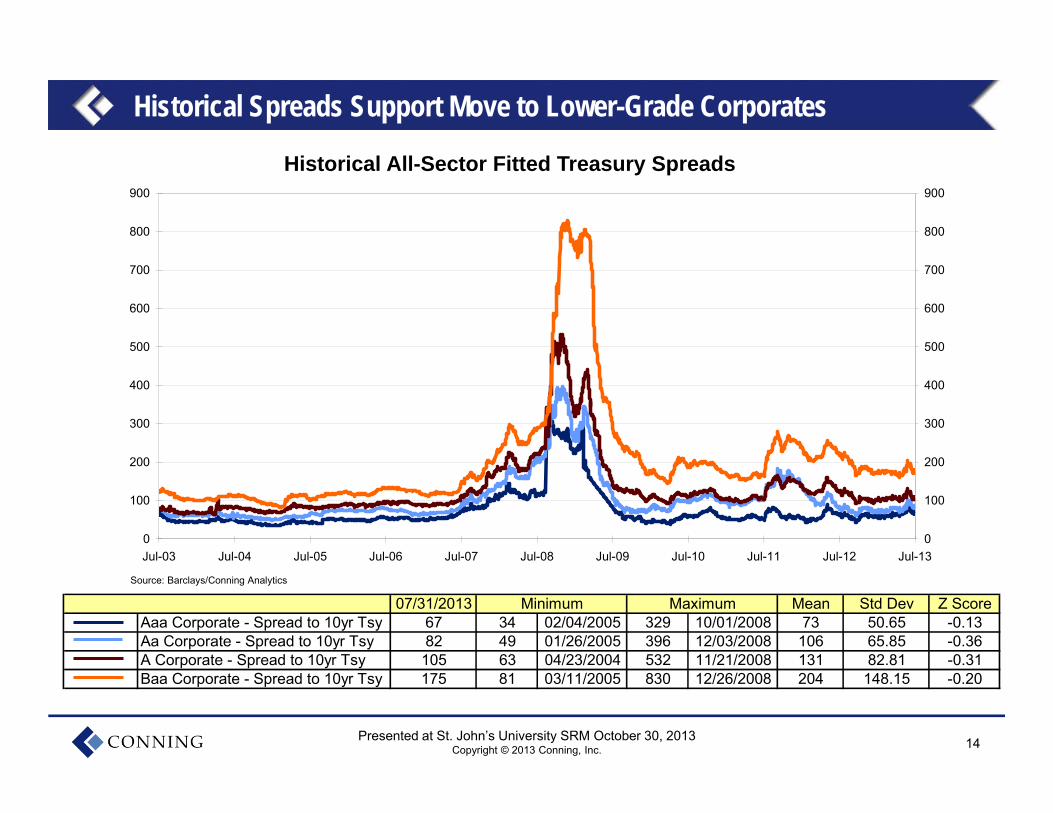

Historical All-Sector Fitted Treasury Spreads

Historical Spreads Support Move to Lower-Grade Corporates

0

100

200

300

400

500

600

700

800

900

Jul-03 Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12 Jul-13

Source: Barclays/Conning Analytics

0

100

200

300

400

500

600

700

800

900

07/31/2013 Mean Std Dev Z ScoreAaa Corporate - Spread to 10yr Tsy 67 34 02/04/2005 329 10/01/2008 73 50.65 -0.13Aa Corporate - Spread to 10yr Tsy 82 49 01/26/2005 396 12/03/2008 106 65.85 -0.36A Corporate - Spread to 10yr Tsy 105 63 04/23/2004 532 11/21/2008 131 82.81 -0.31Baa Corporate - Spread to 10yr Tsy 175 81 03/11/2005 830 12/26/2008 204 148.15 -0.20

Minimum Maximum

15Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

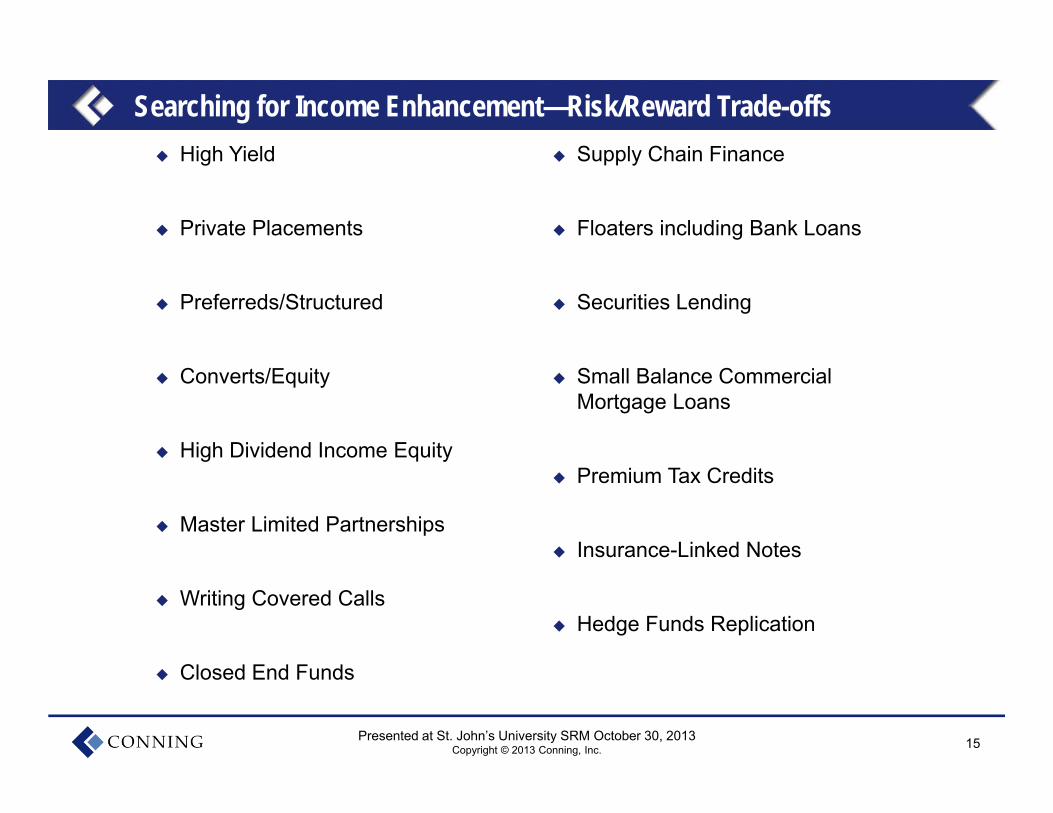

Searching for Income Enhancement—Risk/Reward Trade-offs High Yield

Private Placements

Preferreds/Structured

Converts/Equity

High Dividend Income Equity

Master Limited Partnerships

Writing Covered Calls

Closed End Funds

Supply Chain Finance

Floaters including Bank Loans

Securities Lending

Small Balance Commercial Mortgage Loans

Premium Tax Credits

Insurance-Linked Notes

Hedge Funds Replication

16Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

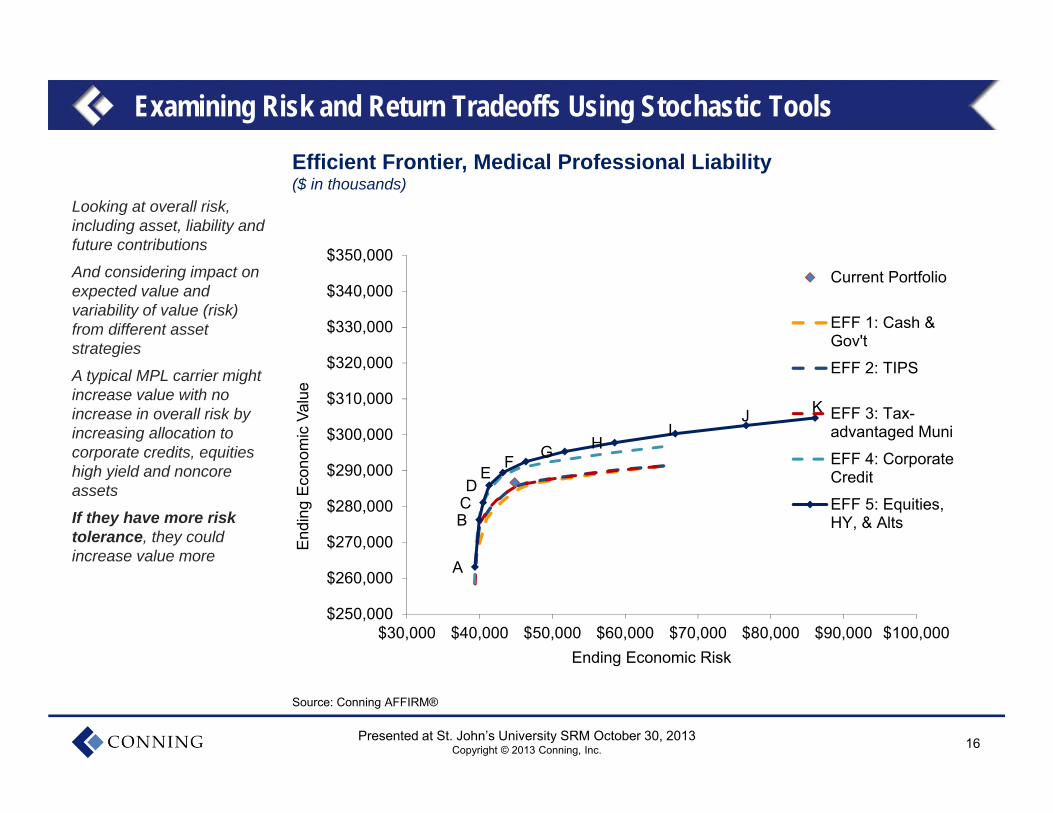

Efficient Frontier, Medical Professional Liability($ in thousands)

Source: Conning AFFIRM®

A

BCD

EF G H

IJ K

$250,000

$260,000

$270,000

$280,000

$290,000

$300,000

$310,000

$320,000

$330,000

$340,000

$350,000

$30,000 $40,000 $50,000 $60,000 $70,000 $80,000 $90,000 $100,000

End

ing

Eco

nom

ic V

alue

Ending Economic Risk

Current Portfolio

EFF 1: Cash &Gov't

EFF 2: TIPS

EFF 3: Tax-advantaged Muni

EFF 4: CorporateCredit

EFF 5: Equities,HY, & Alts

Examining Risk and Return Tradeoffs Using Stochastic Tools

Looking at overall risk, including asset, liability and future contributions

And considering impact on expected value and variability of value (risk) from different asset strategies

A typical MPL carrier might increase value with no increase in overall risk by increasing allocation to corporate credits, equities high yield and noncore assets

If they have more risk tolerance, they could increase value more

17Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

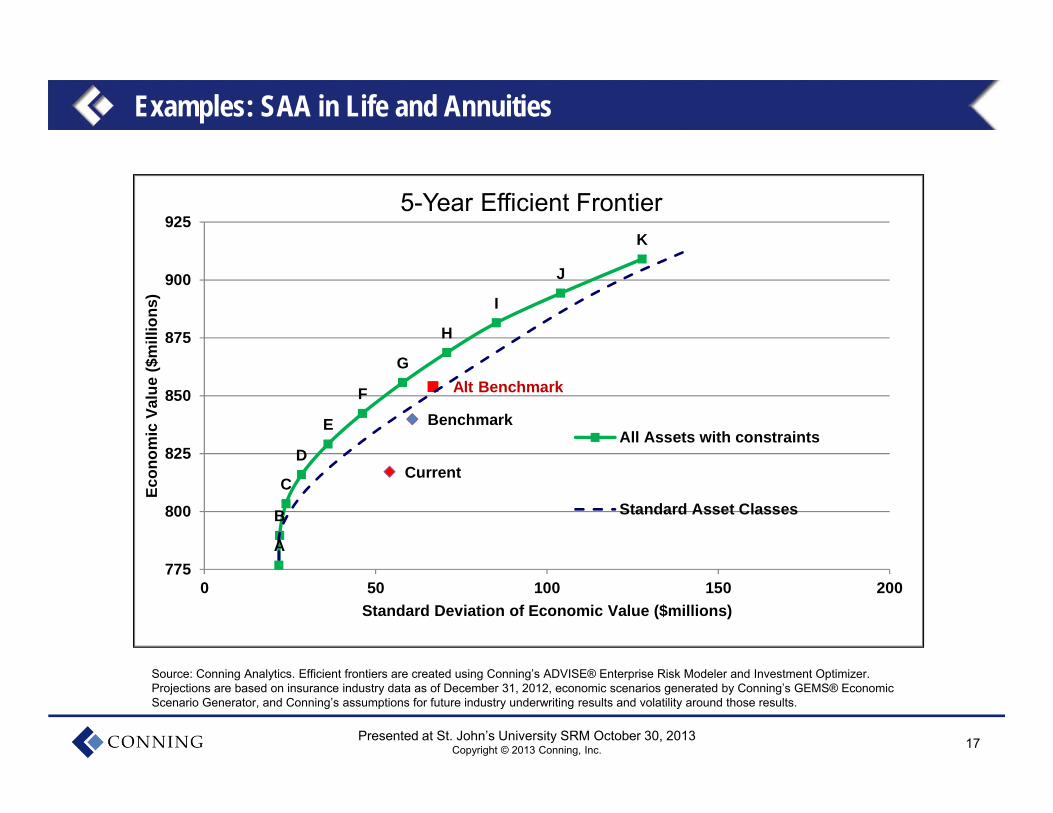

Examples: SAA in Life and Annuities

A

B

C

D

E

F

G

H

I

J

K

Current

Alt Benchmark

Benchmark

775

800

825

850

875

900

925

0 50 100 150 200

Econ

omic

Val

ue ($

mill

ions

)

Standard Deviation of Economic Value ($millions)

5-Year Efficient Frontier

All Assets with constraints

Standard Asset Classes

Source: Conning Analytics. Efficient frontiers are created using Conning’s ADVISE® Enterprise Risk Modeler and Investment Optimizer. Projections are based on insurance industry data as of December 31, 2012, economic scenarios generated by Conning’s GEMS® Economic Scenario Generator, and Conning’s assumptions for future industry underwriting results and volatility around those results.

18Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

$150

$200

$250

$300

$350

$400

$450

2003 2005 2007 2009 2011 2013F2015FFinancial Leverage

SurplusPremium/SurplusReserves/Surplus

Commercial Lines Personal Lines

Source: Conning Property-Casualty Forecast & Analysis by Line of Insurance, 2013Q3 Edition. $ in billions

Capital recovery and buildup includes investment gains and additional capital paid inCapital recovery and buildup includes investment gains and additional capital paid in

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

$100

$150

$200

$250

$300

2003 2005 2007 2009 2011 2013F2015F

Financial Leverage

SurplusPremium/SurplusReserves/Surplus

Headwinds: Capital Buildup Works Against Discipline?

19Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

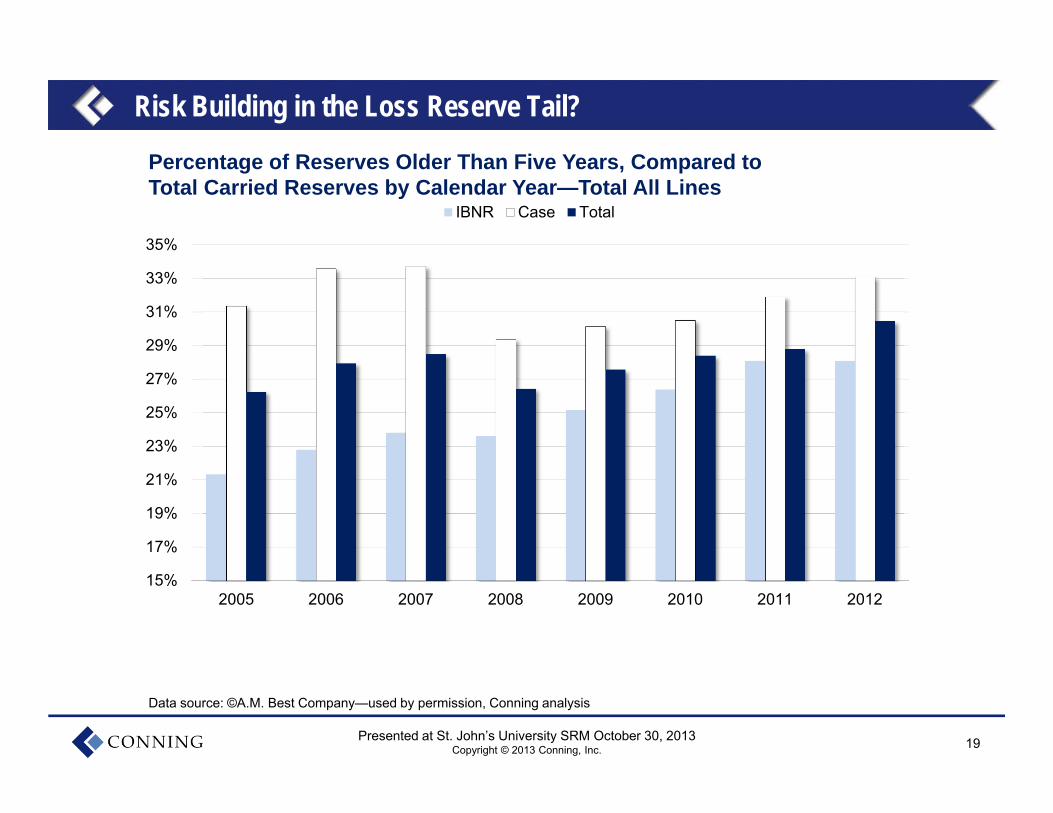

Risk Building in the Loss Reserve Tail?

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

35%

2005 2006 2007 2008 2009 2010 2011 2012

IBNR Case Total

Percentage of Reserves Older Than Five Years, Compared to Total Carried Reserves by Calendar Year—Total All Lines

Data source: ©A.M. Best Company—used by permission, Conning analysis

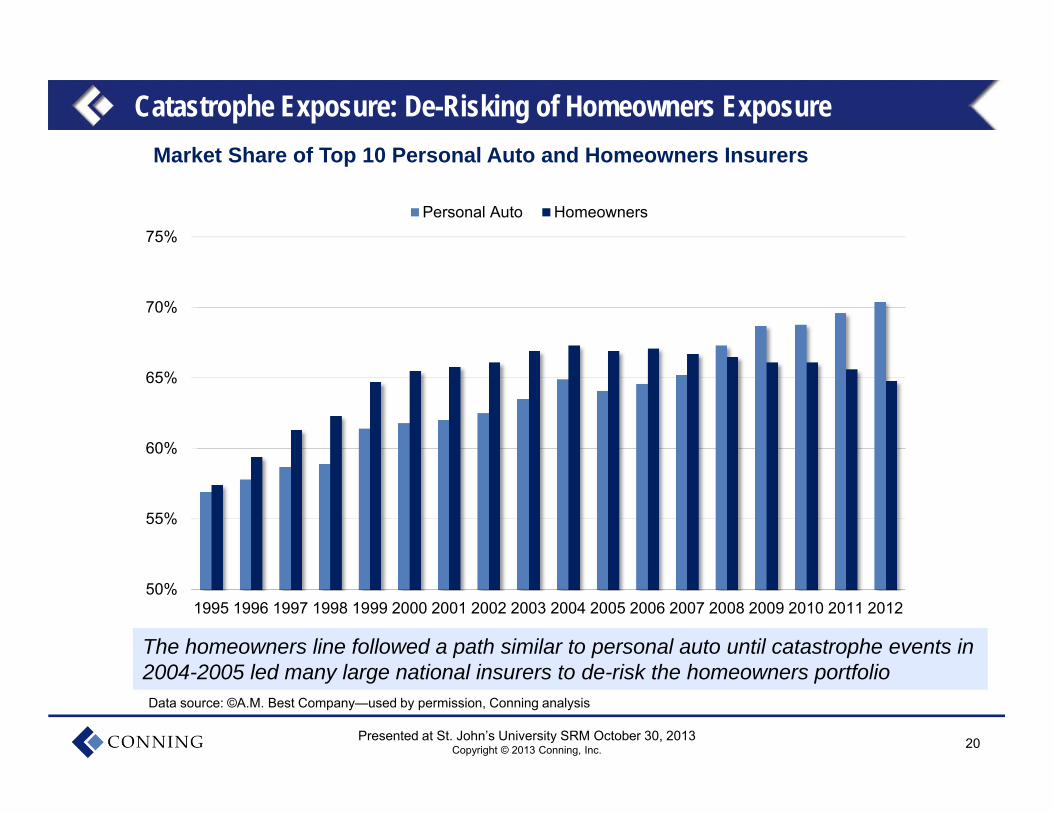

20Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

50%

55%

60%

65%

70%

75%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Personal Auto Homeowners

Catastrophe Exposure: De-Risking of Homeowners Exposure

Data source: ©A.M. Best Company—used by permission, Conning analysis

Market Share of Top 10 Personal Auto and Homeowners Insurers

The homeowners line followed a path similar to personal auto until catastrophe events in 2004-2005 led many large national insurers to de-risk the homeowners portfolioThe homeowners line followed a path similar to personal auto until catastrophe events in 2004-2005 led many large national insurers to de-risk the homeowners portfolio

21Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

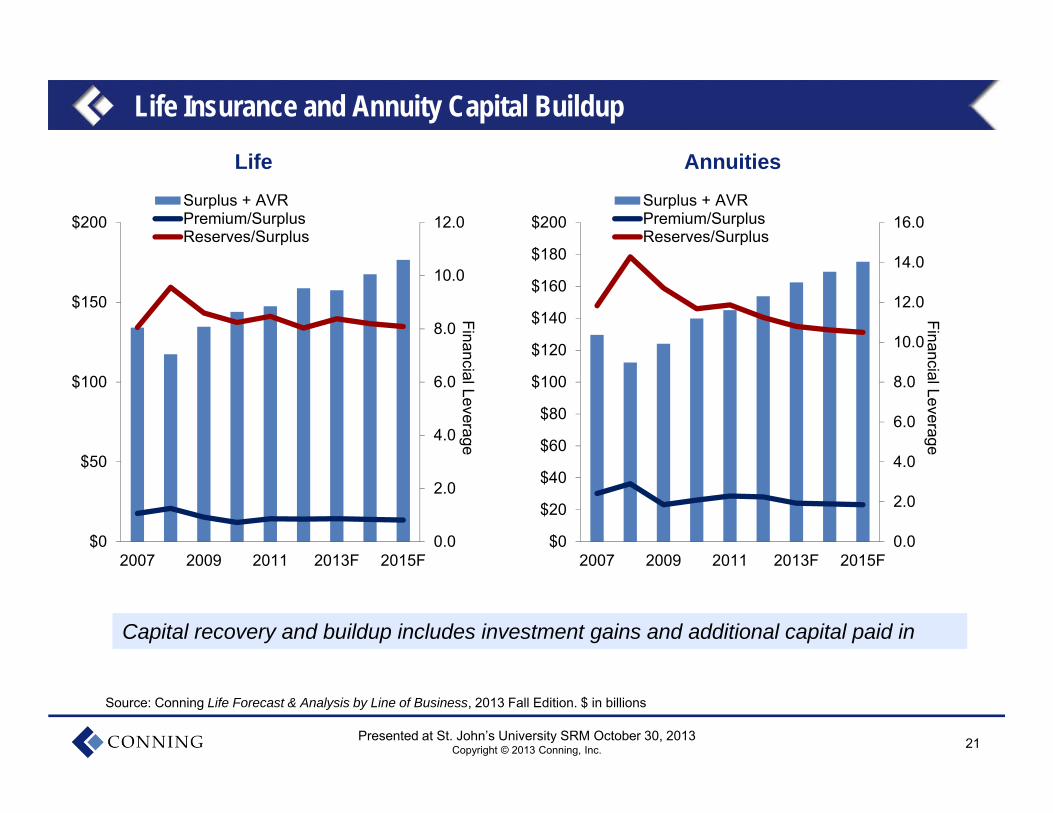

Life Insurance and Annuity Capital Buildup

Source: Conning Life Forecast & Analysis by Line of Business, 2013 Fall Edition. $ in billions

0.0

2.0

4.0

6.0

8.0

10.0

12.0

$0

$50

$100

$150

$200

2007 2009 2011 2013F 2015FFinancial Leverage

Surplus + AVRPremium/SurplusReserves/Surplus

Life Annuities

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2007 2009 2011 2013F 2015F

Financial Leverage

Surplus + AVRPremium/SurplusReserves/Surplus

Capital recovery and buildup includes investment gains and additional capital paid inCapital recovery and buildup includes investment gains and additional capital paid in

22Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

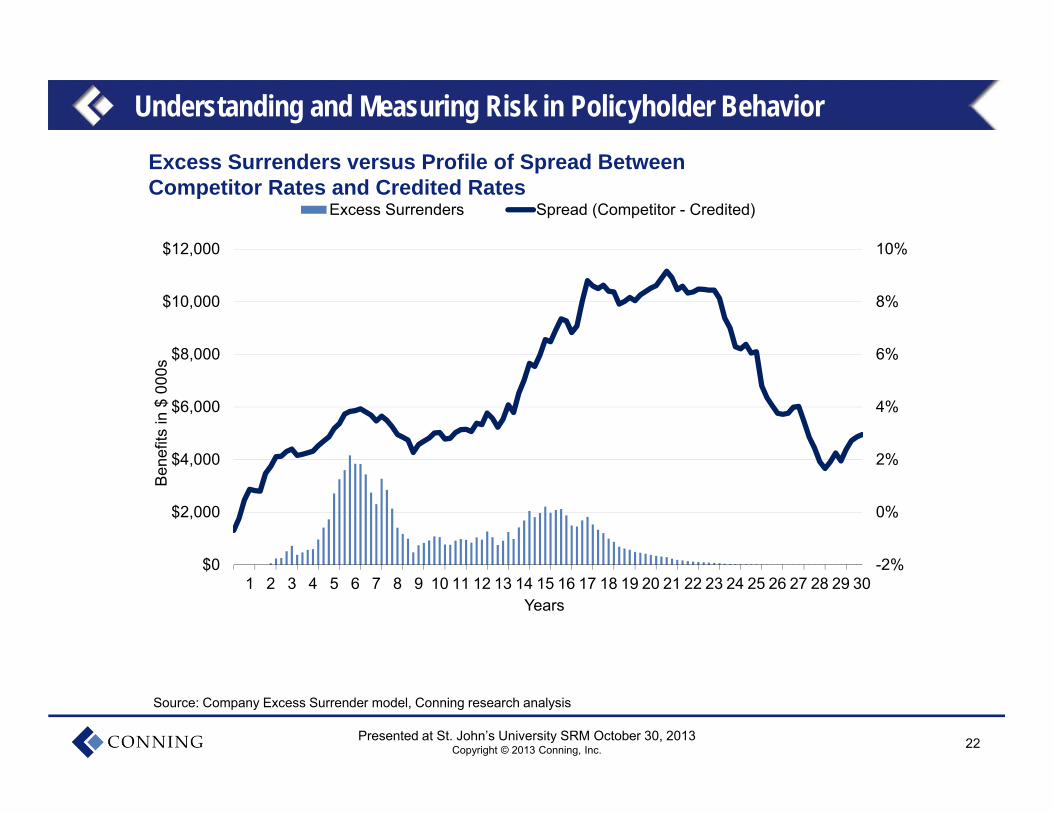

Excess Surrenders versus Profile of Spread BetweenCompetitor Rates and Credited Rates

Source: Company Excess Surrender model, Conning research analysis

Understanding and Measuring Risk in Policyholder Behavior

-2%

0%

2%

4%

6%

8%

10%

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Ben

efits

in $

000

s

Years

Excess Surrenders Spread (Competitor - Credited)

23Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

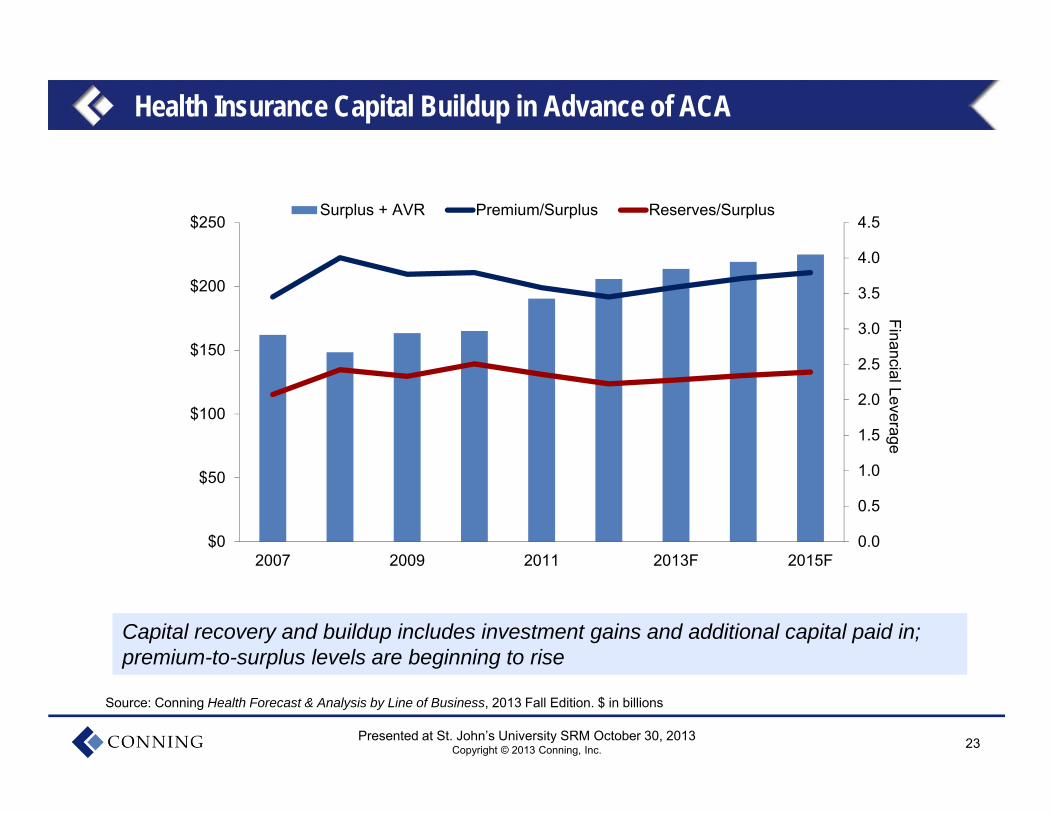

Health Insurance Capital Buildup in Advance of ACA

Source: Conning Health Forecast & Analysis by Line of Business, 2013 Fall Edition. $ in billions

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

$0

$50

$100

$150

$200

$250

2007 2009 2011 2013F 2015F

Financial Leverage

Surplus + AVR Premium/Surplus Reserves/Surplus

Capital recovery and buildup includes investment gains and additional capital paid in; premium-to-surplus levels are beginning to riseCapital recovery and buildup includes investment gains and additional capital paid in; premium-to-surplus levels are beginning to rise

24Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

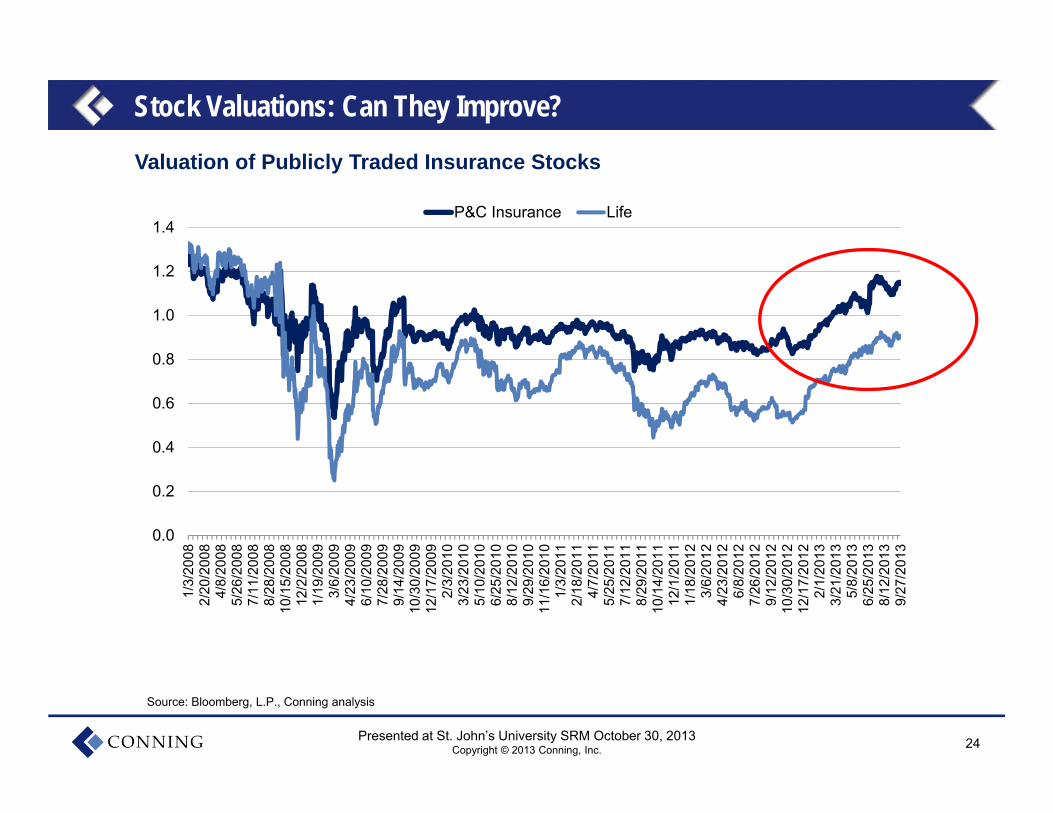

Stock Valuations: Can They Improve?

Source: Bloomberg, L.P., Conning analysis

Valuation of Publicly Traded Insurance Stocks

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1/3/

2008

2/20

/200

84/

8/20

085/

26/2

008

7/11

/200

88/

28/2

008

10/1

5/20

0812

/2/2

008

1/19

/200

93/

6/20

094/

23/2

009

6/10

/200

97/

28/2

009

9/14

/200

910

/30/

2009

12/1

7/20

092/

3/20

103/

23/2

010

5/10

/201

06/

25/2

010

8/12

/201

09/

29/2

010

11/1

6/20

101/

3/20

112/

18/2

011

4/7/

2011

5/25

/201

17/

12/2

011

8/29

/201

110

/14/

2011

12/1

/201

11/

18/2

012

3/6/

2012

4/23

/201

26/

8/20

127/

26/2

012

9/12

/201

210

/30/

2012

12/1

7/20

122/

1/20

133/

21/2

013

5/8/

2013

6/25

/201

38/

12/2

013

9/27

/201

3

P&C Insurance Life

25Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Investments in Technology and Analytics Paying Off?

Technology overhaul, replacing legacy systems, moving to the cloud

Information and analytics transforming at all levels

26Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

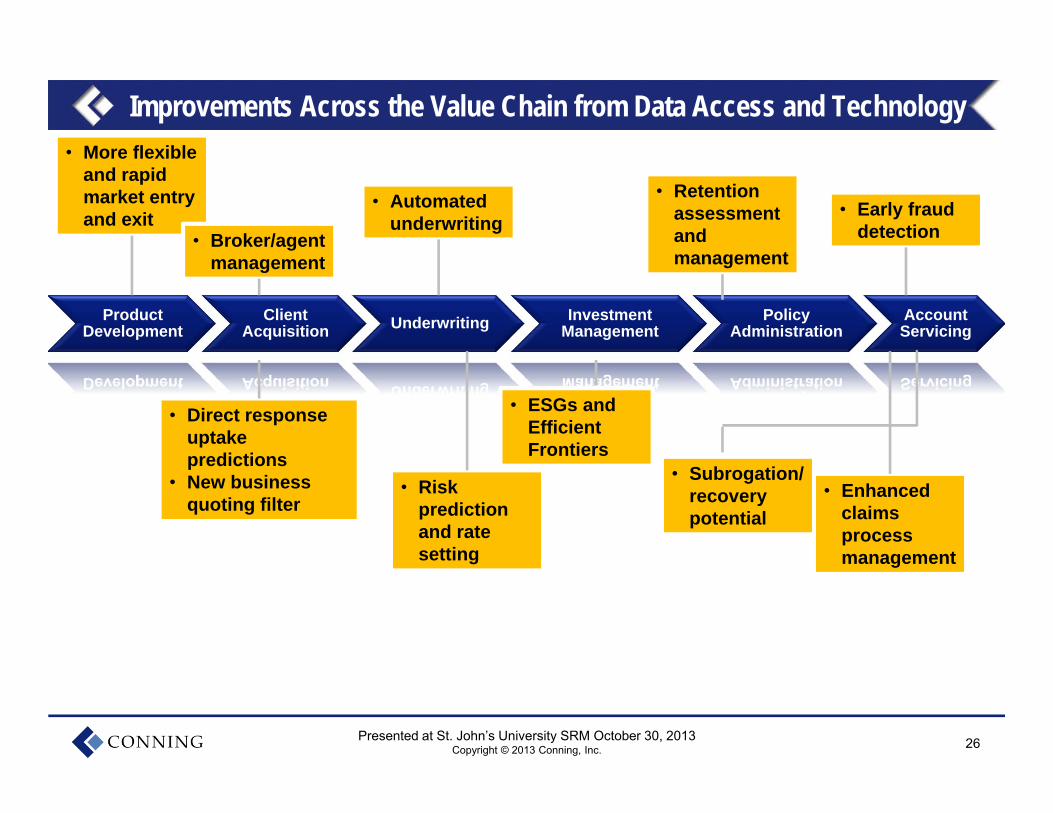

Improvements Across the Value Chain from Data Access and Technology

Product Development

Client Acquisition Underwriting Investment

ManagementPolicy

AdministrationAccount Servicing

• Enhanced claims process management

• Risk prediction and rate setting

• More flexible and rapid market entry and exit

• Retention assessment and management

• Direct response uptake predictions

• New business quoting filter

• Automated underwriting

• Broker/agent management

• Early fraud detection

• Subrogation/ recovery potential

• ESGs and Efficient Frontiers

27Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Amount Spent on IT Increasing—Property-Casualty Sector

$0

$1

$2

$3

$4

$5

$6

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

IT Expense (right scale) % of DPW % of NPW

Technology and Data Investments Paying Off?

$ in billions. Data source: © A.M. Best Company—used by permission, Conning analysis

28Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

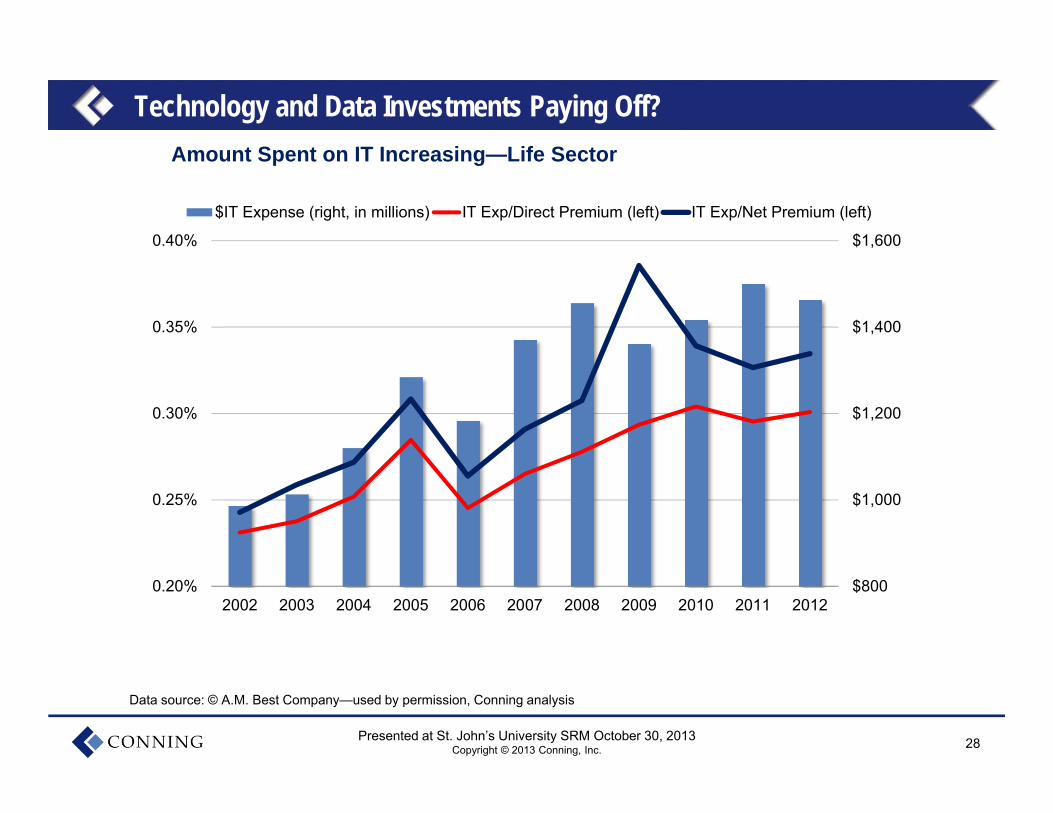

Technology and Data Investments Paying Off?

$800

$1,000

$1,200

$1,400

$1,600

0.20%

0.25%

0.30%

0.35%

0.40%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$IT Expense (right, in millions) IT Exp/Direct Premium (left) IT Exp/Net Premium (left)

Amount Spent on IT Increasing—Life Sector

Data source: © A.M. Best Company—used by permission, Conning analysis

29Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Importance of Big Data, Advance Analytics, and Data Management

Five stages of data management Acquisition and reconciliation Integration across the enterprise Enhanced and predictive analytics Governance Data security

Vendors pick up where large companies leave off

30Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Next Generation

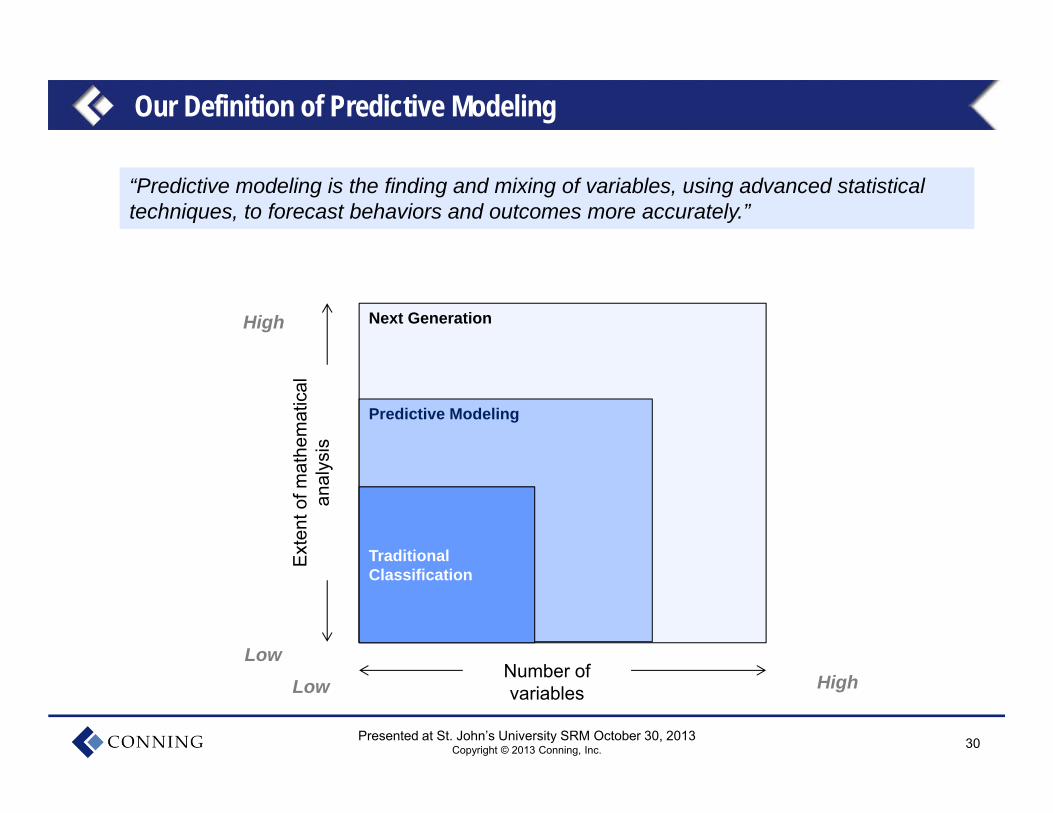

Our Definition of Predictive Modeling

Predictive Modeling

Traditional Classification

Ext

ent o

f mat

hem

atic

al

anal

ysis

Number of variables

High

HighLow

Low

“Predictive modeling is the finding and mixing of variables, using advanced statistical techniques, to forecast behaviors and outcomes more accurately.”“Predictive modeling is the finding and mixing of variables, using advanced statistical techniques, to forecast behaviors and outcomes more accurately.”

31Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

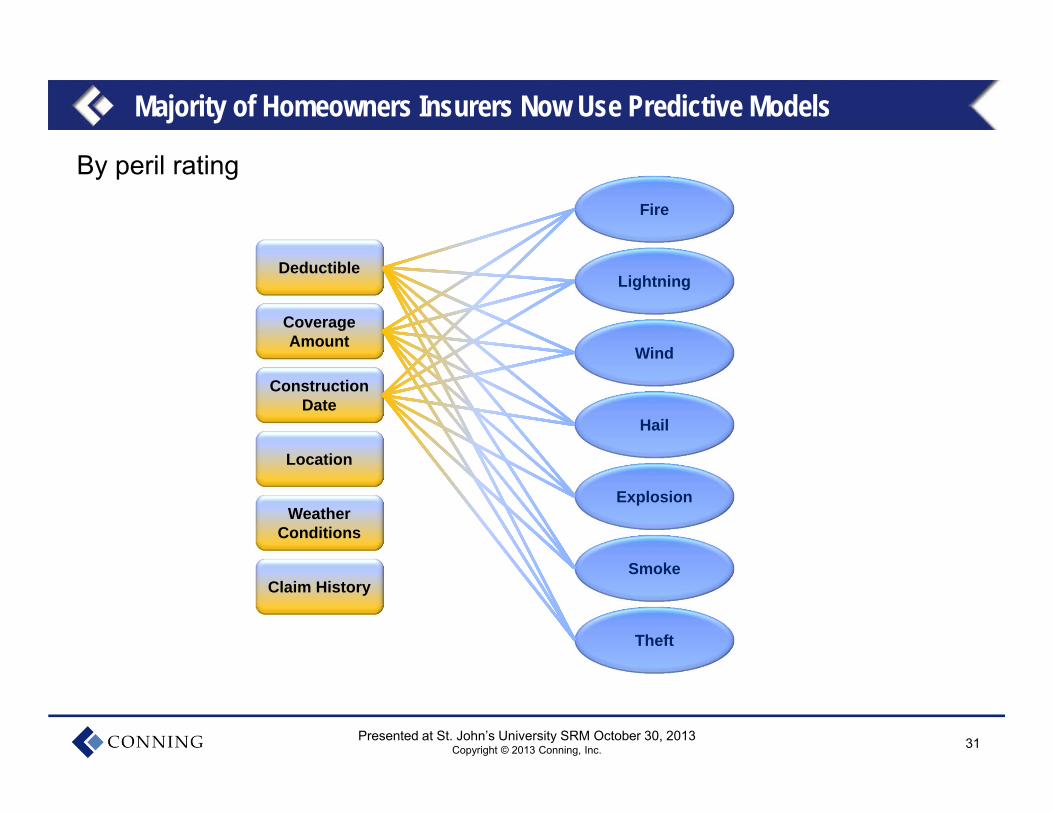

Majority of Homeowners Insurers Now Use Predictive Models

By peril rating

Deductible

Coverage Amount

Construction Date

Location

Weather Conditions

Claim History

Fire

Lightning

Wind

Hail

Explosion

Smoke

Theft

32Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

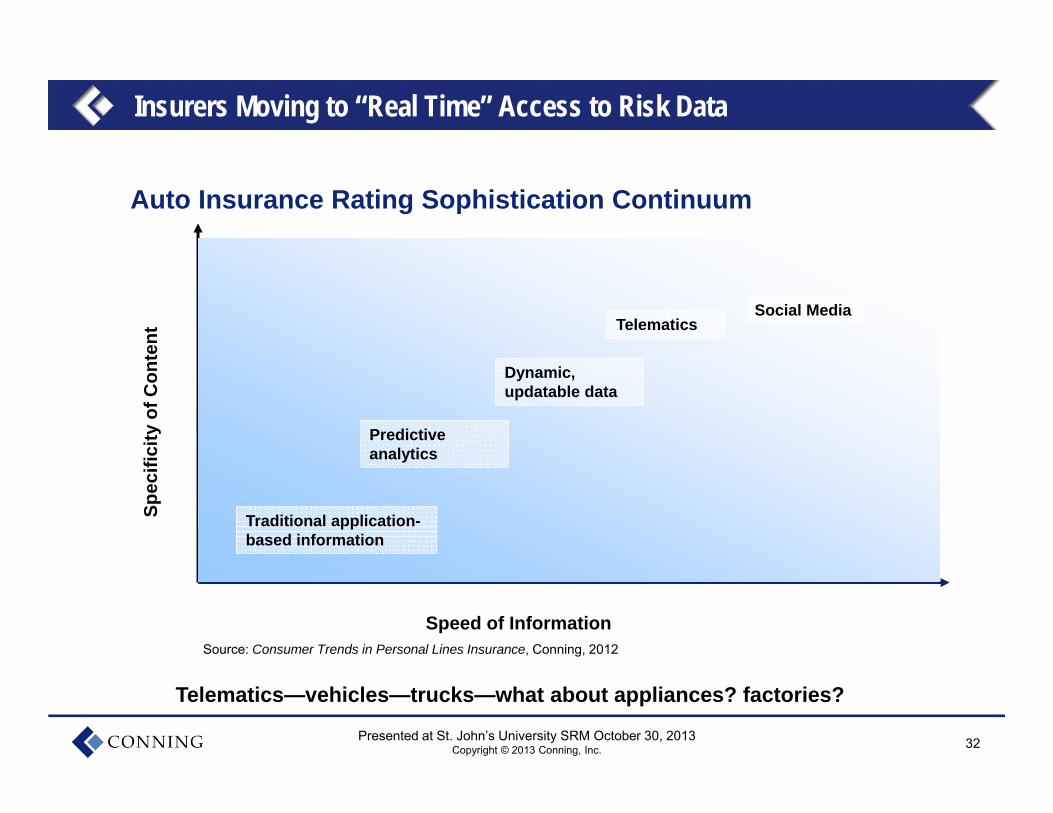

Auto Insurance Rating Sophistication Continuum

Speed of Information

Spec

ifici

ty o

f Con

tent

Traditional application-based information

Predictive analytics

Dynamic, updatable data

TelematicsSocial Media

Source: Consumer Trends in Personal Lines Insurance, Conning, 2012

Insurers Moving to “Real Time” Access to Risk Data

Telematics—vehicles—trucks—what about appliances? factories?

33Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

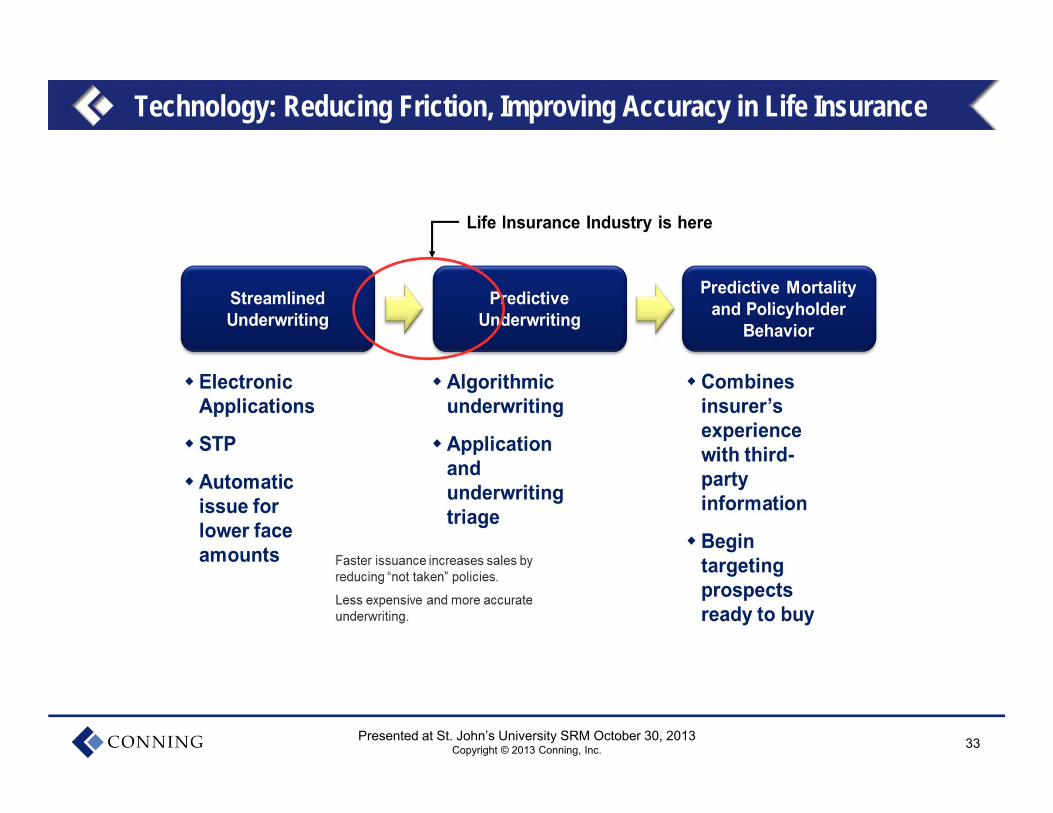

Technology: Reducing Friction, Improving Accuracy in Life Insurance

34Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

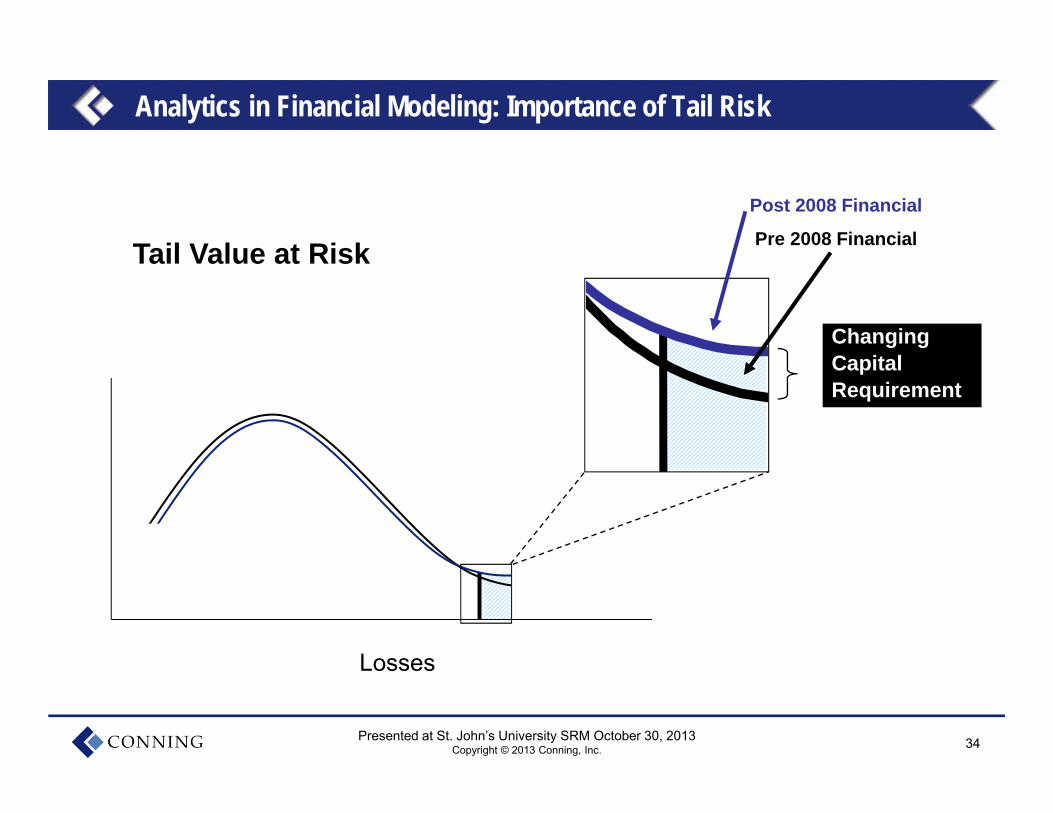

Analytics in Financial Modeling: Importance of Tail Risk

Tail Value at Risk

Losses

ChangingCapitalRequirement

Post 2008 Financial

Pre 2008 Financial

35Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

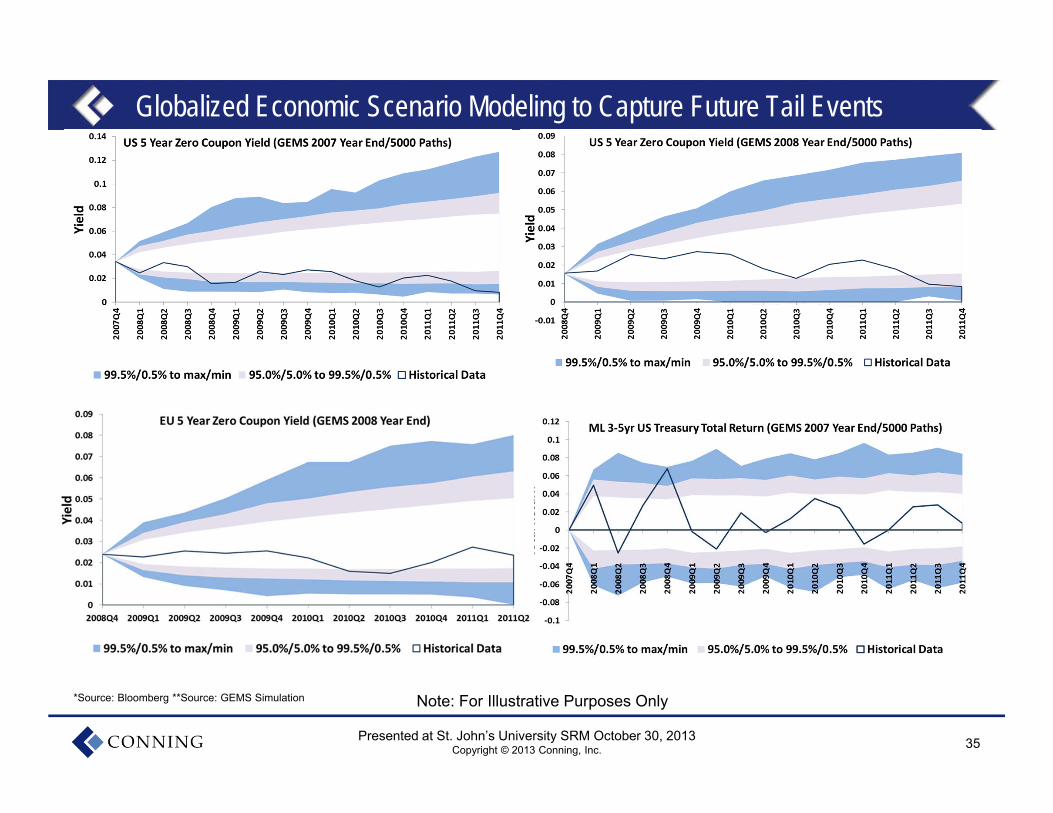

*Source: Bloomberg **Source: GEMS Simulation

Globalized Economic Scenario Modeling to Capture Future Tail Events

Note: For Illustrative Purposes Only

36Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

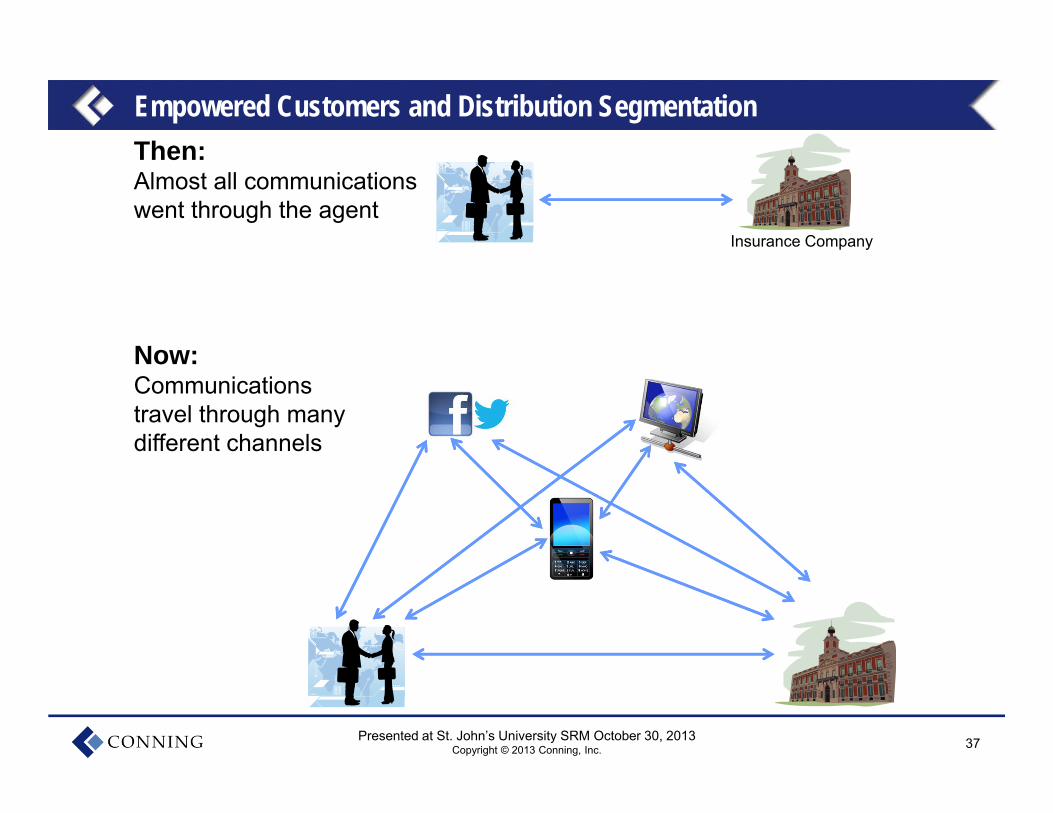

Addressing a Changing Customer Base

Empowered customers and distribution segmentation

Service delivery arms race: mobile, digital, social networks

Middle market outperforms: targeting specialized risk and

service

New risks and new opportunities emerge—but sold, not bought

37Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Then: Almost all communicationswent through the agent

Now:Communications travel through many different channels

Insurance Company

Empowered Customers and Distribution Segmentation

38Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

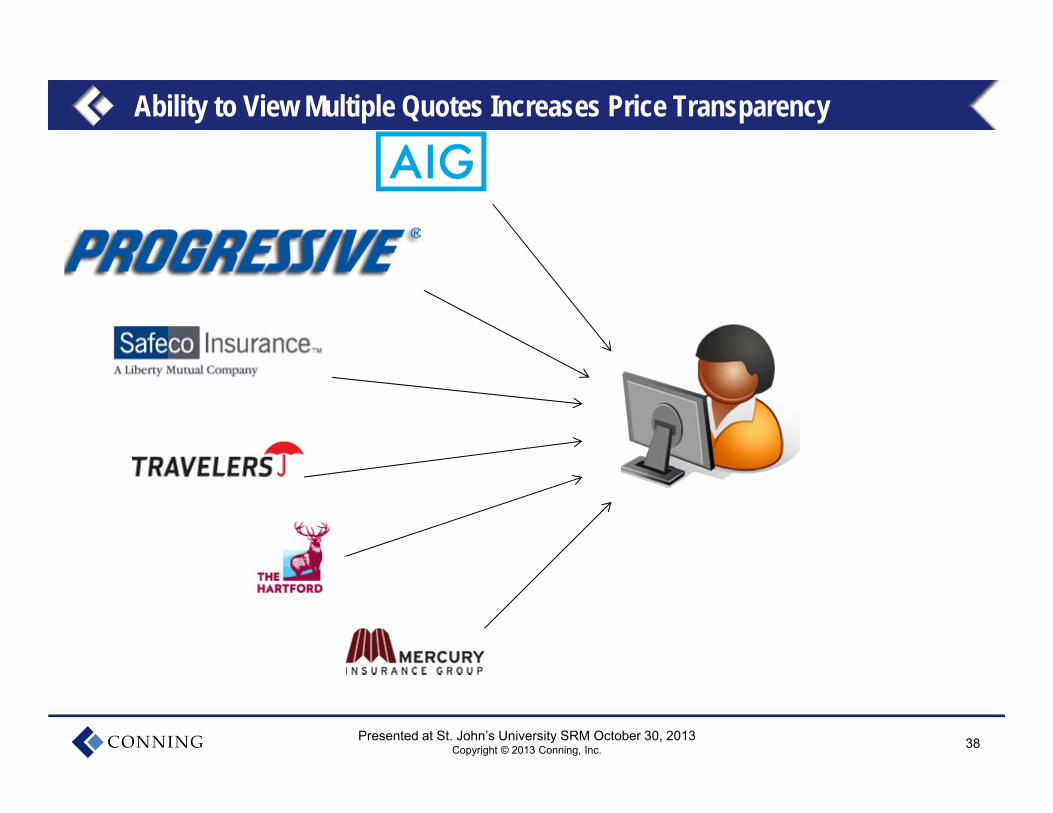

Ability to View Multiple Quotes Increases Price Transparency

39Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

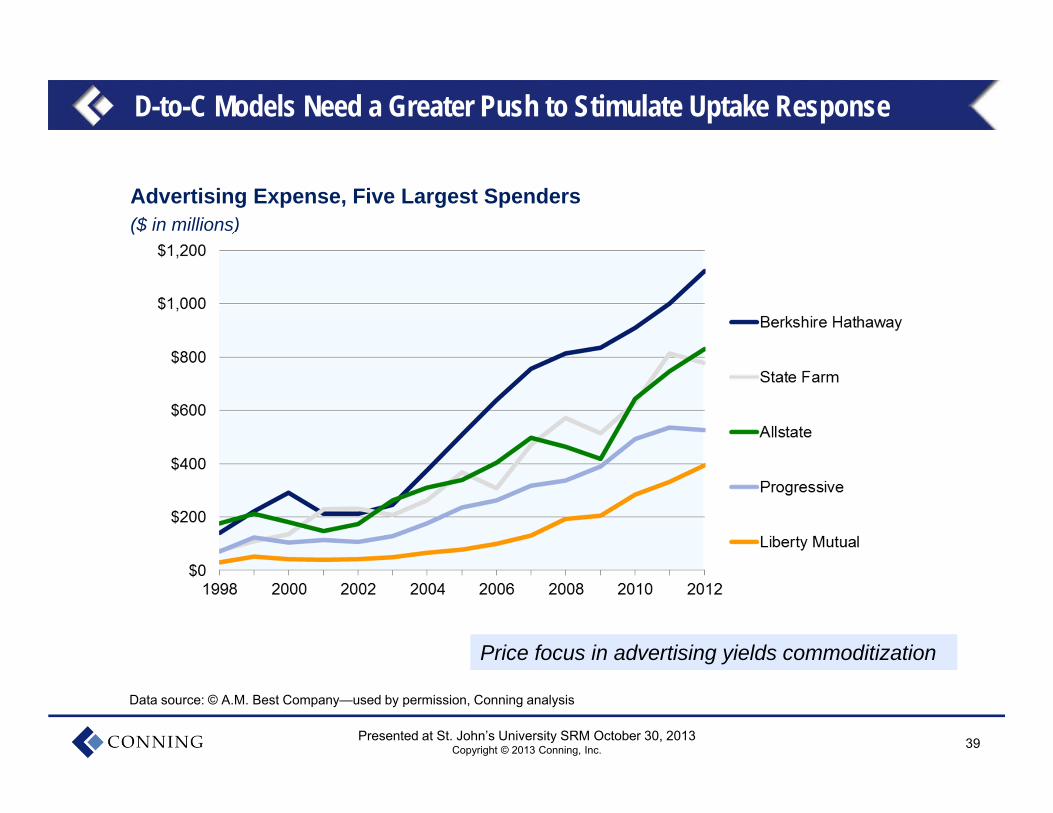

D-to-C Models Need a Greater Push to Stimulate Uptake Response

Advertising Expense, Five Largest Spenders($ in millions)

Data source: © A.M. Best Company—used by permission, Conning analysis

Price focus in advertising yields commoditization Price focus in advertising yields commoditization

40Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Segmentation Opportunities—Views Will Vary by Generation

Depression era→savers Boomer generation→spenders Generations Y and C→renters?

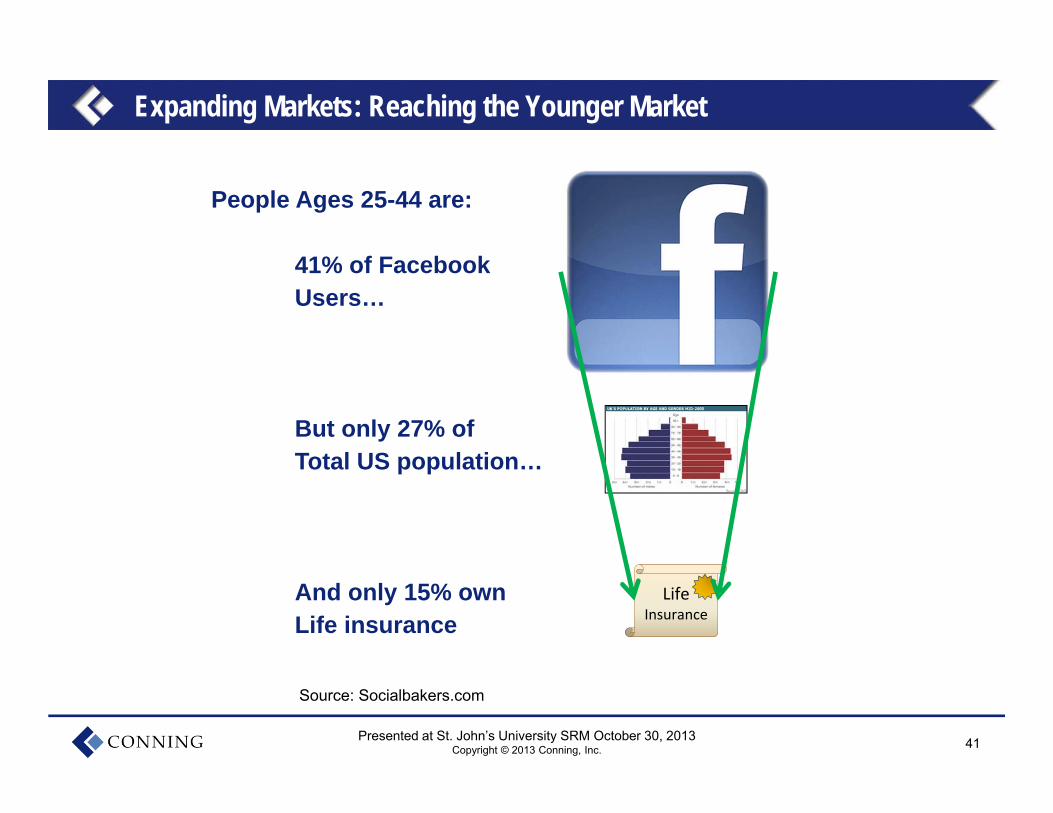

41Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

People Ages 25-44 are:

41% of Facebook Users…

But only 27% of Total US population…

And only 15% ownLife insurance

Expanding Markets: Reaching the Younger Market

Source: Socialbakers.com

Life Insurance

42Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

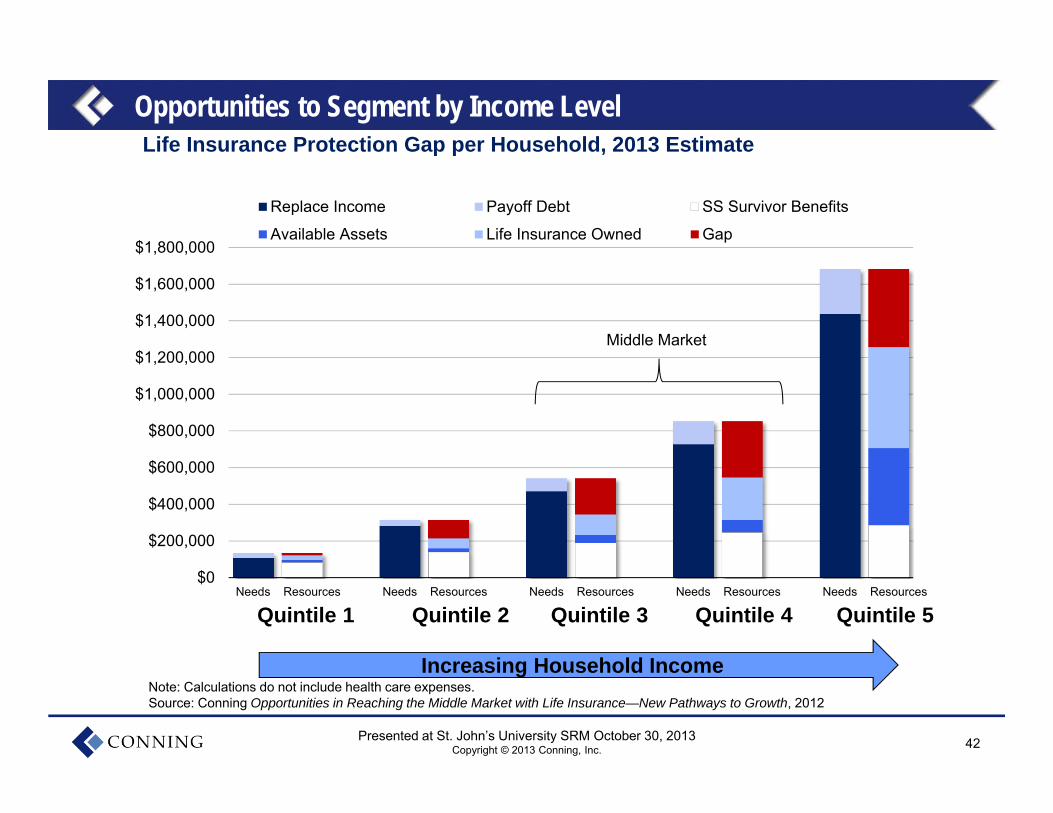

Opportunities to Segment by Income LevelLife Insurance Protection Gap per Household, 2013 Estimate

Note: Calculations do not include health care expenses.Source: Conning Opportunities in Reaching the Middle Market with Life Insurance—New Pathways to Growth, 2012

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

Needs Resources Needs Resources Needs Resources Needs Resources Needs Resources

Replace Income Payoff Debt SS Survivor Benefits

Available Assets Life Insurance Owned Gap

Quintile 1 Quintile 2 Quintile 3 Quintile 4 Quintile 5

Middle Market

Increasing Household Income

43Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Insurers Continue to Advance Service with Mobile Phone Offerings

44Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

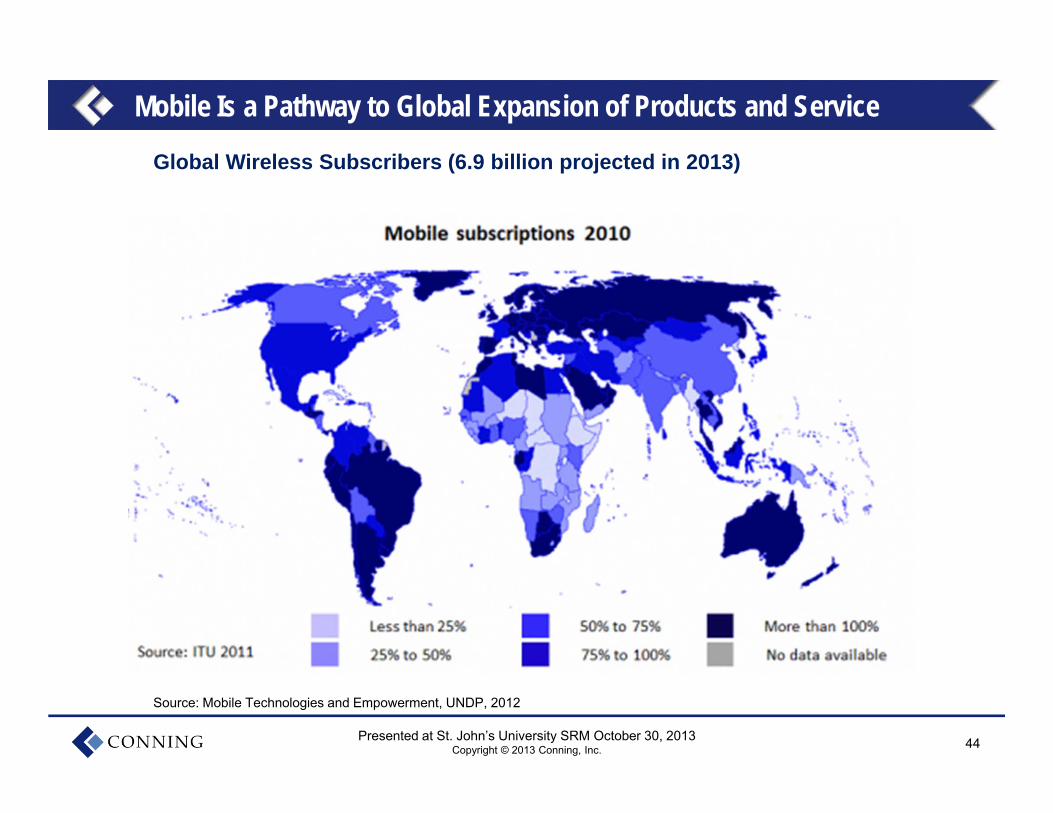

Mobile Is a Pathway to Global Expansion of Products and Service

Source: Mobile Technologies and Empowerment, UNDP, 2012

Global Wireless Subscribers (6.9 billion projected in 2013)

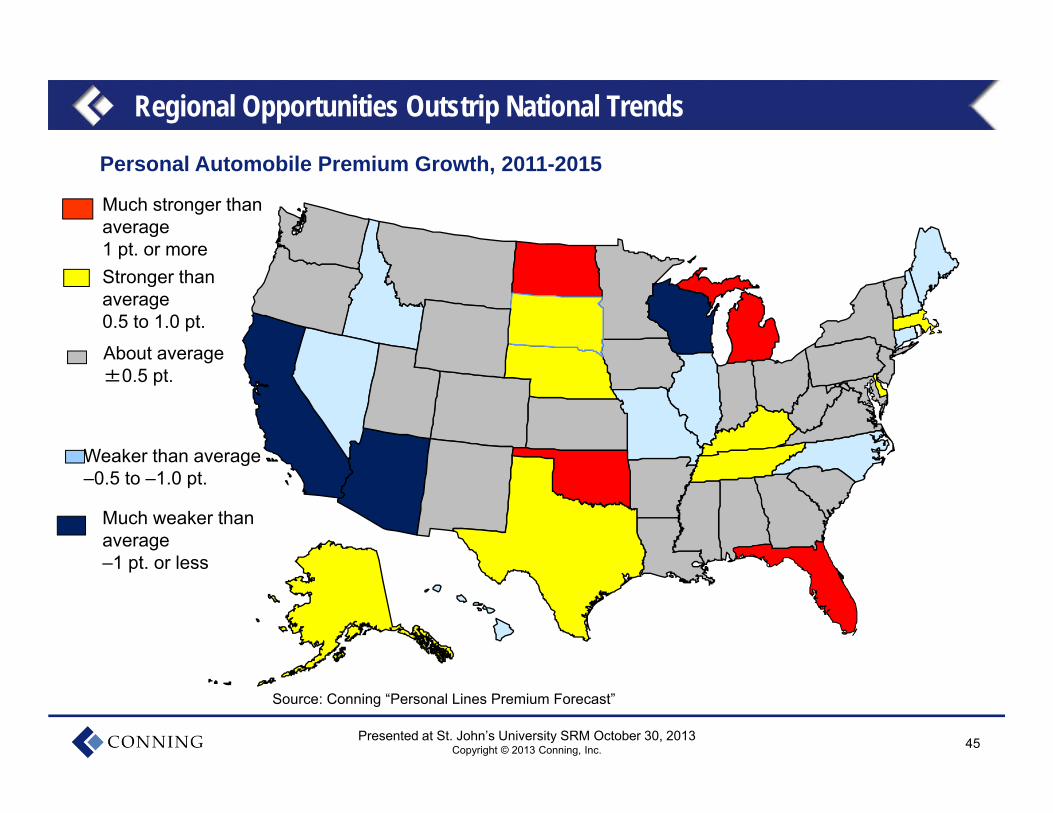

45Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Personal Automobile Premium Growth, 2011-2015

Much stronger than average1 pt. or moreStronger than average0.5 to 1.0 pt.

About average±0.5 pt.

Weaker than average–0.5 to –1.0 pt.

Much weaker than average–1 pt. or less

Source: Conning “Personal Lines Premium Forecast”

Regional Opportunities Outstrip National Trends

46Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

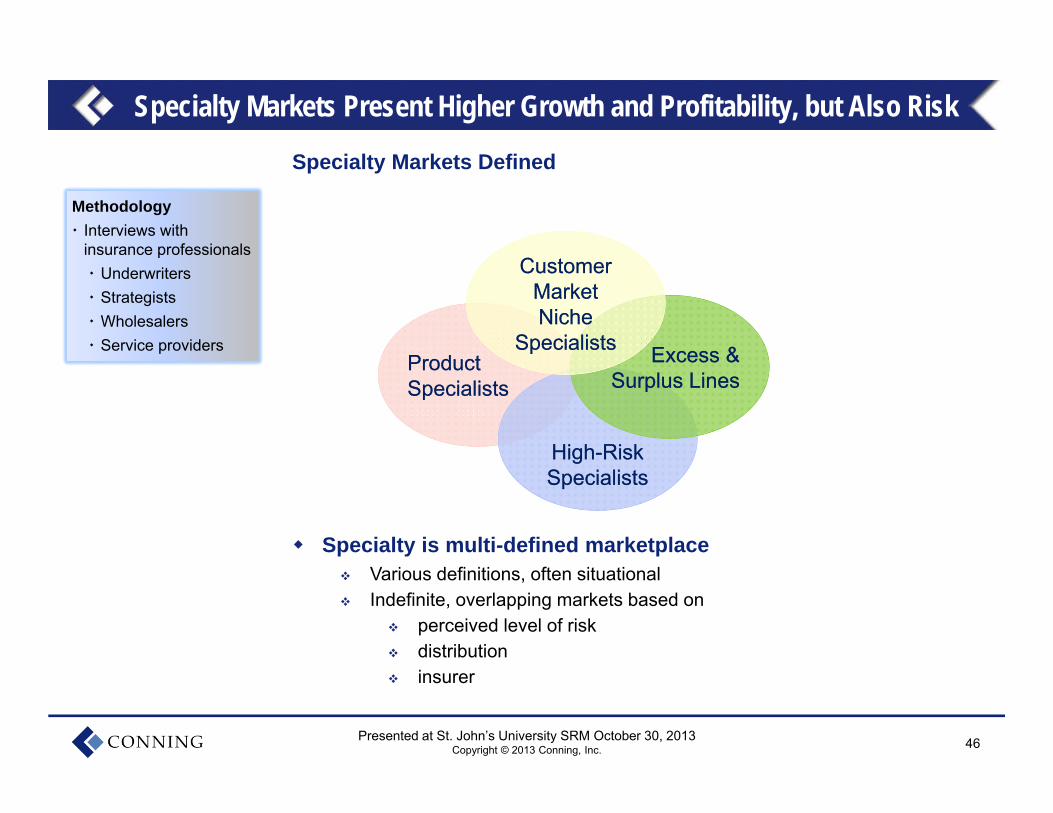

Specialty Markets Present Higher Growth and Profitability, but Also Risk

Specialty Markets Defined

Specialty is multi-defined marketplace Various definitions, often situational Indefinite, overlapping markets based on

perceived level of risk distribution insurer

Product SpecialistsProduct Specialists

High-Risk SpecialistsHigh-Risk Specialists

Excess & Surplus Lines

Excess & Surplus Lines

Customer Market Niche

Specialists

Customer Market Niche

Specialists

Methodology Interviews with

insurance professionals Underwriters Strategists Wholesalers Service providers

47Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

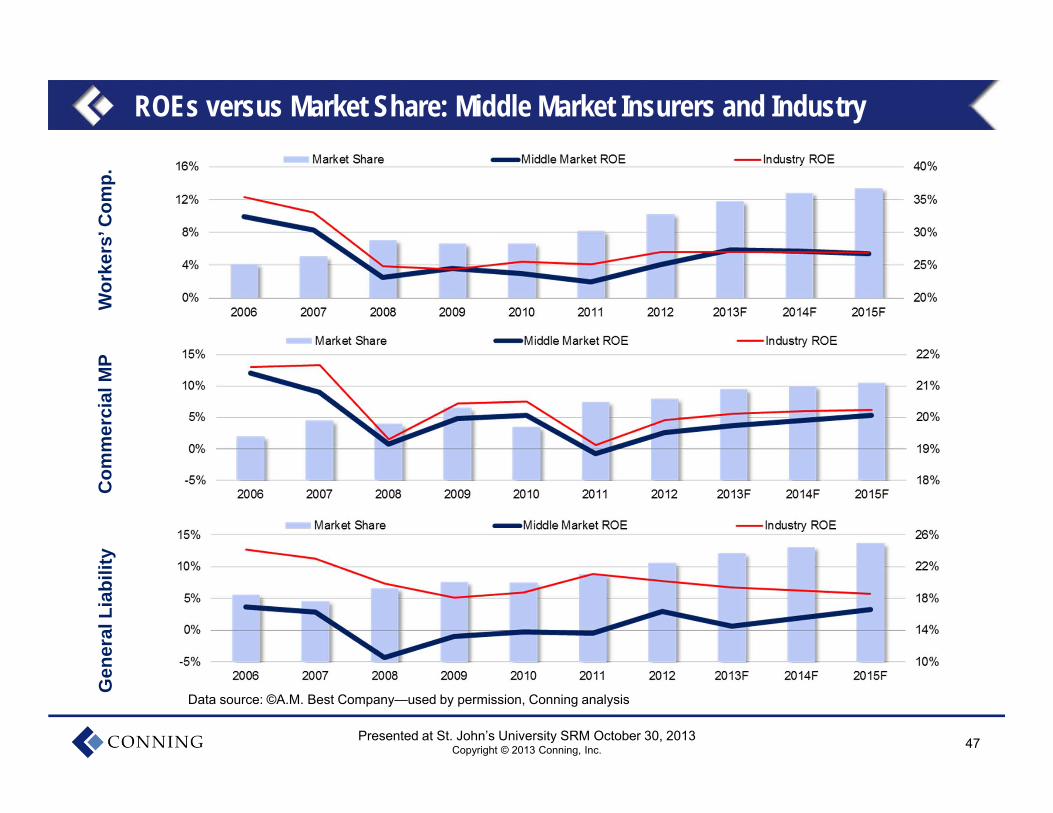

ROEs versus Market Share: Middle Market Insurers and IndustryW

orke

rs’ C

omp.

Com

mer

cial

MP

Gen

eral

Lia

bilit

y

Data source: ©A.M. Best Company—used by permission, Conning analysis

48Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

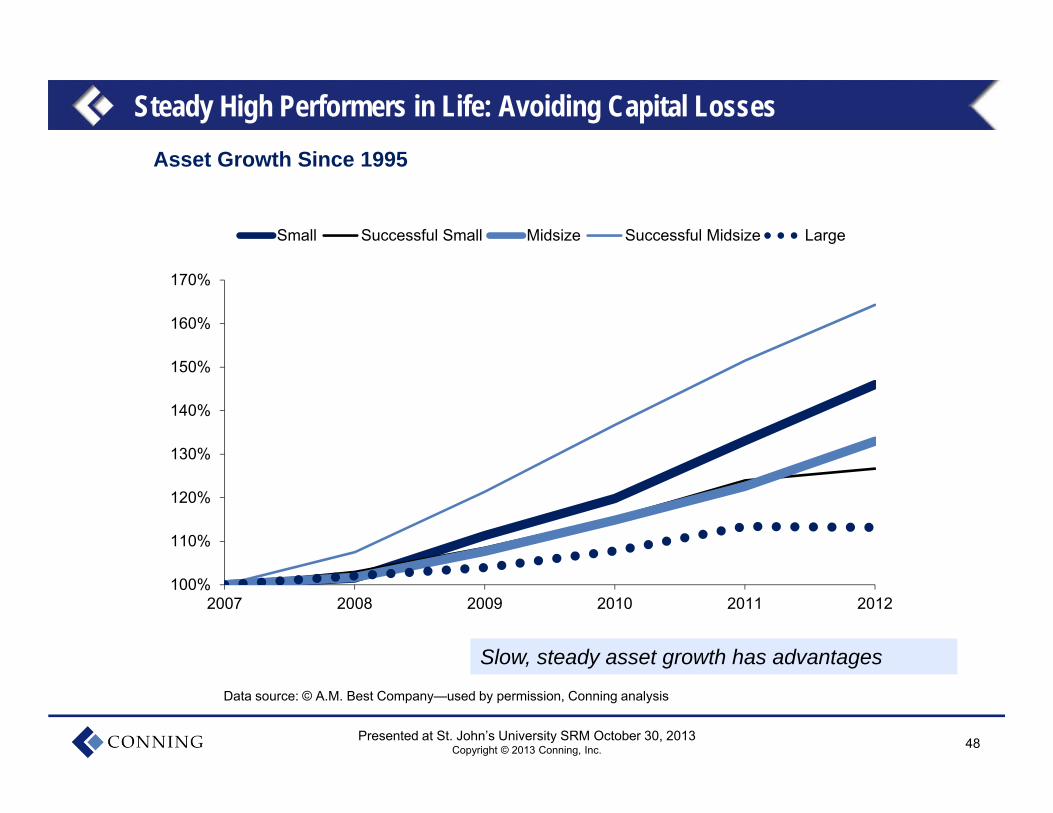

Steady High Performers in Life: Avoiding Capital LossesAsset Growth Since 1995

100%

110%

120%

130%

140%

150%

160%

170%

2007 2008 2009 2010 2011 2012

Small Successful Small Midsize Successful Midsize Large

Data source: © A.M. Best Company—used by permission, Conning analysis

Slow, steady asset growth has advantagesSlow, steady asset growth has advantages

49Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Cyber Risks: Identity, Personal Data, Denial of Service Pandemic: Bird Flu/Swine Flu Food-borne Pathogens: listeria, salmonella, vibrio, etc. Nanotechnology: The Next Asbestos? Synthetic Biology: Food Supply and Medical Technology Pharma and Antivirals: Product Liability and Water Pollution Global Warming and Regulatory Mandates D&O Exposure from JOBS act Securities Class Actions, Patents, Intellectual Property Electromagnetic Pollution Social Media (Personal Liability) BioTerrorism or Water Supply: Slow to Present Infrastructure Failure and Business Interruption 3D Printing Oil and gas fracking

New Customer Risks and New Opportunities—Sold, Not Bought

50Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

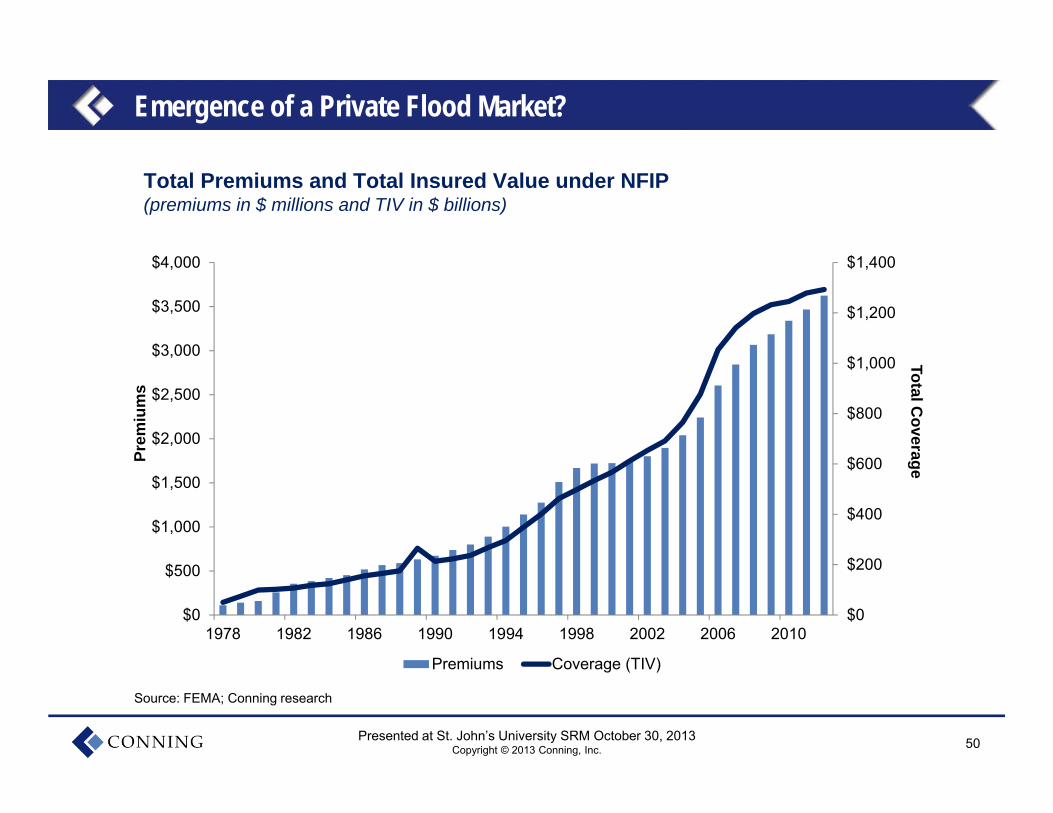

Emergence of a Private Flood Market?

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1978 1982 1986 1990 1994 1998 2002 2006 2010

Total Coverage

Prem

ium

s

Premiums Coverage (TIV)

Total Premiums and Total Insured Value under NFIP(premiums in $ millions and TIV in $ billions)

Source: FEMA; Conning research

51Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Customers’ own risk retention: RRGs, Captives, Deductibles

Global capital: marginalizes dedicated capital, opens new

markets

Competition from outside? Challenging the Value Proposition

Competition from Outside? Challenging the Value Proposition

52Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

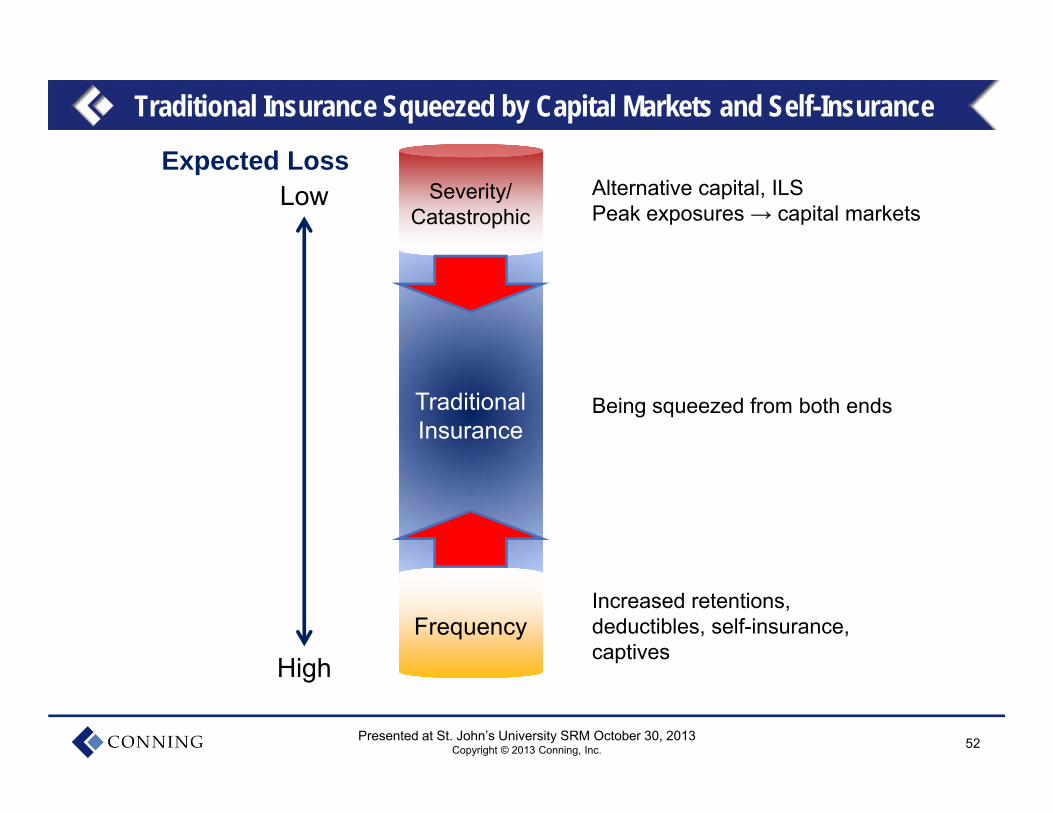

Traditional Insurance Squeezed by Capital Markets and Self-Insurance

Traditional InsuranceTraditional Insurance

Expected LossLow

High

Severity/ Catastrophic

Severity/ Catastrophic

FrequencyFrequency

Alternative capital, ILSPeak exposures → capital markets

Being squeezed from both ends

Increased retentions, deductibles, self-insurance, captives

53Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

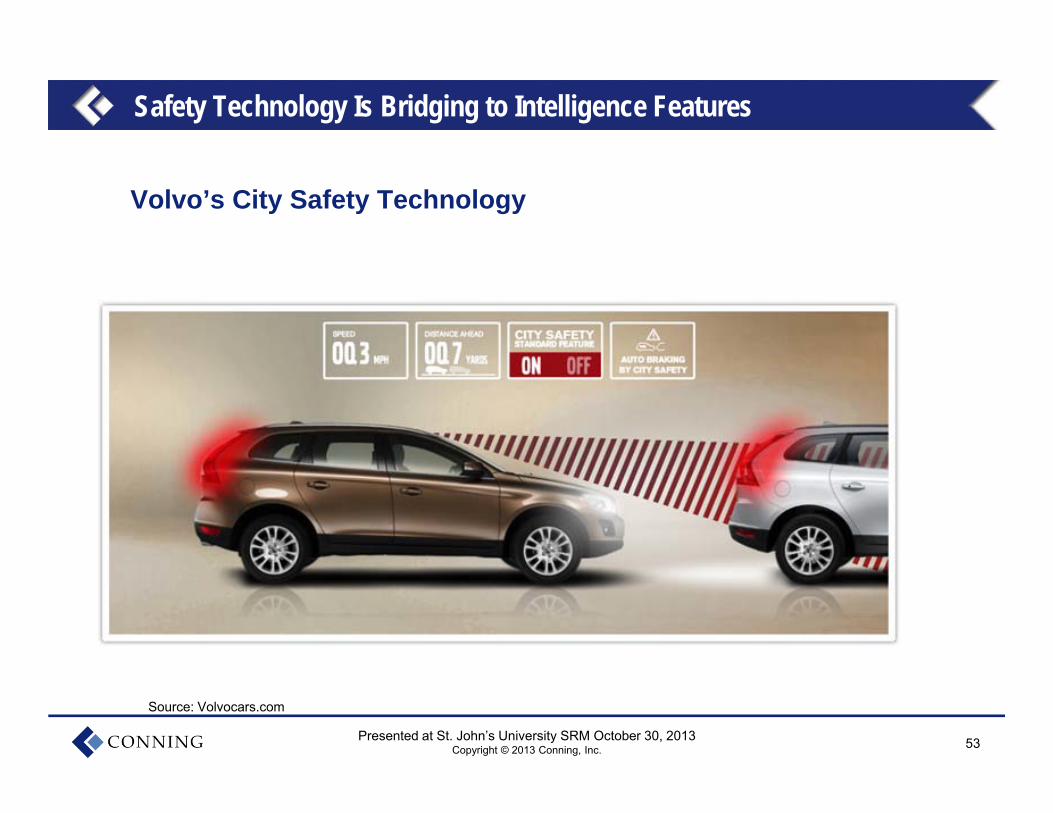

Safety Technology Is Bridging to Intelligence Features

Volvo’s City Safety Technology

Source: Volvocars.com

54Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

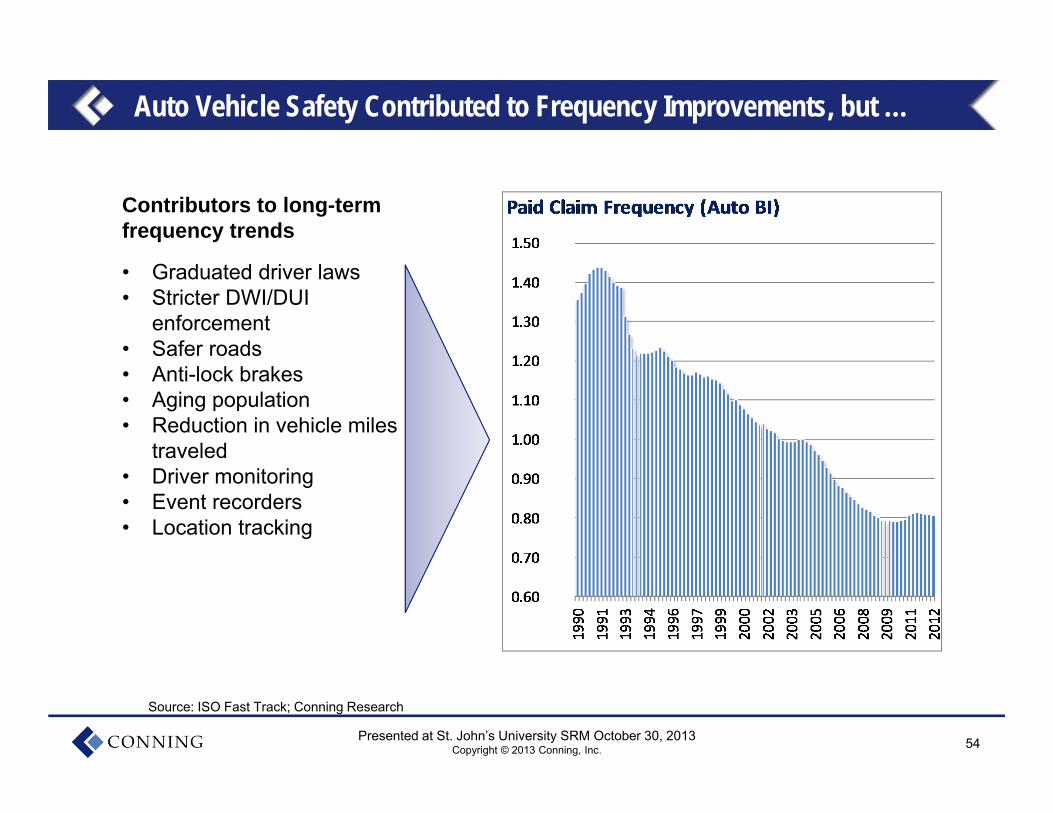

Auto Vehicle Safety Contributed to Frequency Improvements, but …

Contributors to long-term frequency trends

• Graduated driver laws• Stricter DWI/DUI

enforcement• Safer roads• Anti-lock brakes• Aging population• Reduction in vehicle miles

traveled• Driver monitoring• Event recorders• Location tracking

Source: ISO Fast Track; Conning Research

55Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

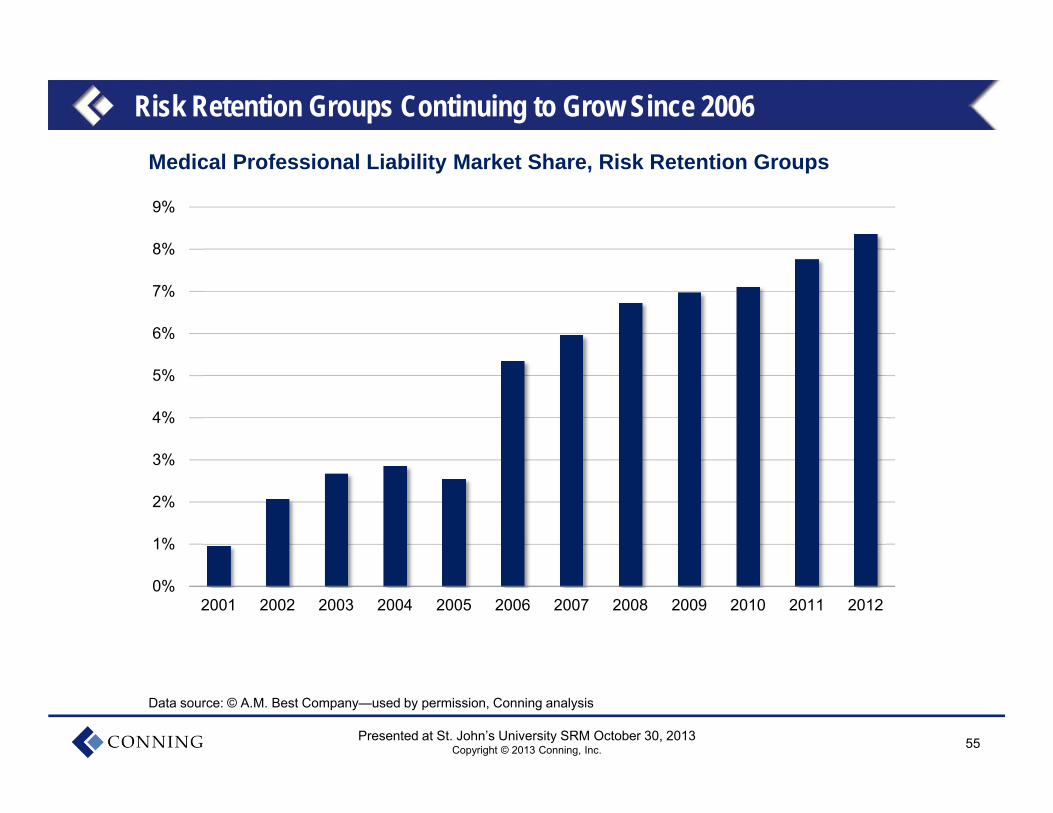

Medical Professional Liability Market Share, Risk Retention Groups

Data source: © A.M. Best Company—used by permission, Conning analysis

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Risk Retention Groups Continuing to Grow Since 2006

56Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

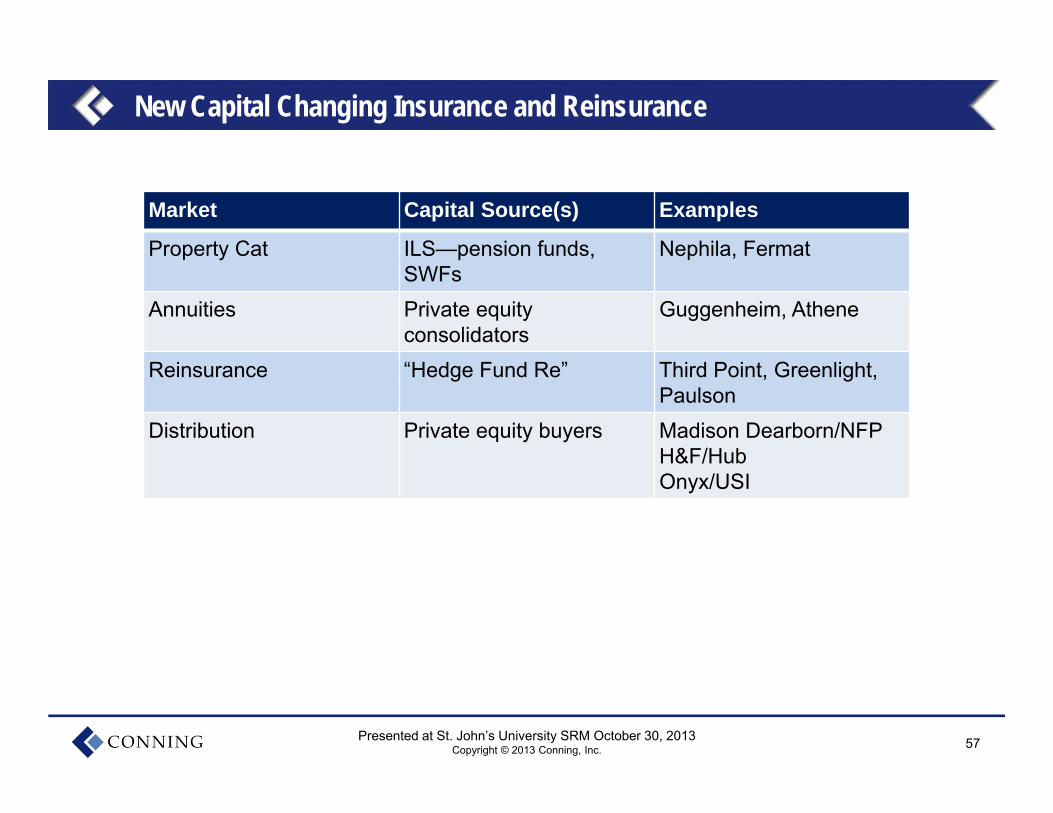

New Capital Changing Insurance and Reinsurance

Global Platforms ILS

Nontraditional capital changing reinsurance landscape Swaps, sidecars Reaction of reinsurers, impact on pricing Cat modeling customers gain access to cat models

Lloyd’s Global Capital and Emerging Markets

Domestic vs. international players Risk accumulation and credit risk

Contingent Capital

57Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

New Capital Changing Insurance and Reinsurance

Market Capital Source(s) Examples

Property Cat ILS—pension funds, SWFs

Nephila, Fermat

Annuities Private equity consolidators

Guggenheim, Athene

Reinsurance “Hedge Fund Re” Third Point, Greenlight, Paulson

Distribution Private equity buyers Madison Dearborn/NFPH&F/HubOnyx/USI

58Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Potential New Entrants Challenging the Value Proposition

Banks, brokers Alternative capital Government safety nets and subsidies

But what about….

Big Box Retailers Walmart Costco

Technology and eCommerce Google, Amazon Crowdfunding

Examples

59Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

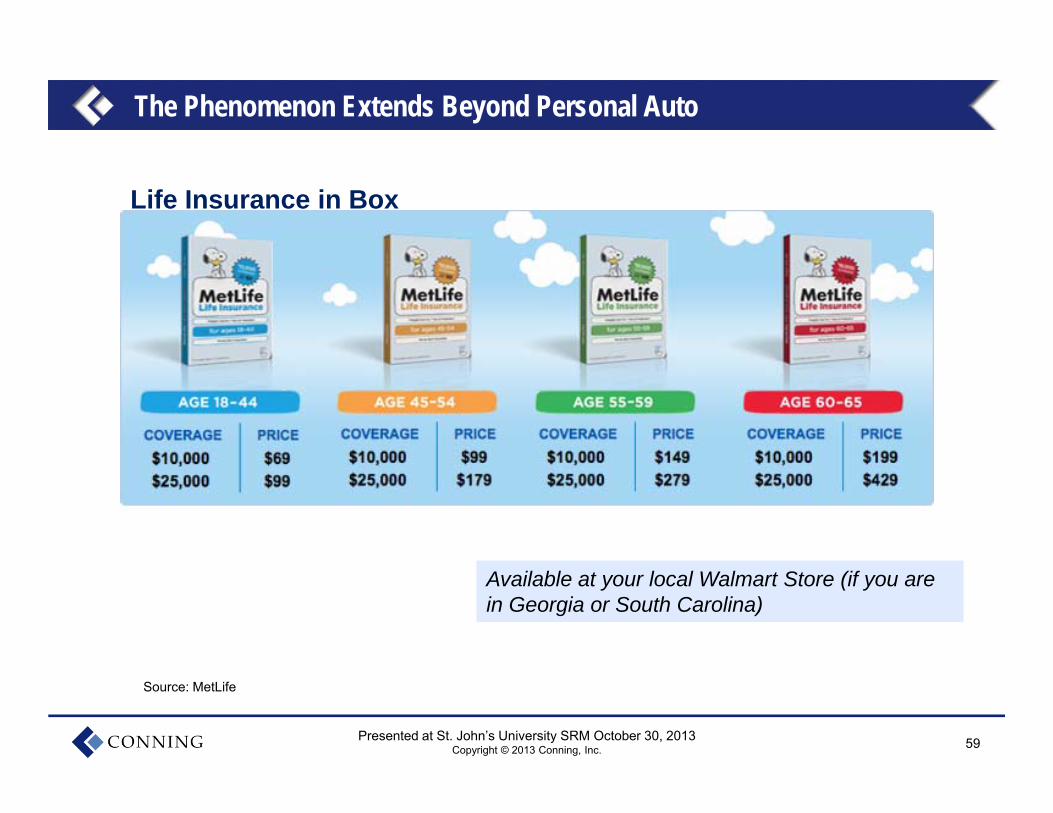

The Phenomenon Extends Beyond Personal Auto

Life Insurance in Box

Source: MetLife

Available at your local Walmart Store (if you are in Georgia or South Carolina)Available at your local Walmart Store (if you are in Georgia or South Carolina)

60Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Regulatory Complexity Challenging the Business Model

Multiple layers of jurisdiction

Competing and sometimes conflicting purposes

Opportunities for the nimble?

61Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

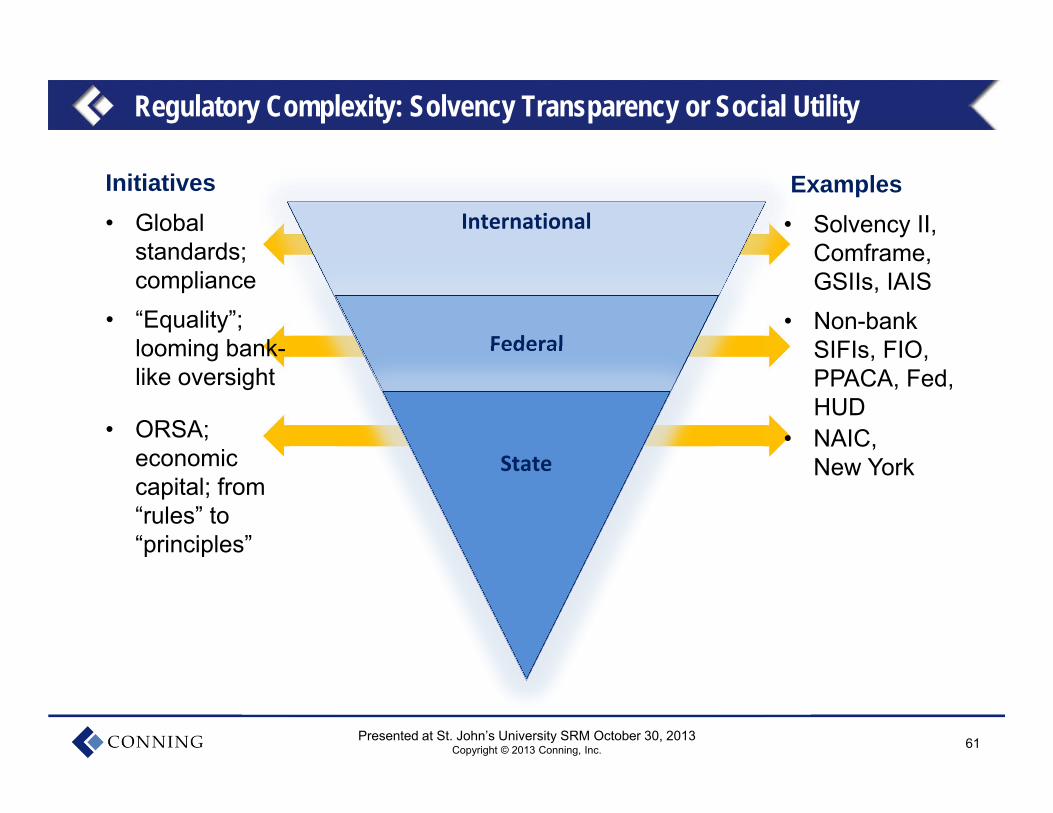

Regulatory Complexity: Solvency Transparency or Social Utility

International

Federal

State

Initiatives

• “Equality”; looming bank-like oversight

• Global standards; compliance

• ORSA; economic capital; from “rules” to “principles”

Examples

• Non-bank SIFIs, FIO, PPACA, Fed, HUD

• Solvency II, Comframe, GSIIs, IAIS

• NAIC, New York

62Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

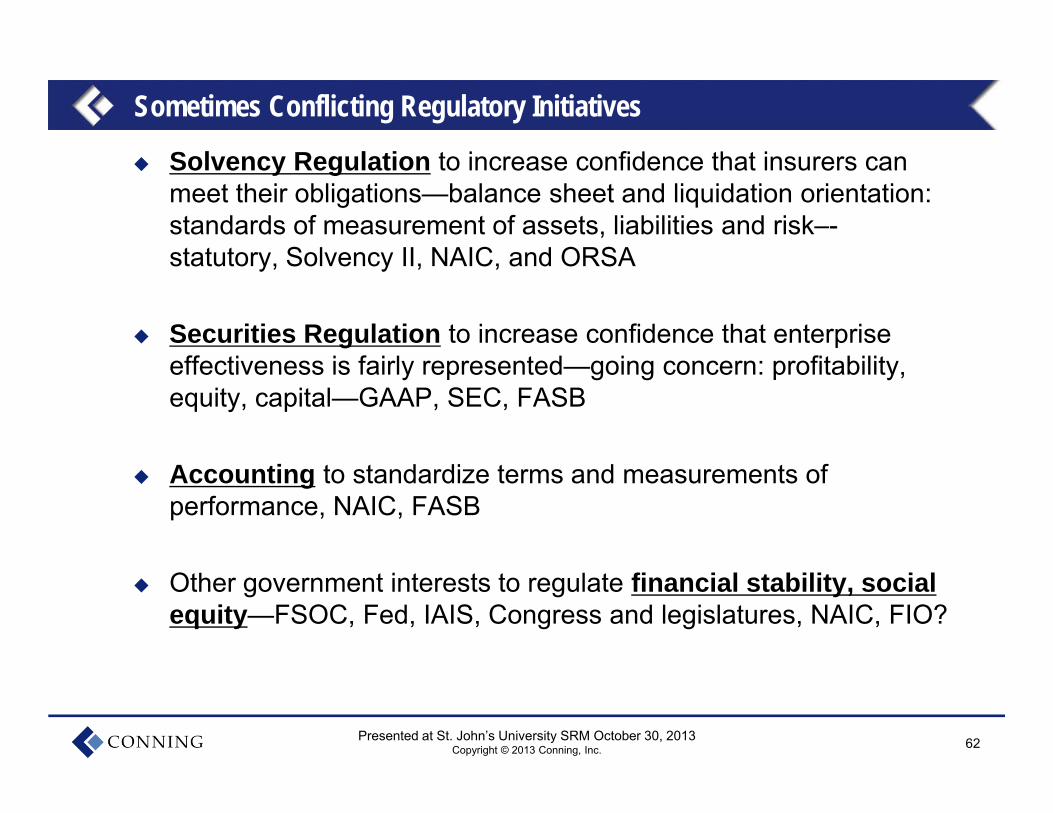

Sometimes Conflicting Regulatory Initiatives

Solvency Regulation to increase confidence that insurers can meet their obligations—balance sheet and liquidation orientation: standards of measurement of assets, liabilities and risk–-statutory, Solvency II, NAIC, and ORSA

Securities Regulation to increase confidence that enterprise effectiveness is fairly represented—going concern: profitability, equity, capital—GAAP, SEC, FASB

Accounting to standardize terms and measurements of performance, NAIC, FASB

Other government interests to regulate financial stability, social equity—FSOC, Fed, IAIS, Congress and legislatures, NAIC, FIO?

63Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

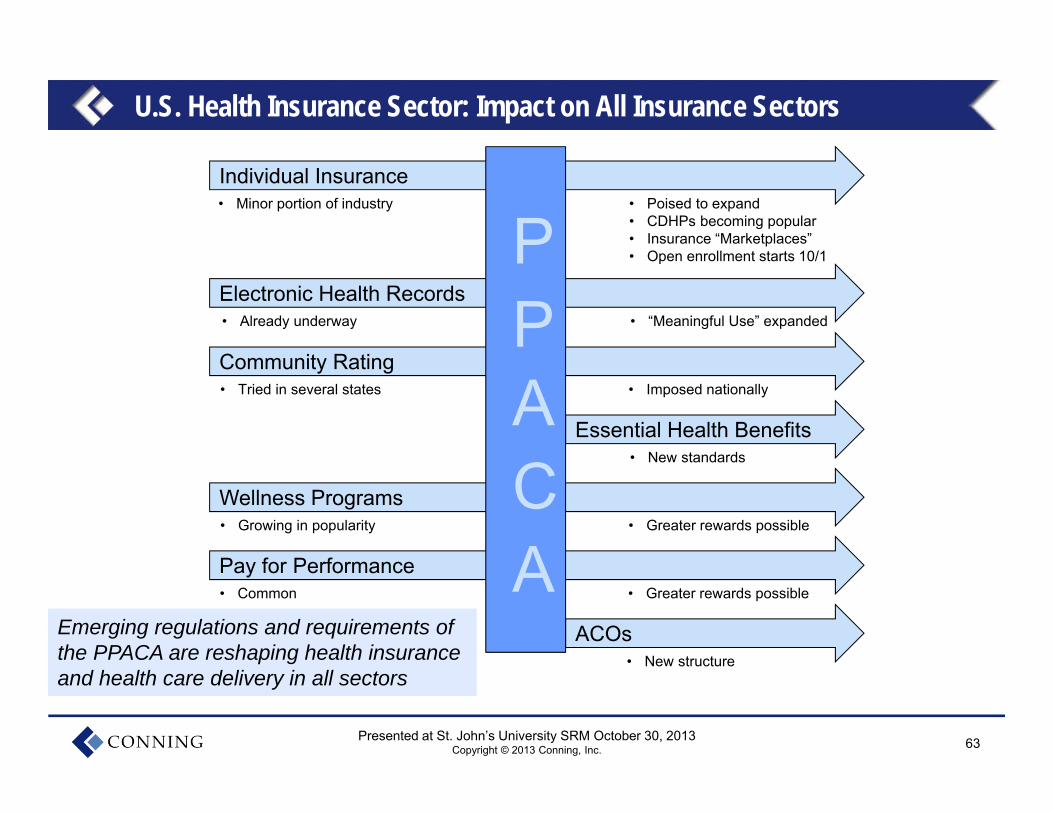

U.S. Health Insurance Sector: Impact on All Insurance Sectors

Pay for Performance

Electronic Health Records

Community Rating

Essential Health Benefits

Wellness Programs

Individual Insurance

ACOs

• Minor portion of industry • Poised to expand• CDHPs becoming popular• Insurance “Marketplaces”• Open enrollment starts 10/1

• Already underway • “Meaningful Use” expanded

• Tried in several states • Imposed nationally

• New standards

• Growing in popularity • Greater rewards possible

• Common • Greater rewards possible

• New structure

PPACA

Emerging regulations and requirements of the PPACA are reshaping health insurance and health care delivery in all sectors

Emerging regulations and requirements of the PPACA are reshaping health insurance and health care delivery in all sectors

64Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

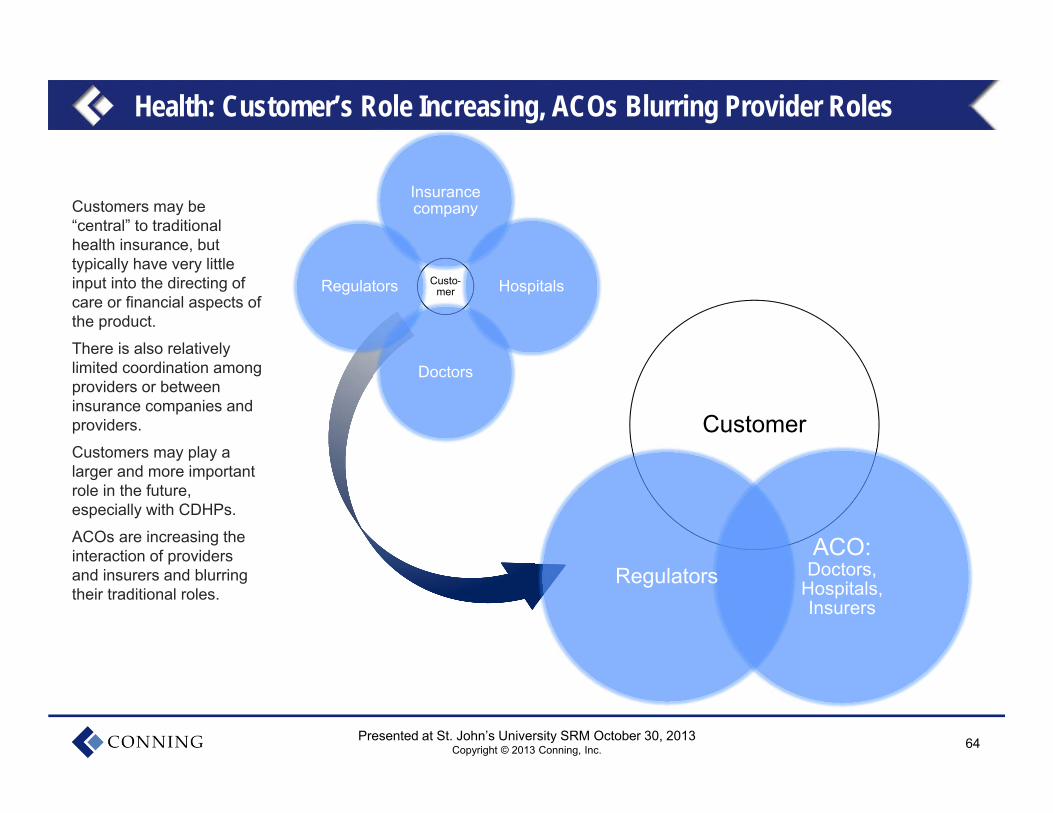

Health: Customer’s Role Increasing, ACOs Blurring Provider Roles

Custo-mer

Insurance company

Hospitals

Doctors

Regulators

Customer

ACO:Doctors,

Hospitals, Insurers

Regulators

Customers may be “central” to traditional health insurance, but typically have very little input into the directing of care or financial aspects of the product.

There is also relatively limited coordination among providers or between insurance companies and providers.

Customers may play a larger and more important role in the future, especially with CDHPs.

ACOs are increasing the interaction of providers and insurers and blurring their traditional roles.

65Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

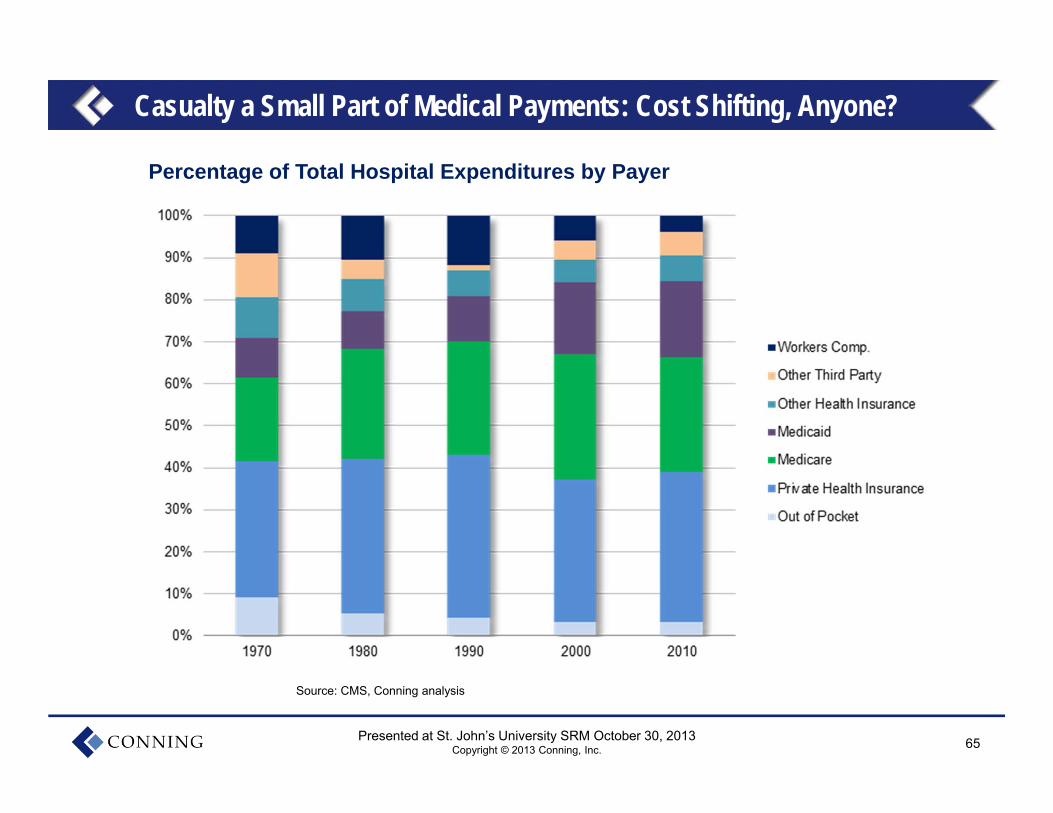

Casualty a Small Part of Medical Payments: Cost Shifting, Anyone?

Source: CMS, Conning analysis

Percentage of Total Hospital Expenditures by Payer

66Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

Fourteen in Fourteen: Trends to Watch in Insurance 1. Good news: Strong performance—pricing, underwriting, risk discipline

2. Headwinds: Economy and reduced portfolio yields

3. Headwinds: Capital buildup and increasing elements of risk

4. Technology transformation paying off?

5. Data and analytics: application across the value chain

6. Changing customer base: empowered customers and need to segment

7. New models of service through technology: pathway to global?

8. Mid Market outperforms: Targeting specialized risk and service

9. New risks and new opportunities emerging—sold, not bought

10. Customer risk retention: challenging the value proposition

11. Competition from outside: leveraging different parts of the value chain

12. Global capital flows: marginalizing dedicated capital

13. Competition among regulators challenging the competitive market?

14. Health care transformation: more challenges and opportunities

67Presented at St. John’s University SRM October 30, 2013Copyright © 2013 Conning, Inc.

DisclosuresConning & Company is the parent of Conning, Inc., Goodwin Capital Advisers, Inc. and Conning Investment Products, Inc., a FINRA-registered broker dealer, andan affiliate of Conning Asset Management Limited, and Cathay Conning Asset Management Limited (CCAM) (together, “Conning”). Conning is a portfoliocompany of the funds managed by Aquiline Capital Partners LLC (a New York-based private equity firm,) with offices in Hartford, Purchase, London, Cologne, andHong Kong.

Conning, Inc. and Goodwin Capital Advisers, Inc. are registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of1940. Conning, Inc. is also registered with the Ontario Securities Commission. Conning Asset Management Limited is authorized and regulated by the UnitedKingdom's Financial Conduct Authority, and Cathay Conning Asset Management Limited is regulated by Hong Kong’s Securities and Futures Commission.Conning primarily provides asset management services for third-party assets. Conning predominantly invests client portfolios in fixed income strategies inaccordance with guidelines supplied by its institutional clients.

Conning, Inc. is registered as an Investment Adviser with the SEC and has noticed other jurisdictions it is conducting securities advisory business when requiredby law. In any other jurisdictions where it has not provided notice and is not exempt or excluded from those laws, it cannot transact business as an investmentadviser and may not be able to respond to individual inquiries if the response could potentially lead to a transaction in securities.

All investment performance information included within this material is historical. Past performance is not indicative of future results. Any tax related informationcontained within this presentation is for informational purposes only and should not be considered tax advice. You should consult a tax professional with anyquestions.

For complete details regarding Conning and its services, you should refer to our Form ADV Part 2, which may be obtained by calling us.

Legal Disclaimer

Copyright 2013 Conning, Inc. This document and the software described within are copyrighted with all rights reserved. No part of this document may bereproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior writtenpermission of Conning. Conning does not make any warranties, express or implied, in this document. In no event shall Conning be liable for damages of any kindarising out of the use of this document or the information contained within it.

This document contains information that is confidential or proprietary to Conning (or their direct and indirect subsidiaries). By accepting this document you agreethat: (1) if there is any pre-existing contract containing disclosure and use restrictions between your company and Conning, you and your company will use thisinformation in reliance on and subject to the terms of any such pre-existing contract; or (2) if there is no contractual relationship between you and your companyand Conning, you and your company agree to protect this information and not to reproduce, disclose or use the information in any way, except as may be requiredby law.

ADVISE®, FIRM®, and GEMS® are registered trademarks of Conning, Inc.

This material is for informational purposes only and should not be interpreted as an offer to sell, or a solicitation or recommendation of an offer to buy any security,product or service, or retain Conning for investment advisory services. This information is not intended to be nor should it be used as investment advice andshould not be copied or distributed without the prior consent of Conning.

Disclosure C11#1412415Presentation C11#1728790

About Conning

Conning (www.conning.com) is a leading investment management company for the global insurance industry, Cathay Conning Asset Management, and its Goodwin Capital Advisers subsidiary. The

Company’s unique combination of asset management, risk and capital management solutions, and insurance research helps clients achieve their financial goals through customized business and

investment strategies. The company is headquartered in Hartford, Connecticut, with additional offices in New York, London, Cologne, and Hong Kong.

Insurance Research

Conning publishes a number of insurance industry research services, including its Insurance Segment Reports semiannual line-of-business reviews; its Forecast & Analysis service, which offers a forward

look at the industry; and its well-known Strategic Study series of executive reports on key products and trends and issues of critical industry importance. All are available in print and online through our web-

based research portal Conning Library (www.conninglibrary.com).

For more information on our insurance research services, please call 888-707-1177 or visit www.conningresearch.com.

This presentation has been prepared for and distributed exclusively to specific clients of Conning. Further distribution, sale, or reproduction, in whole or in part, and by any means, is prohibited. Statements and information in this report were compiled from sources

that we consider to be reliable or are expressions of our opinion. The presentation is not intended to be complete, and we do not guarantee its accuracy. It does not constitute and must not be considered investment advice. With offices in Hartford, New York, London,

Cologne, and Hong Kong, Conning is a portfolio company of the funds managed by Aquiline Capital Partners LLC (“Aquiline”), a NewYork-based private equity firm.