united property & casualty insurance company · underwriting guidelines . 1. coverages, forms...

TRANSCRIPT

United Property & Casualty

Insurance Company

HOMEOWNERS PROGRAM MANUAL

MASSACHUSETTS

Effective 04/01/2016 (New Business) 05/15/2016 (Renewal Business)

UNITED INSURANCE MANAGEMENT, LC

Managing General Agent

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-i Ed. 05/13 v.6.4

Table of Contents

UNDERWRITING GUIDELINES 1. Coverages, Forms and Limits ....................................................................................................... HO-1-1 2. General Underwriting Requirements ............................................................................................ HO-2-1 3. Ineligible Risks .............................................................................................................................. HO-3-1 4. Binding Authority ........................................................................................................................... HO-4-1 5. Application and Submission Requirements .................................................................................. HO-5-1 6. Loss Settlement Conditions .......................................................................................................... HO-6-1 7. Payment Plans .............................................................................................................................. HO-7-1 8. Individual Insurance Financial Scoring ......................................................................................... HO-8-1 9. Special State Requirements ......................................................................................................... HO-9-1

GENERAL RULES 100. Description of Coverages.......................................................................................................... HO-101-1 110. Mandatory Coverages ............................................................................................................... HO-110-1 120. Eligibility .................................................................................................................................... HO-120-1 130. Secondary Residence Premises ............................................................................................... HO-130-1 140. Seasonal Dwellings ................................................................................................................... HO-140-1 150. Policy Period ............................................................................................................................. HO-150-1 160. Protection Classification Codes and Information ...................................................................... HO-160-1 170. Method of Payment ................................................................................................................... HO-170-1 180. Changes or Cancellations ......................................................................................................... HO-180-1 190. Construction Definitions ............................................................................................................ HO-190-1 200. Single Building Definition .......................................................................................................... HO-200-1 210. Minimum Premium .................................................................................................................... HO-210-1 220. Manual Premium Revision ........................................................................................................ HO-220-1 230. Transfer or Assignment ............................................................................................................. HO-230-1 240. Waiver of Premium ................................................................................................................... HO-240-1 250. Whole Dollar Premium Rule...................................................................................................... HO-250-1 300. Base Premium Computation ..................................................................................................... HO-300-1 310. Ordinance or Law Coverage – All Forms except Ho 00 04 ...................................................... HO-310-1 315. Superior Construction ............................................................................................................... HO-315-1 316. Restriction of Individual Policies ............................................................................................... HO-316-1 317. Additional Interest ..................................................................................................................... HO-317-1 318. Loss Settlement Options ........................................................................................................... HO-318-1 319. Special Personal Property Coverage HO 00 04 and HO 00 06 ............................................... HO-319-1 410. Town House or Row House – Forms HO 00 03 and HO 00 05 Only ....................................... HO-410-1 420. Personal Property (Coverage C) Valuation – Replacement Cost/Actual Cash Value .............. HO-420-1 430. Protective Devices .................................................................................................................... HO-430-1 440. Deductibles ............................................................................................................................... HO-440-1 450. Additional Amounts of Insurance – Form HO 00 03 and HO 00 05 Only ................................. HO-450-1 460. Maximum Credit Rule ............................................................................................................... HO-460-1 465. Supplemental Heating Surcharge..……………………………………………………...…………..HO-465-1 470. New Home Credit – Forms HO 00 03 and HO 00 05 Only ....................................................... HO-470-1 475. Older Home Surcharge – Forms HO 00 03 and HO 00 05 Only…………………………………HO-475-1 480. Renewal Credit – Forms HO 00 03 and HO 00 05 Only ........................................................... HO-480-1 481. Building Additions and Alterations at Other Residence ............................................................ HO-481-1 482. Building Additions and Alterations – Increased Limits – HO 00 04 .......................................... HO-482-1 490. Inflation Guard – Forms HO 00 03 and HO 00 05 Only ............................................................ HO-490-1

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-ii Ed. 05/13 v.6.4

500. Business Property – Increased Limits ...................................................................................... HO-500-1 510. Credit Card, Fund Transfer Card, Forgery and Counterfeit Money .......................................... HO-510-1 520. Companion Automobile Policy Credit – Forms HO 00 03 and HO 00 05 Only ........................ HO-520-1 525. Mature Homeowner Credit – All Forms ……………………………………………….……………..HO-525-1 530. Form HO 00 06 – Coverage A Dwelling Basic and Increased Limits and Special Coverage .. HO-530-1 540. Form HO 00 06 – Units Regularly Rented to Others ................................................................ HO-540-1 550. Permitted Incidental Occupancies – Residence Premises ....................................................... HO-550-1 551. Loss of Use – Increase Only ..................................................................................................... HO-551-1 553. Sinkhole Collapse Coverage All Forms except HO 00 04 and HO 00 06 ................................ HO-553-1 560. Special Computer Coverage ..................................................................................................... HO-560-1 561. Other Members of a Named Insured’s Household ................................................................... HO-561-1 562. Residence Held in Trust All Forms except HO 00 04 ............................................................... HO-562-1 563. Student Away from Home ......................................................................................................... HO-563-1 565. Equipment Breakdown Coverage – HO 00 03, HO 00 05, and HO 00 06 ............................... HO-565-1 570. Loss Assessment Coverage ..................................................................................................... HO-570-1 580. Other Structures – HO 00 03 and HO 00 05 Only .................................................................... HO-580-1 585. Flood Policy Credit – Forms HO 00 03 and HO 00 05 Only ..................................................... HO-585-1 590. Refrigerated Personal Property ................................................................................................ HO-590-1 600. Personal Property – Increased and Reduced Limits ................................................................ HO-600-1 610. Scheduled Personal Property ................................................................................................... HO-610-1 611. Rental to Others – Extended Theft Coverage – All Forms except HO 00 05, HO 00 04 with HO 05 24 or HO 00 06 with HO 17 31 ............................................................................... HO-611-1 620. Golf Cart Physical Damage....................................................................................................... HO-620-1 630. Water Back Up and Sump Overflow ......................................................................................... HO-630-1 640. Water Loss Prevention Credit ................................................................................................... HO-640-1 645. Limited Fungi, Wet or Dry Rot or Bacteria Coverage ............................................................... HO-645-1 650. Loss Free Credit – All Forms .................................................................................................... HO-650-1 655. Earthquake Coverage ............................................................................................................... HO-655-1 660. Identity Theft Expense and Resolution Services Coverage ..................................................... HO-660-1 670. Lead Poisoning Exclusion and Coverage Option ..................................................................... HO-670-1 674. Modified Other Insurance and Service Agreement Condition – Form HO 00 06 Only……… .HO-674-1 675. Optional Property Remediation for Escaped Liquid Fuel and Limited Escaped Liquid Fuel Liability Coverages ............................................................................................................ HO-675-1 676. Relocation Expenses for Tenants – Forms HO 00 03 and HO 00 05 Only .............................. HO-676-1 677. Residence Employees .............................................................................................................. HO-677-1 678. Business Pursuits ..................................................................................................................... HO-678-1 680. Safe Home Credit – Forms HO 00 03 and HO 00 05 Only ....................................................... HO-680-1 685. Evacuation Coverage ................................................................................................................ HO-685-1 690. Building Code Effectiveness Grading ....................................................................................... HO-690-1 700. Ultra Endorsement – Forms HO 00 03 and HO 00 05 .............................................................. HO-700-1 701. Premier Endorsement – Forms HO 00 03 and HO 00 05 ......................................................... HO-701-1 703. Protector Endorsement – Forms HO 00 03 and HO 00 05 ....................................................... HO-703-1 710. Premier Protective Condominium Endorsement – HO 00 06 Only........................................... HO-710-1 720. Premier Mini-Farm Endorsement – Forms HO 00 03 and HO 00 05 ....................................... HO-720-1 800. Basic and Increased Limits – Residence Premises .................................................................. HO-800-1 810. Other Structures Rented to Others – Residence Premises ...................................................... HO-810-1 815. Additional Residence Rented to Others .................................................................................... HO-815-1 820. Permitted Incidental Occupancies – Residence Premises ....................................................... HO-820-1 830. Outboard Motors and Watercraft………………………………………………………………….HO-830-1 840. Personal Injury .......................................................................................................................... HO-840-1

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-iii Ed. 05/13 v.6.4

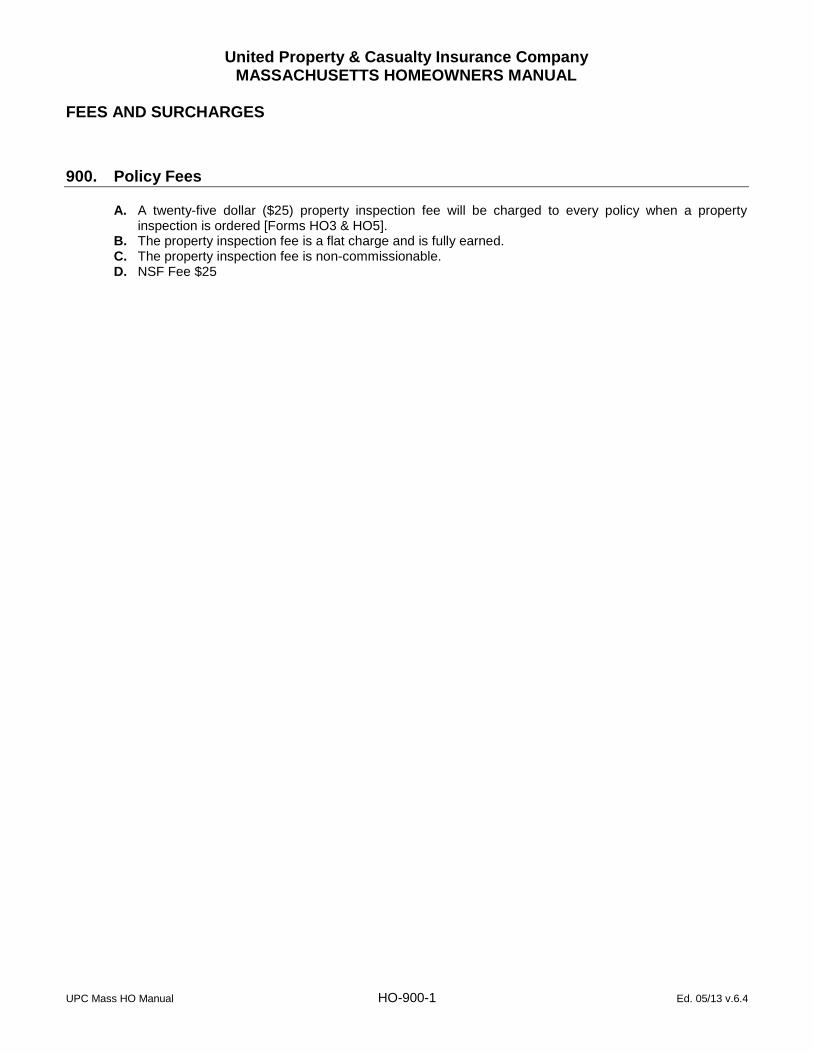

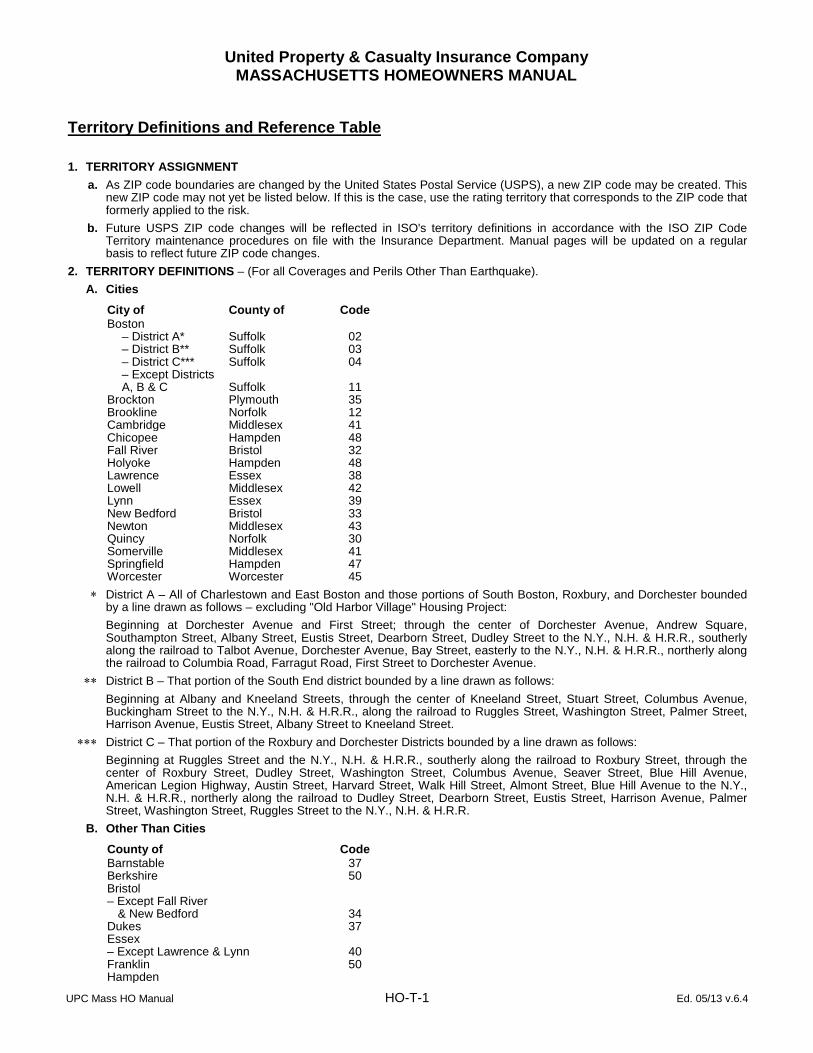

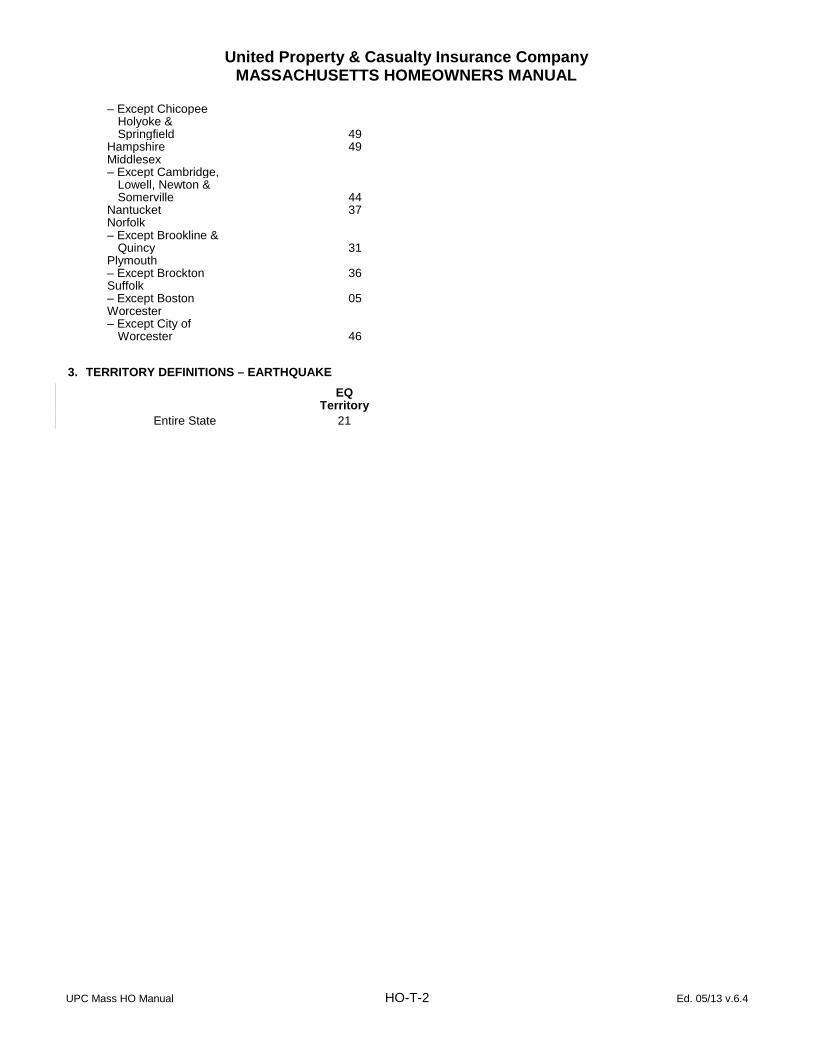

FEES AND SURCHARGES 900. Policy Fees ............................................................................................................. …………...HO-900-1 Territory Definitions and Reference Table .................................................................................... HO-T-1 300. Base Premium Determination – Table Index ....................................................................... HO-T-3

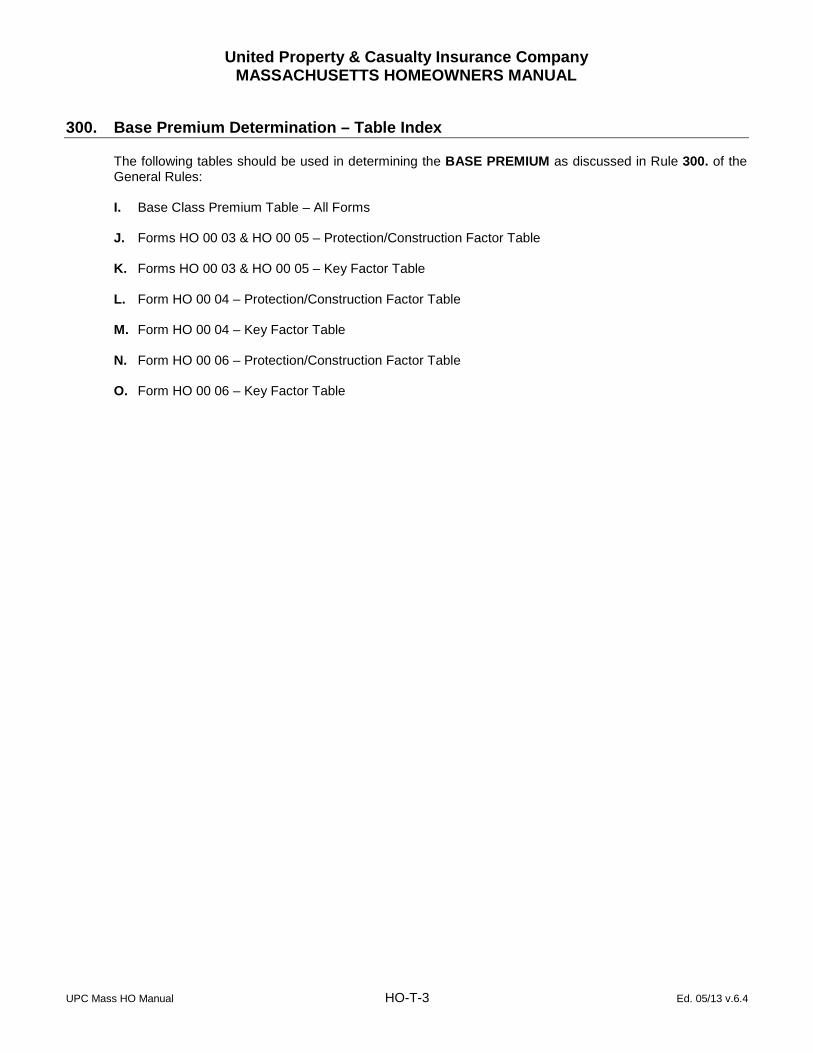

A. Base Class Premium Table – All Forms B. CAT Band Surcharge C. Forms HO 00 03 & HO 00 05 – Protection/Construction Factor Table D. Forms HO 00 03 & HO 00 05 – Key Factor Table E. Form HO 00 04 – Protection/Construction Factor Table F. Form HO 00 04 – Key Factor Table G. Form HO 00 06 – Protection/Construction Factor Table H. Form HO 00 06 – Key Factor Table

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

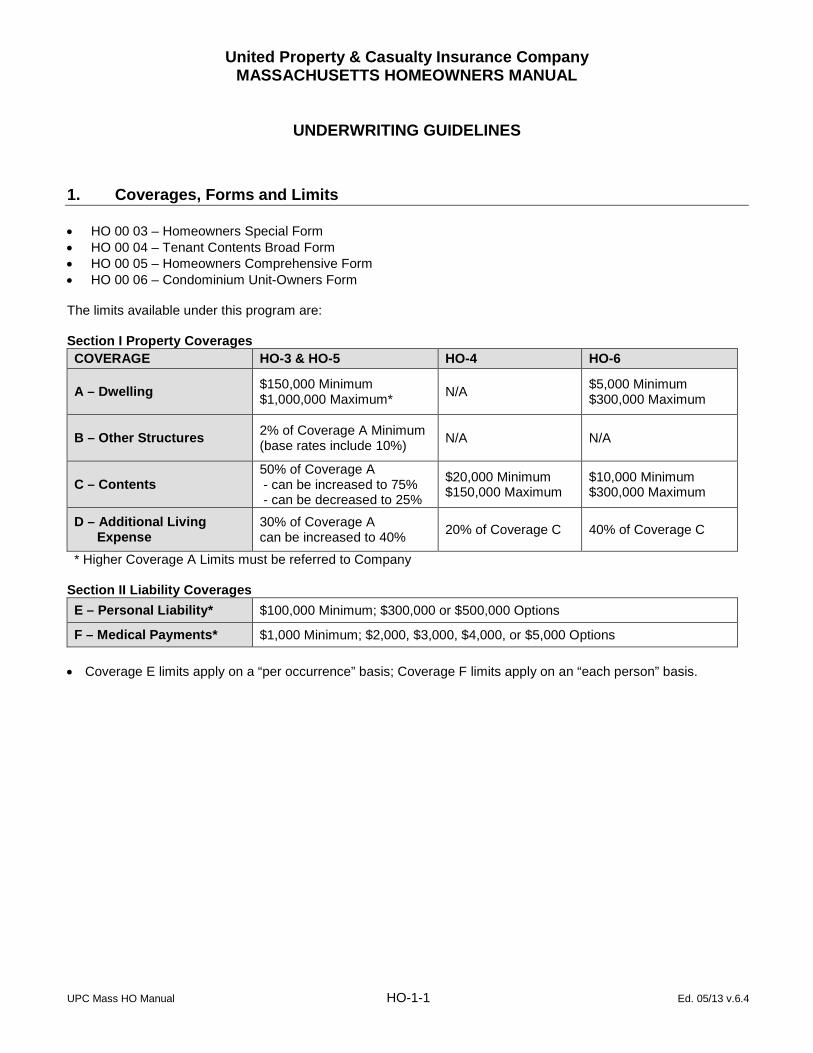

UPC Mass HO Manual HO-1-1 Ed. 05/13 v.6.4

UNDERWRITING GUIDELINES

1. Coverages, Forms and Limits • HO 00 03 – Homeowners Special Form • HO 00 04 – Tenant Contents Broad Form • HO 00 05 – Homeowners Comprehensive Form • HO 00 06 – Condominium Unit-Owners Form The limits available under this program are: Section I Property Coverages COVERAGE HO-3 & HO-5 HO-4 HO-6

A – Dwelling $150,000 Minimum $1,000,000 Maximum* N/A $5,000 Minimum

$300,000 Maximum

B – Other Structures 2% of Coverage A Minimum (base rates include 10%)

N/A

N/A

C – Contents 50% of Coverage A - can be increased to 75% - can be decreased to 25%

$20,000 Minimum $150,000 Maximum

$10,000 Minimum $300,000 Maximum

D – Additional Living Expense

30% of Coverage A can be increased to 40% 20% of Coverage C 40% of Coverage C

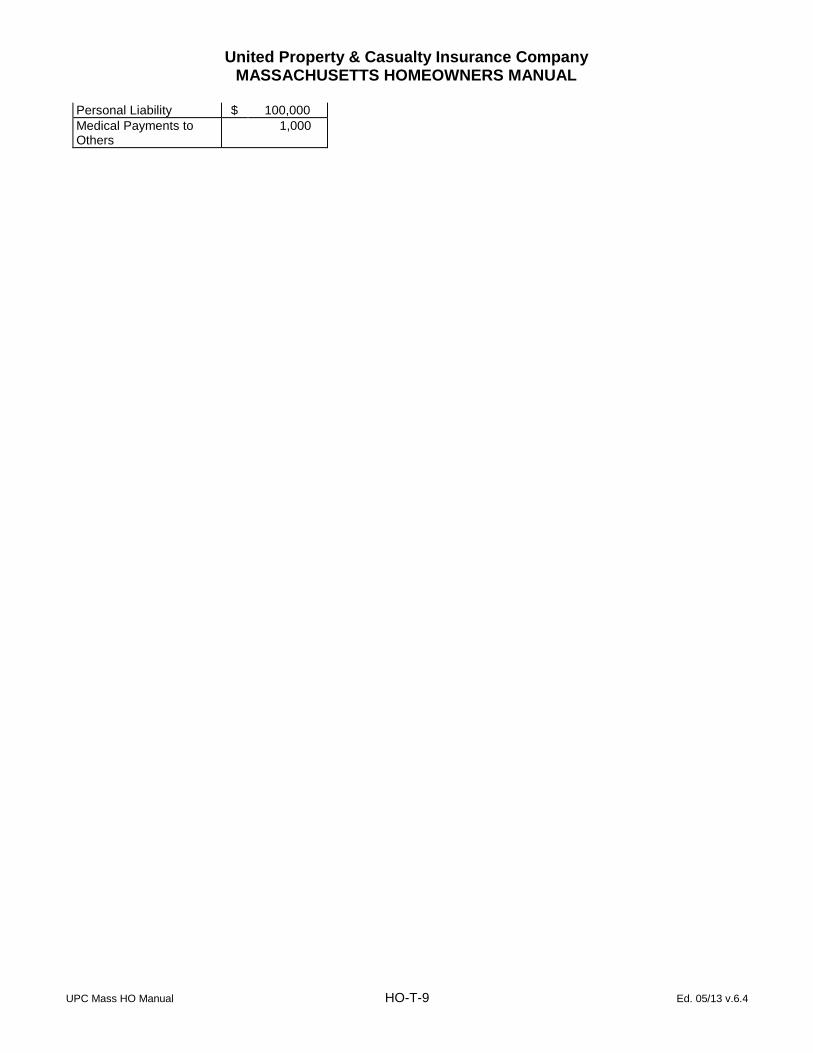

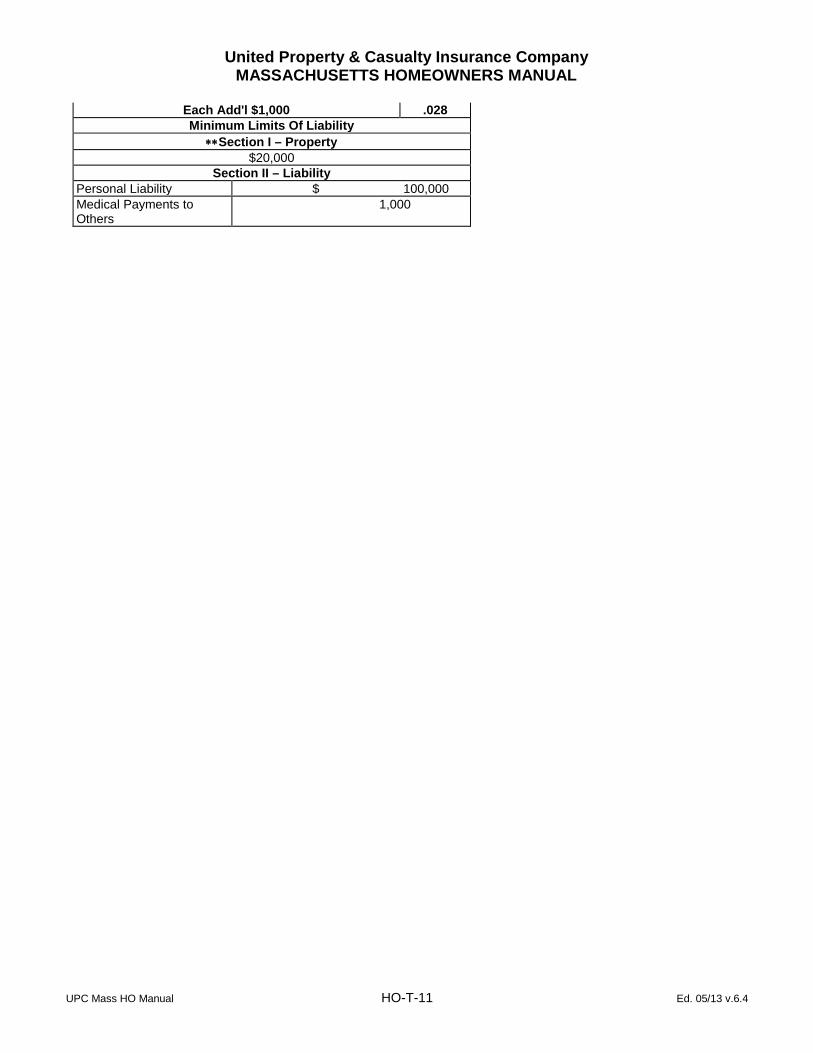

* Higher Coverage A Limits must be referred to Company Section II Liability Coverages E – Personal Liability* $100,000 Minimum; $300,000 or $500,000 Options

F – Medical Payments* $1,000 Minimum; $2,000, $3,000, $4,000, or $5,000 Options • Coverage E limits apply on a “per occurrence” basis; Coverage F limits apply on an “each person” basis.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-2-1 Ed. 05/13 v.6.4

2. General Underwriting Requirements

A. Dwellings must be insured to 100% of replacement cost. B. Dwellings must be protected by smoke detectors in good working order located close to the kitchen and

all sleeping areas.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-3-1 Ed. 05/13 v.6.4

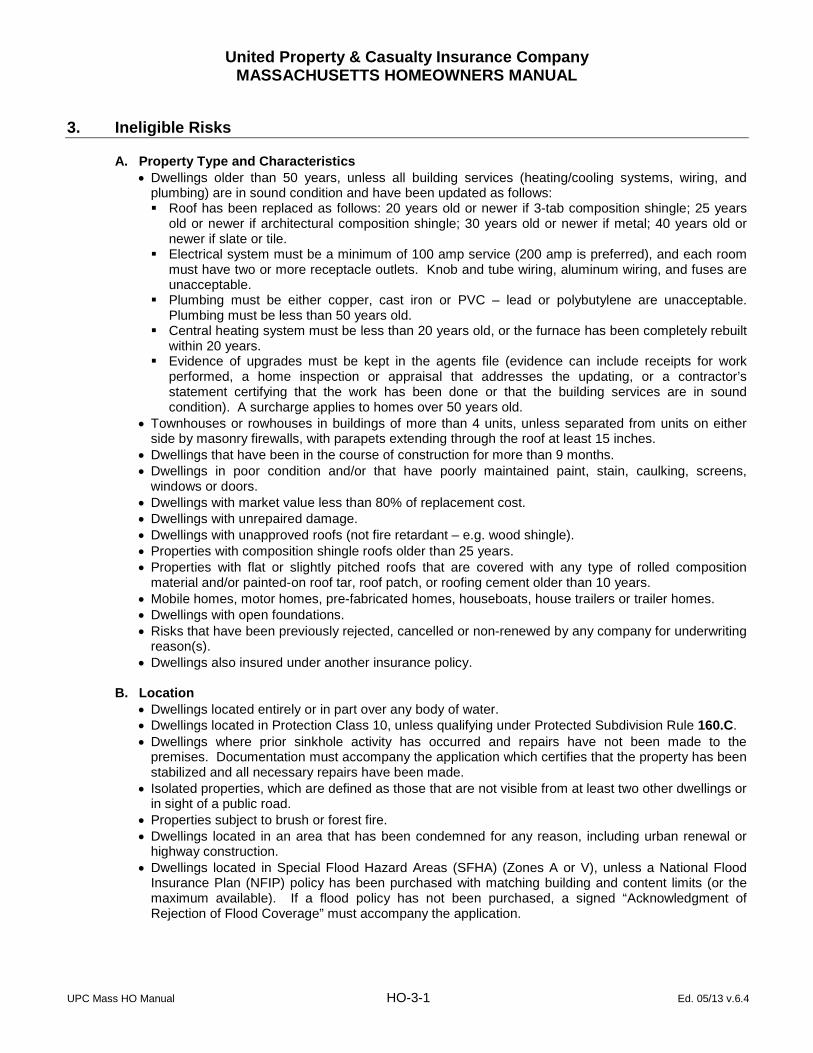

3. Ineligible Risks

A. Property Type and Characteristics

• Dwellings older than 50 years, unless all building services (heating/cooling systems, wiring, and plumbing) are in sound condition and have been updated as follows: Roof has been replaced as follows: 20 years old or newer if 3-tab composition shingle; 25 years

old or newer if architectural composition shingle; 30 years old or newer if metal; 40 years old or newer if slate or tile.

Electrical system must be a minimum of 100 amp service (200 amp is preferred), and each room must have two or more receptacle outlets. Knob and tube wiring, aluminum wiring, and fuses are unacceptable.

Plumbing must be either copper, cast iron or PVC – lead or polybutylene are unacceptable. Plumbing must be less than 50 years old.

Central heating system must be less than 20 years old, or the furnace has been completely rebuilt within 20 years.

Evidence of upgrades must be kept in the agents file (evidence can include receipts for work performed, a home inspection or appraisal that addresses the updating, or a contractor’s statement certifying that the work has been done or that the building services are in sound condition). A surcharge applies to homes over 50 years old.

• Townhouses or rowhouses in buildings of more than 4 units, unless separated from units on either side by masonry firewalls, with parapets extending through the roof at least 15 inches.

• Dwellings that have been in the course of construction for more than 9 months. • Dwellings in poor condition and/or that have poorly maintained paint, stain, caulking, screens,

windows or doors. • Dwellings with market value less than 80% of replacement cost. • Dwellings with unrepaired damage. • Dwellings with unapproved roofs (not fire retardant – e.g. wood shingle). • Properties with composition shingle roofs older than 25 years. • Properties with flat or slightly pitched roofs that are covered with any type of rolled composition

material and/or painted-on roof tar, roof patch, or roofing cement older than 10 years. • Mobile homes, motor homes, pre-fabricated homes, houseboats, house trailers or trailer homes. • Dwellings with open foundations. • Risks that have been previously rejected, cancelled or non-renewed by any company for underwriting

reason(s). • Dwellings also insured under another insurance policy.

B. Location • Dwellings located entirely or in part over any body of water. • Dwellings located in Protection Class 10, unless qualifying under Protected Subdivision Rule 160.C. • Dwellings where prior sinkhole activity has occurred and repairs have not been made to the

premises. Documentation must accompany the application which certifies that the property has been stabilized and all necessary repairs have been made.

• Isolated properties, which are defined as those that are not visible from at least two other dwellings or in sight of a public road.

• Properties subject to brush or forest fire. • Dwellings located in an area that has been condemned for any reason, including urban renewal or

highway construction. • Dwellings located in Special Flood Hazard Areas (SFHA) (Zones A or V), unless a National Flood

Insurance Plan (NFIP) policy has been purchased with matching building and content limits (or the maximum available). If a flood policy has not been purchased, a signed “Acknowledgment of Rejection of Flood Coverage” must accompany the application.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-3-2 Ed. 05/13 v.6.4

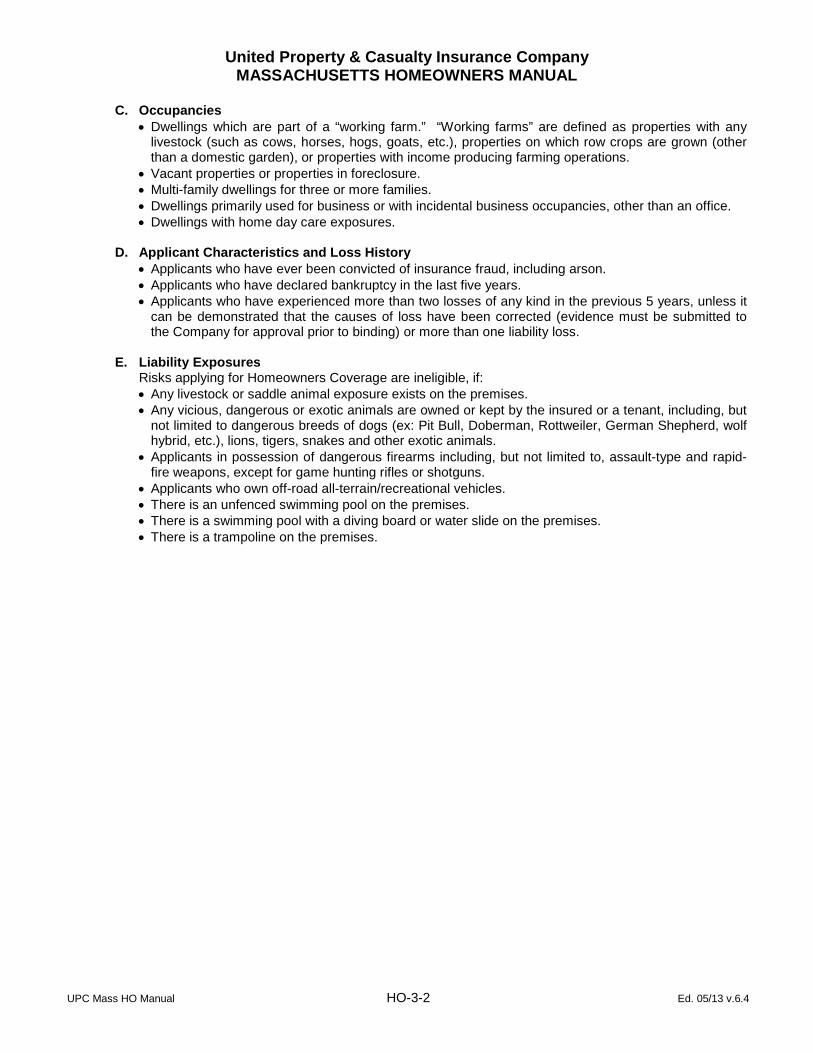

C. Occupancies • Dwellings which are part of a “working farm.” “Working farms” are defined as properties with any

livestock (such as cows, horses, hogs, goats, etc.), properties on which row crops are grown (other than a domestic garden), or properties with income producing farming operations.

• Vacant properties or properties in foreclosure. • Multi-family dwellings for three or more families. • Dwellings primarily used for business or with incidental business occupancies, other than an office. • Dwellings with home day care exposures.

D. Applicant Characteristics and Loss History

• Applicants who have ever been convicted of insurance fraud, including arson. • Applicants who have declared bankruptcy in the last five years. • Applicants who have experienced more than two losses of any kind in the previous 5 years, unless it

can be demonstrated that the causes of loss have been corrected (evidence must be submitted to the Company for approval prior to binding) or more than one liability loss.

E. Liability Exposures

Risks applying for Homeowners Coverage are ineligible, if: • Any livestock or saddle animal exposure exists on the premises. • Any vicious, dangerous or exotic animals are owned or kept by the insured or a tenant, including, but

not limited to dangerous breeds of dogs (ex: Pit Bull, Doberman, Rottweiler, German Shepherd, wolf hybrid, etc.), lions, tigers, snakes and other exotic animals.

• Applicants in possession of dangerous firearms including, but not limited to, assault-type and rapid-fire weapons, except for game hunting rifles or shotguns.

• Applicants who own off-road all-terrain/recreational vehicles. • There is an unfenced swimming pool on the premises. • There is a swimming pool with a diving board or water slide on the premises. • There is a trampoline on the premises.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-4-1 Ed. 05/13 v.6.4

4. Binding Authority

Agents have the authority to bind coverage on any risk that is not identified as “ineligible” in the Ineligible Risks section of this underwriting guide. Agent’s authority is for the limits stated and the forms of coverage outlined in the various sections of this guide. Any exceptions must be referred to the Company for approval prior to binding. Agent’s binding authority for new business, or for increases in coverage on existing business is suspended immediately when the National Hurricane Center (NHC) of the National Weather Service has issued a Tropical Storm Watch, Tropical Storm Warning, Hurricane Watch, or Hurricane Warning for any coastal area of New England. Renewals will only be issued on an “as expiring” basis for coverage and perils; limits will only be increased to keep pace with established inflation factors. The Company will restore binding authority as soon as the NHC lifts the storm designation for all affected New England coastal areas. If any exceptional circumstances exist which warrant the Company giving consideration to acceptance of additional liability, the line must be submitted to the Company’s Underwriting Department for approval. An example is when coverage is required in order to close on the purchase of a home – in this situation, the agent must contact the Company for approval, and proof of the real estate closing must accompany the application along with the appropriate payment.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-5-1 Ed. 05/13 v.6.4

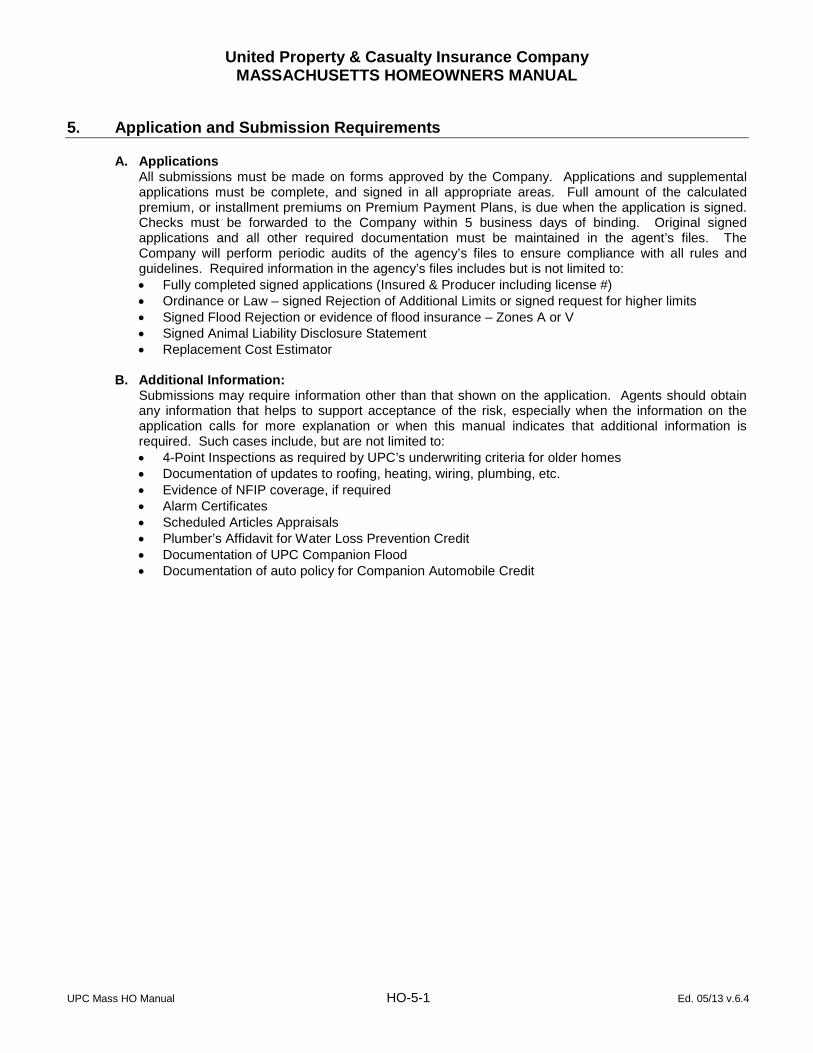

5. Application and Submission Requirements

A. Applications All submissions must be made on forms approved by the Company. Applications and supplemental applications must be complete, and signed in all appropriate areas. Full amount of the calculated premium, or installment premiums on Premium Payment Plans, is due when the application is signed. Checks must be forwarded to the Company within 5 business days of binding. Original signed applications and all other required documentation must be maintained in the agent’s files. The Company will perform periodic audits of the agency’s files to ensure compliance with all rules and guidelines. Required information in the agency’s files includes but is not limited to: • Fully completed signed applications (Insured & Producer including license #) • Ordinance or Law – signed Rejection of Additional Limits or signed request for higher limits • Signed Flood Rejection or evidence of flood insurance – Zones A or V • Signed Animal Liability Disclosure Statement • Replacement Cost Estimator

B. Additional Information: Submissions may require information other than that shown on the application. Agents should obtain any information that helps to support acceptance of the risk, especially when the information on the application calls for more explanation or when this manual indicates that additional information is required. Such cases include, but are not limited to: • 4-Point Inspections as required by UPC’s underwriting criteria for older homes • Documentation of updates to roofing, heating, wiring, plumbing, etc. • Evidence of NFIP coverage, if required • Alarm Certificates • Scheduled Articles Appraisals • Plumber’s Affidavit for Water Loss Prevention Credit • Documentation of UPC Companion Flood • Documentation of auto policy for Companion Automobile Credit

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-6-1 Ed. 05/13 v.6.4

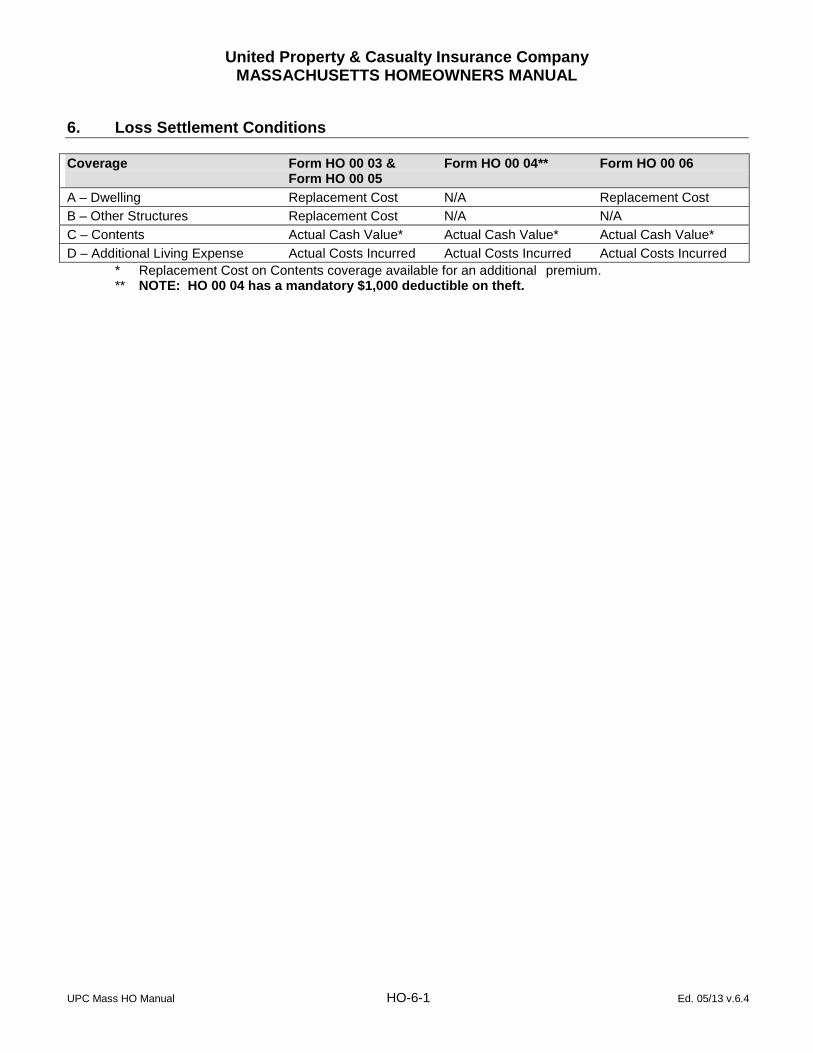

6. Loss Settlement Conditions Coverage Form HO 00 03 & Form HO 00 04** Form HO 00 06 Form HO 00 05 A – Dwelling Replacement Cost N/A Replacement Cost B – Other Structures Replacement Cost N/A N/A C – Contents Actual Cash Value* Actual Cash Value* Actual Cash Value* D – Additional Living Expense Actual Costs Incurred Actual Costs Incurred Actual Costs Incurred

* Replacement Cost on Contents coverage available for an additional premium. ** NOTE: HO 00 04 has a mandatory $1,000 deductible on theft.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-7-1 Ed. 05/13 v.6.4

7. Payment Plans (see Rule 170. for details)

• 1 Pay Plan: Full payment at inception. • 2 Pay Plan: 50%/50%, plus a $5 service charge with each installment. • 3 Pay Plan: 40%/30%/30%, plus a $5 service charge with each installment. • 4 Pay Plan: 25%/25%/25%/25%, plus a $5 service charge with each installment. • 11 Pay Play: 11 equal monthly installments, automatically deducted from insured’s bank account, plus

a $2 service charge with each installment.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-8-1 Ed. 05/13 v.6.4

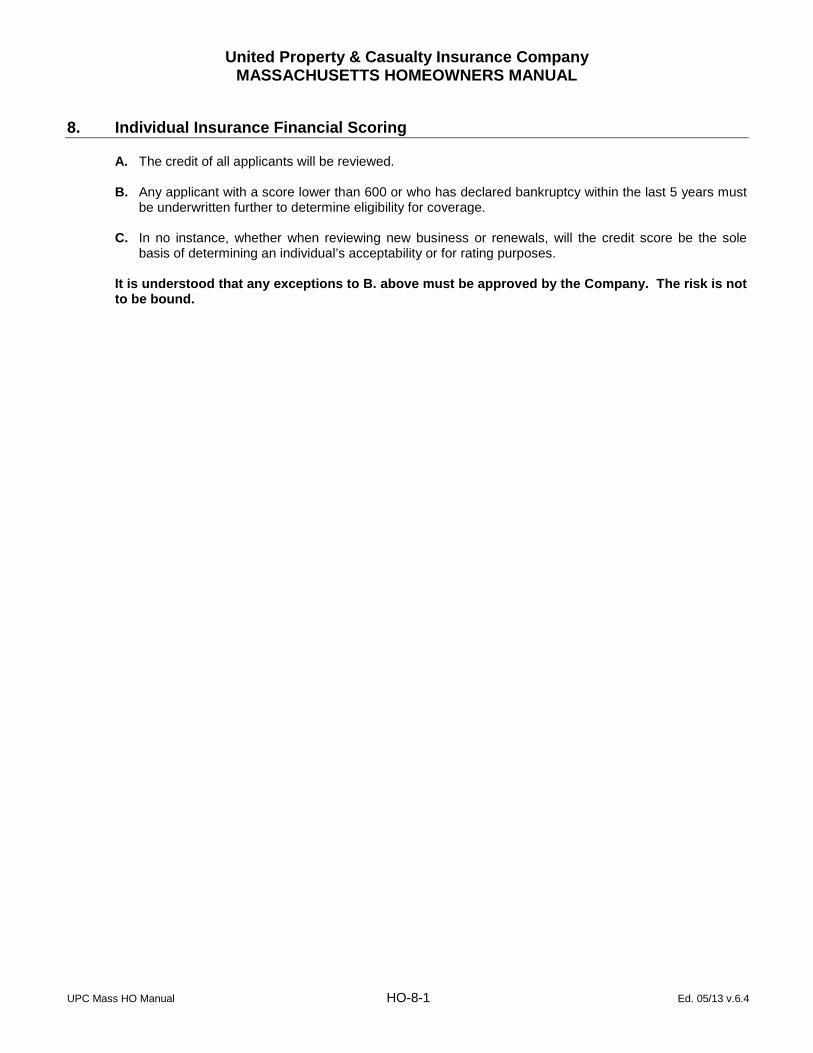

8. Individual Insurance Financial Scoring

A. The credit of all applicants will be reviewed. B. Any applicant with a score lower than 600 or who has declared bankruptcy within the last 5 years must

be underwritten further to determine eligibility for coverage.

C. In no instance, whether when reviewing new business or renewals, will the credit score be the sole basis of determining an individual’s acceptability or for rating purposes.

It is understood that any exceptions to B. above must be approved by the Company. The risk is not to be bound.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-9-1 Ed. 05/13 v.6.4

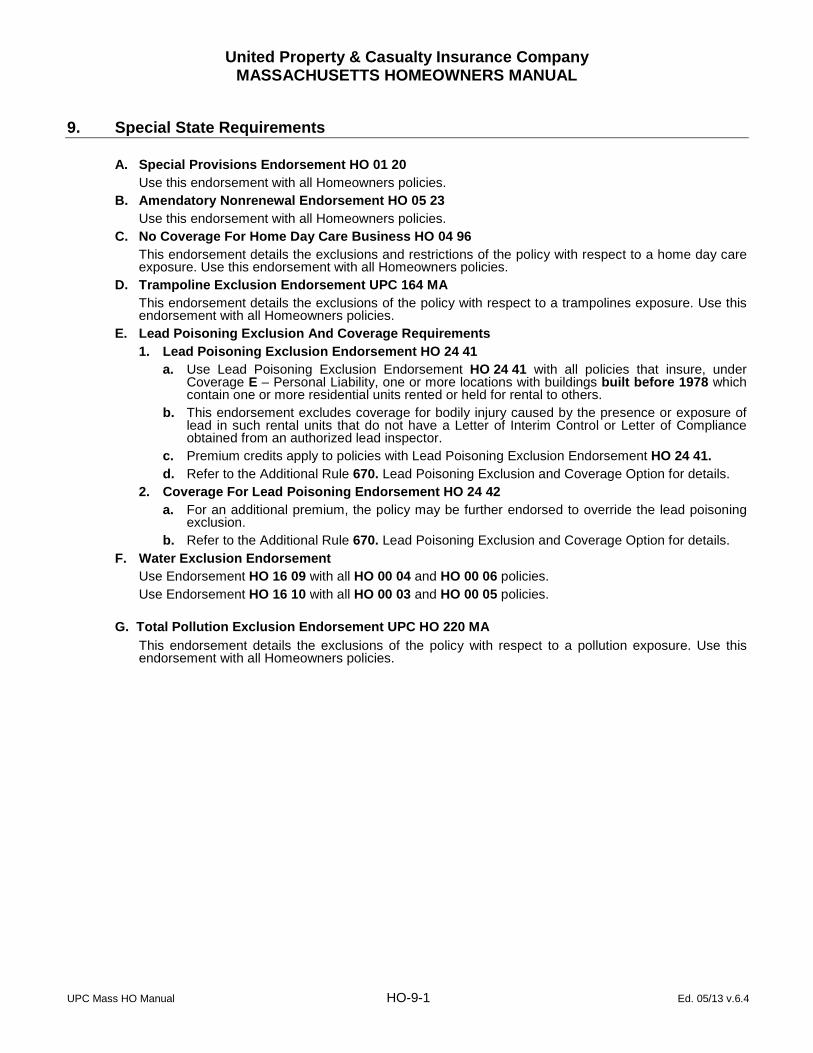

9. Special State Requirements A. Special Provisions Endorsement HO 01 20

Use this endorsement with all Homeowners policies. B. Amendatory Nonrenewal Endorsement HO 05 23

Use this endorsement with all Homeowners policies. C. No Coverage For Home Day Care Business HO 04 96

This endorsement details the exclusions and restrictions of the policy with respect to a home day care exposure. Use this endorsement with all Homeowners policies.

D. Trampoline Exclusion Endorsement UPC 164 MA This endorsement details the exclusions of the policy with respect to a trampolines exposure. Use this endorsement with all Homeowners policies.

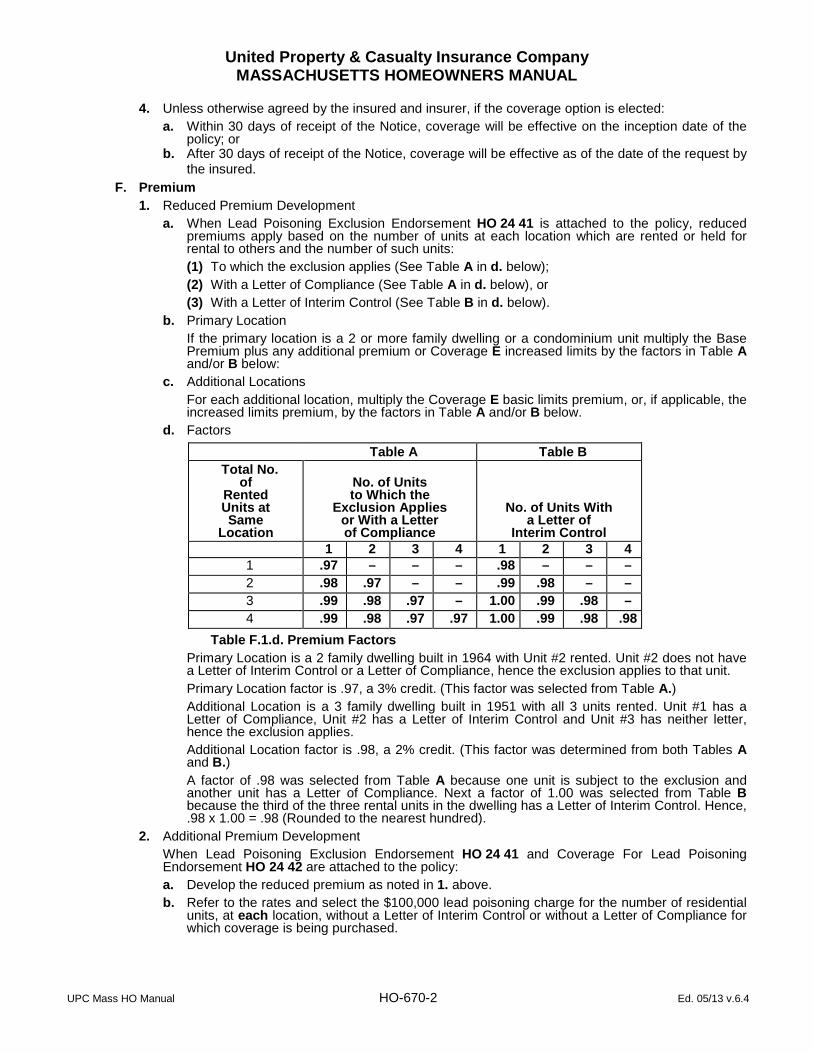

E. Lead Poisoning Exclusion And Coverage Requirements 1. Lead Poisoning Exclusion Endorsement HO 24 41 a. Use Lead Poisoning Exclusion Endorsement HO 24 41 with all policies that insure, under

Coverage E – Personal Liability, one or more locations with buildings built before 1978 which contain one or more residential units rented or held for rental to others.

b. This endorsement excludes coverage for bodily injury caused by the presence or exposure of lead in such rental units that do not have a Letter of Interim Control or Letter of Compliance obtained from an authorized lead inspector.

c. Premium credits apply to policies with Lead Poisoning Exclusion Endorsement HO 24 41. d. Refer to the Additional Rule 670. Lead Poisoning Exclusion and Coverage Option for details. 2. Coverage For Lead Poisoning Endorsement HO 24 42 a. For an additional premium, the policy may be further endorsed to override the lead poisoning

exclusion. b. Refer to the Additional Rule 670. Lead Poisoning Exclusion and Coverage Option for details.

F. Water Exclusion Endorsement Use Endorsement HO 16 09 with all HO 00 04 and HO 00 06 policies. Use Endorsement HO 16 10 with all HO 00 03 and HO 00 05 policies.

G. Total Pollution Exclusion Endorsement UPC HO 220 MA This endorsement details the exclusions of the policy with respect to a pollution exposure. Use this endorsement with all Homeowners policies.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-100-1 Ed. 05/13 v.6.4

GENERAL RULES

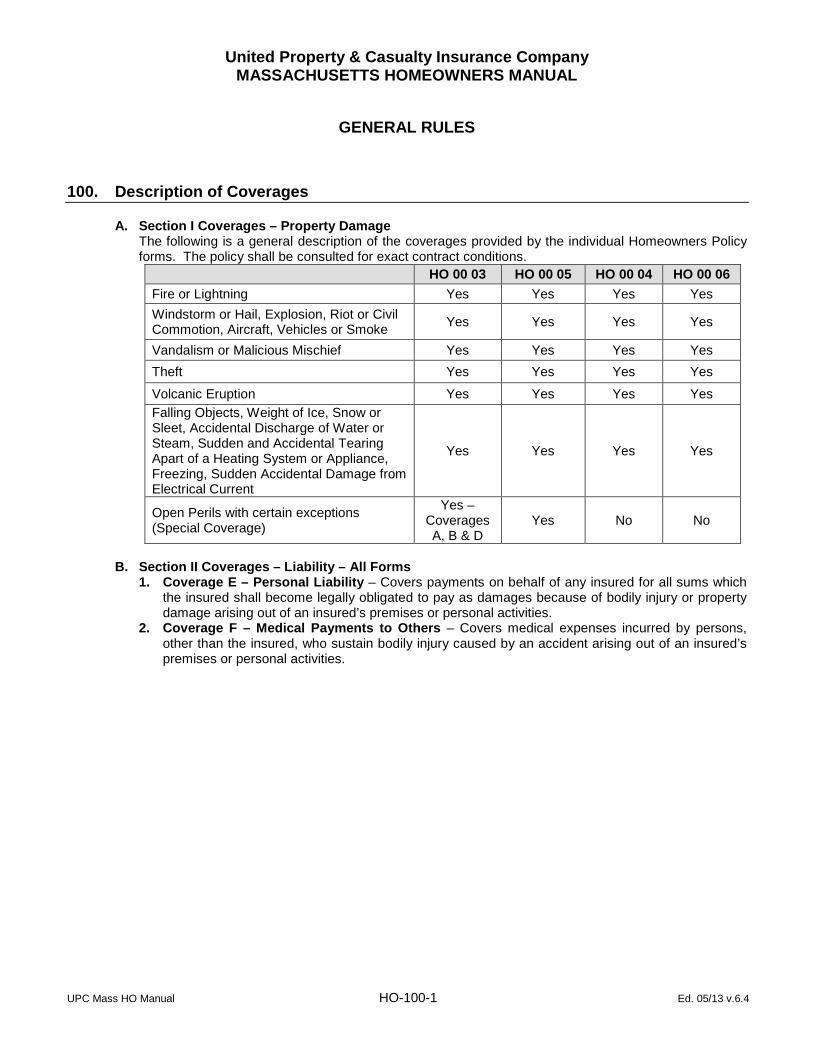

100. Description of Coverages

A. Section I Coverages – Property Damage

The following is a general description of the coverages provided by the individual Homeowners Policy forms. The policy shall be consulted for exact contract conditions.

HO 00 03 HO 00 05 HO 00 04 HO 00 06 Fire or Lightning Yes Yes Yes Yes Windstorm or Hail, Explosion, Riot or Civil Commotion, Aircraft, Vehicles or Smoke Yes Yes Yes Yes

Vandalism or Malicious Mischief Yes Yes Yes Yes Theft Yes Yes Yes Yes

Volcanic Eruption Yes Yes Yes Yes Falling Objects, Weight of Ice, Snow or Sleet, Accidental Discharge of Water or Steam, Sudden and Accidental Tearing Apart of a Heating System or Appliance, Freezing, Sudden Accidental Damage from Electrical Current

Yes Yes Yes Yes

Open Perils with certain exceptions (Special Coverage)

Yes – Coverages A, B & D

Yes No No

B. Section II Coverages – Liability – All Forms

1. Coverage E – Personal Liability – Covers payments on behalf of any insured for all sums which the insured shall become legally obligated to pay as damages because of bodily injury or property damage arising out of an insured’s premises or personal activities.

2. Coverage F – Medical Payments to Others – Covers medical expenses incurred by persons, other than the insured, who sustain bodily injury caused by an accident arising out of an insured’s premises or personal activities.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-110-1 Ed. 05/13 v.6.4

110. Mandatory Coverages

It is mandatory that insurance be written for all coverages provided under both Section I and II of the Homeowners Policy.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-120-1 Ed. 05/13 v.6.4

120. Eligibility

A. Forms HO 00 03 and HO 00 05 – a Homeowners Policy may be issued:

1. To the owner-occupant(s) of a dwelling which is used exclusively for private residential purposes (except as provided in Rule 120.F.) and contains not more than 2 families; or

2. To the purchaser-occupant(s) who has entered into a long term installment contract for the purchase of the dwelling and who occupies the dwelling but to whom title does not pass from the seller until all the terms of the installment contract have been satisfied. The seller retains title until completion of the payments and in no way acts as a mortgagee. The seller’s interest in the building and premises liability may be covered using Endorsement HO 04 41 – Additional Insured; or

3. To the occupant of a dwelling under a life estate arrangement when the Coverage A amount is at least 80% of the dwelling’s replacement cost. The owner’s interest in the building and premises liability may be covered using Endorsement HO 04 41 – Additional Insured; or

4. To cover dwellings in the course of construction provided the policy is issued only in the name of the intended owner-occupant(s) of the dwelling.

5. It is permissible to extend the Homeowners Policy, without additional premium charge, to cover the interest of a non-occupant joint owner in the building and for premises liability. Use Endorsement HO 04 41 – Additional Insured.

B. Form HO 00 04 – a Homeowners Policy may be issued to:

1. The tenant(s) (non-owner) of a dwelling or an apartment situated in any building; or 2. The owner-occupant(s) of a dwelling, cooperative unit or of a building containing an apartment not otherwise eligible for a Homeowners Policy under Rule 120.A. above; provided the residence premises occupied by the insured is used exclusively for residential purposes (except as provided in Rule 120.F.), and is not occupied by more than one additional family or more than two boarders or roomers.

C. Form HO 00 06 – a Homeowners Policy may be issued to: The owner(s) of a condominium or cooperative unit which is used exclusively for residential purposes (except as provided in Rule 120.F.).

D. Subject to all other sections of this rule, a Homeowners Policy may be issued to cover a seasonal

dwelling. (See Rule 140). E. A Homeowners Policy shall not be issued to cover any mobile home, trailer home, or housetrailer.

F. Certain business occupancies are permitted, provided:

1. The premises is occupied principally for private residential purposes; and 2. There is no other business occupancy on the premises. When the business is conducted on the residence premises, refer to Rule 550 for Section I Coverage and Rule 820 for Section II Coverage. When the business is not conducted from the residence premises, this coverage is not available.

G. All policies are issued with the mandatory HO 04 96 – No Section II – Liability Coverages for Home Day Care Business endorsement. No policy shall be issued for an occupancy where child care is provided to unrelated individuals for compensation, unless all of the following criteria are met: 1. A current copy of a Certificate of Insurance from the insurer providing Commercial Liability

coverage at limits equal to or greater than the Company Personal Liability limits is provided to the Company.

2. A current copy of the current Child Care License for the covered premises issued by the appropriate governmental entity of jurisdiction is provided to the Company prior to issuance or renewal of each policy period.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-130-1 Ed. 05/13 v.6.4

130. Secondary Residence Premises

Homeowners Coverage on a secondary residence premises must be provided under a separate policy.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-140-1 Ed. 05/13 v.6.4

140. Seasonal Dwellings

A seasonal dwelling is a dwelling with continuous unoccupancy for extended periods of time. Any property that falls into this category must be protected in at least one of the following ways in order to qualify for coverage under the homeowners program: 1. Central station fire and burglar alarm system completely protecting the dwelling, or

2. Dwelling is located in a gated community, or

3. Dwelling is located in a multi-unit building protected by a security guard and/or with controlled access, or

4. Dwelling is actively managed by a property management firm who checks on the property on a regular (at least weekly) basis.

If the dwelling is unoccupied during the late fall, winter and early spring months, in addition to the above one of the following forms of protection is also required: A. The water must be turned off at the point of service; pipes, sinks, toilets, traps, and appliances (i.e.

dishwashers, refrigerators, washing machines, etc.) must be drained and winterized by a licensed plumber (copy of plumber’s work order is required to be obtained for the file). If the heat is left on at 50 degrees, the winterization does not need to be done by a plumber.

B. An automatic water shut-off alarm system must be present – this system must have been installed by a licensed plumber and a copy of the plumber’s work order or invoice must be obtained.

C. A freeze alarm must be present. The freeze alarm must be programmed to automatically dial a telephone number when the temperature inside the dwelling drops below a pre-set range. The freeze alarm must:

1. Send a warning call to the pre-programmed telephone number within 30 minutes of the temperature in the dwelling dropping below 40 degrees Fahrenheit.

2. Plug into an existing telephone line. 3. Allow the status of the alarm to be checked remotely. 4. Contain a battery back-up to continue operation during power outages.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-150-1 Ed. 05/13 v.6.4

150. Policy Period

A policy may be written for a period of one year and may be extended for successive policy periods by extension certificate or renewal policy based upon the forms, premiums and endorsements then in effect for the Company.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-160-1 Ed. 05/13 v.6.4

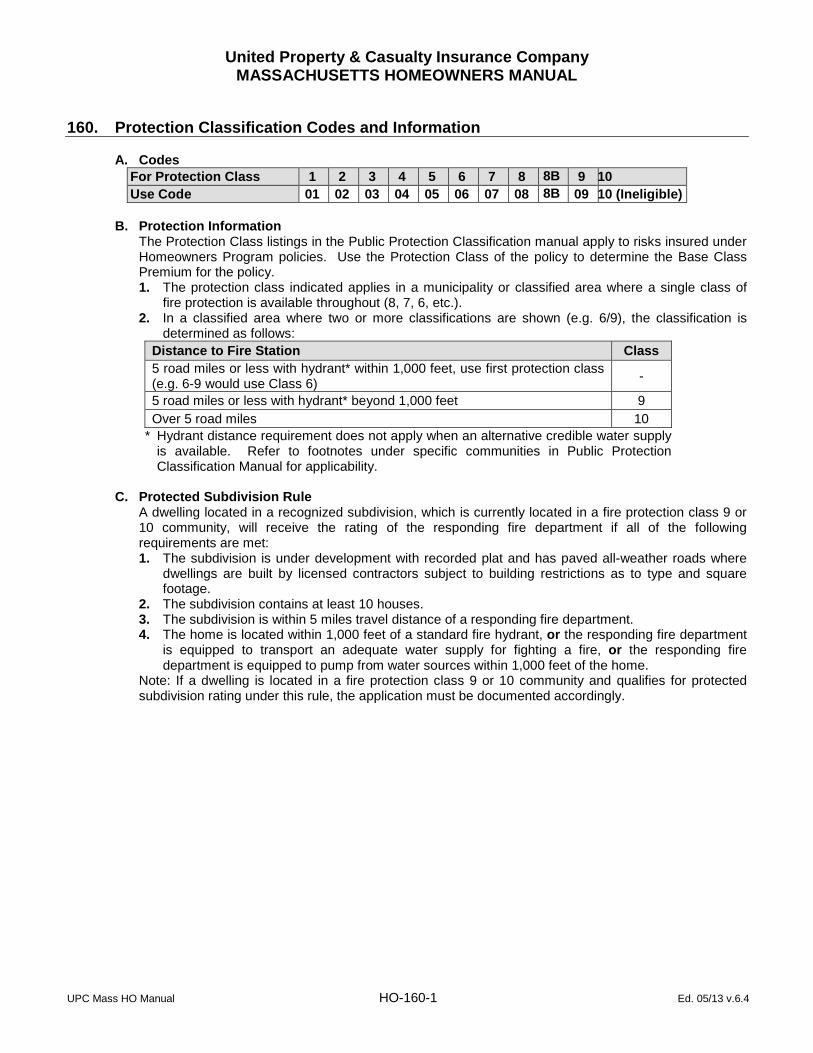

160. Protection Classification Codes and Information

A. Codes

For Protection Class 1 2 3 4 5 6 7 8 8B 9 10 Use Code 01 02 03 04 05 06 07 08 8B 09 10 (Ineligible)

B. Protection Information

The Protection Class listings in the Public Protection Classification manual apply to risks insured under Homeowners Program policies. Use the Protection Class of the policy to determine the Base Class Premium for the policy. 1. The protection class indicated applies in a municipality or classified area where a single class of

fire protection is available throughout (8, 7, 6, etc.). 2. In a classified area where two or more classifications are shown (e.g. 6/9), the classification is

determined as follows: Distance to Fire Station Class 5 road miles or less with hydrant* within 1,000 feet, use first protection class (e.g. 6-9 would use Class 6) -

5 road miles or less with hydrant* beyond 1,000 feet 9 Over 5 road miles 10

* Hydrant distance requirement does not apply when an alternative credible water supply is available. Refer to footnotes under specific communities in Public Protection Classification Manual for applicability.

C. Protected Subdivision Rule

A dwelling located in a recognized subdivision, which is currently located in a fire protection class 9 or 10 community, will receive the rating of the responding fire department if all of the following requirements are met: 1. The subdivision is under development with recorded plat and has paved all-weather roads where

dwellings are built by licensed contractors subject to building restrictions as to type and square footage.

2. The subdivision contains at least 10 houses. 3. The subdivision is within 5 miles travel distance of a responding fire department. 4. The home is located within 1,000 feet of a standard fire hydrant, or the responding fire department

is equipped to transport an adequate water supply for fighting a fire, or the responding fire department is equipped to pump from water sources within 1,000 feet of the home.

Note: If a dwelling is located in a fire protection class 9 or 10 community and qualifies for protected subdivision rating under this rule, the application must be documented accordingly.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-170-1 Ed. 05/13 v.6.4

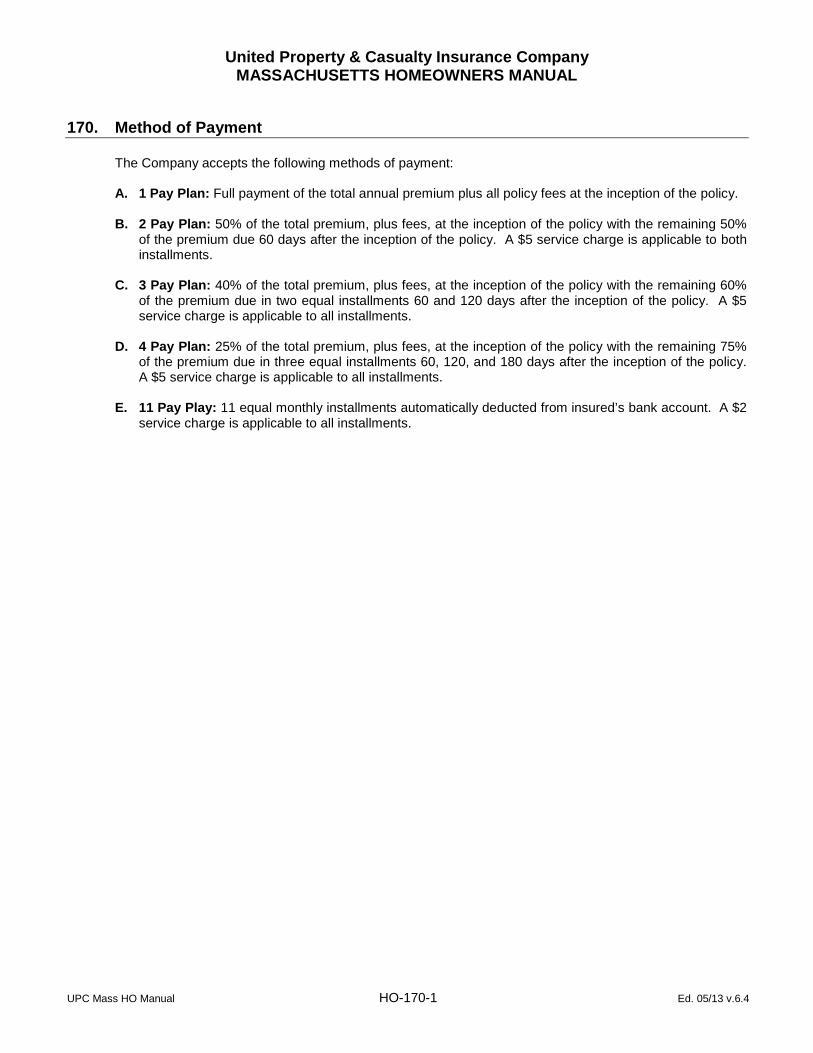

170. Method of Payment

The Company accepts the following methods of payment: A. 1 Pay Plan: Full payment of the total annual premium plus all policy fees at the inception of the policy. B. 2 Pay Plan: 50% of the total premium, plus fees, at the inception of the policy with the remaining 50%

of the premium due 60 days after the inception of the policy. A $5 service charge is applicable to both installments.

C. 3 Pay Plan: 40% of the total premium, plus fees, at the inception of the policy with the remaining 60%

of the premium due in two equal installments 60 and 120 days after the inception of the policy. A $5 service charge is applicable to all installments.

D. 4 Pay Plan: 25% of the total premium, plus fees, at the inception of the policy with the remaining 75%

of the premium due in three equal installments 60, 120, and 180 days after the inception of the policy. A $5 service charge is applicable to all installments.

E. 11 Pay Play: 11 equal monthly installments automatically deducted from insured’s bank account. A $2

service charge is applicable to all installments.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-180-1 Ed. 05/13 v.6.4

180. Changes or Cancellations

A. It is not permissible to cancel any of the mandatory coverages in the policy unless the entire policy is

cancelled. B. If insurance is increased, cancelled or reduced, the additional or return premium shall be calculated on

a pro rata basis, subject to the minimum premium requirement.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-190-1 Ed. 05/13 v.6.4

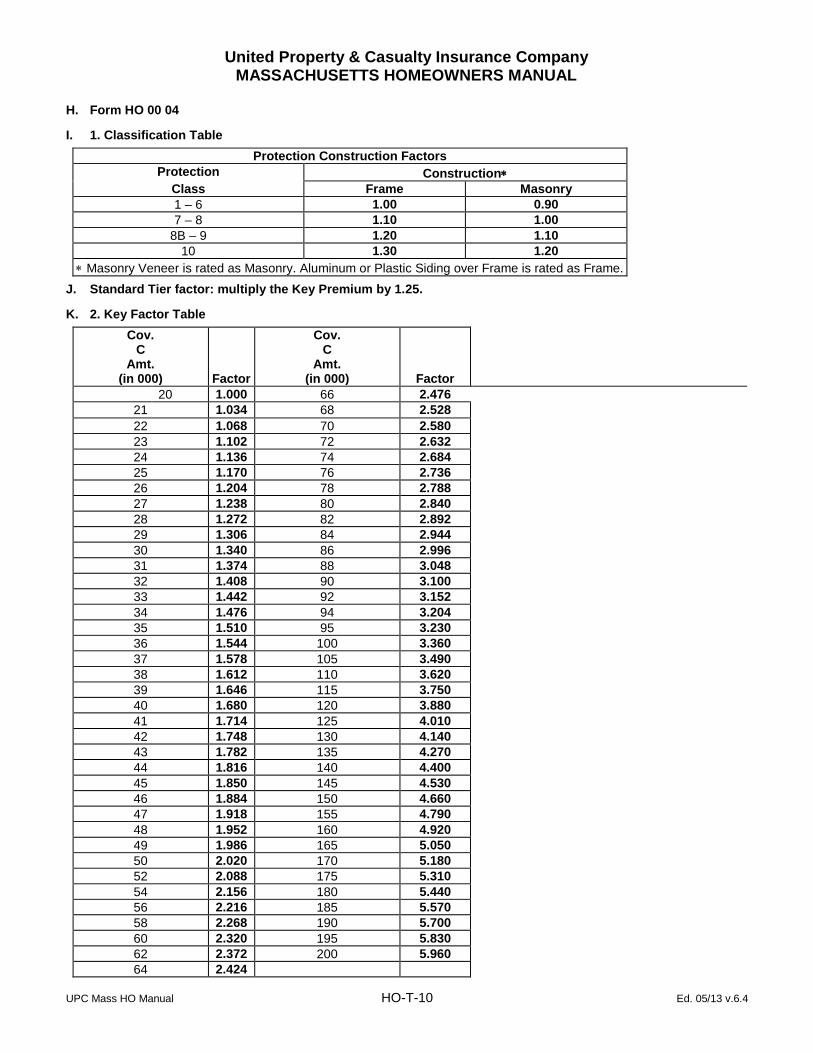

190. Construction Definitions

A. Frame – Exterior walls of wood or other combustible construction, including iron-clad wood, stucco on

wood, plaster on combustible supports, or aluminum or plastic siding over frame. B. Masonry Veneer – Exterior walls of wood or other combustible construction on combustible supports,

veneered with brick or stone. C. Masonry – Exterior walls constructed of masonry materials such as adobe, brick, concrete, gypsum

block, hollow concrete block, stone, tile or similar materials and floors and roof of combustible construction (disregarding floors resting directly on the ground).

D. Superior (see Rule 315 for rating information)

1. Non-Combustible – Exterior walls, floors and roof constructed of, and supported by, metal, asbestos, gypsum, or other non-combustible materials.

2. Masonry Non-Combustible – Exterior walls constructed of masonry materials (as described in B. above) and floors and roof of metal or other non-combustible materials.

3. Fire Resistive – Exterior walls, floors and roof constructed of masonry or other fire resistive materials.

Note: Mixed (Masonry/Frame) – a combination of both frame and masonry construction shall be classed and coded as frame when the exterior walls of frame construction (including gables) exceed 33 1/3% of the total exterior wall area; otherwise class as masonry.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-200-1 Ed. 05/13 v.6.4

200. Single Building Definition

A. All buildings or sections of buildings which are accessible through unprotected openings shall be

considered as a single building. B. Buildings which are separated by adequate clear space shall be considered separate buildings.

C. Buildings or sections of buildings which are separated by:

1. A 6-inch reinforced concrete or an 8-inch masonry party wall; or 2. A documented minimum two-hour non-combustible wall which has been laboratory tested for independent structural integrity under fire conditions which pierces the roof and extends above it for at least 15 inches, and which pierces or extends to the innerside of the exterior masonry wall shall be considered separate buildings. Access between buildings with independent walls or through masonry party walls described above shall be protected by at least a Class A Fire Door installed in a masonry wall section.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-210-1 Ed. 05/13 v.6.4

210. Minimum Premium

A. The minimum annual premium charged for each policy shall be $500 for HO3 & HO5 policies and

$300 for HO4 & HO6 policies. B. The minimum annual premium shall include all chargeable endorsements or coverages, if written at

inception of the policy.

C. Fees and surcharges are not included in the minimum annual premium, and are fully earned upon inception.

D. Assessments are not included in the minimum annual premium. Assessments are not fully earned – if

the policy is amended or cancelled, the additional or return premium, including assessments, shall be calculated on a pro rata basis.

E. The property inspection fee is not included in the minimum annual premium, and is fully earned upon

inception.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-220-1 Ed. 05/13 v.6.4

220. Manual Premium Revision

A manual premium revision shall be made in accordance with the following procedures: A. The effective date of such revision shall be as announced. B. The revision shall apply to any policy or endorsement in the manner outlined in the announcement of

the revision.

C. Unless otherwise provided at the time of the announcement of the premium revision, the revision shall not affect: 1. in-force policy forms, endorsements or premiums, until the policy is renewed; or 2. in the case of a Premium Payment Plan, in-force policy premiums, until the anniversary following

the effective date of the revision.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-230-1 Ed. 05/13 v.6.4

230. Transfer or Assignment

Transfer or assignment is not available. New applications are required.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-240-1 Ed. 05/13 v.6.4

240. Waiver of Premium

When a policy is endorsed after the inception date, the amount of additional or return premium that may be waived is $5.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-250-1 Ed. 05/13 v.6.4

250. Whole Dollar Premium Rule

Each premium shown on the policy and endorsements shall be rounded to the nearest whole dollar. A premium of fifty cents ($.50) or more shall be rounded to the next higher whole dollar. A premium of forty-nine cents ($.49) or less shall be rounded to the next lower whole dollar. In the event of cancellation by the Company, the return premium may be carried to the next higher whole dollar.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-300-1 Ed. 05/13 v.6.4

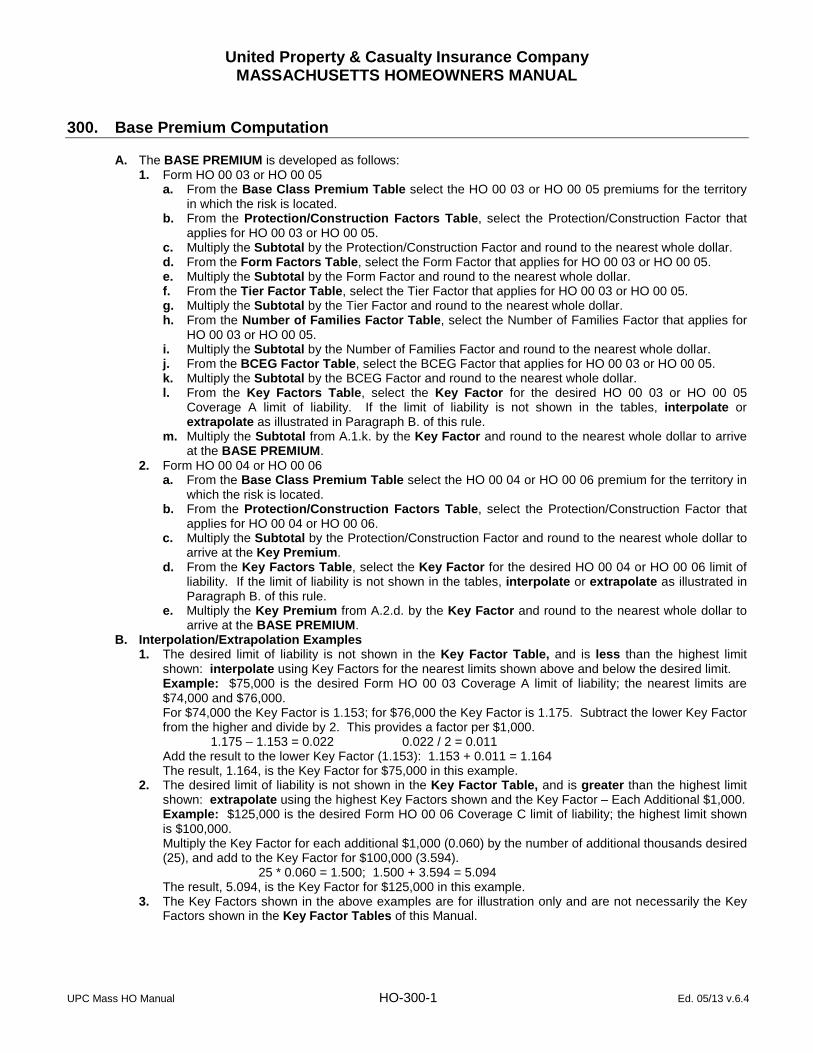

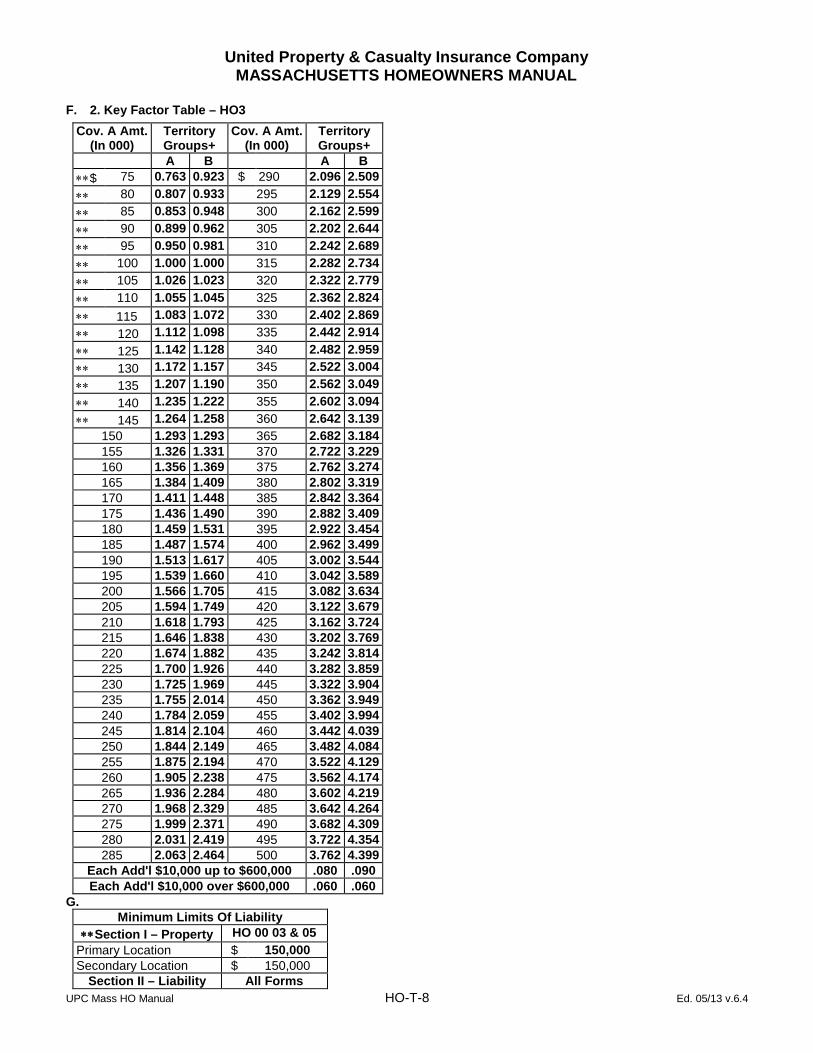

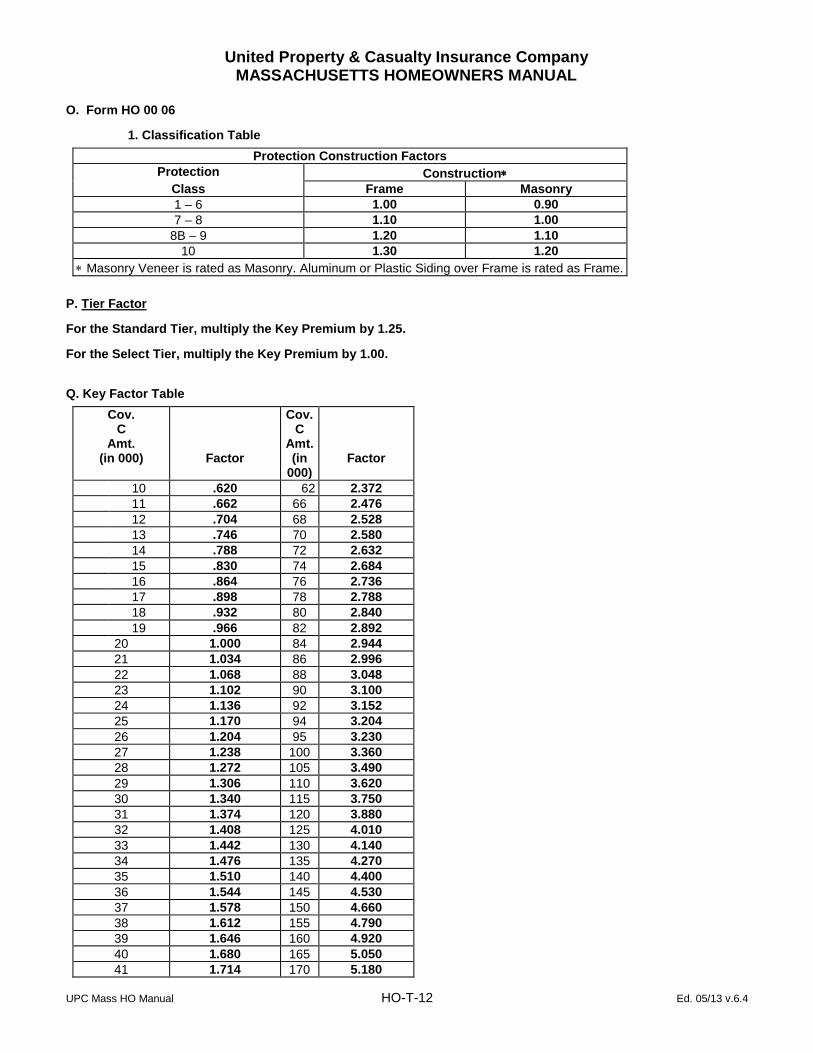

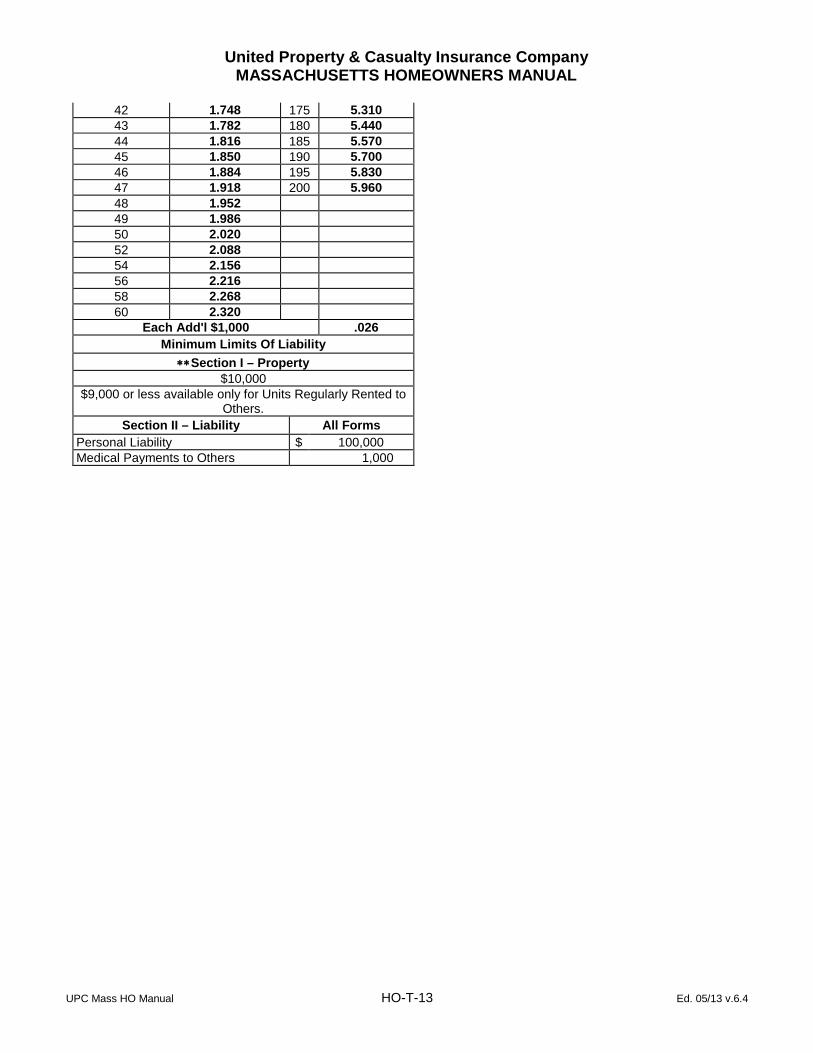

300. Base Premium Computation

A. The BASE PREMIUM is developed as follows:

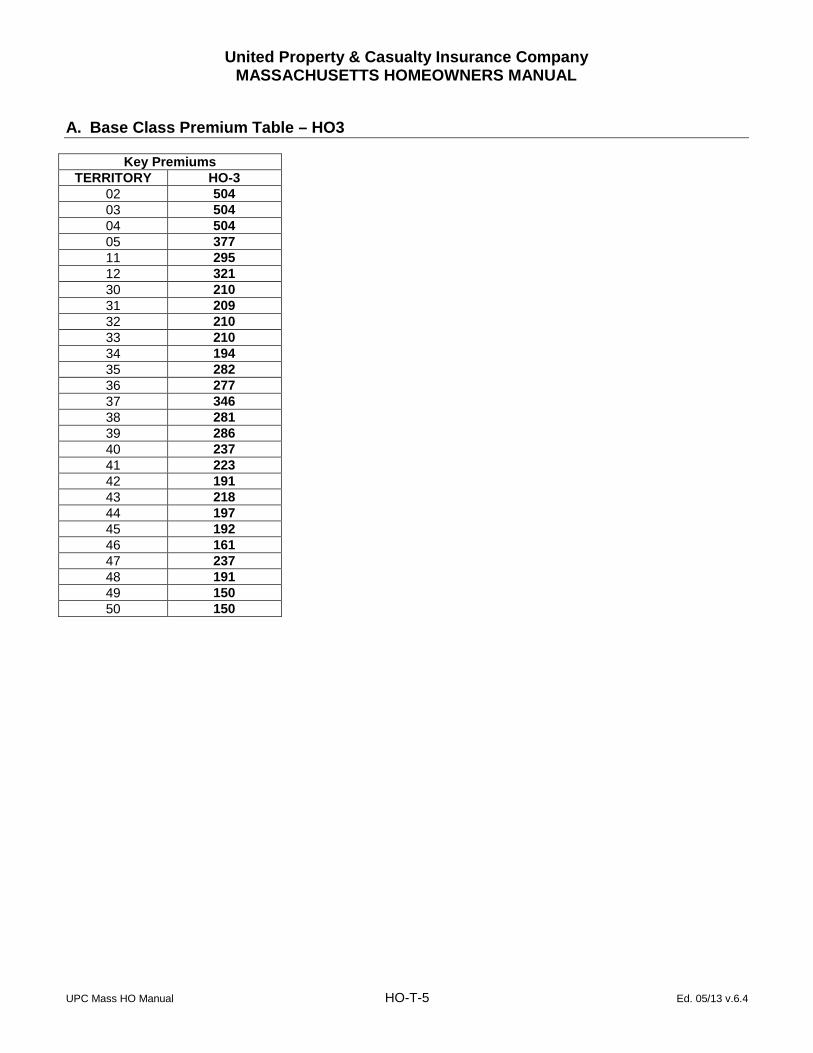

1. Form HO 00 03 or HO 00 05 a. From the Base Class Premium Table select the HO 00 03 or HO 00 05 premiums for the territory

in which the risk is located. b. From the Protection/Construction Factors Table, select the Protection/Construction Factor that

applies for HO 00 03 or HO 00 05. c. Multiply the Subtotal by the Protection/Construction Factor and round to the nearest whole dollar. d. From the Form Factors Table, select the Form Factor that applies for HO 00 03 or HO 00 05. e. Multiply the Subtotal by the Form Factor and round to the nearest whole dollar. f. From the Tier Factor Table, select the Tier Factor that applies for HO 00 03 or HO 00 05. g. Multiply the Subtotal by the Tier Factor and round to the nearest whole dollar. h. From the Number of Families Factor Table, select the Number of Families Factor that applies for

HO 00 03 or HO 00 05. i. Multiply the Subtotal by the Number of Families Factor and round to the nearest whole dollar. j. From the BCEG Factor Table, select the BCEG Factor that applies for HO 00 03 or HO 00 05. k. Multiply the Subtotal by the BCEG Factor and round to the nearest whole dollar. l. From the Key Factors Table, select the Key Factor for the desired HO 00 03 or HO 00 05

Coverage A limit of liability. If the limit of liability is not shown in the tables, interpolate or extrapolate as illustrated in Paragraph B. of this rule.

m. Multiply the Subtotal from A.1.k. by the Key Factor and round to the nearest whole dollar to arrive at the BASE PREMIUM.

2. Form HO 00 04 or HO 00 06 a. From the Base Class Premium Table select the HO 00 04 or HO 00 06 premium for the territory in

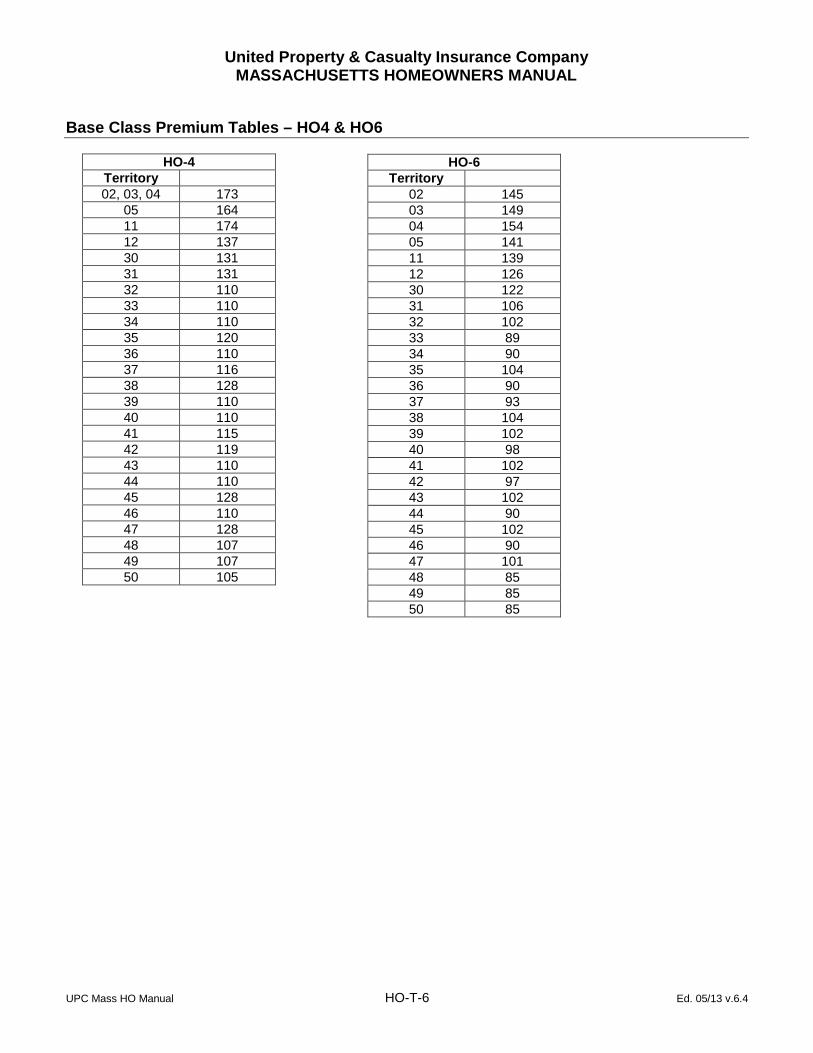

which the risk is located. b. From the Protection/Construction Factors Table, select the Protection/Construction Factor that

applies for HO 00 04 or HO 00 06. c. Multiply the Subtotal by the Protection/Construction Factor and round to the nearest whole dollar to

arrive at the Key Premium. d. From the Key Factors Table, select the Key Factor for the desired HO 00 04 or HO 00 06 limit of

liability. If the limit of liability is not shown in the tables, interpolate or extrapolate as illustrated in Paragraph B. of this rule.

e. Multiply the Key Premium from A.2.d. by the Key Factor and round to the nearest whole dollar to arrive at the BASE PREMIUM.

B. Interpolation/Extrapolation Examples 1. The desired limit of liability is not shown in the Key Factor Table, and is less than the highest limit

shown: interpolate using Key Factors for the nearest limits shown above and below the desired limit. Example: $75,000 is the desired Form HO 00 03 Coverage A limit of liability; the nearest limits are $74,000 and $76,000. For $74,000 the Key Factor is 1.153; for $76,000 the Key Factor is 1.175. Subtract the lower Key Factor from the higher and divide by 2. This provides a factor per $1,000.

1.175 – 1.153 = 0.022 0.022 / 2 = 0.011 Add the result to the lower Key Factor (1.153): 1.153 + 0.011 = 1.164 The result, 1.164, is the Key Factor for $75,000 in this example.

2. The desired limit of liability is not shown in the Key Factor Table, and is greater than the highest limit shown: extrapolate using the highest Key Factors shown and the Key Factor – Each Additional $1,000. Example: $125,000 is the desired Form HO 00 06 Coverage C limit of liability; the highest limit shown is $100,000. Multiply the Key Factor for each additional $1,000 (0.060) by the number of additional thousands desired (25), and add to the Key Factor for $100,000 (3.594). 25 * 0.060 = 1.500; 1.500 + 3.594 = 5.094 The result, 5.094, is the Key Factor for $125,000 in this example.

3. The Key Factors shown in the above examples are for illustration only and are not necessarily the Key Factors shown in the Key Factor Tables of this Manual.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-310-1 Ed. 05/13 v.6.4

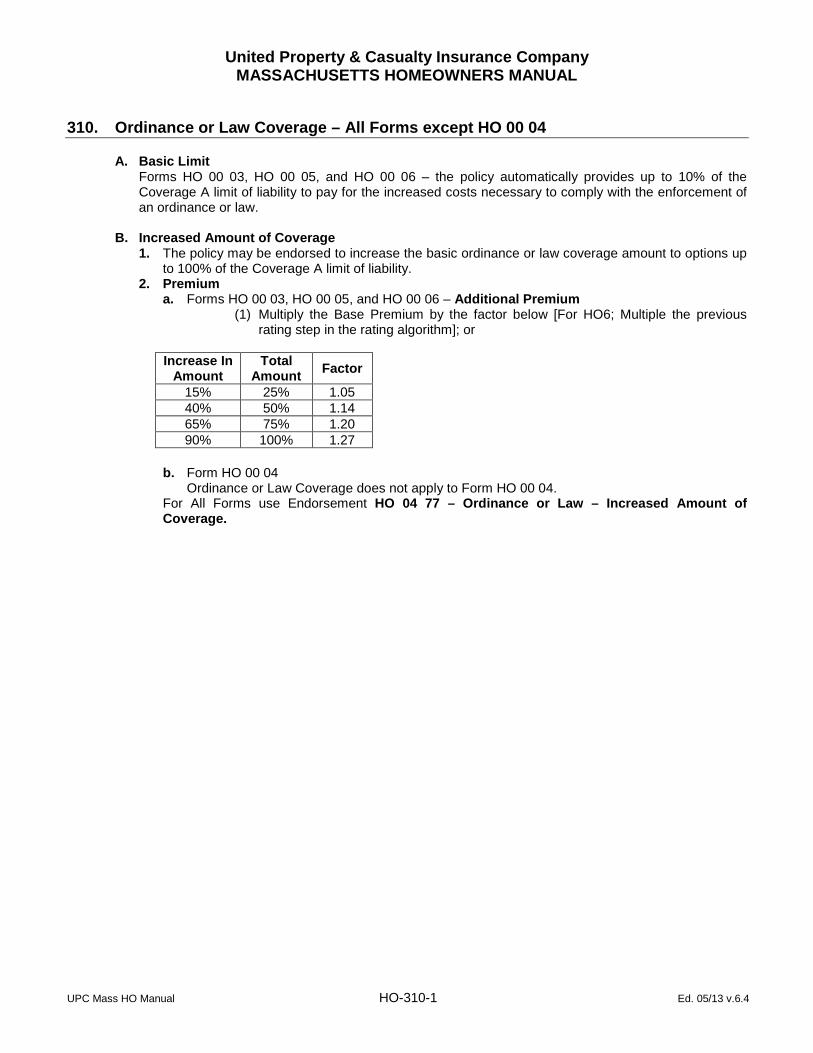

310. Ordinance or Law Coverage – All Forms except HO 00 04

A. Basic Limit

Forms HO 00 03, HO 00 05, and HO 00 06 – the policy automatically provides up to 10% of the Coverage A limit of liability to pay for the increased costs necessary to comply with the enforcement of an ordinance or law.

B. Increased Amount of Coverage

1. The policy may be endorsed to increase the basic ordinance or law coverage amount to options up to 100% of the Coverage A limit of liability.

2. Premium a. Forms HO 00 03, HO 00 05, and HO 00 06 – Additional Premium

(1) Multiply the Base Premium by the factor below [For HO6; Multiple the previous rating step in the rating algorithm]; or

Increase In Amount

Total Amount Factor

15% 25% 1.05 40% 50% 1.14 65% 75% 1.20 90% 100% 1.27

b. Form HO 00 04

Ordinance or Law Coverage does not apply to Form HO 00 04. For All Forms use Endorsement HO 04 77 – Ordinance or Law – Increased Amount of Coverage.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-315-1 Ed. 05/13 v.6.4

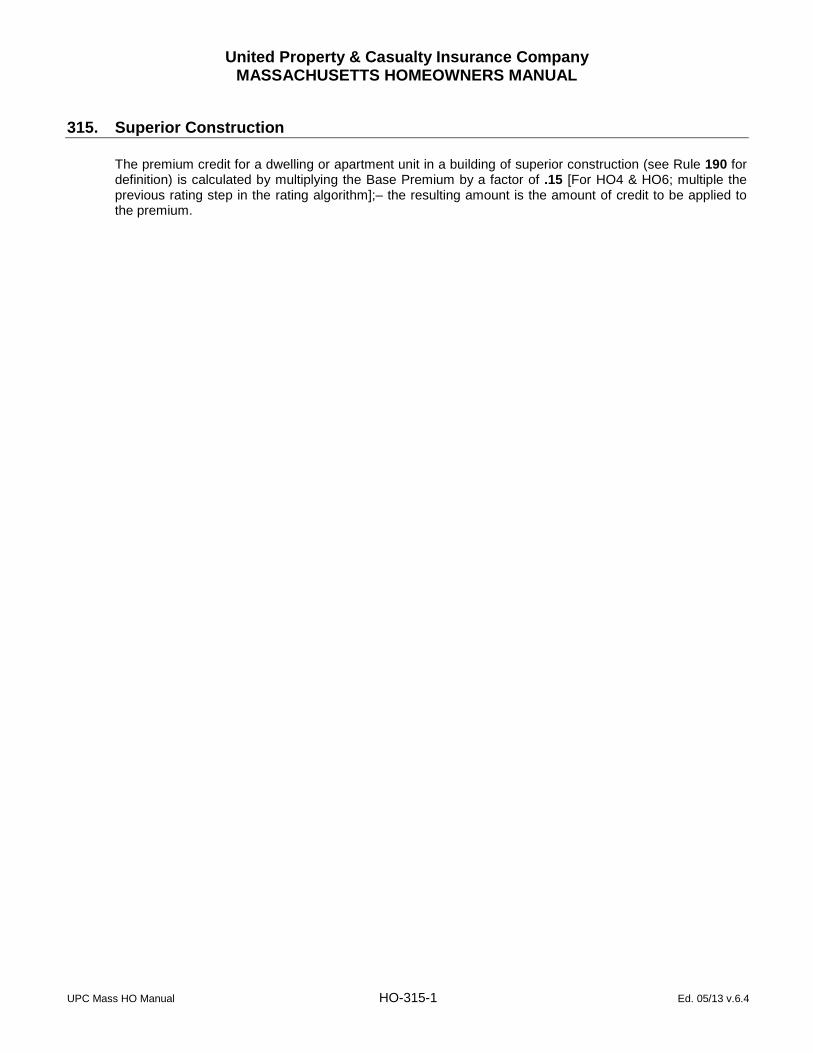

315. Superior Construction

The premium credit for a dwelling or apartment unit in a building of superior construction (see Rule 190 for definition) is calculated by multiplying the Base Premium by a factor of .15 [For HO4 & HO6; multiple the previous rating step in the rating algorithm];– the resulting amount is the amount of credit to be applied to the premium.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-316-1 Ed. 05/13 v.6.4

316. Restriction Of Individual Policies

If a policy would not be issued because of unusual circumstances or exposures, the named insured may request a restriction of the policy provided no reduction in the premium is allowed. Such requests shall be referred to the company.

The following paragraph is added:

The following recommended form of request signed by the Named Insured shall be submitted in duplicate to the Insurance Department for approval: Request for Issuance of a Policy Subject to Restriction in coverage. The coverage afforded under the policy to which this endorsement is attached is not obtainable by the undersigned Named Insured at standard rates and its issuance is therefore requested subject to the following restriction:

(Insert here applicable restriction) (Signature of Named Insured)

The following endorsement, duplicate copies of which shall be signed by the Named Insured and the company, shall be attached to the policy and the daily report:

At the request of the Named Insured, it is agreed that this policy is restricted in the following respects:

(Insert here applicable restriction)

Insurance Company By (Title) (Signature of Named Insured)

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-317-1 Ed. 05/13 v.6.4

317. Additional Interest A. In addition to the mortgagee(s) shown in the Declarations or elsewhere in the policy, other persons or

organizations may have an insurable interest in the residence premises. When coverage is not provided to such persons or organizations under Additional Insured Endorsement HO 04 41 or its equivalent, their interest in the residence premises may be acknowledged by naming them in the endorsement referenced in Paragraph D.

B. Such persons or organizations are entitled to receive notification if the policy is canceled or nonrenewed by the insurer.

C. No additional charge is made for use of this endorsement.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-318-1 Ed. 05/13 v.6.4

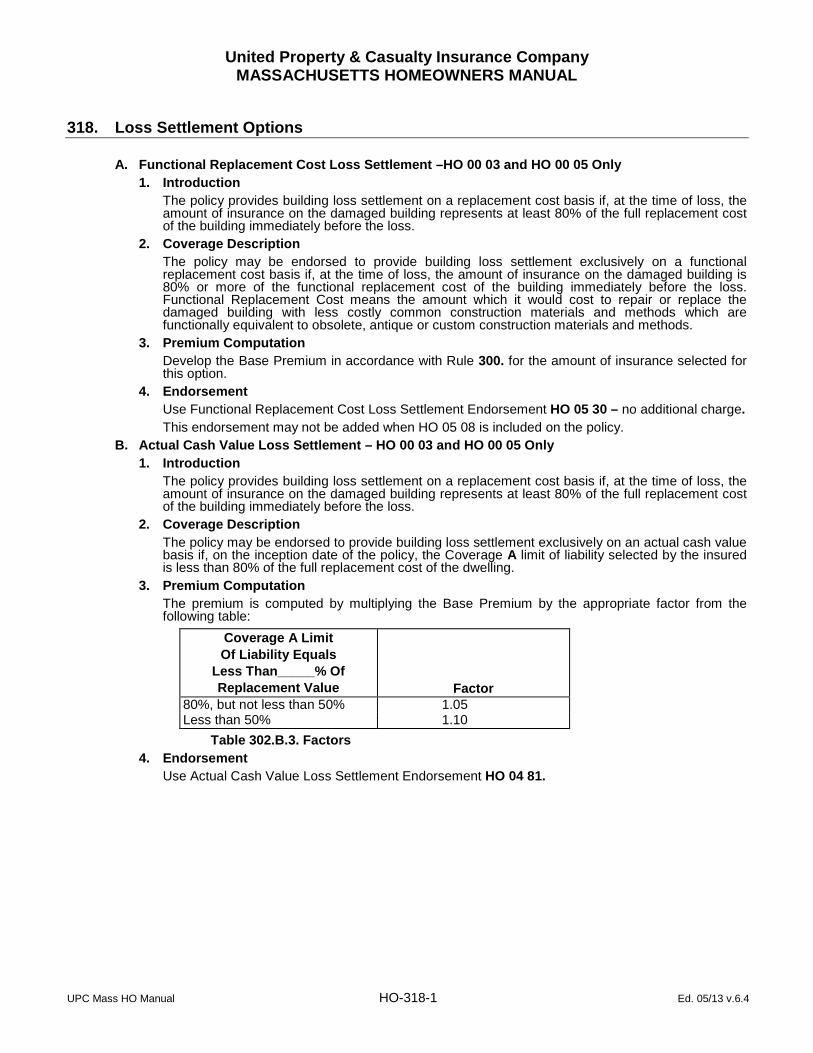

318. Loss Settlement Options A. Functional Replacement Cost Loss Settlement –HO 00 03 and HO 00 05 Only 1. Introduction

The policy provides building loss settlement on a replacement cost basis if, at the time of loss, the amount of insurance on the damaged building represents at least 80% of the full replacement cost of the building immediately before the loss.

2. Coverage Description The policy may be endorsed to provide building loss settlement exclusively on a functional replacement cost basis if, at the time of loss, the amount of insurance on the damaged building is 80% or more of the functional replacement cost of the building immediately before the loss. Functional Replacement Cost means the amount which it would cost to repair or replace the damaged building with less costly common construction materials and methods which are functionally equivalent to obsolete, antique or custom construction materials and methods.

3. Premium Computation Develop the Base Premium in accordance with Rule 300. for the amount of insurance selected for this option.

4. Endorsement Use Functional Replacement Cost Loss Settlement Endorsement HO 05 30 – no additional charge. This endorsement may not be added when HO 05 08 is included on the policy.

B. Actual Cash Value Loss Settlement – HO 00 03 and HO 00 05 Only 1. Introduction

The policy provides building loss settlement on a replacement cost basis if, at the time of loss, the amount of insurance on the damaged building represents at least 80% of the full replacement cost of the building immediately before the loss.

2. Coverage Description The policy may be endorsed to provide building loss settlement exclusively on an actual cash value basis if, on the inception date of the policy, the Coverage A limit of liability selected by the insured is less than 80% of the full replacement cost of the dwelling.

3. Premium Computation The premium is computed by multiplying the Base Premium by the appropriate factor from the following table:

Coverage A Limit Of Liability Equals

Less Than_____% Of Replacement Value

Factor 80%, but not less than 50% 1.05 Less than 50% 1.10

Table 302.B.3. Factors 4. Endorsement

Use Actual Cash Value Loss Settlement Endorsement HO 04 81.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-319-1 Ed. 05/13 v.6.4

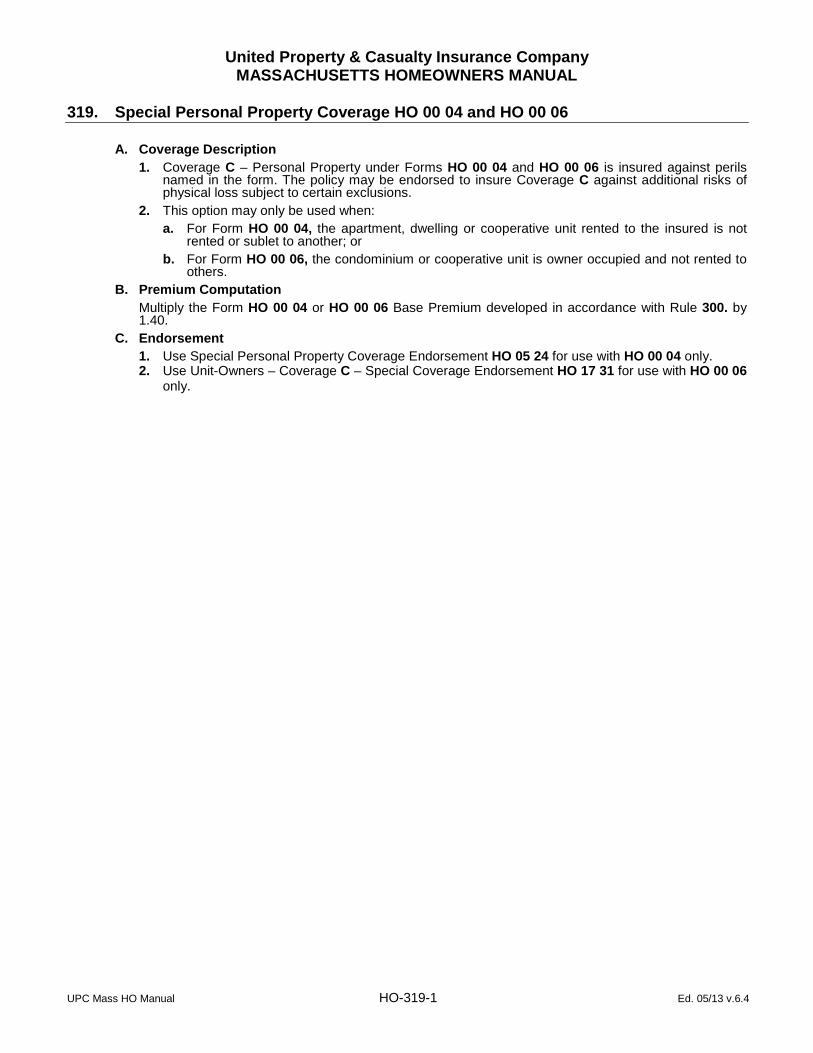

319. Special Personal Property Coverage HO 00 04 and HO 00 06

A. Coverage Description 1. Coverage C – Personal Property under Forms HO 00 04 and HO 00 06 is insured against perils

named in the form. The policy may be endorsed to insure Coverage C against additional risks of physical loss subject to certain exclusions.

2. This option may only be used when: a. For Form HO 00 04, the apartment, dwelling or cooperative unit rented to the insured is not

rented or sublet to another; or b. For Form HO 00 06, the condominium or cooperative unit is owner occupied and not rented to

others. B. Premium Computation

Multiply the Form HO 00 04 or HO 00 06 Base Premium developed in accordance with Rule 300. by 1.40.

C. Endorsement 1. Use Special Personal Property Coverage Endorsement HO 05 24 for use with HO 00 04 only. 2. Use Unit-Owners – Coverage C – Special Coverage Endorsement HO 17 31 for use with HO 00 06

only.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-410-1 Ed. 05/13 v.6.4

410. Town House or Row House – Forms HO 00 03 and HO 00 05 Only

The premium for an eligible 1 family dwelling in a townhouse or rowhouse structure is calculated by multiplying the Base Premium by the appropriate factor below. Total No. of Individual Family Protection Class

Units Within the Fire Division 1– 8 9 1 & 2 1.00 1.00 3 & 4 1.10 1.15 5 & Over Ineligible Ineligible

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-420-1 Ed. 05/13 v.6.4

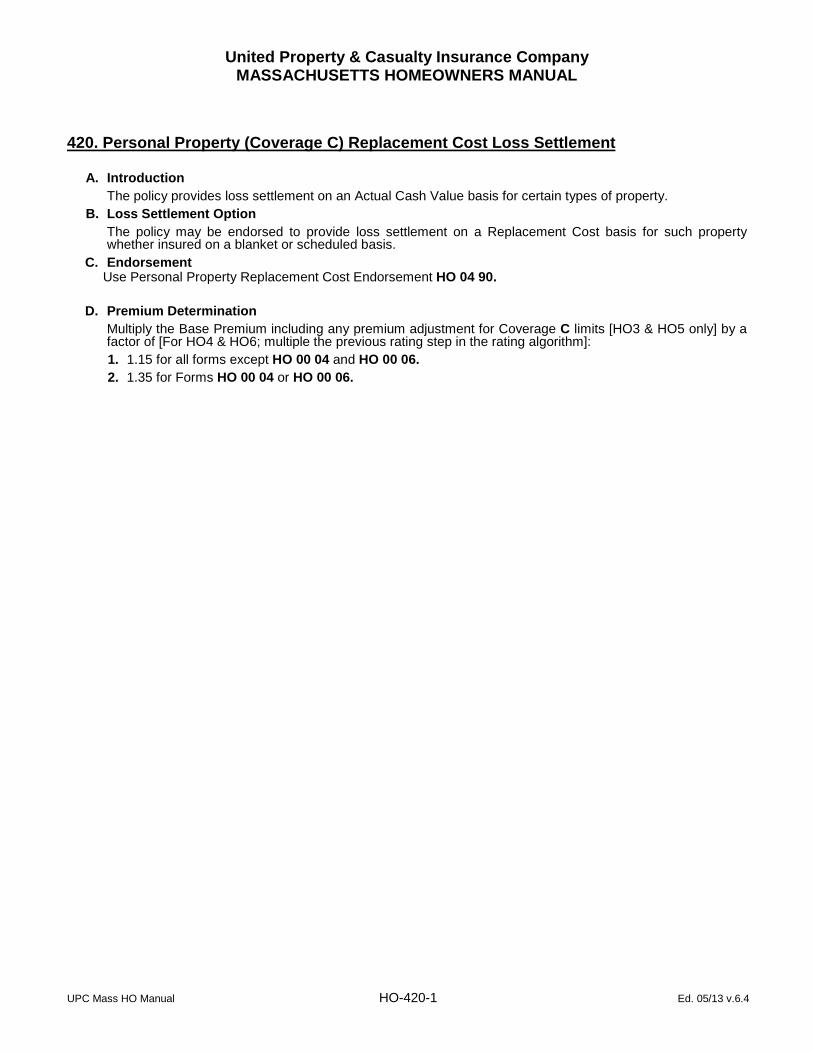

420. Personal Property (Coverage C) Replacement Cost Loss Settlement A. Introduction

The policy provides loss settlement on an Actual Cash Value basis for certain types of property. B. Loss Settlement Option

The policy may be endorsed to provide loss settlement on a Replacement Cost basis for such property whether insured on a blanket or scheduled basis.

C. Endorsement Use Personal Property Replacement Cost Endorsement HO 04 90.

D. Premium Determination Multiply the Base Premium including any premium adjustment for Coverage C limits [HO3 & HO5 only] by a factor of [For HO4 & HO6; multiple the previous rating step in the rating algorithm]:

1. 1.15 for all forms except HO 00 04 and HO 00 06. 2. 1.35 for Forms HO 00 04 or HO 00 06.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-430-1 Ed. 05/13 v.6.4

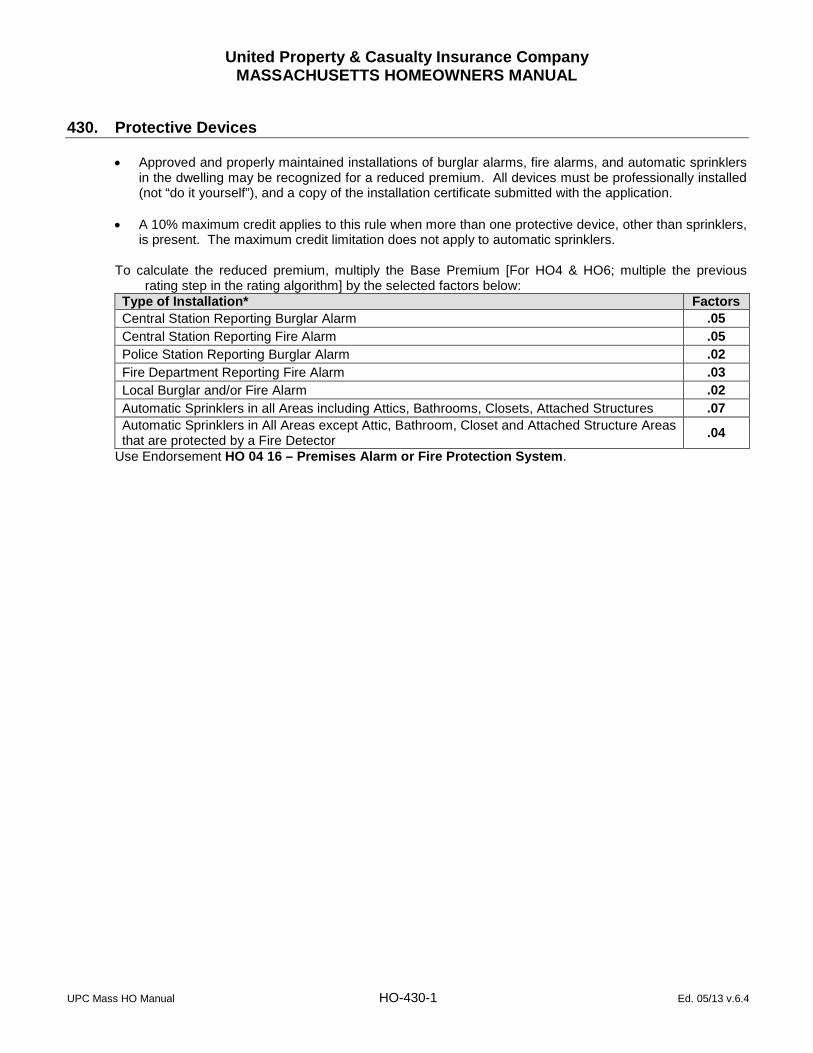

430. Protective Devices

• Approved and properly maintained installations of burglar alarms, fire alarms, and automatic sprinklers

in the dwelling may be recognized for a reduced premium. All devices must be professionally installed (not “do it yourself”), and a copy of the installation certificate submitted with the application.

• A 10% maximum credit applies to this rule when more than one protective device, other than sprinklers,

is present. The maximum credit limitation does not apply to automatic sprinklers. To calculate the reduced premium, multiply the Base Premium [For HO4 & HO6; multiple the previous

rating step in the rating algorithm] by the selected factors below: Type of Installation* Factors Central Station Reporting Burglar Alarm .05 Central Station Reporting Fire Alarm .05 Police Station Reporting Burglar Alarm .02 Fire Department Reporting Fire Alarm .03 Local Burglar and/or Fire Alarm .02 Automatic Sprinklers in all Areas including Attics, Bathrooms, Closets, Attached Structures .07 Automatic Sprinklers in All Areas except Attic, Bathroom, Closet and Attached Structure Areas that are protected by a Fire Detector .04

Use Endorsement HO 04 16 – Premises Alarm or Fire Protection System.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-440-1 Ed. 05/13 v.6.4

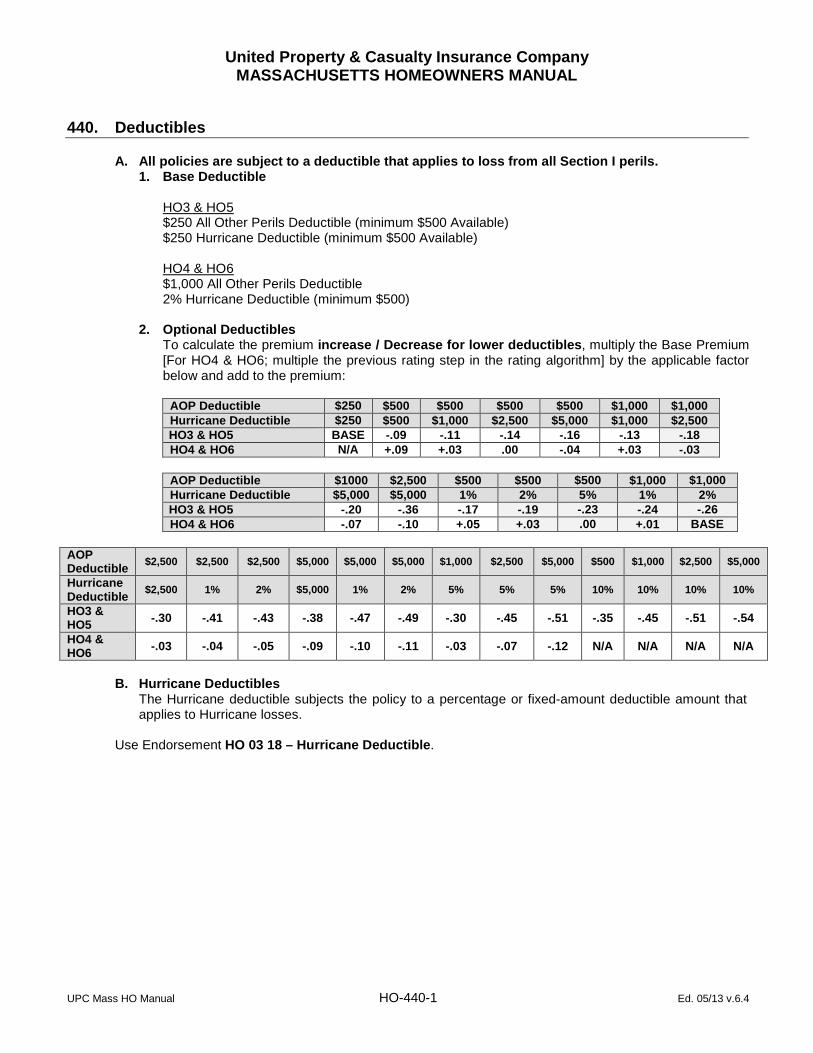

440. Deductibles

A. All policies are subject to a deductible that applies to loss from all Section I perils.

1. Base Deductible HO3 & HO5 $250 All Other Perils Deductible (minimum $500 Available) $250 Hurricane Deductible (minimum $500 Available) HO4 & HO6 $1,000 All Other Perils Deductible 2% Hurricane Deductible (minimum $500)

2. Optional Deductibles To calculate the premium increase / Decrease for lower deductibles, multiply the Base Premium [For HO4 & HO6; multiple the previous rating step in the rating algorithm] by the applicable factor below and add to the premium:

AOP Deductible $250 $500 $500 $500 $500 $1,000 $1,000 Hurricane Deductible $250 $500 $1,000 $2,500 $5,000 $1,000 $2,500 HO3 & HO5 BASE -.09 -.11 -.14 -.16 -.13 -.18 HO4 & HO6 N/A +.09 +.03 .00 -.04 +.03 -.03

AOP Deductible $1000 $2,500 $500 $500 $500 $1,000 $1,000 Hurricane Deductible $5,000 $5,000 1% 2% 5% 1% 2% HO3 & HO5 -.20 -.36 -.17 -.19 -.23 -.24 -.26 HO4 & HO6 -.07 -.10 +.05 +.03 .00 +.01 BASE

AOP Deductible $2,500 $2,500 $2,500 $5,000 $5,000 $5,000 $1,000 $2,500 $5,000 $500 $1,000 $2,500 $5,000

Hurricane Deductible $2,500 1% 2% $5,000 1% 2% 5% 5% 5% 10% 10% 10% 10%

HO3 & HO5 -.30 -.41 -.43 -.38 -.47 -.49 -.30 -.45 -.51 -.35 -.45 -.51 -.54

HO4 & HO6 -.03 -.04 -.05 -.09 -.10 -.11 -.03 -.07 -.12 N/A N/A N/A N/A

B. Hurricane Deductibles

The Hurricane deductible subjects the policy to a percentage or fixed-amount deductible amount that applies to Hurricane losses.

Use Endorsement HO 03 18 – Hurricane Deductible.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-450-1 Ed. 05/13 v.6.4

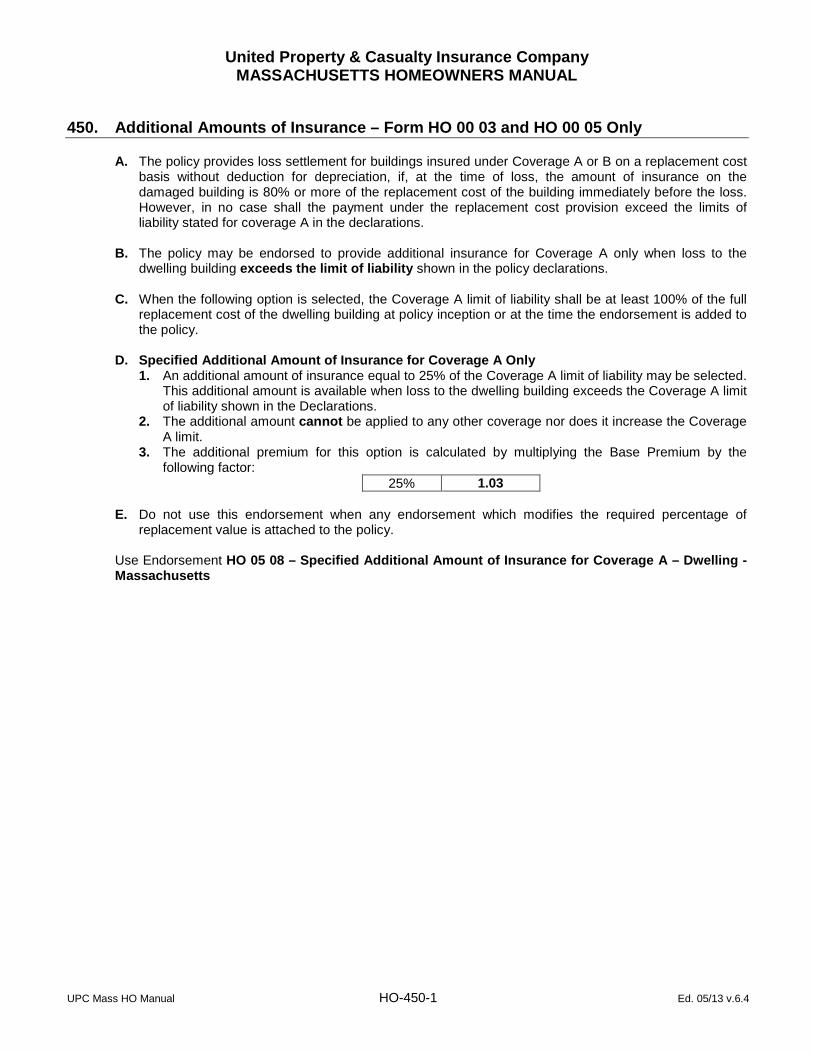

450. Additional Amounts of Insurance – Form HO 00 03 and HO 00 05 Only

A. The policy provides loss settlement for buildings insured under Coverage A or B on a replacement cost

basis without deduction for depreciation, if, at the time of loss, the amount of insurance on the damaged building is 80% or more of the replacement cost of the building immediately before the loss. However, in no case shall the payment under the replacement cost provision exceed the limits of liability stated for coverage A in the declarations.

B. The policy may be endorsed to provide additional insurance for Coverage A only when loss to the

dwelling building exceeds the limit of liability shown in the policy declarations.

C. When the following option is selected, the Coverage A limit of liability shall be at least 100% of the full replacement cost of the dwelling building at policy inception or at the time the endorsement is added to the policy.

D. Specified Additional Amount of Insurance for Coverage A Only

1. An additional amount of insurance equal to 25% of the Coverage A limit of liability may be selected. This additional amount is available when loss to the dwelling building exceeds the Coverage A limit of liability shown in the Declarations.

2. The additional amount cannot be applied to any other coverage nor does it increase the Coverage A limit.

3. The additional premium for this option is calculated by multiplying the Base Premium by the following factor:

25% 1.03

E. Do not use this endorsement when any endorsement which modifies the required percentage of replacement value is attached to the policy.

Use Endorsement HO 05 08 – Specified Additional Amount of Insurance for Coverage A – Dwelling - Massachusetts

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-460-1 Ed. 05/13 v.6.4

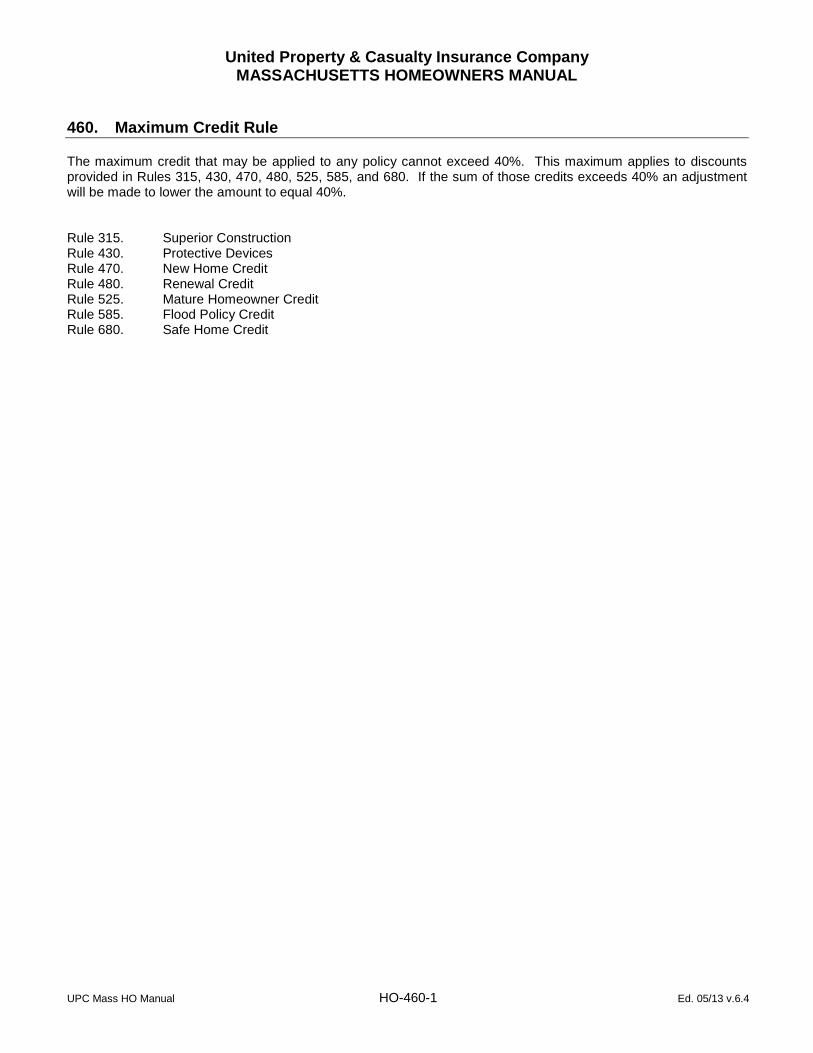

460. Maximum Credit Rule The maximum credit that may be applied to any policy cannot exceed 40%. This maximum applies to discounts provided in Rules 315, 430, 470, 480, 525, 585, and 680. If the sum of those credits exceeds 40% an adjustment will be made to lower the amount to equal 40%. Rule 315. Superior Construction Rule 430. Protective Devices Rule 470. New Home Credit Rule 480. Renewal Credit Rule 525. Mature Homeowner Credit Rule 585. Flood Policy Credit Rule 680. Safe Home Credit

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-465-1 Ed. 05/13 v.6.4

465. Supplemental Heating Surcharge – Forms HO 00 03 and HO 00 05 Only Apply a $50 surcharge to the Annual Premium when the home is equipped with a woodstove, a woodstove insert, or other supplemental heating device.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-470-1 Ed. 05/13 v.6.4

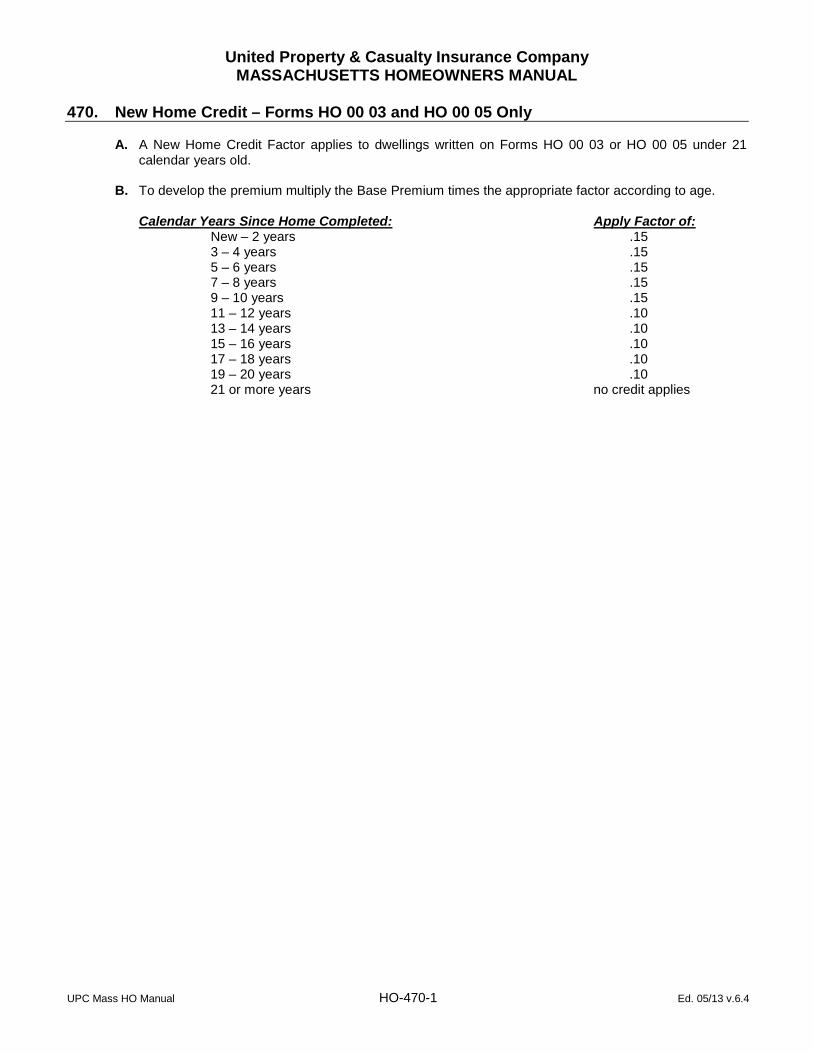

470. New Home Credit – Forms HO 00 03 and HO 00 05 Only A. A New Home Credit Factor applies to dwellings written on Forms HO 00 03 or HO 00 05 under 21

calendar years old. B. To develop the premium multiply the Base Premium times the appropriate factor according to age.

Calendar Years Since Home Completed: Apply Factor of: New – 2 years .15 3 – 4 years .15 5 – 6 years .15 7 – 8 years .15 9 – 10 years .15 11 – 12 years .10 13 – 14 years .10 15 – 16 years .10 17 – 18 years .10 19 – 20 years .10 21 or more years no credit applies

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-480-1 Ed. 05/13 v.6.4

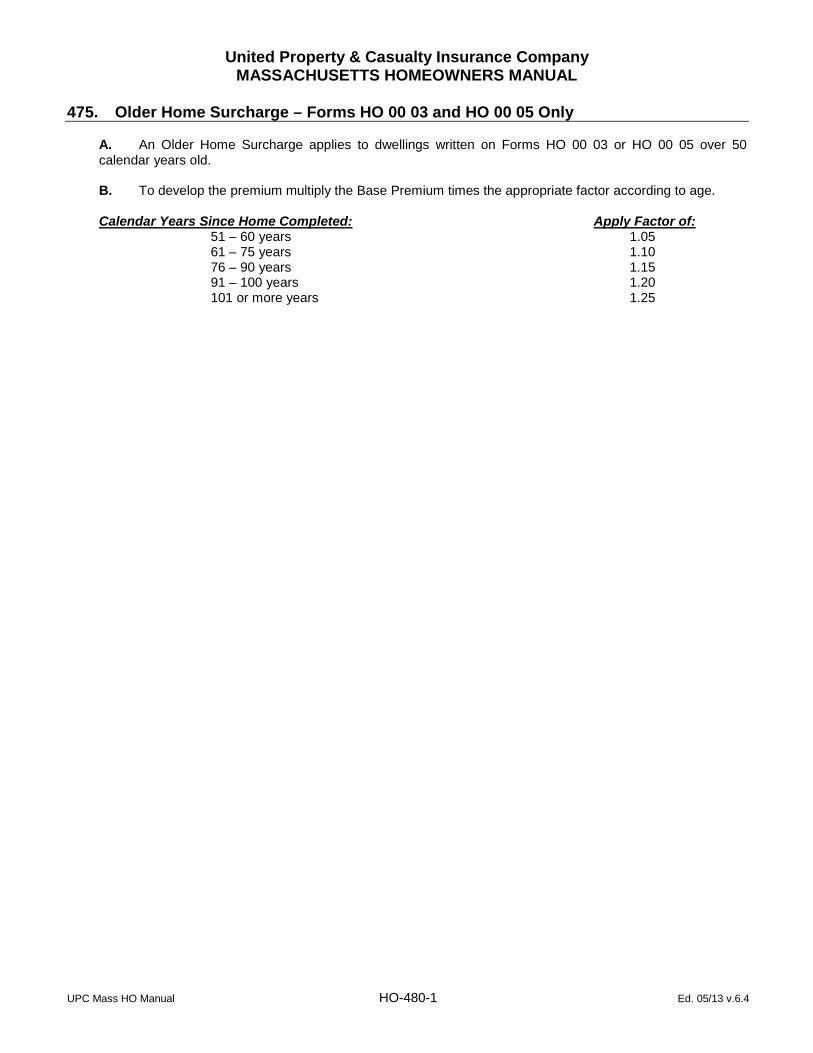

475. Older Home Surcharge – Forms HO 00 03 and HO 00 05 Only A. An Older Home Surcharge applies to dwellings written on Forms HO 00 03 or HO 00 05 over 50 calendar years old. B. To develop the premium multiply the Base Premium times the appropriate factor according to age. Calendar Years Since Home Completed: Apply Factor of: 51 – 60 years 1.05 61 – 75 years 1.10 76 – 90 years 1.15 91 – 100 years 1.20 101 or more years 1.25

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-480-1 Ed. 05/13 v.6.4

480. Renewal Credit – Forms HO 00 03 and HO 00 05 Only

A. 5% Renewal Credit. Available to Insureds who have been continuously insured with the Company on Forms HO 00 03 or HO 00 05 for two years or longer and have not had any losses/claims during that period.

B. To develop the premium credit multiply the Base Premium times the discount factor listed in A. above. Note: This discount may only be applied at a renewal of an applicable Company policy, or upon assumption of a roll-over book from another company for which the Company is using renewal guidelines.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-481-1 Ed. 05/13 v.6.4

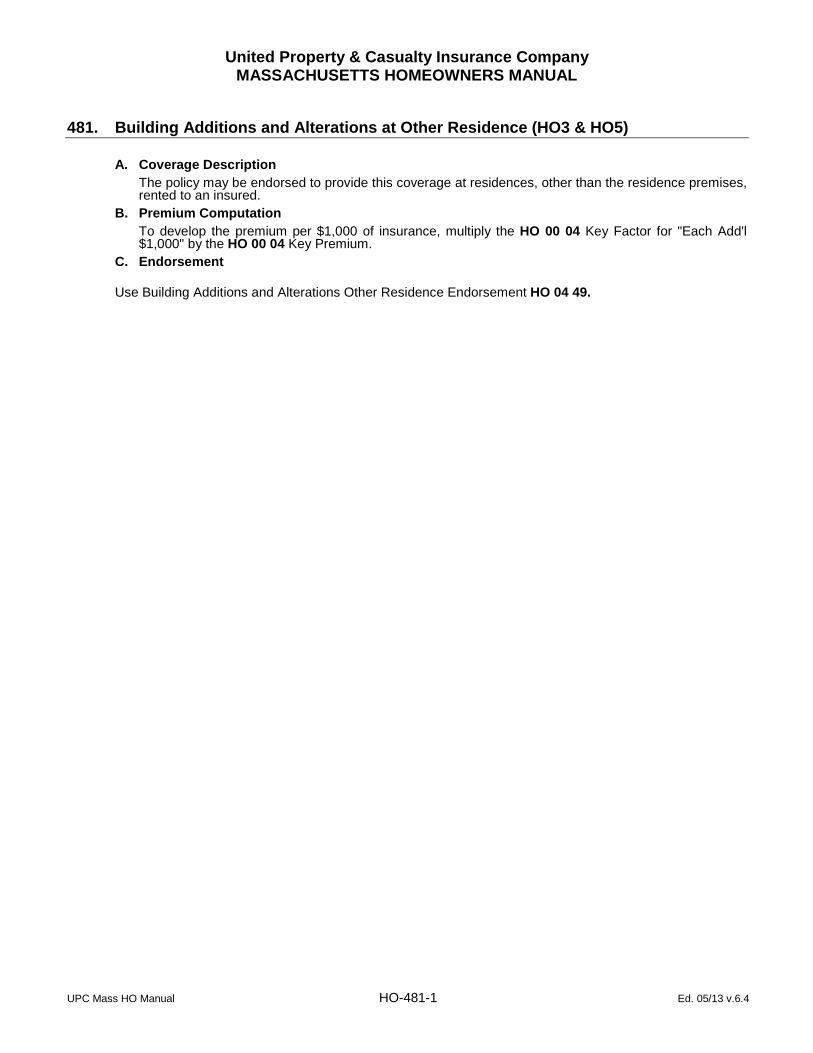

481. Building Additions and Alterations at Other Residence (HO3 & HO5) A. Coverage Description

The policy may be endorsed to provide this coverage at residences, other than the residence premises, rented to an insured.

B. Premium Computation To develop the premium per $1,000 of insurance, multiply the HO 00 04 Key Factor for "Each Add'l $1,000" by the HO 00 04 Key Premium.

C. Endorsement

Use Building Additions and Alterations Other Residence Endorsement HO 04 49.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-482-1 Ed. 05/13 v.6.4

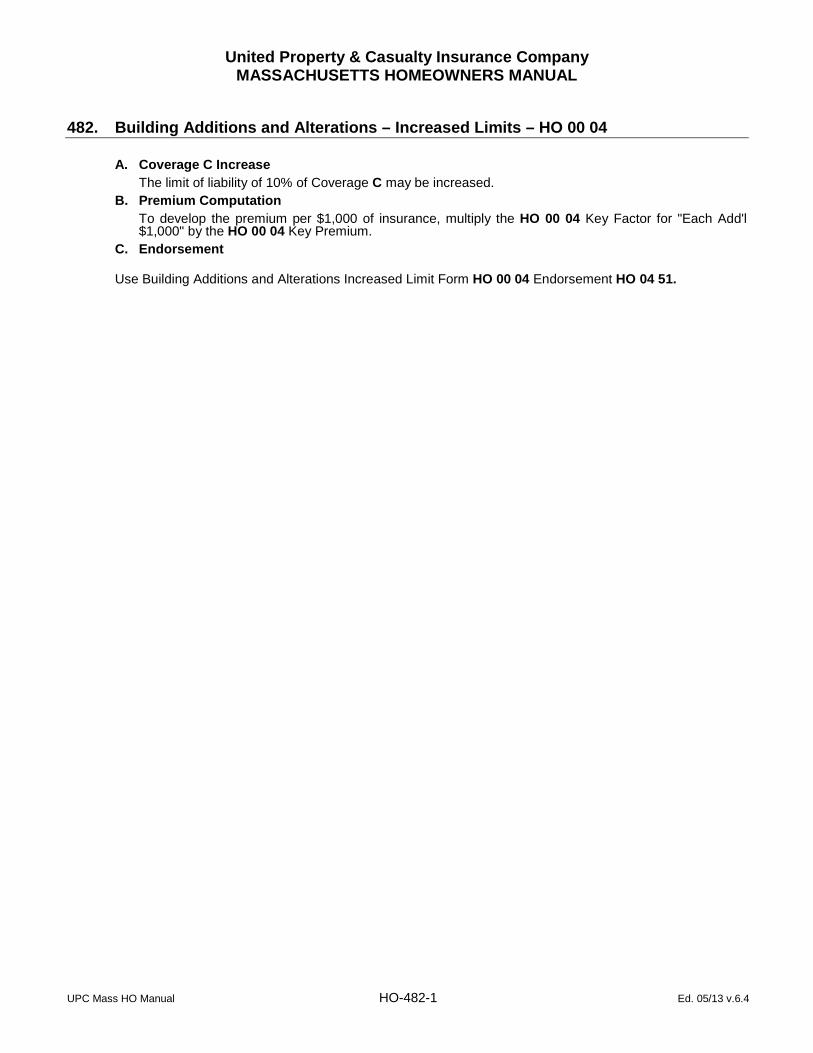

482. Building Additions and Alterations – Increased Limits – HO 00 04

A. Coverage C Increase The limit of liability of 10% of Coverage C may be increased.

B. Premium Computation To develop the premium per $1,000 of insurance, multiply the HO 00 04 Key Factor for "Each Add'l $1,000" by the HO 00 04 Key Premium.

C. Endorsement Use Building Additions and Alterations Increased Limit Form HO 00 04 Endorsement HO 04 51.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-490-1 Ed. 05/13 v.6.4

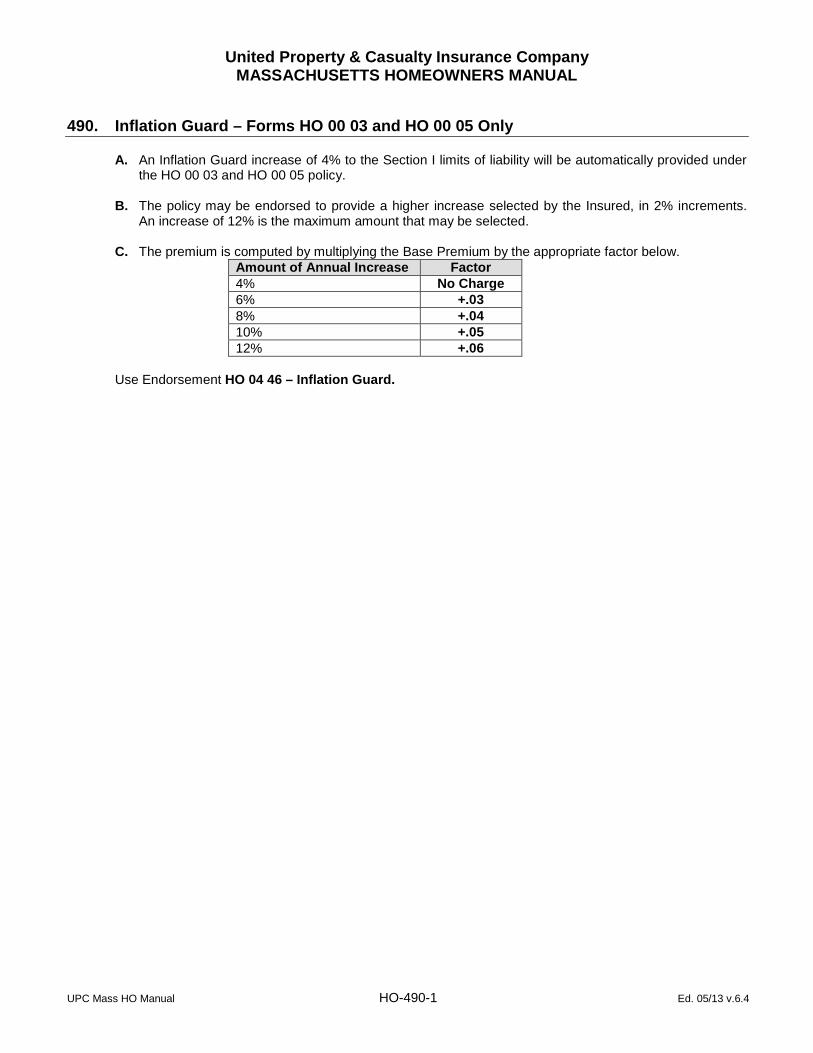

490. Inflation Guard – Forms HO 00 03 and HO 00 05 Only

A. An Inflation Guard increase of 4% to the Section I limits of liability will be automatically provided under the HO 00 03 and HO 00 05 policy.

B. The policy may be endorsed to provide a higher increase selected by the Insured, in 2% increments.

An increase of 12% is the maximum amount that may be selected.

C. The premium is computed by multiplying the Base Premium by the appropriate factor below. Amount of Annual Increase Factor 4% No Charge 6% +.03 8% +.04 10% +.05 12% +.06

Use Endorsement HO 04 46 – Inflation Guard.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-500-1 Ed. 05/13 v.6.4

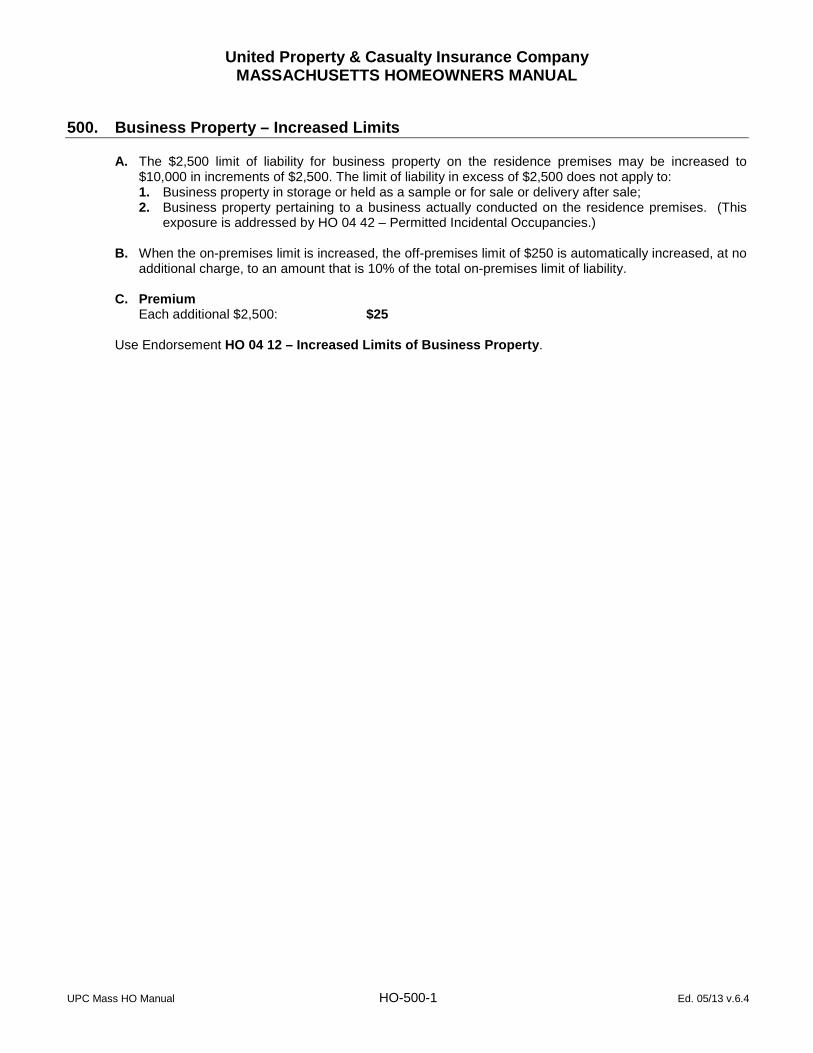

500. Business Property – Increased Limits

A. The $2,500 limit of liability for business property on the residence premises may be increased to

$10,000 in increments of $2,500. The limit of liability in excess of $2,500 does not apply to: 1. Business property in storage or held as a sample or for sale or delivery after sale; 2. Business property pertaining to a business actually conducted on the residence premises. (This

exposure is addressed by HO 04 42 – Permitted Incidental Occupancies.)

B. When the on-premises limit is increased, the off-premises limit of $250 is automatically increased, at no additional charge, to an amount that is 10% of the total on-premises limit of liability.

C. Premium

Each additional $2,500: $25

Use Endorsement HO 04 12 – Increased Limits of Business Property.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-510-1 Ed. 05/13 v.6.4

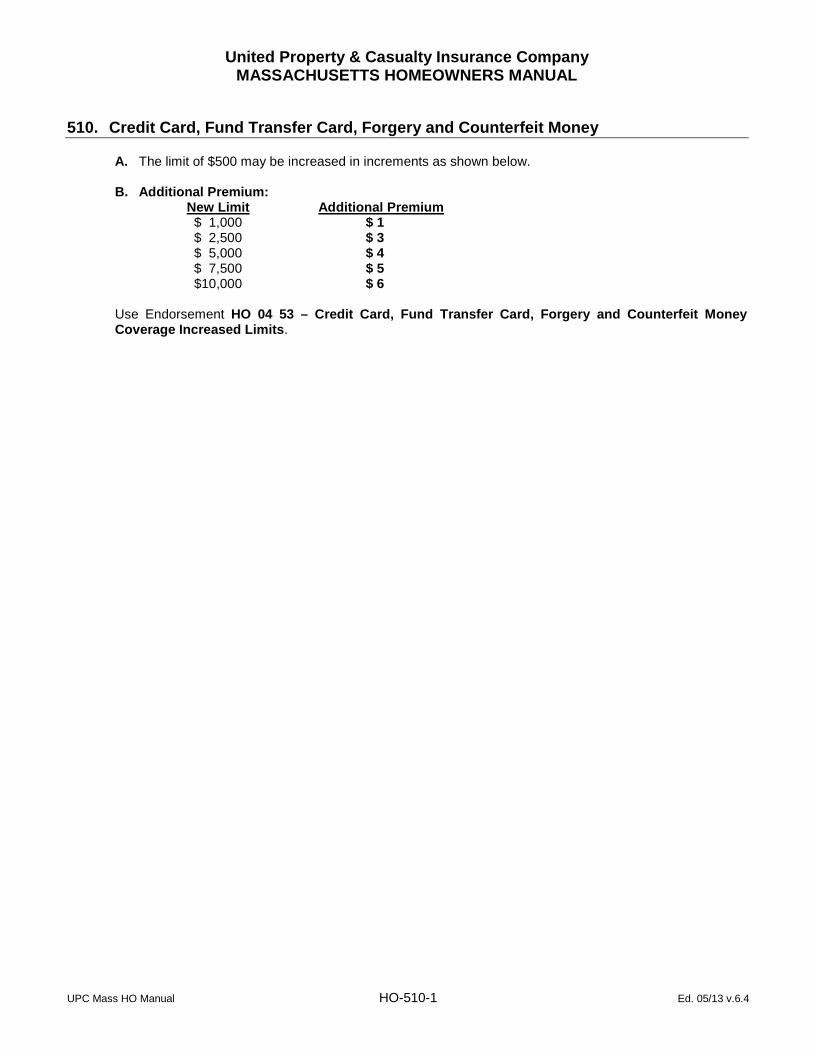

510. Credit Card, Fund Transfer Card, Forgery and Counterfeit Money

A. The limit of $500 may be increased in increments as shown below. B. Additional Premium:

New Limit Additional Premium $ 1,000 $ 1 $ 2,500 $ 3 $ 5,000 $ 4 $ 7,500 $ 5 $10,000 $ 6

Use Endorsement HO 04 53 – Credit Card, Fund Transfer Card, Forgery and Counterfeit Money Coverage Increased Limits.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-520-1 Ed. 05/13 v.6.4

520. Companion Automobile Policy Credit – Forms HO 00 03 and HO 00 05 Only A. All Automobile Carriers Excluding Arbella Insurance Group

1. A companion policy credit is available on the HO 00 03 or HO 00 05 policy when the insured owner-occupant of the home also purchases an automobile policy through the same agent. “Owner” includes joint ownership by a husband and wife.

2. A copy of the current automobile policy declarations page, or a copy of the automobile insurance

application, must be kept in the insured’s homeowner policy file in the agent’s office along with all other policy documentation. The automobile policy must be kept in force yearly in order for the companion policy credit to continue to apply to the HO 00 03 or HO 00 05 policy.

3. To compute the credit multiply the Total Premium Without Fees times a factor of .05.

B. Automobile Carrier Arbella Insurance Group

1. A companion policy credit is available on the HO 00 03 or HO 00 05 policy when the insured owner-occupant of the home also purchases an automobile policy through the Arbella Insurance Group. “Owner” includes joint ownership by a husband and wife.

2. A copy of the current automobile policy declarations page, or a copy of the automobile insurance

application, must be kept in the insured’s homeowner policy file in the agent’s office along with all other policy documentation. The automobile policy must be kept in force yearly in order for the companion policy credit to continue to apply to the HO 00 03 or HO 00 05 policy.

3. To compute the credit multiply the Total Premium Without Fees times a factor of .10.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-520-1 Ed. 05/13 v.6.4

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-525-1 Ed. 05/13 v.6.4

525. Mature Homeowner Credit – All Forms The policyholder is eligible if the following criteria are met:

1. One of the Named Insureds is age 50 or older and is not employed more than 20 hours a week outside the residence premises.

If the policy is eligible, a 15% discount is applied to the Base Premium [For HO4 & HO6; multiple the previous rating step in the rating algorithm]. The credit shall not be applied midterm. The “Mature Homeowner Credit” criteria must be indicated on the application for this discount to be applied.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-530-1 Ed. 05/13 v.6.4

530. Form HO 00 06 – Coverage A Dwelling Basic and Increased Limits and Special Coverage

A. Basic Limits

The policy automatically provides a basic Coverage A limit of $5,000 on a named peril basis. If increased limits are not desired, enter “$5,000” under Cov. A – Dwelling on the Declarations pages.

B. Increased Limits The basic limit may be increased. The premium is developed based on the additional amount of insurance. To develop the premium for each additional $1,000 of insurance, multiply the HO 00 06 Key Factor for “Each Additional $1,000” by the HO 00 06 Key Premium.

C. Special Coverage The Section I Perils Insured Against may be broadened to cover open perils. The additional premium is developed as shown on the rate page. 1. Charge per policy for $5,000 in basic form: $6 2. Rate for each additional $1,000 for Coverage A: $1

Use Endorsement HO 17 32 – Unit-Owners Coverage A – Special Coverage.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-540-1 Ed. 05/13 v.6.4

540. Form HO 00 06 – Units Regularly Rented to Others

A. There is no coverage for Coverage C – Personal Property when the residence premises is rented or

held for rental to others. The policy may be endorsed, however, to provide such coverage, including Theft.

B. Short term rentals (rental period of less than six months duration) or units rented more than twice per

year are not allowed.

C. Premium Multiply the previous rating step in the rating algorithm (reflecting the credit or surcharge for optional deductibles) by a factor of 1.25.

Use Endorsement HO 17 33 – Unit-Owners Rental to Others.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-550-1 Ed. 05/13 v.6.4

550. Permitted Incidental Occupancies – Residence Premises

A. Coverage for a permitted incidental occupancy is limited under Section I and excluded under Section II.

The policy may be endorsed to provide expanded Section I Coverage and Section II Coverage on a permitted incidental occupancy in the dwelling or in another structure on the residence premises.

B. Permitted Incidental Occupancies

1. Offices 2. Storage of merchandise if the value of the merchandise does not exceed $10,000.

C. If the permitted incidental occupancy is located in another structure, Coverage B does not apply to that

structure. See E. below, for charge for specific insurance on the structure. D. The permitted incidental occupancies endorsement also covers personal property pertaining to the

permitted incidental occupancy within the Coverage C limits stated in the declarations. If increased Coverage C limits are desired, see Rule 600.A.

E. Premium

1. Section I Coverages a. If the permitted incidental occupancy is located in the dwelling, no additional charge is made. b. If the permitted incidental occupancy is located in another structure, an additional premium is

required. Determine the premium from the rate shown below. Rate per $1,000 for business in other structure: $6

2. Section II Coverages Refer to Rule 820. to develop the premium for the increased Coverage E and F exposure.

Use Endorsement HO 04 42 – Permitted Incidental Occupancies – Residence Premises for Sections I and II Coverage.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-551-1 Ed. 05/13 v.6.4

551. Loss of Use – Increase Only (HO3 & HO5)

A. When the limit of liability for Coverage D is increased, charge the rate per $1,000 of additional insurance.

B. Premium

a. Rate per $1,000……………………………………………………………………. $4

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-553-1 Ed. 05/13 v.6.4

553. Sinkhole Collapse Coverage All Forms Except HO 00 04 and HO 00 06 A. Coverage Description

The policy may be endorsed to provide Sinkhole Collapse Coverage. B. Premium Determination 1. Rate is 0.35 per $1,000 2. Multiply the rate per $1,000 by: a. Coverage A amount of insurance; b. Increased Limits for Coverages C and D; c. Loss Assessment Coverage, increased limits and additional locations; d. Ordinance Or Law Coverage, basic amount and, if applicable, increased amount of coverage;

e. Other Building or Structure options for example: Other Structures Rented To Others (Residence Premises) Endorsement HO 04 40; Other Structures (Increased Limits) Endorsement HO 04 48; Building Additions And Alterations (Other Residence) Endorsement HO 04 49; and Building Additions And Alterations (Increased Limit Form HO 00 04) Endorsement HO 04 51.

C. Endorsement Use Sinkhole Collapse Endorsement HO 04 99.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-560-1 Ed. 05/13 v.6.4

560. Special Computer Coverage

A. The policy may be endorsed to insure computers and related equipment against additional risks of

physical loss subject to certain exclusions, for an additional premium. Coverage is available up to a maximum limit of $10,000. Use the rate shown in B. below.

B. Rate per $1,000 of coverage: $7.50

Use Endorsement HO 04 14 – Special Computer Coverage.

United Property & Casualty Insurance Company MASSACHUSETTS HOMEOWNERS MANUAL

UPC Mass HO Manual HO-561-1 Ed. 05/13 v.6.4

561. Other Members of a Named Insured’s Household

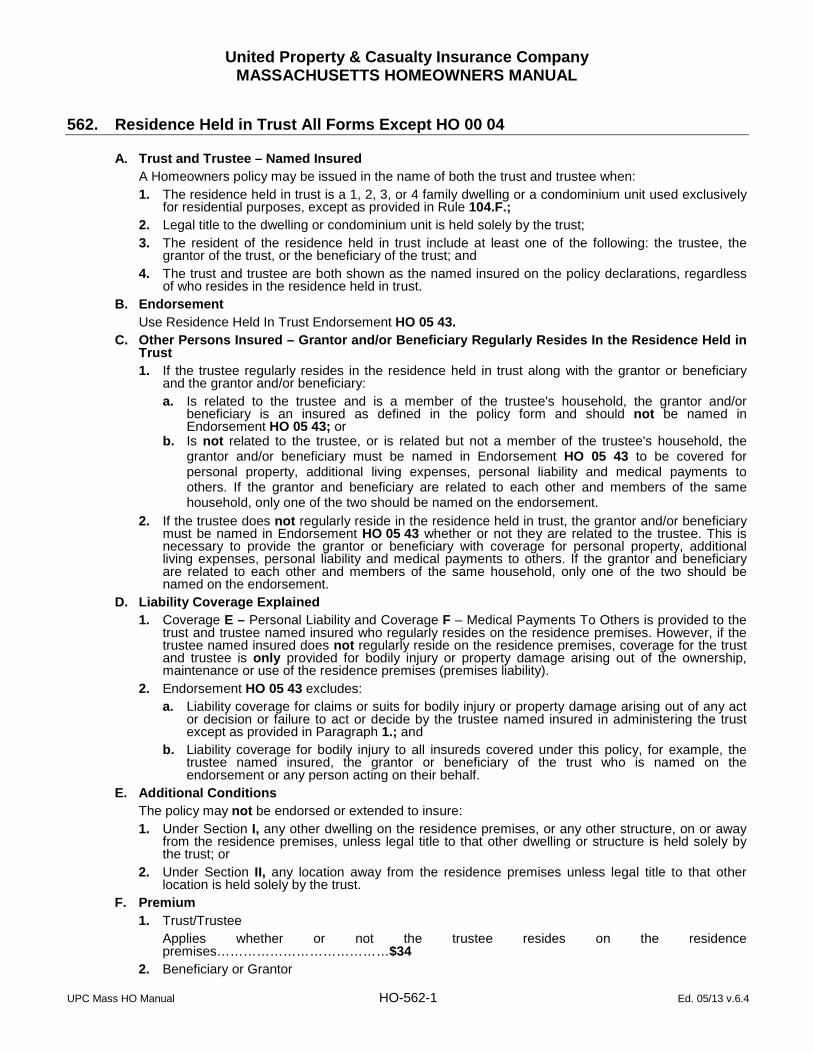

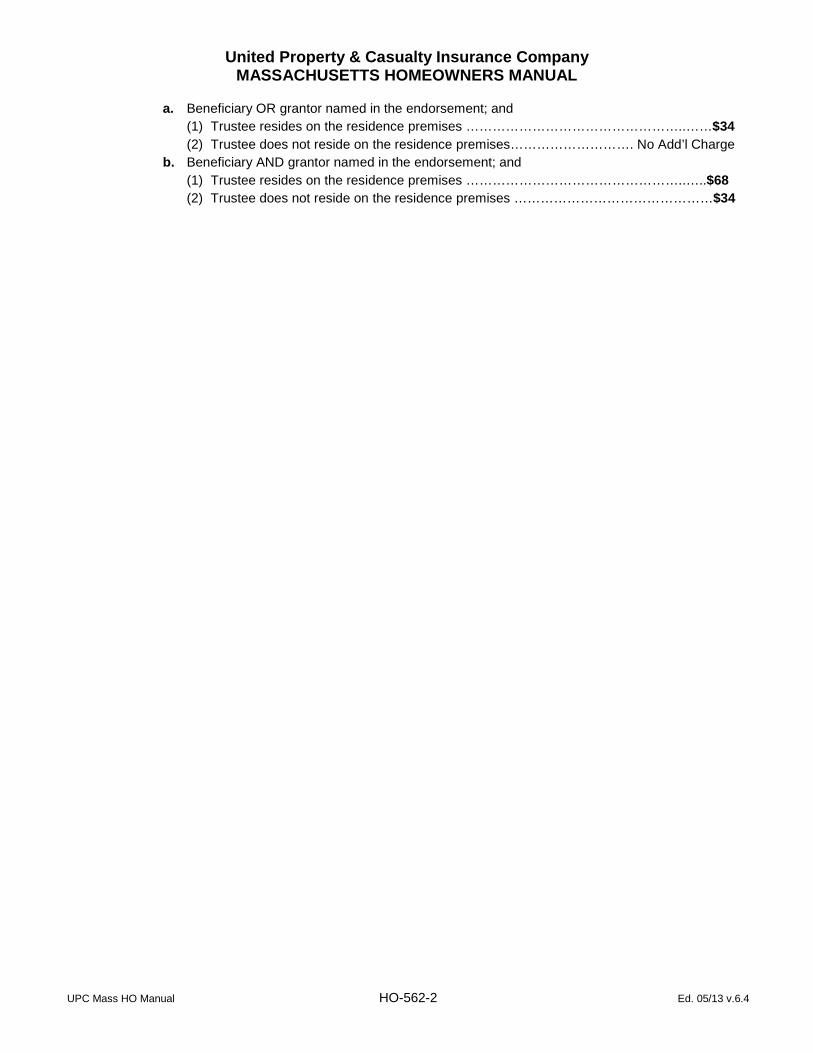

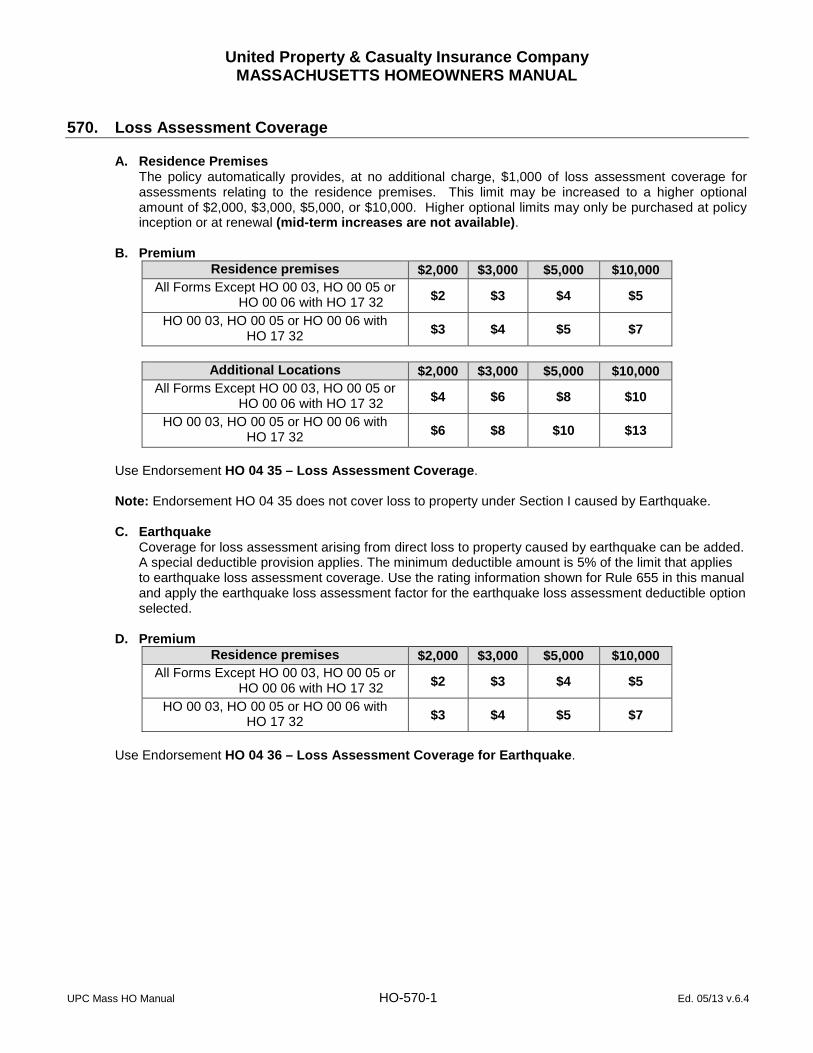

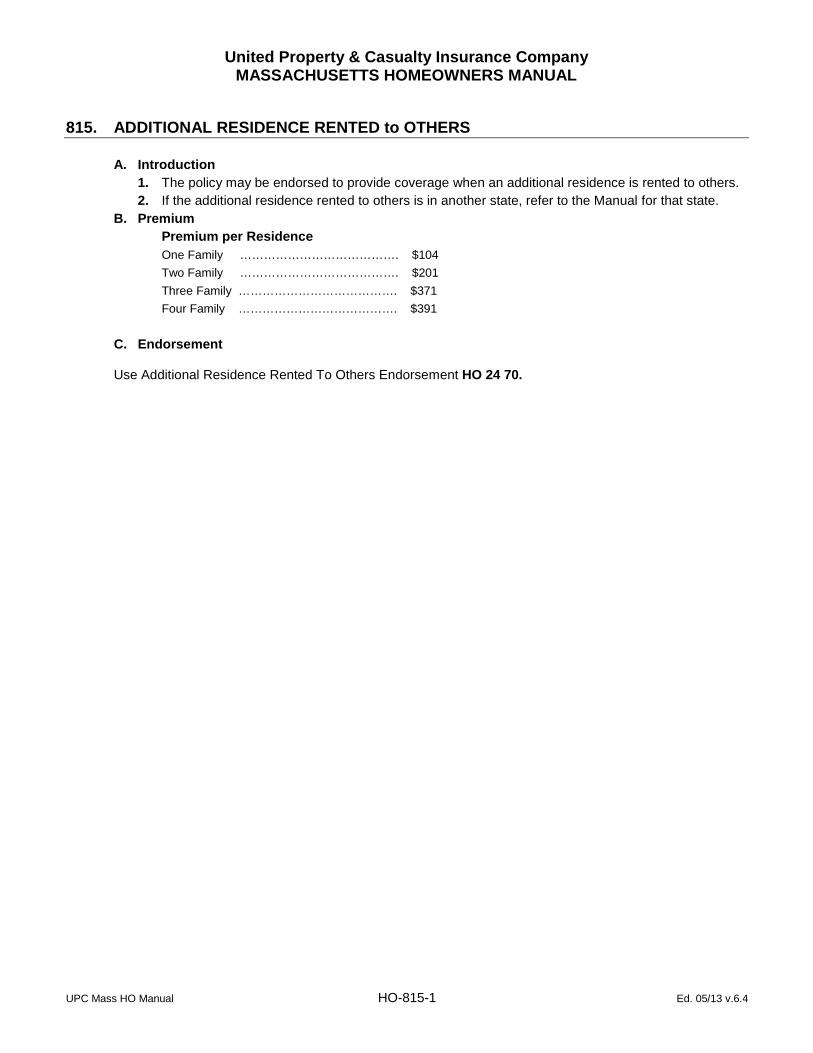

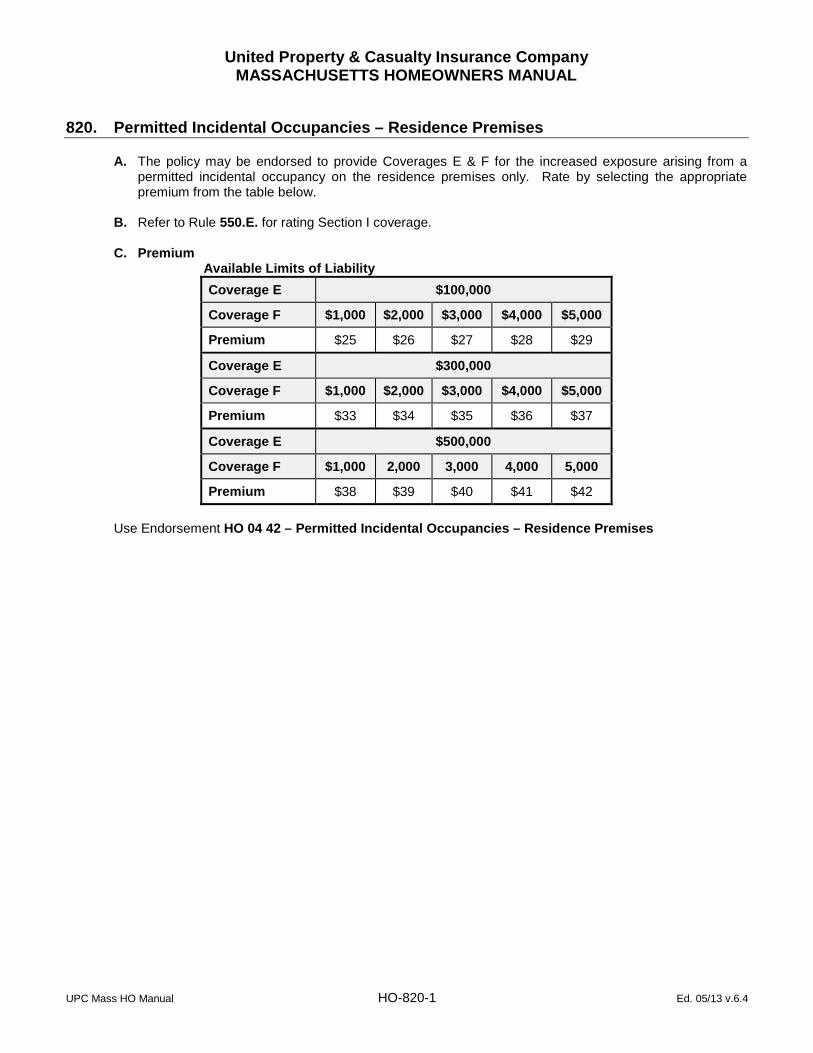

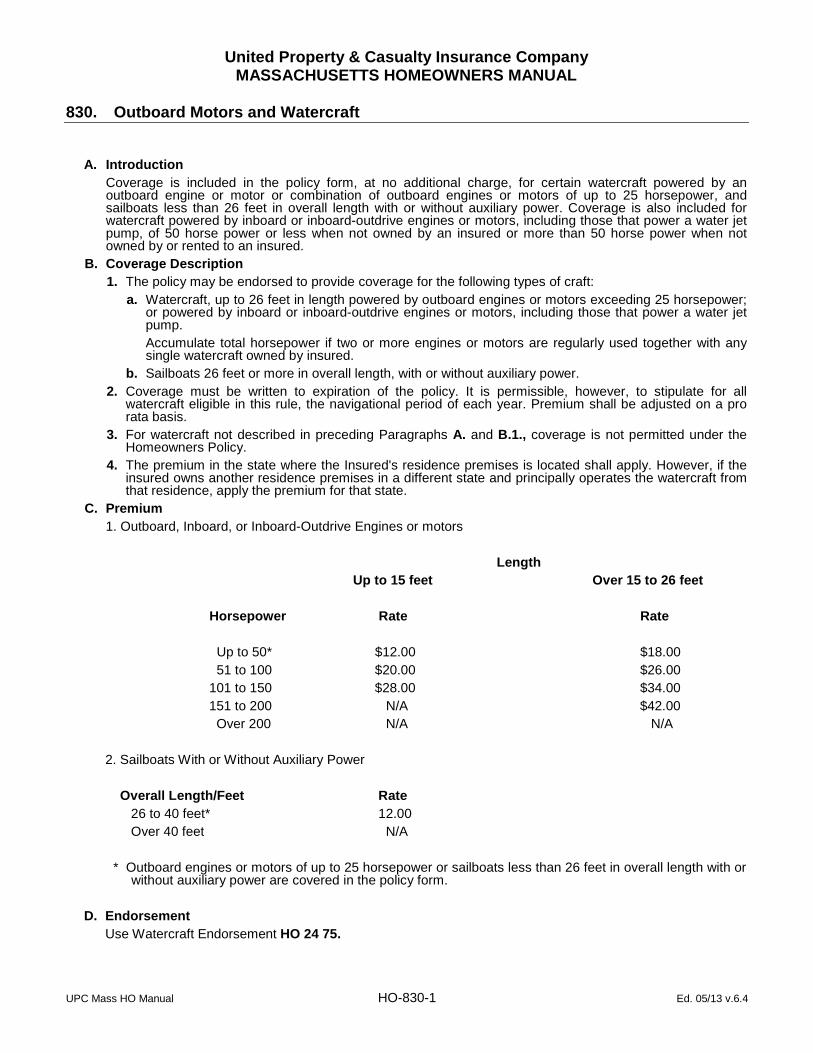

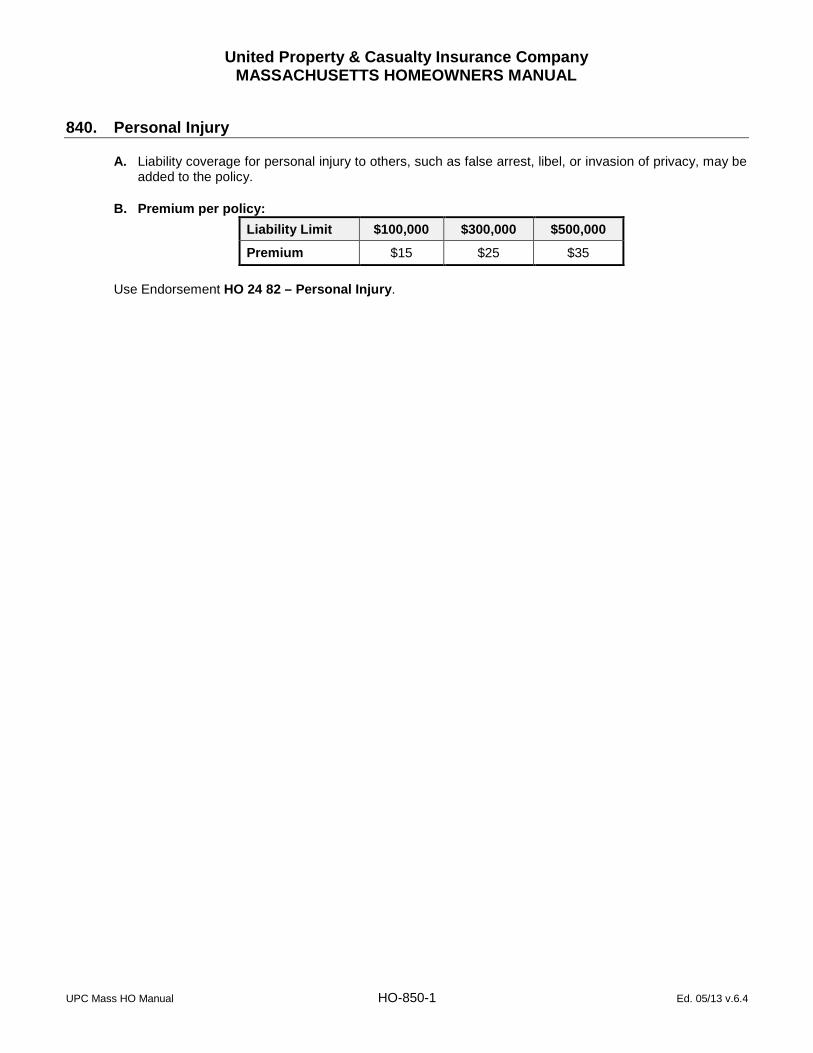

A. Introduction The policy provides coverage to named insureds, resident relatives who are members of the insured's household and persons under the age of 21 who are in the care of an insured.