uncertainty and economic self-sufficiency

TRANSCRIPT

Journal or International Economics 23 (1987) 167-178. North-Holland

UNCERTAINTY AND ECONOMIC SELF-SUFFICIENCY

Leonard K. CHENG* University of Florida, Gainesuille, FL 3261 I, USA

Received June 1986. revised version received November 1986

Existing formal analysis of international trade under uncertainty has established that it is never optimal to forgo completely the opportunity of trade. This paper uses some simple trade models to derive conditions under which zero trade or complete self-sulficiency is optimal when uncertainty is present. The paper does not advocate extreme policies against international trade and specialization. Its purpose is to show that under certain circumstances involving uncertainty economic selr-sufliciency in some goods may be desirable.

1. Introduction

Perhaps the most forceful of the welfare conclusions derived from classical and neo-classical theories of international trade is that, from the point of view of individual countries, trade is superior to autarky. However, despite the demonstration of the benefits of international exchange and production according to comparative advantage by Adam Smith and his followers, time and again there are suggestions that in particular instances self-sufficiency or less reliance on international trade is warranted. While complete self-sufficiency (autarky) may be impractical, many countries do attach importance to a certain degree of self-sufficiency in particular goods.

Existing formal analysis of international trade under uncertainty has shown that under reasonable conditions it is optimal for a risk-averse country to depart from free-trade production in the direction of autarky when international trade is subject to uncertainty. The same analysis has established that it is never optimal to forgo completely the opportunity of trade. This paper uses some simple trade models to derive conditions under which zero trade or complete self-sufficiency is optimal when uncertainty is present.’ It does not advocate extreme policies against international trade and specialization. Its purpose is to show that under certain circumstances involving uncertainty self-sufficiency in some goods may be desirable.

*I am grateful to Dave Denslow, Timothy Fries, John Pomery, and two referees for their valuable comments, and in particular to Arye Hillman for his numerous suggestions and encouragement. Support provided by the Center Ior International Economics and Business Studies at the University of Florida is also acknowledged.

‘While both ‘zero trade’ and ‘complete self-sufficiency imply no trade with the rest of the world, in this paper the first term is used when a country is endowed with fixed quantities of goods and the second term is used when different production possibilities are allowed for.

0022-1996/87/$3.50 0 1987, Elsevier Science Publishers B.V. (North-Holland)

168 L.K. Cheng, Uncertainty and economic sel/-su&iency

To rule out all non-economic arguments for self-sufficiency and economic arguments which are based on incomplete risk markets,2*3 the political economy of protection,4 and imperfect information when trade decisions are not made by consumers themselves, 5 I follow much of the literature by assuming that a small country can be represented by an individual who seeks to maximize his/her expected utility of consumption. In this framework, several general conclusions regarding optimal (i.e. expected-utility-maximizing) production and trade have been reached.6 If trading decisions can be made ex post (i.e. after uncertainty is resolved), then a country will always trade to maximize its ex post utility whenever world markets are open. Even if trade decisions have to be made ex ante (i.e. before uncertainty is resolved), R&in’s (1974a) Non-autarky Theorem states that zero trade is never optimal for any distribution of random relative prices. While it may be optimal for a country to produce closer to its autarkic point and engage in less trade than in the absence of uncertainty, this is by no means inevitable even if the country is risk averse.’ Autarkic production is in general suboptimal,* and since the Non-autarky Theorem holds for any production point, complete self-sufficiency cannot be optimal.

These conclusions are not surprising. International trade, by offering opportunities to exchange and to specialize, always expands but never contracts a country’s consumption possibility set. Complete self-sufficiency is optimal only if no combination of exchange and specialization permits the country to do better than under autarky. Zero trade is optimal only if it cannot gain from exchange at the endowment point. Risk-aversion by itself is not a sufficient condition for complete self-sufficiency or zero trade because a risk-averter ‘always takes some part of a favorable gamble’ [Arrow (1971, p. IO)]. In addition, since indirect utility functions are quasi-convex in prices, decision-makers with fixed income generally have a desire to be exposed to random variations in relative prices [see Karni (1979, p. 1395)]. Therefore, very unfavorable conditions must be present to make exchange and specialization completely unattractive.

‘For a critical review of the major arguments for self-sufficiency, see Cheng (1986). ‘Economic arguments for self-sutliciency or trade reduction based on incomplete risk markets

are found in Cassing, Hillman and Long (1986). Eaton and Grossman (1983, Newbery and Stiglitz (1984a, 1984b), and Shy (1985a, 1985b).

%ee, for example, Baldwin (1982), Hillman (1982). and Mayer (1984). ‘See Isachsen (1976). ‘For extensive surveys of the literature on international trade under uncertainty, the reader is

referred to Pomery (1979, 1984). A brief summary of results relating to optimal production and trade is given in Cheng (1986).

‘In fact, it is easy to construct examples in which trade arises solely from uncertain relative prices. A risk-averse country’s expected utility may be higher in the presence of uncertainty in its terms of trade [see Eaton (1979) and Tumovsky (1974)].

sFor instance, it is sub-optimal when the autarkic point is interior and the country is not infmitely risk-averse in the sense that it does not ignore possible outcomes other than the worst.

L.K. Cheng, Uncertainty and economic self-suflciency 169

The next section presents four cases in which zero trade or complete self- sufficiency is optimal. The key elements are uncertainty, risk-aversion, rigidity in production and the lack of substitutability in consumption. It will be shown that uncertainty and rigidity in consumption are necessary conditions while risk-aversion and rigidity in production are sufficient. By focusing on the role of ordinal preferences in decision-making under uncertainty, section 3 attempts to provide a unifying explanation for the different cases. The final section contains come concluding remarks.

2. Instances in which zero trade or complete self-sufficiency may be optimal

2.1. Case 1

To show that complete self-sufficiency may be optimal, one must first pass a major hurdle erected by Ruffin’s (1974a) Non-autarky Theorem. This theorem was established despite the requirement that the decision to trade had to be made before relative prices were known. Let x and m be two goods and suppose a country is endowed with k units of each. Throughout this paper, let p=p,,,/p, be the relative price of good m in terms of good x and let e, and e, denote the quantities of ‘autonomous exports’ of goods x and m, respectively.g The consumption of goods, c, and c,, depends on the quantities of autonomous exports:

cx=k+pem-exr (14

c,=k+eJp-e,. (lb)

Assuming that the indifference curve passing through the endowment point is smooth and downward-sloping at that point, Ruflin proved that, by choosing e, and e, appropriately, ex ante trade unambiguously dominated zero trade in every state of nature.

Now let us deviate from Ruflin’s assumption about the autarkic’ indif- ference curve by supposing that the country has Leontief preferences so that its utility function is given by

U(cx, c,) = U (min Cc.&, CA, (2)

where a>O. If a= 1, then the country’s utility as a function of e, and e, is given by

wk, e,) = W+pe,--A, ifp$eJe,, V(k+e.Jp-e,), if ple.Je,. (3)

‘Autonomous exports are quantities of exports to which a country has precommitted itself before their prices are known.

110 L.K. Cheng, Uncertainty and economic selj-suficiency

From (3) it follows that w(O,O) > w(e,,e,) for any p#e.Je, with e, and e,,, not simultaneously equal to zero. Thus, zero trade is optimal and dominates ex ante trade.

It is necessary to point out the special features of this example. The relative endowment ratio coincides with the fixed proportion of the Leontief preferences because a was assumed to be equal to unity. The preferences violate a condition which was referred to by Pomery (1979, p. 139) as ‘sufficient continuity’ of the autarkic indifference curve. As a result, the argument which led Ruflin to conclude that kx ante trade unambiguously dominated zero trade in every state of nature fails here. The lack of substitutability in consumption in conjunction with the absence of unwanted goods in autarky precludes any gains from trade. Consequently, it was not even necessary to invoke risk-aversion to establish the dominance of zero trade over ex ante trade.

If at the endowment point some degree of substitutability in consumption is allowed, then Ruffin’s Non-autarky Theorem is resurrected. But as the elasticity of substitution decreases, given any e, and e,, an increasingly smaller part of the corresponding ‘commitment curve’ (i.e. the locus of possible consumption points generated by e, and e, at all possible relative prices) lo lies above the autarkic indifference curve. When the elasticity becomes zero, the entire commitment curve lies below the autarkic indif- ference curve. Therefore, by continuity the amounts of optimal autonomous exports must be sufficiently close to zero if the elasticity of substitution around the autarkic point approaches zero.”

On the other hand, if preferences are Leontief but a is different from unity, there will be unwanted (surplus) goods in autarky and it is always optimal to trade. If the country is not risk-seeking, however, then only part of the unwanted good will be committed for export. In both this and the above situations the optimal amount of ex ante trade will be smaller as the country becomes more risk-averse.

2.2. Case 212

This case involves less restrictive assumptions than the previous one in that different production possibilities are allowed and trade decisions are made ex post. With appropriate units of measurement, let x = 1 -nt(x, mz0) represent a country’s Ricardian production frontier. A production decision

“See Pomery (1979, pp. 137-140) and RutTm (1974a) for further discussion. “As extreme examples, consider exportable items such as wigs and luxurious hotels. These are

poor substitutes for basic necessities such as food and clothing. “The structure of this model is analytically identical to a model analyzed by Stiglitz (1970,

pp. 323-327) in the context of demand for linancial assets.

LX. Cheng, Uncertainty and economic selj-sujiciency 171

has to be made ex ante and cannot be changed ex post. Without loss of generality, we continue to assume that a in (2) is equal to unity.13

Let c=min(c,,c,). Given any value of p and the output of m, the maximum value of c,c*, is given by

c*= l-(l-&m l+p *

The deviation of c* from its autarkic value can be expressed as a function of the deviation of m from the autarkic production point, i.e.

where Ac*=c*-$ and Am=m-i. In the language of gambling, Am represents both the direction and

magnitude of a bet and AC* represents the random return. If U exhibits risk- aversion, then autarkic production (Am =0) is optimal if E[(p- l)/( 1 +p)] =0, since a risk-averter takes no part of a fair game [Arrow (1971, p. loo)]. Furthermore, if the country produces at the autarkic point, it will not trade at all independently of the realized value of p due to the lack of substitut- ability in consumption. That is to say, complete self-sufficiency is optimal if EC(P-W(~ +P)I=O.

It is easy to see that if p is non-random and takes on its expected value, Ep, then the country will specialize in x or m and trade accordingly if Ep# 1. Examples can be constructed satisfying both E[(p- l)/( 1 +p)] =0 and EP# Al4 so we conclude that there are situations under which complete self- sufficiency is optimal if p is random but complete specialization is optimal if p is non-random.

2.3. Case 3

In this case we allow for some ex post adjustment in production but consider the risk of market foreclosure (due to the outbreak of wars, blockades, embargoes, etc.) instead of random relative prices. From a welfare point of view, complete market foreclosure ex post is at least as damaging as any realization of random terms of trade. Unlike random relative prices, which can be regarded as offering a two-sided bet, the risk of market foreclosure is a one-sided bet, because it is equivalent to a very large p (say

131f a is set very close to zero (but still positive), then our model becomes a ‘vent-for-surplus’ model of international trade in which good x is almost exclusively for export.

14For instance, p =i and p = 2 with equal probabilities of 4.

172 L.K. Cheng, Uncertainty and economic seljkuflciency

co) with the restriction that good m (x) be imported (exported) or a very small p (say 0) with the restriction that good M (x) be exported (imported).

Suppose the probability of complete market foreclosure is given by n, positive but smaller than unity. When the world market is not foreclosed, the relative price of good m is assumed to be fixed at p< 1. As in case 2, the country’s ex ante production frontier is given by x= 1 -m, so that the ex ante opportunity cost of good m in terms of good x (or vice versa) is equal to unity. To reflect short-run rigidities in production, the ex post opportunity costs are assumed to be given by q > 1. If q = co, then ex post adjustment is impossible.

Let m, be the ex ante choice of m and let u(m,) and uo(mo) be the maximum utility levels associated with m, when the market is open and foreclosed, respectively. Because p< 1, u(m,) is decreasing in mo. On the other hand, since the autarkic point occurs at mA=$, uo(mo) is increasing in m, for m. -z+ but is decreasing in m, for m,,zi. Therefore, to identify the optimal me, we only need to consider the interval CO,*].

Let m, be the ex post value of m which maximizes ex post utility subject to mo. For simplicity, assume further that q1 l/p so that ml =mo when the market is open. If the market is foreclosed, m, = [ 1 +(q - l)mJ( 1 + q). Hence, for OSm,5+,

h&J = WC1 + (4 - lhl/U + dh @a)

4h) = WC1 -mot 1 -FM 1+ PH. (et.4

Within this interval, any deviation from mA=i can be regarded as a gamble with production and trade. Each unit of decrease in m below mA raises consumption (c*) by (1 -p)/( 1 +p) units with probability (1 -n) and lowers consumption by (q- l)/( 1 +q) units with probability l7. The game is fair if J7(q- 1)/(1 +q)=(l -n)(l -p)/(l +p), and is unfavorable if II(q- l)/ (1 + q) > (1 - n)( 1 -J?)/( 1 + p). Consequently, complete self-sufficiency is optimal if l7(q - l)/( 1 + q) > (I- n)( I- p)/( 1 + fi) and the country is risk-neutral, or if l7(q - l)/( 1 + q) 2 (1 - rr)( 1 --I)/( 1 + p) and the country is risk-averse.

We can re-interpret x and m as two essential parts (e.g. body and engine) that are combined in a fixed proportion to produce a final product (e.g. aircraft). Rigidity in input combination appears to be quite common in the real world. The lack of any essential parts may render the other parts useless. This is true for any vertically integrated production process. Therefore, if the supply of parts through trade is uncertain and if the resumption of parts production involves loss in efficiency [such as forgetting-by-not-doing as emphasized by Arad and Hillman (1979)], then the above results indicate that a country which has decided to produce a final product may also wish to be completely self-sufficient in all essential parts.

L.K. Cheng, Uncertainty and economic sel/-sulficiency 173

2.4. Case 4

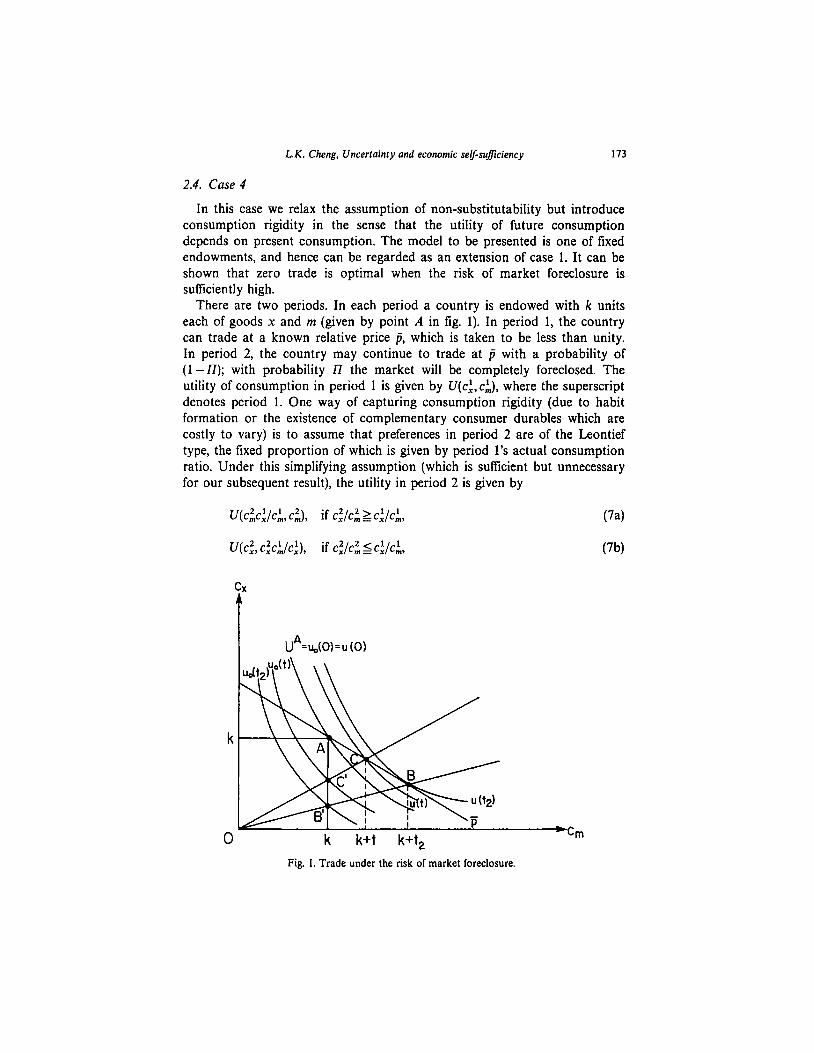

In this case we relax the assumption of non-substitutability but introduce consumption rigidity in the sense that the utility of future consumption depends on present consumption. The model to be presented is one of fixed endowments, and hence can be regarded as an extension of case 1. It can be shown that zero trade is optimal when the risk of market foreclosure is sufficiently high.

There are two periods. In each period a country is endowed with k units each of goods x and m (given by point A in fig. 1). In period 1, the country can trade at a known relative price p, which is taken to be less than unity. In period 2, the country may continue to trade at jj with a probability of (1 -II); with probability Z7 the market will be completely foreclosed. The utility of consumption in period 1 is given by U(c~,c,$ where the superscript denotes period 1. One way of capturing consumption rigidity (due to habit formation or the existence of complementary consumer durables which are costly to vary) is to assume that preferences in period 2 are of the Leontief type, the fixed proportion of which is given by period l’s actual consumption ratio. Under this simplifying assumption (which is suflicient but unnecessary for our subsequent result), the utility in period 2 is given by

(W

cx

t

k

0 k k+t k+t2 *Cm

Fig. 1. Trade under the risk of market foreclosure.

174 L.K. Cheng. Uncerlainty and economic selj-suficiency

where ci and ci are consumption in period 2. From (7) one sees that a consumption bundle, say B, which is preferred to another, say C, in period 1 may be inferior to C in period 2 if actual consumption in period 1 is sufficiently close to C.

In fig. 1, if the country trades to point C by importing t of good m, its utility in period 1 is u(t), which is also its utility in period 2 if the market does not foreclose. Should the market foreclose, its utility in period 2 is given by u,,(t). Assuming that utility across periods can be compared, the optimal 1 is one which maximizes u(t) +/3[nu,(c) +( 1 -Il)u(c)J, where p< 1 is a dis- count factor. It is easy to see that UJC) is increasing in t for cc0 and decreasing in c for t >O; u(c) is, on the other hand, increasing in t for tee, and decreasing in c for c>tl. Thus, c=O dominates c CO and we need to consider only 0 s t S t2.

By definition, u(c)=U(k-@,k+t) and u’(t)=U,--pU,, where u’=&J/c% measures the marginal benefits of trade, Uz = iXJ/ac,,, and U 1 = dU/Sc,. From (7a), it follows that for ~20, u,(c) is equal to U(k(k-pc)/(k+t),k). This indicates that the welfare loss due to habit formation (from the consump- tion of imports) in the event of market foreclosure is equivalent to losing [k-k(k-pt)/(k+t)] =[k(l +p)c/(k+t)] units of good x. The marginal costs of trade in the event of market foreclosure are given by -u;(t)= k2U,(p+ l)/ (k+c)2. Evaluated at t=O, the marginal costs are equal to U,(@+ 1). A sufficient condition for zero trade to be optimal is that”

Cl +pu -n)]u’(t)~,~,+~nu~(c)~,~~~o, (84 and for all c E [0, c2],

both u’(t) and u;(c) are non-increasing in t.’ 6 W

Condition (8) says that, starting from zero trade, the expected marginal benefits of trade fall short of its expected marginal costs, and that the payoff does not improve as t increases from 0 to t,. Substituting the expression of u’

15When a country’s preferences are not of the Leontief type, its decision problem can no longer be treated as a standard betting problem in the sense that real income (measured by the quantity of consumption along the 45” line) is linear in the decision variable. In this problem, the potential loss from trade is equal to k(l +@)t/(k+t), a non-linear function of the decision variable 1. The potential gain is given by (y(l) -k), where y(r) is delined by U(y(t), y(t)) c UN-p, k+t). Depending on the ordinal prekrence map, y may or may not be linear in L.

“u’(I) is non-increasing in I if and only if U,,+jj2U,,-2pU,,60. where U,,, U,,, etc. are second derivatives of U. u;(t) is non-increasing in t if and only if Ullk2(p+ 1)+2U, .(k+C)$O. The behavior of u(t) can be independent of that of u,(t) for tE[O, t2]. The reason is that in this range u(t) and u,(t) cover two mutually exclusive parts of the consumption space [in fig. 1, U”=u(O)=u,(O) is their boundary]. As a result, the above conditions can be satisfied simultaneously.

LX. Cheng, Uncertainty and economic sel/-sujkiency 175

and ub into (8a), the latter can be simplified to yield:

nr(‘+P) [

(U2 -WJ - P 1 w,-w,)+u,(p+ 1) * (9)

The term (U,-FU,) measures the long-run marginal benefits of trade at autarky if the world market remains open; the term (Vi@+ 1)) measures the marginal costs of trade at autarky due to habit formation in the event of market foreclosure. As (1 +j3)//?>2 and Ki’< 1, for condition (9) to hold the expression in brackets must be sufficiently smaller than one-half, which implies that (U,(p+ 1)) must be sufficiently larger than (U,-PU,). That is to say, the available imports do not contribute much to utility in the long run, but once they are imported and consumed, the loss in utility in the short run due to their sudden curtailment is great. This property captures the ‘foreign dependence hooker effect’ discussed by Tolley and Wilman (1977, p. 324).

3. Ordinal preferences and risk-bearing

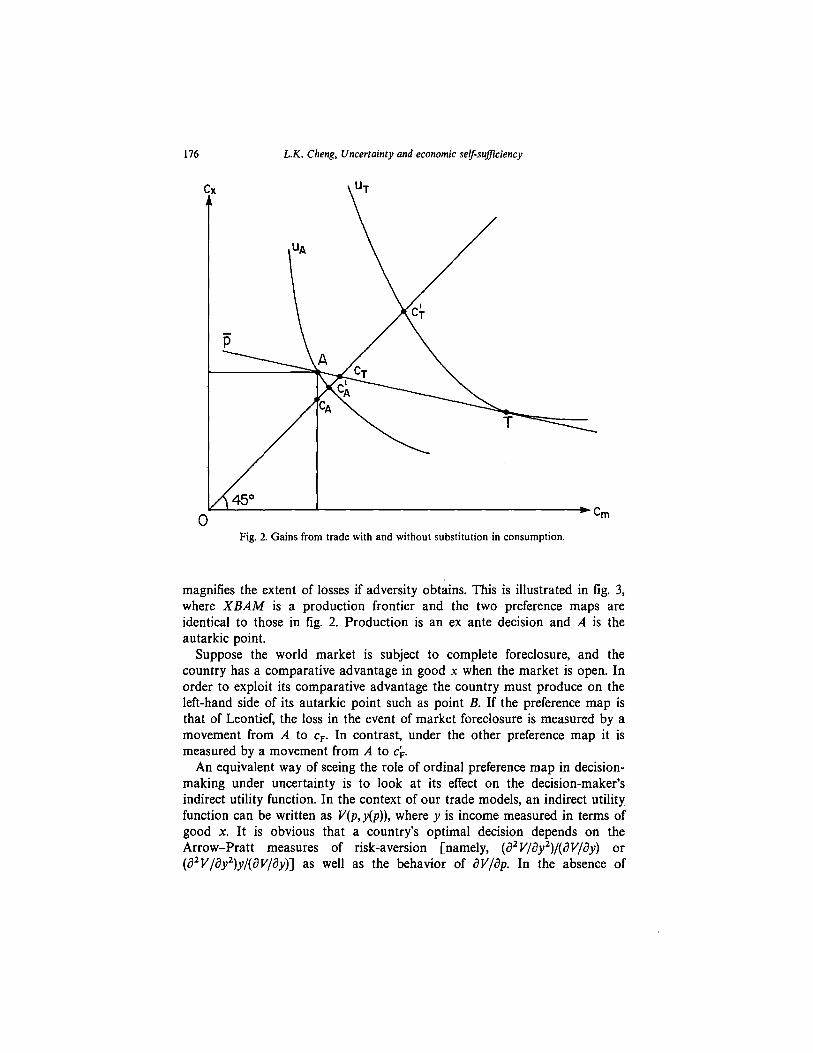

In all the cases examined in the above section, the lack of ex ante or ex post substitutability in consumption played a key role in the result that complete self-sufficiency or zero trade may be optimal. An explanation is that in situations involving multivariate risks, of which international trade is an example, the ordinal preference map plays an important role in addition to the cardinal properties of the utility function which represents the preferences [see Karni (1979) and references cited therein]. With a fixed endowment point (as in cases 1 and 4), Leontief preferences imply the following. (a) If there are unwanted (surplus) goods in autarky, then trade is always beneficial. (b) Gains from trade are limited so that unless a country is risk- seeking, its involvement in trade would also be limited. This is illustrated in fig. 2.

In the figure, A is an endowment point and jj represents the world price line. Two different preference maps are considered. The first represents Leontief preferences with unitary proportion. The second allows for sub- stitutability and two indifference curves, uA and ur, are shown. The gains from trade are measured by a movement from cA to cr under the first preference map but from cX to c; under the second.

With a limited degree of substitutability implication (b) remains intact and implication (a) is essentially unchanged. When substitution is possible, there will no longer be unwanted goods in autarky. But unless the endowment ratio happens to be close to the desired consumption ratios, the autarkic relative price will be extreme, and trade is likely to be beneficial.

The lack of substitutability in consumption not only reduces the extent of gains from trade and specialization under favorable conditions, but also

L.K. Cheng, Uncertainty and economic se&sutciency

Fig. 2. Gains from trade with and without in consumption.

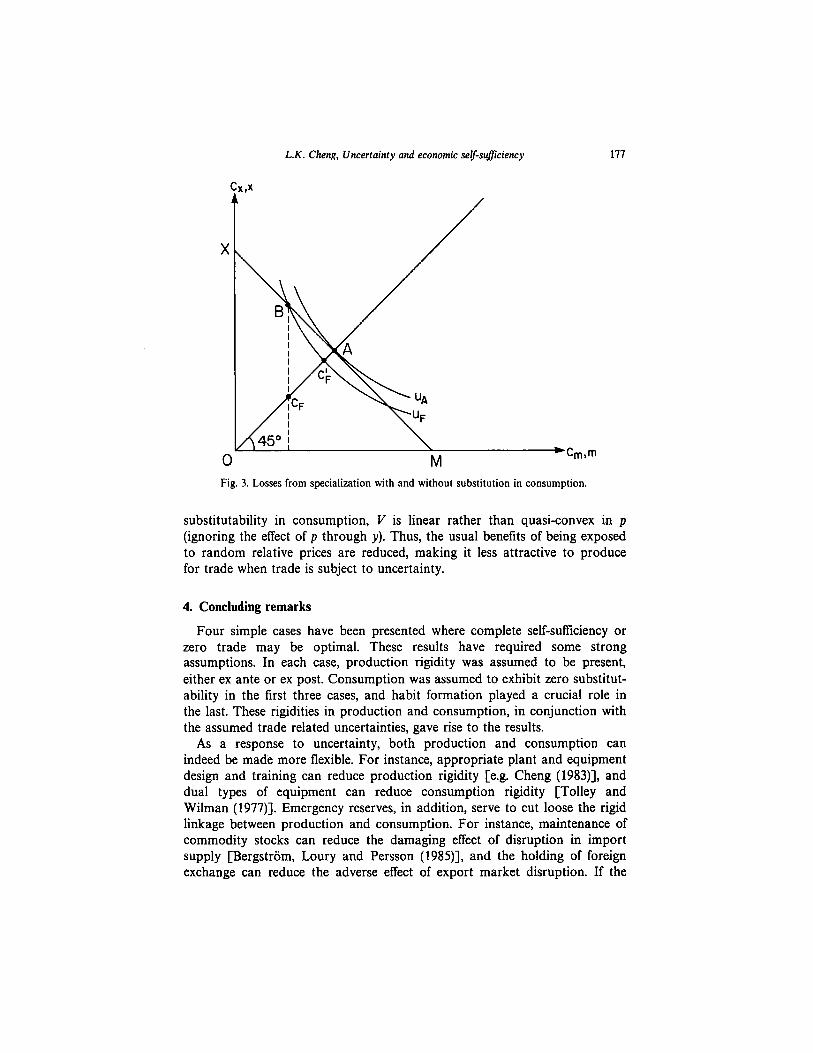

magnifies the extent of losses if adversity obtains. This is illustrated in fig. 3, where XBAM is a production frontier and the two preference maps are identical to those in fig. 2. Production is an ex ante decision and A is the autarkic point.

Suppose the world market is subject to complete foreclosure, and the country has a comparative advantage in good x when the market is open. In order to exploit its comparative advantage the country must produce on the left-hand side of its autarkic point such as point B. If the preference map is that of Leontief, the loss in the event of market foreclosure is measured by a movement from A to cF In contrast, under the other preference map it is measured by a movement from A to c;.

An equivalent way of seeing the role of ordinal preference map in decision- making under uncertainty is to look at its effect on the decision-maker’s indirect utility function. In the context of our trade models, an indirect utility function can be written as V(p, y(p)), where y is income measured in terms of good x. It is obvious that a country’s optimal decision depends on the Arrow-Pratt measures of risk-aversion [namely, (a* V/ay*)/(aV//lay) or (a*V/~Yy*)y/(aV/~?y)] as well as the behavior of i3V/dp. In the absence of

L.K. Cheng, Uncertainty and economic self-sulfciency 177

0 M *Cm,m

Fig. 3. Losses from specialization with and without substitution in consumption.

substitutability in consumption, V is linear rather than quasi-convex in p (ignoring the effect of p through y). Thus, the usual benefits of being exposed to random relative prices are reduced, making it less attractive to produce for trade when trade is subject to uncertainty.

4. Concluding remarks

Four simple cases have been presented where complete self-sufficiency or zero trade may be optimal. These results have required some strong assumptions. In each case, production rigidity was assumed to be present, either ex ante or ex post. Consumption was assumed to exhibit zero substitut- ability in the first three cases, and habit formation played a crucial role in the last. These rigidities in production and consumption, in conjunction with the assumed trade related uncertainties, gave rise to the results.

As a response to uncertainty, both production and consumption can indeed be made more flexible. For instance, appropriate plant and equipment design and training can reduce production rigidity [e.g. Cheng (1983)], and dual types of equipment can reduce consumption rigidity [Tolley and Wilman (1977)]. Emergency reserves, in addition, serve to cut loose the rigid linkage between production and consumption. For instance, maintenance of commodity stocks can reduce the damaging effect of disruption in import supply [Bergstrom, Loury and Persson (1985)], and the holding of foreign exchange can reduce the adverse effect of export market disruption. If the

178 L.K. Cheng, Uncertainty and economic seljkufficiency

costs of acquiring such flexibility are high or rise sufficiently steeply, however, the optima1 volume of trade, while non-zero, may still be small and the optima1 production may still be close to autarky.

References Anderson, James E. and John G. Riley, 1976, International trade with fluctuating prices,

International Economic Review 17, 76-97. Arad, Ruth W. and Arye L. Hillman, 1979, Embargo threat, learning and departure from

comparative advantage, Journal of International Economics 9, 265-275. Arrow, Kenneth J., 1971, Essays in the theory of risk-bearing (Markham, Chicago). Baldwin, Robert E., 1982, The political economy of protection, in: Jagdish N. Bhagwati, ed.,

Import competition and response (University of Chicago, Chicago, IL), 263-286. BergstrBm, Clas, Glen C. Loury and Mats Persson, 1985, Embargo threats and the management

of emergency reserves, Journal of Political Economy 93, 26-42. Cassing, James H., Arye L. Hillman and Ngo V. Long, 1986, Risk aversion, terms of trade

uncertainty and social consensus trade policy, Oxford Economic Papers 38, 234-242. Cheng, Leonard, 1983, Ex ante plant design, portfolio theory, and uncertain terms of trade,

Journal of International Economics 14, 25-51. Cheng, Leonard, 1986, Economic arguments for self-sutliciency and trade reduction, Mimeo.

(Department of Economics, University of Florida, Gainesville, FL). Eaton, Jonathan, 1979, The allocation of resources in an open economy with uncertain terms of

trade, International Economic Review 20, 391-403. Eaton, Jonathan and Gene M. Grossman, 1985, Tariffs as insurance: Optimal commercial policy

when domestic markets are incomplete, Canadian Journal of Economics 18,258-272. Hillman, Arye L., 1982, Declining industries and political-support protectionist motives,

American Economic Review 72, 1180-l 187. Isachsen, Ame L., 1976, The case for reduced openness, Memorandum (Institute of Economics,

University of Oslo). Kami, Edi, 1979, On multivariate risk aversion, Econometrica 47, 1391-1401. Mayer, Wolfgang, 1984, Endogenous tariff formation, American Economic Review 74,970-985. Newbery, David M.G. and Joseph E. Stiglitz, 1984a, Pareto inferior trade, Review of Economic

Studies 51, 1-12. Newbery, David M.G. and Joseph E. Stiglitz, 1984b, Risk and trade policy, Economic Theory

Discussion Paper no. 77 (Department of Applied Economics, University of Cambridge, Cambridge).

Pomery, John, 1979, Uncertainty and international trade, in Rudiger Dornbusch and Jacob A. Frenkel, eds., International economic policy (Johns Hopkins University, Baltimore).

Pomery, John, 1984, Uncertainty in trade models, in Ronald W. Jones and Peter B. Kenen, eds., Handbook of international economics, vol. 1 (North-Holland, Amsterdam).

RuNin, Roy J., 1974a, International trade under uncertainty, Journal of International Economics 4.243-259.

Rullin, Roy J., 1974b, Comparative advantage under uncertainty, Journal of International Economics 4,261-273.

Shy, Oz, 1985a, Pareto inferior trade: A general equilibrium approach, Working paper no. 183 (Department of Economics, State University of New York, Albany, New York).

Shy, Oz, 1985b, Trade restrictions that improve world welfare in a world with incomplete markets for risk, Working paper no. 184 (Department of Economics, State University of New York, Albany, New York).

Stiglitz, Joseph E., 1970, A consumption-oriented theory of the demand for linancial assets and the term structure of interest rates, Review of Economic Studies 37, 321-351.

Tolley, George S. and John D. Wilman, 1977, The foreign dependence question, Journal of Political Economy 85, 323-348.

Tumovsky, Stephen J., 1974, Technological and price uncertainty in a Ricardian model of international trade, Review of Economic Studies 41, 201-217.